1 Sector View Banking -...

16

June 21, 2018 Sector Update ICICI Securities Ltd | Retail Equity Research NCLT resolution & peaking NPAs to aid revival From start of calendar year, banking sector has remained volatile given industry participants grappling with concerns including high slippages, frauds and NPA divergences. New framework by RBI (discarding past restructuring formats) further accentuated the intensity of problems for the banking sector and especially PSBs. Therefore, private banks have out performed Bank Nifty rising ~8.9% (31 March 2018 to 19 June 2018). Among private peers, street has been favouring retail centric banks including Kotak Bank, IndusInd Bank and HDFC Bank. PSB, though witnessed marginal pick up at 3.3% during April-June’18, still continue to under perform on YTD basis (-19.1%). Key factors to watch out for in coming quarters….. 1. Slippages from exposure under various format of restructuring 2. Accretion of stressed asset from exposure to power sector and recovery from some resolution under Samadhan scheme 3. Resolution of NCLT/IBC assets and extent of haircut 4. Sustainability of credit growth momentum; gauge early sign of credit demand from corporate segment Led by fraud, NPA divergence and new RBI norms abolishing restructuring, GNPA surged at | 10.2 lakh crore (16% QoQ) in FY18. However, overall stressed assets remained broadly stable at ~13% of advances (~| 11.4 lakh crore) indicating peaking of the cycle. Risk from exposure to stressed power assets at ~| 1.8 lakh crore and resolution under ‘Samadhan scheme’ remains need to be keenly monitored. With bulk of cases under NCLT 1 nearing resolution, corporate banks would see heightened shift in their GNPA ratio owing to resolutions and recoveries. Early recognition and resolution, though positive in long run, will keep credit cost elevated in FY19E. Credit growth in banking system continued at modest pace of ~10% YoY, however, distribution of the same remained uneven. Retail centric private banks witnessed healthy growth of 20%+, while corporate banks, especially PSBs, lagged behind with many of them reporting de-growth. Private bank (our coverage) clocked 23.2% YoY growth in advances, while PSBs have lacked behind as a slew of them are in PCA. Going ahead, retail credit is expected to remain healthy with elevated competitive intensity. Rising commodity and crude prices to keep demand for working capital firm; however, capex driven growth is seen to remain muted. Given capital constraint and lending restriction (11 of 21 PSBs under PCA), private banks will continue to seize market share. With bank’s focus turning from recognition of bad asset to resolution of stressed assets, credit cost is expected to remain elevated in FY19E. However, increase in coverage ratio and revival in balance sheet growth will be return accretive from FY20E. Rapid movement in G-sec yield to keep treasury volatile. Though benign margin and higher credit cost in near term is expected to keep profitability modest; moderation in slippages and recovery in some of NCLT cases will support return ratios, thereby warranting gradual upward re-rating select large cap PSB stock. With gradual improvement anticipated in the sector, we prefer selective stock selection. We remain positive on retail centric private banks with consistent growth and returns track record. Therefore, recommend Kotak Mahindra Bank and HDFC Bank. As a major beneficiary of recovery in NCLT cases, we remain positive on SBI (from our coverage) among PSU banks. Retail NBFCs with consistent earnings trajectory like Bajaj Finance and HDFC Ltd continue to remain our picks. Out performance of retail banks continues….. 1-Jan-18 28-Mar-18 19-Jun-18 YTD May - Jun'18 Bank Nifty 25318 25107 26266 3.7% 4.6% PSB 3679 2879 2975 -19.1% 3.3% Private 14021 13688 14902 6.3% 8.9% Axis Bank 565 509 516 -8.6% 1.4% HDFC Bank 1857 1891 2025 9.0% 7.1% Kotak Bank 1002 1049 1307 30.5% 24.6% IndusInd Bank 1626 1796 1930 18.7% 7.5% Research Analyst Kajal Gandhi [email protected] Vasant Lohiya [email protected] Vishal Narnolia [email protected] Banking Sector View Neutral Source: Capital line, ICICI Direct Research

Transcript of 1 Sector View Banking -...

June 21, 2018

Sector Update

ICICI Securities Ltd | Retail Equity Research

NCLT resolution & peaking NPAs to aid revival

From start of calendar year, banking sector has remained volatile given

industry participants grappling with concerns including high slippages,

frauds and NPA divergences. New framework by RBI (discarding past

restructuring formats) further accentuated the intensity of problems for

the banking sector and especially PSBs. Therefore, private banks have out

performed Bank Nifty rising ~8.9% (31 March 2018 to 19 June 2018).

Among private peers, street has been favouring retail centric banks

including Kotak Bank, IndusInd Bank and HDFC Bank. PSB, though

witnessed marginal pick up at 3.3% during April-June’18, still continue to

under perform on YTD basis (-19.1%).

Key factors to watch out for in coming quarters…..

1. Slippages from exposure under various format of restructuring

2. Accretion of stressed asset from exposure to power sector and

recovery from some resolution under Samadhan scheme

3. Resolution of NCLT/IBC assets and extent of haircut

4. Sustainability of credit growth momentum; gauge early sign of

credit demand from corporate segment

Led by fraud, NPA divergence and new RBI norms abolishing

restructuring, GNPA surged at | 10.2 lakh crore (16% QoQ) in FY18.

However, overall stressed assets remained broadly stable at ~13% of

advances (~| 11.4 lakh crore) indicating peaking of the cycle. Risk from

exposure to stressed power assets at ~| 1.8 lakh crore and resolution

under ‘Samadhan scheme’ remains need to be keenly monitored. With

bulk of cases under NCLT 1 nearing resolution, corporate banks would

see heightened shift in their GNPA ratio owing to resolutions and

recoveries. Early recognition and resolution, though positive in long run,

will keep credit cost elevated in FY19E.

Credit growth in banking system continued at modest pace of ~10% YoY,

however, distribution of the same remained uneven. Retail centric private

banks witnessed healthy growth of 20%+, while corporate banks,

especially PSBs, lagged behind with many of them reporting de-growth.

Private bank (our coverage) clocked 23.2% YoY growth in advances,

while PSBs have lacked behind as a slew of them are in PCA. Going

ahead, retail credit is expected to remain healthy with elevated

competitive intensity. Rising commodity and crude prices to keep

demand for working capital firm; however, capex driven growth is seen to

remain muted. Given capital constraint and lending restriction (11 of 21

PSBs under PCA), private banks will continue to seize market share.

With bank’s focus turning from recognition of bad asset to resolution of

stressed assets, credit cost is expected to remain elevated in FY19E.

However, increase in coverage ratio and revival in balance sheet growth

will be return accretive from FY20E. Rapid movement in G-sec yield to

keep treasury volatile. Though benign margin and higher credit cost in

near term is expected to keep profitability modest; moderation in

slippages and recovery in some of NCLT cases will support return ratios,

thereby warranting gradual upward re-rating select large cap PSB stock.

