1 Preliminary Results Year to 31 December 2003. 2 Sir Neville Simms Chairman.

47

1 Preliminary Results Year to 31 December 2003

-

Upload

sharlene-mitchell -

Category

Documents

-

view

216 -

download

2

Transcript of 1 Preliminary Results Year to 31 December 2003. 2 Sir Neville Simms Chairman.

1

Preliminary ResultsYear to 31 December 2003

2

Sir Neville SimmsChairman

3

Philip CoxChief Executive Officer

Group overview

2003 EPS in line with earnings guidance

Earnings underpinned by good performance in all regions outside the US

Impairment in US at £404m is the prudent approach

Free cash flow positive Balance sheet liquidity

2003 EPS in line with earnings guidance

Earnings underpinned by good performance in all regions outside the US

Impairment in US at £404m is the prudent approach

Free cash flow positive Balance sheet liquidity

2003 2002

EPS

PBIT

Free cash flow*

15.5p

£388m

£252m

* Free cash flow is defined as operating cash flow, minus interest, tax and maintenance capex, but before growth capex

10.2 p

£285m

£121m

All numbers are before exceptional items

North AmericaNorth America

Key highlights 2003

Comprehensive review of options for US business underway

Pre-emptive discussions with bank group to renegotiate non-recourse project debt - $900m

Focussed cost reduction plan implemented– $12m saving in cash operating costs– creation of ‘in house’ outage teams

Hays mothballed in early 2004 for indefinite period

Alstom turbine performance on track– LD ‘buydowns’ £56m in 2003

Comprehensive review of options for US business underway

Pre-emptive discussions with bank group to renegotiate non-recourse project debt - $900m

Focussed cost reduction plan implemented– $12m saving in cash operating costs– creation of ‘in house’ outage teams

Hays mothballed in early 2004 for indefinite period

Alstom turbine performance on track– LD ‘buydowns’ £56m in 2003

ERCOT market background

Demand (peak)

Capacity

Reserve margin

Demand growth (2.8%)

In construction

Mothballed / retired (inc Hays)

Controlled by banks / distressed

GW > 30 years

Distressed GW > 30 years

60.2

81.2

35%

1.7

2.4

8.7*

32.7

22.6

7.3

GW

Demand / Supply

$1+ $2+ $4

Gas price$perBTUm

North Zonepremium

$/MWh

* of which 1.9 Reliability Must Run CCGT plant- 7200 heat rate- calendar average spreads- south zone prices

8

6

4

2

0 2002actual

2003actual

2004 Feb 04

forward curve

$MWh

Market spark spreads(peak hours)

3.15 5.30 5.00 - 5.50

+

+

ERCOT - market update

North Zone redefined - positive for Midlothian– planned move to nodal pricing (a refined

zonal system) in 2006, a further positive for Midlothian

Transparent market mechanism required Plant retirement largest single variable -

particularly older high heat rate plant– 8.7 GW mothballed to date - of which 1.9 GW

Reliability Must Run Demand growth 3% pa

North Zone redefined - positive for Midlothian– planned move to nodal pricing (a refined

zonal system) in 2006, a further positive for Midlothian

Transparent market mechanism required Plant retirement largest single variable -

particularly older high heat rate plant– 8.7 GW mothballed to date - of which 1.9 GW

Reliability Must Run Demand growth 3% pa

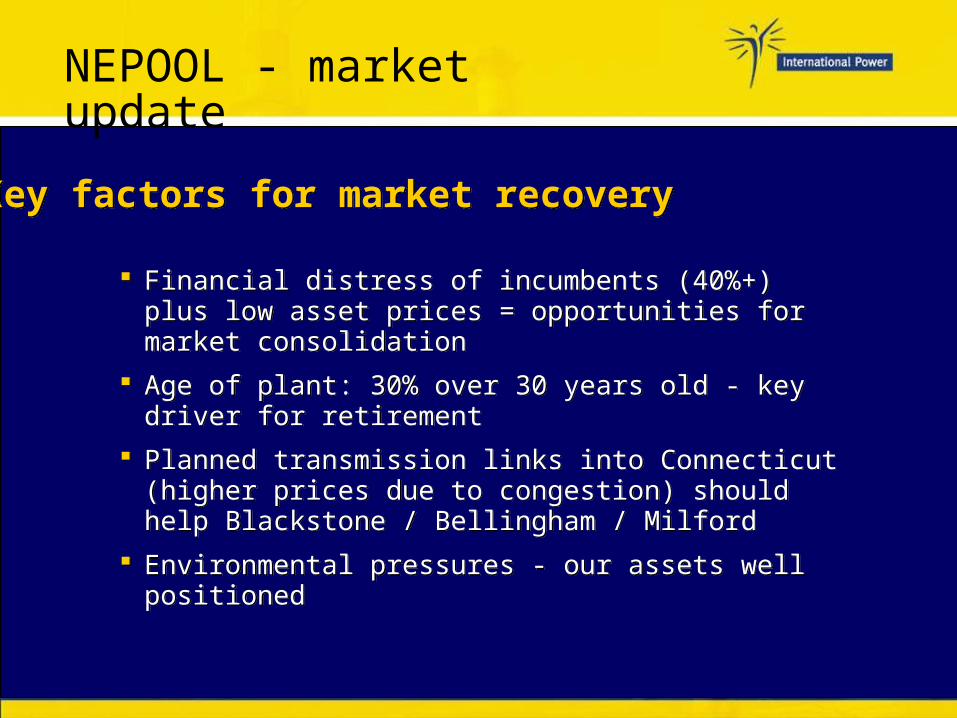

Key factors for market recoveryKey factors for market recovery

NEPOOL market background

Demand (peak)

Capacity

Reserve margin

Demand growth (1.5%)

In construction

Mothballed / retired

Controlled by banks / distressed

GW > 30 years

Distressed GW > 30 years

25.4

31.4

24%

0.4

0.4

1.1

15.0

10.7

4.8

GW

Market spark spreads*(peak hours)Demand / Supply

15

12

9

6

3

02002

actual2003

actual2004

Feb 04forward curve

Gas price$perBTUm

CCGT plant- 7200 heat rate- calendar average spreads- excludes ICAP / UCAP

$MWh

$3.70 $6.80 $6.50 -7.00

*

NEPOOL - market update

Financial distress of incumbents (40%+) plus low asset prices = opportunities for market consolidation

