1 NEW RULES FOR BOND INVESTING Planning for the Individual Investor Stan Richelson, J.D.,LLM & Hildy...

33

1 NEW RULES FOR BOND INVESTING Planning for the Individual Investor Stan Richelson, J.D.,LLM & Hildy Richelson, Ph.D. Scarsdale Investment Group, Ltd., Blue Bell, PA 19422 215-646-8768; 215-646-7693 [email protected] Authors: The Money-Making Guide to Bonds: Straightforward Strategies for Picking the Right Bonds and Bond Funds , Bloomberg Press. © Stan Richelson and Hildy Richelson 2006

-

Upload

kathleen-hodge -

Category

Documents

-

view

217 -

download

0

Transcript of 1 NEW RULES FOR BOND INVESTING Planning for the Individual Investor Stan Richelson, J.D.,LLM & Hildy...

1

NEW RULES FOR BOND INVESTING

Planning for the Individual Investor

Stan Richelson, J.D.,LLM & Hildy Richelson, Ph.D. Scarsdale Investment Group, Ltd., Blue Bell, PA 19422

215-646-8768; [email protected]

Authors: The Money-Making Guide to Bonds: Straightforward Strategies for Picking the Right Bonds and Bond Funds, Bloomberg Press.© Stan Richelson and Hildy Richelson 2006

2

The Case for Bonds

• There are beliefs that we take for granted that guide our lives, and we assume that they are true.

• For example, the statement that stocks will always outperform bonds is assumed to be true in financial planning.

• The corollary to that is that bonds are for old people.

• We are here to make the case for bonds and to suggest new ways to look at bond investing.

3

Bonds Suitable for Individuals

• Individual Investors and Institutions should follow different investment rules because they are not alike.– Endowments keep growing/investors

ultimately draw down their capital– Endowments live forever/ investors ultimately

die

4

Indecision

5

Richelson’s Bonds for the Individual Investor

Plain Vanilla Bonds• Highly rated individual

bonds• Treasury bonds• US Agency bonds• Highly rated US corporate

bonds• Highly rated muni bonds• Foreign bonds-US

currency denominated

Not Bonds for Us• Junk bonds• Emerging Market bonds• Foreign currency bonds• Mortgage backed

securities • UITs• Bond Funds• Bond ETFs

6

7

Stock vs. Bond Performance

• Old Rule: Stocks will always outperform bonds over every 10-year period.– Since stocks have outperformed bonds in the past,

they will continue to outperform bonds in the future.– Stocks’ higher risk will bring greater rewards.

• New Rule: It is uncertain that stocks will outperform bonds over every 10-year period because the world of the present is different than the past.

8

Stock vs. Bond Performance

• Stock Investing has been risky in the past• Crash of 1929 • Crash of 1987 (508 points or 22.6%)• Bear market of 2000-2002• Japanese stock market declined 80.5% from 1989

to 2003.• Will stocks be risky in the future?

