1 Is the Comprehensive Assessment really comprehensive? R. Baviera, Politecnico Milano, Nicola Bruti...

24

1 Is the Comprehensive Assessment really comprehensive? R. Baviera, Politecnico Milano, Nicola Bruti Liberati QFinLab E. Barucci, Politecnico Milano, Nicola Bruti Liberati QFinLab C. Milani, Centro Europa Ricerche Paris, VIII Financial Risks International Forum, March 30-31, 2015

-

Upload

ilene-fletcher -

Category

Documents

-

view

218 -

download

0

Transcript of 1 Is the Comprehensive Assessment really comprehensive? R. Baviera, Politecnico Milano, Nicola Bruti...

1

Is the Comprehensive Assessment really comprehensive?

Is the Comprehensive Assessment really comprehensive?

R. Baviera, Politecnico Milano, Nicola Bruti Liberati QFinLab

E. Barucci, Politecnico Milano, Nicola Bruti Liberati QFinLab

C. Milani, Centro Europa Ricerche

Paris, VIII Financial Risks International Forum, March 30-31, 2015

22R. Baviera Is the Comprehensive Assessment really comprehensive?

Outline

Comprehensive Assessment

Asset Quality Review (AQR) and Stress Tests (ST); The role of shortfall.

The analysis

Research questions; Dataset; Reference model.

Results

Main results; Further results; Is the Comprehensive Assessment really comprehensive?

33R. Baviera Is the Comprehensive Assessment really comprehensive?

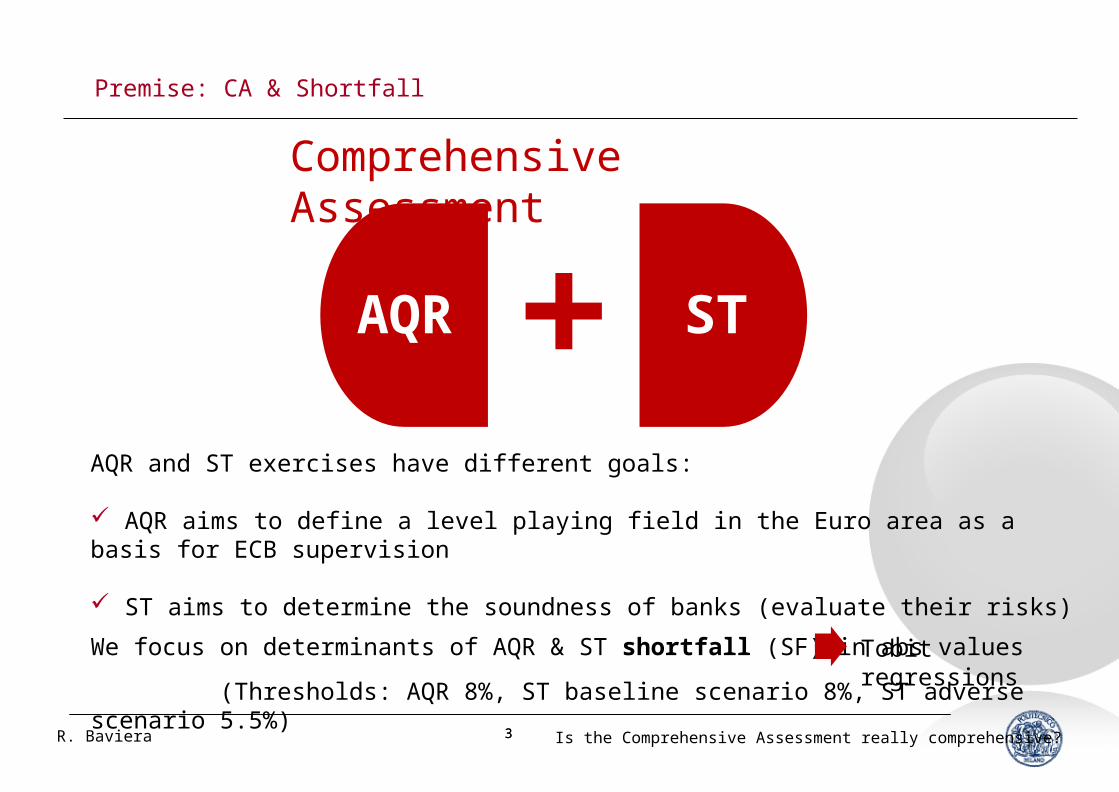

Premise: CA & Shortfall

AQR and ST exercises have different goals:

AQR aims to define a level playing field in the Euro area as a basis for ECB supervision

ST aims to determine the soundness of banks (evaluate their risks)

AQR

ST

Comprehensive Assessment

We focus on determinants of AQR & ST shortfall (SF) in abs values

(Thresholds: AQR 8%, ST baseline scenario 8%, ST adverse scenario 5.5%)

Tobit regressions

44R. Baviera Is the Comprehensive Assessment really comprehensive?

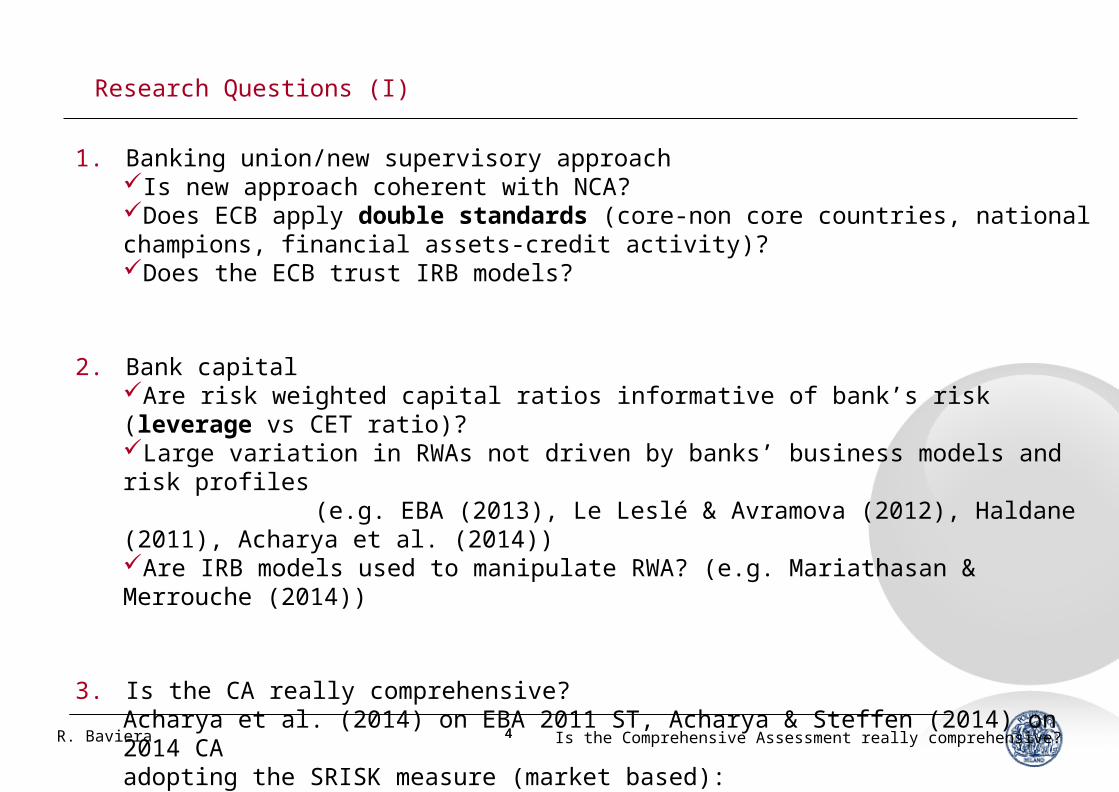

Research Questions (I)

1. Banking union/new supervisory approachIs new approach coherent with NCA?Does ECB apply double standards (core-non core countries, national champions, financial assets-credit activity)?Does the ECB trust IRB models?

