1 Development of Financial Markets in India Rakesh Mohan Deputy Governor Reserve Bank of India...

26

1 Development of Financial Markets in India Rakesh Mohan Deputy Governor Reserve Bank of India Lecture at the First Indian-French Financial Forum at Mumbai, May 16, 2007

-

Upload

gabriel-jackson -

Category

Documents

-

view

213 -

download

0

Transcript of 1 Development of Financial Markets in India Rakesh Mohan Deputy Governor Reserve Bank of India...

1

Development of Financial Markets in India

Rakesh MohanDeputy Governor

Reserve Bank of India

Lecture at the First Indian-French Financial Forum

at Mumbai, May 16, 2007

2

Scheme of the Presentation

Role of Financial Markets Money Market Government Securities Market Foreign Exchange Market Financial Market Integration

3

Role of Financial Markets

Intermediate between savers and investors Generate resources for investment and growth Allocate resources efficiently Improve the efficacy of the transmission

mechanism of monetary policy

4

Financial Markets in Pre-reform Period – Major Problems

Administered Interest rates Limited Instruments Restrictions on Participation Segmentation of Markets

5

Money Market

Role of the Money Market Key role in the transmission of monetary policy

impulses Major Reforms Introduced

Development of the Liquidity Adjustment Facility Development of collateralised instruments – CBLO and

Market Repo Modification in issuance norms and maturity profile of

CD and CP Setting up of central counter party – Clearing

Corporation of India Ltd. (CCIL)

6

Money MarketImpact – Increase in Activity

(Rupees crore)

Average Daily Turnover Outstanding Amount

Year Call Money Market

Market Repo

(Outside the LAF)

Collateralised Borrowing and

Lending Obligation

(CBLO)

Term Money Market

Money Market - Total (2 to5)

