1 How do Central Banks Write? An Evaluation of Inflation Reports by Inflation Targeting Central...

19

1 How do Central Banks Write? An Evaluation of Inflation Reports by Inflation Targeting Central Banks Comment By Peter Andrews, Monetary Assessment and Strategy Division Bank of England

-

Upload

miranda-reeves -

Category

Documents

-

view

213 -

download

1

Transcript of 1 How do Central Banks Write? An Evaluation of Inflation Reports by Inflation Targeting Central...

1

How do Central Banks Write?An Evaluation of Inflation Reports by

Inflation Targeting Central Banks

Comment By Peter Andrews,

Monetary Assessment and Strategy Division

Bank of England

Benchmarking and Measuring Performance

MONETARY ANALYSIS AIMS 2003/4

To ensure that the Inflation Report and MPC Minutes present

a clear account of the MPC’s latest economic assessment and

policy conclusions.

PERFORMANCE INDICATORS

Media coverage

Quality of, and feedback on, the Inflation Reports and

MPC minutes

Bank Objectives for 2002/03 (2002 Annual Report, p36)

3. To build public support for price stability, and public understanding of the MPC’s approach to its remit, through speeches, the Inflation Report and other publications, and

through other initiatives

2

Objectives of publishing the IR

• The Inflation Report serves two purposes. First, its preparation provides a … framework for discussion among MPC members as an aid to our decision making. Second, its publication allows us to share our thinking and explain the reasons for our decisions.

• Also a requirement under the Bank of England Act 1998

3

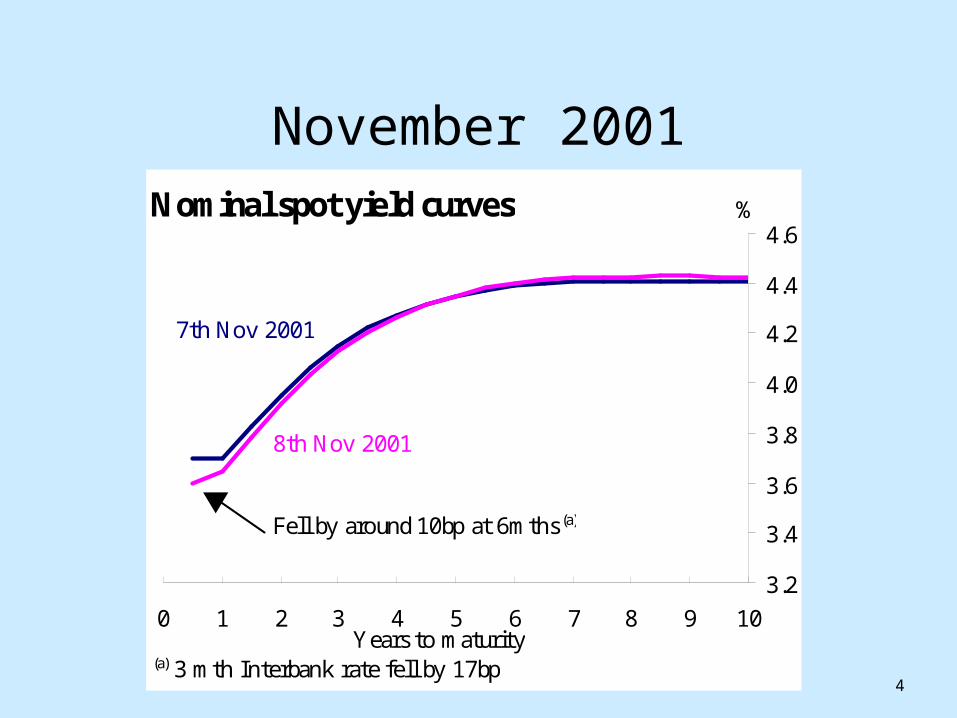

November 2001

4

Nominal spot yield curves

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

0 1 2 3 4 5 6 7 8 9 10

%

Years to maturity

Fell by around 10bp at 6mths (a)

7th Nov 2001

8th Nov 2001

(a) 3 mth Interbank rate fell by 17bp

November 2001

5

Implied forward inflation

1.9

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2.7

0 2 4 6 8 10

%

Years to maturity

Rose by up to 12bp

7th Nov 2001

8th Nov 2001

February 2003

6

Nominal spot yield curves

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

0 1 2 3 4 5 6 7 8 9 10

%

Years to maturity

Fell by almost 20bp at 1yr (a)

