1 Novo Nordisk A focused global healthcare company with biotech expertise Investor Presentation...

51

1 Novo Nordisk Novo Nordisk A focused global healthcare company A focused global healthcare company with biotech expertise with biotech expertise Investor Presentation Investor Presentation August 2001 August 2001

-

date post

22-Dec-2015 -

Category

Documents

-

view

221 -

download

6

Transcript of 1 Novo Nordisk A focused global healthcare company with biotech expertise Investor Presentation...

1

Novo NordiskNovo Nordisk

A focused global healthcare company A focused global healthcare company with biotech expertisewith biotech expertise

Investor PresentationInvestor Presentation

August 2001August 2001

2

Novo Nordisk todayNovo Nordisk today

Consistent, strong organic growthConsistent, strong organic growth

Focused on few therapeutic areas with large unmet Focused on few therapeutic areas with large unmet medical needsmedical needs

Leadership in diabetes and most extensive diabetes Leadership in diabetes and most extensive diabetes pipeline in the industrypipeline in the industry

Becoming an established player in general haemostasis Becoming an established player in general haemostasis managementmanagement

Proven biotech and drug delivery capabilitiesProven biotech and drug delivery capabilities

Strong intellectual property portfolioStrong intellectual property portfolio

Low exposure to patent expirationsLow exposure to patent expirations

Track record of delivering on promisesTrack record of delivering on promises

3

HRTHRTHuman growth Human growth hormonehormone

Intellectual Intellectual propertyproperty

Diabetes careDiabetes care Coagulation Coagulation disordersdisorders

PrimaryPrimarygrowth growth driversdrivers

Secondary value

drivers

Novo Nordisk – Future Key DriversNovo Nordisk – Future Key Drivers

4

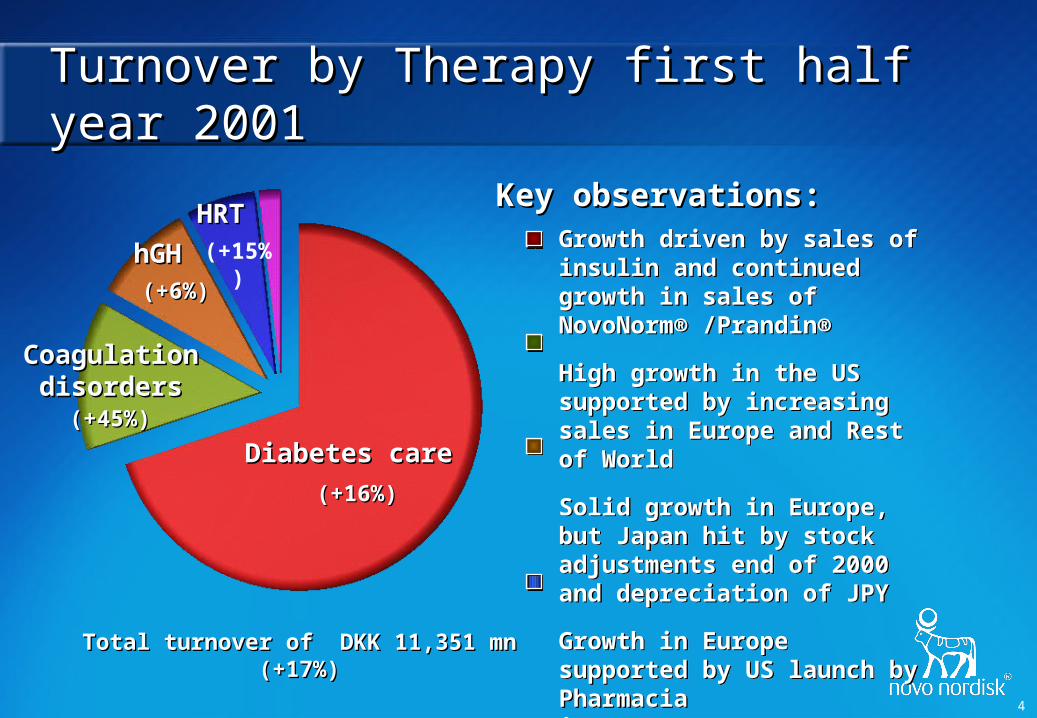

Turnover by Therapy first half year 2001Turnover by Therapy first half year 2001

Growth driven by sales of insulin and continued growth in sales of NovoNorm® /Prandin®

High growth in the US supported by increasing sales in Europe and Rest of World

Solid growth in Europe, but Japan hit by stock adjustments end of 2000 and depreciation of JPY

Growth in Europe supported by US launch by Pharmacia in Q2/Q3 2000

Growth driven by sales of insulin and continued growth in sales of NovoNorm® /Prandin®

High growth in the US supported by increasing sales in Europe and Rest of World

Solid growth in Europe, but Japan hit by stock adjustments end of 2000 and depreciation of JPY

Growth in Europe supported by US launch by Pharmacia in Q2/Q3 2000

Diabetes careDiabetes care

(+16%)(+16%)

CoagulationCoagulationdisordersdisorders

(+45%)(+45%)

(+6%)(+6%)

hGHhGH

HRTHRT(+15%)

Key observations:Key observations:

Total turnover of DKK 11,351 mn (+17%)Total turnover of DKK 11,351 mn (+17%)

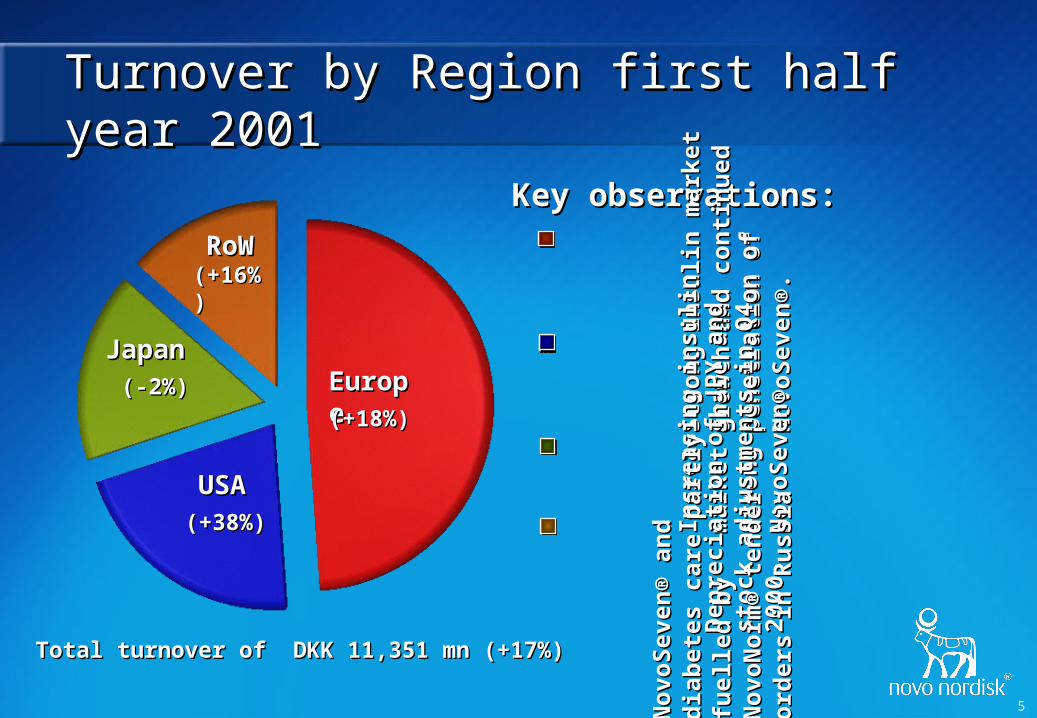

5

Key observations:Key observations:

Turnover by Region first half year 2001Turnover by Region first half year 2001

Str

on

g i

nsu

lin

mar

ket

gro

wth

S

tro

ng

in

suli

n m

arke

t g

row

th

and

co

nti

nu

ed p

enet

rati

on

of

and

co

nti

nu

ed p

enet

rati

on

of

No

voS

even

No

voS

even

®®. .

Incr

easi

ng

in

suli

n m

arke

t In

crea

sin

g i

nsu

lin

mar

ket

shar

e an

d s

tro

ng

sh

are

and

str

on

g

pen

etra

tio

n o

f N

ovo

Sev

enp

enet

rati

on

of

No

voS

even

®®

Dep

reci

atio

n o

f JP

Y a

nd

sto

ck

Dep

reci

atio

n o

f JP

Y a

nd

sto

ck

adju

stm

ents

in

Q4

2000

adju

stm

ents

in

Q4

2000

No

voS

even

No

voS

even

® a

nd

dia

bet

es

® a

nd

dia

bet

es

care

par

tly

fuel

led

by

care

par

tly

fuel

led

by

No

voN

orm

No

voN

orm

®® t

end

er

ten

der

o

rder

s in

Ru

ssia

ord

ers

in R

uss

ia

EuropeEurope(+18%)(+18%)

RoWRoW(+16%)(+16%)

USAUSA(+38%)(+38%)

JapanJapan(-2%)(-2%)

Total turnover of DKK 11,351 mn (+17%)Total turnover of DKK 11,351 mn (+17%)

6

HRTHRTHuman growth Human growth hormonehormone

Intellectual Intellectual propertyproperty

Diabetes careDiabetes care Coagulation Coagulation disordersdisorders

PrimaryPrimarygrowth growth driversdrivers

Secondary value

drivers

Novo Nordisk – Future Key DriversNovo Nordisk – Future Key Drivers

Diabetes careDiabetes care

7

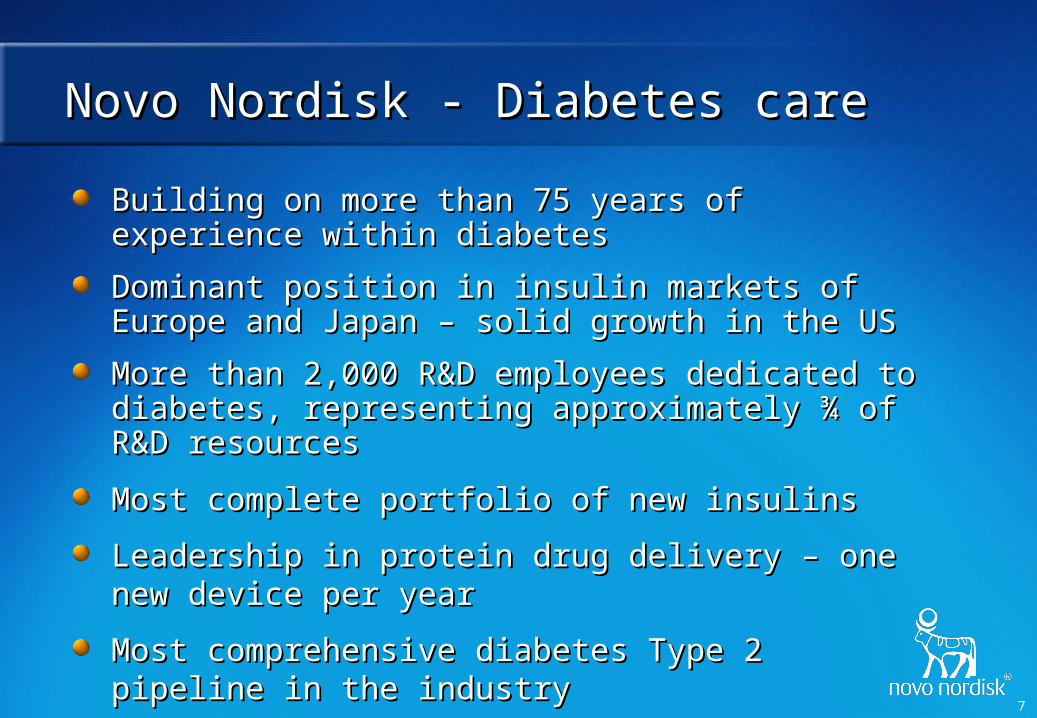

Novo Nordisk - Diabetes careNovo Nordisk - Diabetes care

Building on more than 75 years of experience within Building on more than 75 years of experience within diabetesdiabetes

