1 IS 8950 Building the Network Economy: Markets and Models.

37

1 IS 8950 Building the Network Economy: Markets and Models

-

date post

21-Dec-2015 -

Category

Documents

-

view

222 -

download

0

Transcript of 1 IS 8950 Building the Network Economy: Markets and Models.

1

IS 8950

Building the Network Economy: Markets and Models

2

Creating Business Advantage with IT

3

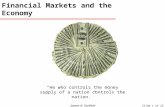

20th Century Technology, Business, and Societal Evolution

1900 1950 2000

AgriculturalEconomy

IndustrialEconomy

InformationEconomy

Typical mathematical formula:D=B2-4AC

Equivalent FOR TR AN statement:D=B**2-4*A*CTelegraph

Technology Evolution

Social and Business Evolution

Photos reprinted with permission from AT&T and IBM

4

Technological Changes at the verge of the 21st Century

• The Internet and broadband networks– Low cost, standardized, global alternatives

• Old: expensive, specialized, and proprietary– Enable the transmission of multimedia digital information on a common communication

channel• The WWW and high-performance servers

– Flexible, standardized, powerful platforms for creating and storing information in all its forms (text, data, voice, and video)

• The Uniform Resource Locator (URL) and browser– Common approaches for identifying and locating information anywhere on the Internet and

easy-to-use tools for accessing, packaging, and displaying multimedia information• Multimedia digital devices

– Portable Internet access devices that provide a single point of entry to voice, television, and information (laptops, palm pilots, interactive TV set-top boxes, and game consoles).

• Wireless networks and protocols– Technology and supporting business infrastructure to enable access to the Internet,

untethered by physical wires• Object-oriented programming language and database technologies (Java, Jini, XML)

– Powerful new approaches to developing information systems that take full advantage of the flexibility, modularity, connectivity, and multimedia features of the Internet.

5

Before and After the “bubble”

• 1999, $32 billion (90% of the total invested by venture capitalists) invested in technology

• 2nd Quarter 2000 investment only 3%• Companies with valuation in excess of $1 billion

went out of business• 1/2000 – 1/2002: over 780 Internet firms went

out of business• By 2001 established firms began to take

advantage of the decreased strength of new entrants

6

Frameworks for analyzing the impact of IT on Strategy

• Value Chain Analysis

• Industry and Competitive Analysis (the five forces)

• The three generic strategies

• Strategic Grid Analysis

7

Value Chain Analysis

• For identifying and analyzing the stream of activities through which products and services are created and delivered to customers

• Evaluate the cost incurred and value created• Economies of scale: leverage capabilities and

infrastructure to increase revenues and profitability within a single product line or market

• Economies of scope: leverage capabilities and infrastructure to launch new product lines or business or enter new markets

8

9

Industrial vs. Networked Economy

Industrial Networked

Production and distribution technology

Machines, railroads, steam engines, telephones

Broadband networks, wireless networks, multimedia content creation, flexible/real-time knowledge access & management

Operating model The assembly line, marketing, sales, and after-sales service channels

Integrated supply chains and buy chains

Management model Hierarchy Teams, partnerships, consortia

Social/regulatory system Specialized work, pay-for-performance incentives, worker education, unions, antitrust laws

Ownership incentives, freelancing, virtual work, distance learning, digital copyright laws

10

Market Roles

11

Comparing Industrial and Information Economy

Characteristics Industrial Economy Network Economy

Criteria for Economic Success Internal, proprietary, and specialized economies of scale, and scope; Economies of scope are limited by the level of infrastructure specialization required

External, networked, and shared economies of scale and scope; Economies of scale and scope are dramatically increased by the ability to build new businesses on the non-proprietary, flexible, shared, and ubiquitous Internet infrastructure

Technological Innovations Production, communication, and distribution technologies

Distribution, communication, and information technologies; the ability to “assemble” component pieces

Operating Innovations Standardization of work; job specialization; assembly line operations; value chain industry structure