Age of plant: 30% over 30 years old - key driver for retirement

Planned transmission links into Connecticut (higher prices due to congestion) should help Blackstone / Bellingham / Milford

Environmental pressures - our assets well positioned

Financial distress of incumbents (40%+) plus low asset prices = opportunities for market consolidation

Age of plant: 30% over 30 years old - key driver for retirement

Planned transmission links into Connecticut (higher prices due to congestion) should help Blackstone / Bellingham / Milford

Environmental pressures - our assets well positioned

Key factors for market recoveryKey factors for market recovery

US strategy

US debt negotiations the clear priority– comprehensive review of options– long term solution required

Operate and trade current portfolio to maximum efficiency

Growth opportunities– low asset prices in ERCOT and NEPOOL

create merchant opportunities– contracted assets

US debt negotiations the clear priority– comprehensive review of options– long term solution required

Operate and trade current portfolio to maximum efficiency

Growth opportunities– low asset prices in ERCOT and NEPOOL

create merchant opportunities– contracted assets

EuropeEurope

Key highlights 2003

Record financial performance at EOP– power, district heating both strong performers -

power forward contracted through 2004

Consistent high availability at Pego (Portugal) and Uni-Mar (Turkey) ensured strong financial results

Flexible and responsive UK operations delivered improved H2 performance– successful and quick demothballing of Deeside

250 MW unit

Record financial performance at EOP– power, district heating both strong performers -

power forward contracted through 2004

Consistent high availability at Pego (Portugal) and Uni-Mar (Turkey) ensured strong financial results

Flexible and responsive UK operations delivered improved H2 performance– successful and quick demothballing of Deeside

250 MW unit

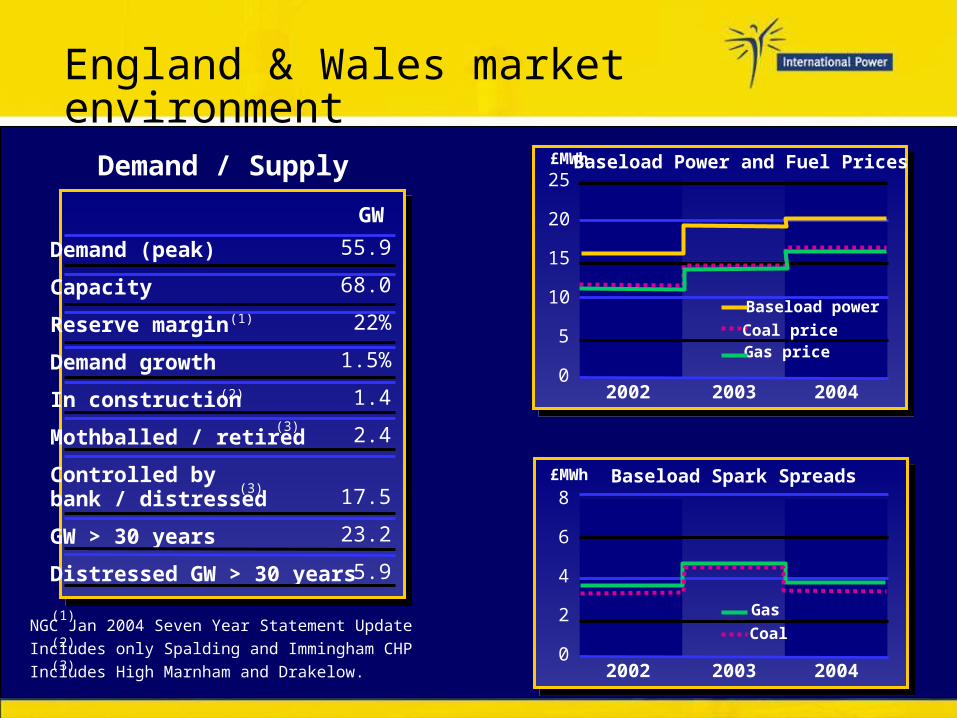

England & Wales market environment

Demand (peak)

Capacity

Reserve margin

Demand growth

In construction

Mothballed / retired

Controlled by bank / distressed

GW > 30 years

Distressed GW > 30 years

55.9

68.0

22%

1.5%

1.4

2.4

17.5

23.2

5.9

GW

Demand / Supply

(1)

(2)

(3)

(3)

(1)

(2)

(3)

NGC Jan 2004 Seven Year Statement UpdateIncludes only Spalding and Immingham CHPIncludes High Marnham and Drakelow.

25

20

15

10

5

02002 2003 2004

£MWh

8

6

4

2

02002 2003 2004

£MWh

Gas price

Baseload power

Coal price

Baseload Spark Spreads

Baseload Power and Fuel Prices

Gas

Coal

UK 2005 forward power prices currently £4 MWh up on 2004– starting to reflect cost of carbon

Carbon allocations announced:– UK targets higher CO2 emission reductions than EU – power industry bears disproportionate reduction - lobbying

continues– gas plants advantaged vs coal - positive for Deeside; uncertainty

for Rugeley Deeside and Rugeley allocations represent load factors of 65% and

47% respectively Carbon allocation and CO2 prices also drive FGD decisions at coal

fired plants– opt in LCPD = capex– opt out LCPD = lower load factor– decision by June 2004

European assets:– EOP has FGD installed - well positioned– PEGO expects to fit FGD (capex cost recovered through PPA)

UK 2005 forward power prices currently £4 MWh up on 2004– starting to reflect cost of carbon

Carbon allocations announced:– UK targets higher CO2 emission reductions than EU – power industry bears disproportionate reduction - lobbying

continues– gas plants advantaged vs coal - positive for Deeside; uncertainty

for Rugeley Deeside and Rugeley allocations represent load factors of 65% and

47% respectively Carbon allocation and CO2 prices also drive FGD decisions at coal

fired plants– opt in LCPD = capex– opt out LCPD = lower load factor– decision by June 2004

European assets:– EOP has FGD installed - well positioned– PEGO expects to fit FGD (capex cost recovered through PPA)

