1 Dr Mojeed Olujinmi A. Alabi CAFRAD REVIEW OF THE MISSIONS OF AUDIT INSTITUTIONS IN AFRICA IN THE...

34

1 Dr Mojeed Olujinmi A. Alabi CAFRAD REVIEW OF THE MISSIONS OF AUDIT INSTITUTIONS IN AFRICA IN THE CONTEXT OF THE GLOBAL ECONOMIC/FINANCIAL CRISIS

-

Upload

randell-merritt -

Category

Documents

-

view

216 -

download

0

Transcript of 1 Dr Mojeed Olujinmi A. Alabi CAFRAD REVIEW OF THE MISSIONS OF AUDIT INSTITUTIONS IN AFRICA IN THE...

1

Dr Mojeed Olujinmi A. Alabi CAFRAD

REVIEW OF THE MISSIONS OF AUDIT

INSTITUTIONS IN AFRICA IN THE CONTEXT OF

THE GLOBAL ECONOMIC/FINANCIAL CRISIS

2

Paper Presented at the 2nd Pan-African Conference of Auditors-General

Tangier, Morocco, 14-16 December 2009

• Dr Mojeed Olujinmi A. AlabiExpert in Good Governance, Ethics & Professionalism in the Public SectorAfrican Training and Research Centre in Administration for Development (CAFRAD)[email protected]; [email protected]+212645902676, +2348068964365, +447509106047

3

Why Audit of Financial Information?

• Significance of Transparency and Accountability for Good Governance (Africa & Global)

• Failure of Accountability/Transparency breeds corruption and economic mismanagement

• Good governance requires independence & autonomy of audit institutions

• Role of Auditors in promoting good governance and political stability – sound financial management is a key element of good governance

• Significance of national and jurisdictional regulatory systems audit institutions for financial accountability

4

Why Accountability?

• Accountability is critical to development objectives

• Governments & donor agencies use public resources; need for “transparent, economic, and efficient use of public funds” (Cheryl W. Gray, Independent Evaluation Group, the World Bank, 2008)

• Primary responsibility to respective constituencies

5

Accountability for Whom? (Audit Stakeholders)

• Citizens’ demand for service delivery and results• The Parliaments as Controllers of Public Funds• Civil Society Organisations (CSOs) committed to accountability and good governance

• International Donor and Finance Agencies, in order to protect their assistance/investments against misuse

• External auditors• Regulatory authorities

6

Requirements of Accountability

• Sound and efficient public financial management (PFM) systems

• Constant assessment and overhaul of the strengths and weaknesses of PFM systems for improved performance and results

7

Why Auditing?Audit of financial information serves many useful purpose in society:

. Helps to strengthen domestic financial systems by encouraging sound regulation and supervision

• Makes for greater transparency and accountability• Assists to provide more efficient and robust institutions, markets

and infrastructures, in both the private and the public sectors• For the private sector especially, it assists to provide financial

stability by facilitating better-informed lending and investment decisions

• Helps to promote/improve integrity integrity in government and other corporate operations

• Helps to avert/reduce the risks of financial distress and system collapse

8

Global Economic/Financial Crisis?!

• The global economic/financial crisis is therefore

a failure of audit !

. Couldn’t audit have helped prevent or at least moderate the impact of the crisis?

9

Additional Challenges of Auditing in Africa

• Political• Economic• Constitutional/Legal• Bureaucratic• Financial• Institutional• Lack of Human Capacity• Socio-Cultural – illiteracy, etc

10

Has the Crisis any impact on Auditing Practice?

• Although there are disagreements on whether and the extent of the crisis on Africa, available data shows an awareness of the effect among auditors and audit staff as the statistics below show

• A survey by the Global Audit Information Network (GAIN), a premier benchmarking programme of the Institute of Internal Auditors (IIA) shows the following results for Africa:

11

Impact on Organisation

• 1: Overall, how would you rate the impact of the current economic crisis on your organization

• Little or no impact 25.9% • Mild 29.6% • Moderate 28.7% • Severe 9.3%• Enterprise threatening 6.5%