Knowledge work; job expansion; work teams (face-to-face and virtual); extended enterprise; outsourcing and partnerships; value networks

Management Innovations Hierarchical coordination and supervision; compliance-based control; pay-for-performance incentives; centralized planning & control

Networked coordinating and supervision; ownership incentives; information-based (“learning”) models of control; distributed planning and control

Societal/Regulatory Innovations Urban growth; mass transportation; social security and welfare; unions, federal regulations; domestic economy

Work-at-home; self-employment; personal pension and savings programs; global economy

Length of Time to Achieve Economies of Scale and Scope

Decades Uncertain

Dominant Industry Power Producers Solution assemblers and channel managers

12

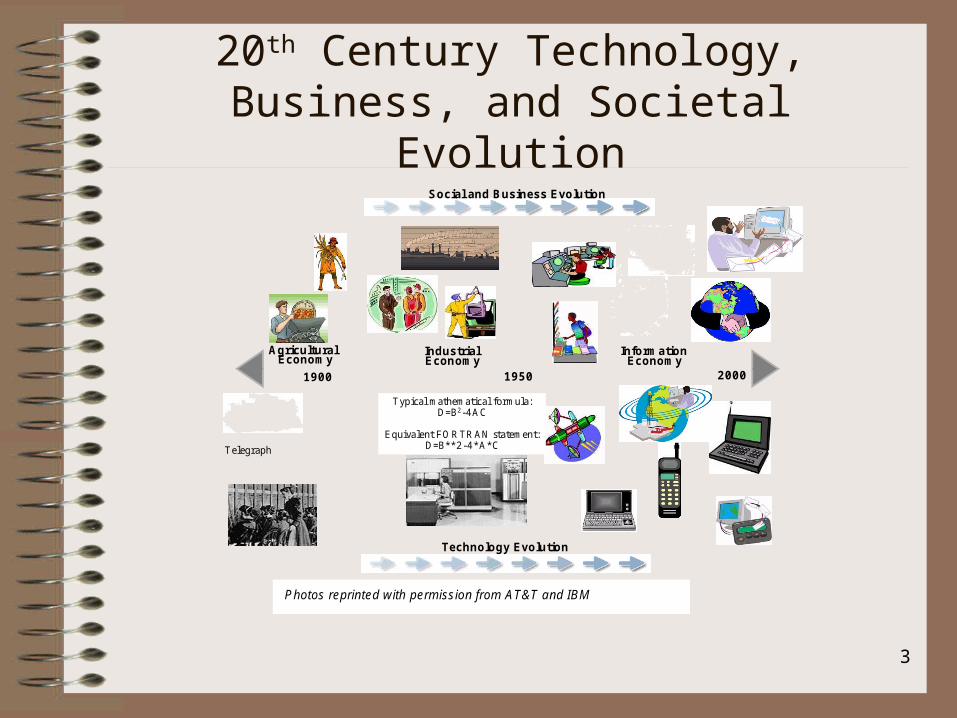

Industry and Competitive Analysis

• The five basic forces:1. Bargaining power of suppliers

2. Bargaining power of buyers

3. Threat of new entrants

4. Threat of substitute products or services

5. Competitive intensity and positioning among traditional business rivals

13

Forces influencing industry and competitive advantage

14

Generic Strategies

• 3-strategies to achieve proprietary advantage within industry:– Cost leadership

– Differentiation

– Focus

• Key questions in each generic strategy:– Should we lower cost or differentiate our products and

services?

– Should we target a broad market or a narrow one?

