1 “Getting Paid for Your Exports in a Challenging Global Economy” Lansing, MI November 17, 2011...

39

1 “Getting Paid for Your Exports in a Challenging Global Economy” Lansing, MI November 17, 2011 Bill Richeson, CTP Senior Vice President International Division PNC Bank Ph: (616)771-8849

-

Upload

jonathan-neal -

Category

Documents

-

view

215 -

download

0

Transcript of 1 “Getting Paid for Your Exports in a Challenging Global Economy” Lansing, MI November 17, 2011...

1

“Getting Paid for Your Exports in a

Challenging Global Economy”

Lansing, MI

November 17, 2011

Bill Richeson, CTP

Senior Vice President

International Division

PNC Bank

Ph: (616)771-8849

2

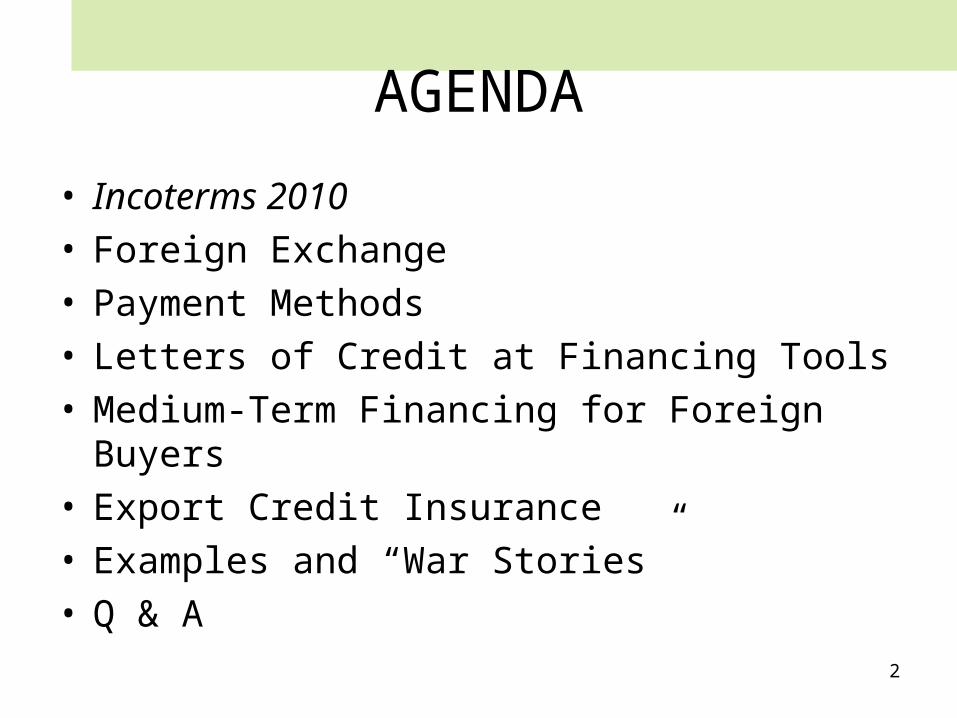

AGENDA

• Incoterms 2010• Foreign Exchange• Payment Methods• Letters of Credit at Financing Tools• Medium-Term Financing for Foreign Buyers• Export Credit Insurance• Examples and “War Stories”• Q & A

3

Pricing/Shipping Terms

• Known as Incoterms 2010– Published by:

ICC Publishing Corporation156 Fifth AvenueNew York, New York 10010(212) 206-1150 Website: http://www.iccwbo.org

• A set of international rules, initially formulated in 1936 by the International Chamber of Commerce (ICC) to define & interpret a standard set of pricing/shipping terms for international trade.

