1 OPEN INVESTMENT and the Committee on Foreign Investment in the United State (CFIUS)

20

1 OPEN INVESTMENT and the Committee on Foreign Investment in the United State (CFIUS)

-

Upload

john-heath -

Category

Documents

-

view

214 -

download

0

Transcript of 1 OPEN INVESTMENT and the Committee on Foreign Investment in the United State (CFIUS)

1

OPEN INVESTMENT and the

Committee on Foreign Investment

in the United State (CFIUS)

2

Foreign Direct Investment

In the United States

3

“The United States unequivocally supports international investment in this country and is equally committed to securing fair, equitable, and nondiscriminatory treatment for U.S. investors abroad …”

- President George W. Bush May 10, 2007

The United States is a Staunch Supporter of Open Investment

Foreign Direct Investment into the United States:

• Equals 15% of U.S. GDP ($1.9 trillion stock in 2005)

• Employs 4.5% of U.S. private sector (5.1 million in 2005)

- provides for 4.6 million additional U.S. jobs indirectly

• Pays 30% higher compensation than the U.S. average

• Generates 13% of R&D spending ($30 billion)

• Accounts for 19% of U.S. exports ($153.9 billion)

4

• Non-discrimination: Committed to national treatment and most-favored-nation treatment across nearly the entire economy

• Transparency: Administrative Procedures Act provides for notice & comment on proposed regulations and publication of final regulations

• Administrative-judicial process: Efficient, predictable, and transparent

FDI in the U.S.: Committed to a Level Playing Field

5

• Energy: Prohibition on licenses for nuclear energy enrichment operations

• Communications: 25% foreign equity cap for broadcast, common carrier, and radio licenses

• Air Carriers: 25% foreign equity cap• Maritime Transport: No majority share in US vessels;

25% foreign equity cap for coastal shipping companies

FDI in the U.S.: Key Legal Prohibitions

Also: Several exceptions to U.S. WTO commitments for state-level measures, but these apply only to purely intra-state commerce

Exceptions to U.S. nondiscriminatory treatment of FDI are few, transparently disclosed, and generally cannot be expanded, per our trade commitments:

6

• Doing business: Both foreign-owned & domestic businesses are subject to nondiscriminatory federal regulations, depending on their activities/sector

• Key regulatory clearances that are relevant to FDI transactions:

– Antitrust: DOJ and FTC conduct 30-day reviews of large mergers

– Securities: SEC requires disclosure of information about registered debt and equity, as well as about public companies and their sale

– Defense: DOD issues facility & security clearances and, clears foreign acquisitions of US firms with classified contracts

– Cross-border flows: Commerce & State regulate dual-use and military-use exports, and DHS regulates imports and immigration visas

– Communications: FCC approves telecom mergers and licenses

– Financial: Federal Reserve, OCC, SEC issue bank/brokerage licenses and review mergers; impose non-discriminatory prudential regulations

– Other sectoral clearances: Depending on the sector, other agencies may require licenses or clearance, including DOT, DOE, FERC, etc.