Dominant position in insulin markets of Europe and Dominant position in insulin markets of Europe and Japan – solid growth in the USJapan – solid growth in the US

More than 2,000 R&D employees dedicated to diabetes, More than 2,000 R&D employees dedicated to diabetes, representing approximately ¾ of R&D resourcesrepresenting approximately ¾ of R&D resources

Most complete portfolio of new insulinsMost complete portfolio of new insulins

Leadership in protein drug delivery – one new device per Leadership in protein drug delivery – one new device per yearyear

Most comprehensive diabetes Type 2 pipeline in the Most comprehensive diabetes Type 2 pipeline in the industryindustry

8

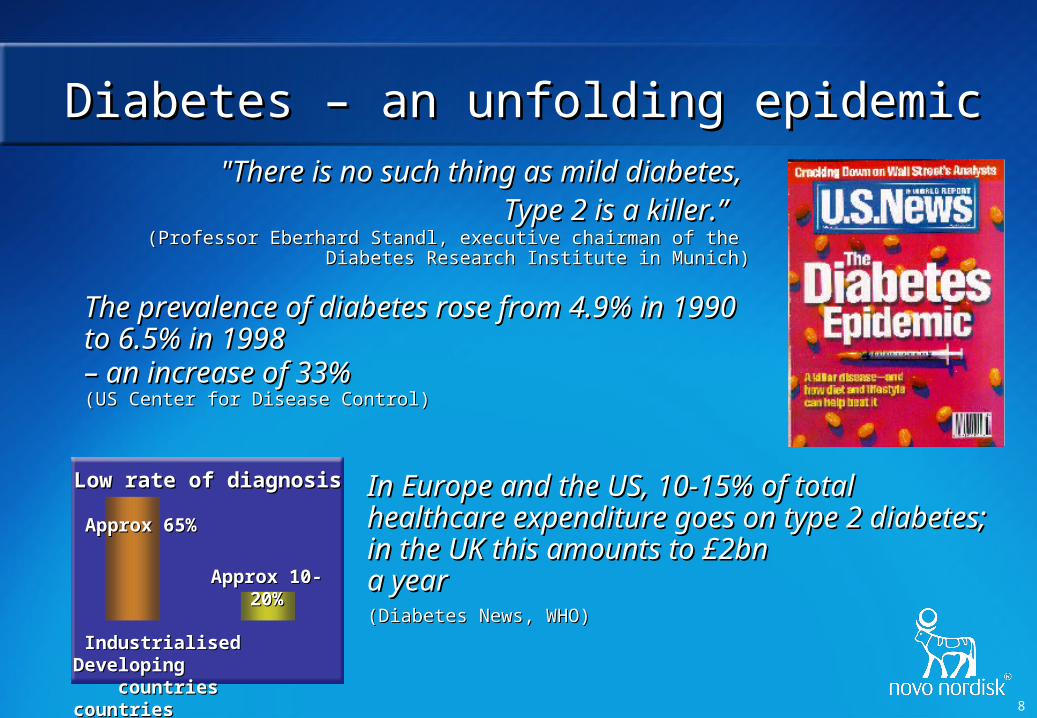

Diabetes – an unfolding epidemicDiabetes – an unfolding epidemic

Industrialised Developing Industrialised Developing countries countriescountries countries

Low rate of diagnosisLow rate of diagnosis

Approx 65%Approx 65%

Approx 10-20%Approx 10-20%

"There is no such thing as mild diabetes, "There is no such thing as mild diabetes, Type 2 is a killer.”Type 2 is a killer.”

(Professor Eberhard Standl, executive chairman of the (Professor Eberhard Standl, executive chairman of the Diabetes Research Institute in Munich)Diabetes Research Institute in Munich)

The prevalence of diabetes rose from 4.9% in 1990 The prevalence of diabetes rose from 4.9% in 1990 to 6.5% in 1998 to 6.5% in 1998 – an increase of 33%– an increase of 33% (US Center for Disease Control)(US Center for Disease Control)

In Europe and the US, 10-15% of total In Europe and the US, 10-15% of total healthcare expenditure goes on type 2 healthcare expenditure goes on type 2 diabetes; in the UK this amounts to £2bn diabetes; in the UK this amounts to £2bn a year a year (Diabetes News, WHO)(Diabetes News, WHO)

9

Towards more intensive/flexible treatmentTowards more intensive/flexible treatment

Short-acting market growth: Short-acting market growth: 11.5% CAGR since 199611.5% CAGR since 1996

Premixed market growth: Premixed market growth: 9.3% CAGR since 19969.3% CAGR since 1996

Long-acting market growth: Long-acting market growth: 0.4% CAGR since 19960.4% CAGR since 1996

Note: Note: All figures are based on MAT Q1 volumes, industrialised world only. All figures are based on MAT Q1 volumes, industrialised world only.

Novo NordiskNovo Nordiskmarket share 2001market share 2001

00

2020

4040

6060

8080

100100

120120

140140

160160

180180

19961996 19971997 19981998 19991999 20002000 20012001

Meg

a Un

its in 1,000

Meg

a Un

its in 1,000

Insulin market volumeInsulin market volume

25% 39%

36%25%

39% 36%

19%19%

33% 47%

33% 47%

+6%+6%+8%+8%

+8%+8%+3%+3%+5%+5%

39%39%

52%52%

41%41%

Long-actingLong-acting

PremixedPremixed

Short-acting Short-acting

10

6.2%6.2%

4.0%4.0%

9.1%9.1%

11.8%11.8%

0.8%0.8%

World World

RoW RoW

Japan Japan

Europe Europe

USA USA

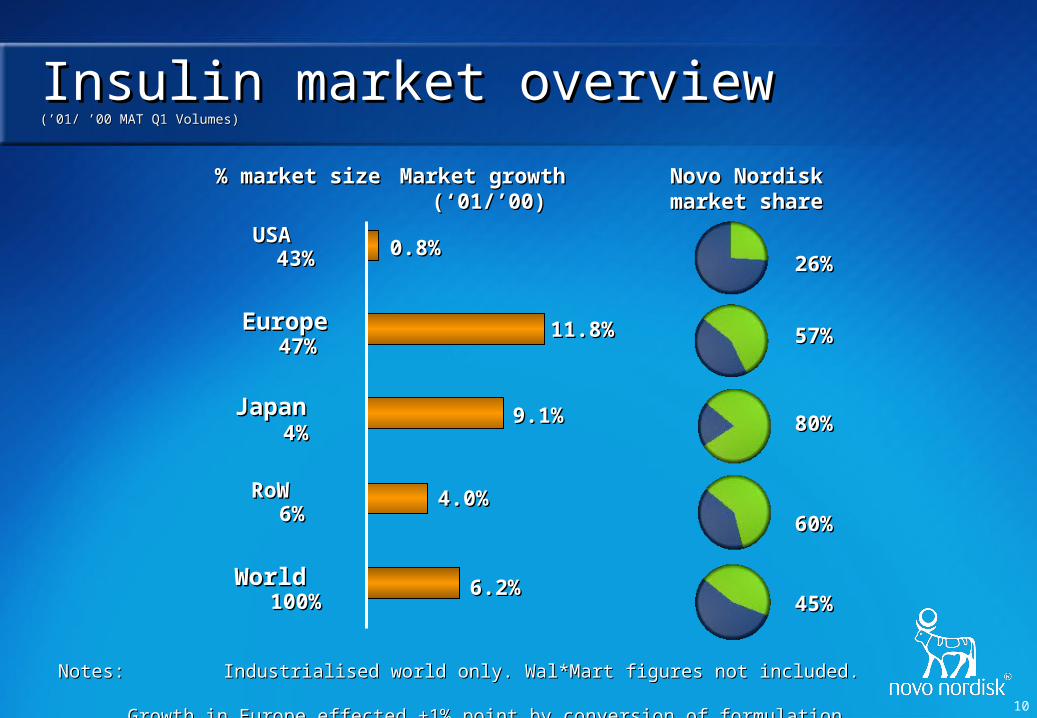

Insulin market overviewInsulin market overview(’01/ ’00 MAT Q1 Volumes)(’01/ ’00 MAT Q1 Volumes)

Novo NordiskNovo Nordiskmarket sharemarket share

Market growth Market growth (‘(‘001/’00)1/’00)

4343%%

4747%%

4%4%

66%%

% market size % market size

100%100%

Notes: Notes: Industrialised world only. Wal*Mart figures not included. Industrialised world only. Wal*Mart figures not included. Growth in Europe effected +1% point by conversion of formulation. Growth in Europe effected +1% point by conversion of formulation.

26%26%

57%57%

80%80%

60%60%

45%45%

11

Upgrading the insulin marketUpgrading the insulin market

De

vic

e p

en

etr

atio

nD

ev

ice

pe

ne

trat

ion

Insu

lin a

nal

og

ue

Insu

lin a

nal

og

ue

pe

ne

tra

tio

np

en

etr

ati

on

100%

100%

100%

100%

0%0%

(+50

% p

rem

ium

)(+

50%

pre

miu

m)

(+30

% p

rem

ium

)(+

30%

pre

miu

m)

Increasing turnover Increasing turnover per patientper patient

US

A

Jap

anE

uro

pe

12

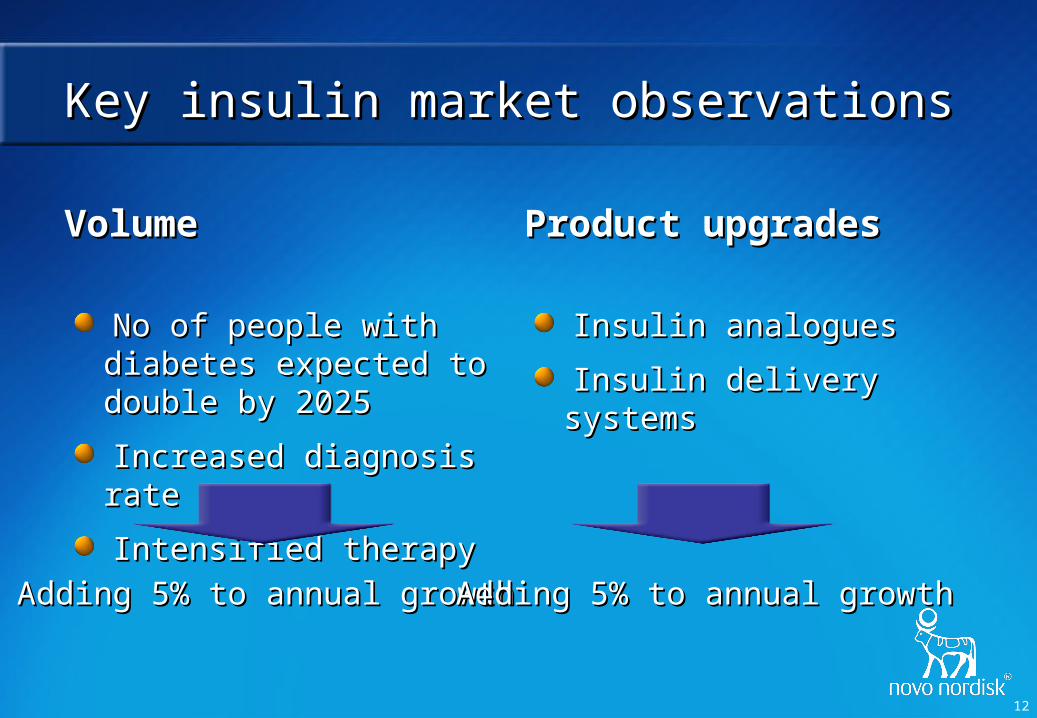

Key insulin market observationsKey insulin market observations

VolumeVolume

No of people with diabetes No of people with diabetes expected to double by 2025expected to double by 2025