Know the Rules

4

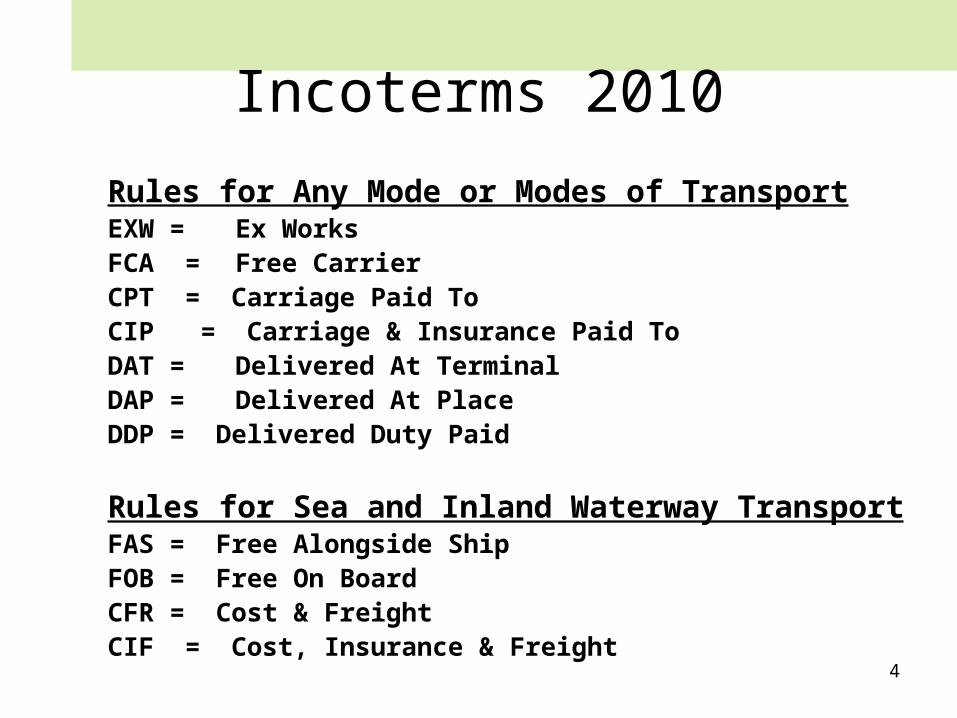

Incoterms 2010

Rules for Any Mode or Modes of TransportEXW = Ex WorksFCA = Free CarrierCPT = Carriage Paid ToCIP = Carriage & Insurance Paid ToDAT = Delivered At TerminalDAP = Delivered At PlaceDDP = Delivered Duty Paid

Rules for Sea and Inland Waterway TransportFAS = Free Alongside ShipFOB = Free On BoardCFR = Cost & FreightCIF = Cost, Insurance & Freight

5

Foreign Exchange

• There is foreign exchange risk to someone in every international transaction – even those payable in U.S. dollars

• Four Basic Risks- Fluctuation risk- Transaction risk – cash flow risk- Economic risk – operating risk vs. competitors- Translation risk – accounting riskYou must quantify and manage this riskBanks have tools and expertise to help you mitigate these risks

6

Foreign Exchange

Common Uses of Foreign Exchange• Transactions – used to make or receive

payments in another currency• Precautionary hedges – to protect against

unexpected changes in exchange rates• Speculative positions – to profit from

expected changes in exchange rates• Foreign investments – to buy and sell

foreign assets

7

Payment Methods

8

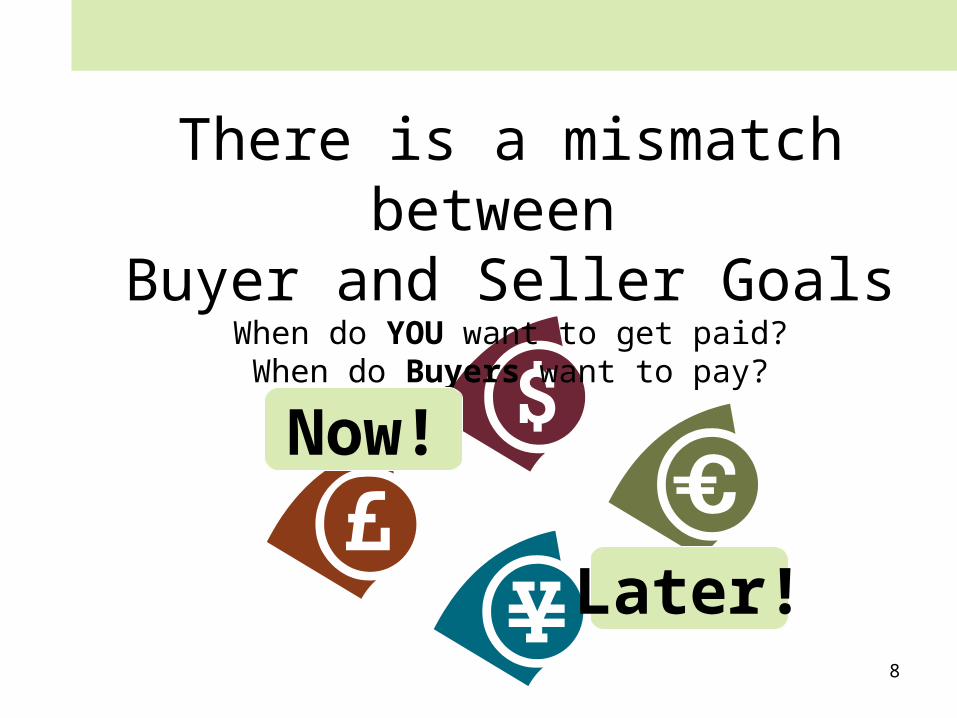

There is a mismatch between Buyer and Seller Goals

When do YOU want to get paid?When do Buyers want to pay?

Now!

Later!

9

Payment Methods: 4 Methods

Buyer (Importer) Perspective• Open Account• Documentary Collection• Letter of Credit• Cash In Advance

Seller (Exporter) Perspective• Cash In Advance• Letter of Credit• Documentary Collection• Open Account

Buyer & Seller have Reversed Priorities!

