1 REPUBLIC OF SOUTH AFRICA Investor Presentation Presenter: Lungisa Fuzile | Director General,...

30

1 REPUBLIC OF SOUTH AFRICA Investor Presentation Presenter: Lungisa Fuzile | Director General, National Treasury | February 2012

-

Upload

alvin-lamb -

Category

Documents

-

view

213 -

download

0

Transcript of 1 REPUBLIC OF SOUTH AFRICA Investor Presentation Presenter: Lungisa Fuzile | Director General,...

1

REPUBLIC OF SOUTH AFRICA

Investor Presentation

Presenter: Lungisa Fuzile | Director General, National Treasury | February 2012

2

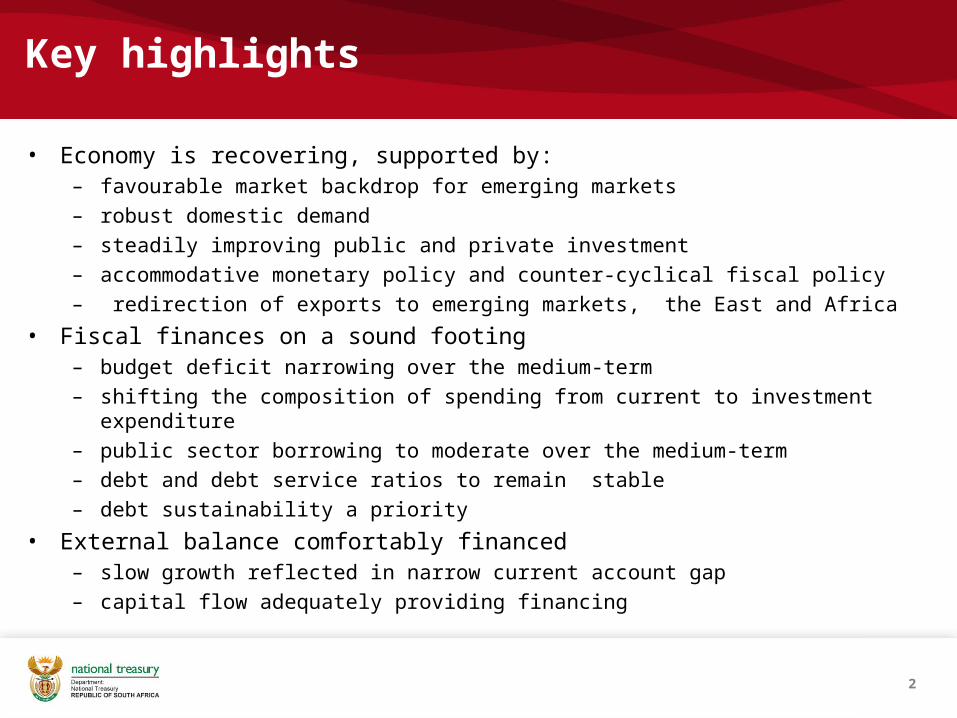

Key highlights

• Economy is recovering, supported by:– favourable market backdrop for emerging markets– robust domestic demand– steadily improving public and private investment– accommodative monetary policy and counter-cyclical fiscal policy– redirection of exports to emerging markets, the East and Africa

• Fiscal finances on a sound footing– budget deficit narrowing over the medium-term– shifting the composition of spending from current to investment expenditure– public sector borrowing to moderate over the medium-term– debt and debt service ratios to remain stable– debt sustainability a priority

• External balance comfortably financed– slow growth reflected in narrow current account gap– capital flow adequately providing financing

