1 Introducing the 2008 Michigan Earned Income Tax Credit Scott B. Darragh Office of Revenue and Tax...

21

1 Introducing the 2008 Michigan Earned Income Tax Credit Scott B. Darragh Office of Revenue and Tax Analysis Michigan Department of Treasury EITC Learning Exchange June 13, 2008

-

Upload

branden-farmer -

Category

Documents

-

view

216 -

download

0

Transcript of 1 Introducing the 2008 Michigan Earned Income Tax Credit Scott B. Darragh Office of Revenue and Tax...

1

Introducing the 2008 Michigan Earned Income Tax Credit

Scott B. DarraghOffice of Revenue and Tax Analysis

Michigan Department of Treasury

EITC Learning ExchangeJune 13, 2008

2

Any opinions expressed today should be viewed as strictly my own, and may not represent the views of the State Treasurer or the Michigan Department of Treasury.

3

Life as an Economist

An economist is someone who gets rich explaining to others why they are poor. (Source unknown)

A woman hears from her doctor that she only has half a year to live. The doctor advises her to marry an economist. The woman asks, "Will this cure my illness?" "No," the doctor answers, "but the six months will seem like a lifetime!"

--Taken from Jeff Thredgold, On the One Hand: The Economist's Joke Book.

4

Federal and State EITCs

The federal EITC will provide approximately $44.7 billion in benefits to recipients in 2008 (2009 Budget of the U.S.).

The number of states with EITCs has grown from 7 in 1994 to 22 in 2008 (CBPP).

State EITCs typically are structured to mirror federal eligibility and equal a percentage of the federal credit (piggyback credits).

5

Brief Recent History of EITC

The last major expansion of federal EITC occurred in 1993.

“Last year, we fought for, and won, a major expansion of the EITC…. This credit will help millions of workers and is a cornerstone of our effort to reform the welfare system and make work pay.”President Clinton, memorandum dated March 9, 1994

6

Recent History (cont.)

Combined with welfare reform enacted in 1996, the EITC reflects a policy shift that ties public assistance to work.

Federal legislation enacted in 1997, 2001, and 2004 has:– Modified the rules for qualifying children;– reduced marriage penalties in the EITC; and– sought to improve compliance with EITC

requirements.