Increased diagnosis rateIncreased diagnosis rate

Intensified therapyIntensified therapy

Product upgradesProduct upgrades

Insulin analoguesInsulin analogues

Insulin delivery systemsInsulin delivery systems

Adding 5% to annual growthAdding 5% to annual growth Adding 5% to annual growthAdding 5% to annual growth++

13

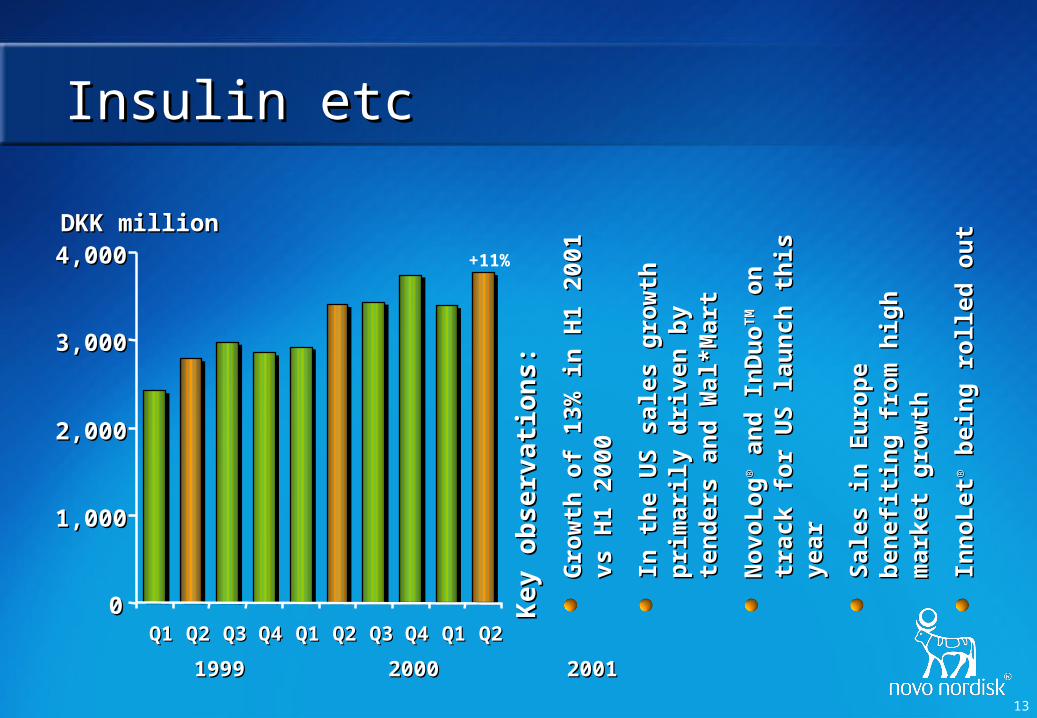

Insulin etcInsulin etc

Ke

y o

bs

erva

tio

ns

:K

ey

ob

ser

vati

on

s:

Gro

wth

of

13%

in

H1

2001

vs

Gro

wth

of

13%

in

H1

2001

vs

H1

2000

H1

2000

In t

he

US

sal

es g

row

th

In t

he

US

sal

es g

row

th

pri

mar

ily

dri

ven

by

ten

der

s p

rim

aril

y d

rive

n b

y te

nd

ers

and

Wal

*Mar

tan

d W

al*M

art

No

voL

og

No

voL

og

®® a

nd

In

Du

o a

nd

In

Du

oT

MT

M o

n

on

tr

ack

for

US

lau

nch

th

is y

ear

trac

k fo

r U

S l

aun

ch t

his

yea

r

Sal

es i

n E

uro

pe

ben

efit

ing

S

ales

in

Eu

rop

e b

enef

itin

g

fro

m h

igh

mar

ket

gro

wth

fr

om

hig

h m

arke

t g

row

th

Inn

oL

etIn

no

Let

®® b

ein

g r

oll

ed o

ut

bei

ng

ro

lled

ou

t

00

1,0001,000

2,0002,000

3,0003,000

4,0004,000

Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2

DKK millionDKK million

19991999 2000 2001 2000 2001

+11%

14

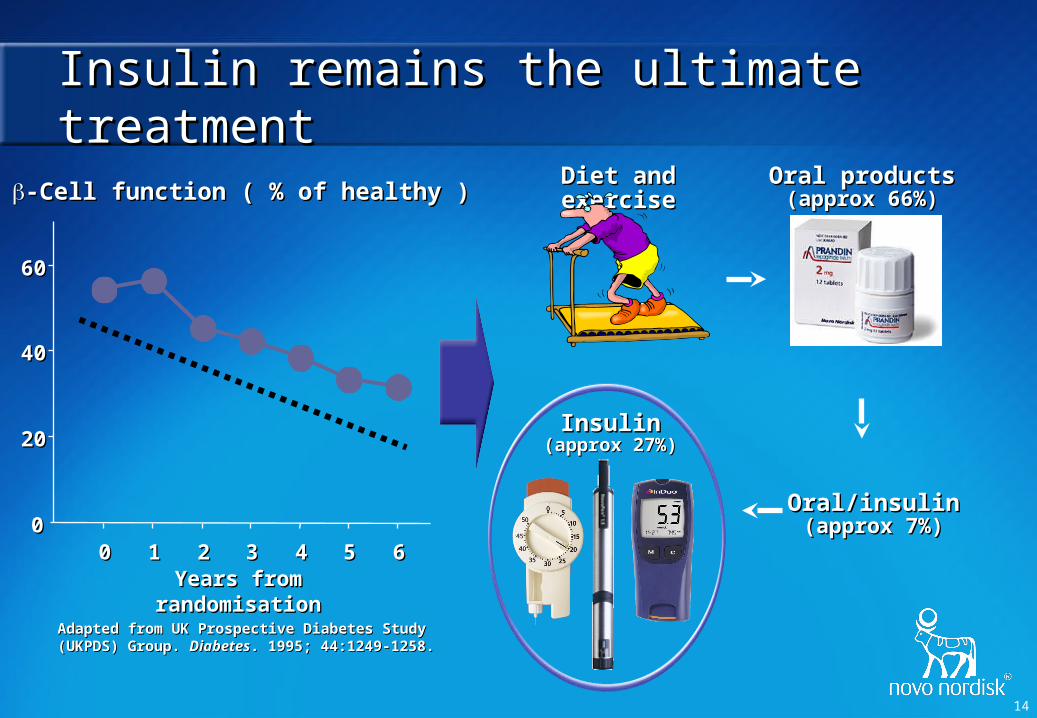

Insulin remains the ultimate treatmentInsulin remains the ultimate treatment

00

2020

4040

6060

00 11 22 33 44 55 66Years from randomisationYears from randomisation

Adapted from UK Prospective Diabetes Study (UKPDS) Adapted from UK Prospective Diabetes Study (UKPDS) Group. Group. DiabetesDiabetes. 1995; 44:1249-1258.. 1995; 44:1249-1258.

-Cell function ( % of healthy ) -Cell function ( % of healthy ) Diet and exerciseDiet and exercise Oral productsOral products

(approx 66%)(approx 66%)

Oral/insulinOral/insulin(approx 7%)(approx 7%)

InsulinInsulin(approx 27%)(approx 27%)

15

NovoNormNovoNorm®® /Prandin /Prandin®®

Ke

y o

bs

erva

tio

ns

:K

ey

ob

ser

vati

on

s:

Gro

wth

of

50%

in

H1

2001

G

row

th o

f 50

% i

n H

1 20

01

vs H

1 20

00vs

H1

2000

In E

uro

pe

No

voN

orm

In

Eu

rop

e N

ovo

No

rm ®®

co

nti

nu

ed t

o p

enet

rate

co

nti

nu

ed t

o p

enet

rate

n

icel

yn

icel

y

Fir

st h

alf

2001

eff

ecte

d b

y F

irst

hal

f 20

01 e

ffec

ted

by

ten

der

ord

ers

in R

uss

ia a

nd

te

nd

er o

rder

s in

Ru

ssia

an

d

sto

ck p

ilin

g i

n t

he

US

sto

ck p

ilin

g i

n t

he

US

Fir

st m

ove

in

to O

ral

An

ti

Fir

st m

ove

in

to O

ral

An

ti

Dia

bet

ics

(OA

D)

Dia

bet

ics

(OA

D)

DKK millionDKK million

19991999 2000 2001 2000 2001

00

100100

200200

300300

400400

500500

Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2

+49%

16

00

5050

100100

150150

200200

250250

300300

350350

19961996 19971997 19981998 19991999 20002000 20012001

MA

TQ

1.19

96=

100

MA

TQ

1.19

96=

100

Growth opportunities in OADGrowth opportunities in OAD

Sales development in USDSales development in USDCAGR: 26%CAGR: 26%

No of treated patientsNo of treated patients CAGR: 13%CAGR: 13%

Growth in USD 5.8 bn OAD marketGrowth in USD 5.8 bn OAD marketKey observations Novo NordiskKey observations Novo Nordisk

Experience in the OAD Experience in the OAD market from market from NovoNormNovoNorm®® /Prandin /Prandin®®

Novartis partner on Novartis partner on NN622 for North NN622 for North AmericaAmerica

Broad pipeline of Broad pipeline of innovative approaches innovative approaches for Type 2 diabetesfor Type 2 diabetes

17

Diabetes pipelineDiabetes pipeline

NN2211NN2211 (GLP-1 analogue)(GLP-1 analogue)

NN1215NN1215 (LABI)(LABI)

NN1998NN1998 (AERx)(AERx)

NN4201NN4201 (Hepatic glucose regulator)(Hepatic glucose regulator)

NN304NN304 (Basal analogue) (Basal analogue)

NN414NN414 (Insulin secretion)(Insulin secretion)

NN622NN622 (Dual-acting sensitiser)(Dual-acting sensitiser)

Phase 1Phase 1 Phase 2Phase 2 Phase 3Phase 3

NN2344NN2344 (Insulin sensitiser)(Insulin sensitiser)