3

Table of contents

1) Global Macro Developments 4 3) Public Finance 14

2) South African Economic Performance 7

4) Monetary Policy 23 5) External Vulnerability 27 6) Conclusion 29

4

1. Global Macro Developments

5

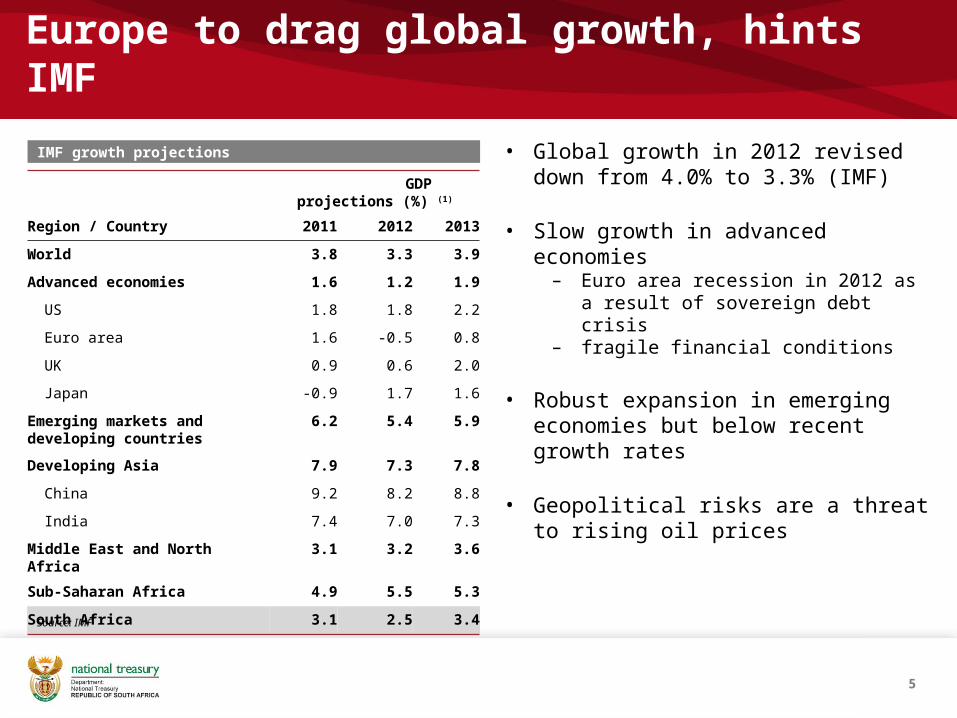

Europe to drag global growth, hints IMF

• Global growth in 2012 revised down from 4.0% to 3.3% (IMF)

• Slow growth in advanced economies– Euro area recession in 2012 as a result of

sovereign debt crisis– fragile financial conditions

• Robust expansion in emerging economies but below recent growth rates

• Geopolitical risks are a threat to rising oil prices

IMF growth projections

GDP projections (%) (1)

Region / Country 2011 2012 2013

World 3.8 3.3 3.9

Advanced economies 1.6 1.2 1.9

US 1.8 1.8 2.2

Euro area 1.6 -0.5 0.8

UK 0.9 0.6 2.0

Japan -0.9 1.7 1.6

Emerging markets and developing countries

6.2 5.4 5.9

Developing Asia 7.9 7.3 7.8

China 9.2 8.2 8.8

India 7.4 7.0 7.3

Middle East and North Africa 3.1 3.2 3.6

Sub-Saharan Africa 4.9 5.5 5.3

South Africa 3.1 2.5 3.4

Source: IMF

6

Global manufacturing activity tentative

Eurozone : Some silver lining could emerge

China : Expansion slowing down

Source: Bloomberg , SA National Treasury

USA: Signs of health evident

UK : On a potential path to recovery

7

2. South Africa Economic Performance

8

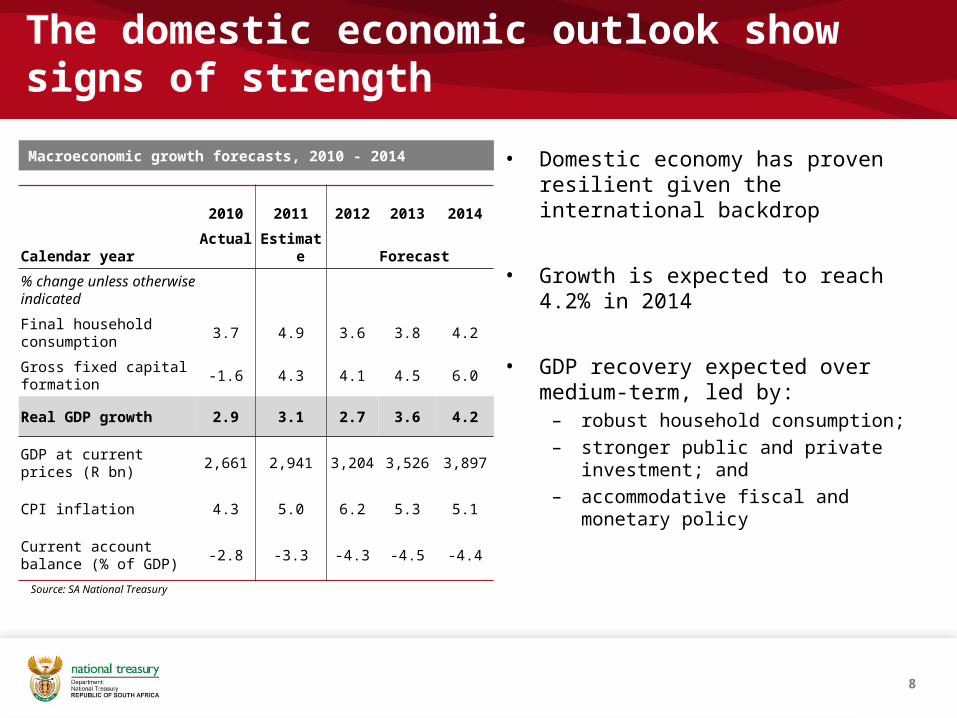

The domestic economic outlook show signs of strength

• Domestic economy has proven resilient given the international backdrop

• Growth is expected to reach 4.2% in 2014

• GDP recovery expected over medium-term, led by:

– robust household consumption;– stronger public and private investment;

and– accommodative fiscal and monetary policy

2010 2011 2012 2013 2014

Calendar year Actual Estimate Forecast

% change unless otherwise indicated

Final household consumption

3.7 4.9 3.6 3.8 4.2

Gross fixed capital formation

-1.6 4.3 4.1 4.5 6.0

Real GDP growth 2.9 3.1 2.7 3.6 4.2

GDP at current prices (R bn)