7

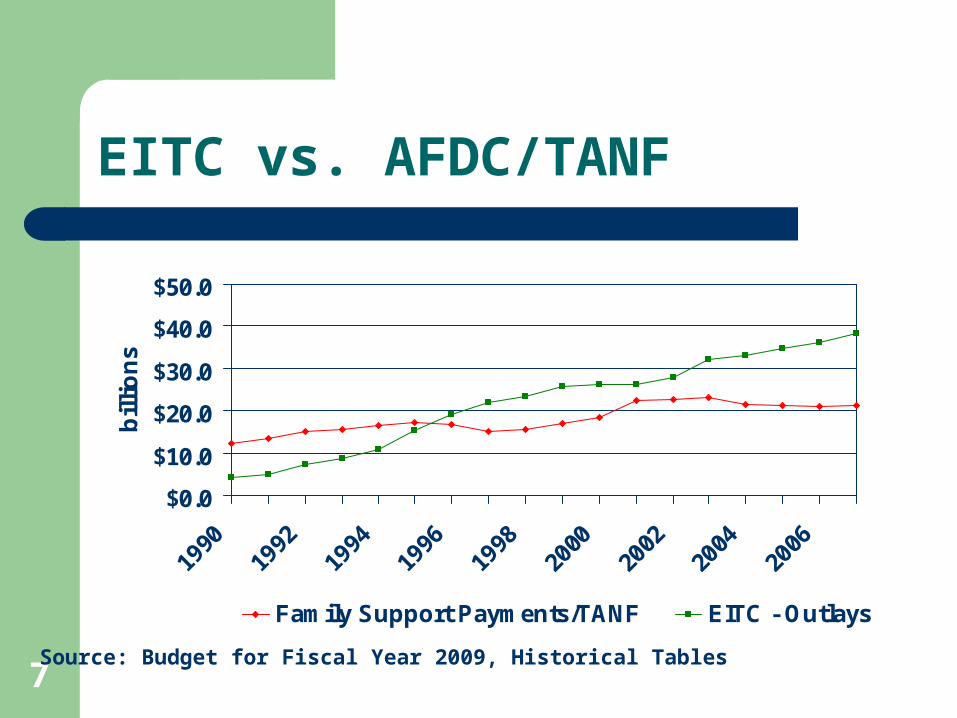

EITC vs. AFDC/TANF

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

1990

1992

1994

1996

1998

2000

2002

2004

2006

bil

lio

ns

Family Support Payments/TANF EITC - Outlays

Source: Budget for Fiscal Year 2009, Historical Tables

8

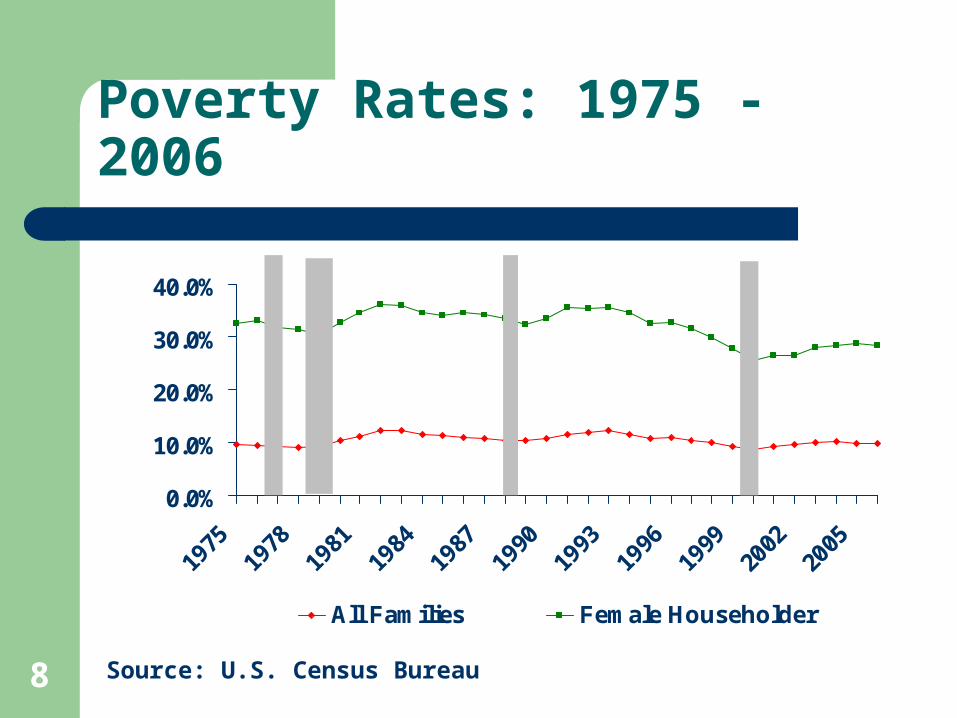

Poverty Rates: 1975 - 2006

0.0%

10.0%

20.0%

30.0%

40.0%

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

All Families Female Householder

Source: U.S. Census Bureau

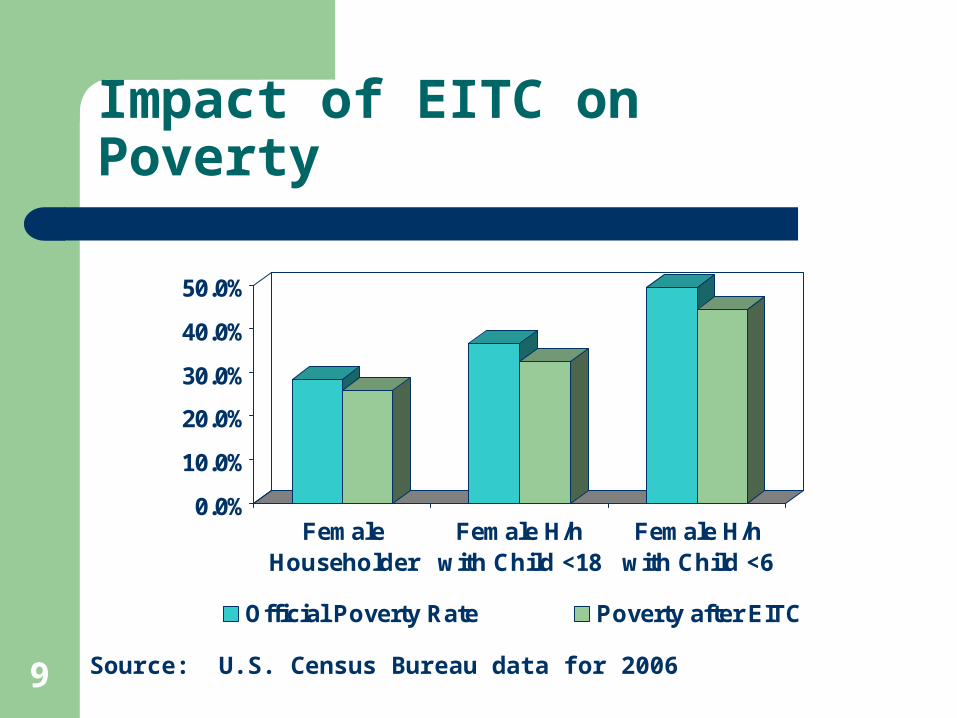

9

Impact of EITC on Poverty

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

FemaleHouseholder

Female H/hwith Child <18

Female H/hwith Child <6

Official Poverty Rate Poverty after EITC