18

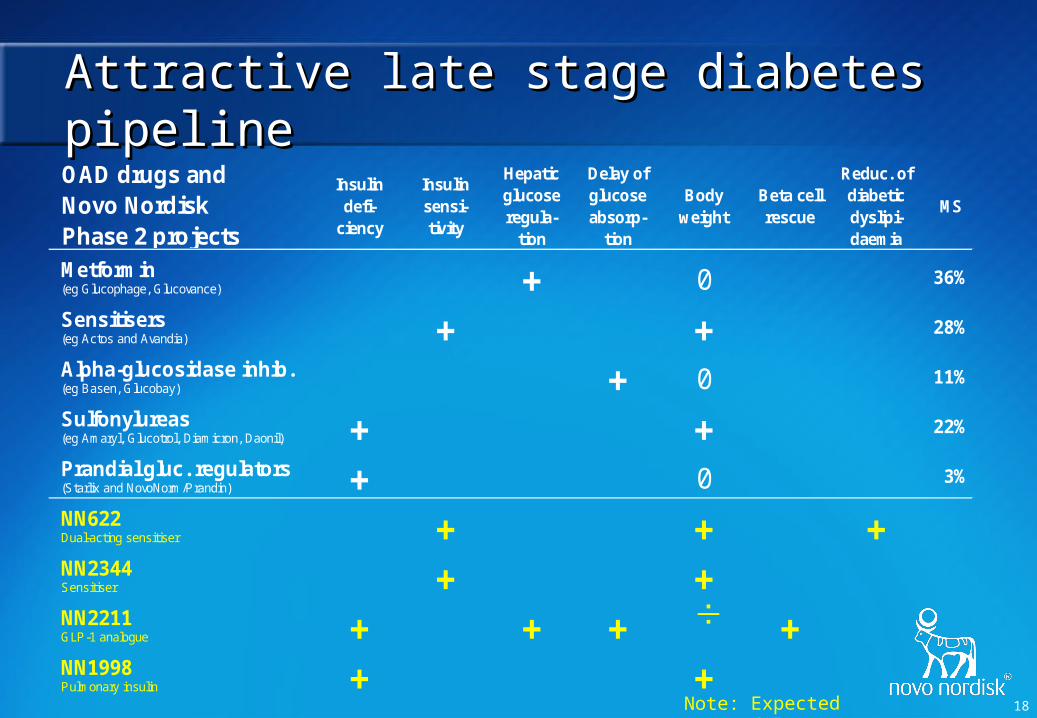

Attractive late stage diabetes pipelineAttractive late stage diabetes pipelineOAD drugs and Novo Nordisk Phase 2 projects

Insulin defi-

ciency

Insulin sensi-tivity

Hepatic glucose regula-

tion

Delay of glucose absorp-

tion

Body weight

Beta cell rescue

Reduc. of diabetic dyslipi-daemia

MS

Metformin (eg Glucophage, Glucovance) + 0 36%

Sensitisers (eg Actos and Avandia) + + 28%

Alpha-glucosidase inhib. (eg Basen, Glucobay) + 0 11%

Sulfonylureas (eg Amaryl, Glucotrol, Diamicron, Daonil) + + 22%

Prandial gluc. regulators (Starlix and NovoNorm/Prandin) + 0 3%

NN622Dual-acting sensitiser + + +NN2344Sensitiser + +NN2211GLP-1 analogue + + + +NN1998Pulmonary insulin + +

Note: Expected profiles

19

Novo Nordisk – Future Key DriversNovo Nordisk – Future Key Drivers

Diabetes careDiabetes careCoagulation Coagulation

disordersdisorders

PrimaryPrimarygrowth growth driversdrivers

Secondary Secondary valuevalue

driversdrivers HRTHRTHuman growth Human growth

hormonehormoneIntellectual Intellectual

propertyproperty

20

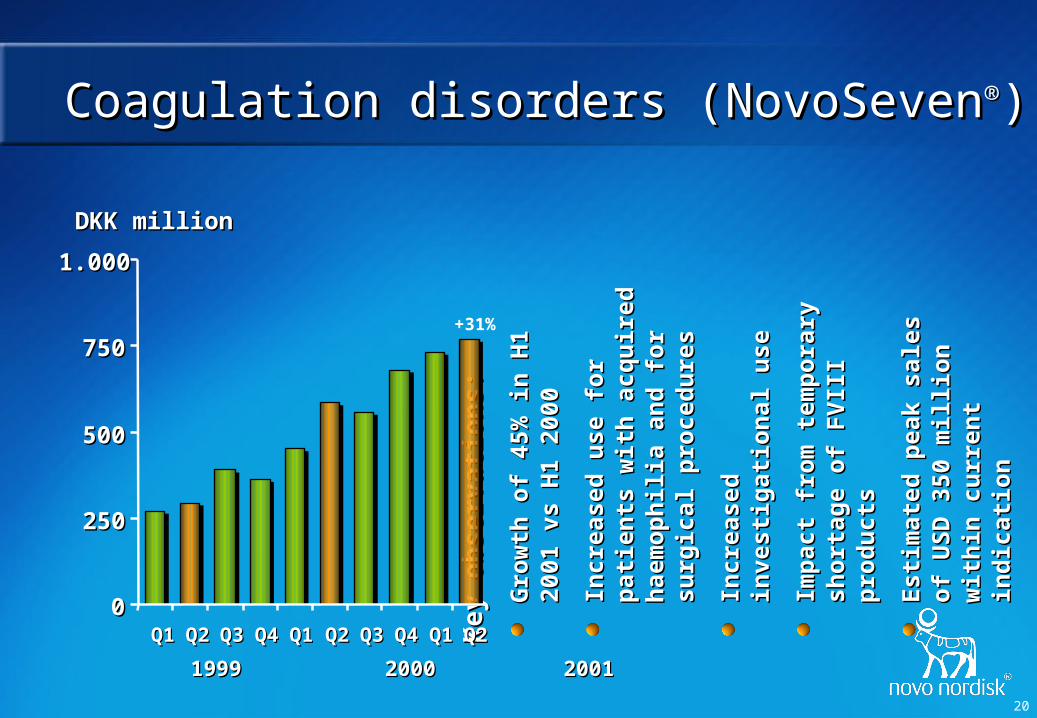

Coagulation disorders (NovoSevenCoagulation disorders (NovoSeven®®))

Ke

y o

bs

erva

tio

ns

:K

ey

ob

ser

vati

on

s:

Gro

wth

of

45%

in

H1

2001

G

row

th o

f 45

% i

n H

1 20

01

vs H

1 20

00vs

H1

2000

Incr

ease

d u

se f

or

pat

ien

ts

Incr

ease

d u

se f

or

pat

ien

ts

wit

h a

cqu

ired

hae

mo

ph

ilia

w

ith

acq

uir

ed h

aem

op

hil

ia

and

fo

r su

rgic

al p

roce

du

res

and

fo

r su

rgic

al p

roce

du

res

Incr

ease

d i

nve

stig

atio

nal

In

crea

sed

in

vest

igat

ion

al

use

use

Imp

act

fro

m t

emp

ora

ry

Imp

act

fro

m t

emp

ora

ry

sho

rtag

e o

f F

VII

I p

rod

uct

ssh

ort

age

of

FV

III

pro

du

cts

Est

imat

ed p

eak

sale

s o

f E

stim

ated

pea

k sa

les

of

US

D 3

50 m

illi

on

wit

hin

U

SD

350

mil

lio

n w

ith

in

curr

ent

ind

icat

ion

curr

ent

ind

icat

ion

DKK millionDKK million

19991999 2000 2001 2000 2001

00

250250

500500

750750

1.0001.000

Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2

+31%

21

The key advantages of NovoSevenThe key advantages of NovoSeven®® are: are:

Injury site selective activation of platelets Injury site selective activation of platelets creates high local thrombin generation creates high local thrombin generation which secures a tight fibrin clotwhich secures a tight fibrin clot

Efficacy independent of inhibitor titerEfficacy independent of inhibitor titer

Effective during & after surgeryEffective during & after surgery

Low thrombogenicityLow thrombogenicity

Good safety profileGood safety profile

Home treatmentHome treatment

Attractive cost/benefit ratioAttractive cost/benefit ratio

Advantages of NovoSevenAdvantages of NovoSeven®®

A bleeding episode

FVIIa/NovoSeven®®

Tissue factor

22

Beyond haemophilia treatmentBeyond haemophilia treatment

HaemostasisHaemostasisManagementManagement

NovoSevenNovoSeven®® in bleeding conditions in bleeding conditions Coagulation factor deficienciesCoagulation factor deficiencies

Platelet defectsPlatelet defects

General haemostasisGeneral haemostasis

Reduction of blood and plasma transfusionsReduction of blood and plasma transfusions

No product offers this safety and efficacy profileNo product offers this safety and efficacy profile

Increasing supportive data from investigational useIncreasing supportive data from investigational use

NovoSevenNovoSeven®® is a science-driven product is a science-driven product

HaeHaemmophiliaophiliaTreatmentTreatment

23

SpontaneousSpontaneousbleedingbleeding

Single Single FactorFactor

MultipleMultipleFactorsFactors

SurgicalSurgicalbleedingbleeding

Lack ofLack ofplateletsplatelets

DefectiveDefectiveplateletsplatelets

Coagulation FactorCoagulation FactorDeficiencyDeficiency

PlateletPlateletDisorderDisorder

GeneralGeneralHaemostasisHaemostasis

Haemophilia Haemophilia with inhibitorswith inhibitors

Upper Upper gastrointestinal gastrointestinal

bleedings *)bleedings *)

Orthotopic liver Orthotopic liver transplantations *)transplantations *)

Liver resection *)Liver resection *)

Intra-cerebral Intra-cerebral bleedingsbleedings

TraumatologyTraumatology

Vitamin K-Vitamin K-antagonistsantagonists

Stem cell Stem cell transplantationtransplantation

Liver resection Liver resection

*) *) == Patients with chronic liver diseasePatients with chronic liver disease

NovoSevenNovoSeven®® indication expansions indication expansions

24

Clinical areaClinical area Status on projectStatus on project

Building Strong Scientific EvidenceBuilding Strong Scientific Evidence

Orthotopic liver transplantation*Orthotopic liver transplantation* Ongoing Ph 2/3 projectOngoing Ph 2/3 projectUpper GI bleeds*Upper GI bleeds* Ph 2 study has been initiatedPh 2 study has been initiatedLiver resection*Liver resection* Ph 2 study has been initiatedPh 2 study has been initiated

Liver resectionLiver resection Exploratory Ph 2 study has been initiatedExploratory Ph 2 study has been initiatedBone marrow transplantationsBone marrow transplantations Ph 2 study has been initiatedPh 2 study has been initiatedIntra-cerebral bleedsIntra-cerebral bleeds Exploratory Ph 2 study has been initiatedExploratory Ph 2 study has been initiated

Reversal of anti-coagulantia therapyReversal of anti-coagulantia therapy Ph 2 study expected to start later this yearPh 2 study expected to start later this year

TraumatologyTraumatology Ph 2 study expected to start by year end 2001Ph 2 study expected to start by year end 2001

* Patients with chronic liver disease. * Patients with chronic liver disease.