With gradual improvement anticipated in the sector, we prefer selective

stock selection. We remain positive on retail centric private banks with

consistent growth and returns track record. Therefore, recommend Kotak

Mahindra Bank and HDFC Bank. As a major beneficiary of recovery in

NCLT cases, we remain positive on SBI (from our coverage) among PSU

banks. Retail NBFCs with consistent earnings trajectory like Bajaj Finance

and HDFC Ltd continue to remain our picks.

Out performance of retail banks continues…..

1-Jan-18 28-Mar-18 19-Jun-18 YTD

May -

Jun'18

Bank Nifty 25318 25107 26266 3.7% 4.6%

PSB 3679 2879 2975 -19.1% 3.3%

Private 14021 13688 14902 6.3% 8.9%

Axis Bank 565 509 516 -8.6% 1.4%

HDFC Bank 1857 1891 2025 9.0% 7.1%

Kotak Bank 1002 1049 1307 30.5% 24.6%

IndusInd Bank 1626 1796 1930 18.7% 7.5%

Research Analyst

Kajal Gandhi

Vasant Lohiya

Vishal Narnolia

Banking Sector View

Neutral

Source: Capital line, ICICI Direct Research

Page 2 ICICI Securities Ltd | Retail Equity Research

Large NPAs recognised in Q4; FY19E to see peaking of impaired assets

As expected, Q4FY18 has been a washout quarter for the banking sector.

Absolute GNPA of PSU banks increased by 31% YoY (15% QoQ) to |

896601 crore while that of private banks increased 39% YoY to | 127985

crore. GNPA ratio of the entire industry is ~11.8% as on FY18 while

absolute GNPA rose by 15.7% QoQ to | 1024586 crore. Corporate based

private banks like Axis Bank witnessed heightened NPA pressure along

with most PSU banks. The slippages during Q4FY18 for top 6 PSU banks

increased by >80% QoQ to ~| 112000 crore, while the same for top 6

private banks increased at a higher rate of ~140% to ~| 37500 crore. The

reasons for such rise in impaired assets are frauds, new NPA framework

introduced by RBI (discarding past restructuring formats), NPA

divergences & absence of any resolution in large NCLT cases referred

earlier. Further, these slippages mainly came from restructured book,

SDR, S4A and 5/25 schemes announced by RBI. Post such large

reorganisation and with resolution of NCLT accounts (~40% of GNPLs as

on FY18) expected by H1FY19, we expect normalisation in NPA levels in

FY19E. However, the exposure to power sector needs to be keenly

watched over next two to three quarters. Credit cost i.e provisioning

would stay a bit elevated owing to ageing of NPLs.

Exhibit 1: Stressed assets (GNPA + RA) at ~12.7% as of FY18

FY14 FY15 FY16 FY17 Q1FY18 Q2FY18 Q3FY18 Q4FY18

GNPA 242000 303978 575313 776835 829336 840250 885788 1024586

NNPA 136000 158211 331340 430173 467013 452523 469278 517775

GNPA ratio 4.1 4.5 7.6 9.9 10.9 10.8 10.9 11.8

NNPA ratio 2.2 2.4 5.1 5.5 6.1 5.8 5.8 6.0

RA Total 370523 437182 293670 254772 240000 210000 190000 76000

RA as % of advances 5.9 6.4 3.9 3.2 3.1 2.7 2.3 0.9

Stressed assets (GNPA + RA) 612523 741160 868983 1031607 1069336 1050250 1075788 1100586

Stressed assets as % of loans 10 10.85 11.5 13.1 14.0 13.5 13.2 12.7

SDR, S4A, 5/25 & others 100000 100000 100000 100000 100000 40000

Total stressed asset 612523 741160 968983 1131607 1169336 1150250 1175788 1140586

GNPA of PSU banks 523398 684733 733136 733974 777266 896601

GNPA of Private banks 51915 92102 96201 106275 108522 127985

Source: RBI, ICICI Direct Research; *RA is a calculated figure.

Page 3 ICICI Securities Ltd | Retail Equity Research

Resolution of Bhushan Steel under IBC – A historic break through

In May 2018, NCLT approved resolution of one of the large accounts in

the NCLT 1 list named Bhushan Steel which had outstanding debt of ~|

56000 crore. Tata Steel via its 100% subsidiary would be the new

promoter with ~73% stake. For this, Tata Steel paid ~| 35200 crore to the

lenders, which entails a haircut of ~37%. This is a big breakthrough in the

IBC process, as a large account has been resolved at such low haircut.

Banks have already made at-least 50% provision towards this account in

general; with some large corporate banks have even made provision

coverage upwards of 60%. Thus, with haircut being lower than provision

made, banks would benefit in terms of write back as seen in the below

exhibit. SBI, PNB and Axis bank have high exposure to Bhushan steel.

However, write back as percentage of operating profit would be higher for

banks like UCO bank, United Bank, J&K bank, Allahabad bank and Central

bank of India. This is largely owing to their weak operational earnings.

Exhibit 2: Bank wise exposure to Bhushan Steel and write back on resolution as % of operating

profit

Banks (| Crore) Exposure Write back @ 13% FY18 PPP Write backas % of PPP

Allahabad Bank 1911 248 3438 7.2

Axis Bank 1940 252 15594 1.6

Bank of Baroda 1600 208 12006 1.7

Bank of Maha 1242 161 2191 7.4

Central Bank 1155 150 2733 5.5

City Union Bank 0 0 1208 0.0

Corporation Bank 929 121 3950 3.1

DCB Bank 0 0 525 0.0

Dena Bank 596 78 1171 6.6

Dhanlaxmi Bank 0 0 146 0.0

Federal Bank 0 0 2291 0.0

HDFC Bank 0 0 32625 0.0

I O B 958 125 3629 3.4

IDFC Bank 0 0 1427 0.0

IndusInd Bank 102 13 6656 0.2

J & K Bank 830 108 1144 9.4

Karnataka Bank 0 0 1473 0.0

Karur Vysya Bank 191 25 1777 1.4

Kotak Mah. Bank 0 0 7158 0.0

LVB 37 5 355 1.4

OBC 1578 205 3703 5.5

Punjab & Sind 693 90 1145 7.9

PNB 4905 638 10294 6.2

RBL Bank 0 0 1331 0.0

South Ind.Bank 150 20 1481 1.3

SBI 12873 1673 59511 2.8

Syndicate Bank 1757 228 3864 5.9

UCO Bank 1119 145 1334 10.9

UNION BANK OF INDIA 1577 205 7540 2.7

UNITED BANK OF INDIA 777 101 1024 9.9

Vijaya Bank 416 54 3098 1.7

Yes Bank 325 42 7748 0.5

Total 45493 5914 233077

Source: Company, media articles; ICICIdirect.com Research; In the Bhushan Steel case haircut is 37% while

provision made is ~50%. Thus write back for lenders is ~13%.