LowestRisk

HighestRisk

BestCashFlow

WorstCashFlow

10

Choice of Methods

(What Determines?) • Buyer-Seller Relationship• Buyer’s credit standing• Competition• Uniqueness of the product (custom made?)• Country conditions (political, economic)• Cash flow considerations• Transaction costs• Other

11

Payment Methods: 4 Methods

• Cash in Advance

• Documentary Collection

TermsFavorSeller

TermsFavorBuyer

• Letter of Credit

• Open Account

12

Risk Evaluation and Mitigation

• High Risk – Cash-in-Advance or Confirmed LC• Moderate Risk – Advised or Confirmed LC• Low Risk – Documentary Collection (at sight)• Very Low Risk: Documentary Collection (Time) or, Open

Account (possibly with Credit Insurance)• Lowest Risk – Open Account on extended terms

Make Decisions to Mitigate the Risks

Consider ALL risks, not just credit risks

13

Cash In Advance

• Buyer Pays– Wire Transfer– Check– Draft– Credit Card

• Seller Ships– No risk for seller except order cancellation– Foreign Import Regulations may prohibit– Hard sell to buyer– Consider the type of payment (Wire Transfer Best)– Requires little to no credit understanding of the buyer– KYC (Important)

14

Open Account

• Seller Ships• Buyer Pays

– Wire Transfer– Check– Draft– Credit Card

• Ship it and hope you get paid • Foreign import regulations may prohibit• Full Country & Buyer Credit Risk• Consider payment type (wire transfer best)• Requires extensive knowledge of the buyer

(underwriting, trade references, excellent reputation)

15

Letters of Credit

A versatile tool for closing the gap that exists between buyers and

sellers.

16

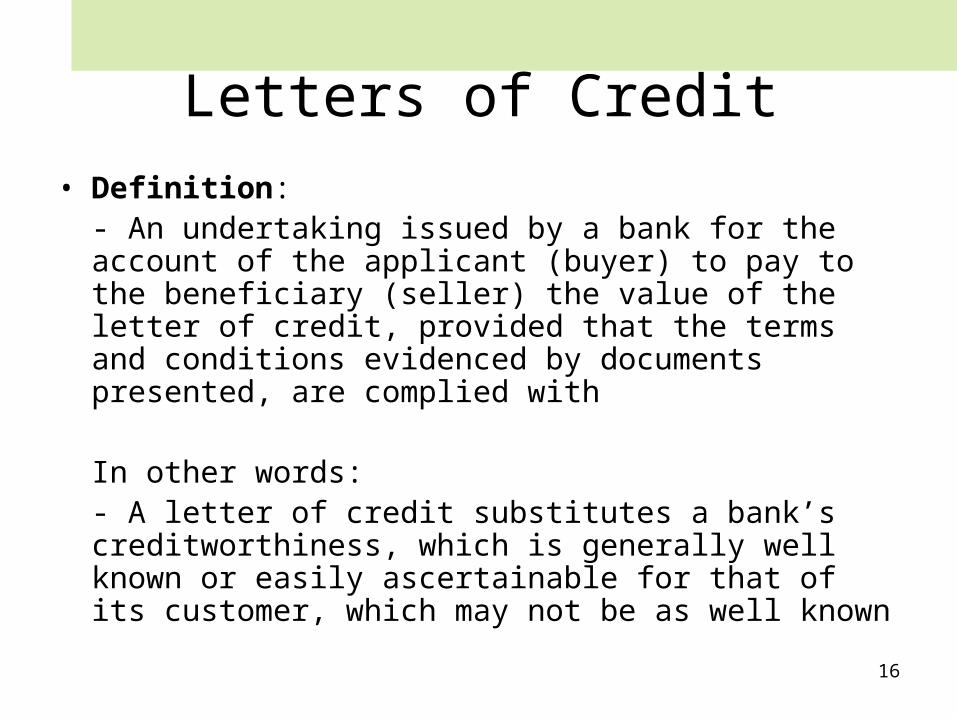

Letters of Credit

• Definition:- An undertaking issued by a bank for the account of the applicant (buyer) to pay to the beneficiary (seller) the value of the letter of credit, provided that the terms and conditions evidenced by documents presented, are complied with

In other words:- A letter of credit substitutes a bank’s creditworthiness, which is generally well known or easily ascertainable for that of its customer, which may not be as well known