Carbon update

European strategy

Support the drive for consolidation in UK power generation

Opportunities in liberalising markets where we already have a presence– Portugal– Czech Republic– Turkey

Support the drive for consolidation in UK power generation

Opportunities in liberalising markets where we already have a presence– Portugal– Czech Republic– Turkey

Middle EastMiddle East

Middle East - highlights in 2003 Umm Al Nar - Abu Dhabi

– 2,200 MW, 162 MIGD - brownfield project– bid, won and financed $2.1 bn project– partners - TEPCO and Mitsui– 23 year PPA with ADWEC

Saudi Aramco - Saudi Arabia– 1,075 MW, + steam - 4 plants - greenfield project– bid, won and financed $700m project– partner - Saudi Oger– 20 year ECAs with Saudi Aramco

Shuweihat - Abu Dhabi– 1,500 MW, 100 MIGD - greenfield project– successfully commissioned 2 gas turbines and

desalination unit ahead of schedule– 20 year PPA with ADWEC

Strong operational and customer focus to ensure assets perform to contract

Strong growth region for IPR

Umm Al Nar - Abu Dhabi– 2,200 MW, 162 MIGD - brownfield project– bid, won and financed $2.1 bn project– partners - TEPCO and Mitsui– 23 year PPA with ADWEC

Saudi Aramco - Saudi Arabia– 1,075 MW, + steam - 4 plants - greenfield project– bid, won and financed $700m project– partner - Saudi Oger– 20 year ECAs with Saudi Aramco

Shuweihat - Abu Dhabi– 1,500 MW, 100 MIGD - greenfield project– successfully commissioned 2 gas turbines and

desalination unit ahead of schedule– 20 year PPA with ADWEC

Strong operational and customer focus to ensure assets perform to contract

Strong growth region for IPR

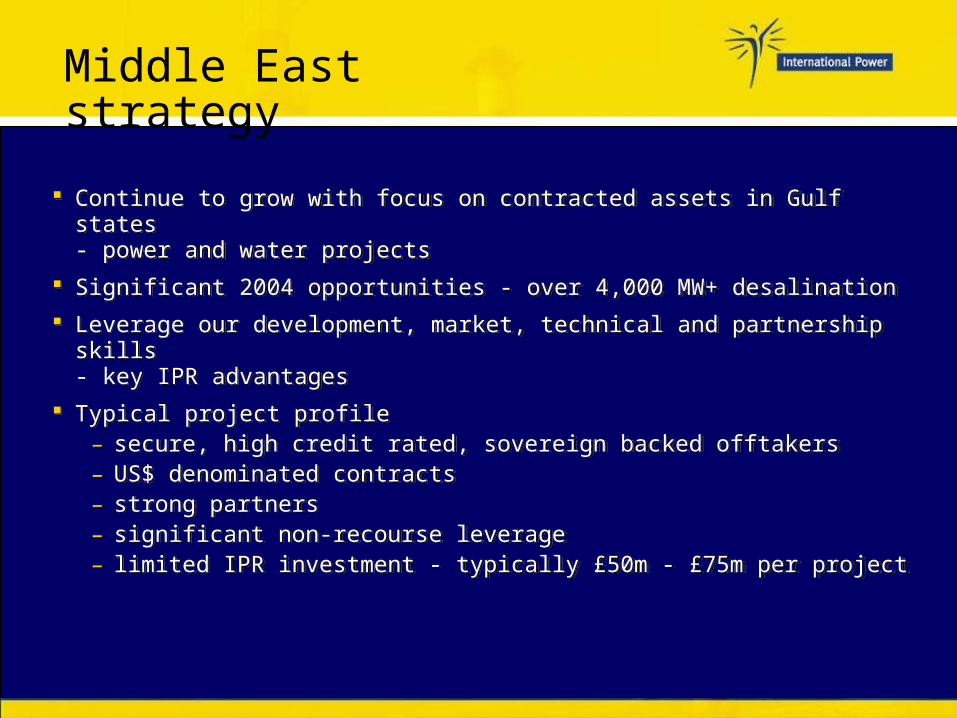

Middle East strategy

Continue to grow with focus on contracted assets in Gulf states - power and water projects

Significant 2004 opportunities - over 4,000 MW+ desalination

Leverage our development, market, technical and partnership skills - key IPR advantages

Typical project profile– secure, high credit rated, sovereign backed offtakers– US$ denominated contracts– strong partners– significant non-recourse leverage– limited IPR investment - typically £50m - £75m per project

Continue to grow with focus on contracted assets in Gulf states - power and water projects

Significant 2004 opportunities - over 4,000 MW+ desalination

Leverage our development, market, technical and partnership skills - key IPR advantages

Typical project profile– secure, high credit rated, sovereign backed offtakers– US$ denominated contracts– strong partners– significant non-recourse leverage– limited IPR investment - typically £50m - £75m per project

AustraliaAustralia

Australia - achievements 2003

Strong forward contracted position in 2003 underpinned earnings

SEA Gas 687km pipeline– construction completed 1 January 2004 - on time,

and on budget Hazelwood mine

– first coal delivered from new mine extension in early February 04

– long term security of supply Canunda wind farm (46 MW)

– permitted, construction starts Q2– 10 year offtake with AGL– commercial operation planned Q2 2005

Strong forward contracted position in 2003 underpinned earnings

SEA Gas 687km pipeline– construction completed 1 January 2004 - on time,

and on budget Hazelwood mine

– first coal delivered from new mine extension in early February 04

– long term security of supply Canunda wind farm (46 MW)

– permitted, construction starts Q2– 10 year offtake with AGL– commercial operation planned Q2 2005

Australia market background

Demand GW (peak)

Capacity GW *

Reserve margin %

Demand growth

Demand GW (peak)

Capacity GW *

Reserve margin %

Demand growth

VictoriaVictoria S AustraliaS Australia

2.8

3.7

32%

3.0%

Reserve margin tightening in Victoria and SA but not yet reflected in forward curve