FDI in the U.S.: Non-Discriminatory Business Regulations

7

U.S. Government Roles in

Investment Policy

8

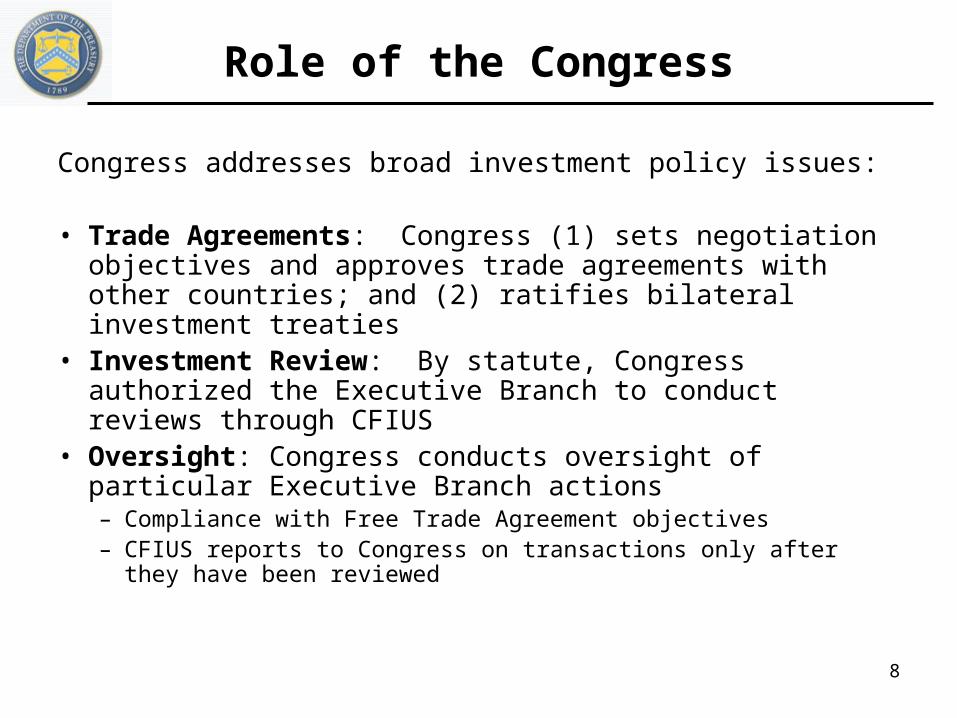

Role of the Congress

Congress addresses broad investment policy issues:

• Trade Agreements: Congress (1) sets negotiation objectives and approves trade agreements with other countries; and (2) ratifies bilateral investment treaties

• Investment Review: By statute, Congress authorized the Executive Branch to conduct reviews through CFIUS

• Oversight: Congress conducts oversight of particular Executive Branch actions– Compliance with Free Trade Agreement objectives– CFIUS reports to Congress on transactions only after they have

been reviewed

9

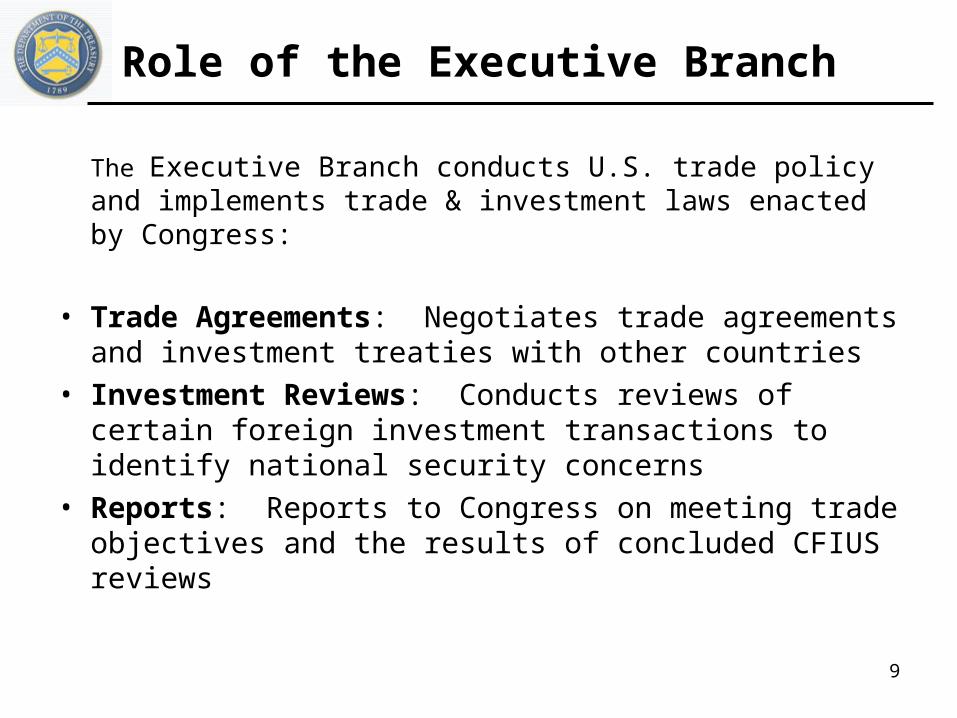

Role of the Executive Branch

The Executive Branch conducts U.S. trade policy and implements trade & investment laws enacted by Congress:

• Trade Agreements: Negotiates trade agreements and investment treaties with other countries

• Investment Reviews: Conducts reviews of certain foreign investment transactions to identify national security concerns

• Reports: Reports to Congress on meeting trade objectives and the results of concluded CFIUS reviews

10

Committee on Foreign Investment

in the United States (CFIUS)

11

CFIUS: Purpose

• Review of foreign acquisitions of U.S. businesses, to resolve any national security risks– Limited to acquisitions that result in foreign control– Does not consider U.S. national economic interests

• President alone has power to prohibit transactions– CFIUS may recommend that President prohibit– President has prohibited only one transaction (in 1990)

• Foreign Investment & National Security Act of 2007 (FINSA)– Signed into law July 26; becomes effective October 24– Amends 1988 Exon-Florio legislation under which CFIUS operates– Maintains CFIUS’ fundamental open-investment characteristics

12

CFIUS: Membership

* New member per FINSA

Eight Executive Departments

– Treasury Department (chair)

– State Department

– Commerce Department

– Defense Department

– Justice Department

– Homeland Security Department

– * Energy Department

– * Labor Department (ex-officio)