2. Bank capitalAre risk weighted capital ratios informative of bank’s risk (leverage vs CET ratio)?Large variation in RWAs not driven by banks’ business models and risk profiles

(e.g. EBA (2013), Le Leslé & Avramova (2012), Haldane (2011), Acharya et al. (2014))Are IRB models used to manipulate RWA? (e.g. Mariathasan & Merrouche (2014))

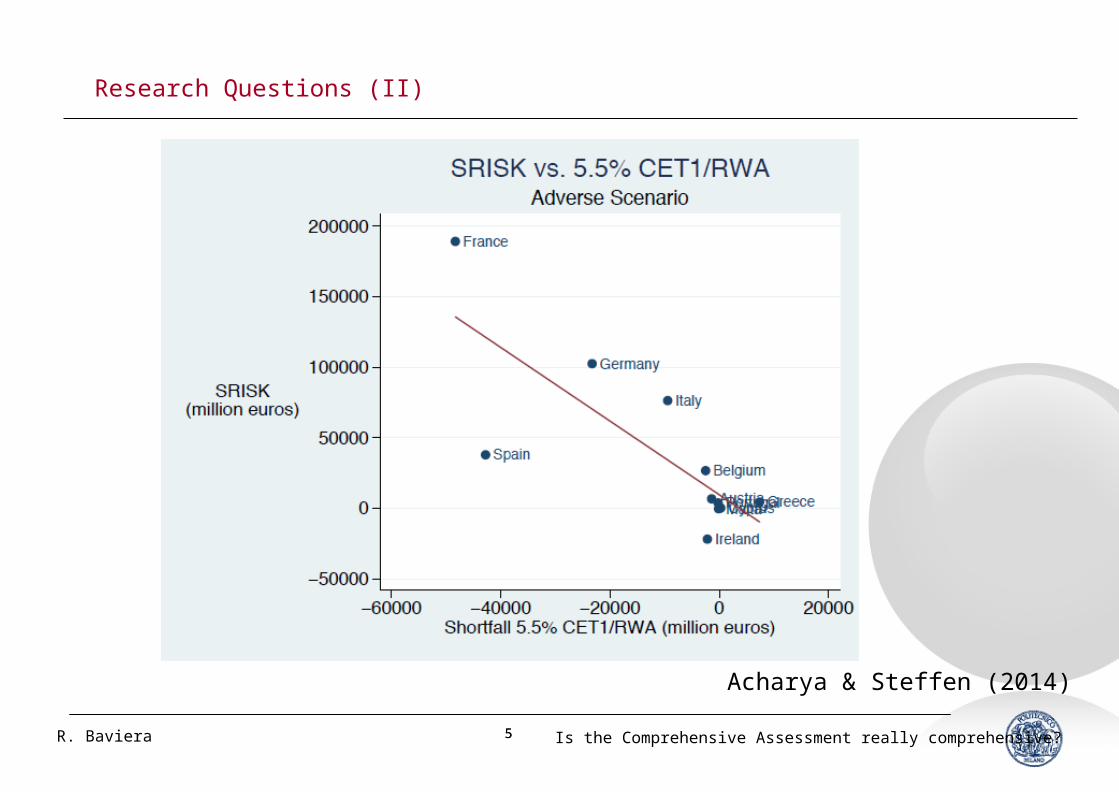

3. Is the CA really comprehensive?Acharya et al. (2014) on EBA 2011 ST, Acharya & Steffen (2014) on 2014 CAadopting the SRISK measure (market based): the adjustment should be much higher than the one computed by the CA SF computed w.r.t. a RWA capital ratio is negatively related to SRISK

55R. Baviera Is the Comprehensive Assessment really comprehensive?

Research Questions (II)

Acharya & Steffen (2014)

66R. Baviera Is the Comprehensive Assessment really comprehensive?

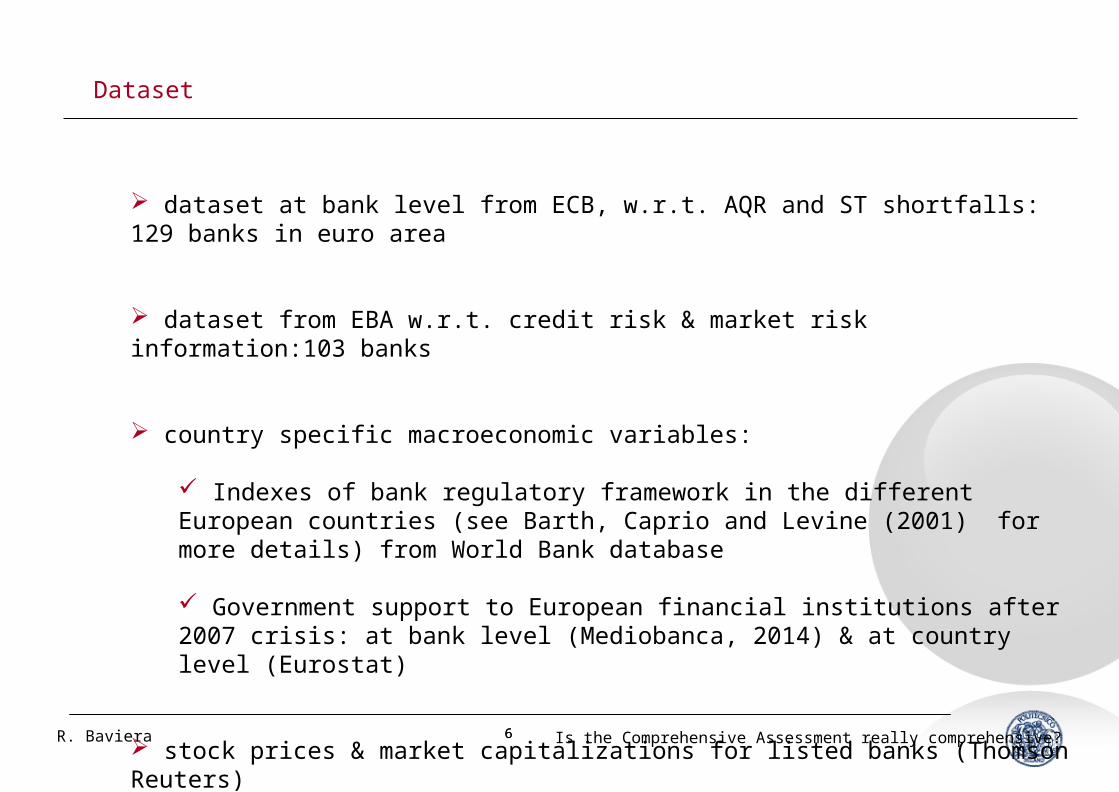

Dataset

dataset at bank level from ECB, w.r.t. AQR and ST shortfalls: 129 banks in euro area

dataset from EBA w.r.t. credit risk & market risk information:103 banks

country specific macroeconomic variables:

Indexes of bank regulatory framework in the different European countries (see Barth, Caprio and Levine (2001) for more details) from World Bank database

Government support to European financial institutions after 2007 crisis: at bank level (Mediobanca, 2014) & at country level (Eurostat)

stock prices & market capitalizations for listed banks (Thomson Reuters)

77R. Baviera Is the Comprehensive Assessment really comprehensive?

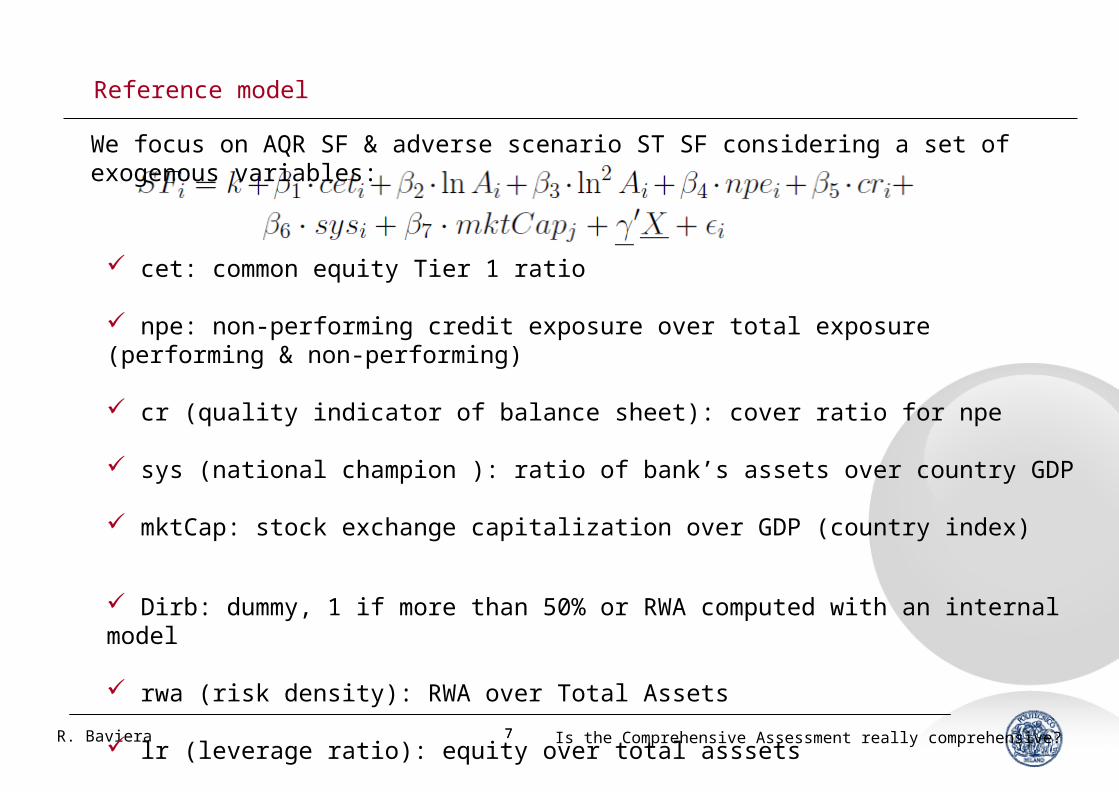

Reference model

We focus on AQR SF & adverse scenario ST SF considering a set of exogenous variables:

cet: common equity Tier 1 ratio

npe: non-performing credit exposure over total exposure (performing & non-performing)

cr (quality indicator of balance sheet): cover ratio for npe

sys (national champion ): ratio of bank’s assets over country GDP

mktCap: stock exchange capitalization over GDP (country index)

Dirb: dummy, 1 if more than 50% or RWA computed with an internal model

rwa (risk density): RWA over Total Assets

lr (leverage ratio): equity over total asssets

88R. Baviera Is the Comprehensive Assessment really comprehensive?