9

History of Dividends on Large Company Stocks

• 1926 to 1954: Dividends always above 5%• 1950: Dividends peaked at 8.77%

• 1975 to 1985: Dividends generally around 5%• Current dividends

– On large company stocks:1.8%– On most small and midsize company stocks:0%

• 1926-1959: Dividends higher than interest paid on long-term Treasury bonds

10

11

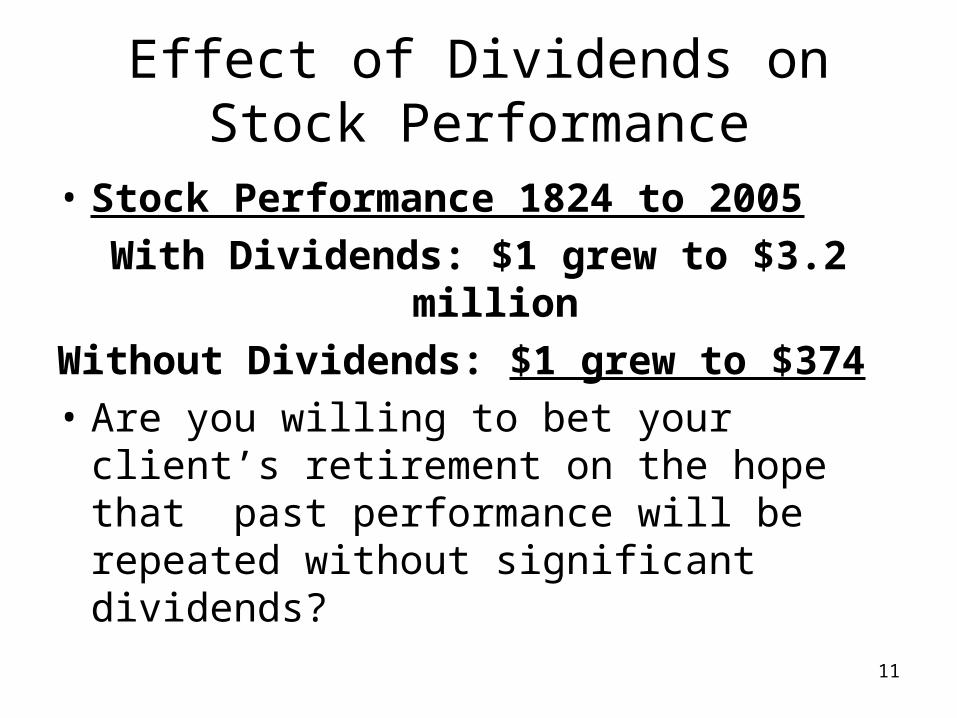

Effect of Dividends on Stock Performance

• Stock Performance 1824 to 2005

With Dividends: $1 grew to $3.2 million

Without Dividends: $1 grew to $374

• Are you willing to bet your client’s retirement on the hope that past performance will be repeated without significant dividends?

12

Effect of Losses in First Years of Retirement

• Losses in the first years of retirement devastate portfolio performance.– Retirement date: 1973. Market loss -14.6%– Retirement date: 1974. Market loss - 26.5%– Retirement date: 2000. Market loss - 9.1%– Retirement date: 2001. Market loss - 11.9%– Retirement date: 2002. Market loss - 22.1%

13

Effect of Losses in First Years of Retirement

• Story of Bob Goodtiming, owner of a $1 million portfolio– Retirement year 1: stocks decline 10%. He

withdraws $100,000.– Retirement year 2: stocks decline 10%. He

withdraws $100,000.– Beginning of retirement year 3: Portfolio is

down to $620,000.– The Wal-Mart job is looking very attractive.

14

Historical Stock Returns After Costs

• Old Rule: The historical return of stocks is around 10%.

• New Rule: The actual historical return on stocks is much less than 10% when taxes, transaction costs and bad timing are taken into account.

15

Persistent Drags on Stock Performance

• The 10% historical return on stocks ignores the following:– Income taxes paid to Federal, and sometimes

to state & local governments.– Transactions costs when stocks are bought

and sold.– Investor’s bad timing due to emotion.