25

Novo Nordisk – Future Key DriversNovo Nordisk – Future Key Drivers

Diabetes careDiabetes care Coagulation Coagulation disorderdisorder

PrimaryPrimarygrowth growth driversdrivers

Secondary Secondary valuevalue

driversdrivers

Human growth Human growth hormonehormone

Intellectual Intellectual propertyproperty HRTHRT

26

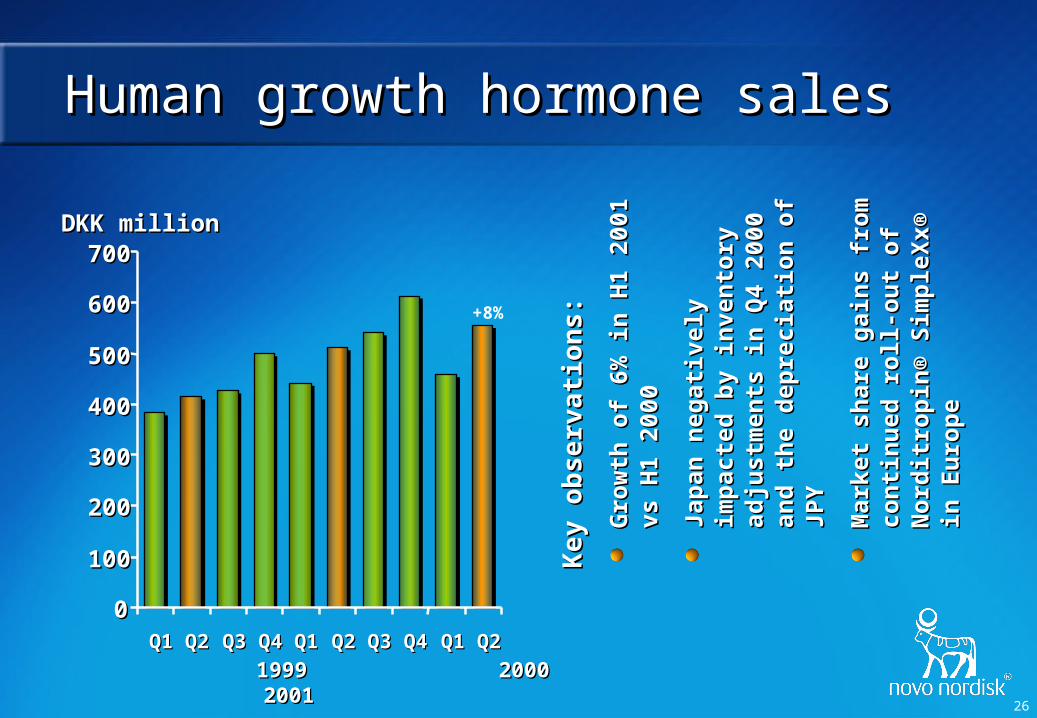

Ke

y o

bs

erva

tio

ns

:K

ey

ob

ser

vati

on

s:

Gro

wth

of

6% i

n H

1 20

01 v

s G

row

th o

f 6%

in

H1

2001

vs

H1

2000

H1

2000

Jap

an n

egat

ivel

y im

pac

ted

Ja

pan

neg

ativ

ely

imp

acte

d

by

inve

nto

ry a

dju

stm

ents

in

b

y in

ven

tory

ad

just

men

ts i

n

Q4

2000

an

d t

he

dep

reci

atio

n

Q4

2000

an

d t

he

dep

reci

atio

n

of

JPY

of

JPY

Mar

ket

shar

e g

ain

s fr

om

M

arke

t sh

are

gai

ns

fro

m

con

tin

ued

ro

ll-o

ut

of

con

tin

ued

ro

ll-o

ut

of

No

rdit

rop

in®

Sim

ple

Xx®

in

N

ord

itro

pin

® S

imp

leX

x® i

n

Eu

rop

eE

uro

pe

Human growth hormone salesHuman growth hormone sales

1999 2000 20011999 2000 2001

00

100100

200200

300300

400400

500500

600600

700700

Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2

DKK millionDKK million

+8%

27

Novo Nordisk – Future Key DriversNovo Nordisk – Future Key Drivers

Diabetes careDiabetes care Coagulation Coagulation disorderdisorder

PrimaryPrimarygrowth growth driversdrivers

Secondary Secondary valuevalue

driversdrivers

Intellectual Intellectual propertyproperty

HRTHRTHuman growth Human growth hormonehormone

28

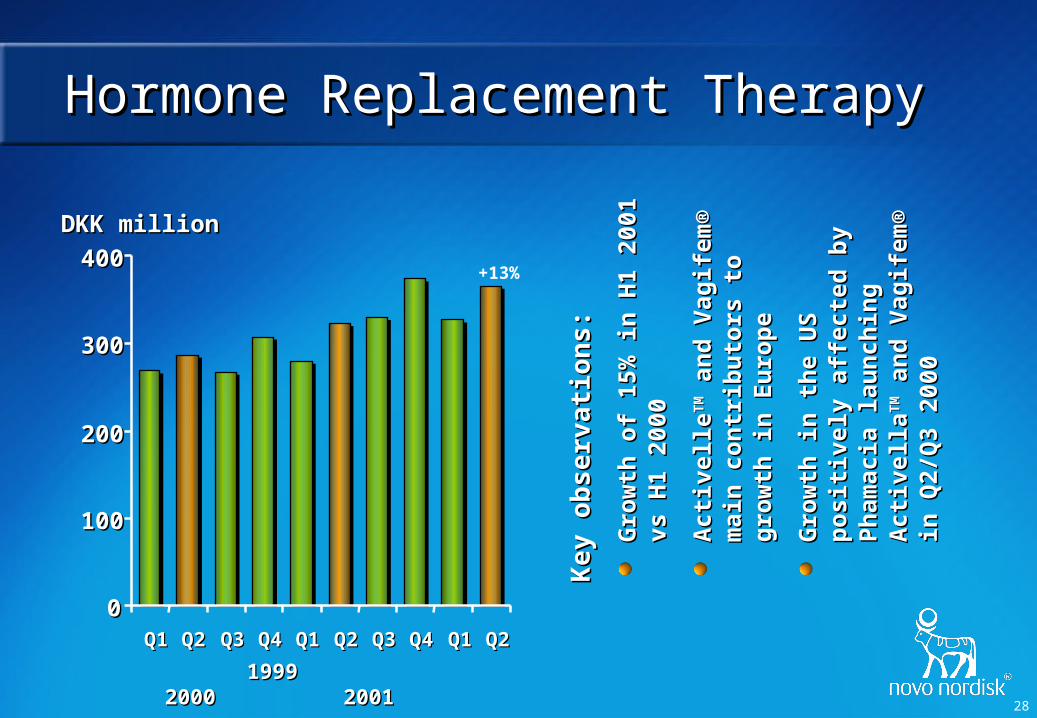

Ke

y o

bs

erva

tio

ns

:K

ey

ob

ser

vati

on

s:

Gro

wth

of

15%

in

H1

2001

G

row

th o

f 15

% i

n H

1 20

01

vs H

1 20

00vs

H1

2000

Act

ivel

leA

ctiv

elle

TM

TM a

nd

Vag

ifem

® m

ain

a

nd

Vag

ifem

® m

ain

co

ntr

ibu

tors

to

gro

wth

in

co

ntr

ibu

tors

to

gro

wth

in

E

uro

pe

Eu

rop

e

Gro

wth

in

th

e U

S p

osi

tive

ly

Gro

wth

in

th

e U

S p

osi

tive

ly

affe

cted

by

Ph

amac

ia

affe

cted

by

Ph

amac

ia

lau

nch

ing

Act

ivel

lala

un

chin

g A

ctiv

ella

TM

TM a

nd

a

nd

V

agif

em®

in

Q2/

Q3

2000

Vag

ifem

® i

n Q

2/Q

3 20

00

Hormone Replacement TherapyHormone Replacement Therapy

19991999 2000 2001 2000 2001

00

100100

200200

300300

400400

Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1 Q2Q2

DKK millionDKK million

+13%

29

Novo Nordisk – Future Key DriversNovo Nordisk – Future Key Drivers

Diabetes careDiabetes careCoagulation Coagulation

disorderdisorder

PrimaryPrimarygrowth growth driversdrivers

Secondary Secondary valuevalue

driversdrivers HRTHRTHuman growth Human growth

hormonehormoneIntellectual Intellectual

propertyproperty

30

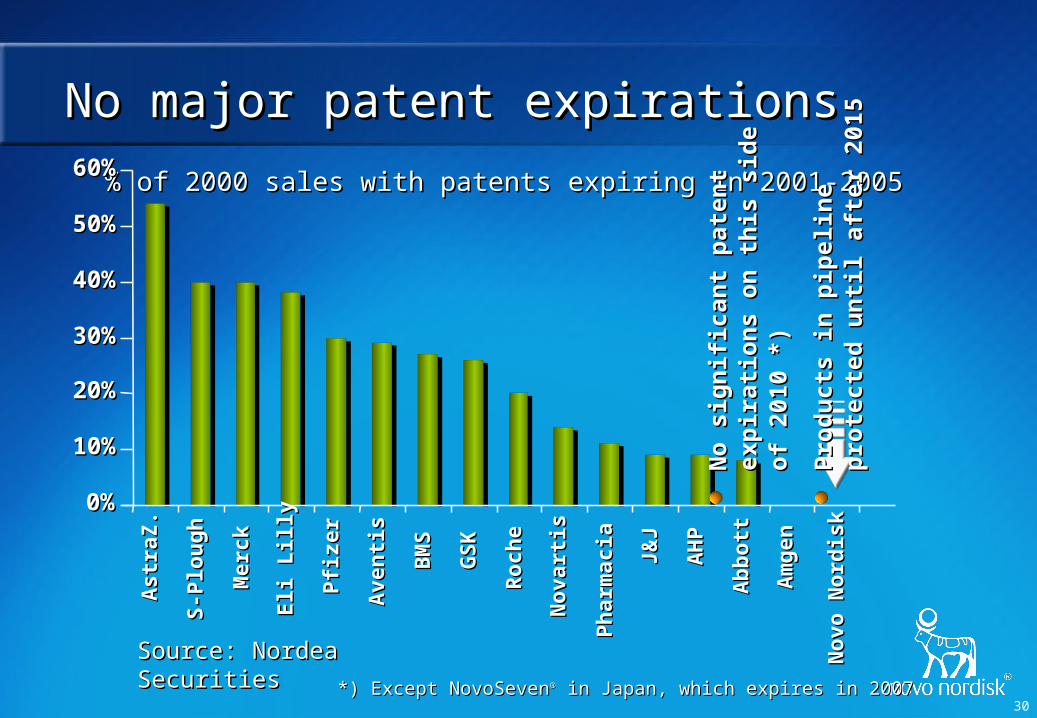

Source: Nordea SecuritiesSource: Nordea Securities

% of 2000 sales with patents expiring in 2001-2005% of 2000 sales with patents expiring in 2001-2005

No major patent expirationsNo major patent expirations

0%0%

10%10%

20%20%

30%30%

40%40%

50%50%

60%60%A

stra

Z.

Ast

raZ

.