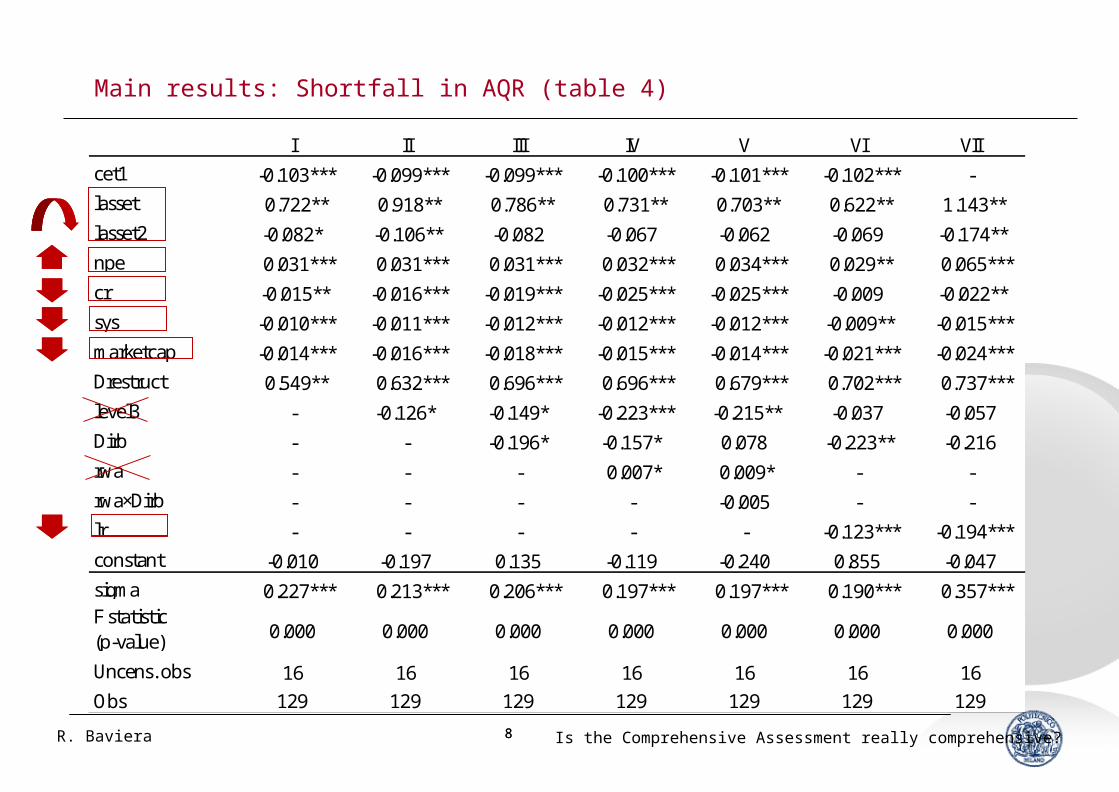

Main results: Shortfall in AQR (table 4)

I II III IV V VI VII

cet1 -0.103*** -0.099*** -0.099*** -0.100*** -0.101*** -0.102*** -

lasset 0.722** 0.918** 0.786** 0.731** 0.703** 0.622** 1.143**

lasset2 -0.082* -0.106** -0.082 -0.067 -0.062 -0.069 -0.174**

npe 0.031*** 0.031*** 0.031*** 0.032*** 0.034*** 0.029** 0.065***

cr -0.015** -0.016*** -0.019*** -0.025*** -0.025*** -0.009 -0.022**

sys -0.010*** -0.011*** -0.012*** -0.012*** -0.012*** -0.009** -0.015***

marketcap -0.014*** -0.016*** -0.018*** -0.015*** -0.014*** -0.021*** -0.024***

Drestruct 0.549** 0.632*** 0.696*** 0.696*** 0.679*** 0.702*** 0.737***

level3 - -0.126* -0.149* -0.223*** -0.215** -0.037 -0.057

Dirb - - -0.196* -0.157* 0.078 -0.223** -0.216

rwa - - - 0.007* 0.009* - -

rwa×Dirb - - - - -0.005 - -

lr - - - - - -0.123*** -0.194***

constant -0.010 -0.197 0.135 -0.119 -0.240 0.855 -0.047

sigma 0.227*** 0.213*** 0.206*** 0.197*** 0.197*** 0.190*** 0.357***F statistic (p-value) 0.000 0.000 0.000 0.000 0.000 0.000 0.000

Uncens. obs 16 16 16 16 16 16 16

Obs 129 129 129 129 129 129 129

99R. Baviera Is the Comprehensive Assessment really comprehensive?

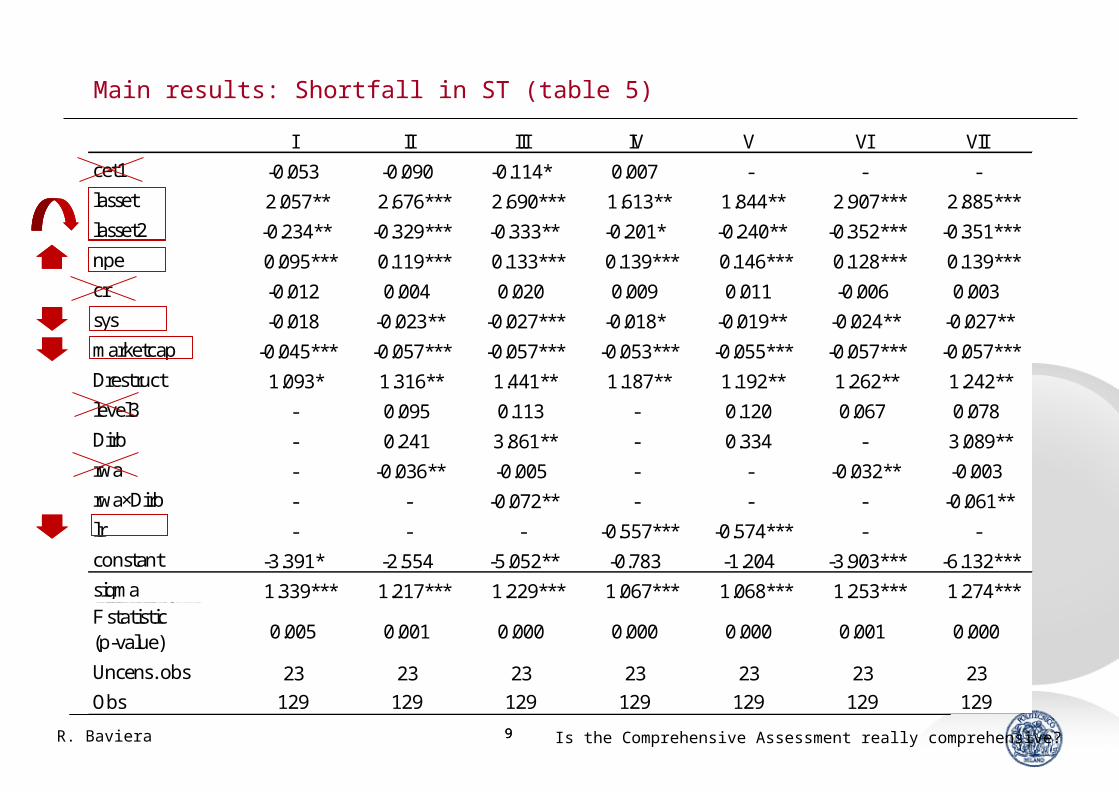

Main results: Shortfall in ST (table 5)