Page 4 ICICI Securities Ltd | Retail Equity Research

Steel accounts under NCLT near resolution; other accounts struggle

The following table explains the recent status or position of the other 11

accounts in the NCLT 1 list announced by RBI last year. Apart from

Bhushan Steel, other account that has seen resolution is the Electrosteel

Steel (amount outstanding ~| 13000 crore) which was acquired by

Vedanta. Further, lenders of Monnet Ispat & energy Ltd (which has dues

of ~| 12000 crore) has approved the resolution plan submitted by

consortium of JSW Steel Ltd and AION Investments Pvt. Ltd. This deal

would entail haircut of ~70%.

The other large account in the NCLT list 1, which is under focus is the

Essar steel account (dues of ~| 49000 crore), where in bids have been

put by Arcelor Mittal & Numetal. The account was admitted in August

2017, but owing to certain legal and technical issues the resolution is

expected to be delayed and could fructify in Q2FY19 quarter. The

resolution of this account will be another big breakthrough form the

lenders as haircut expected in this case could be lower than even 37%

seen in Bhushan Steel.

Exhibit 3: Recent status of the accounts under NCLT List 1 of the RBI

Company Lead Bank Debt (in | crore) Appointment Date Highest Bid (| crore) Highest Bidder

Expected/

Actual

Haircut (%) Status/Remarks

Era Infra Engineering UBI 10065 17.04.2017 NA NA NA The account might largely go under liquidation

Jyoti Structures SBI 7000 17.07.2017 NA Netmagic NA

A group of high net-worth investors led by Sharad Sanghi, chief of Netmagic Solutions, have only shown

interest in acquiring Jyoti Structures. Lenders could receive | 3000 crore over a period of 15 years, as per the

existing resolution plan placed by these HNI investers

Alok Industries SBI 29500 24.07.2017 5050 RIL-JM Financial ARC 82.9 RIL-JM Financial ARC are the sole bidder for the company

Electrosteel Steel SBI 13000 26.07.2017 5320 Vedanta 60.0 One of the two accounts which got successfully resolved under IBC

Monnet Ispat & Energy SBI 10359 26.07.2017 3700 JSW-AION 73.0 The resolution plan submitted by a JSW-AION has been approved by lenders

Bhushan Power & Steel PNB 47204 28.07.2017 24500 Tata Steel 48.0 Tata Steel is said to have put in a bid of | 24500, including capital infusion of | 7500

Amtek Auto Corp. Bank 14074 02.08.2017 3520 Liberty House 75.0 Liberty House has emerged as the highest bidder. Liquidation value was set at ~| 4000 crore

Bhushan Steel SBI 56000 03.08.2017 35200 Tata Steel 37.0 Tata Steel has acquired Bhushan Steel

ABG Shipyard

Large

Private Bank 9290 04.08.2017 NA Liberty House NA

Liberty House was the sole bidder but the offer was rejected by lenders as the bid value at ~| 2200 crore

was lower than liquidation value. The NCLT has rescheduled the hearing till June,25 2018

Essar Steel SBI 49212 07.08.2017 37000

Numetal & Arcelor

Mittal 25.0

The two frontrunners for Essar has been Arcelor Mittal & Numetal. While Arcelor Mittal is believed to have

given offer of ~| 30500 crore in the first round, Numetal is estimated to have given offer of ~| 37000 crore

in round two

Jaypee Infratech PSU Bank 9635 14.08.2017 NA NA NA

The Supreme Court recently stayed liquidation proceedings against Jaypee Infratech Ltd. The creditors’

committee for Jaypee Infratech had estimated the liquidation value at ~| 7759 crore

Lanco Infratech PSU Bank 44365 16.08.2017 NA NA NA

It could be liquidated as it failed to get a resolution plan approved within the stipulated 270 days. However, on

June 19, the NCLT would here revised resolution of Thriveni Earthmovers and other matters

Source: Company, Media articles; ICICIdirect.com Research

Recently, RIL-JM Financial combined, (who are the sole bidder for Alok

industries which has dues of ~| 29500 crore) had put the bid for the

company at ~| 5050 crore. This could entail a haircut of >80%.

In case of other 7 accounts, some might go for liquidation or are stuck in

litigations and thus no concrete resolution has happened despite

completion of 270 days since admission in to NCLT. But it expected that,

these could get resolved by Q2FY19.

The second list of 28 accounts under NCLT list has exposure of ~|

140000 crore. This list includes companies like Castex Technologies,

Coastal Projects, East Coast Energy, IVRCL, Monnet Power, Soma

Enterprise, Videocon Industries, Ruchi Soya industries, SE Manufacturing,

etc. Currently, companies in the NCLT list 2 are also in the various stages

of the resolution process especially Ruchi Soya, Monnet Power etc. As

per banks, this list would see resolutions by end of FY19.

Page 5 ICICI Securities Ltd | Retail Equity Research

Combined haircut in case of NCLT list 1 is expected at ~50%. Steel

accounts (4 accounts having outstanding dues of ~| 130000 crore or

>50% share of NCLT list 1) in the list together would have lower haircut

at <40% owing to turnaround in the sector and high interest for the

respective companies shown by bidders. Other accounts owing to lack of

interest by bidders & liquidations would entail higher haircuts of 60%+ for

the lenders. The accounts in NCLT list 2 overall might see haircuts of

>50% considering the recent news on resolution process of the

individual accounts.

With the bulk of the results of the accounts referred under both the list of

NCLT expected over two quarters, banks would witness healthy degree of

write backs & reduction in GNPA & NNPA. Further, with resolution there

would be high degree of accounts which would require re-financing and

thus would create lending opportunities for large corporate base banks

like SBI, Axis Bank, Yes Bank and others. Private Banks like HDFC Bank,

Indusind Bank and Kotak Mahindra Bank would further gain market share

as they are in a better position to lap this opportunity than PSU banks (as

half of them are under lending restrictions from RBI)

As seen in the below table, just a resolution of the steel accounts in NCLT

list 1 would help reduce GNPA & NNPA ratio by ~150 bps and ~80 bps,

respectively from levels seen in FY18.