15

Generic Strategies

Competitive Scope

Cost leadership

Cost focus

Differentiation

Differentiation focus

Broad Target

Lower Cost Differentiation

Narrow Target

Competitive Advantage

16

Strategic Grid Analysis

Factory Strategic

Support Turnaround

Goal: Improve performance of core processes

Leadership: Business unit executives

Project Management: Process reengineering

Goal: Improve local performance

Leadership: Local level oversight

Project Management: Grassroots experimentation

Goal: Transform organization or industry

Leadership: Senior executives & board

Project Management: Change management

Goal: I dentify and launch new ventures

Leadership: Venture incubation unit

Project Management: New venture development

IT Impact on Core Strategy

IT Im

pac

t o

n C

ore

Op

erat

ion

s

Low

High

High

17

Source: Source: McFarlanMcFarlan, Warren F., , Warren F., Tale of Two Airlines in the Information Age: Or Why the Spirit oTale of Two Airlines in the Information Age: Or Why the Spirit of King f King George III is Alive and Well !George III is Alive and Well ! Teaching Note, Copyright © 1995 President and Fellows Harvard CTeaching Note, Copyright © 1995 President and Fellows Harvard Collegeollege

STRATEGIC IMPACTSTRATEGIC IMPACT——APPLICATIONS DEVELOPMENT APPLICATIONS DEVELOPMENT PORTFOLIOPORTFOLIO

Strategic

Dependence

Existing

Operating

Systems

A - Major Electronic Components Firms

B - Major Brokerage

C - Large Agricultural Firm

E - Major Airline

F - Major Consulting Organization

G - Insurance Broker

StrategicFactory

Support Turnaround

High

Low High

A

CG

BE

F

Tale of Two Airlines TN, Slide 5 of 6Tale of Two Airlines TN, Slide 5 of 6

18

Analyzing the Impact of IT on Strategic Decision Making

• Can IT be used to reengineer core value activities and change the bases of competition?

• Can IT change the nature of relationships and the balance of power among buyers and suppliers?

• Can IT build or reduce barriers to entry?• Can IT increase or decrease switching costs?• Can IT add value to existing products and

services or create new ones?

19

Can IT be used to reengineer core value activities and change the bases of competition?

• IT systems are used to automate activities• 1950s and 1960s automate routine, information-intensive “back-office”

transactions (payroll processing, accounting, and general ledger postings).• Apply benefits to “front-office” activities (transactions for suppliers,

distributors, customers, and other value chain participants).• Increased benefits when IT is used to transform and inform• Streamlined and integrate value chain to eliminate redundancies, reduce

cycle times, and achieve greater efficiency and productivity.• American Hospital and Supply Corporation (AHSC) and American Airlines

(AA)– Used IT to fundamentally alter the basis of competition in their respective

industry;– Strategies that radically changed the cost structure

• Charles Schwab – Fundamentally changed the basis of competition

20

Can IT change the nature of relationships and the balance of power among buyers and suppliers?

• AHSC increased speed of fulfillment between suppliers and hospital buyers

• Suppliers succumbed to the pressure to put their catalogs online and join the electronic market

• Customers encouraged channel consolidation, unwilling to put up with the problems of using different supplier systems

• Chemdex established a neutral, third-party virtual marketplace for life sciences industry

• Global Healthcare Exchange (GHX); increased the bargaining power of suppliers

• Group Purchasing Organizations (GPOs); health care providers

21

Can IT build or reduce barriers to entry?

• AHSC and AA built and operated a proprietary system; for example, other airlines were forced to tie to the dominant force

• Overtime technology-based advantages decreased• Sustainable advantages are found in second-order barriers

– Exploiting the value information generated by the technology and the value of the community of suppliers, customers, and partners

• Internet technologies provide lower entry barriers in the online market– “knowledge and community barriers” provide a more sustainable entry

barrier within Internet-based electronic markets– Example: Amazon.com

• Order fulfillment capability with 99% on-time delivery• Attracts over 25 million customers• Shift from pure-play e-retailer to an online/offline logistics services provider

22

Can IT increase or decrease switching costs?

• To provide a sustainable source of revenues, an IT system ideally should be easy to start using but difficult to stop using

• Switching costs are substantially reduced, – easy to compare prices – difficult to achieve strong customer loyalty

• Intuit: avoid switching by storing personal information, switching requires re-entering

• Online bill paying service: integrate many services to avoid switching

23

Can IT add value to existing products and services or create new ones?