I II III IV V VI VII

cet1 -0.053 -0.090 -0.114* 0.007 - - -

lasset 2.057** 2.676*** 2.690*** 1.613** 1.844** 2.907*** 2.885***

lasset2 -0.234** -0.329*** -0.333** -0.201* -0.240** -0.352*** -0.351***

npe 0.095*** 0.119*** 0.133*** 0.139*** 0.146*** 0.128*** 0.139***

cr -0.012 0.004 0.020 0.009 0.011 -0.006 0.003

sys -0.018 -0.023** -0.027*** -0.018* -0.019** -0.024** -0.027**

marketcap -0.045*** -0.057*** -0.057*** -0.053*** -0.055*** -0.057*** -0.057***

Drestruct 1.093* 1.316** 1.441** 1.187** 1.192** 1.262** 1.242**

level3 - 0.095 0.113 - 0.120 0.067 0.078

Dirb - 0.241 3.861** - 0.334 - 3.089**

rwa - -0.036** -0.005 - - -0.032** -0.003

rwa×Dirb - - -0.072** - - - -0.061**

lr - - - -0.557*** -0.574*** - -

constant -3.391* -2.554 -5.052** -0.783 -1.204 -3.903*** -6.132***

sigma 1.339*** 1.217*** 1.229*** 1.067*** 1.068*** 1.253*** 1.274***F statistic (p-value) 0.005 0.001 0.000 0.000 0.000 0.001 0.000

Uncens. obs 23 23 23 23 23 23 23

Obs 129 129 129 129 129 129 129

1010R. Baviera Is the Comprehensive Assessment really comprehensive?

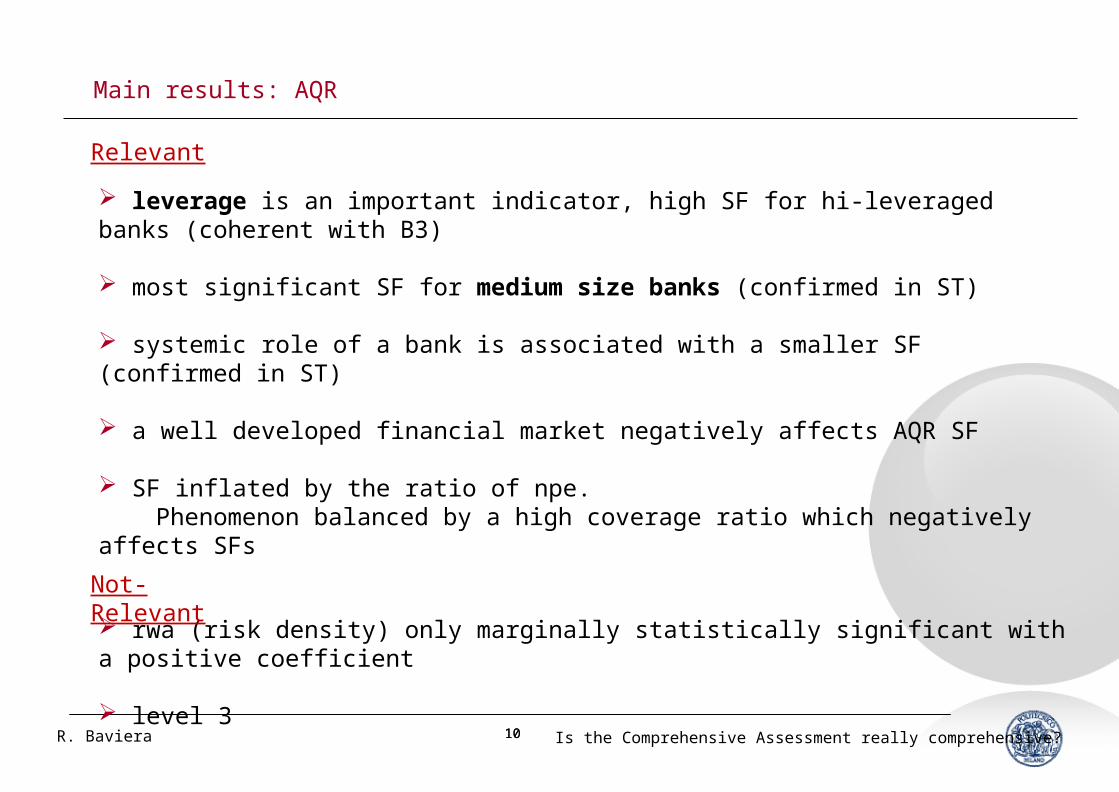

Main results: AQR

leverage is an important indicator, high SF for hi-leveraged banks (coherent with B3)

most significant SF for medium size banks (confirmed in ST)

systemic role of a bank is associated with a smaller SF (confirmed in ST)

a well developed financial market negatively affects AQR SF

SF inflated by the ratio of npe. Phenomenon balanced by a high coverage ratio which negatively affects SFs

rwa (risk density) only marginally statistically significant with a positive coefficient

level 3

Relevant

Not-Relevant

1111R. Baviera Is the Comprehensive Assessment really comprehensive?

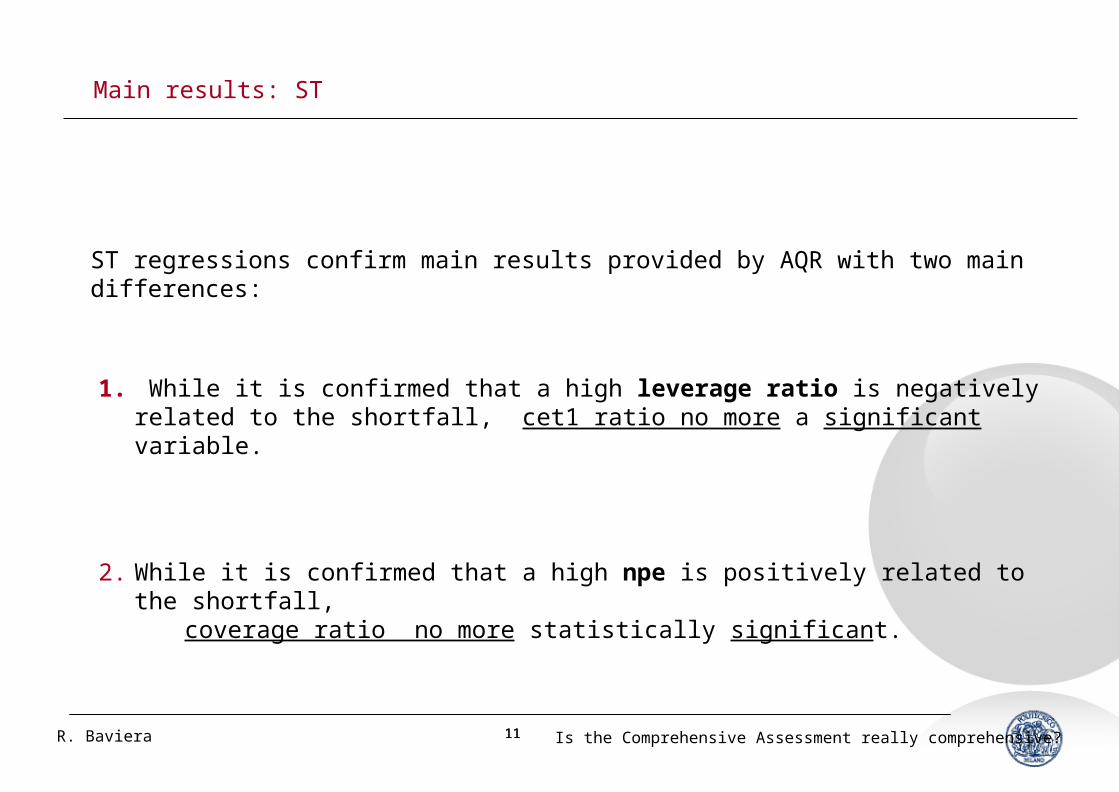

Main results: ST

1. While it is confirmed that a high leverage ratio is negatively related to the shortfall, cet1 ratio no more a significant variable.

2. While it is confirmed that a high npe is positively related to the shortfall, coverage ratio no more statistically significant.

ST regressions confirm main results provided by AQR with two main differences:

1212R. Baviera Is the Comprehensive Assessment really comprehensive?