2,661 2,941 3,204 3,526 3,897

CPI inflation 4.3 5.0 6.2 5.3 5.1

Current account balance (% of GDP)

-2.8 -3.3 -4.3 -4.5 -4.4

Source: SA National Treasury

Macroeconomic growth forecasts, 2010 - 2014

9

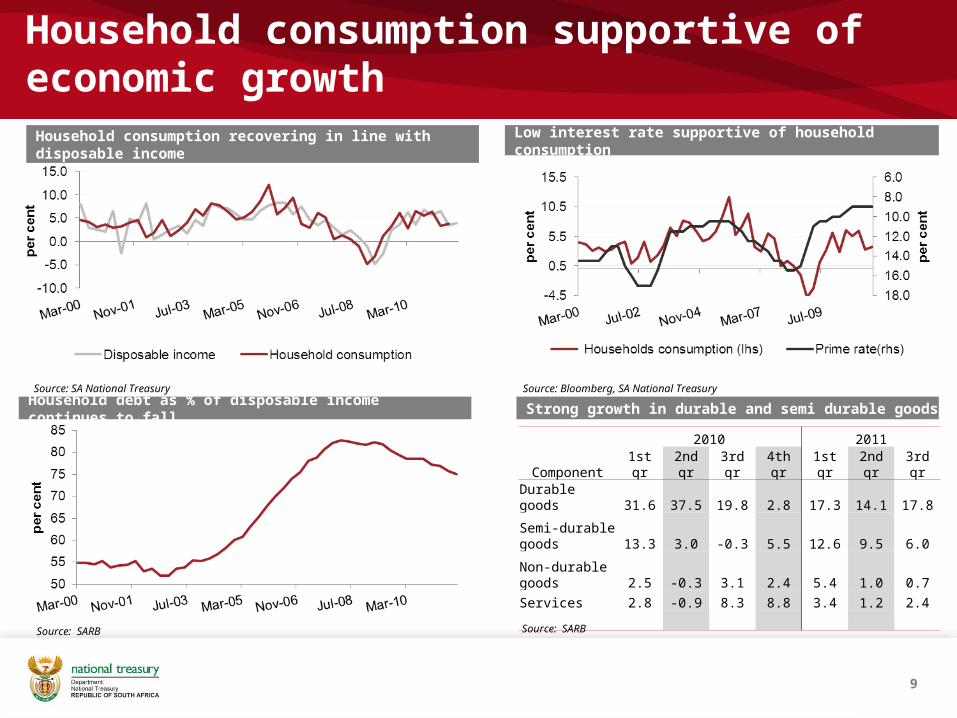

Household consumption supportive of economic growth

Source: SARB

Household consumption recovering in line with disposable income

Household debt as % of disposable income continues to fall

Source: Bloomberg, SA National Treasury

Low interest rate supportive of household consumption

Source: SA National Treasury

Strong growth in durable and semi durable goods

Component

2010 2011

1st qr 2nd qr 3rd qr 4th qr 1st qr 2nd qr 3rd qr

Durable goods 31.6 37.5 19.8 2.8 17.3 14.1 17.8

Semi-durable goods 13.3 3.0 -0.3 5.5 12.6 9.5 6.0

Non-durable goods 2.5 -0.3 3.1 2.4 5.4 1.0 0.7

Services 2.8 -0.9 8.3 8.8 3.4 1.2 2.4

Source: SARB

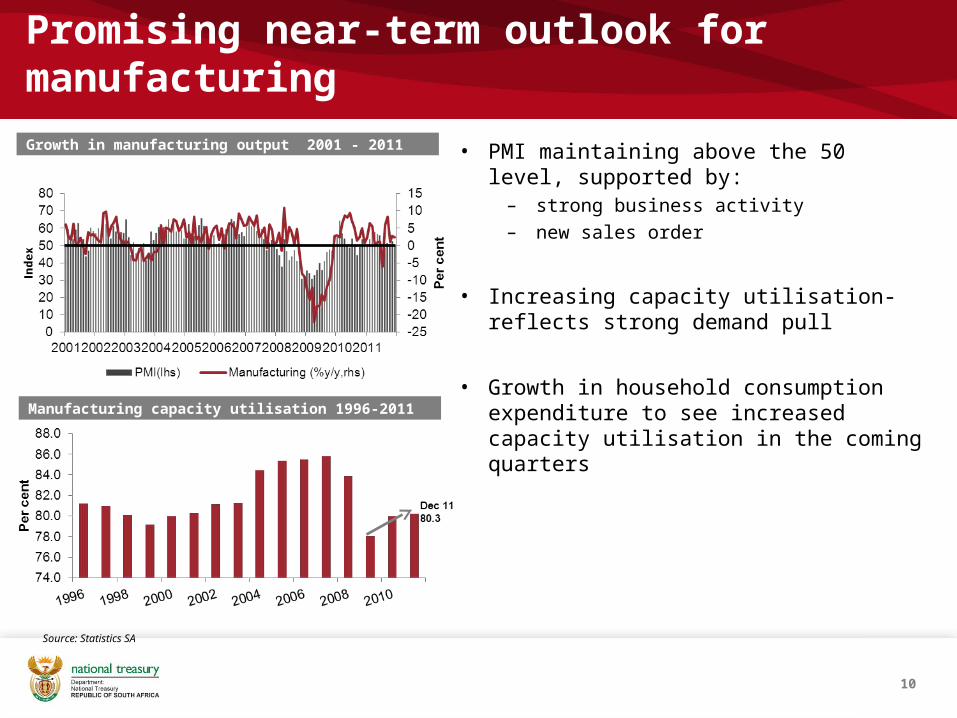

Promising near-term outlook for manufacturing

10

Growth in manufacturing output 2001 - 2011

Manufacturing capacity utilisation 1996-2011

• PMI maintaining above the 50 level, supported by:

– strong business activity– new sales order

• Increasing capacity utilisation-reflects strong demand pull

• Growth in household consumption expenditure to see increased capacity utilisation in the coming quarters

Source: Statistics SA

Manufacturing to benefit from government support

11

• Manufacturing production increased by 2.5% during 2011. Supported by:

– production of motor vehicle & parts;

– basic iron and steel; and

– petrochemicals

• Manufacturing competitiveness enhancement programme will begin in 2012/13,

– production support mechanism;

– distressed funding support to boost productivity and competitiveness; and

– raise investment and create jobs

– R5.75 billion allocation to the programme over three years

Growth in manufacturing output by sector, 2008-2011

1. Weights are based on Statistics South Africa 2005 Large Sample Survey2. Second half of 2011 compared with first half of 20083. Quarter on quarter, seasonally adjusted and annualisedSource: Statistics South Africa

Percetange Weights1

Change from Pre-recession

highs 2 2011 Q420113

Basic iron and steel 22.9 -19.0 2.8 35.9

Petrochemicals 22.1 -6.6 1.4 0.2

Food and beverages 15.4 11.4 2.5 2.4

Motor vehicles and parts 10.9 -12.2 7.4 -31.6

Wood and paper 10.2 -8.9 1.3 38.1

Furniture and other 5.2 -24.9 1.1 -31.4

Textiles and clothing 4.9 -23.2 -2.9 -9.4

Glass,etc 4.8 -14.6 2.4 2.5

Electrical Machinery 2.5 5.8 1.9 17.2

Radio and television 1.1 3.2 11.8 -8.9

Total 100.0 -9.3 2.5 4.1

12

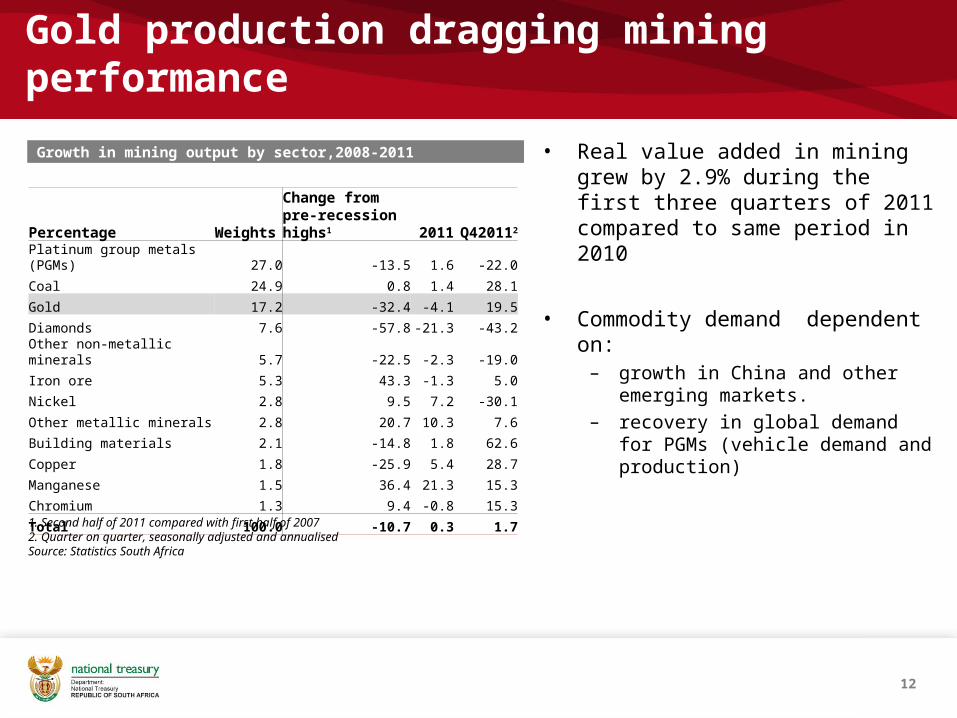

Gold production dragging mining performance

• Real value added in mining grew by 2.9% during the first three quarters of 2011 compared to same period in 2010

• Commodity demand dependent on:– growth in China and other emerging

markets.– recovery in global demand for PGMs

(vehicle demand and production)