Exhibit 4: Impact on headline asset quality numbers of the sector on resolution of steel accounts

| Crore

GNPA of the banking system as on Q4FY18 1024586

NNPA of the banking system as on Q4FY18 517775

GNPA % as on Q4FY18 11.8%

NNPA % as on Q4FY18 6.0%

Banks exposure to 12 accounts in NCLT ~280000

Within above, top 4 steel accounts exposure is 130000

Approximate provisions towards these steel accounts is ~50% 65000

Thus, balance unprovided portion of the above companies forming part of industry's NNPA 65000

Resolutions is expected in above 12 accounts in by H1FY19

Higher interest is seen in steel related assets and hence haircut would be lower than other sector

In this scenario, GNPA & NNPA picture would improve as follows

GNPA of the banking system after settlement in 4 steel accounts under NCLT 894586

NNPA of the banking system after settlement in 4 steel accounts under NCLT 452775

GNPA % after settlement in 4 steel accounts under NCLT 10.3%

NNPA % after settlement in 4 steel accounts under NCLT 5.2%

Thus, assuming propbable resolution in steel accounts with hair cut to be borne by banks staying at ~40%,

the balance exposure to such steel accounts could turn standard

Source: Company, Media articles, Management commentary; ICICI Direct Research

In the below exhibit we have tried to indicate by how much the headline

asset quality i.e GNPA ratio & NNPA ratio of top banks having exposure to

NCLT lists would be impacted on account of resolutions expected in

FY19E. These six banks’ exposure in the NCLT lists at ~| 151000 crore is

~40% of the total NCLT exposure. SBI would be one of the key

beneficiaries of the resolutions in the NCLT accounts as this exposure

accounts for ~34.7% of its total GNPA (which is higher compared to

peers). Further, SBI also has higher provisions coverage of 63% towards

such accounts within the PSU bank. Thus, any resolution with lower

haircut (the banks expects haircut of ~52% in NCLT list 1) would entail

healthy write backs for SBI. Apart from SBI, Union Bank could witness

higher gains. In the private space, corporate banks like Axis Bank would

be key beneficiary owing to higher provision coverage of 68% on NCLT

accounts.

Page 6 ICICI Securities Ltd | Retail Equity Research

Exhibit 5: Impact on headline asset quality of top banks, due to resolution of NCLT accounts

Banks NCLT 1 NCLT 2 GNPA NNPA GNPA ratio % NNPA ratio %

SBI 49116 28510 77626 223400 110855 34.7% 63.0% 10.9% 5.7% 7.1% 3.7%

PNB 11000 6500 17500 86620 48684 20.2% 45.3% 18.4% 11.2% 14.7% 9.2%

BOB 7158 3830 10988 56480 23483 19.5% 55.2% 12.3% 5.5% 9.9% 4.2%

Union Bank 7700 4800 12500 49369 24326 25.3% 60.0% 15.7% 8.4% 11.7% 6.2%

Axis Bank 5071 1003 6074 34248 16592 17.7% 67.9% 6.8% 3.4% 5.6% 2.8%

Total 98249 53043 151292 559913 280689 27.0%

NCLT exposure %

of GNPA

PCR on NCLT

exposure

GNPA ratio post

resolution

NNPA ratio post

resolution

Total

exposure

Source: Company, ICICIdirect.com Research

We overall expect that FY19E would witness the peaking of the impaired

assets cycle for the banking sector as a whole as bulk of problem assets

seems to have now been recognised and/or are in the process of

resolution. However, exposure to power assets still posses risk and thus

need to be keenly monitored. Especially the next two quarters are crucial

as bulk of the resolutions in the NCLT list 1 would happen during this

period. Accounts in the NCLT list 2 is expected to get resolved by end of

FY19E. Large corporate based PSU & private banks would thus see

heightened shift in their GNPA ratio in next two quarters owing to

resolutions and recoveries. We expect, credit cost for the year would stay

elevated on account of ageing of NPLs and any major relief on

provisioning front would occur post FY19E.

Indian banks have been sitting on a huge pile of bad assets. Despite huge

sum of ~| 4.1 lakh crore been written-off till date (of which ~| 1.9 lakh

crore was written off in last 2 years), Indian banks are saddled with GNPA

at | 10.2 lakh crore in FY18 (~11.8% of loans). GNPA of PSU banks

increased 31% YoY (15% QoQ) to | 896601 crore, while that of private

banks increased 39% YoY to | 127985 crore. Led by new RBI norms

abolishing restructuring, major proportion of accretion was from various

restructured buckets including standard, SDR, S4A and flexible

restructuring. Frauds, NPA divergence and absence of resolution in NCLT

cases further added to the asset quality woes. PSB and corporate based

private banks like Axis Bank witnessed heightened asset quality pressure

impacting profitability.

Despite elevated slippages, overall stressed assets (GNPA + restructured

asset) remained broadly stable at ~13% of advances (~| 11.4 lakh crore)

which indicates peaking of the cycle. Going ahead, some of the exposure

to power sector, currently classified as restructured, is expected to slip

into NPA in coming 2 quarters. Factoring GNPA at ~| 10.25 lakh crore,

restructured assets at ~| 1.2 lakh crore and ~| 50000 crore slippage from

power sector, overall stressed asset is seen at ~| 12 lakh crore. However,

PCR (without technical w/off) at ~43% provides some bit of comfort.

Further, peaking of stressed assets and anticipated recovery from NCLT

account induces long term confidence in mechanism.

Year-wise write-off in last 10 years….

Fiscals Amount (in | crore)