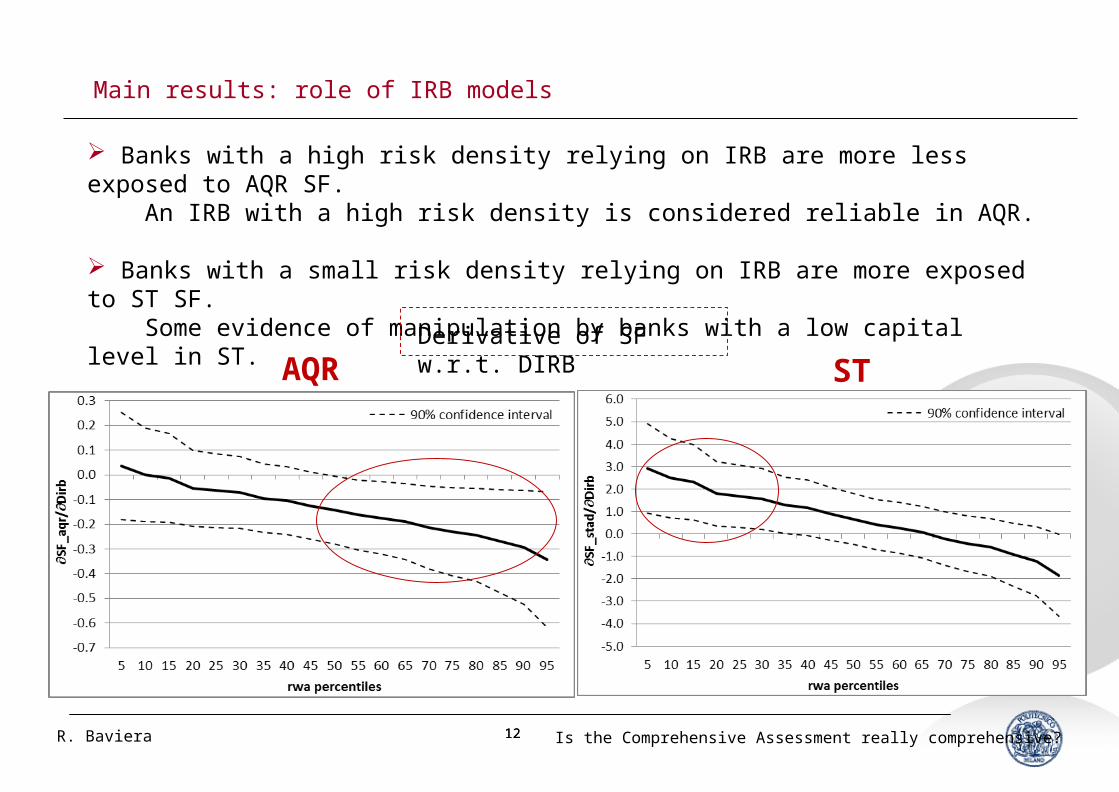

Main results: role of IRB models

Banks with a high risk density relying on IRB are more less exposed to AQR SF. An IRB with a high risk density is considered reliable in AQR.

Banks with a small risk density relying on IRB are more exposed to ST SF. Some evidence of manipulation by banks with a low capital level in ST.

AQR STDerivative of SF w.r.t. DIRB

1313R. Baviera Is the Comprehensive Assessment really comprehensive?

Further results: Home bias

AQR SF is positively & significantly affected by the concentration of the banking activity in the country where the bank is incorporated. Effect mostly concentrated on large banks: for both credit exposure & government bonds (notice that the latter were not part of the review).

Curiously enough, ST SF not affected by the non diversification of the banking activity.

1414R. Baviera Is the Comprehensive Assessment really comprehensive?

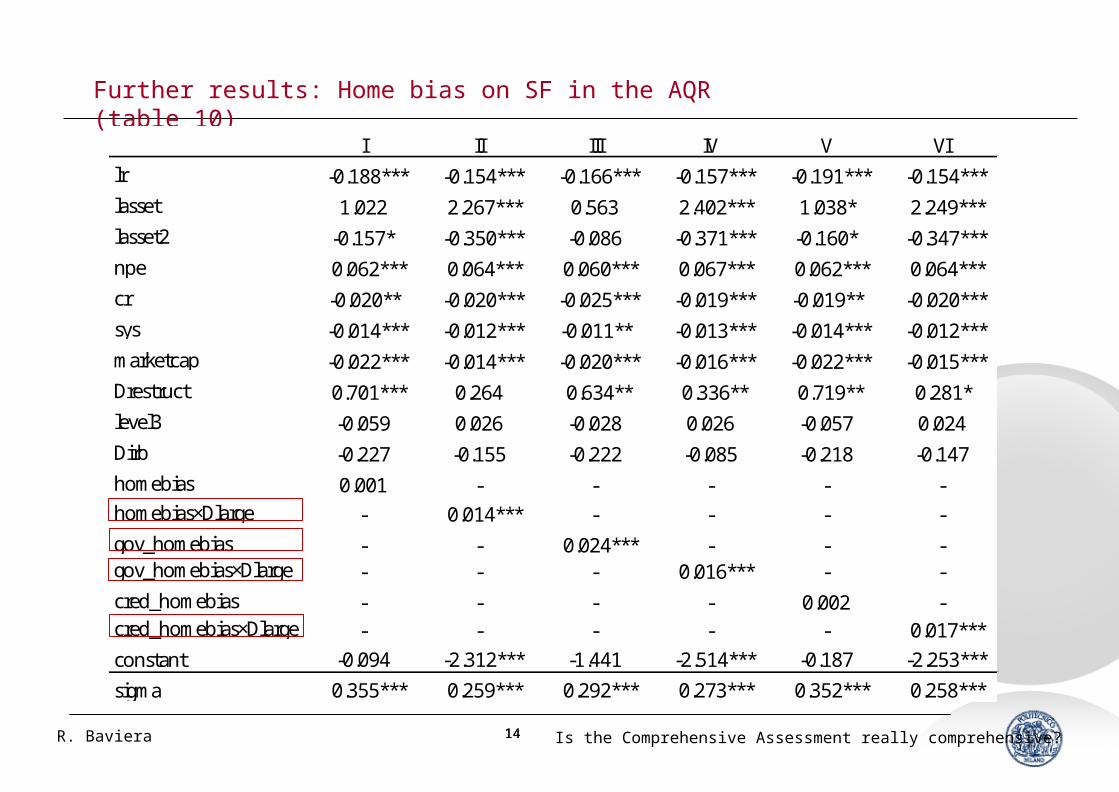

Further results: Home bias on SF in the AQR (table 10)

I II III IV V VI

lr -0.188*** -0.154*** -0.166*** -0.157*** -0.191*** -0.154***

lasset 1.022 2.267*** 0.563 2.402*** 1.038* 2.249***

lasset2 -0.157* -0.350*** -0.086 -0.371*** -0.160* -0.347***

npe 0.062*** 0.064*** 0.060*** 0.067*** 0.062*** 0.064***

cr -0.020** -0.020*** -0.025*** -0.019*** -0.019** -0.020***

sys -0.014*** -0.012*** -0.011** -0.013*** -0.014*** -0.012***

marketcap -0.022*** -0.014*** -0.020*** -0.016*** -0.022*** -0.015***

Drestruct 0.701*** 0.264 0.634** 0.336** 0.719** 0.281*

level3 -0.059 0.026 -0.028 0.026 -0.057 0.024

Dirb -0.227 -0.155 -0.222 -0.085 -0.218 -0.147

homebias 0.001 - - - - -homebias×Dlarge - 0.014*** - - - -

gov_homebias - - 0.024*** - - -gov_homebias×Dlarge - - - 0.016*** - -

cred_homebias - - - - 0.002 -cred_homebias×Dlarge - - - - - 0.017***

constant -0.094 -2.312*** -1.441 -2.514*** -0.187 -2.253***

sigma 0.355*** 0.259*** 0.292*** 0.273*** 0.352*** 0.258***

1515R. Baviera Is the Comprehensive Assessment really comprehensive?