Growth in mining output by sector,2008-2011

Percentage WeightsChange from pre-recession highs1 2011 Q420112

Platinum group metals (PGMs) 27.0 -13.5 1.6 -22.0

Coal 24.9 0.8 1.4 28.1

Gold 17.2 -32.4 -4.1 19.5

Diamonds 7.6 -57.8 -21.3 -43.2

Other non-metallic minerals 5.7 -22.5 -2.3 -19.0

Iron ore 5.3 43.3 -1.3 5.0

Nickel 2.8 9.5 7.2 -30.1

Other metallic minerals 2.8 20.7 10.3 7.6

Building materials 2.1 -14.8 1.8 62.6

Copper 1.8 -25.9 5.4 28.7

Manganese 1.5 36.4 21.3 15.3

Chromium 1.3 9.4 -0.8 15.3

Total 100.0 -10.7 0.3 1.7

1. Second half of 2011 compared with first half of 20072. Quarter on quarter, seasonally adjusted and annualisedSource: Statistics South Africa

13

Shifting trade patterns

• South Africa’s trade patterns have changed in response to global growth trends

• Emerging Markets and SADC share in South Africa’s export basket is rising:

– exports to China increased to 13% in 2011 (averaged 4.2% between 2005-2008)

– SADC absorbed 10.5% of South Africa’s exports over the past year

– share of exports to the European Union declined from 33% in 2005 to 21.6% in 2011

Source: SA National Treasury

Mapping South Africa’s exports,2011

Automobiles (26.1) Platinum (11.6) Rhodium( 5.9)Palladium (5.3)

Purifying Machinery (11.4) Platinum (7.1)Coal (7.0)Automobiles (6.2)

Aviation spirit (6.1) Iron & Steel (3.6) Electrical energy (2.1) Diesel trucks( 5.3)

Iron ore(45.9) Coal (7.0) Chromium ores (10.9) Ferro-chromium (8.9)

Platinum (37.5) Iron ore (11.8) Aluminium (4.8) Ferro-chromium (4.8)

Region/Country Share of Exports (%) Main Products (%)

14

3. Public Finance

15

Consolidated government fiscal framework

Primary budget deficit to narrow significantly overthe medium-term

Source: SA National Treasury

Source: SA National Treasury

• Improvement of 0.7% in the budget balance from 5.5% at 2011 MTBPS as a result of:

– revenue overruns – relatively slow growth in expenditure

• Stabilisation of non-interest spending and

higher revenue to reduce primary budget deficit from -1.6% in 2009/10 to -0.3% of GDP in 2014/15

• Shifting the composition of spending from current to investment expenditure

Consolidated government fiscal framework, 2010/11 – 2014/15

2010/11 2011/12 2012/13 2013/14 2014/15R billion Actual Estimate Medium-term estimates

Revenue 757.5 830.2 904.8 1,005.9 1,118.2% of GDP 27.5 27.7 27.4 27.8 28

Expenditure 874.2 972.5 1,058.3 1,149.1 1,239.7% of GDP 31.7 32.5 32.1 31.7 31.0

Budget balance -116.6 -142.3 -153.5 -143.2 -121.5% of GDP -4.2 -4.8 -4.6 -4.0 -3.0

16

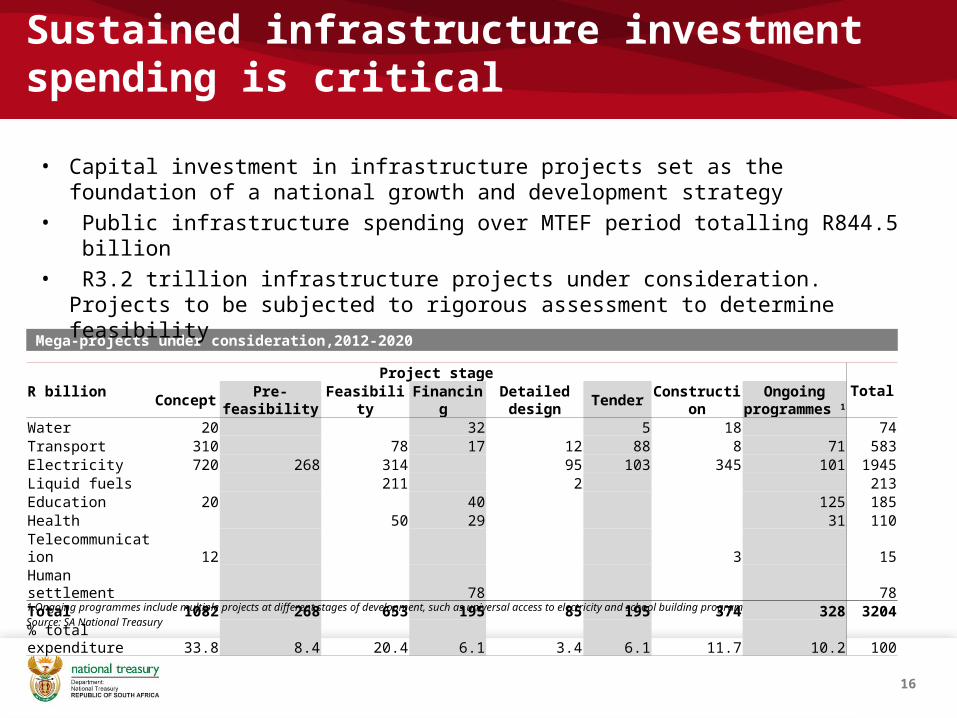

Sustained infrastructure investment spending is critical

Mega-projects under consideration,2012-2020

• Capital investment in infrastructure projects set as the foundation of a national growth and development strategy