Source: U.S. Census Bureau data for 2006

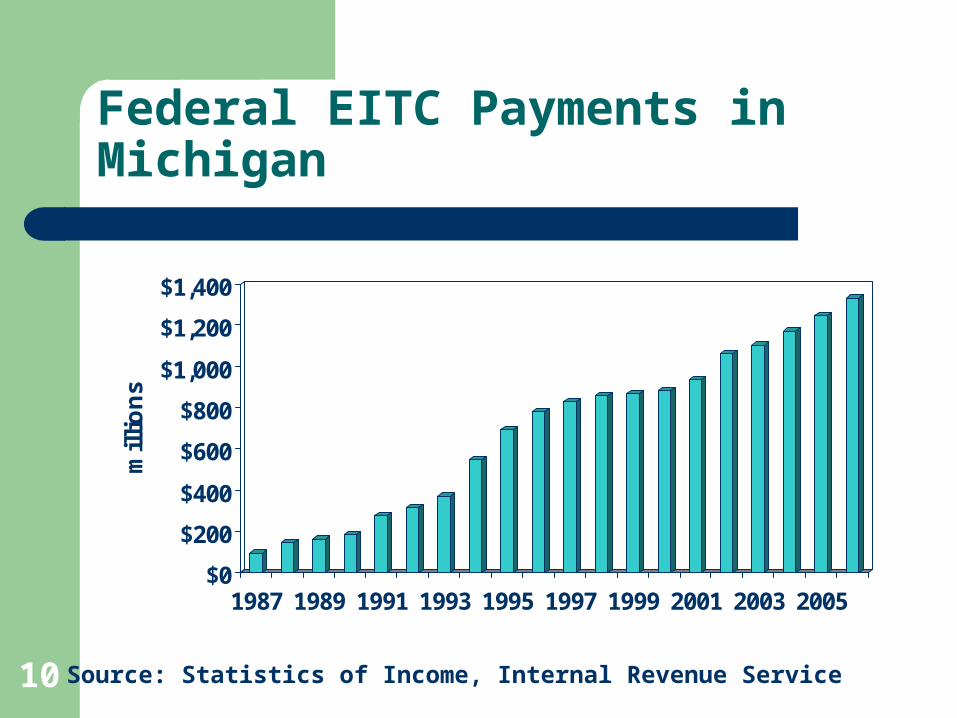

10

Federal EITC Payments in Michigan

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

mil

lio

ns

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

Source: Statistics of Income, Internal Revenue Service

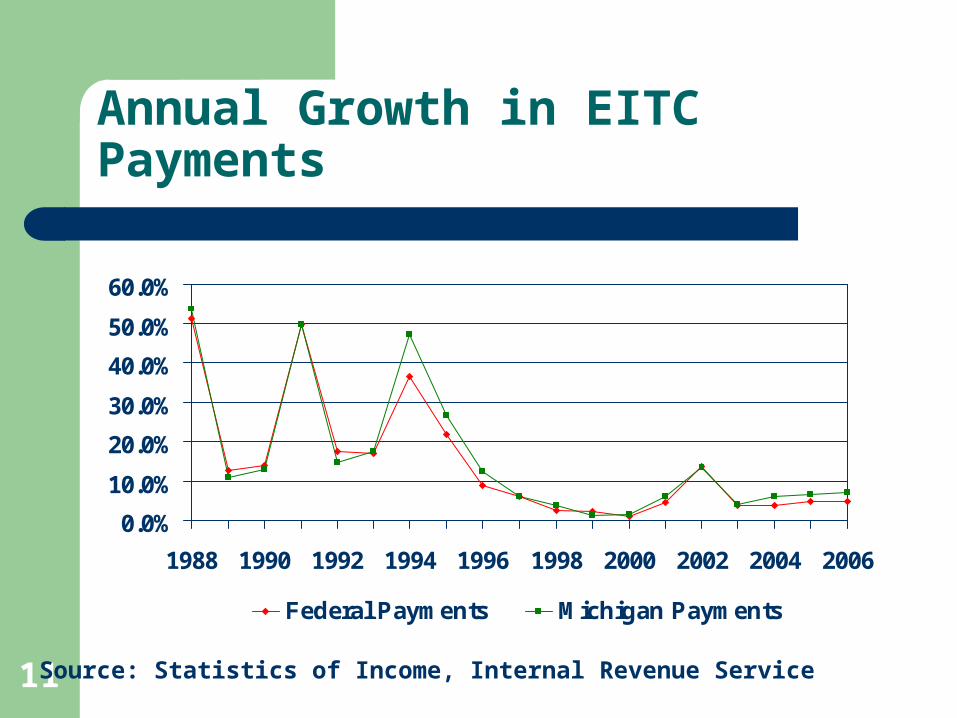

11

Annual Growth in EITC Payments

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

Federal Payments Michigan Payments

Source: Statistics of Income, Internal Revenue Service

12

Errors in Claiming EITC

Errors associated with EITC administration have generated a lot of attention.

Over-claiming EITC– IRS estimates approximately 23-28% paid in error, although the