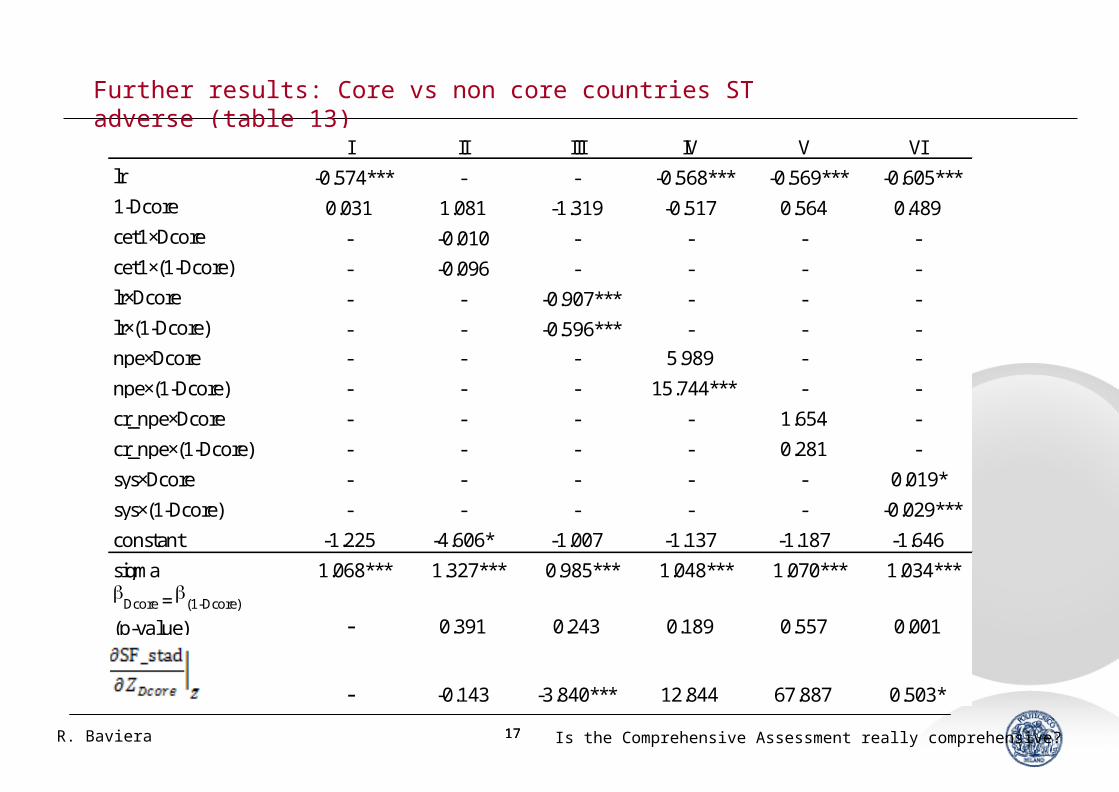

Further results: Core vs non core countries

The dummy DCORE for banks incorporated in the countries:Austria, Belgium, Germany, Finland, France, Luxembourg, Netherland.

DCORE is significant in AQR but not in ST:

AQR SFs are higher in case of a non core country.

ST adverse scenario didn’t penalize non core countries.

This interpretation is confirmed by the interactions between 1-DCORE, DCORE and CET1, LR, NPE, CR, SYS

The coefficients of the interaction with CET1 and LR negative and stat. significant

Higher npe or cr in core countries are associated to a small SF, the opposite non core

1616R. Baviera Is the Comprehensive Assessment really comprehensive?

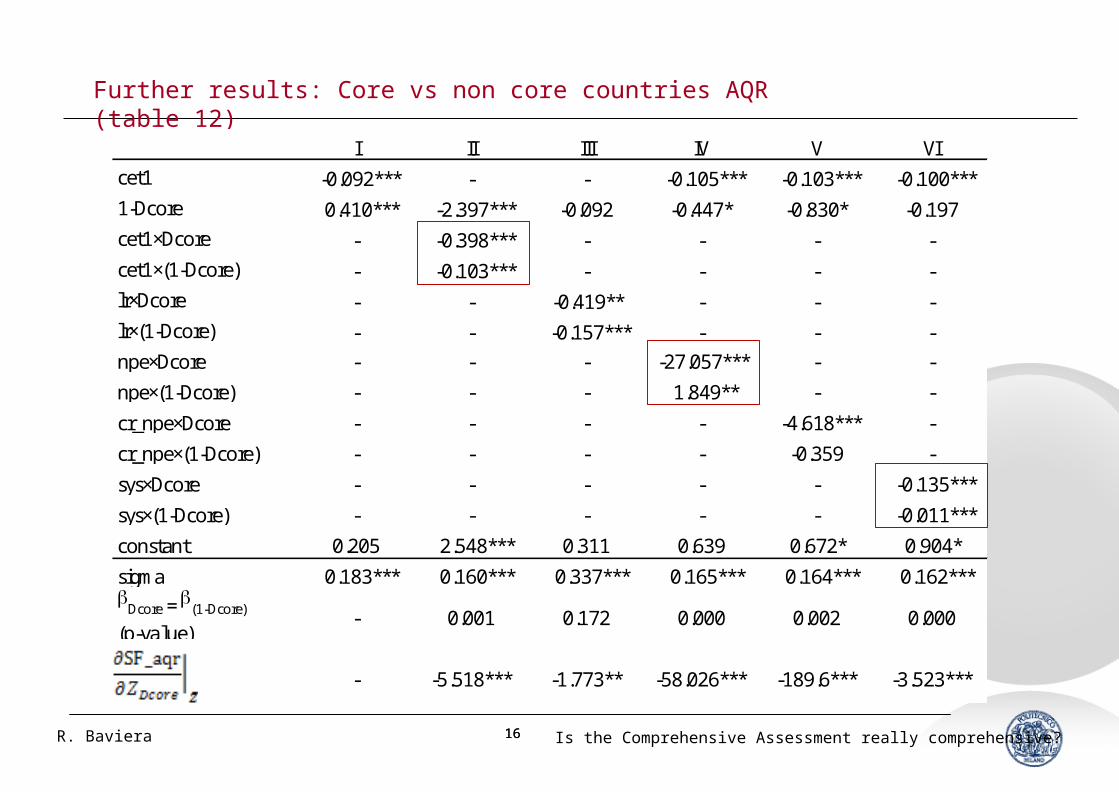

Further results: Core vs non core countries AQR (table 12)

I II III IV V VI

cet1 -0.092*** - - -0.105*** -0.103*** -0.100***

1-Dcore 0.410*** -2.397*** -0.092 -0.447* -0.830* -0.197

cet1×Dcore - -0.398*** - - - -

cet1×(1-Dcore) - -0.103*** - - - -

lr×Dcore - - -0.419** - - -

lr×(1-Dcore) - - -0.157*** - - -

npe×Dcore - - - -27.057*** - -

npe×(1-Dcore) - - - 1.849** - -

cr_npe×Dcore - - - - -4.618*** -

cr_npe×(1-Dcore) - - - - -0.359 -

sys×Dcore - - - - - -0.135***

sys×(1-Dcore) - - - - - -0.011***

constant 0.205 2.548*** 0.311 0.639 0.672* 0.904*

sigma 0.183*** 0.160*** 0.337*** 0.165*** 0.164*** 0.162***bDcore = b(1-Dcore)

(p-value) - 0.001 0.172 0.000 0.002 0.000

- ‐5.518*** ‐1.773** ‐58.026*** ‐189.6*** ‐3.523***

- ‐3.542*** ‐1.054 18.775** ‐16.382 ‐0.552***

1717R. Baviera Is the Comprehensive Assessment really comprehensive?

Further results: Core vs non core countries ST adverse (table 13)

I II III IV V VI

lr -0.574*** - - -0.568*** -0.569*** -0.605***

1-Dcore 0.031 1.081 -1.319 -0.517 0.564 0.489

cet1×Dcore - -0.010 - - - -

cet1×(1-Dcore) - -0.096 - - - -

lr×Dcore - - -0.907*** - - -

lr×(1-Dcore) - - -0.596*** - - -

npe×Dcore - - - 5.989 - -

npe×(1-Dcore) - - - 15.744*** - -

cr_npe×Dcore - - - - 1.654 -

cr_npe×(1-Dcore) - - - - 0.281 -

sys×Dcore - - - - - 0.019*

sys×(1-Dcore) - - - - - -0.029***

constant -1.225 -4.606* -1.007 -1.137 -1.187 -1.646

sigma 1.068*** 1.327*** 0.985*** 1.048*** 1.070*** 1.034***bDcore = b(1-Dcore)

(p-value) - 0.391 0.243 0.189 0.557 0.001

- ‐0.143 ‐3.840*** 12.844 67.887 0.503*

- 0.020 ‐4.977*** 163.150*** 12.734 ‐0.428

1818R. Baviera Is the Comprehensive Assessment really comprehensive?

Is the CA really comprehensive?

CA weaknesses on the market side

Inadequate information set

Valuation of Level 3 assets

Off balance sheet items

Methodology

PD & LGD impacts only on CVA

1919R. Baviera Is the Comprehensive Assessment really comprehensive?