17

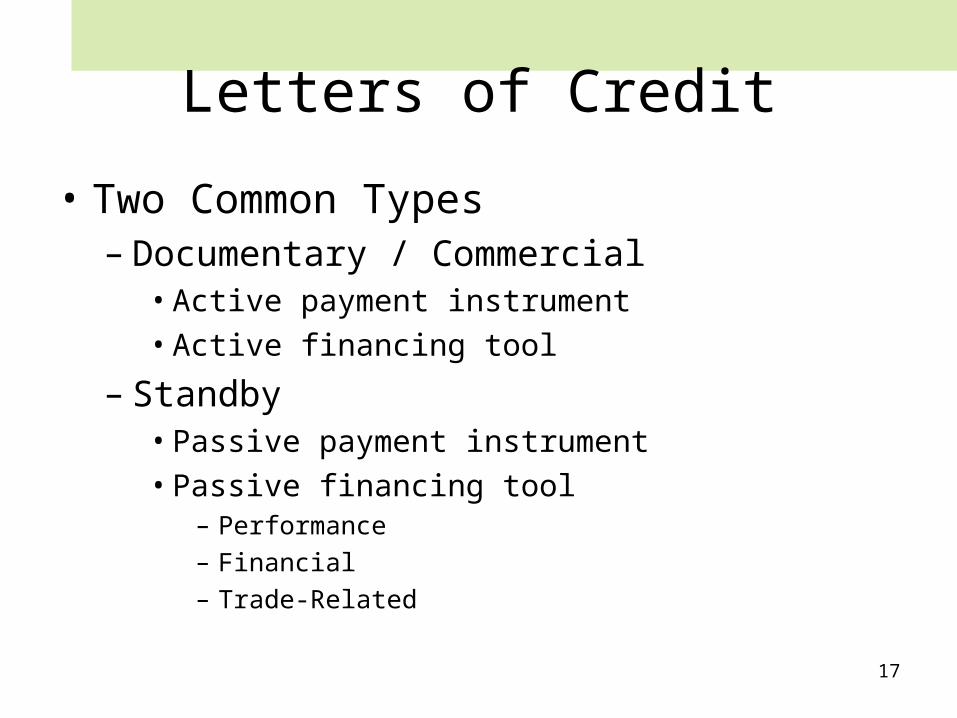

Letters of Credit

• Two Common Types– Documentary / Commercial

• Active payment instrument

• Active financing tool

– Standby• Passive payment instrument

• Passive financing tool– Performance– Financial– Trade-Related

18

Independence Principle

Importer (Buyer)Buyer has an obligation to the

Issuing Bank to pay upon claim for

payment

Issuing Bank has the obligation to the Exporter to pay if he has complied with all the terms and

conditions in the L/C

Exporter and Importer have a sales contract between them which

supports the underlying transaction

Issuing Bank Exporter (Seller)

Separate Contracts

Advising/Confirming bank

19

Sales Contract

(Issuing Bank) (Advising Bank)

Sight LC Transaction FlowBuyer (Applicant) Seller (Beneficiary)

22

Application

Foreign BANK PNC Bank

44

LC Advised

33

LC Issued

11

Importer (Buyer)

Issuing Bank

Exporter (Seller)

Advising/Confirming bank

20

Shipment

Documents

Payment Claim

Buyer pays BEFORE receipt

of goods

Sight LC Transaction Flow

5

$

Buyer Seller

(Applicant)

Foreign BANK PNC Bank

8

7

$

8

6$8

21

Time LC Transaction Flow

Shipment

Payment Documents

Payment At Maturity

5

$

Buyer Seller

(Applicant)

Foreign BANK PNC Bank

8

$

8

6$8 Documents6 Documents

Acceptance7

6

Advised Letters of Credit

Beneficiary:• Bears credit risk of the issuing bank• Bears full country risk of the transaction• Responsible for ensuring compliance with Pro Forma

Advising Bank: • Responsibility limited to authentication • Has no payment obligation • Advocate for beneficiary

23

Role of the Advising Bank

• Verify the authenticity of the Letter of Credit, thereby protecting the beneficiary from fraud

• Advocate for the beneficiary– No conflict of interest

• Other benefits of using your bank– Commitment to Customer Service– Relationship Pricing– Consistency in Processing

If you want more protection the next step is to consider having the letter of credit confirmed