• Grocery stores: add the business of selling information; – sale scanner data on consumer shopping behavior

• Information content of products; a 2000 late model car has more computer chips than the U.S. National Defense Department in 1960; – Provide mechanics and manufacturers with driving

behaviors

• Transform products from analog to digital– Books, magazines, music, video, and games

24

Crafting Business Models

25

Business models

• Network economy business models– Portals– Aggregators– Exchanges– Marketplaces

• Describes how a company made money and delivered value to customers, suppliers, partners, employees, and owners

– How is a software developer going to make money in the growing pressure to go to Open Source: Linux (Windows), Open Office (MS Office), GIMP (Photoshop)

• Industrial economy: “I sell insurance” or “I sell cars”; describes how a business was structured, what types of people were needed, and what roles they filled.

• Building blocks:– Concepts– Capabilities– Value

26

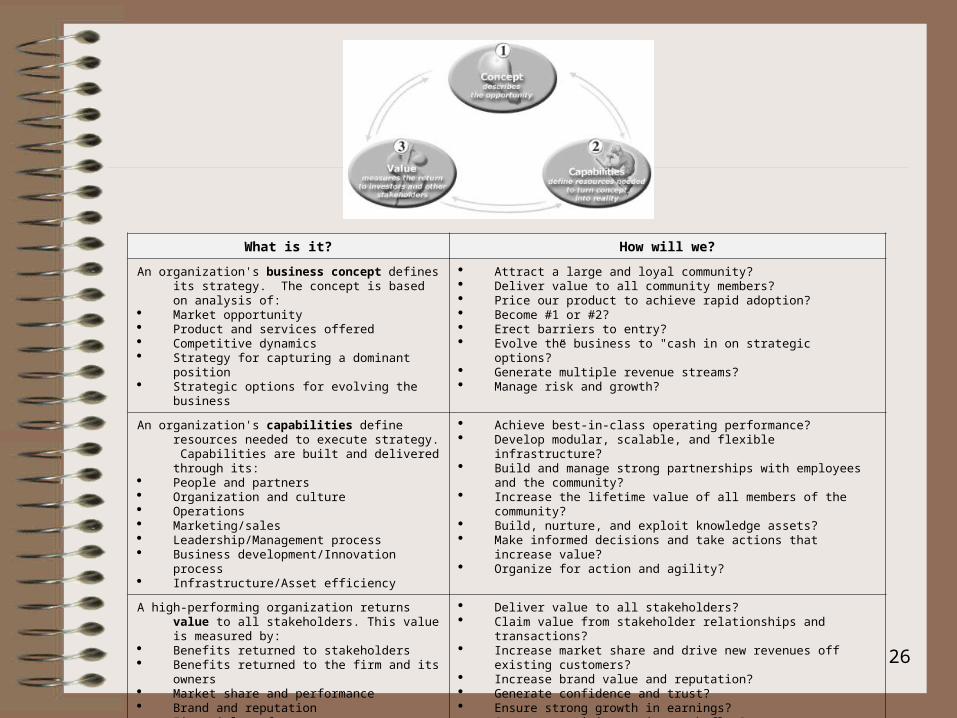

What is it? How will we?

An organization's business concept defines its strategy. The concept is based on analysis of:

Market opportunity Product and services offered Competitive dynamics Strategy for capturing a dominant position Strategic options for evolving the business

Attract a large and loyal community? Deliver value to all community members? Price our product to achieve rapid adoption? Become #1 or #2? Erect barriers to entry? Evolve the business to "cash in on strategic options?” Generate multiple revenue streams? Manage risk and growth?

An organization's capabilities define resources needed to execute strategy. Capabilities are built and delivered through its:

People and partners Organization and culture Operations Marketing/sales Leadership/Management process Business development/Innovation process Infrastructure/Asset efficiency

Achieve best-in-class operating performance? Develop modular, scalable, and flexible infrastructure? Build and manage strong partnerships with employees and the

community? Increase the lifetime value of all members of the community? Build, nurture, and exploit knowledge assets? Make informed decisions and take actions that increase value? Organize for action and agility?