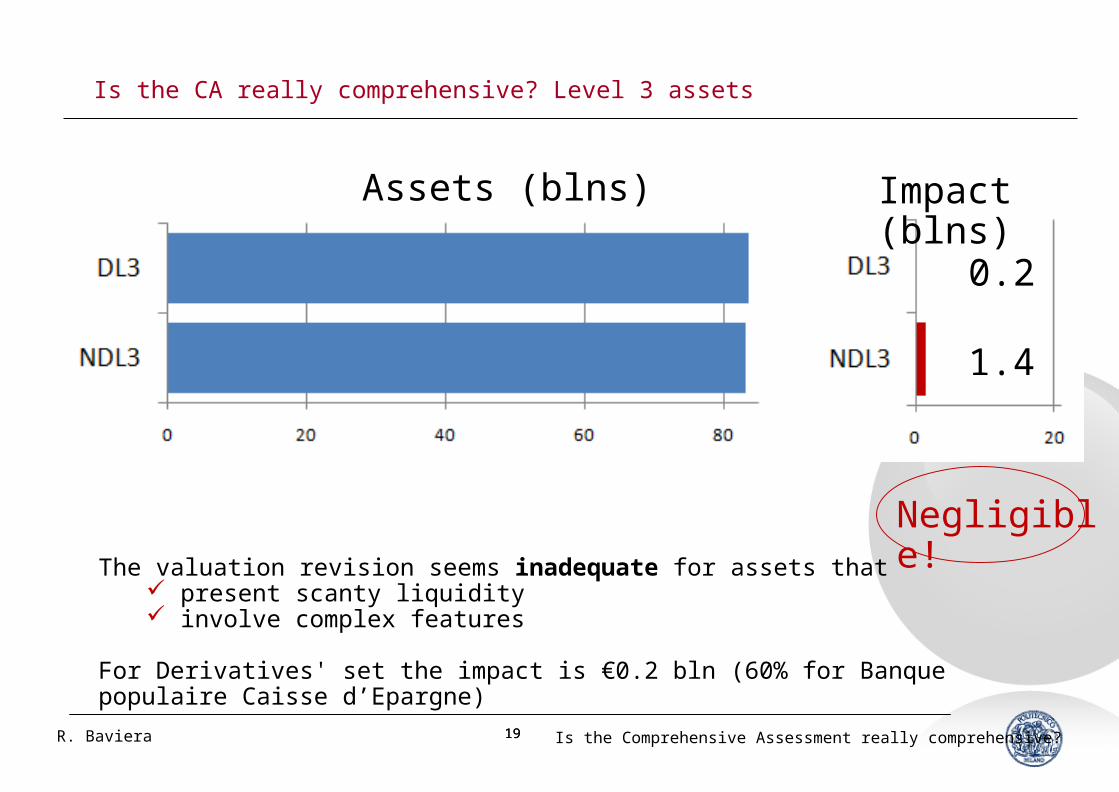

Is the CA really comprehensive? Level 3 assets

0.2

1.4

The valuation revision seems inadequate for assets that present scanty liquidity involve complex features

For Derivatives' set the impact is €0.2 bln (60% for Banque populaire Caisse d’Epargne)

Assets (blns) Impact (blns)

Negligible!

2020R. Baviera Is the Comprehensive Assessment really comprehensive?

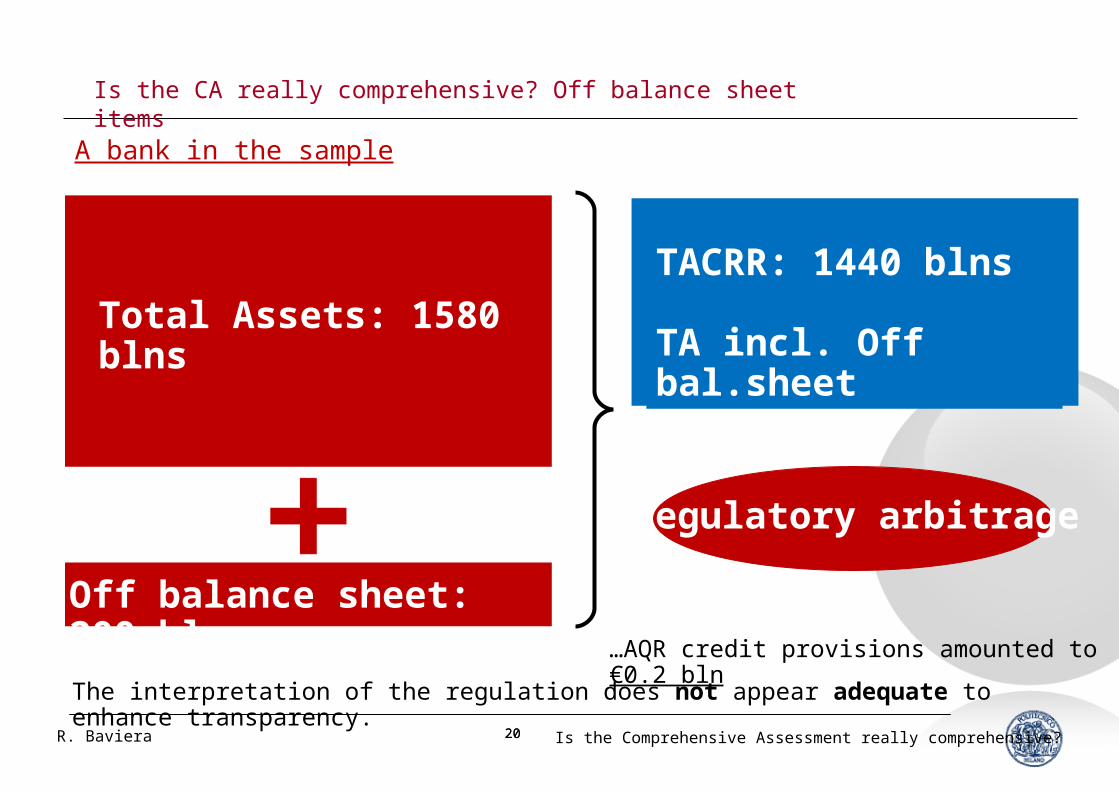

Is the CA really comprehensive? Off balance sheet items

A bank in the sample

Off balance sheet: 200 blns

Total Assets: 1580 blns

TACRR: 1440 blns

TA incl. Off bal.sheet

…AQR credit provisions amounted to €0.2 bln

The interpretation of the regulation does not appear adequate to enhance transparency.

Regulatory arbitrage

2121R. Baviera Is the Comprehensive Assessment really comprehensive?

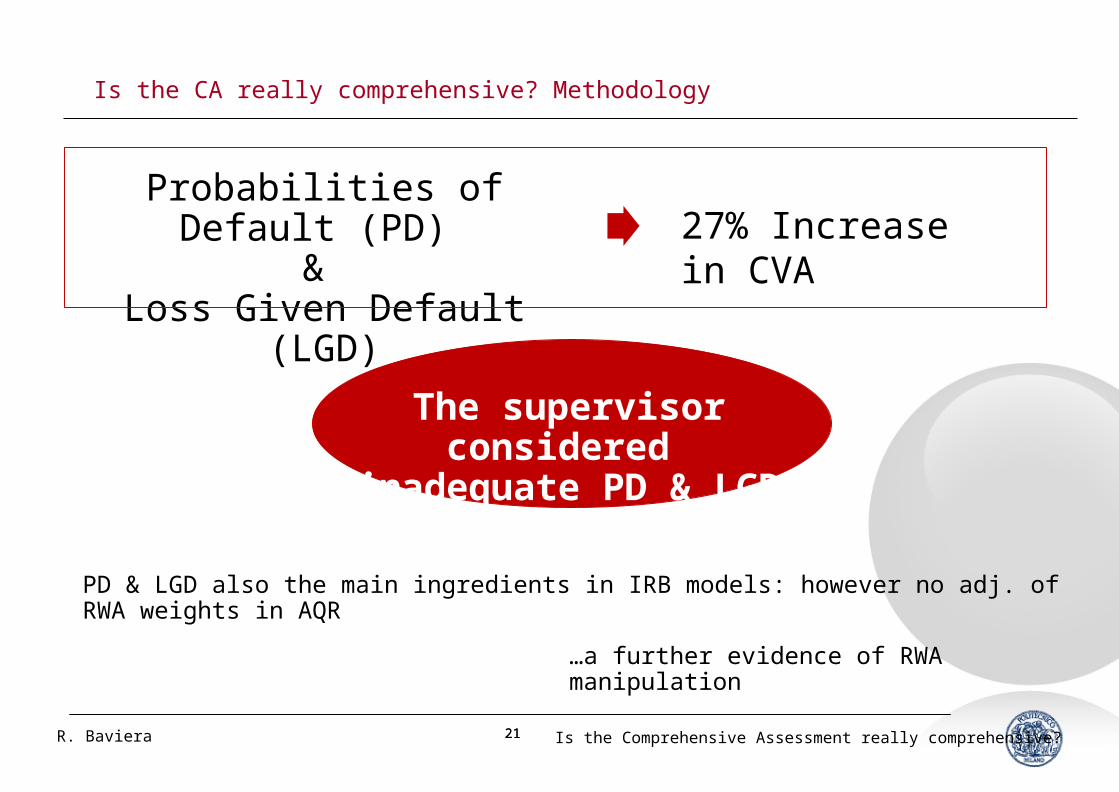

Is the CA really comprehensive? Methodology

Probabilities of Default (PD)

& Loss Given Default (LGD)

27% Increase in CVA

PD & LGD also the main ingredients in IRB models: however no adj. of RWA weights in AQR

The supervisor considered

inadequate PD & LGD

…a further evidence of RWA manipulation

2222R. Baviera Is the Comprehensive Assessment really comprehensive?