12

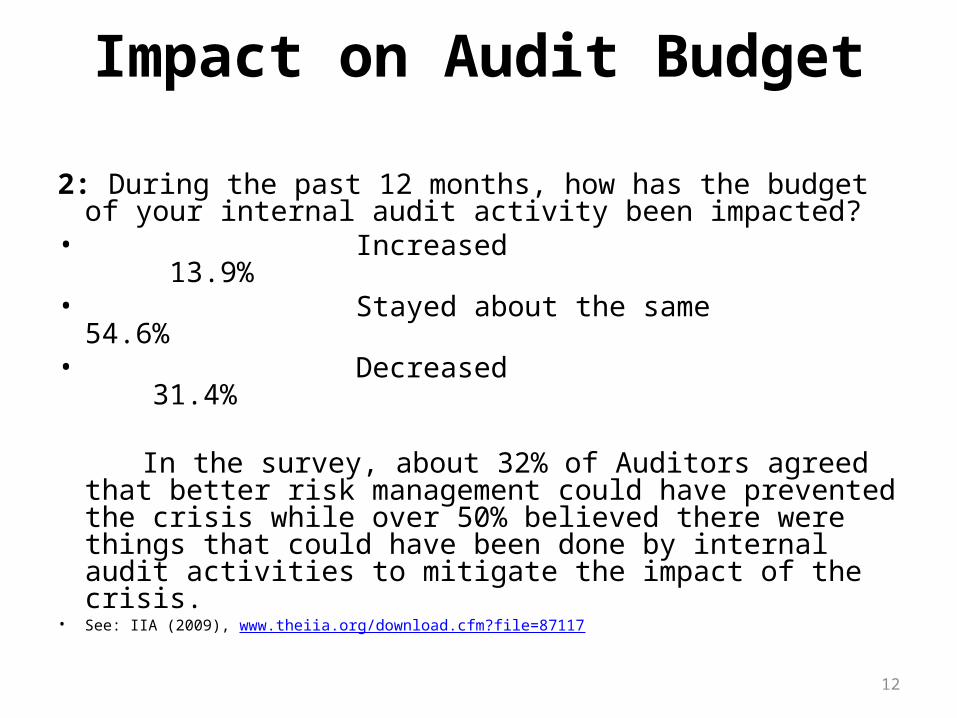

Impact on Audit Budget

2: During the past 12 months, how has the budget of your internal audit activity been impacted?

• Increased 13.9% • Stayed about the same 54.6% • Decreased 31.4%

In the survey, about 32% of Auditors agreed that better risk management could have prevented the crisis while over 50% believed there were things that could have been done by internal audit activities to mitigate the impact of the crisis.

• See: IIA (2009), www.theiia.org/download.cfm?file=87117

13

Impact on Audit , based on a survey by IIA

• Reduction in travels and cut on travel related expenses• reduction in training expenses (more than 80% responses)• reduction in/elimination of contracting and other

administrative expenses• staff compensation frozen/reduced• freeze on employment/vacancies not filled• layoff of internal audit staff/retrenchment• negative impact on overhead costs, eg stationery,

accommodation, office equipment• implementation of third party audits management

relaxation measures

14

Responsibility for the Crisis?

• Auditors have not been in the eyes of the storm as the political gladiators who are under increasing pressures from the citizenry to fix the economy, or the financial regulators who are blamed for not keeping the excesses of the CEOs in check, or even the academics who are asked to explain the failure of tested theories and assumptions.

• Nonetheless...

15

Auditors … Blameworthy!• Auditors have been blamed for causing, or at least failing to prevent or foresee the crisis.

• Nick Mathiason noted in The Observer (UK) of Sunday 25 October 2009, auditors “signed off trillion-dollar balance sheets, sanctioned increased dividends in bank shares that collapsed months later, blithely assumed markets would function seamlessly and established controversial rules that inflated bubbles and amplified losses”.

16

Key Observations/Global Trends

• The global economic/financial downturn is significantly impacting the internal audit profession

• Internal auditors were not ad idem on whether better risk management could have played any mitigating role in the crisis

• But, the majority felt “there were more things internal audit activities could have done” in order to soften its impact

• The recession has impacted the resources of internal audit functions.

• Accordingly, organisations are redirecting their internal audit resources to cover recession-related risks; and,

See: http://www.theiia.org/theiia/newsroom/newsreleases/index.cfm?i=9822

17

Areas of Realisation

• To what extent are African auditors ‘redirecting’ their resources to cover recession and post-recession related risks as a way of not only mitigating the effects of the current meltdown but also preventing a re-occurrence, at least in the foreseeable future?

• In what ways has the recession impacted on the practice of auditing in Africa?

• What aspects of the missions of chief audit executives need to be redefined and how do we go about these?

18

Implications of the Crisis for Audit Institutions in Africa

• Auditors and accountants would be under increasing pressure to prepare more accurate account books and detect frauds financial irregularities timely

• Auditors and accountants would face greater challenge to their professional integrity, and might face lawsuits for failure to detect frauds and financial irregularities

19

More…

• Government audits would be under immense pressure to strictly follow the code of accounting ethics to prevent financial frauds and corrupt practices with a view to improving public service management (PSM)

• Auditors would be expected to convince or exert pressure on their clients (governmental and non-governmental) to make disclosures of financial details that could be relevant to proper risk assessment/management

20

Response Mechanisms• One response mechanism, suggested by the WB (2008), is

that analyses and diagnosis of the PFM systems of (African) countries (including public expenditure management, financial management (FM), and procurement) be carried out on a regular basis

• The objectives are: To further developmental objectives, by helping to identify goals, define priorities, and adopt implementation strategies; and, to help ensure that public funds are judiciously used

• With or without the assistance of the World Bank, individual or group of countries could develop instruments of assessment, based on their peculiarities but in line with international (or regional) shared (not necessarily ‘best’) practices.

