1 Global Imbalances – Adjustments by Surplus/Deficit Countries Dr Michael Lim Mah Hui May 23, 2011...

52

1 Global Imbalances – Adjustments by Surplus/Deficit Countries Dr Michael Lim Mah Hui May 23, 2011 South Centre Geneva

-

Upload

maud-bradford -

Category

Documents

-

view

219 -

download

2

Transcript of 1 Global Imbalances – Adjustments by Surplus/Deficit Countries Dr Michael Lim Mah Hui May 23, 2011...

1

Global Imbalances – Adjustments by Surplus/Deficit Countries

Dr Michael Lim Mah HuiMay 23, 2011South Centre

Geneva

2

Three Structural Imbalances to Global Financial Crisis

Current Account Imbalance Imbalance between financial sector and

real economy – financialization of economy Income and Wealth Imbalance

Thesis

Current account imbalance is only a manifestation of more serious structural imbalances

These are sectoral imbalance btw finance and real economy, and income and wealth inequality

3

Bernanke and Savings Glut

Bernanke blames current account surplus countries for excess savings > lower interest rates > financing deficits and debt of US

Disingenuous to blame surplus countries and not deficit countries

A country cant run surplus unless other countries run deficit

Question is what cause surplus & deficit4

Surplus = Savings > InvestmentsDeficit = Investments > Savings

China accused of pursuing weak exchange rate policy to boost exports; US guilty of pursuing loose monetary policy that encourage excessive borrowings & consumption

Important question is what cause some countries to have excess savings over investments and others excess investments over savings

5

U.S. – Inequality, Under-consumption and Financial Crisis

Wage stagnation & growing inequality > under-consumption by majority

Under-consumption by majority and excess savings by minority – 2 sides of same coin

Under-consumption resolved by over-consumption thru rising household debt

Excess savings recycled thru financial system to finance HH debt > debt bubble

6

7

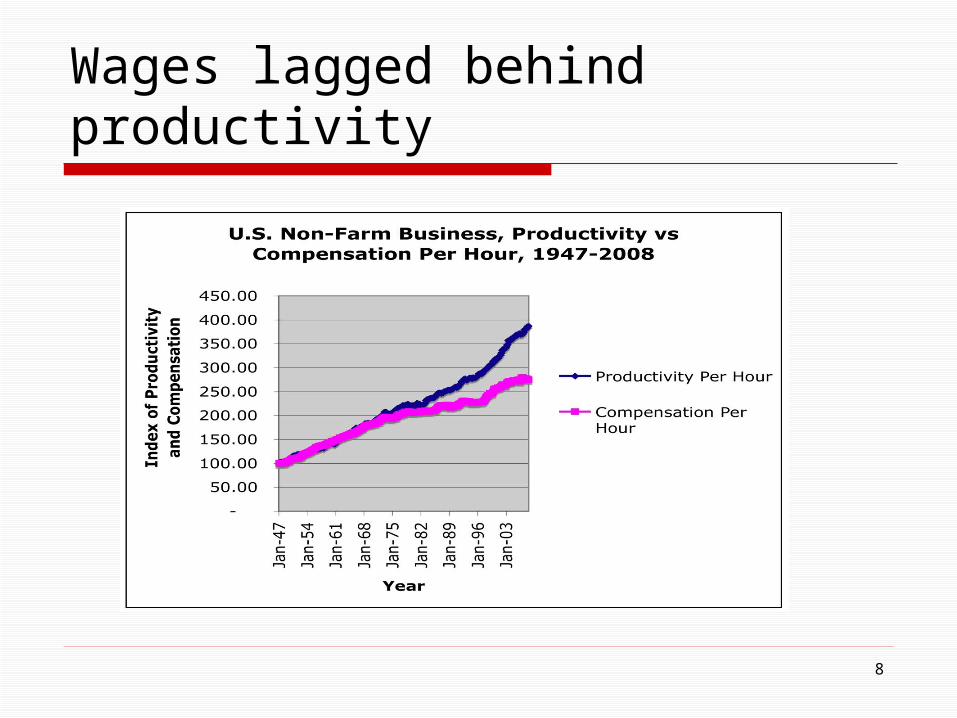

CEO’s Pay, Corp Profits, S&P 500 Prodn Workers Pay, Fed Min wage

1990-2005Minm wage minus 9%

Prodn WorkersPay + 4%

Corp Profits + 107%

S&P 500 +141%

CEO’s Pay+300%

Wages lagged behind productivity

8

U.S. inequality and two bubbles

Excess savings also > asset bubble as risk appetite rises

Both eventually imploded > financial crisis

9

10

Inequality Preceded Great Depression and GFC

China – Inequality, Under-consumption & CA Surplus

Inequality also > underconsumption Share of GDP to labor fell from 57% to

37% over last 20 years Share of personal consumption to GDP fell

from 55% to 35% over same period High savings rate of 50% due to

precautionary savings and high corporate savings and investments for export > current account surplus