FY18 115000

FY17 81000

FY16 57585

FY15 49018

FY14 34409

FY13 27231

FY12 15551

FY11 17794

FY10 11185

FY09 7461

FY08 8019

Source: Media Articles, ICICI Direct Research

Source: SBI Life RHP, ICICIdirect.com, Research

Page 7 ICICI Securities Ltd | Retail Equity Research

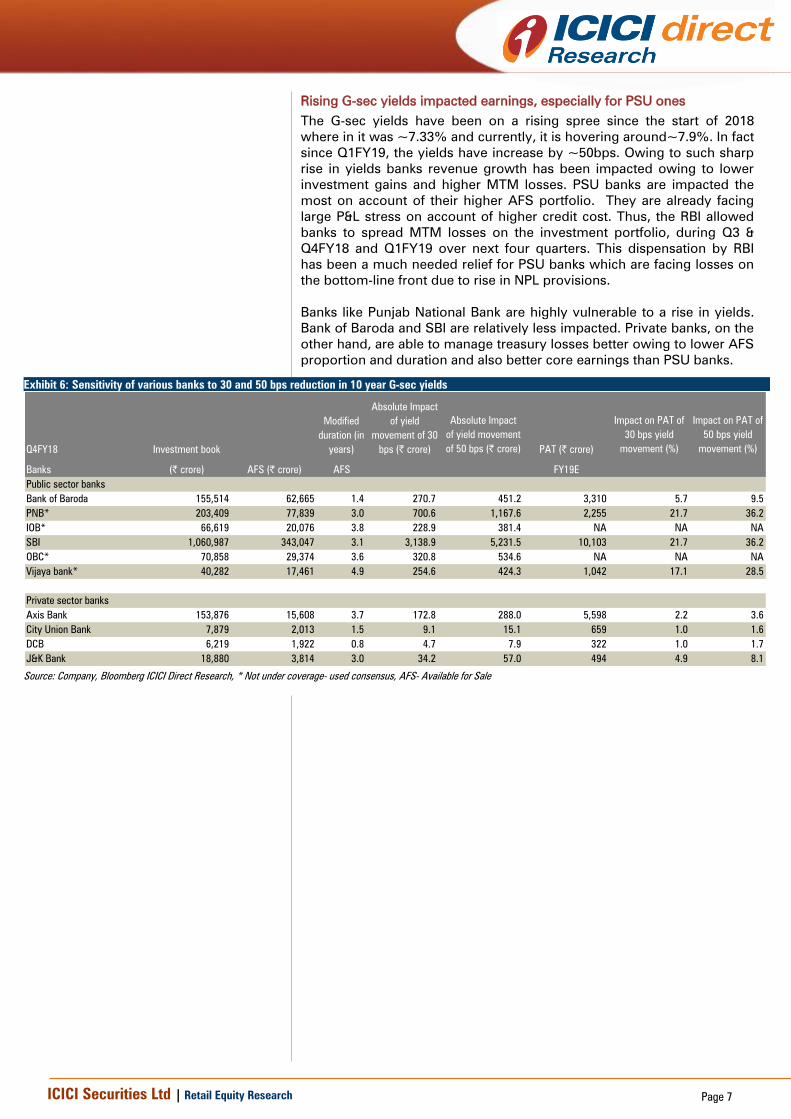

Rising G-sec yields impacted earnings, especially for PSU ones

The G-sec yields have been on a rising spree since the start of 2018

where in it was ~7.33% and currently, it is hovering around~7.9%. In fact

since Q1FY19, the yields have increase by ~50bps. Owing to such sharp

rise in yields banks revenue growth has been impacted owing to lower

investment gains and higher MTM losses. PSU banks are impacted the

most on account of their higher AFS portfolio. They are already facing

large P&L stress on account of higher credit cost. Thus, the RBI allowed

banks to spread MTM losses on the investment portfolio, during Q3 &

Q4FY18 and Q1FY19 over next four quarters. This dispensation by RBI

has been a much needed relief for PSU banks which are facing losses on

the bottom-line front due to rise in NPL provisions.

Banks like Punjab National Bank are highly vulnerable to a rise in yields.

Bank of Baroda and SBI are relatively less impacted. Private banks, on the

other hand, are able to manage treasury losses better owing to lower AFS

proportion and duration and also better core earnings than PSU banks.

Exhibit 6: Sensitivity of various banks to 30 and 50 bps reduction in 10 year G-sec yields

Q4FY18 Investment book

Absolute Impact

of yield movement

of 50 bps (| crore) PAT (| crore)

Impact on PAT of

30 bps yield

movement (%)

Impact on PAT of

50 bps yield

movement (%)

Banks (| crore) AFS (| crore) AFS FY19E

Public sector banks

Bank of Baroda 155,514 62,665 1.4 270.7 451.2 3,310 5.7 9.5

PNB* 203,409 77,839 3.0 700.6 1,167.6 2,255 21.7 36.2

IOB* 66,619 20,076 3.8 228.9 381.4 NA NA NA

SBI 1,060,987 343,047 3.1 3,138.9 5,231.5 10,103 21.7 36.2

OBC* 70,858 29,374 3.6 320.8 534.6 NA NA NA

Vijaya bank* 40,282 17,461 4.9 254.6 424.3 1,042 17.1 28.5

Private sector banks

Axis Bank 153,876 15,608 3.7 172.8 288.0 5,598 2.2 3.6

City Union Bank 7,879 2,013 1.5 9.1 15.1 659 1.0 1.6

DCB 6,219 1,922 0.8 4.7 7.9 322 1.0 1.7

J&K Bank 18,880 3,814 3.0 34.2 57.0 494 4.9 8.1

Absolute Impact

of yield

movement of 30

bps (| crore)

Modified

duration (in

years)

Source: Company, Bloomberg ICICI Direct Research, * Not under coverage- used consensus, AFS- Available for Sale

Page 8 ICICI Securities Ltd | Retail Equity Research

Samadhan scheme – step towards resolution of stressed power sector

Higher momentum in corporate capex lending and subsequent economic

slowdown has left Indian banks battling with large pile of stressed asset

over last couple of years. Banking industry has seen stressed asset (GNPA

+ RA) more than doubled in last 5 years to ~| 12 lakh crore as of March

2018. As a step towards decoding asset quality concerns, RBI has

announced new framework for faster resolution of stressed assets. Under

the new norms, existing classification of stressed assets in various

buckets (SDR, S4A, flexible restructuring etc) stands withdrawn. In

addition, the new norm mandates lenders to classify even a one day

delay in debt servicing as default and formulate resolution in 180 days. In

backdrop of these norms and concern regarding quantum of stressed

exposure, focus has now turned to power sector. Overall banking

industry exposure to power sector stood at ~| 5.2 lakh crore as of March

2018, of which ~| 1.8 lakh crore (~ 75000 MW) is classified under

stressed category.

Exhibit 7: Power sector exposure of banks (Dec’17)

Fund based Non fund based

Bank of Baroda 26058 6646 399380 6.5% 8.2%

Union Bank of India 21112 8674 314474 6.7% 9.5%

Axis Bank 19242 5466 420923 4.6% 5.9%

State Bank of India 16502 2753 1924578 0.9% 1.0%

HDFC Bank 15809 3463 631215 2.5% 3.1%

Syndicate Bank 13078 742 219449 6.0% 6.3%

Allahbad Bank 12658 2250 161792 7.8% 9.2%

Corporation Bank 10072 747 129085 7.8% 8.4%

IndusInd Bank 5626 7726 128542 4.4% 10.4%

Bank of Maharashtra 4737 863 95169 5.0% 5.9%

Kotak Mahindra Bank 2439 463 159071 1.5% 1.8%

Federal Bank 1551 17 85922 1.8% 1.8%

RBL Bank 1532 1233 36890 4.2% 7.5%

Vijaya Bank 1050 72 110622 0.9% 1.0%

Yes Bank 14984 6701 171515 8.7% 12.6%

Total exposure

as % of loans

Loan book as of

Dec'17| crore

Exposure as of Dec '17 Funded exposure

as % of loans

Source: Company, ICICI Direct Research

Currently, ~75000 MW of power generating assets, either under

operation or under construction, stand stressed due to lower availability

of coal, lack of PPAs and delays in regulatory clearances. The government

has reviewed 34 stressed thermal power projects (~40130 MW) with debt

of ~| 1.8 lakh crore. As of April’18, total power sector loans in India are

5,18,763 crore. And total infra loans stand at | 8,87,816 crore. Hence, |1.8

lakh crore form ~34.7% of power loans. Parts of these loans are already

under NPA or restructuring buckets.

Of this, projects comprising ~8.8 GW (constituting debt worth | 43700

crore) has been resolved with the help of schemes like SHAKTI (for coal

availability), sale to ARCs, etc. Projects with capacity of ~9.9 GW (debt of

| 34600 crore) have referred to NCLT, wherein ~8.8 GW worth of projects

are in early stages of construction with major milestones yet to be

achieved. Remaining ~23 GW of projects are awaiting resolution with

some of them under various stages of bidding.