2004 and 2005 forward prices show progressive recovery from 2003

– but not yet to 2001 and 2002 levels

8.5

9.5

12%

3.0%

* Includes average interconnector availability of 50%

Australia strategy

Scale - largest privately owned generator

Optimise forward contracted position

Preserve position as low cost producer in both Victoria and South Australia

Growth through acquisition– principal targets are contracted assets

Scale - largest privately owned generator

Optimise forward contracted position

Preserve position as low cost producer in both Victoria and South Australia

Growth through acquisition– principal targets are contracted assets

Rest of the WorldRest of the World

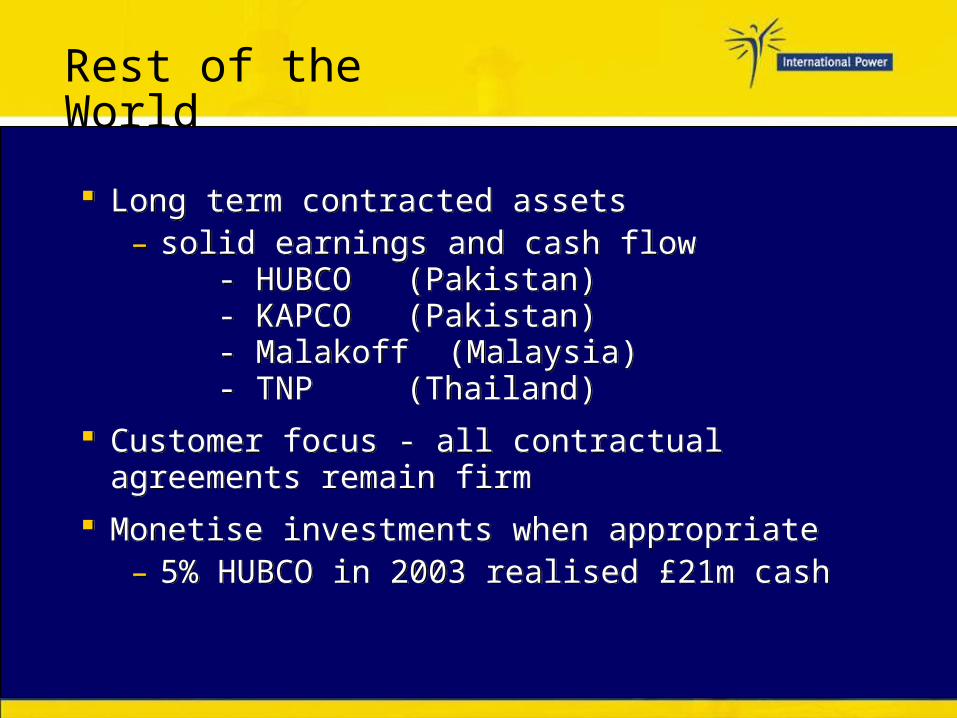

Rest of the World

Long term contracted assets – solid earnings and cash flow

- HUBCO (Pakistan) - KAPCO (Pakistan) - Malakoff (Malaysia) - TNP (Thailand)

Customer focus - all contractual agreements remain firm

Monetise investments when appropriate– 5% HUBCO in 2003 realised £21m cash

Long term contracted assets – solid earnings and cash flow

- HUBCO (Pakistan) - KAPCO (Pakistan) - Malakoff (Malaysia) - TNP (Thailand)

Customer focus - all contractual agreements remain firm

Monetise investments when appropriate– 5% HUBCO in 2003 realised £21m cash

26

Mark WilliamsonChief Financial Officer

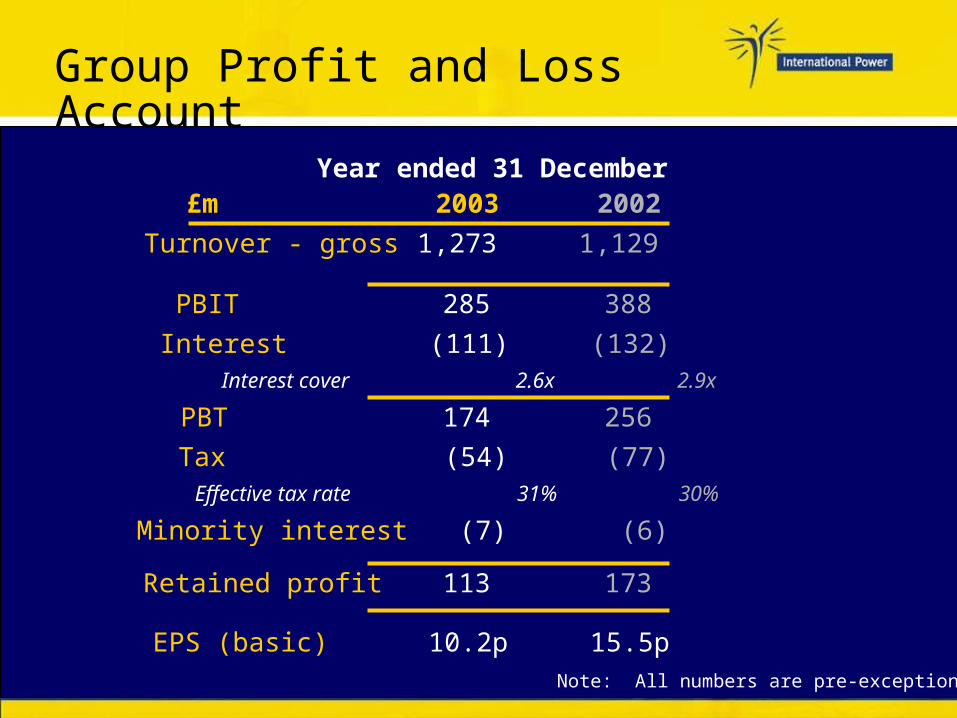

Group Profit and Loss Account

1,129 1,273 Turnover - gross

256 174 PBT

Year ended 31 December

15.5p

173

(6)31%

(77)

2.6x

(132)

388

2002

(7)Minority interest30%Effective tax rate

2.9xInterest cover

10.2pEPS (basic)

113 Retained profit

(54)Tax

(111)Interest

285 PBIT

2003£m

Note: All numbers are pre-exceptional

Exceptional items

- (16)Capitalised financing charges write off

- (404)US impairment

- 3 China exit

- 7 Czech Republic (sale of shares)