11

Decline in Private Consumption in China

12

13

Inequality, Under-consumption and Current Account Imbalances

Both in China and U.S. inequality > under consumption

In U.S. under-consumption “solved” by debt aided by over-leveraged & exotic financial system where savings recycled to household debt

In China – excess savings channeled to investments for exports; bank lending to 18% of bank loans

Policy Implications and Lessons

Global current account imbalance related to income imbalance & sectoral imbalance

For surplus countries, need to reduce dependence on exports in favor of domestic consumption

Rebalancing requires reducing inequality Wages must rise in tandem with

productivity increases Growth must be with employment creation

14

Policy Implications

For deficit countries like US, also need to have wages rise to strengthen household balance sheet, and to reduce debt

Reduce financialization and speculation For surplus countries, rechannel excess

savings from investments in US debt or from exotic financial instruments to regional and domestic investments.

15

Policy Implications

SWF instead of investing in speculative finance & adding to fin fragility; rechannel funds for intra-regional development

Concept of SARR – socially accept rate of return

16

THANK YOU

17

18

19

20

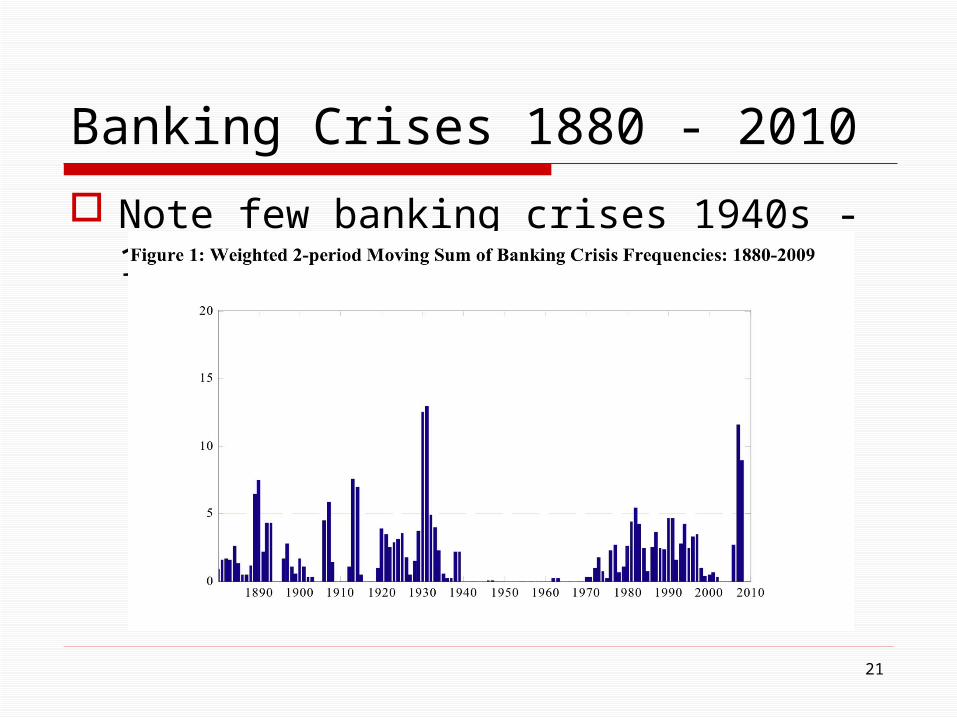

Globalization = Increasing world integration thru trade, capital, labor, information flows Globalization uneven and asymmetric High growth but increasing inequality Fuelled by deregulation and liberalization Frequency of financial crisis increased after

liberalization -1970-2007–127 financial crises

High correlation btw inequality and financial crisis

Banking Crises 1880 - 2010

Note few banking crises 1940s -1970s

21

22

Inequality & Financial Crisis

Key to understanding long term structural causes of Global Financial Crisis is to examine the link between:

growth, debt, inequality, financialization.