A consortium of lenders led by SBI has introduced a new scheme –

Samadhan (Scheme of Asset Management and Debt Change Structure)

for speedy resolution of stressed assets through sale or takeover; thereby

preventing liquidation. Completed or near-completion power plants with

partial or full PPAs and locational advantage have been considered for

this scheme. Under the scheme, lenders have finalized 11 power projects

Page 9 ICICI Securities Ltd | Retail Equity Research

(highlighted in Exhibit below) with combined capacity of ~12640 MW and

exposure of ~| 70,000 crore.

Exhibit 8: SBI has short listed 11 power projects under Samadhan scheme

Developer Project Unit State O/s Debt (| crore) Equity (| crore) Total (| crore)

KSKMahanadiPowerCompanyLtd Akaltara 1 to 6 Chhattisgarh 17194 3234 20428

Jaypee Power Ventures Pvt Limited (Bara) Bara 1 to 3 U.P 11494 4044 15537

RKMPowergenPrivateLimitedUchpinda Uchpinda 1 to 4 Chhattisgarh 9146 2586 11732

Jaypee Power Ventures Pvt Limited (Nigrie) Nigrie 1 & 2 M.P 6211 3812 10023

Coastal EnergenPrivate Limited MutiaraTPP 1 & 2 T.N 6132 1574 7706

Jindal IndiaThermalPowerLimited Derang 1 & 2 Odisha 5381 1494 6875

SKS Power Generation Binjkote 1 to 4 Chattisgrah 4801 862 5663

Avantha Power(Jhabua) Seoni Jhabua 1 MP 3488 1348 4836

Lanco LancoAnpara C 1 & 2 U.P 3071 969 4040

Ind BharathEnergy (Utkal) Ltd Utkal 1 & 2 Odisha 3046 1172 4219

Adani Power MaharashtraLimited TiroraTPP Ph 1 to 5 Maharashtra 11765 4947 16712

Lanco Amarkantak PowerLimited 3 & 4 Chhattisgarh 8782 1533 10315

GMR Chhattisgarh Energy Limited Raikheda 1 & 2 Chhattisgarh 8174 3368 11541

RattanIndiaNasik PowerLimited Nasik 1 to 5 Maharashtra 7108 2455 9562

Lanco BabandhPowerLimited 1 & 2 Odisha 6976 1123 8099

DB PowerLimited Baradhra 1 & 2 Chhattisgarh 6721 2244 8965

Essar Power (Mahaan) Limited Mahan 1 & 2 MP 5951 2266 8217

MonnetPowerCompanyLimited Malibrahmani 1 & 2 Odisha 5300 1273 6573

Athena Chattisgarh Power (P) Limited Singhitarai 1 & 2 Chhattisgarh 5256 968 6224

Lanco VidarbhaThermalPowerLimited 1 & 2 Maharashtra 4762 1079 5841

GMR Kamlanga Energy Limited Kamalnga 1 to 3 Odisha 4100 2250 6350

GVK Industries Limited (GoindwalSaheb)(GoindwalSaheb) 1 & 2 Punjab 3523 1250 4773

Essar Power(Jharkand) Limited Tori 1 & 2 Jharkhand 3112 1719 4831

Adani Korba West 1 Chattisgrah 3099 1830 4929

East Coast Energy BhavanpaDu 1 & 2 AP 2834 836 3670

Kanti BijleeUtpadanNigam Ltd Muzzaffarpur TPP 3 & 4 Bihar 2506 1277 3784

Adhunik & Power MahadevPrasad 1 & 2 Jharkhand 2474 903 3377

DamodarValleyCorporation Raghunathpur TPP 1 & 2 W.B 2318 2626 4944

JaypeePowerVenturesPvt Limited(Bina) Bina 1 & 2 M.P 2254 1264 3518

Visa PowerLimited DeveriTPP 1 & 2 Chhattisgarh 2253 427 2680

Madhucon SimhapuriEnergyLtd(Phase I &II) 1 to 4 A.P 2206 1035 3242

VandanaVidyutLimited SaloraTPP 1 & 2 Chhattisgarh 1489 541 2030

KVKNilachalPower Nilachal 1 to 3 Odisha 1072 1116 2188

GMR Energy (P) Limited EMCOWarora 1 & 2 Maharashtra 3 1063 1066

Total stressed loans 174000 60489 234489

Projects marked bold are power plants short listed under Samadhan scheme

Source: Company, ICICI Direct Research

As per SBI Samadhan Scheme, debt of each project is to be rated by

credit rating agencies. The rating agency will identify sustainable and

unsustainable portions of each project. Further, the lenders propose to

take equity stake in a project by converting part of unsustainable portion

of debt into equity. While developers will get to retain a minor share, the

majority shareholding will be offered through bidding to new investors.

Existing promoters of the project will be asked to take a hefty haircut and

will not be allowed to hold more than 24.5% in the project. In addition,

the lenders are also entitled to make investments as per their exposure in

each power project with the lead lender to invest ~| 10 crore, while co-

lenders to infuse equity on pro-rata basis of their exposure.

In development towards goal to achieve resolution in short listed power

projects, lenders have started to shelve power projects on sale. SBI led

consortium has put on sale 1200 MW thermal power plant in Chhattisgarh

by SKS Power Generation (Chhattisgarh). Bids are invited for another

thermal power project in Tamil Nadu – Coastal Energen with operational

capacity of 1200 MW. In addition, NTPC is in discussion with lenders to

acquire 3 projects – Jaiprakash Group’s Nigrie project with capacity of

1320 MW, 1980 MW Bara plant operating under Jaiprakash Group’s

subsidiary Prayagraj Power Company. The third project is Jindal India’s

1200 MW Angul plant in Odisha.

Page 10 ICICI Securities Ltd | Retail Equity Research

With deadline of seeking resolution in 180 days, failure of which will lead

to initiation of insolvency proceeding in NCLT and thereby higher

provision, lenders seek to complete the resolution under Samadhan

scheme in 120 days. The scheme is aimed at preventing power

generation projects from going into liquidation, receiving better

valuations and securing speedy resolution. Such faster resolution will

enable garnering better value of stressed asset for lenders which will

prohibit any substantial impact on future profitability. However, buyer’s

appetite and response in respect of power projects needs to be seen.

Credit growth to hover around 10% mirroring 1x nominal GDP growth

Credit growth remained modest at ~10%, though improved on YoY

basis. However, wide disparity was witnessed among peers with private

retail centric banks witnessing healthy growth of 20%+ while banks with

substantial corporate exposure, especially PSB, lagging behind with many

of them reporting de-growth. Private banks (our coverage) has clocked

23.2% YoY growth in advances, while PSBs have lacked behind as a slew

of them are in PCA.

Among the segments, retail segment has seen continued healthy growth

at ~18-20% in FY15-18; however, growth to industry has remained

muted. Going ahead, credit to retail segment is expected to remain

healthy, while capex driven loan growth is seen to remain muted.

Increasing commodity and crude prices would keep demand for working

capital loans intact. Retail centric banks will continue growth, though

competitive intensity is here to remain elevated. Among peers, private

banks are seen to gain market share ahead, led by capital constraint and

lending restriction (11 out of 21 PSBs under PCA).