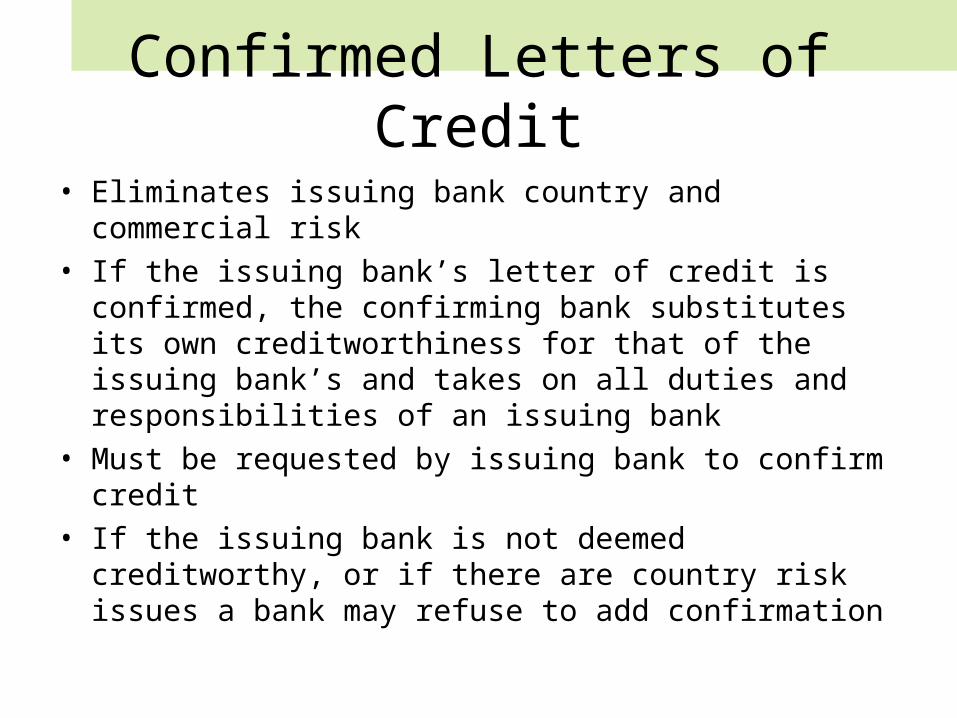

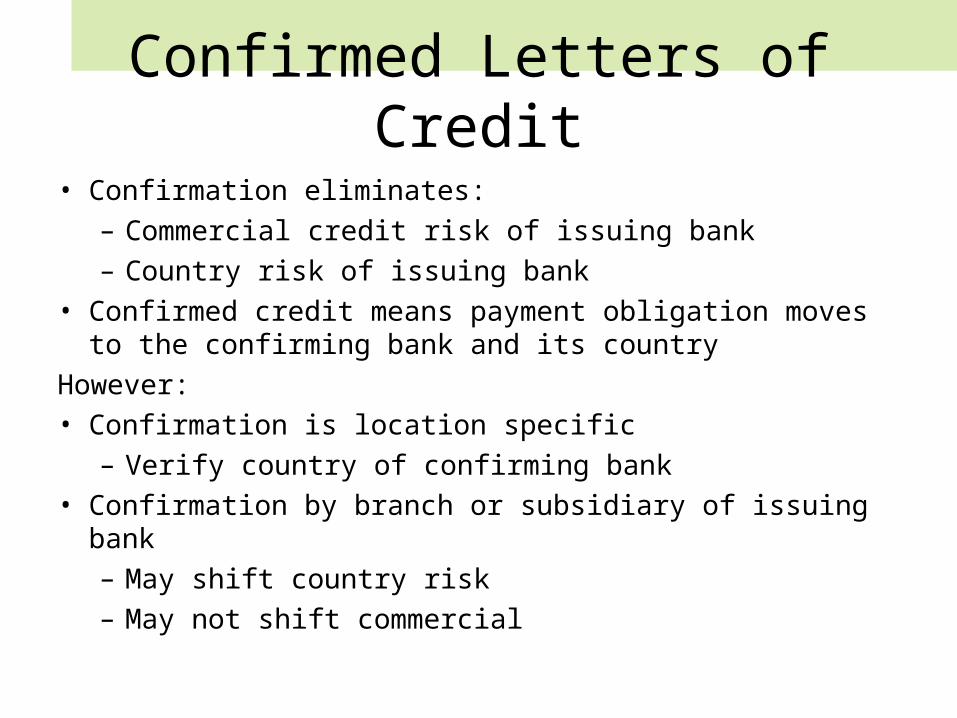

Confirmed Letters of Credit

• Eliminates issuing bank country and commercial risk• If the issuing bank’s letter of credit is confirmed, the

confirming bank substitutes its own creditworthiness for that of the issuing bank’s and takes on all duties and responsibilities of an issuing bank

• Must be requested by issuing bank to confirm credit• If the issuing bank is not deemed creditworthy, or if there

are country risk issues a bank may refuse to add confirmation

Confirmed Letters of Credit

• Confirmation eliminates:

– Commercial credit risk of issuing bank

– Country risk of issuing bank

• Confirmed credit means payment obligation moves to the confirming bank and its country

However:

• Confirmation is location specific

– Verify country of confirming bank

• Confirmation by branch or subsidiary of issuing bank

– May shift country risk

– May not shift commercial

26

Payment Method: Letter of CreditSet it up right!

1. Irrevocable2. Issue Date, Expiry Date &

Location3. Issuing Bank/Advising Bank4. Importer/Exporter5. Value & Currency6. Description of Goods/Services7. Required Documents8. Payment Terms9. Incoterms

10.Port-To-Port Info

11.UCP 600

12.LC Fees - Who Pays?

13.Latest Ship Date

14.Presentation Date

15.Partial Shipments (Y/N)

16.Transshipments (Y/N)

17.Paying Bank

18.Drawee Bank

19.Reimbursing Bank

20.Confirming Bank

20 Points of Negotiation in Structuring your LC

27

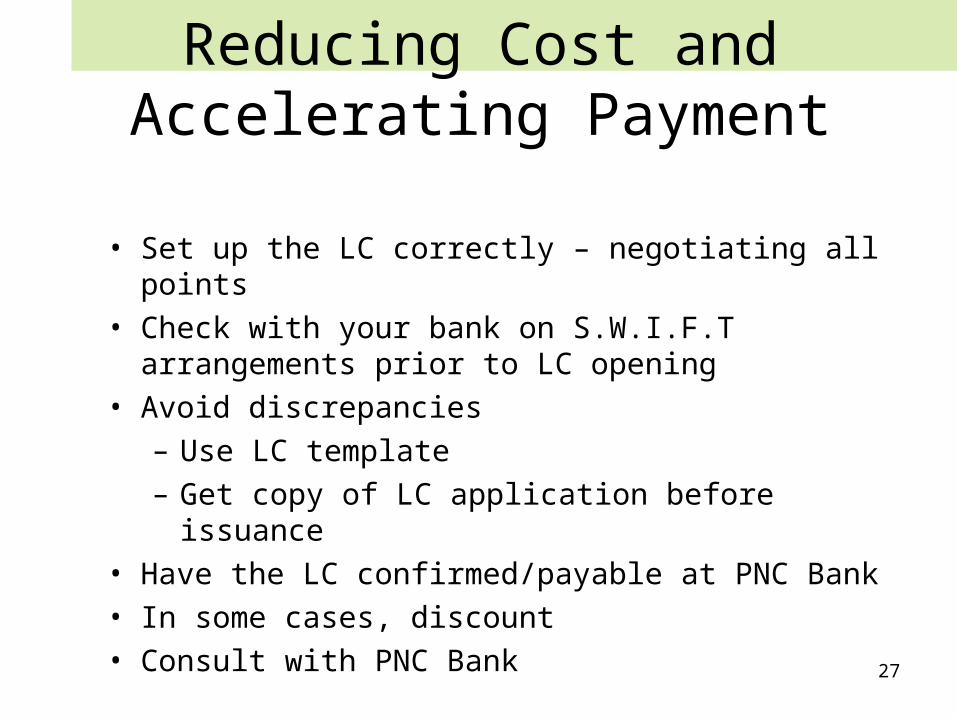

Reducing Cost and Accelerating Payment

• Set up the LC correctly – negotiating all points• Check with your bank on S.W.I.F.T arrangements

prior to LC opening• Avoid discrepancies

– Use LC template– Get copy of LC application before issuance

• Have the LC confirmed/payable at PNC Bank• In some cases, discount• Consult with PNC Bank