23

After post WW2 growth, U.S. real GDP growth on decline fr 4.4% to 2.6% (1960-2006)

Chart 2: Avg Real GDP growth

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

1960-69 1970-79 1980-89 1990-99 2000-06

Year

Per

Cen

t G

DP

Gro

wth

Avg Real GDP growthl

1960-69 - 4.4%

1970-79 – 3.3%

1980-89 – 3.1%

1990-99 – 3.1%

2000-06 – 2.6%

24

Debt-driven Economy, 1960-2007Chart 3 : U.S. GDP & Debt by Sector

1960-2007

-

10,000

20,000

30,000

40,000

50,000

60,000

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

07

Year

US

$ b

illion

sGDP

Total Debt

Financial Debt

Non-FinancialCorporateHousehold Debt

Government Debt

GDP rose - 27x

Total Debt - 64x

Financial -490x

Household- 64x

Non Financial Corp – 53x

Govt- 24x

Income and Wealth Inequality in U.S. Worsened after 1970s

1970-2006, real wages of workers stagnated, while that of CEOs spiraled

Share of GDP going to capital increasing and to labor decreasing

Gini index rose fr 0.35 to 0.46 – worse than many third world countries

Top 1% took 25% of total income Top 1% took 33% of total wealth

25

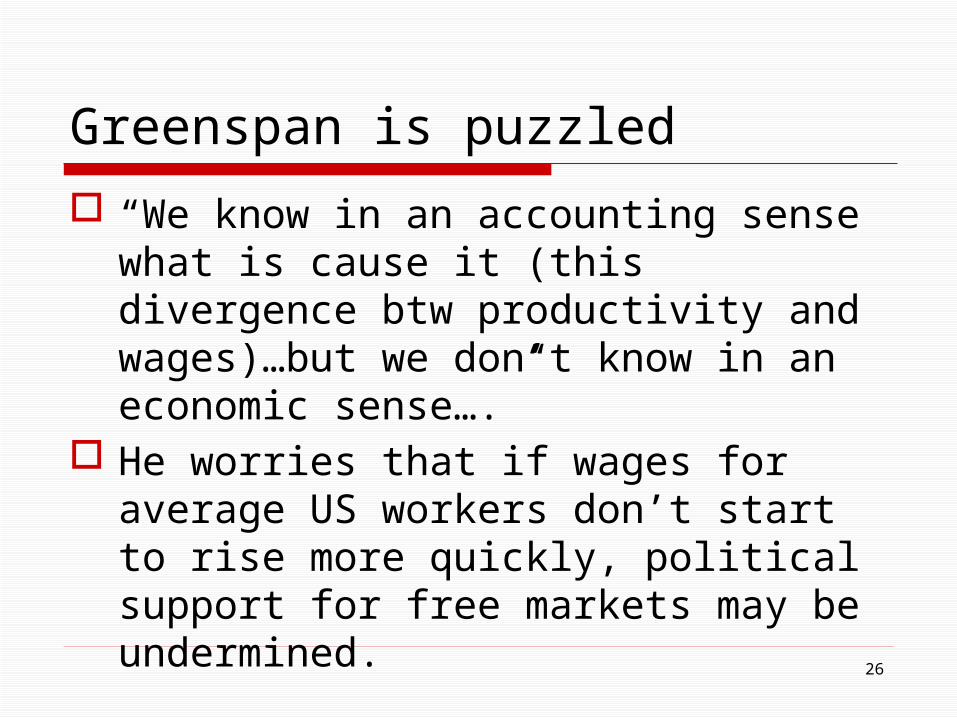

Greenspan is puzzled

“We know in an accounting sense what is cause it (this divergence btw productivity and wages)…but we don’t know in an economic sense….”

He worries that if wages for average US workers don’t start to rise more quickly, political support for free markets may be undermined.