estimates are a few years old– Errors related to qualified child, filing status, and income– Changes have been implemented at federal level to potentially

address some of these problems Under-claiming EITC

– GAO estimates approximately 25% don’t claim the credit, representing approximately 11% of total credits

– Under-claim highest for filers without children or more than 2 qualifying children

13

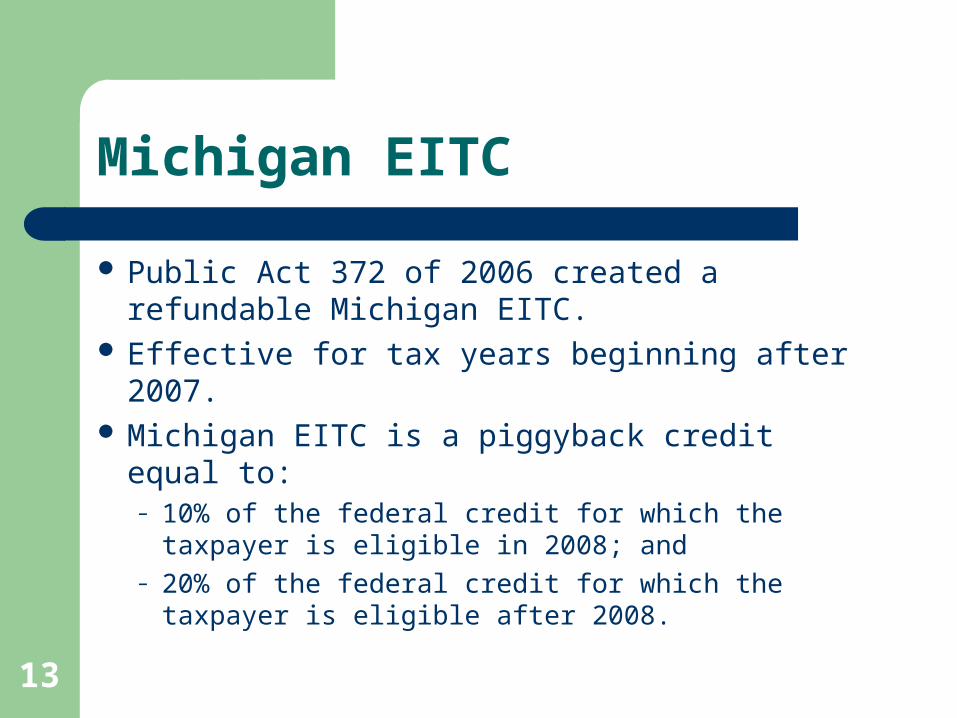

Michigan EITC

Public Act 372 of 2006 created a refundable Michigan EITC.

Effective for tax years beginning after 2007. Michigan EITC is a piggyback credit equal to:

– 10% of the federal credit for which the taxpayer is eligible in 2008; and

– 20% of the federal credit for which the taxpayer is eligible after 2008.