• Public infrastructure spending over MTEF period totalling R844.5 billion• R3.2 trillion infrastructure projects under consideration. Projects to be subjected to

rigorous assessment to determine feasibility

Source: SA National Treasury

Project stage

TotalR billionConcept Pre-feasibility Feasibility Financing

Detailed design

TenderConstructio

nOngoing

programmes 1

Water 20 32 5 18 74Transport 310 78 17 12 88 8 71 583Electricity 720 268 314 95 103 345 101 1945Liquid fuels 211 2 213Education 20 40 125 185Health 50 29 31 110Telecommunication 12 3 15Human settlement 78 78Total 1082 268 653 195 85 195 374 328 3204% total expenditure 33.8 8.4 20.4 6.1 3.4 6.1 11.7 10.2 100

1.Ongoing programmes include multiple projects at different stages of development, such as universal access to electricity and school building program

Major economic infrastructure projects

17

Energy• Kusile and Medupi are under

construction – first units will be operational in 2013 and 2014 respectively

• 1 415 MW of the 3 725 MW renewable energy programme has been procured

• SANRAL to spend R25 billion on new roads and R18 billion on maintenance

• PRASA to spend R80 billion over 20 years on commuter rail

Transport

Water & Sanitation

Telecommunication

• The Komati water augmentation scheme scheduled to be completed in 2012

• Olifants river water resource scheduled to be completed in 2016

• R75 billion to be spent on water infrastructure over the MTEF

• R433 million allocated to acid mine drainage

• Sentech’s digitalization of the television terrestrial network

• Infraco’s projects to increase broadband capacity

18

Public sector borrowing requirement set to moderate over medium-term

• The public sector borrowing requirement is projected to fall from 7.2% as a percentage of GDP in 2011/12 to 5.1% by 2014/15

– SOEs ability to collect internally generated funds has improved, putting less pressure on debt finance

– lower municipal debt issuance

• Borrowing of non-financial public enterprises to decline from 2.3% to 1.9% of GDP over the forecast period

Source: SA National Treasury

1.3

6.8

4.5 4.9 4.84.1

3.21.7

2.9

22.3 2.3

2.1

1.9

-1.5

2.6

-2

0

2

4

6

8

10

per

cen

t o

f G

DP

General government Non-financial public enterprises

Public sector borrowing requirement

Forecast to decrease from 7.2% to 5.1%

19

Public debt sustainable over medium-term

• Net loan debt forecasted to peak at around 38.5% of GDP in 2014/15

• Counter-cyclical fiscal stance led to increased borrowing to meet expenditure commitments

• From 2013/14 onward, new government borrowing will finance investment spending

Net loan debt stabilises at 38.5% of GDP

As at 31 March 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

R billion Actual Estimate Medium-term estimates

Domestic Gross loan debt1 529.7 705.5 892.7 1,072.9 1,247.4 1,430.6 1,595.6

Cash balances -101.3 -106.6 -111.4 -129.4 -109.1 -103.4 -102.2

Net loan debt2 428.4 598.9 781.3 943.5 1,138.3 1,327.2 1,493.4

Foreign Gross loan debt1 97.3 99.5 97.9 129.5 107.5 97.6 99.3

Cash balances - -25.2 -60.4 -75.5 -56.4 -54.1 -55.0

Net loan debt2 97.3 74.3 37.5 54.0 51.1 43.5 44.3

Total gross loan debt

627.0 805.0 990.6 1,202.4 1,354.9 1,528.2 1,694.9

Total net loan debt 525.7 673.1 818.8 997.5 1,189.4 1,370.7 1,537.7

As percentage of GDP: Total gross loan debt

27.1 33.0 36.0 40.1 41.0 42.2 42.4

Total net loan debt 22.7 27.6 29.8 33.3 36.0 37.8 38.5

1. Forward estimates are based on projections of exchange and inflation rates2. Net loan debt is calculated with due account of the cash balances of the National Revenue Fund(bank balances of government's accounts with the Reserve Bank and commercial banks)3. Foreign currency deposits revaluated at forward estimates of exchange ratesSource: National Treasury