28

What to do When the LC Arrives

• Read the letter of credit very carefully• Ensure you can comply with the terms (all 20+ points)• Send copy of LC to freight forwarder• Ask about anything you don’t understand• If incorrect, reject the LC immediately• If necessary, request the buyer amend the Letter of

Credit

29

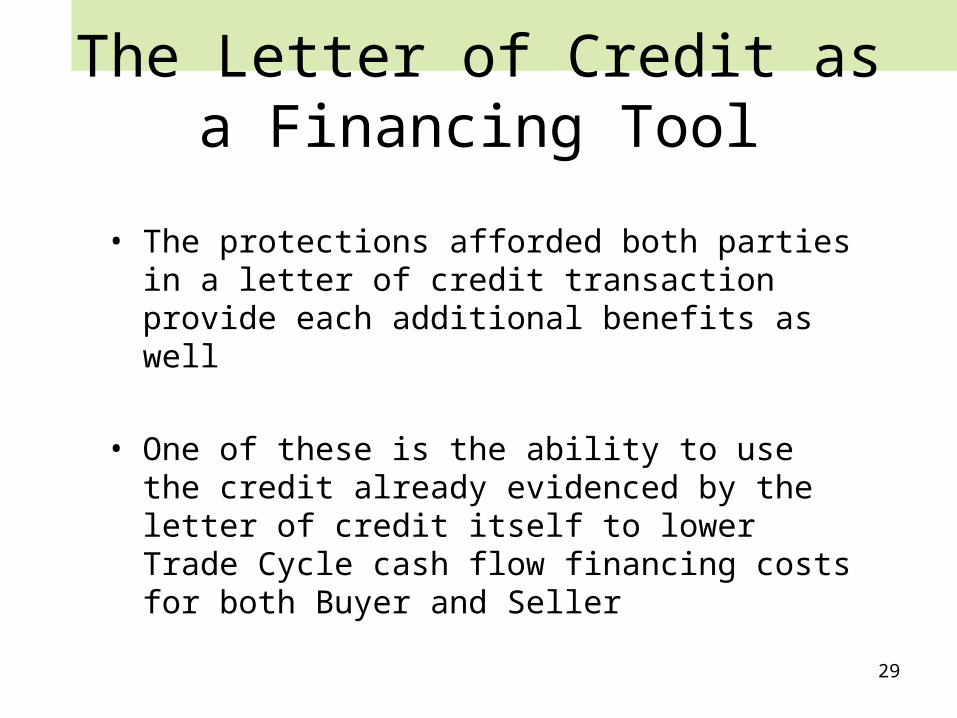

The Letter of Credit as a Financing Tool

• The protections afforded both parties in a letter of credit transaction provide each additional benefits as well

• One of these is the ability to use the credit already evidenced by the letter of credit itself to lower Trade Cycle cash flow financing costs for both Buyer and Seller

30

Documentary Collections

• Disguised open account transactions

• Less secure than letters of credit

• More secure than open account

• Benefits– Don’t encumber buyer’s line of credit– Very inexpensive– Effective if properly structured

• Use of correct Incoterms• Role of banks and freight forwarders

31

Shipment

Buyer pays BEFORE receipt of goods

Sight Collection (D/P)