14

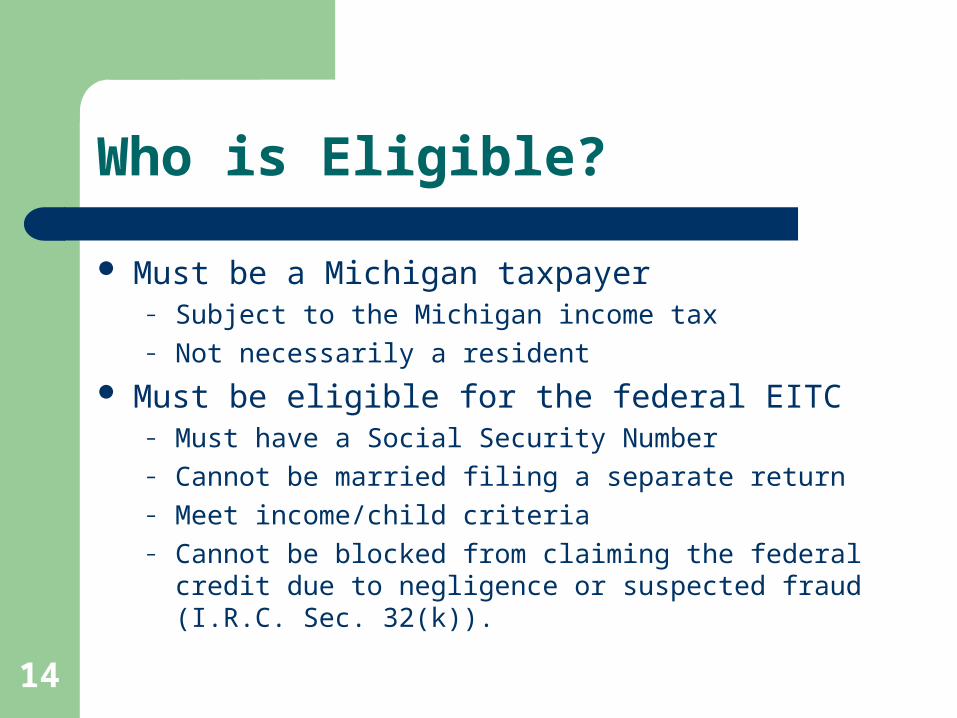

Who is Eligible?

Must be a Michigan taxpayer– Subject to the Michigan income tax– Not necessarily a resident

Must be eligible for the federal EITC– Must have a Social Security Number– Cannot be married filing a separate return– Meet income/child criteria– Cannot be blocked from claiming the federal credit due to

negligence or suspected fraud (I.R.C. Sec. 32(k)).

15

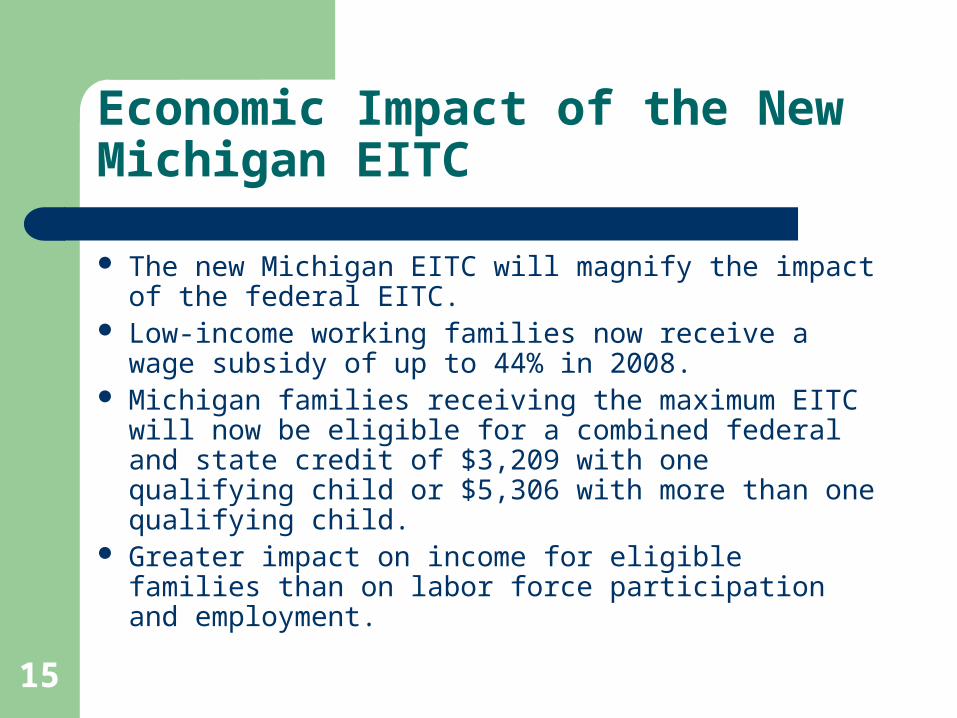

Economic Impact of the New Michigan EITC

The new Michigan EITC will magnify the impact of the federal EITC.