16

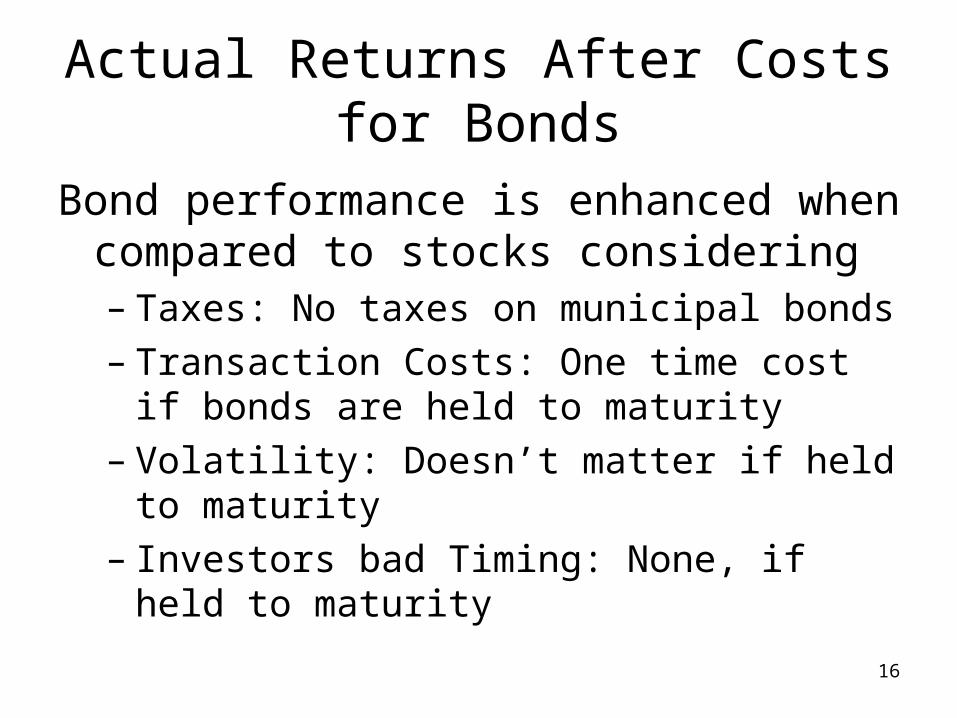

Actual Returns After Costs for Bonds

Bond performance is enhanced when compared to stocks considering– Taxes: No taxes on municipal bonds– Transaction Costs: One time cost if bonds are

held to maturity– Volatility: Doesn’t matter if held to maturity– Investors bad Timing: None, if held to maturity

17

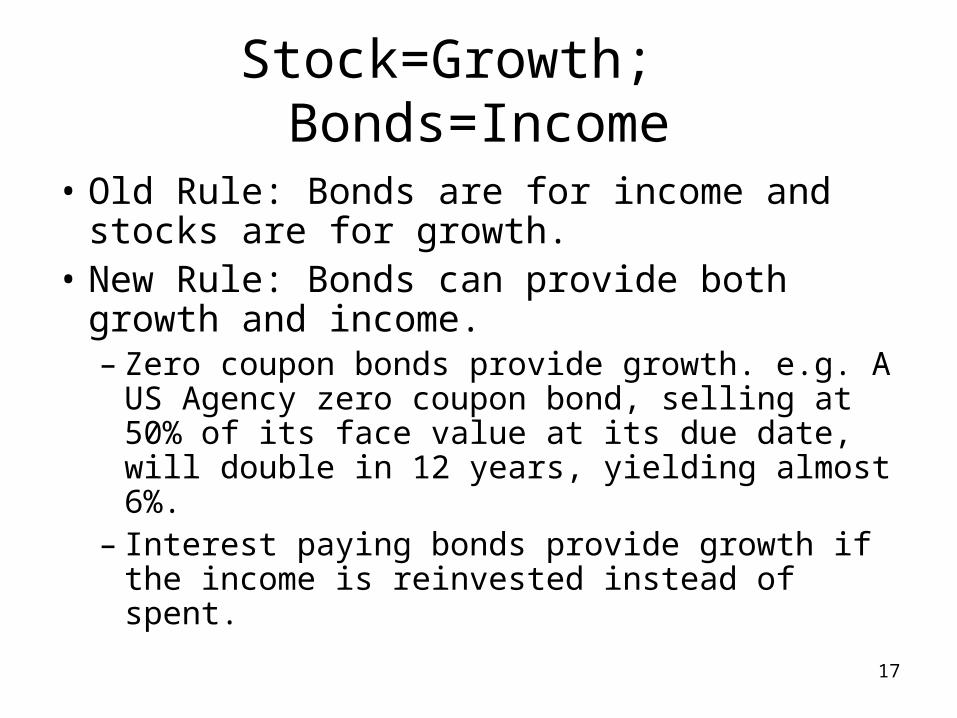

Stock=Growth; Bonds=Income

• Old Rule: Bonds are for income and stocks are for growth.

• New Rule: Bonds can provide both growth and income.– Zero coupon bonds provide growth. e.g. A US

Agency zero coupon bond, selling at 50% of its face value at its due date, will double in 12 years, yielding almost 6%.

– Interest paying bonds provide growth if the income is reinvested instead of spent.

18

Inflation

• Old Rule: Stocks provide a hedge against inflation. Bonds are destroyed by inflation.

• New Rule: Stocks do poorly when there is significant inflation. Bond holders increase cash flow in inflationary times, when interest rate rise.