A high-performing organization returns value to all stakeholders. This value is measured by:

Benefits returned to stakeholders Benefits returned to the firm and its owners Market share and performance Brand and reputation Financial performance

Deliver value to all stakeholders? Claim value from stakeholder relationships and transactions? Increase market share and drive new revenues off existing customers? Increase brand value and reputation? Generate confidence and trust? Ensure strong growth in earnings? Generate positive equity cash flow? Increase stock price and market value?

27

Users and Providers of Network

• Two key value chain roles:– Producers: design and build products and services

– Distributors: enable buyers and sellers to connect, communicate, and transact

28

Network Users—Focused Distributors Model

Model & Examples Model Differentiators Likely Revenues

Likely Costs

Own Inv. Sell online Price Set Online

Physical Product orService

RetailerToysRus.comStaples.com

Yes Yes No Yes Product/svc. sales

Advertising & marketing; Physical facilities, inventory & customer svc.; R&D; IT infrastructure

MarketplaceEloan.com InsWeb.com

Possibly Yes No No Transaction fees; Service fees; Commissions

Advertising & marketing; R&D; IT infrastructure

AggregatorAutoweb.com

No No No Possibly Referral fees;Advertising & marketing fees

Advertising & marketing; R&D; IT infrastructure

InfomediaryInternet Securities

No Yes Yes No Subscription fees; Advertising fees

Advertising & marketing; R&D; IT infrastructure; content acquisition

ExchangeeBay.comFreemarkets.com

Possibly Possibly Yes Possibly Depends on model

Advertising & marketing; Staff support for auctions (especially B-2-B); Inventory & logistics if inventory control; R&D; Technical infrastructure

Focused Distributor Business Model Trends Focused distributors that do not allow customers and the business community to transact business online are losing power. Aggregators are evolving to marketplaces and/or vertical portals. Multiple business models are required to ensure flexibility and sustainability. Focused distributors are aligning closely with vertical and horizontal portals or are evolving their model to become vertical portals.

29

Network Users—Portal Business Model

Model & Examples Model Differentiators Likely Revenues Likely Costs

Gateway Access

Deep Content & Solutions

Affinity Group Focus

Horizontal PortalsAOL.comYahoo!.comQuicken.com Small Business

Yes Through partnerships

with vertical & affinity portals

Possibly; Often through

partnerships

Advertising, affiliation & slotting fees; Possibly subscription or access fees

Advertising, marketing & sales; Content/info asset mgmt.; R&D; IT infrastructure

Vertical PortalsWebMD.com Covisint.com

Limited Yes No Transaction fees; Commissions; Advertising, affiliation & slotting fees

Advertising, marketing & sales; Content/info asset mgmt.; R&D; IT infrastructure; Legacy system integration to support transactions

Affinity PortalsRealtor.com iVillage.com

Possibly Focused on affinity group

Yes Referral fees;Advertising, affiliation & slotting fees

Advertising, marketing & sales; Content/info asset mgmt.; R&D; IT infrastructure

Portal Business Model Trends:Horizontal and vertical portals are emerging as dominant sources of power within consumer and business markets. Horizontal portals are joining forces with horizontal infrastructure portals to provide, not just access to content and services, but also access to network and hosting services. Large media and entertainment portals that represent convergence of data, telephone, television, and radio networks are emerging in the consumer space. These portals unite content development, packaging, and distribution components of the value chain. B2B portals provide both horizontal access to business networks and vertical industry-wide solutions.