-

-

17

35

HUBCO - sale of share

- impairment reversal

Year ended 31 December

(60)

1

(61)

42

(58)

(45)

2002

(332)

26

(358)

-

-

-

2003

Tax effect

Net

Total

KAPCO dividend

Rugeley impairment

Deeside impairment

£m

US Impairment

Key assumptions:

Whole life cash flow used

Current forward curve in short term

New entrant pricing assumed at market equilibrium for long term

Discounted at WACC of the US business

Key assumptions:

Whole life cash flow used

Current forward curve in short term

New entrant pricing assumed at market equilibrium for long term

Discounted at WACC of the US business

265 600 Current carrying valueUS installed merchant capacity is 4,050 MW

(178)

443

$/kW

(404)Impairment

1,004 Book value of US assets pre impairment

£m

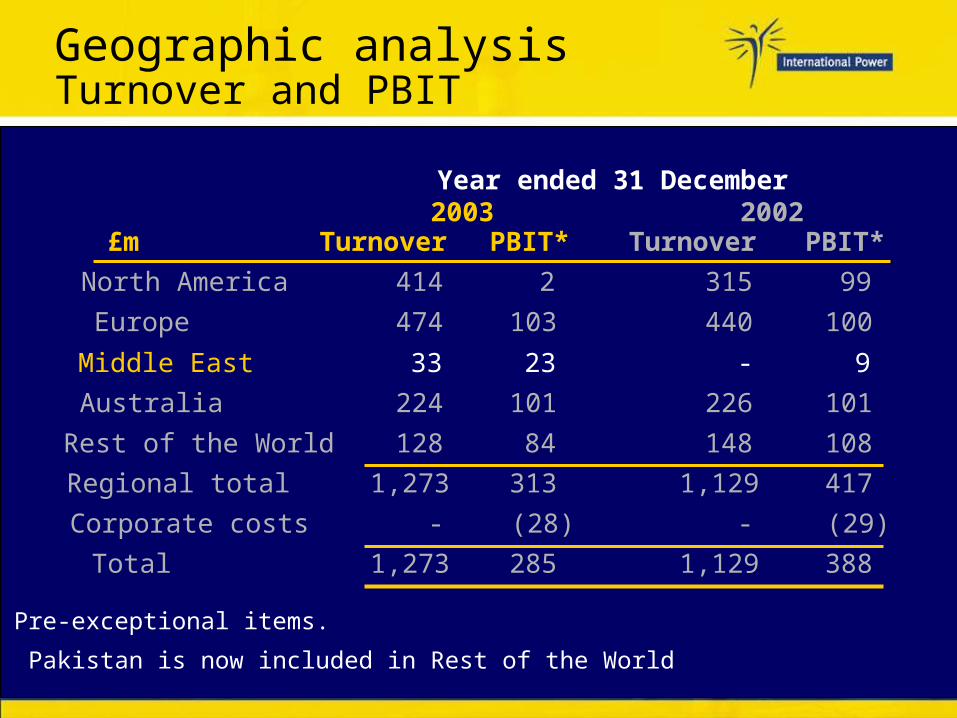

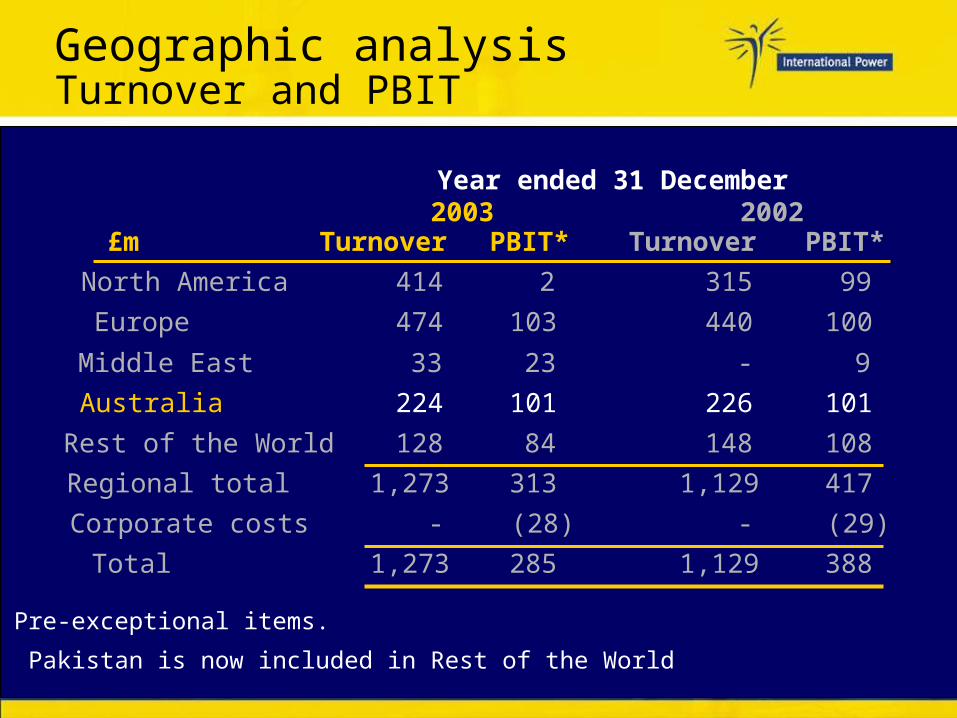

Geographic analysisTurnover and PBIT

Year ended 31 December

417 1,129313 1,273Regional total

* Pre-exceptional items.

Pakistan is now included in Rest of the World

388 1,129285 1,273Total

(29)-(28)-Corporate costs

108 14884 128Rest of the World

101 226101 224Australia

9 -23 33Middle East

100 440103 474Europe

99 3152 414North America

PBIT*TurnoverPBIT*Turnover£m20022003

Geographic analysisTurnover and PBIT

Year ended 31 December

417 1,129313 1,273Regional total

388 1,129285 1,273Total

(29)-(28)-Corporate costs

108 14884 128Rest of the World

101 226101 224Australia

9 -23 33Middle East

100 440103 474Europe

99 3152 414North America

PBIT*TurnoverPBIT*Turnover£m20022003

* Pre-exceptional items.