S-P

lou

gh

S-P

lou

gh

Mer

ckM

erck

Eli

Lill

yE

li L

illy

Pfi

zer

Pfi

zer

Ave

nti

sA

ven

tis

BM

SB

MS

GS

KG

SK

Ro

che

Ro

che

NNoo

vart

isva

rtis

Ph

arm

acia

Ph

arm

acia

J&J

J&J

AH

PA

HP

Ab

bo

ttA

bb

ott

Am

gen

Am

gen

No

vo N

ord

isk

No

vo N

ord

isk

No

sig

nif

ican

t p

aten

t ex

pir

atio

ns

No

sig

nif

ican

t p

aten

t ex

pir

atio

ns

on

th

is s

ide

of

2010

*)

on

th

is s

ide

of

2010

*)

Pro

du

cts

in p

ipel

ine

pro

tect

ed

Pro

du

cts

in p

ipel

ine

pro

tect

ed

un

til

afte

r 20

15u

nti

l af

ter

2015

*) Except NovoSeven*) Except NovoSeven®® in Japan, which expires in 2007 in Japan, which expires in 2007

31

FinancialsFinancials

32

FFinancial results first inancial results first half year 2001half year 2001

Net turnoverNet turnover 11,35111,351 9,6699,669 1717

Operating profit as reported Operating profit as reported 2,7402,740 2,2712,271 2121Operating profit adjustedOperating profit adjusted*) *) 2,4452,445 1,9411,941 2626

Financial itemsFinancial items 241241 66 N/AN/AProfit before taxProfit before tax 2,9812,981 2,2772,277 3131Net profitNet profit 1,9081,908 1,4201,420 3434

Earnings per share (DKK)Earnings per share (DKK) 5.485.48 4.044.04 3636 Earnings Earnings per ADS (USD)**per ADS (USD)**)) 0.620.62 0.460.46 3636

**)) Excluding non-recurring items such as Seroxat® licence income and one-off settlements Excluding non-recurring items such as Seroxat® licence income and one-off settlements of patent disputes of patent disputes

****)) Translated for convenience at the end of June 2001 at the exchange rate of Translated for convenience at the end of June 2001 at the exchange rate of USD 100 = DKK USD 100 = DKK 878.98878.98

DKK millionDKK million 20012001 20002000 % change % change

33

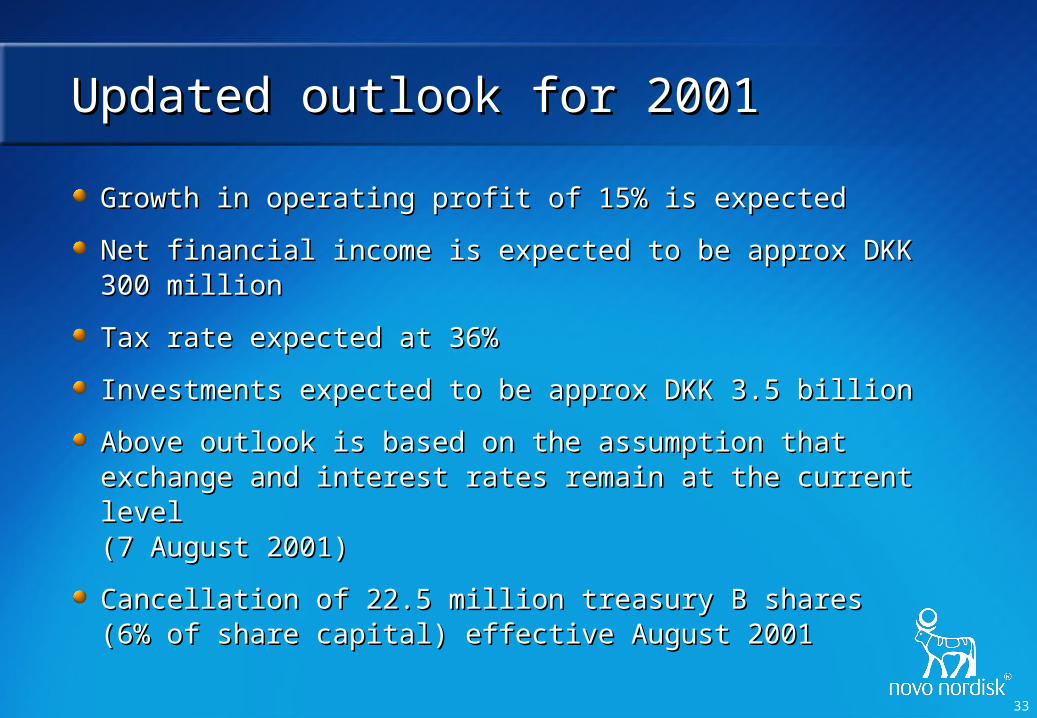

Updated outlook for 2001Updated outlook for 2001

Growth in operating profit of 15% is expectedGrowth in operating profit of 15% is expected

Net financial income is expected to be approx DKK 300 Net financial income is expected to be approx DKK 300 millionmillion

Tax rate expected at 36%Tax rate expected at 36%

Investments expected to be approx DKK 3.5 billionInvestments expected to be approx DKK 3.5 billion

Above outlook is based on the assumption that exchange Above outlook is based on the assumption that exchange and interest rates remain at the current level and interest rates remain at the current level (7 August 2001)(7 August 2001)

Cancellation of 22.5 million treasury B shares Cancellation of 22.5 million treasury B shares (6% of share capital) effective August 2001(6% of share capital) effective August 2001

34

Long-term Financial Targets Long-term Financial Targets

Financial targets Financial targets

EBIT growth of 15% per annumEBIT growth of 15% per annum

EBIT margin of 25%EBIT margin of 25%

ROIC of 25% (post-tax) per annumROIC of 25% (post-tax) per annum

Cash to earnings of 60%Cash to earnings of 60%

Balancing Balancing growth and valuegrowth and value

Observations from 2000 Observations from 2000

EBIT growth of 37%EBIT growth of 37%

EBIT margin of 23.1%EBIT margin of 23.1%

ROIC (post-tax) of 22.3%ROIC (post-tax) of 22.3%

Cash earnings ratio of 87.9%Cash earnings ratio of 87.9%

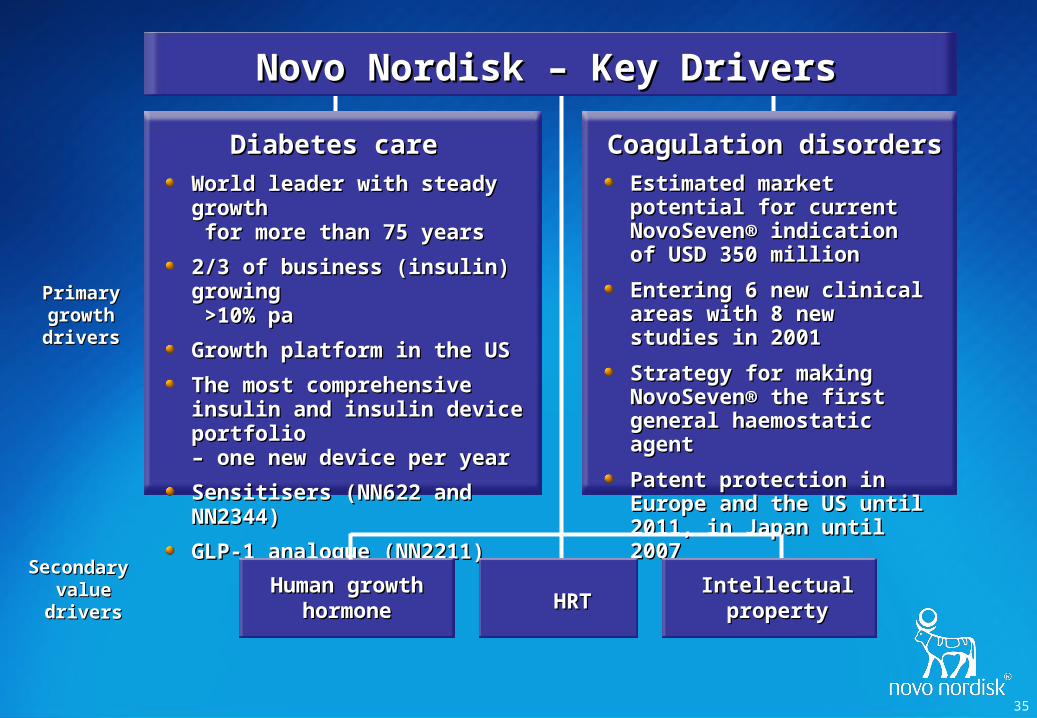

35

Estimated market potential Estimated market potential for current NovoSeven® for current NovoSeven® indication of USD 350 million indication of USD 350 million

Entering 6 new clinical areas Entering 6 new clinical areas with 8 new studies in 2001with 8 new studies in 2001

Strategy for making Strategy for making NovoSeven® the first general NovoSeven® the first general haemostatic agenthaemostatic agent

Patent protection in Europe Patent protection in Europe and the US until 2011, in and the US until 2011, in Japan until 2007Japan until 2007

PrimaryPrimarygrowthgrowthdriversdrivers

Secondary Secondary valuevalue

driversdrivers

Novo Nordisk – Key DriversNovo Nordisk – Key Drivers

World leader with steady growthWorld leader with steady growth for more than 75 years for more than 75 years

2/3 of business (insulin) growing2/3 of business (insulin) growing >10% pa >10% pa

Growth platform in the USGrowth platform in the US

The most comprehensive insulin The most comprehensive insulin and insulin device portfolio and insulin device portfolio – one new device per year– one new device per year

Sensitisers (NN622 and NN2344)Sensitisers (NN622 and NN2344)

GLP-1 analogue (NN2211)GLP-1 analogue (NN2211)

Diabetes careDiabetes care Coagulation disordersCoagulation disorders

HRTHRTHuman growth Human growth

hormonehormoneIntellectual Intellectual

propertyproperty

36

Forward-looking statementsForward-looking statements

This presentation contains forward-looking statements as the term is defined in the US This presentation contains forward-looking statements as the term is defined in the US Private Securities Litigation Reform Act of 1995. Private Securities Litigation Reform Act of 1995.

Such forward-looking statements are subject to risk and uncertainties that may cause Such forward-looking statements are subject to risk and uncertainties that may cause actual results to differ materially from expectations, including unexpected actual results to differ materially from expectations, including unexpected developments in the international currency exchange and securities markets, developments in the international currency exchange and securities markets, government-mandated or market-driven price decreases for Novo Nordisk's products in government-mandated or market-driven price decreases for Novo Nordisk's products in the company's major markets and the introduction of competing products within Novo the company's major markets and the introduction of competing products within Novo Nordisk's core businesses. Nordisk's core businesses.

These and other risks and uncertainties are further described in reports filed with the These and other risks and uncertainties are further described in reports filed with the US Securities and Exchange Commission (SEC) by Novo Nordisk and readily available US Securities and Exchange Commission (SEC) by Novo Nordisk and readily available to the public, including the company's Form 20-F, which was filed on 27 April 2001. to the public, including the company's Form 20-F, which was filed on 27 April 2001.

37

Investor InformationInvestor Information

Investor Relations contacts:Investor Relations contacts:

Novo Nordisk A/S Novo Nordisk A/S Investor Relations Investor Relations Novo Allé Novo Allé DK 2880 BagsværdDK 2880 BagsværdDenmark Denmark Fax (+45) 4444 2314. Fax (+45) 4444 2314.

Peter HaahrPeter HaahrPhone (+45) 4442 1207Phone (+45) 4442 1207 E-mail: [email protected]: [email protected]

Palle Holm Olesen Palle Holm Olesen Phone (+45) 4442 6175Phone (+45) 4442 6175 E-mail: [email protected]: [email protected]

Rasmus JorgensenRasmus JorgensenPhonePhone (+1) 212 867 0123 (+1) 212 867 0123 E-mail: [email protected]: [email protected]