Exhibit 9: Retail segment growth continue to remain healthy

(Amt in | crore) Apr-17 Mar-18 Apr-18 YoY growth

Non-Food Credit 6848875 7688423 7580392 10.7%

Agriculture & Allied Activities 969982 1030215 1026878 5.9%

Industry 2624492 2699268 2651077 1.0%

Services 1641167 2050471 1981294 20.7%

Personal Loans 1613231 1908469 1921142 19.1%

Source: RBI, ICICI Direct Research

Adding to the woes of NPA banks, margins continued to remain under

pressure given interest reversal and change in loan mix towards low

yielding retail loans. Transition to MCLR from base rate regime has also

kept margins benign. However, stable CASA (post surge seen at the time

of demon) and higher proportion of retail deposit partially rescued the

pressure. Going ahead, margins are expected to remain steady at current

level in near term for reasons similar to seen in the recent past (tilt

towards retail loans and higher slippages from restructured/ watch list

pool). However, recognition of bulk of the pain and anticipated recovery

from few of the NCLT accounts (which are in the last phase of resolution)

bodes well for improvement in margins. Increase in MCLR rates will

provide relief in near term.

Credit growth witnessed pick up in FY18….

0

20000

40000

60000

80000

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

| crore

Source: RBI, ICICI Direct Research

Source: SBI Life RHP, ICICIdirect.com, Research

Page 11 ICICI Securities Ltd | Retail Equity Research

Exhibit 10: Quarterly margin trend

NIM (%) Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18 Q4FY18

PSU coverage

Bank of Baroda 2.3 2.1 2.2 2.1 2.3 2.7 2.5

SBI 2.8 2.7 2.7 2.4 2.4 2.5 2.5

Private coverage

Axis Bank 3.6 3.4 3.8 3.6 3.5 3.4 3.3

City Union Bank 4.2 4.2 4.2 4.5 4.5 4.4 4.4

Development Credit Bank 4.0 4.0 4.0 4.2 4.2 4.1 4.1

IndusInd Bank 4.0 4.0 4.0 4.0 4.0 4.0 4.0

HDFC Bank 4.2 4.1 4.3 4.4 4.3 4.3 4.3

Jammu & Kashmir Bank 3.4 3.3 3.5 3.7 3.8 4.0 3.2

Yes Bank 3.4 3.5 3.6 3.7 3.7 3.5 3.4

Source: Company, ICICI Direct Research

Recoveries to rise, but still some time to buy PSBs

Indian banking industry has been battling with concerns revolving around

slower credit off-take, benign margins and elevated asset quality pressure

in last couple of fiscals. Introduction of new framework by RBI, abolishing

existing restructuring mechanism acted as a further blow to banks

denting their performance. Though revised framework have led to

accelerated recognition of stressed asset impacting profitability in near

term; long term benefit in terms of early recognition of stress and faster

resolution will benefit the sector as a whole.

Despite elevated slippages, overall stressed assets (GNPA + restructured

asset) remained broadly stable at ~13% of advances (~| 11.4 lakh crore)

which indicates peaking of the cycle. Going ahead, some of the exposure

to power sector, currently classified as restructured, is expected to slip

into NPA in coming 2 quarters. Factoring GNPA at ~| 10.25 lakh crore,

restructured assets at ~| 1.2 lakh crore and ~| 50000 crore slippage from

power sector, overall stressed asset is seen at ~| 12 lakh crore. However,

PCR (without technical w/off) at ~43% provides some bit of comfort.

Further, peaking of stressed assets and anticipated recovery from NCLT

account induces long term confidence.

Bank’s focus has now turned from recognition of bad asset to resolution

of stressed assets and improvement in provision coverage. Therefore,

credit cost is expected to remain high in FY19E but lower than FY18.

However, increase in coverage ratio and focus on balance sheet growth

will be return accretive from FY20E onwards. Though benign margin and

higher credit cost in near term is expected to keep profitability modest;

moderation in slippages and recovery in some of the NCLT referred cases

will lead to improvement in return ratios, thereby warranting upward re-

rating of the stock.

We expect outlook on sector to improve gradually, therefore, selective

stock picking is advisable. We remain positive on retail centric private

banks including Kotak Mahindra Bank, HDFC Bank and City Union Bank.

As the major beneficiary of recovery NCLT cases, we remain positive on

SBI (from our coverage) among PSU banks. Retail NBFCs with consistent

earnings trajectory like Bajaj Finance and HDFC Ltd continues to remain

our picks.

Page 12 ICICI Securities Ltd | Retail Equity Research

Exhibit 11: Valuation of India banks under coverage

CMP M Cap

(|) TP(|) Rating (| Cr) FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E

Bank of Baroda (BANBAR) 123 185 Buy 36,199 4 8 14 32.4 15.8 9.0 0.9 0.9 0.8 0.1 0.3 0.4 2 5 8

State Bank of India (STABAN) 271 340 Buy 240,527 4 9 18 77.0 30.3 14.8 1.8 1.5 1.5 0.1 0.2 0.4 1 3 6

Axis Bank (AXIBAN) 514 600 Buy 140,151 15 15 39 33.5 34.5 13.1 2.6 2.4 1.9 0.6 0.6 1.2 7 6 12

City Union Bank (CITUNI) 184 200 Buy 13,050 9 11 12 20.7 17.5 15.2 3.3 2.8 2.2 1.6 1.6 1.6 15 16 15

DCB Bank (DCB) 176 215 Buy 5,708 8 10 14 21.7 16.8 12.7 2.2 2.0 1.7 1.0 1.0 1.1 11 12 14

Federal Bank (FEDBAN) 83 105 Buy 16,738 5 6 8 17.1 13.9 10.6 1.8 1.4 1.2 0.8 0.9 1.0 10 11 12

HDFC Bank (HDFBAN) 2,060 2,300 Buy 556,880 67 78 94 30.6 26.4 21.9 5.3 3.9 3.4 1.8 1.8 1.9 18 17 17

IndusInd Bank (INDBA) 1,957 2,050 Buy 117,366 59 74 92 33.2 26.4 21.3 5.2 4.4 3.8 1.8 1.9 1.9 16 18 19

Jammu & Kashmir Bk(JAMKAS) 54 75 Buy 3,288 4 9 12 14.9 6.1 4.6 0.9 0.9 0.8 0.2 0.5 0.6 3 8 10

Kotak Mahindra Bank (KOTMAH) 1,326 1,440 Buy 254,318 21 27 34 61.9 48.7 39.5 7.1 6.5 5.8 1.7 1.8 1.9 13 13 15

Yes Bank (YESBAN) 334 375 Hold 79,793 18 24 31 18.2 14.0 10.9 3.1 2.6 2.2 1.7 1.8 1.9 17 19 21

Sector / Company

RoE (%)EPS (|) P/E (x) P/ABV (x) RoA (%)