Pakistan is now included in Rest of the World

Geographic analysisTurnover and PBIT

Year ended 31 December

417 1,129313 1,273Regional total

388 1,129285 1,273Total

(29)-(28)-Corporate costs

108 14884 128Rest of the World

101 226101 224Australia

9 -23 33Middle East

100 440103 474Europe

99 3152 414North America

PBIT*TurnoverPBIT*Turnover£m20022003

* Pre-exceptional items.

Pakistan is now included in Rest of the World

Geographic analysisTurnover and PBIT

Year ended 31 December

417 1,129313 1,273Regional total

388 1,129285 1,273Total

(29)-(28)-Corporate costs

108 14884 128Rest of the World

101 226101 224Australia

9 -23 33Middle East

100 440103 474Europe

99 3152 414North America

PBIT*TurnoverPBIT*Turnover£m20022003

* Pre-exceptional items.

Pakistan is now included in Rest of the World

Geographic analysisTurnover and PBIT

Year ended 31 December

417 1,129313 1,273Regional total

388 1,129285 1,273Total

(29)-(28)-Corporate costs

108 14884 128

101 226101 224Australia

9 -23 33Middle East

100 440103 474Europe

99 3152 414North America

PBIT*TurnoverPBIT*Turnover£m20022003

Rest of the World

* Pre-exceptional items.

Pakistan is now included in Rest of the World

Geographic analysisTurnover and PBIT

Year ended 31 December

417 1,129313 1,273Regional total

388 1,129285 1,273Total

(29)-(28)-Corporate costs

108 14884 128Rest of the World

101 226101 224Australia

9 -23 33Middle East

100 440103 474Europe

99 3152 414North America

PBIT*TurnoverPBIT*Turnover£m20022003

* Pre-exceptional items.

Pakistan is now included in Rest of the World

Geographic analysisTurnover and PBIT

Year ended 31 December

417 1,129313 1,273Regional total

388 1,129285 1,273Total

(29)-(28)-Corporate costs

108 14884 128

101 226101 224Australia

9 -23 33Middle East

100 440103 474Europe

99 3152 414North America

PBIT*TurnoverPBIT*Turnover£m20022003

Rest of the World

* Pre-exceptional items.

Pakistan is now included in Rest of the World

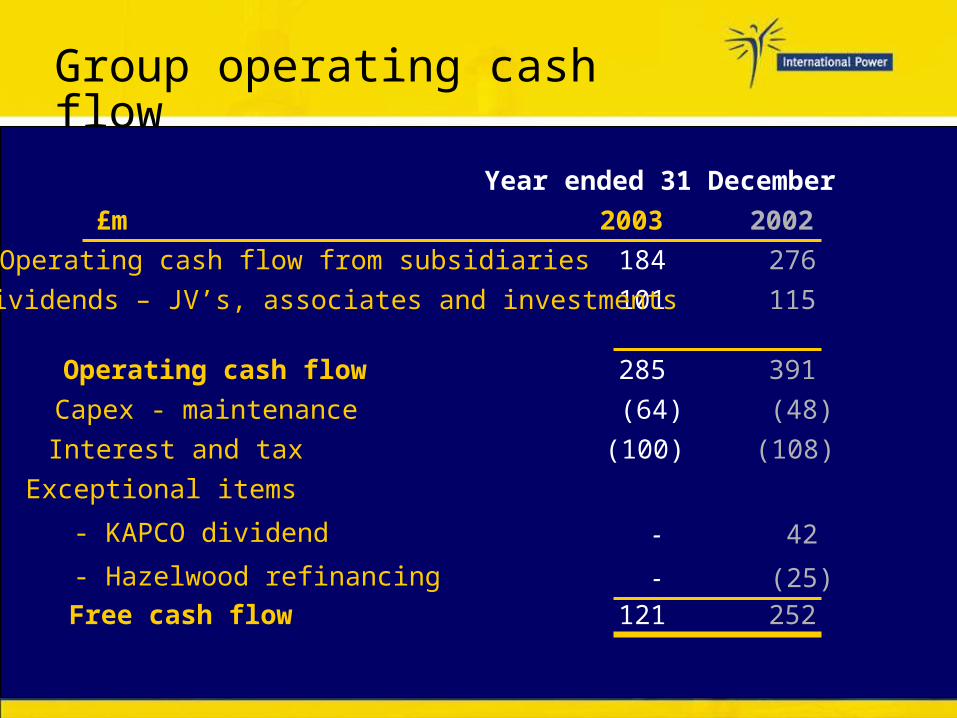

Group operating cash flow

42

(25)

-

-

Exceptional items

- KAPCO dividend

- Hazelwood refinancing

Year ended 31 December

252

(108)

(48)

391

115

276

2002

121 Free cash flow

(100)Interest and tax

(64)Capex - maintenance

285 Operating cash flow

101 Dividends – JV’s, associates and investments

184 Operating cash flow from subsidiaries

2003 £m

Group net cash flow

Year ended 31 December

(812)

(897)

85

75

-

(144)

-

(98)

252

2002

- Acquisitions and greenfield developments

(692)Closing external debt

(812)Opening external debt

120 Net cash flow

(35)Other (FX and share buy-back)