26

27

Many causes for inequality

Education, skills, technology, trade Loss of bargaining power – Reagan broke

national accord btw labor and capital Global labor arbitrage Neo-liberal state policies favor capital Capital share of GDP rose with tax cuts in

dividends, capital gains, estate duties, corporate earnings

Stephen Roach of Morgan Stanley

“ As the pendulum of economic power has swung from labor to capital in the developed world, there is now a clear and growing risk that the pendulum of political power could swing from capital back to labor” (The Next Asia, 2009:91)

28

29

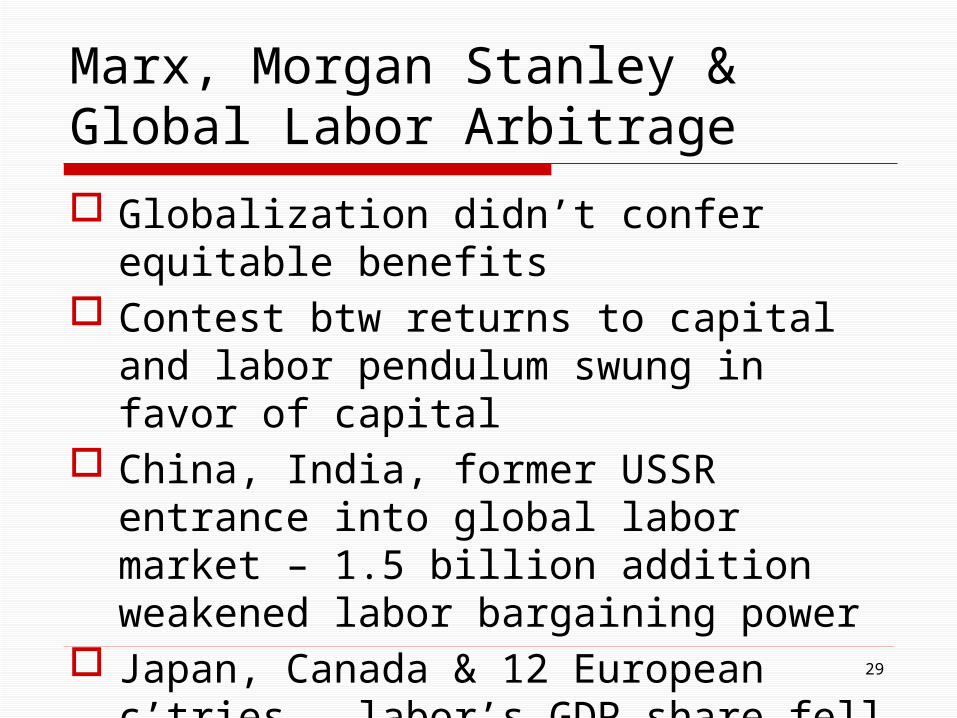

Marx, Morgan Stanley & Global Labor Arbitrage

Globalization didn’t confer equitable benefits

Contest btw returns to capital and labor pendulum swung in favor of capital

China, India, former USSR entrance into global labor market – 1.5 billion addition weakened labor bargaining power

Japan, Canada & 12 European c’tries – labor’s GDP share fell fr 56% to 53.7% btw 2001 & 2006

30

China – Higher Inequality Amidst Growth Boom Wages of Chinese workers lagged behind –

productivity grew 20%, wages 12% (2000-04) In 2002 –it was 57cents, 3% of avg US hourly pay Large pool of migrant workers fr rural sector Share of GDP to labor – drop fr 57% to 37%

(1978-2005) Gini almost doubled fr 0.32 to 0.50 (1978-2006) Premier Wen – China’s economy “unstable,

unbalanced, uncoordinated, unsustainable” Wage situation beginning to reverse

31

Marx - Contest btw Capital & Labor

Capitalism’s basic contradiction – contest btw labor and capital for economic pie – transformed over time

Capital’s strategies to enhance profits - increase capital intensity - part time, temporary, contractual labor - labor flexibility, jobless recovery - leveraged buy-out

32

Inequality and Under-consumption

When wages stagnate or kept low > structural tendency to under-consumption (lack of effective demand) > excess capacity or low production > drag on profit > interruption in the production and accumulation process

Inequality impacts 2 ways – under-consumption on one hand excess savings on other hand

Under-consumption and Excess Savings are two sides of same coin

33

Overconsumption and Debt Bubble

Under-consumption is “resolved” through debt > over-consumption

Wages stagnated but personal consumption rose fr 60% GDP to 72% (1960s to 2007)