Seven White House Agencies

– U.S. Trade Representative

– Office of Science & Technology

– Office of Management & Budget

– Council of Economic Advisors

– National Economic Council

– National Security Council

– * DNI (ex-officio)

13

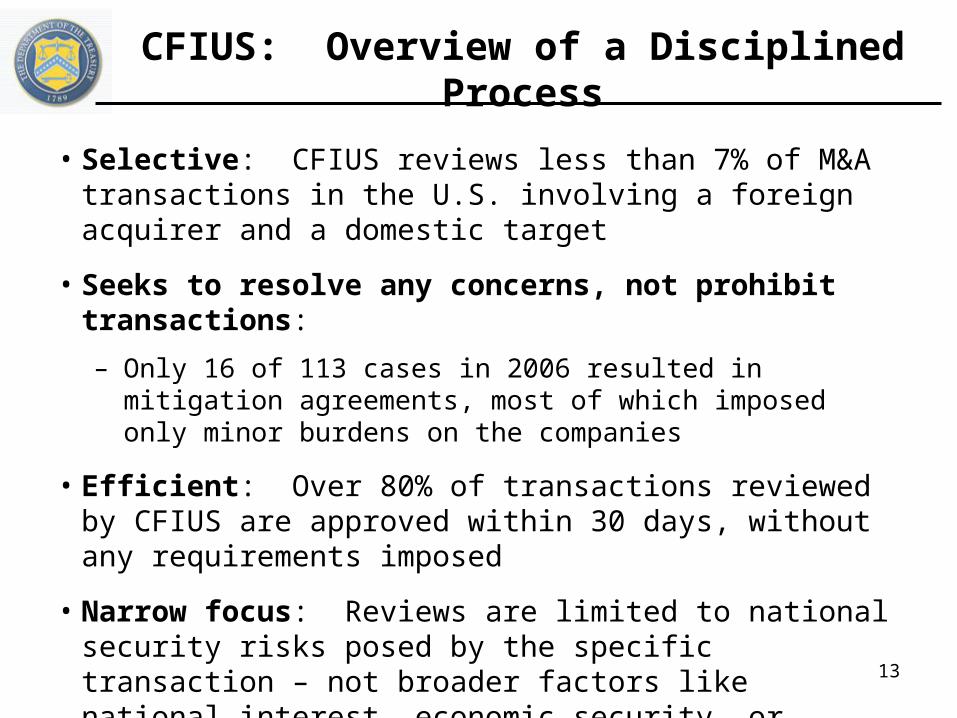

CFIUS: Overview of a Disciplined Process

• Selective: CFIUS reviews less than 7% of M&A transactions in the U.S. involving a foreign acquirer and a domestic target

• Seeks to resolve any concerns, not prohibit transactions:

– Only 16 of 113 cases in 2006 resulted in mitigation agreements, most of which imposed only minor burdens on the companies

• Efficient: Over 80% of transactions reviewed by CFIUS are approved within 30 days, without any requirements imposed

• Narrow focus: Reviews are limited to national security risks posed by the specific transaction – not broader factors like national interest, economic security, or industrial policy