35 Disposal of investments

56 LD buy-downs

(57)Capex – growth

121 Free cash flow

2003£m

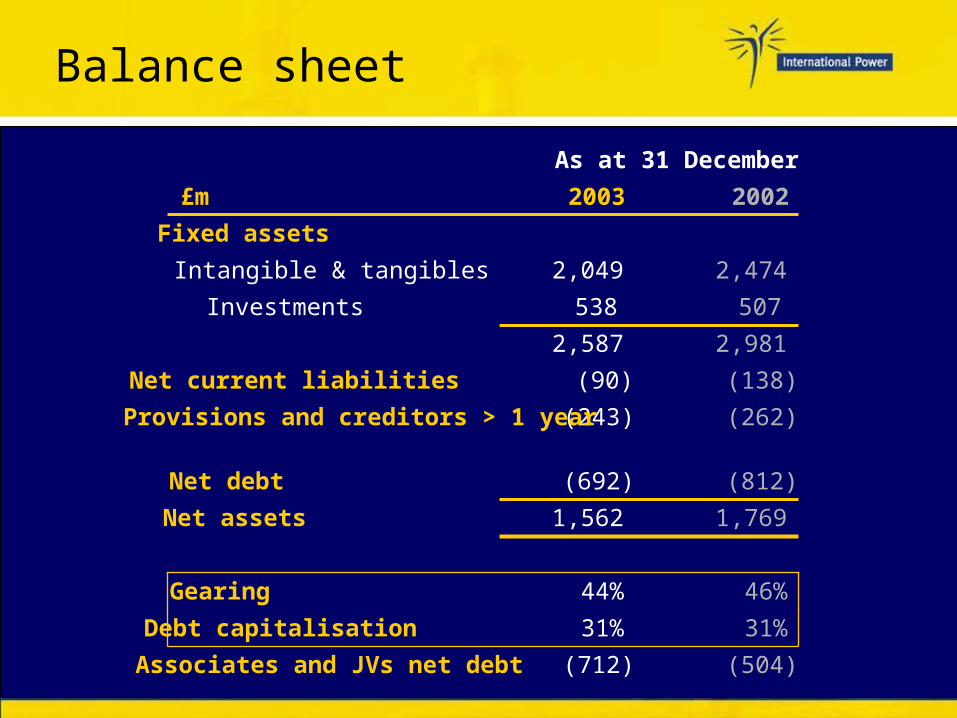

Balance sheet

31%31%Debt capitalisation

(504)(712)Associates and JVs net debt

As at 31 December

2,981 2,587

1,769 1,562 Net assets

2,474 2,049 Intangible & tangibles

507 538 Investments

46%44%Gearing

(812)(692)Net debt

(262)(243)Provisions and creditors > 1 year

(138)(90)Net current liabilities

Fixed assets

20022003£m

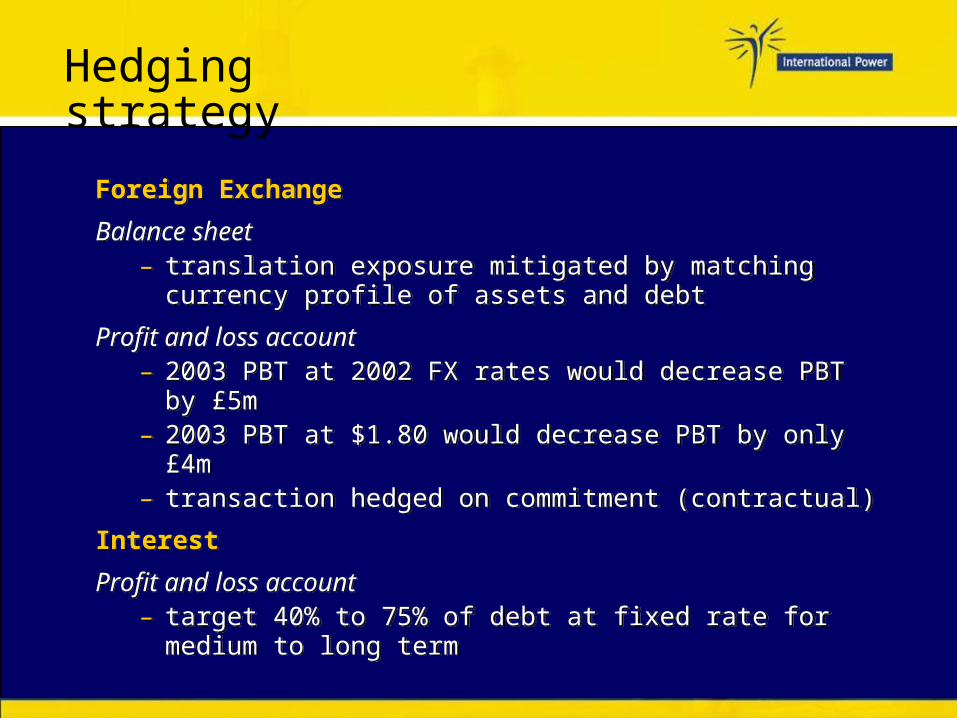

Hedging strategy

Foreign Exchange

Balance sheet– translation exposure mitigated by matching

currency profile of assets and debt

Profit and loss account– 2003 PBT at 2002 FX rates would decrease PBT by

£5m– 2003 PBT at $1.80 would decrease PBT by only £4m– transaction hedged on commitment (contractual)

Interest

Profit and loss account– target 40% to 75% of debt at fixed rate for medium

to long term

Foreign Exchange

Balance sheet– translation exposure mitigated by matching

currency profile of assets and debt

Profit and loss account– 2003 PBT at 2002 FX rates would decrease PBT by

£5m– 2003 PBT at $1.80 would decrease PBT by only £4m– transaction hedged on commitment (contractual)