5th Feb 2003

6th Feb 2003

(a) 3 mth Interbank rate fell by 21bp

February 2003

7

Implied forward inflation

1.9

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2.7

0 2 4 6 8 10

%

Years to maturity

Rose by up to 15bp6th Feb 2003

5th Feb 2003

March 2003 MPC Minutes Release

10

Nominal spot yield curves

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

0 2 4 6 8 10

%

Years to maturity

Rose by almost 20bp

18th Mar 2003

19th Mar 2003

March 2003 MPC Minutes Release

11

Implied forward inflation

1.9

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2.7

0 2 4 6 8 10

%

Years to maturity

Rose by up to 5bp

Fell by up to 5bp

18th Mar 2003

19th Mar 2003

Summary on market measures of surprises

• Short-term interest rates not the clearest measure of surprise

• Long-term rates and inflation expectations are of greater macroeconomic significance

12

Direct measures of public opinion

• Inflation expectations over the next year• Understanding of monetary policy• Effect of interest rates on inflation• Satisfaction with the Bank of England• What is best for the economy, what is best for

individual

Quarterly Bank of England / NOP poll investigates public expectations of:

See K. Scheve “Public Attitudes About Inflation: A comparative Analysis” - in Bank of England Quarterly Bulletin, Autumn 2001

13

Knowledge of Transmission Mechanism (a)(b)

0

10

20

30

40

50

60

70

80

90

100

Nov-00 Feb-01 Feb-02 Feb-03

0

5

10

15

20

25

Agree Disagree

Don't know Balance agree (LHS)(c)(a)Based on answers to Q: "How strongly do you agree with the statement 'A rise in interest rates would make prices in the high street rise more slowly in the medium term, say a year or two'?"(b)Question first asked in Nov 2000, after which time it became an annual question, asked each February.(c) Defined as: "agree" less "disagree" responses

%

(LHS)

pp

14

Satisfaction with Bank of England

0

10

20

30

40

50

60

Nov-99 May-00 Nov-00 May-01 Nov-01 May-02 Nov-02

0

1

2

3

4

5

6

7 ppRepo rate (LHS)(b)

Balance satisfied (RHS)(a)

(a) Balance of respondents answering positively to Q: "How satisfied or dissatisfied are you with the way the Bank of England is doing its job to set interest rates in order to control inflation?" less those answering negatively(b)At time of each quarterly survey

%

15

Who sets interest rates?(a)(b)

0

10

20

30

40

50

60

70

80

90

100

Don't knowOthers (Government, Treasury, P arliament, Others)MP C or Bank of England

(a) Based on (set) answers to Q: "Each month, a group of people meets to set Britain's basic interest rate level. Do you know what this group is?"(b)Annual survey question, since February 2001

Feb02

Feb03

Feb01

Feb00

%

Nov99

May00

Aug00

Nov00

16

Opinion Polling Summary

• Direct measure of public, as opposed to market, understanding

• Can measure understanding of framework and strategy

• But recall many of the public not well informed

17

Range of monetary publications• Inflation Report: describes recent developments and

projections, summarises minutes, annually analyses forecast errors

• MPC minutes: describes recent developments, explains decision, examines alternatives, discusses strategic issues

• Quarterly Bulletin: contains explanatory articles on monetary and financial stability topics, short research articles and speeches

• Working Papers

• Monetary and Financial Statistics (Bankstats)

• Ad hoc publications (eg books describing the Bank model)

• Speeches and IR press conferences: can address objections

18

Points for discussion• Outlook probabilistic (so point forecasts not published by

Bank). Balance of risks essential

• Target continuous through time, not confined to two year horizon

• Role of judgement- in constructing projections

- in making policy after the forecast

• What past knowledge is assumed? - some details, e.g. conventions for exchange rate, not repeated each

time

• Surprises exercise: range of macro control variables is limited, eg activity not included

19

Summary • A welcome contribution to benchmarking and measuring

central bank performance

• Could consider other measures of expectations, eg– Longer-horizon market interest rates and inflation expectations

– Opinion polls

• Inflation reports are only part of central banks’ public information strategy; other publications fulfil some key factors identified in the paper

• Crucial that Inflation Reports are not presented or interpreted mechanically

20

21

How do Central Banks Write?An Evaluation of Inflation Reports by

Inflation Targeting Central Banks

Comment By Peter Andrews,

Monetary Assessment and Strategy Division

Bank of England

![How Should Central Banks Control Inflation[King]](https://static.fdocuments.in/doc/165x107/577cd84e1a28ab9e78a0e8e1/how-should-central-banks-control-inflationking.jpg)