19

Inflation

• Stocks have performed poorly when there is a lot of inflation.

• In the 1970’s there was record breaking inflation– 1973 the Dow was at a high of 1020– 1974 the Dow was at a low of 470;

• a loss of 55%

• One reason: Competition with high yields on bonds. In the 1970’s bond yields ranged from a low of 6% to a high of about 9%.

20

Rising Interest Rates & Bonds

• Old Rule: Rising interest rates are bad for bond investors because the value of bonds decline.

• New Rule: rising interest rates are an opportunity to increase income, yield and cash flow.

21

Rising Interest Rates & Bonds

• If interest rates rise, an investor will not have a loss if he holds to maturity.

• Rising interest rates are a blessing, not a curse. It results in increased cash flow.

22

Using Bonds in a Rising Interest Rate Market

• Reinvest cash on hand

• Reinvest maturing bond capital

• Sell the short-end of the laddered portfolio and reinvest the capital in longer dated bonds.

23

Cash or Invest?

• Old Rule: Interest rates are currently near a 40-year low, so stay in cash because interest rates must rise. If you invest, you will lose money.

• New Rule: Invest your cash when you have it because you cannot predict if interest rates will rise or fall.

24

Quick History of Interest Rates on Long-Term Treasury Bonds

• Current interest rates are actually above average for the last 85 years.– 1921-1966: Interest rates on long-term

Treasury bonds less than 6%. 1944 was the low, with rates at 2%.

– 1967-2001: Interest rate on long-term Treasury bonds always above 5%. 1981 was the high, with rates at 13.9%.

– 1921-2005: Average of about 4.9%– May 2006: About 5.2%

25

Bond Diversification

• Old Rule: Always diversify bond portfolios into all bond sectors, including junk and emerging market bonds to maximize returns.

• New Rule: Don’t diversify into sectors for added return when the spread between safe bonds and risky bonds is small. Stay only in safe bonds to avoid losses.

26

Bond Diversification

• Referring to the high-yield sector of the bond markets, Warren Buffet said in 2004 “Yesterday’s weeds are being priced as flowers.”

• The spread between the 7-year Treasury bond and junk bonds has ranged roughly over the last twenty years between 3% and 10%, and is currently near its low.

• After losses, at a 3% spread you are doomed to a lower return than Treasurys because of the greater risk of default.

27

Bonds vs. Bond Funds (ETFs)

• Old Rule: Investing in bond funds or bond ETFs is the same as investing in individual bonds.

• New Rule: Bonds come due. Bond funds do not have a maturity date and therefore are a different kind of investment.

28

Bonds vs Bond Funds (ETFs)

• Bond funds and bond ETFs– Provide diversification, not essential with high quality

bonds.– Risk portfolio losses if interest rates rise.– Charge fees & trading costs– Subject the investors to additional taxes.

• Individual bonds – Are less expensive if bought and held to maturity– Target planning for life events

29

Performance vs. Cash Flow

• Old Rule: Bond investing is all about performance and trading.

• New Rule: Bond investing is about creating a cash flow.

30

Investments for Volatility or Stability

• Old Rule: View investments as separate from earned income.

• New Rule: Harmonize and integrate cash flows from bonds and earned income, viewing earned income as a variable and bond income as the core for stability.

31

Planning for Transitions

• The client’s earned income should be viewed as variable because they may – Want to walk away from a job– Get laid off or become disabled– Need support for investment transitions-e.g. real

estate where the asset is very illiquid

• Bonds are not just for old people. At every age, people need the flexibility to change what they do and how they live, and deal with bumps in the road.

32

We Live What We Teach

• We never had a bond default, nasty client call or a sleepless night because of our bonds.

• Except for the last 5 years, we had a high return on bonds.

• Last 5 years, even the lower rate of interest on bonds was higher than the return on stocks due to the bear market of 2000 to 2002.

• Our returns overall from our laddered portfolios were higher than 5% because our call protected bonds continued to pay at higher rates.

33

Bond Investments for All Ages at All Times

Fixed income investments provide a

predictable cash flow that will enable you and your clients to

change your lives.

Scarsdale Investment Group, Ltd., Blue Bell, PA 19422

215-646-8768;215-646-7693