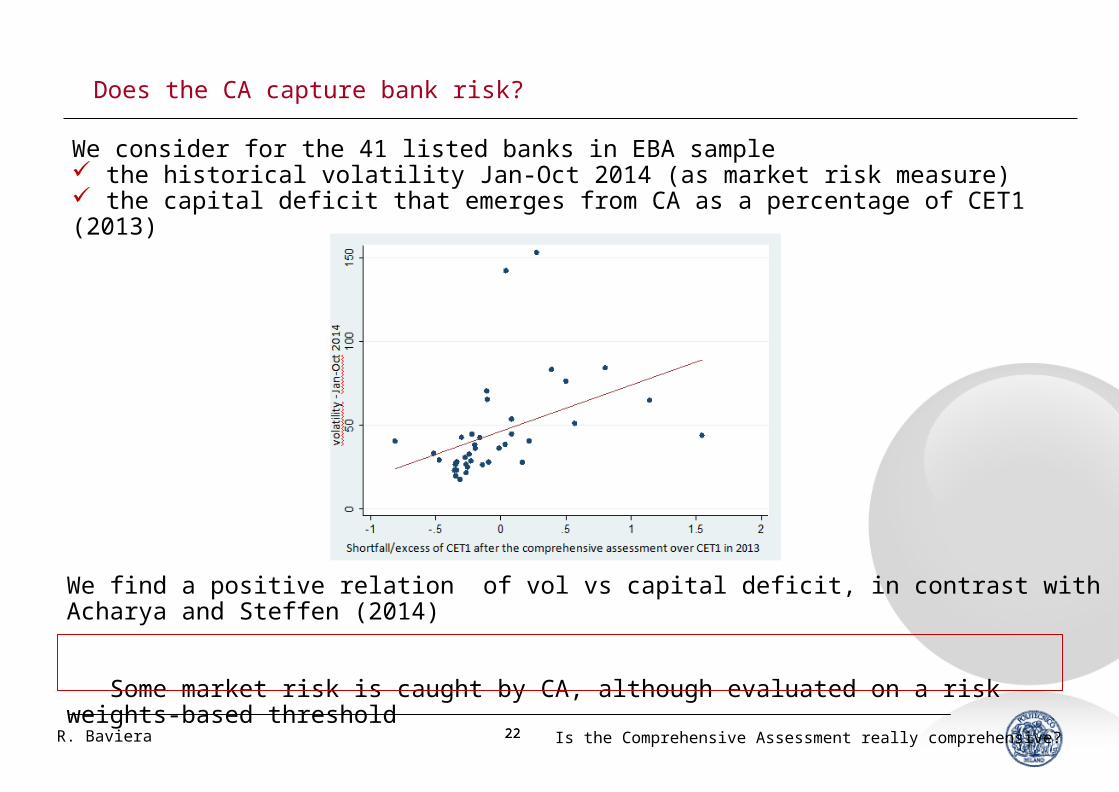

Does the CA capture bank risk?

We consider for the 41 listed banks in EBA sample the historical volatility Jan-Oct 2014 (as market risk measure) the capital deficit that emerges from CA as a percentage of CET1 (2013)

We find a positive relation of vol vs capital deficit, in contrast with Acharya and Steffen (2014)

Some market risk is caught by CA, although evaluated on a risk weights-based threshold

2323R. Baviera Is the Comprehensive Assessment really comprehensive?

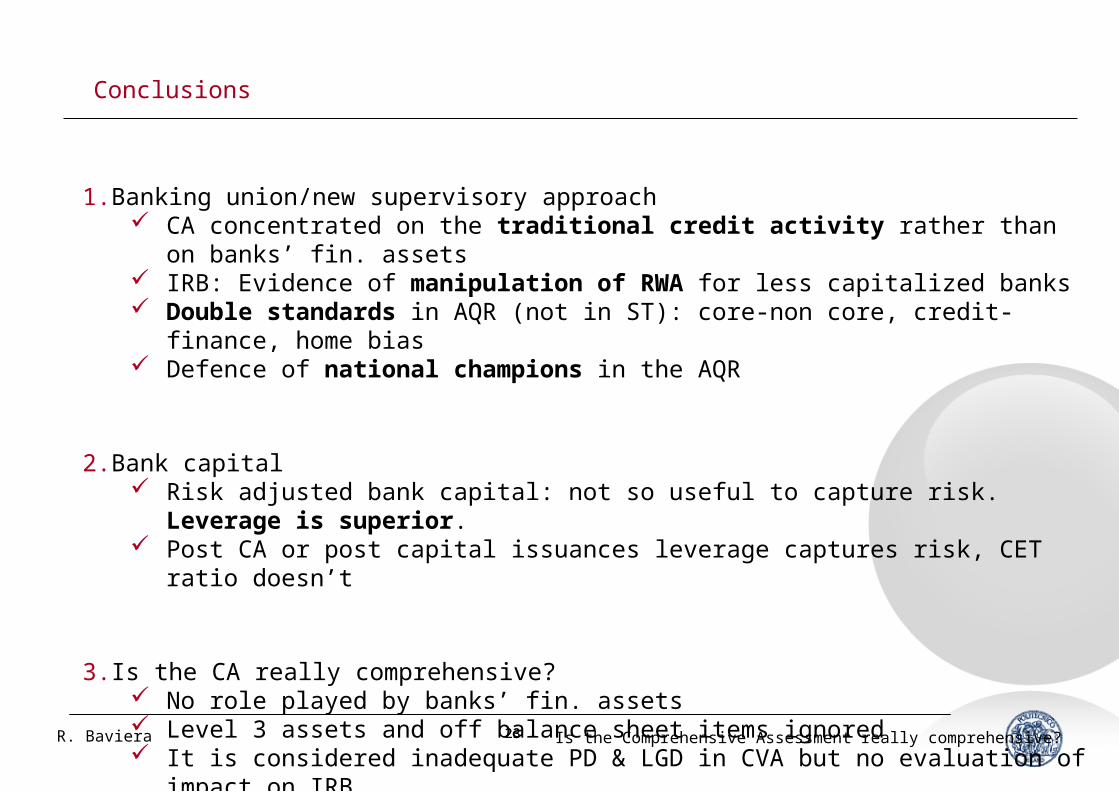

Conclusions

1.Banking union/new supervisory approach CA concentrated on the traditional credit activity rather than on banks’

fin. assets IRB: Evidence of manipulation of RWA for less capitalized banks Double standards in AQR (not in ST): core-non core, credit-finance, home

bias Defence of national champions in the AQR

2.Bank capital Risk adjusted bank capital: not so useful to capture risk. Leverage is

superior. Post CA or post capital issuances leverage captures risk, CET ratio doesn’t

3.Is the CA really comprehensive? No role played by banks’ fin. assets Level 3 assets and off balance sheet items ignored It is considered inadequate PD & LGD in CVA but no evaluation of impact on

IRB CA captures some risk: capital shortfall is related to market volatility

2424R. Baviera Is the Comprehensive Assessment really comprehensive?

Bibliography sketch

[1] V. Acharya, R. Engle & M. Richardson (2014) Testing macroprudential stress tests: the risk of regulatory risk weights, Journal of Monetary Economics, 65: 36-53

[2] V. Acharya & S. Steffen (2014) Benchmarking the European Central Bank’s asset quality review and stress test: a tale of two leverage ratios, VOX, November 2014

[3] E. Barucci, R. Baviera & C. Milani (2014) Is the Comprehensive Assessment Really Comprehensive?, Available at ssrn.com/abstract=2541043

[4] J.R. Barth, G. Caprio & R. Levine (2001) The regulation and supervision of banks around the world - a new database, World Bank Policy Research Working Paper 2588.

[5] F. Cannata, S. Casellina & G. Guidi (2012) Inside the labyrinth of Basel risk weighted assets: how not to get lost, Bank of Italy, occasional paper nr. 132

[6] European Banking Authority (2013) Interim results update of the EBA review of the consistency of risk weighted assets, available on http://goo.gl/IeNuwX

[7] A. Haldane (2011) Capital discipline, Bank of England, mimeo

[8] V. Le Leslé & S. Avramova (2012) Revisiting risk-weighted assets, IMF working paper, 12/90

[9] M. Mariathasan & O. Merrouche (2014) The manipulation of Basel risk-weights, Journal of Financial Intermediation, 23: 300-321