Interest

Profit and loss account– target 40% to 75% of debt at fixed rate for medium

to long term

Financing accomplishments

US$1.8 billion Umm Al Nar financing

Issue of US$ 252 million senior convertible bonds

Rugeley restructuring

New US$450 million corporate revolver put in place

US$510 million, 17 year term Saudi Aramco financing

US$1.8 billion Umm Al Nar financing

Issue of US$ 252 million senior convertible bonds

Rugeley restructuring

New US$450 million corporate revolver put in place

US$510 million, 17 year term Saudi Aramco financing

SeptemberSeptember

JulyJuly

OctoberOctober

FebruaryFebruary

20032003

20042004

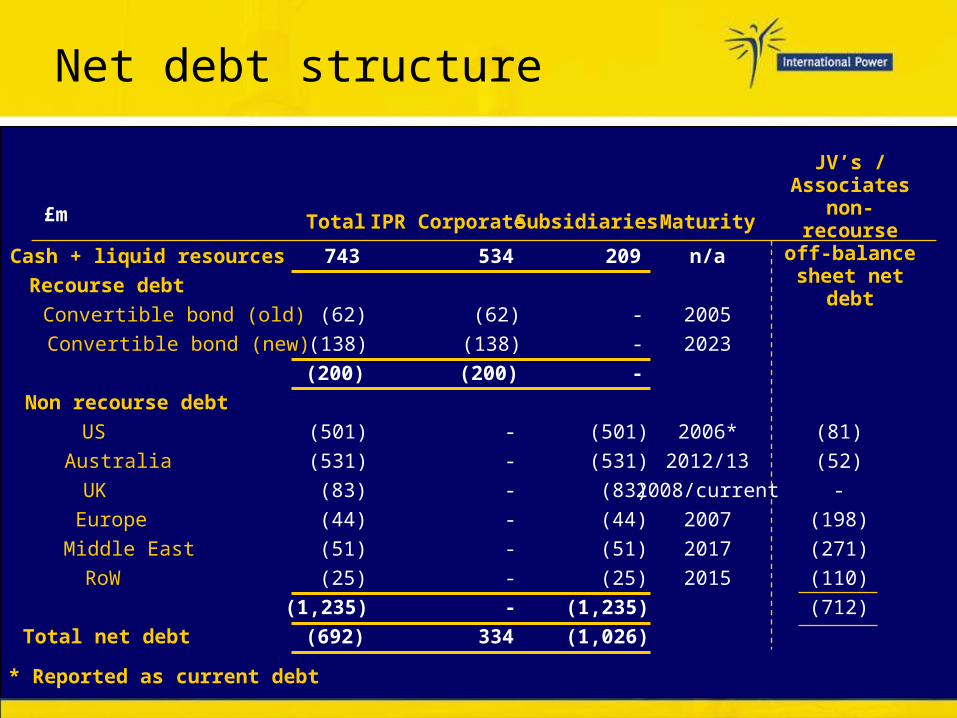

Net debt structure

(1,026)334(692)Total net debt

2015

2017

2007

2008/current

2012/13

2006*

2023

2005

n/a

Maturity

(712)

(110)

(271)

(198)

-

(52)

(81)

JV’s / Associates

non-recourse

off-balance sheet net

debt

(1,235)

(25)

(51)

(44)

(83)

(531)

(501)

-

-

-

209

Subsidiaries

-(1,235)

(25)

(51)

(44)

(83)

(531)

(501)

(200)

(138)

(62)

743

Total

- Europe

- Middle East

- RoW

(200)

-

-

-

(138)

(62)

534

IPR Corporate

Australia

UK

* Reported as current debt

US

Non recourse debt

Convertible bond (new)

Convertible bond (old)

Recourse debt

Cash + liquid resources

£m

In summary:

Low spark spreads in the US

US assets written down

Europe performed well

Highly contracted in all other regions

Cash flow positive

Strong corporate liquidity

Low spark spreads in the US

US assets written down

Europe performed well

Highly contracted in all other regions

Cash flow positive

Strong corporate liquidity

44

Philip CoxChief Executive Officer

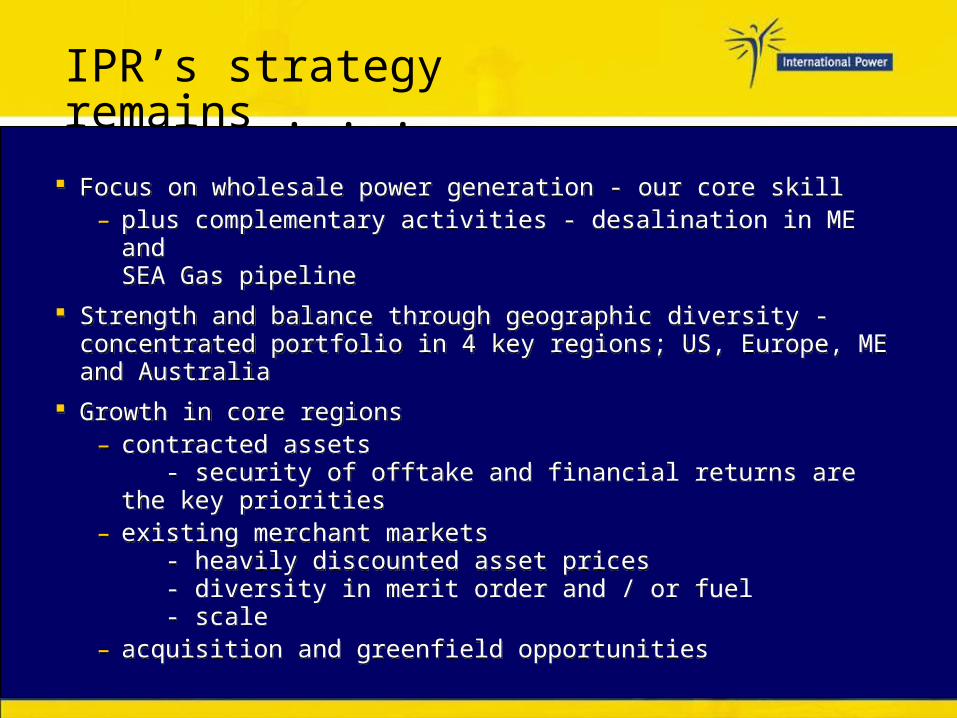

IPR’s strategy remains . . .

Focus on wholesale power generation - our core skill– plus complementary activities - desalination in ME and

SEA Gas pipeline

Strength and balance through geographic diversity - concentrated portfolio in 4 key regions; US, Europe, ME and Australia

Growth in core regions– contracted assets

- security of offtake and financial returns are the key priorities

– existing merchant markets - heavily discounted asset prices - diversity in merit order and / or fuel - scale

– acquisition and greenfield opportunities

Focus on wholesale power generation - our core skill– plus complementary activities - desalination in ME and

SEA Gas pipeline

Strength and balance through geographic diversity - concentrated portfolio in 4 key regions; US, Europe, ME and Australia

Growth in core regions– contracted assets

- security of offtake and financial returns are the key priorities

– existing merchant markets - heavily discounted asset prices - diversity in merit order and / or fuel - scale

– acquisition and greenfield opportunities

Outlook

Clear strategy

US restructuring number 1 priority

Growth opportunities in our core regions

Confirm 2004 earnings guidance of 7 - 9p EPS

Clear strategy

US restructuring number 1 priority

Growth opportunities in our core regions

Confirm 2004 earnings guidance of 7 - 9p EPS

47

Preliminary ResultsYear to 31 December 2003