30

Network Users—Producer Business ModelModel & Examples Model Differentiators Likely Revenues Likely Costs

Sell Physical Product/ Service

Sell Information-

based Product/ Service

Level of Customiza

tion

ManufacturersFord Motor Company Procter & Gamble

Yes Possibly Low to Moderate

Product sales; Service fees Advertising, marketing & sales; Content/info asset mgmt.; R&D; IT infrastructure

Service ProvidersAmerican Express Singapore Airlines

Yes Possibly Moderate to High

Commission, service or transaction fees;

Advertising, marketing & sales; Content/info asset mgmt.; R&D; IT infrastructure

EducatorsHarvard University Virtual University

Possibly Possibly Moderate to High

Registration or event fee; Subscription fee; Hosting fee

Content/info asset mgmt.; R&D;

IT infrastructure

AdvisorsMcKinsey Accenture

Yes Yes Moderate to High

Service fee; Registration or event fee; Membership fee; Commission, transaction or subscription fee

Content/info asset mgmt.; IT infrastructure

Information & News ServicesDow Jones Euromoney

Yes Yes Moderate to High

Subscription fee; Commission, transaction or service fee

Content/info asset mgmt.; Advertising, marketing & sales;

IT infrastructure

Producer PortalsCovisint Global Healthcare Exchange

Possibly Yes High Transaction or service fee; Subscription or membership fee;Consulting and Integration fee; Hosting Fee

Content/info asset; IT Infrastructure and

R&D; software development; Logistics

Producer Business Model TrendsProducers must be best-in-class – the #1 or #2 brand – to survive. Some large full service producers, like American Express and Citigroup in the financial services industry, and AOL Time Warner in the entertainment and media industry, are acquiring a full range of products and services and then integrating them to provide vertical solutions required by customers. These are offered through company-owned portals and also through a wide variety of distribution agreements. Industry supplier coalitions are forming to enable virtually-integrated business-to-business commerce within and across industry groups.

31

Infrastructure Providers—Distributor Model

Models & Examples Model Differentiators Likely Revenues

Likely Costs

Control Inventory

Sell Online Price Set Online

Physical Product or

Service

Infrastructure RetailersCompUSA.com Egghead

Yes Yes Not usually Yes Product sales; Service fees

Advertising & marketing; Physical facilities, inventory &

customer svc.; R&D; IT infrastructure

Infrastructure MarketplacesIngram Micro Tech Data

Usually Yes Not usually, but may be customized

Yes Transaction fees; Service

fees; Commission;

Channel assembly fee

Advertising & marketing; R&D; IT

infrastructure

Infrastructure AggregatorsC/Net ZD Net

No No No Possibly Referral fees;Advertising &

marketing fees

Advertising & marketing; R&D; IT

infrastructure

Infrastructure ExchangesConverge

Possibly Possibly Yes Yes Depends on model

Advertising & marketing; Staff support for auctions (especially

B-2-B); Inventory & logistics if inventory

control; R&D; Technical infrastructure

Infrastructure Distributor Business Model Trends:The speed of obsolescence of the technology, coupled with the complexity of the solution and slim margins, has forced massive consolidation in network and computing technology channels. For many, service revenues are driving profitability. Those distributors that take ownership of inventory are searching for inventory-less, just-in-time business models. Distributors that have the capability for custom configuration of products and services are gaining power.

32

Infrastructure Providers—Portal Model

Models & Examples Model Differentiators Likely Revenues Likely Costs

Internet/Network Access and

Hosting

Hosted Applications and

Solutions

Horizontal Infrastructure PortalsAmerica OnlineBritish TelecomDigex

Yes Through partnerships with non-infrastructure

portals & ASPs

Access fees; Commission, service or transaction fees; Subscription fees; Hosting

fees

R&D; IT infrastructure; Advertising, marketing and

sales

Vertical Infrastructure Portals IBM E-Business SolutionsGE Global eXchange Services

Often through partnerships with

horizontal infrastructure portals

Yes Licensing fees; Service & transaction fees;

Maintenance & update fees; Hosting fees

Advertising, marketing & sales; Content/info asset mgmt.; R&D;