Share informationShare information

Novo Nordisk’sNovo Nordisk’s B shares are listed B shares are listed on the stock exchanges in on the stock exchanges in Copenhagen and London. Its Copenhagen and London. Its ADSs are listed on the New York ADSs are listed on the New York Stock Exchange under the symbol Stock Exchange under the symbol "NVO". For further company "NVO". For further company information, visit Novo Nordisk on information, visit Novo Nordisk on the Internet at the Internet at

http://www.novonordisk.comhttp://www.novonordisk.com

38

AppendixAppendix

39

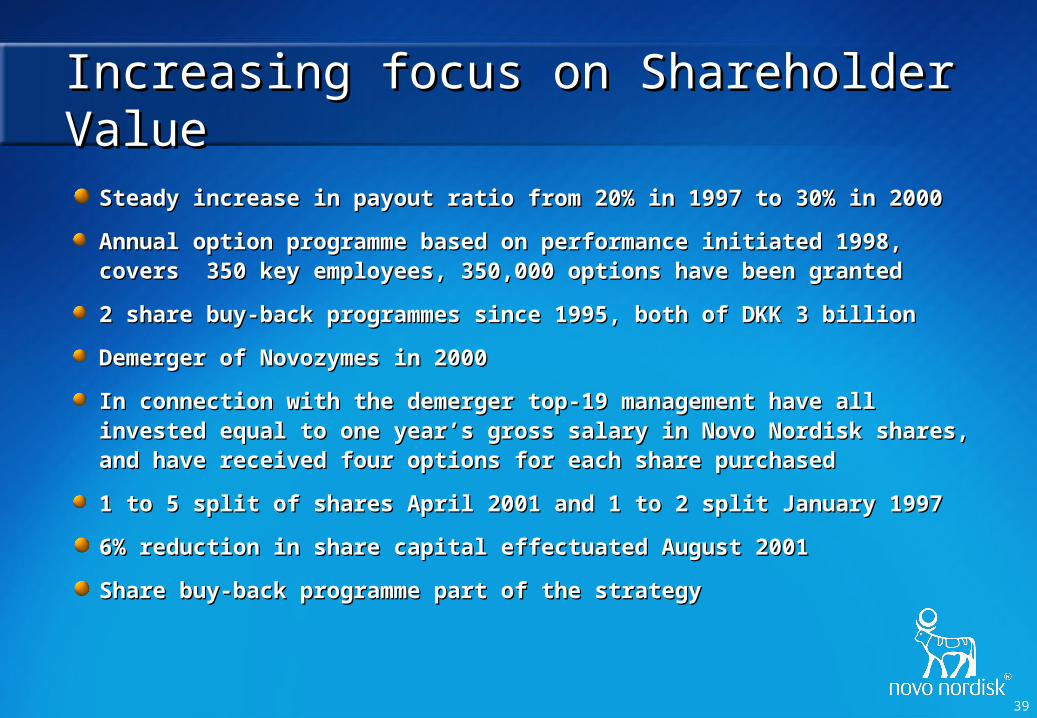

Increasing focus on Shareholder Value Increasing focus on Shareholder Value

Steady increase in payout ratio from 20% in 1997 to 30% in 2000 Steady increase in payout ratio from 20% in 1997 to 30% in 2000

Annual option programme based on performance initiated 1998, Annual option programme based on performance initiated 1998, covers 350 key employees, 350,000 options have been grantedcovers 350 key employees, 350,000 options have been granted

2 share buy-back programmes since 1995, both of DKK 3 billion 2 share buy-back programmes since 1995, both of DKK 3 billion

Demerger of Novozymes in 2000Demerger of Novozymes in 2000

In connection with the demerger top-19 management have all In connection with the demerger top-19 management have all invested equal to one year’s gross salary in Novo Nordisk shares, invested equal to one year’s gross salary in Novo Nordisk shares, and have received four options for each share purchasedand have received four options for each share purchased

1 to 5 split of shares April 2001 and 1 to 2 split January 19971 to 5 split of shares April 2001 and 1 to 2 split January 1997

6% reduction in share capital effectuated August 20016% reduction in share capital effectuated August 2001

Share buy-back programme part of the strategyShare buy-back programme part of the strategy

40

TTurnover by therapy first half year 2001urnover by therapy first half year 2001

DKK million 2001 2000 % of total % change(H1 2001)

Insulin etc 7,169 6,321 63 13

NovoNorm®/Prandin® 769 513 7 50

Diabetes care, total 7,938 6,834 70 16

Coagulation disorders* 1,499 1,034 13 45

Human growth hormone 1,011 952 9 6

HRT 692 603 6 15

Other 211 246 2 -14

Total 11,351 9,669 100 17

* NovoSeven®

41

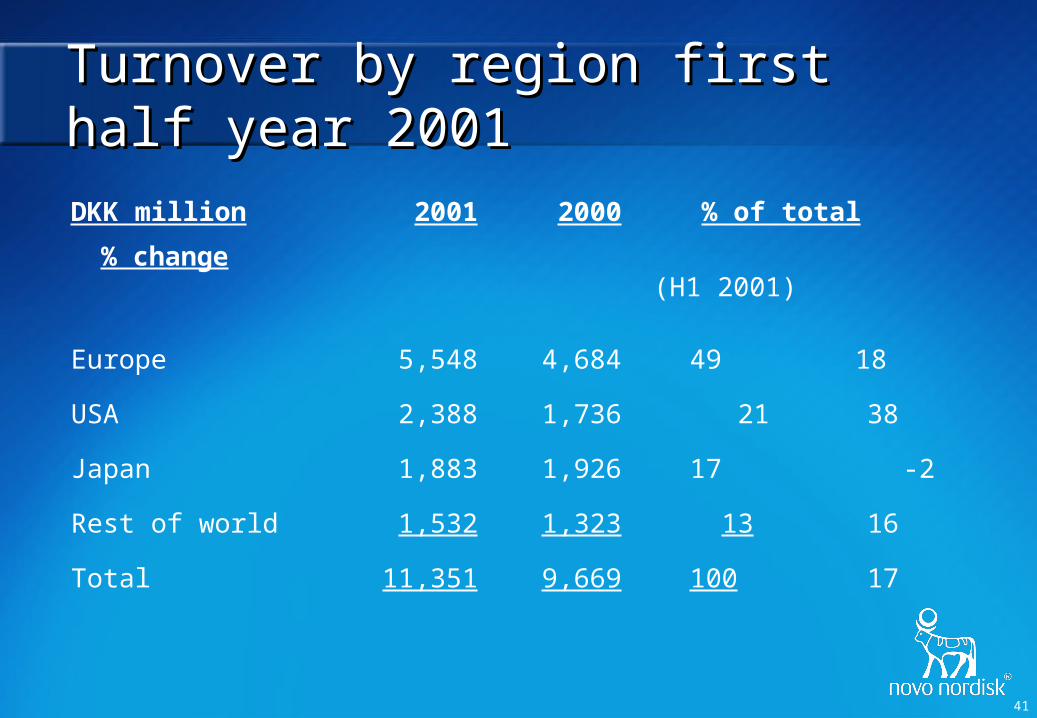

Turnover by region first half year 2001Turnover by region first half year 2001

DKK million 2001 2000 % of total % change (H1 2001)

Europe 5,548 4,684 49 18

USA 2,388 1,736 21 38

Japan 1,883 1,926 17 -2

Rest of world 1,532 1,323 13 16

Total 11,351 9,669 100 17

42

Profit & Loss 1998-2000Profit & Loss 1998-2000

DKK millionDKK million 19981998 19991999 20002000

Net turnoverNet turnover 13,64713,647 16,42316,423 20,81120,811

Y/Y growthY/Y growth +8.4%+8.4% +20.3%+20.3% +26.7%+26.7%

Gross profitGross profit 9,8969,896 12,19612,196 15,76715,767

EBITEBIT 2,9332,933 3,5273,527 4,8164,816

EBIT-marginEBIT-margin 21.5%21.5% 21.5%21.5% 23.1%23.1%

Net financeNet finance 243243 -178-178 2424

Pre-tax profitPre-tax profit 3,1763,176 3,3493,349 4,8404,840

Tax rateTax rate 36.5%36.5% 40.3%40.3% 36.2%36.2%

Net profitNet profit 2,0162,016 2,0012,001 3,0873,087

43

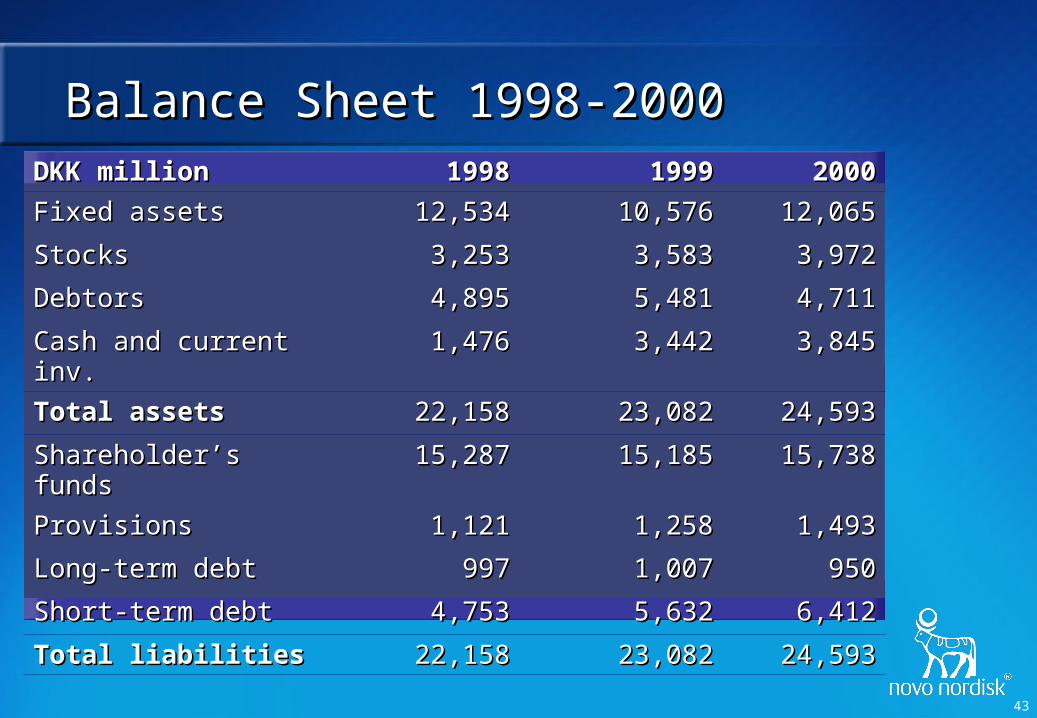

DKK millionDKK million 19981998 19991999 20002000

Fixed assetsFixed assets 12,53412,534 10,57610,576 12,06512,065

StocksStocks 3,2533,253 3,5833,583 3,9723,972

DebtorsDebtors 4,8954,895 5,4815,481 4,7114,711

Cash and current inv.Cash and current inv. 1,4761,476 3,4423,442 3,8453,845

Total assetsTotal assets 22,15822,158 23,08223,082 24,59324,593

Shareholder’s fundsShareholder’s funds 15,28715,287 15,18515,185 15,73815,738

ProvisionsProvisions 1,1211,121 1,2581,258 1,4931,493

Long-term debtLong-term debt 997997 1,0071,007 950950

Short-term debtShort-term debt 4,7534,753 5,6325,632 6,4126,412

Total liabilitiesTotal liabilities 22,15822,158 23,08223,082 24,59324,593

Balance Sheet 1998-2000Balance Sheet 1998-2000

44

Margin DevelopmentMargin Development

Note: EBIT margin as reportedNote: EBIT margin as reported

00

10001000

20002000

30003000

40004000

50005000

60006000

70007000

19971997 19981998 19991999 20002000

DK

K m

illio

nD

KK

mill

ion

R&D costsR&D costsS&D costsS&D costsAdm. costsAdm. costs

00

10001000

20002000

30003000

40004000

50005000

60006000

19971997 19981998 19991999 20002000

DK

K m

illio

nD

KK

mill

ion Production costsProduction costs Development in gross- andDevelopment in gross- and

EBIT-margin 1997-2000EBIT-margin 1997-2000

65%

67%

69%

71%

73%

75%

77%

79%

1997 1998 1999 2000

10%

12%

14%

16%

18%

20%

22%

24%

Gross margin (left-hand scale)

EBIT-margin (right-hand scale)

65%

67%

69%

71%

73%

75%

77%

79%

1997 1998 1999 2000

10%

12%

14%

16%

18%

20%

22%

24%

Gross margin (left-hand scale)

EBIT-margin (right-hand scale)

17

.4%

17

.4%

27

.9%

27

.9% 12

.1%

12

.1%

16

.3%

16

.3% 9.0

%9

.0%

30

.1%

30

.1%

45

Therapy:Therapy: Diet/ExerciseDiet/Exercise Oral products Oral products Oral/InsulinOral/Insulin InsulinInsulin Approx 66% Approx 66% Approx 7% Approx 27% Approx 7% Approx 27%

From diet and exercise to insulinFrom diet and exercise to insulin

Type 1:Type 1:(4 million patients*)(4 million patients*)

Type 2:Type 2:(147 million patients*)(147 million patients*)

* Estimated year 2000 incl. undiagnosed.* Estimated year 2000 incl. undiagnosed.