2

Documents2

Documents3

4

$

4 $4$

Documents4

Foreign BANK PNC Bank

Buyer SellerBuy/Sell Agreement

1

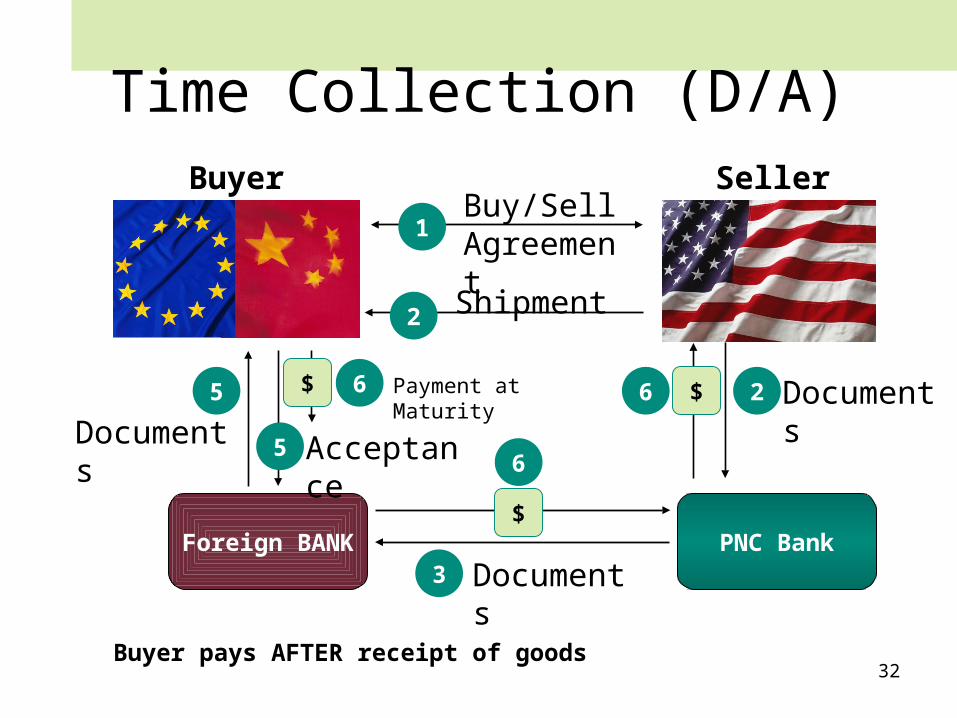

32Buyer pays AFTER receipt of goods

Time Collection (D/A)

Documents2

Documents3

6

$

6 $6$

Documents5

Foreign BANK PNC Bank

Payment at Maturity

5 Acceptance

Buyer Seller

Shipment2

Buy/Sell Agreement

1

33

Documentary Collection

Transaction Flow• Seller ships• Seller presents documents to National City• National City sends documents to a correspondent• Correspondent bank releases documents against:

– Payment (if Documents against Payment – D/P)– Acceptance (if Documents against Acceptance – D/A)– Note: D/A terms represent more risk to the seller.

• Correspondent wires funds to National City• National City pays seller

34

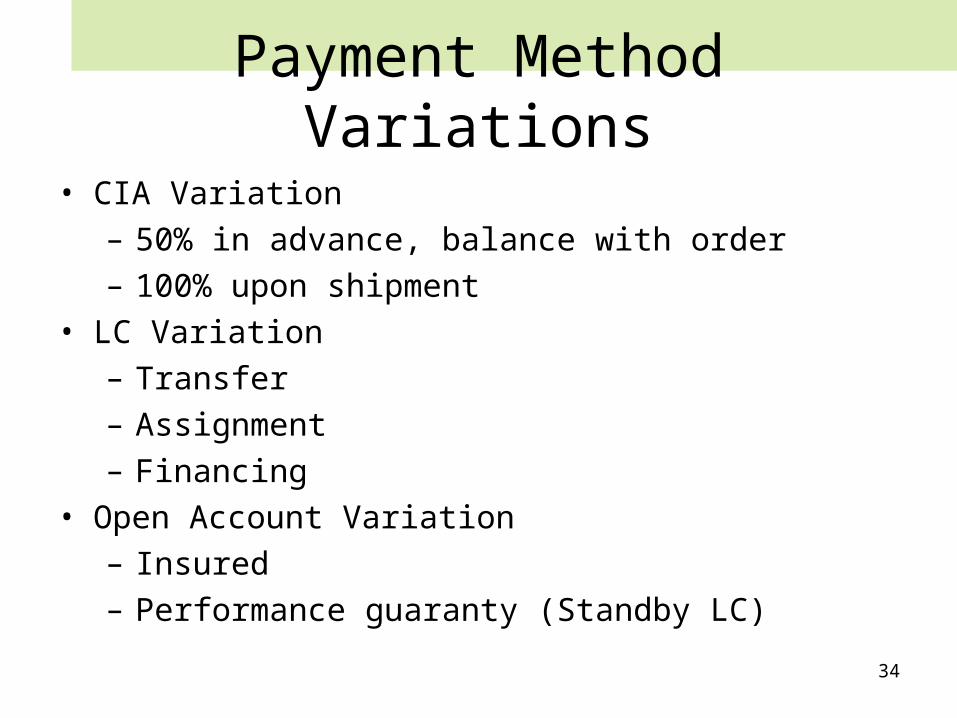

Payment Method Variations

• CIA Variation– 50% in advance, balance with order– 100% upon shipment

• LC Variation– Transfer– Assignment– Financing

• Open Account Variation– Insured– Performance guaranty (Standby LC)