Low-income working families now receive a wage subsidy of up to 44% in 2008.

Michigan families receiving the maximum EITC will now be eligible for a combined federal and state credit of $3,209 with one qualifying child or $5,306 with more than one qualifying child.

Greater impact on income for eligible families than on labor force participation and employment.

16

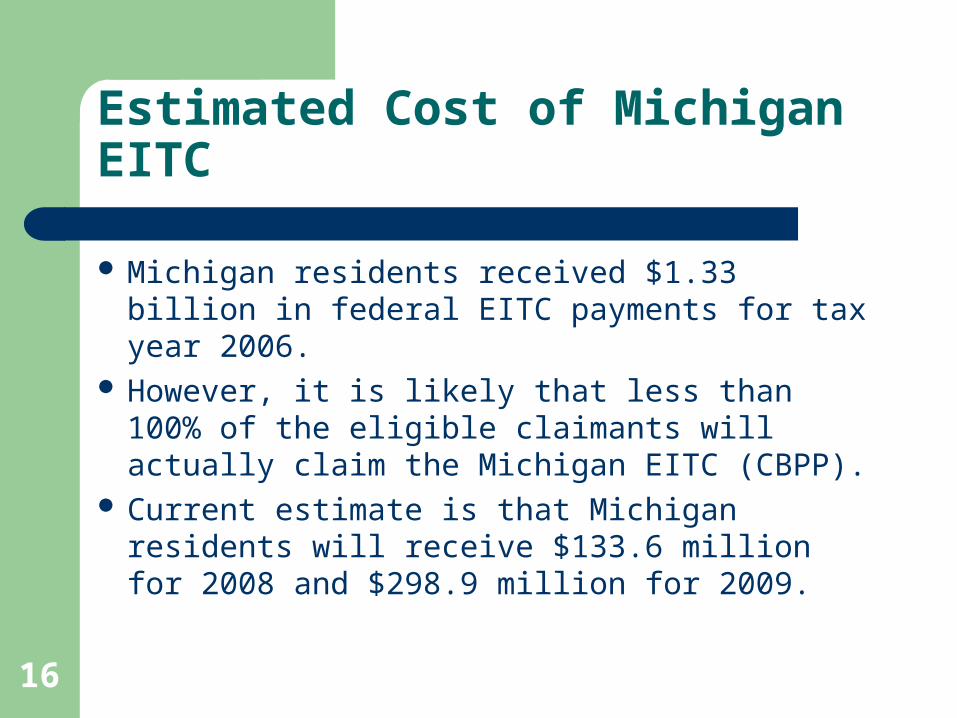

Estimated Cost of Michigan EITC

Michigan residents received $1.33 billion in federal EITC payments for tax year 2006.

However, it is likely that less than 100% of the eligible claimants will actually claim the Michigan EITC (CBPP).

Current estimate is that Michigan residents will receive $133.6 million for 2008 and $298.9 million for 2009.

17

How to Claim the Michigan EITC

Important to remember that Treasury’s plans for administering the Michigan EITC are tentative.

We expect to receive approximately 750,000 EITC claims for tax year 2008.

If similar to the federal EITC, between 80%-90% of the credit claims will be filed electronically.

18

Claiming the EITC (cont.)

To claim the Michigan EITC a taxpayer will likely need to complete a form that resembles the federal Schedule EIC to report qualifying children, earned income, and the amount of federal EITC claimed.

When returns are filed electronically, this reporting will be seamless.

For most paper returns, this will be straightforward as well.

19

Claiming the EITC (cont.)

The process in Michigan will be similar to the process in many other states.

Watch for more information in the Michigan 1040 booklet next January and on the Treasury Website (www.michigan.gov/treasury).

Treasury will work with commercial tax preparers and software developers as part of our annual forms development process and we would expect that the Michigan EITC will be included in their programs.

20

Proposed Legislation

Senate Bill 662, introduced last summer, would make the Michigan EITC conditional on a $250 million balance in the Rainy Day Fund.

House Bill 4645, passed by the House in February, would regulate the refund anticipation loan process.

21

Conclusion

“I think we agree, the past is over.”

Governor George W. Bush – May 10, 2000

And so is my presentation. Any questions?