National savings rate declined by 10% Household debt rose 64x to 100% of GDP Financial innovations fuelled debt bubble – credit

card, home equity low, negative amortization, securitization

Net equity extraction fr homes rose to 9% of disposable income

34

Excess Savings and Asset Bubble Tiny minority with excess savings and liquidity Savings recycled to household loans Not content with fixed deposits High risk appetite Placed in hands of financiers who churn out

derivatives and leveraged instruments Ponzi financing – lending based not on cash flow

but on rising asset prices and taking on more debt Inevitable crash of both asset bubble and debt

bubble

35

Financialization of Economy

Basic dynamics of market economy not changed

Forms & specifics have changed Fr competitive capital to monopoly capital

to finance capital US, btw 1960-2006, financial sector 14% of GDP to 20% (twice as large as next FIRE sector- 30% of total corporate profit

36

Financial fragility and instability major cause of economic crisis Major economic crises caused by fragility,

instability and implosion of financial sector Asset bubble rather than wage and consumer

price inflation causing crisis Central bankers have been remiss and kept eyes

on wrong ball Also misguided in belief in efficient market

hypothesis that markets price assets efficiently and are self-regulating

37

China Equation – Inequality, Under-consumption & Export Surplus

Bernanke – blame Asia for savings gluts and contributing to global imbalances

Disingenuous to blame current account surplus country and not deficit country

US only country with ability to run huge CA deficit for long period because of international curr status

China accused of managing weak yuan to boost exports, US guilty of loose monetary policy that encourage overspending

38

U.S. Current Account Balance

U.S. Current Account Balance

(1,000)

(800)

(600)

(400)

(200)

-

200

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Year

Cu

rren

t A

ccou

nt

Bala

nce $

Bil

lion

U.S.

39

China – Current Account Surplus = Savings Investment Gap More important question is what cause a country

to have more savings than investment and v.v China’s savings over 50%; Investments 40% Private consumption fell from over 70% to 35%

(1960s to 2007) Why high savings?

- precautionary savings – many SOE workers thrown out of work, social services no longer free

- corporate savings – SOEs not taxed, don’t pay out dividends, reinvest into export production

Tale of Two Gluts – Savings Glut and Debt & Overconsumption Glut

China current account surplus rose fr $12bn 1990 to $426bn in 2008

Foreign reserves rose fr $30bn in 1990 $3 trillion in 2011.

Under-consumption and excess savings in poor country funding excess consumption and debt bubble in the U.S.

SWF investments in speculative finance capital adds to financial instability

40

China’s Current Acct Surplus, FX Reserves, U.S. Current Acct Deficit

41

Conclusions and Policy Implications

“There can be no dispute that the current crisis is due to a systemic, policy-driven environment of financialization and speculation originating in the North, often foisted upon reluctant developing countries through misguided advice and aid conditionality. The crisis must be resolved through intervention at those levels.” (UNCTAD)

42

Conclusions

Globalization driven by financial and speculative capital has distorted development in real economy

Two major imbalances – imbalance btw finance and real economy

Inequality is worsening This in turn driven by basic fundamentals of

contest btw capital and labor

43

Conclusions

For now, pendulum has swung in favor of capital, aided by neo-liberal state policies

Inequality has resulted in under-consumption and excess savings whose dynamics are played out in global imbalances and financial crises

If history is any guide, adjustment process without change in policy direction will not resolve the problems

44

Conclusions

Inequality a structural problem that requires policy shift fr market fundamentalism to policy of inclusiveness – raise wages concomitant with productivity increases

Present strategy of reviving growth by cutting labor costs only leads to jobless recovery

45

Conclusions

Without improvement in employment, wages, reduction of inequality, strengthened household balance sheet, growth is not sustainable.

46

Implications for Emerging Economies

Growth must be not be driven by financialization and speculation

Growth must be more balanced and inclusive

Wages must rise with productivity increases if want to reduce export dependence and promote domestic consumption

47

Conclusions

Encourage more debate, dialogue, new ideas and cooperation among EMCs

Formulate new agenda for different type of globalization

48

Some specifics

Presently only 10% of total FDI flows is btw South-South countries

Rather than invest in speculative capital, recycle huge surplus of EMCs within region

Introduce socially acceptable rate of return rather than maximizing shareholders value

Depend more on domestic and intra-regional markets – reduce inequality,

49

Conclusions

Increase regional cooperation in trade, investments, exchange rate coordination

50

IMF Working paper 10/268

Michael Kumhof and Romain Ranciere

Inequality, Leverage and Crises

51

THANK YOU

52