An estimated 25-30 million using medicationAn estimated 25-30 million using medication

46

06000600

NormalNormal

Type 2 diabetesType 2 diabetes

10001000 14001400 18001800 22002200 02000200 06000600

800800

700700

600600

500500

400400

300300

200200

100100

Insu

lin

Sec

reti

on

(p

mo

l/m

in)

Insu

lin

Sec

reti

on

(p

mo

l/m

in)

Kilde: O'MEARA et al. Am. J. Medicine, 1990; 89.Kilde: O'MEARA et al. Am. J. Medicine, 1990; 89.

Insulin Secretion in Normal People and People with Type 2 DiabetesInsulin Secretion in Normal People and People with Type 2 Diabetes

47

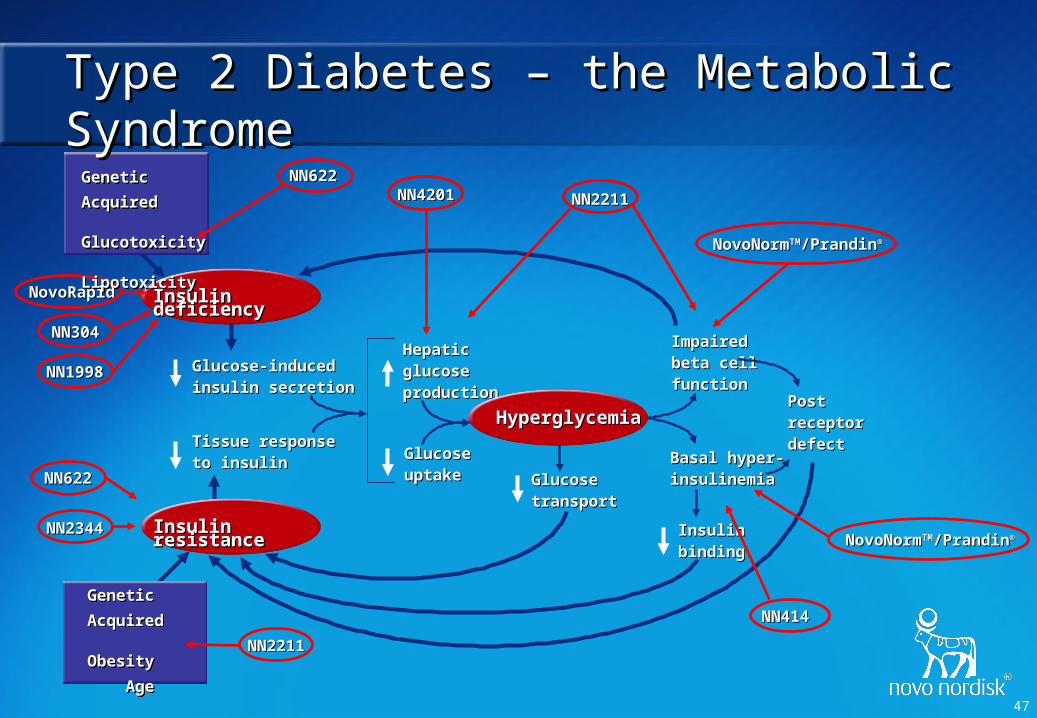

NovoNormNovoNormTMTM/Prandin/Prandin®®

NovoNormNovoNormTMTM/Prandin/Prandin®®

NN304NN304

NN1998NN1998

NN2344NN2344

Glucose-induced Glucose-induced insulin secretioninsulin secretion

Tissue response Tissue response to insulinto insulin

Hepatic Hepatic glucose glucose productionproduction

Glucose Glucose uptakeuptake

ImpairedImpairedbeta cellbeta cellfunctionfunction

Basal hyper- Basal hyper- insulinemiainsulinemia

Post Post receptor receptor defectdefect

GlucoseGlucosetransporttransport

Insulin Insulin bindingbinding

NN414NN414

NN4201NN4201

Genetic

Acquired

Obesity

Age

Genetic

Acquired

Obesity

Age

Insulin deficiencyInsulin deficiency

Insulin resistanceInsulin resistance

NovoRapidNovoRapid

Type 2 Diabetes – the MetabolicType 2 Diabetes – the Metabolic SyndromeSyndrome

Insulin deficiencyInsulin deficiency

Insulin resistanceInsulin resistance

HyperglycemiaHyperglycemia

NN2211NN2211

NN2211NN2211

NN622NN622

NN622NN622Genetic

Acquired Glucotoxicity Lipotoxicity

Genetic

Acquired Glucotoxicity Lipotoxicity

48

The key advantages of NovoSevenThe key advantages of NovoSeven®® are: are:

Injury site selective activation of platelets Injury site selective activation of platelets creates high local thrombin generation creates high local thrombin generation which secures a tight fibrin clotwhich secures a tight fibrin clot

Efficacy independent of inhibitor titerEfficacy independent of inhibitor titer

Effective during & after surgeryEffective during & after surgery

Low thrombogenicityLow thrombogenicity

Good safety profileGood safety profile

Home treatmentHome treatment

Attractive cost/benefit ratioAttractive cost/benefit ratio

Advantages of NovoSevenAdvantages of NovoSeven®®

A bleeding episode

FVIIa/NovoSeven®®

Tissue factor

The key advantages of NovoSevenThe key advantages of NovoSeven®® are: are:

Injury site selective activation of Injury site selective activation of platelets creates high local thrombin platelets creates high local thrombin generation which secures a tight fibrin generation which secures a tight fibrin clotclot

Efficacy independent of inhibitor titerEfficacy independent of inhibitor titer

Effective during & after surgeryEffective during & after surgery

Low thrombogenicityLow thrombogenicity

Good safety profileGood safety profile

Home treatmentHome treatment

Attractive cost/benefit ratioAttractive cost/benefit ratio

TF-Bearing CellTF-Bearing Cell

Activated PlateletActivated Platelet

PlateletPlatelet

VaVa

VaVaTFTFXaXa

XX IIIIThrombinThrombin

VV VaVa

IIIIXX

XaXaVIIIaVIIIa

IXIX

XXXaXa

IIII

IXaIXa

IXaIXa ThrombinThrombin

ThrombinThrombin

TFTF

49

Studies aimed at expanding the indication

Orthotopic liver transplantions*) Reduce bleeding, leading to fewer transfusions and thereby reducing post-operative complications

Liver resections*) Fast induction of haemostasis and hopefully allow for transfusion-free surgery

Upper gastrointestinal bleedings*) Faster haemostasis and reduce re-bleeding episodes

Liver resections in patients with no coagulation disorders

Fast induction of haemostasis and hopefully allow for transfusion-free surgery

Intra-cerebral bleedings Fast haemostasis, reduced mortality and morbidity, thus increased quality of life

Reversal of anticoagulation therapy (vitamin K-antagonists)

Faster haemostasis and reduced number of transfusions, leading to faster recovery

Stem cell/bone marrow transplantations

Faster haemostasis, reduced mortality and number of transfusions. Fewer patients with platelet antibodies

Traumatology Faster haemostasis, reduced mortality and number of transfusions. Fewer multi-organ failures and thereby less surgery and faster recovery

Expected benefits of NovoSeven®New clinical area targeted

*) Patients with chronic liver disease

50

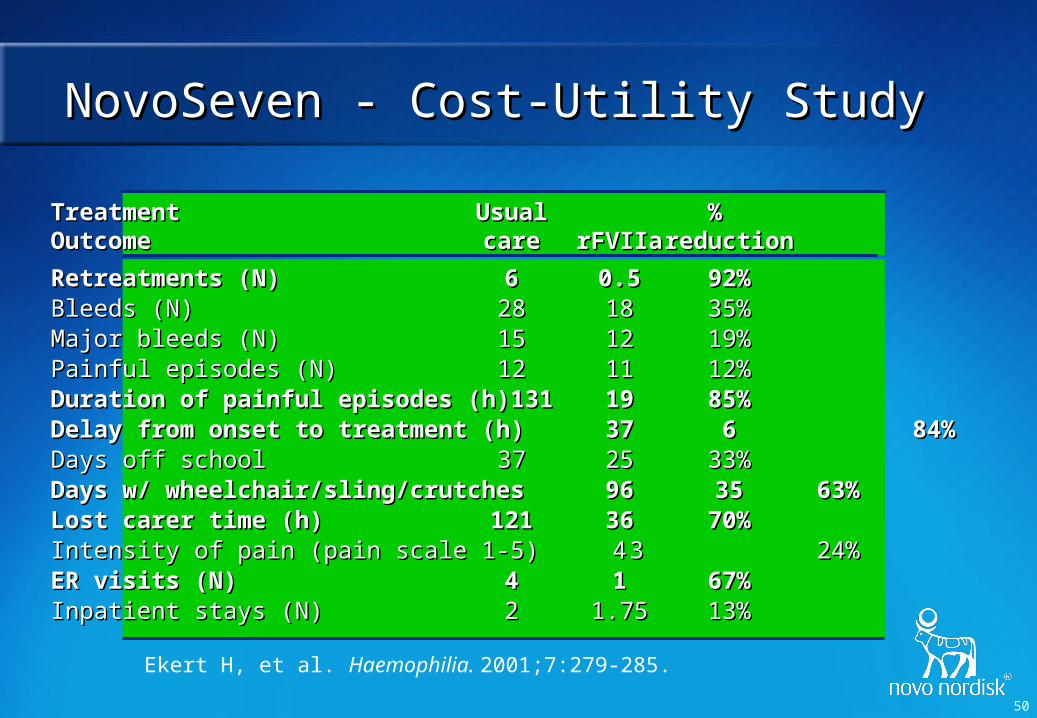

NovoSeven - Cost-Utility StudyNovoSeven - Cost-Utility Study

TreatmentTreatment UsualUsual % % OutcomeOutcome carecare rFVIIarFVIIa reductionreduction

Retreatments (N)Retreatments (N) 66 0.50.5 92%92%Bleeds (N)Bleeds (N) 2828 1818 35%35%Major bleeds (N)Major bleeds (N) 1515 1212 19%19%Painful episodes (N)Painful episodes (N) 1212 1111 12%12%Duration of painful episodes (h)Duration of painful episodes (h) 131131 1919 85%85%Delay from onset to treatment (h)Delay from onset to treatment (h) 3737 66 84%84%Days off schoolDays off school 3737 2525 33%33%Days w/ wheelchair/sling/crutchesDays w/ wheelchair/sling/crutches 9696 3535 63%63%Lost carer time (h)Lost carer time (h) 121121 3636 70%70%Intensity of pain (pain scale 1-5)Intensity of pain (pain scale 1-5) 44 33 24%24%ER visits (N)ER visits (N) 44 11 67%67%Inpatient stays (N)Inpatient stays (N) 22 1.751.75 13%13%

Ekert H, et al. Haemophilia. 2001;7:279-285.

51

Triple Bottom LineTriple Bottom Line

Environmentally Environmentally soundsound

Socially Socially ResponsibleResponsible

EconomicallyEconomicallyviableviable