21

Risk-based Auditing• The response mechanisms may include cost containment and expense

reduction, but we need to do more.

• Shifting of auditing resources to risk management. New approaches to risk management, with focus on such factors as “probability, possible impacts of risks, and ... preparedness for these risks”. (IIA). As the IIA found, the trend should be towards paying more attention to operational risks, the effectiveness of risk management, compliance, etc.

• Risk calculation and accountability assessment should not ignore the private sector.

• Regulatory agencies have to play their own role too, and where regulatory frameworks are lacking or weak, auditors have a duty to raise early warning audit alarms that could trigger appropriate actions before any bubble could burst.

• The overall focus should be on effectiveness of risk management.

22

New Directions and Missions• A realisation that needs and expectations constantly change, and the need

to move with the dynamics of changing expectations; no adherence to rigid rules without contextualising them in the light of changing expectations

• Audit is required to be more coherent in its operation and comprehensive in scope

• Focus on attainment of performance and results• Updating accounting standards regularly to take into account new

directions, ideas, concepts, techniques and tools, as well as giving guidelines on the role of auditing before, during and after the crisis;

• Emphasis on effectiveness auditing and assurance, ethics, education and public sector accounting standards by the International Federation of Accountants (IFAC), International Auditing and Assurance Standards Board (IAASB), Institute of Internal Auditors (IIA) and such other international, regional and national standards-setting bodies.

23

Further Directions and Missions

• Marketing of audit activities to get the top policy makers to give priorities to the needs and requirement of proper auditing, including workshops to non-internal audit staff to enable them understand the role of audit

• Develop and emphasise the importance, strategies and effectiveness of risk management

• Training and capacity-building programmes for audit staff on performance audit, results-based audit, etc., and skills to identify risk exposures and give guidance on mitigating control mechanisms

24

Higher Missions• A realisation that risks of material misstatements in financial

reports are significantly higher than hitherto. Accordingly, audit reports should include: (a) overall decision regarding performance; (b) material weakness in design/implementation of internal controls; (c)report of fraud/financial irregularities; and (d) any doubts about the performance of the organisation/agency

• Early planning of the overall audit strategy; this requires consultation and thorough understanding of work/mandate of the org/agency

• Prior determine early before the audit begins what would constitute material misstatement in the light of the work

25

More on Higher Missions• of an organisation/agency, the expectations of the users of

audit reports, some preliminary assessment of the risks involved, and design of strategies for getting maximum information on grey areas

• Greater attention to areas of risks, particularly management bias (with or without fraudulent intent), fraud, and performance indices. Accordingly, pay attention to the nature, extent and timing of risk assessment procedures; effectiveness of internal controls designed to prevent, detect and correct material misstatements; those risks that require special audit consideration (estimates and disclosures); whether special audit procedures are required; and your response to the possibility of fraud

• For more, see: http://gfc.cpaaustralia.com.au/toolkit/tips-for-auditors-in-the-global- ...

26

Policy Considerations for Governments

• Maintain the independence and integrity of audit institutions

• Infrastructural upgrade, including ICT, to enhance audit and fraud detection

• Legal and institutional reforms of the audit system in furtherance of transparency and accountability

27

Policy Considerations (2)

• Simplicity and clarity in the presentation of audit reports to make them intelligible to parliamentarians and the general public who are the major stakeholders

• Audit reports should be widely publicised while the CSOs should assist in disseminating the contents and imports of such reports

28

Policy Considerations (3)

• Capacity-building and improvement for audit staff to be able to meet the challenges of auditing in a post-crisis situation

• The importance of leadership skills in the functioning and management of audit institutions cannot be over-emphasised

• Political will on the part of Parliament and the government to implement audit reports and sanction offenders

29

Policy Considerations (4)

• Comprehensive anti-corruption/ethics/ integrity strategies honestly implemented to compliment audit investigations and recommendations

• Overall goal - restructuring, modernisation and reinventing of the audit systems for greater transparency and accountability

30

Pearls of Wisdom for Auditors• Think unconventionally• Maintain your professional skepticism• Reassess risks; identify the most significant client exposures• Consult early and regularly with those charged with

governance; and with management, audit committees and experts

• Raise awareness about your work• Keep abreast of the latest ideas, technology, tools, as well as

guidance issued by standard setters and regulators• AND…

31

Be on Alert !!!• Auditors must constantly been on alert in the discharge of their professional duties as the demand of good governance in modern times requires that the monitors be also under constant surveillance

• Unlike the past mistakes, politicians and administrators would be willing, more than ever before, to grill accountants and auditors over what Nick Mathiason called ‘self-regulation and apparent conflicts of interest”.

32

And, finally…

• Watch your back

• OTHERS ARE

WATCHING YOU !!!

33

Quis Custodiet Custodes?

• • •

34

Merci beaucoup!

Thank you