14

CFIUS: Reviews Only Select Transactions

Comparison: Number of Global, U.S. & CFIUS-Reviewed M&A Transactions

Source: Thomson Financial

Date Global M&A U.S. M&AU.S. FDI

M&A CFIUS-Reviewed M&A

Cases % of FDI M&A

2000 38,716 11,137 1,747 72 4.1%

2001 30,174 7,702 1,131 55 4.8%

2002 26,482 7,042 855 43 5.0%

2003 28,830 7,728 900 41 4.5%

2004 31,484 8,547 1,018 53 5.2%

2005 33,570 9,235 1,123 65 5.8%

2006 37,095 10,460 1,730 113 6.5%

15

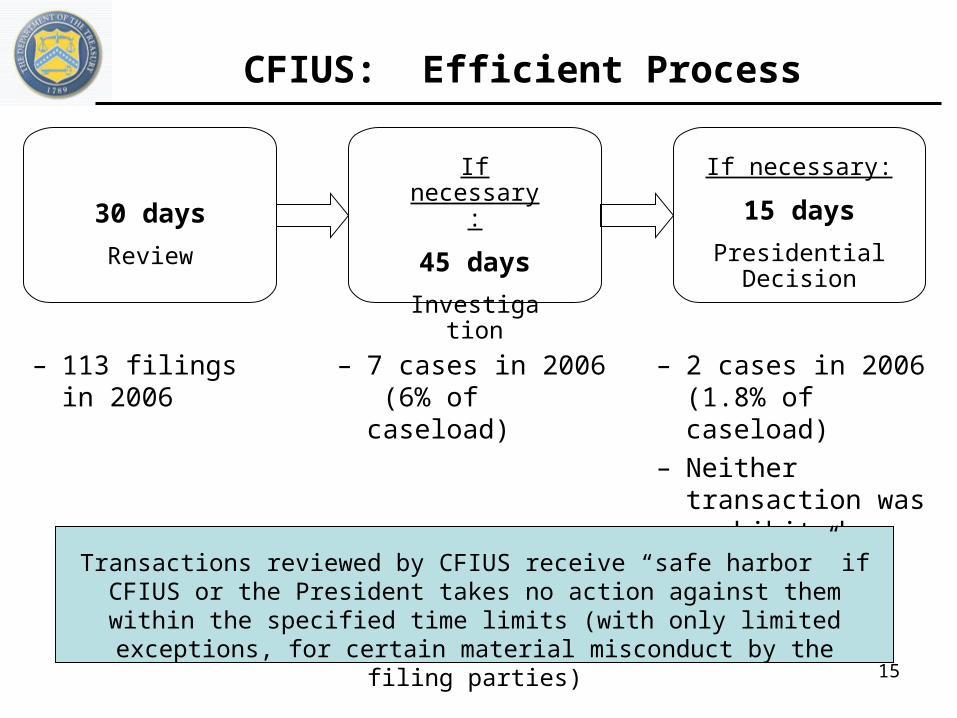

CFIUS: Efficient Process

– 113 filings in 2006

30 days

Review

If necessary:

45 days

Investigation

If necessary:

15 days

Presidential Decision

– 7 cases in 2006 (6% of caseload)

– 2 cases in 2006 (1.8% of caseload)

– Neither transaction was prohibited

Transactions reviewed by CFIUS receive “safe harbor” if CFIUS or the President takes no action against them within the specified time limits (with only limited exceptions, for certain material misconduct by the filing parties)

16

• CFIUS considers only transaction-specific effects on national security, not broader national security policy or other priorities

• 1988 law enumerates several national security factors

• FINSA enumerates additional national security factors that CFIUS already considers when relevant:

CFIUS: Narrow Focus on National Security

1988 Exon Florio statute:– Domestic production and

capability for projected defense needs

– Capability of U.S. to meet national security needs

– Sale/diversion of military technology to certain countries

– U.S. technology leadership in areas affecting national security

FINSA adds:– Security-related impact on

critical infrastructure/technology– Greater emphasis on foreign-

government control– Whether acquisition by SOE

poses risk, given state’s record on nonproliferation, counter-terrorism, technology diversion

– Impact on long-term energy/ critical resources needs

17

FINSA: Improves CFIUS Process While Maintaining its Open Investment Orientation

• Maintains CFIUS’ fundamental open-investment orientation – Maintains very selective focus on cases that raise genuine national security

issues (with no mandatory filing)– Formalizes current practice of seeking to resolve concerns, rather than

prohibit transactions– Maintains current strict deadlines for CFIUS and Presidential action

• Reaffirms Congressional trust in CFIUS– No reporting to Congress is required until after a case is concluded

• And Congress is subject to confidentiality laws– Significant post-decisional and annual reports to Congress

• Improves high-level accountability– Deputy Secretary must sign off on closure of any second-stage

investigation, all cases involving foreign government control, and certain cases involving critical infrastructure

– Assistant Secretary must sign off on closure of all other cases– Treasury Department and any lead agency it appoints for a case have

formal accountability to Congress

18

FINSA: Key Dates

• July 26, 2007:

• October 23, 2007:

• October 24, 2007:

• April 22, 2008:

• April 22, 2008:

President signs FINSA into law

Treasury hosts public meeting to seek comments on CFIUS process

FINSA becomes effective

Final regulations must be published

Guidance must be published on the types of cases that have raised national security considerations

19

CFIUS: Foreign Government Control

• Foreign government control requires higher-level accountability– 1988 law and FINSA both require 2nd-stage investigation of such

cases unless CFIUS affirmatively determines there are no national security concerns

– FINSA requires Deputy Secretary to close out such cases, whereas Assistant Secretary closes out other cases

• CFIUS clears vast majority of foreign government-control cases– 157 transactions reviewed since 1992 (14% of CFIUS caseload)– 20 included mitigation agreements (13%)– 11 proceeded to investigation (7%)

20

CFIUS: Companies’ Best Practices

• Prefiling: Providing information to CFIUS before filing a formal notice, to ensure that the notice is complete

• Stakeholder briefing: Increasingly discussing potentially controversial transactions with Congress

• Business purpose: Demonstrating that the transaction is driven by a commercial rationale

• Problem-solving mentality: Seeking to address national security concerns proactively