Source: Company, ICICI Direct Research

Page 13 ICICI Securities Ltd | Retail Equity Research

Annexure

Exhibit 12: Asset quality trend

Asset quality trend

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY18 Q2FY18 Q3FY18 Q4FY18

PSU coverage

Bank of Baroda 46,173 46,307 48,480 56,480 19,519 19,573 19,852 23,483

SBI* 188,068.0 186,115.0 199,141.0 223,427.5 107760.0 97896.0 102370.0 110854.7

Private coverage

Axis Bank 22,030.9 27,402.3 25,000.5 34,248.6 9766.0 14052.3 11769.5 16591.7

City Union Bank 735 780 860 857 426 441 448 475

Development Credit Bank 285.3 315.8 354.5 369.0 149.1 157.0 161.5 146.7

IndusInd Bank 1,272 1,345 1,499 1,705 508 537 592 746

HDFC Bank 7,242.9 7,702.8 8,234.8 8,607.0 2528.2 2596.8 2773.7 2601.0

Jammu & Kashmir Bank 5,641 5,983 6,232 6,007 2,267 2,443 2,488 2,791

Yes Bank 1,364.4 2,720.3 2,974.3 2,626.8 545.3 1543.3 1595.1 1312.8

GNPA (| crore) NNPA (| crore)

Source: Company, ICICI Direct Research

Exhibit 13: Quarterly margin trend

NIM (%) Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18 Q4FY18

PSU coverage

Bank of Baroda 2.3 2.1 2.2 2.1 2.3 2.7 2.5

SBI 2.8 2.7 2.7 2.4 2.4 2.5 2.5

Private coverage

Axis Bank 3.6 3.4 3.8 3.6 3.5 3.4 3.3

City Union Bank 4.2 4.2 4.2 4.5 4.5 4.4 4.4

Development Credit Bank 4.0 4.0 4.0 4.2 4.2 4.1 4.1

IndusInd Bank 4.0 4.0 4.0 4.0 4.0 4.0 4.0

HDFC Bank 4.2 4.1 4.3 4.4 4.3 4.3 4.3

Jammu & Kashmir Bank 3.4 3.3 3.5 3.7 3.8 4.0 3.2

Yes Bank 3.4 3.5 3.6 3.7 3.7 3.5 3.4

Source: Company, ICICI Direct Research

Exhibit 14: Key financials of industry as on Q4FY18 (listed banks)

(| crore) Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18 Q4FY18

NII 72304 75948 74644 83763 73905 82808 85714 84835

Growth YoY 6.0 11.5 3.7 9.1 2.2 9.0 14.8 1.3

Other income 36553 47788 45890 47039 41877 52189 38218 47391

Growth YoY 38.7 59.3 44.8 12.2 14.6 9.2 -16.7 0.7

Total operating exp. 51133 56467 58764 58557 54053 59536 61162 69366

Staff cost 28534 30520 31668 27968 29149 29088 30128 34342

Operating profit 57724 67268 61770 72246 61729 75460 62771 62860

Growth YoY 16.4 24.2 17.2 27.5 6.9 12.2 1.6 -13.0

Provision 45162 50733 46841 72627 45540 65521 76618 148276

PBT 12468 16503 14891 -418 16149 9899 -13888 -85460

PAT 8388 10809 9460 557 11376 6221 -6943 -55648

Growth YoY -54.8 -39.6 NA NA 35.6 -42.4 NM NM

GNPA 653861 704844 732608 776835 829336 840250 885788 1024586

Growth YoY 109.3 100.8 63.0 31.3 26.8 19.2 20.9 31.9

NNPA 382785 407018 417687 430173 467013 452523 469278 517775

Growth YoY 120.0 110.0 62.6 26.5 22.0 11.2 12.4 20.4

Source: Capitaline, Company, ICICI Direct Research

Page 14 ICICI Securities Ltd | Retail Equity Research

ICICI Direct Research coverage universe (BFSI)

CMP M Cap

(|) TP(|) Rating (| Cr) FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E FY18 FY19E FY20E

Bank of Baroda (BANBAR) 123 185 Buy 36,199 4 8 14 32.4 15.8 9.0 0.9 0.9 0.8 0.1 0.3 0.4 2 5 8

State Bank of India (STABAN) 271 340 Buy 240,527 4 9 18 77.0 30.3 14.8 1.8 1.5 1.5 0.1 0.2 0.4 1 3 6

Axis Bank (AXIBAN) 514 600 Buy 140,151 15 15 39 33.5 34.5 13.1 2.6 2.4 1.9 0.6 0.6 1.2 7 6 12

City Union Bank (CITUNI) 184 200 Buy 13,050 9 11 12 20.7 17.5 15.2 3.3 2.8 2.2 1.6 1.6 1.6 15 16 15

DCB Bank (DCB) 176 215 Buy 5,708 8 10 14 21.7 16.8 12.7 2.2 2.0 1.7 1.0 1.0 1.1 11 12 14

Federal Bank (FEDBAN) 83 105 Buy 16,738 5 6 8 17.1 13.9 10.6 1.8 1.4 1.2 0.8 0.9 1.0 10 11 12

HDFC Bank (HDFBAN) 2,060 2,300 Buy 556,880 67 78 94 30.6 26.4 21.9 5.3 3.9 3.4 1.8 1.8 1.9 18 17 17

IndusInd Bank (INDBA) 1,957 2,050 Buy 117,366 59 74 92 33.2 26.4 21.3 5.2 4.4 3.8 1.8 1.9 1.9 16 18 19

Jammu & Kashmir Bk(JAMKAS) 54 75 Buy 3,288 4 9 12 14.9 6.1 4.6 0.9 0.9 0.8 0.2 0.5 0.6 3 8 10

Kotak Mahindra Bank (KOTMAH) 1,326 1,440 Buy 254,318 21 27 34 61.9 48.7 39.5 7.1 6.5 5.8 1.7 1.8 1.9 13 13 15

Yes Bank (YESBAN) 334 375 Hold 79,793 18 24 31 18.2 14.0 10.9 3.1 2.6 2.2 1.7 1.8 1.9 17 19 21

Sector / Company

RoE (%)EPS (|) P/E (x) P/ABV (x) RoA (%)

Source: Company, ICICI Direct Research

Page 15 ICICI Securities Ltd | Retail Equity Research

RATING RATIONALE

ICICI Direct Research endeavours to provide objective opinions and recommendations. ICICI Direct Research

assigns ratings to its stocks according to their notional target price vs. current market price and then

categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and

the notional target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

research@ICICI Direct Research

Page 16 ICICI Securities Ltd | Retail Equity Research

ANALYST CERTIFICATION

We /I, Kajal Gandhi, CA, Vasant Lohiya, CA and Vishal Narnolia, MBA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research

report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s)

or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Kajal Gandhi, CA, Vasant Lohiya, CA and Vishal Narnolia, MBA Research Analysts of this report have not received any compensation from the companies mentioned in the report in the

preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Kajal Gandhi, CA, Vasant Lohiya, CA and Vishal Narnolia, MBA, Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.