20

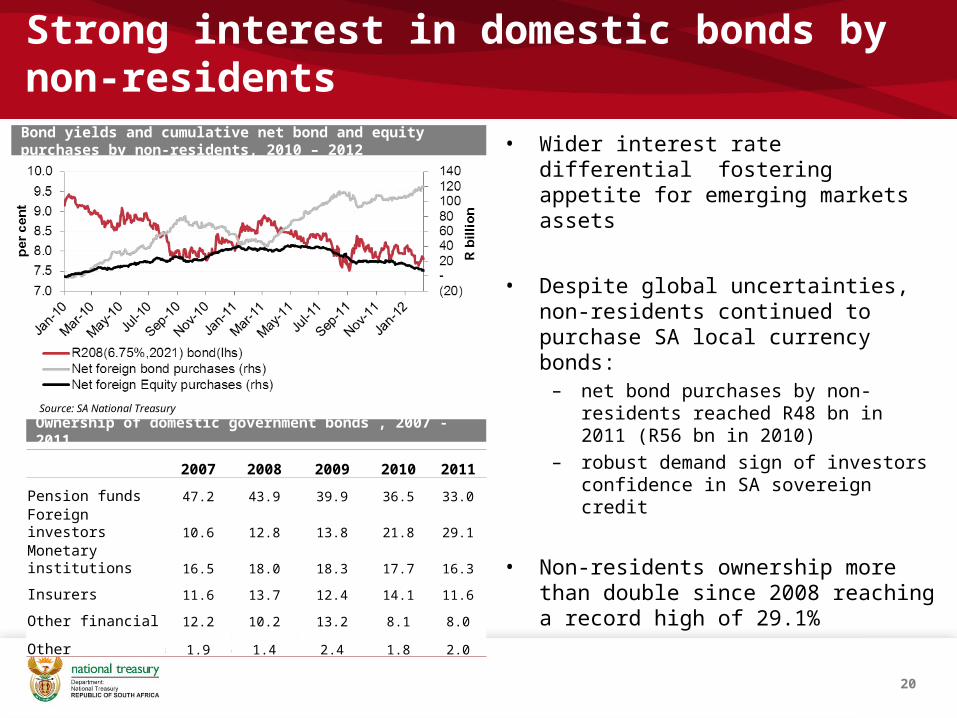

Strong interest in domestic bonds by non-residents

• Wider interest rate differential fostering appetite for emerging markets assets

• Despite global uncertainties, non-residents continued to purchase SA local currency bonds:

– net bond purchases by non-residents reached R48 bn in 2011 (R56 bn in 2010)

– robust demand sign of investors confidence in SA sovereign credit

• Non-residents ownership more than double since 2008 reaching a record high of 29.1%

Ownership of domestic government bonds , 2007 - 2011

Source: SA National Treasury

Bond yields and cumulative net bond and equity purchases by non-residents, 2010 – 2012

Source: Share Transaction Totally Electronic LTD(Strate)

2007 2008 2009 2010 2011

Pension funds 47.2 43.9 39.9 36.5 33.0

Foreign investors 10.6 12.8 13.8 21.8 29.1

Monetary institutions 16.5 18.0 18.3 17.7 16.3

Insurers 11.6 13.7 12.4 14.1 11.6

Other financial 12.2 10.2 13.2 8.1 8.0

Other 1.9 1.4 2.4 1.8 2.0

21

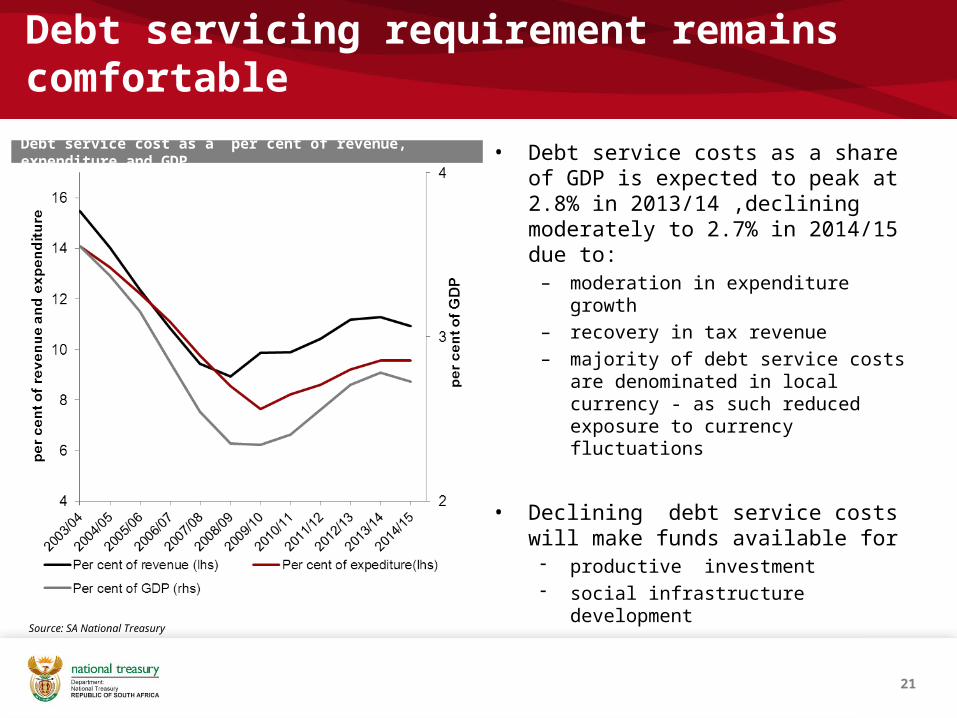

Debt servicing requirement remains comfortable

• Debt service costs as a share of GDP is expected to peak at 2.8% in 2013/14 ,declining moderately to 2.7% in 2014/15 due to:

– moderation in expenditure growth– recovery in tax revenue– majority of debt service costs are

denominated in local currency - as such reduced exposure to currency fluctuations