IT infrastructure

Infrastructure Portal Business Model TrendsHorizontal infrastructure portals (ISPs, Network Service Providers, and Web Hosting Providers) are merging or partnering with horizontal content portals to increase value created through intangible assets such as information, community, and brand. Horizontal content portals such as AOL are vertically integrating with horizontal infrastructure providers, such as Time Warner Cable. (Note: Prior to the AOL Time Warner merger, AOL was both a horizontal portal and a horizontal infrastructure portal.) As Internet advertising revenues fall, horizontal portals such as Yahoo! that do not provide other sources of revenue are evolving their business models to include transaction-oriented services and revenue-sharing partnerships with infrastructure portals..Convergence of voice, data, and video channels and global acceptance of a common set of standards is leading to global industry convergence at the content and infrastructure levels. Aggressive pursuit of a growing market for hosted application services is leading to confusion as players with markedly different business models converge on a common competitive space. Two competing Vertical Infrastructure Portal (ASP) models are emerging: producer-ASPs (for example, Oracle, Siebel, SAP) provide online access to Internet-enabled versions of their brand-name software; distributor-ASPs (for example, US Internetworking and Jamcracker) offer application hosting of many software brands.

33

Infrastructure Providers—Producer Model

Models & Examples Model Differentiators Likely Revenues Likely Costs

Manufacture Equipment

Develop Software

Services/ Consulting

Equipment/Component ManufacturersIBMSonyLucentIntel

Yes Possibly Possibly Product license or sales; Installation &

integration fees; Maintenance, update

& service fees

R&D; Advertising, marketing and sales; Production;

Physical facilities & infrastructure; Specialized

equipment, materials & supplies; IT infrastructure

Software FirmsSAPSiebelOracleMicrosoft

Rarely Yes Possibly Product license or sales; Installation &

integration fees; Maintenance, update

& service fees

R&D; Advertising, marketing and sales; Production;

Physical facilities & infrastructure; Specialized

equipment, materials & supplies; IT infrastructure

Custom Software and Integration Service ProvidersAccentureScientValue-added Resellers

Possibly

Possibly Yes Commission, service or transaction fee

Access to specialized talent.; Professional development and training; Travel

Infrastructure Services Agency.comFederal Express

Rarely Possibly Yes Commission, service or transaction fee;

Hosting fee

Content/info asset mgmt.; R&D; IT infrastructure

Infrastructure Producer Business Model TrendsMany hardware and software producers were early adopters of online commerce, selling directly to Internet-savvy customers and through online distributors. For example, in 1999, over 80% of Cisco’s sales were through online channels—most of which was through online distribution partners.

34

Evolving Business Model

Expand

EnhanceExte

nd

Exit

EnhanceAdd functionality or features to current product/service offerings or improve

performance of existing business

ExpandAdd new product/service offerings or enter new geographic markets

ExtendEnter new line of business and/or add new

business models

ExitExit a business or market or drop a

product/service offering

Expand

EnhanceExte

nd

Exit

Expand

EnhanceExte

nd

Exit

EnhanceAdd functionality or features to current product/service offerings or improve

performance of existing business

ExpandAdd new product/service offerings or enter new geographic markets

ExtendEnter new line of business and/or add new

business models

ExitExit a business or market or drop a

product/service offering

35

Evolving Business Model Example —American Express

ExpandEnhance

Ex

ten

d

Ex

it

ExpandEnhance

Ex

ten

d

Ex

it

36

Evolving Business Model Example —Amazon.com

ExpandEnhance

Exte

nd

Exit

ExpandEnhance

Exte

nd

Exit

37

Analyzing Business Models

Step 1: Profile your current business modelStep 2: Determine how you might evolve your current

model and/or identify new models to pursueStep 3: Use the business model analysis framework to

prioritize new models and initiatives– Evaluate the concept (opportunity)– Evaluate the capabilities and resources required– Evaluate the value proposition (return to all stakeholders)

Step 4: Use the analysis in Step 3 as a benchmark to develop real-time performance monitoring systems

Step 5: Revise your strategy, implementation plan, and performance measurement systems on an ongoing basis