35

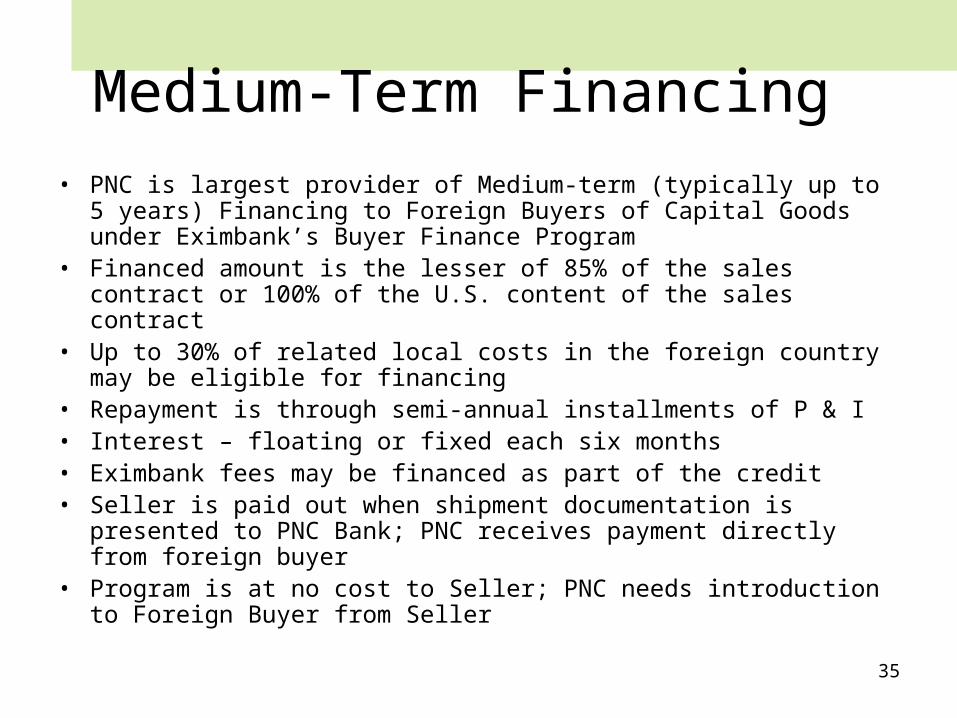

Medium-Term Financing

• PNC is largest provider of Medium-term (typically up to 5 years) Financing to Foreign Buyers of Capital Goods under Eximbank’s Buyer Finance Program

• Financed amount is the lesser of 85% of the sales contract or 100% of the U.S. content of the sales contract

• Up to 30% of related local costs in the foreign country may be eligible for financing

• Repayment is through semi-annual installments of P & I• Interest – floating or fixed each six months• Eximbank fees may be financed as part of the credit• Seller is paid out when shipment documentation is presented to

PNC Bank; PNC receives payment directly from foreign buyer• Program is at no cost to Seller; PNC needs introduction to Foreign

Buyer from Seller

36

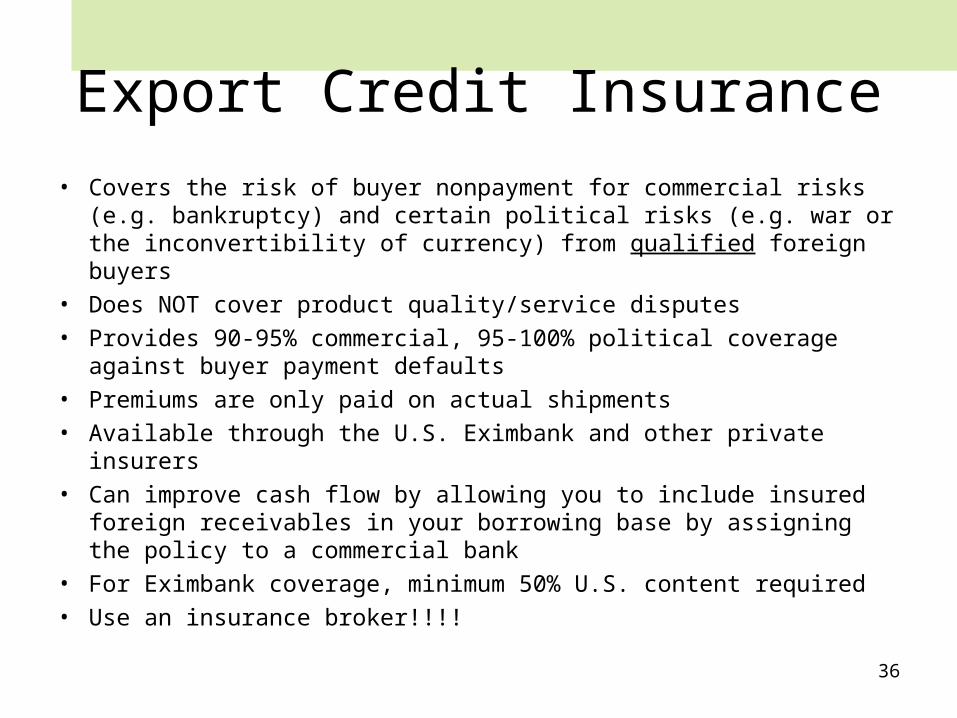

Export Credit Insurance

• Covers the risk of buyer nonpayment for commercial risks (e.g. bankruptcy) and certain political risks (e.g. war or the inconvertibility of currency) from qualified foreign buyers

• Does NOT cover product quality/service disputes• Provides 90-95% commercial, 95-100% political coverage against

buyer payment defaults• Premiums are only paid on actual shipments• Available through the U.S. Eximbank and other private insurers• Can improve cash flow by allowing you to include insured foreign

receivables in your borrowing base by assigning the policy to a commercial bank

• For Eximbank coverage, minimum 50% U.S. content required• Use an insurance broker!!!!

37

“Examples and War Stories”

• Trust Gone Awry on a Documentary Collection• When the credit markets freezed up• “If it sounds too good to be true, it probably is…”• In general, “Possibly trust, but verify…”

38

Contact Information

• Bill Richeson, CTP

Senior Vice President

International Division

PNC Bank

Phone: (616)771-8849

e-mail: [email protected]

SWIFT: PNCCUS33ENJ

Global Client Care Center: 800-682-4689

39