• Declining debt service costs will make funds available for productive investment social infrastructure development

Debt service cost as a per cent of revenue, expenditure and GDP

Source: SA National Treasury

22

Debt metrics highlight South Africa as a relatively low risk investment destination

• Government debt-to-GDP ratio remains low relative to that of the developed world

• It compares favourably to that of emerging markets peers

• The budget framework endeavours to keep the debt ratio low to avoid crowding out non-interest expenditure

Source: IMF World Economic Outlook, September 2011

Gross debt-to-GDP comparison (2011 estimates)

23

4. Monetary Policy

24

Cost push pressures driving inflation

• Headline inflation driven largely by cost push pressures

• Price of electricity has been an important driver of administered prices, as well as petrol prices

• Headline inflation is expected to peak at 6.6% in 2Q:2012 and remain outside the upper end of the target range during 2012

• Core inflation is expected to peak around 5.5 %

Administered prices (% change y/y)

Headline & Core CPI (% change y/y)

Source: SARB

Source: SARB

25

Inflation expectations still anchored

• The overall wage settlement rate increased at a slower pace in 2011, but it is uncertain whether this is sustainable

• Employment growth has surprised on the upside

• Inflation expectations have increased moderately, and seem to be anchored around the upper end of the inflation target

BER Inflation expectations survey, annual averages

Wage settlements

Source: Andrew Levy Employment Publications and Statistics South Africa

Source: Bureau for Economic Research, University of Stellenbosch

26

Subdued credit extension and supportive monetary policy

• Recovery in total loans and advances has been slow when measured in a historical context

• Housing market is relatively weak, reflected by slow growth in mortgage advances

• Economic growth forecasts have been revised lower and subject to global developments

• Conflicting pressures on monetary policy make a stable repo rate more desirable

Subdued credit extension, 12 month growth

Short and long-term interest rates

Months before returnto positive growth

Months after return to positive growth

Source: SARB

27

5. External Vulnerability

28

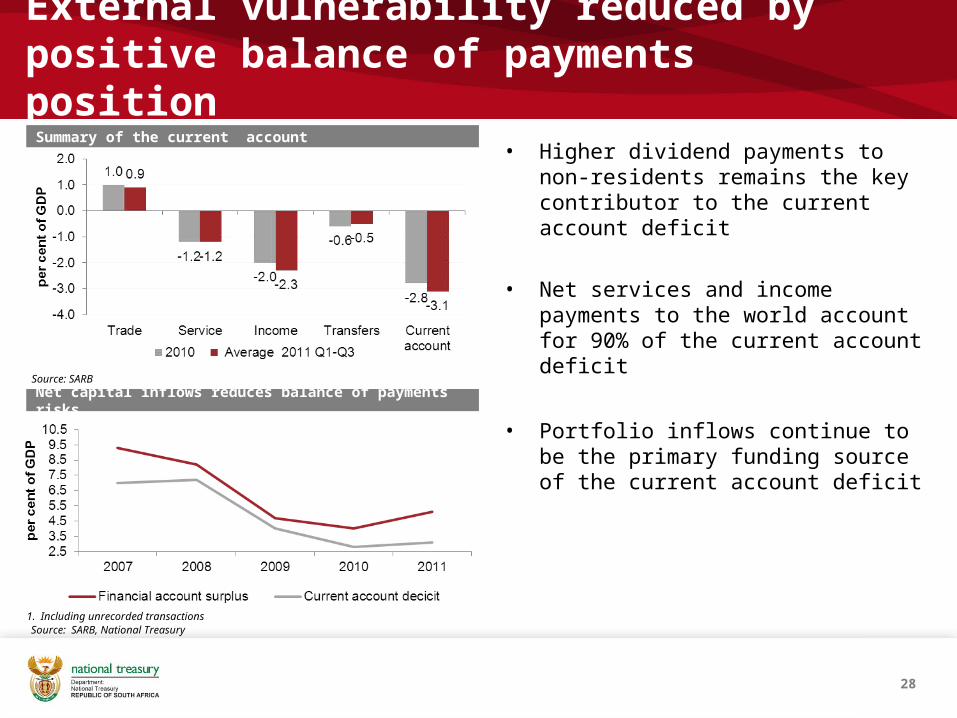

External vulnerability reduced by positive balance of payments position

• Higher dividend payments to non-residents remains the key contributor to the current account deficit

• Net services and income payments to the world account for 90% of the current account deficit

• Portfolio inflows continue to be the primary funding source of the current account deficit

1. Including unrecorded transactions

Source: SARB

Source: SARB, National Treasury

Summary of the current account

Net capital inflows reduces balance of payments risks

29

7. Conclusion

30

• The macroeconomic landscape remains constraint, requiring continued policy accommodation

• Continued focus on job creation, expansion in infrastructure investment and spending on social development

• Fiscal and monetary policy cushioning South Africa from the global slowdown, and employment should continue to expand

• Prudent fiscal management and automatic stabilisers ensure that the fiscal position should return to pre-crisis levels without requiring meaningful fiscal austerity

• Low debt to GDP levels and total external debt remains low and manageable

Concluding thoughts