Commercial

Paper

Certificates of Deposit

1 2 3 4 5 6 7 8

1997-98 22709 - - - 22709 1500 14296

1998-99 26500 - - - 26500 4770 3717

1999-00 23161 6895 - - 30056 7014 1908

2000-01 32157 10500 - - 42657 6751 1199

2001-02 35144 30161 - 195 65500 7927 949

2002-03 29421 46960 30 341 76752 8268 1224

2003-04 17191 10435 515 519 28660 7835 3212

2004-05 14170 17135 6697 526 38528 11723 6052

2005-06 17979 21183 20039 833 60034 17285 27298

2006-07 21725 33676 32390 1012 88803 21478 64954

7

Money MarketImpact – Decline in Volatility

LAF Corridor and Call Rate

0

5

10

15

20

25

5-Ju

n-00

11-J

an-

01

19-A

ug-

01

27-M

ar-

02

2-N

ov-

02

10-J

un-

03

16-J

an-

04

23-A

ug-

04

31-M

ar-

05

6-N

ov-

05

14-J

un-

06

20-J

an-

07

Per c

ent

Call Rate Reverse Repo Rate Repo Rate

8

Money MarketImpact – Decline in Volatility

Variation in Call Money Rates

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

Coe

ffici

ent o

f var

iatio

n

9

Money Market Impact – Improvement in Efficiency

Bid-Ask Spread in the Call Money Market

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

1.25

1.50

4/1

/20

04

5/2

0/2

00

4

7/2

/20

04

8/1

3/2

00

4

9/2

7/2

00

4

11

/6/2

00

4

12/1

5/2

00

4

1/1

9/2

00

5

2/2

5/2

00

5

4/6

/20

05

5/1

6/2

00

5

6/2

1/2

00

5

7/2

9/2

00

5

9/5

/20

05

10/1

1/2

00

5

11

/19

/20

05

12/2

4/2

00

5

1/3

1/2

00

6

3/8

/20

06

4/1

8/2

00

6

5/2

5/2

00

6

6/2

9/2

00

6

8/3

/20

06

9/8

/20

06

10/1

6/2

00

6

11

/23

/20

06

12/2

9/2

00

6

2/7

/07

Per

cen

t

Bid-Ask Spread Mean Mean + 2SD Mean - 2SD

10

Government Securities Market

Significance of the G-Sec. Market Enables smooth raising of government

borrowings Risk free rupee yield curve provides a benchmark

for pricing other debt instruments Plays a key role in the monetary policy

transmission mechanism

11

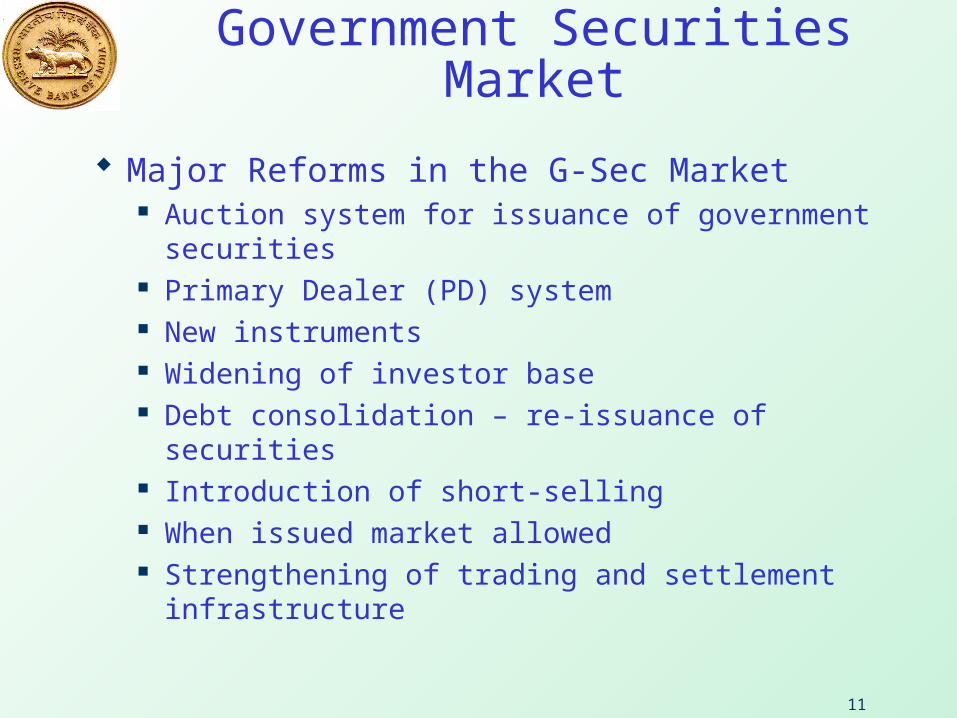

Government Securities Market

Major Reforms in the G-Sec Market Auction system for issuance of government securities Primary Dealer (PD) system New instruments Widening of investor base Debt consolidation – re-issuance of securities Introduction of short-selling When issued market allowed Strengthening of trading and settlement infrastructure

12

Government Securities Market - Impact

Turnover in Government Securities Market

0

20

40

60

80

100

120

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07

0

50

100

150

200

250

300

350

400

Per cent of GDP Per cent of Stock (right scale)

13

Government Securities MarketReasons for the Recent Decline in Activity

Yield and Annual Turnover (market value)

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

Rs. c

rore

0

2

4

6

8

10

12

14

16

Per c

ent

Annual Turnover Yield on 10-year security (end-March)

14

Government Securities MarketEmergence of Yield Curve

Yield Curve Movement - SGL Transactions

4

6

8

10

12

14

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

Years to maturity

Per c

ent

Mar-97 Mar-00 Mar-03 Mar-04 Mar-05 Mar-06

15

Foreign Exchange Market

Major Reforms Market-determined exchange rate in 1993 Current account convertibility in 1994 Substantial liberalisation of capital account

transactions Greater flexibility to market participants to

undertake foreign exchange operations Improvement in market infrastructure

16

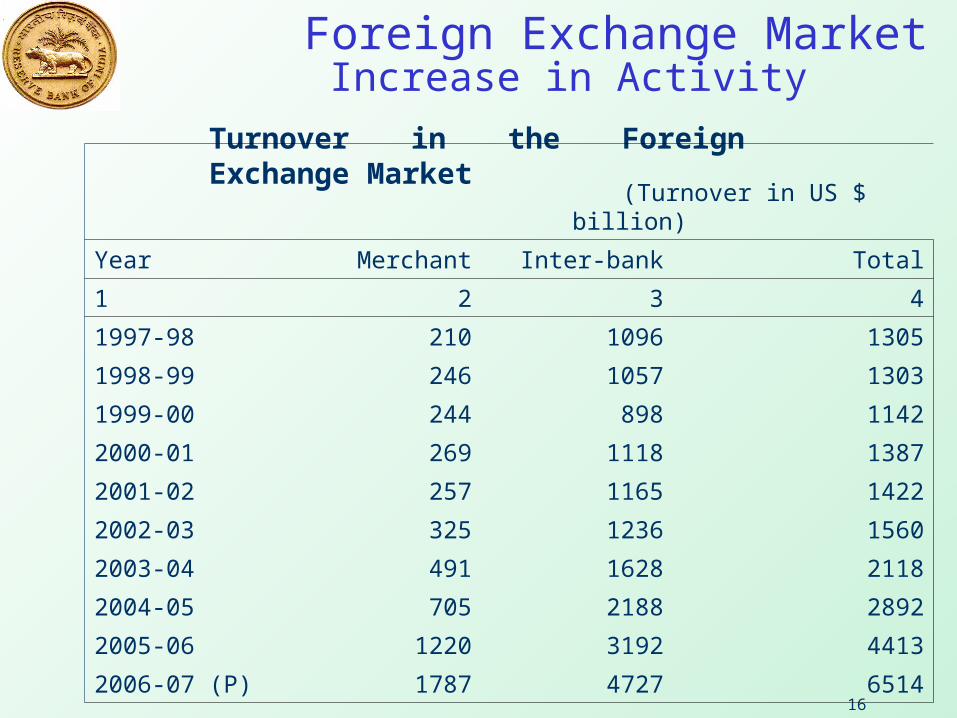

Foreign Exchange MarketIncrease in Activity

Turnover in the Foreign Exchange Market (Turnover in US $ billion)

Year Merchant Inter-bank Total

1 2 3 4

1997-98 210 1096 1305

1998-99 246 1057 1303

1999-00 244 898 1142

2000-01 269 1118 1387

2001-02 257 1165 1422

2002-03 325 1236 1560

2003-04 491 1628 2118

2004-05 705 2188 2892

2005-06 1220 3192 4413

2006-07 (P) 1787 4727 6514

17

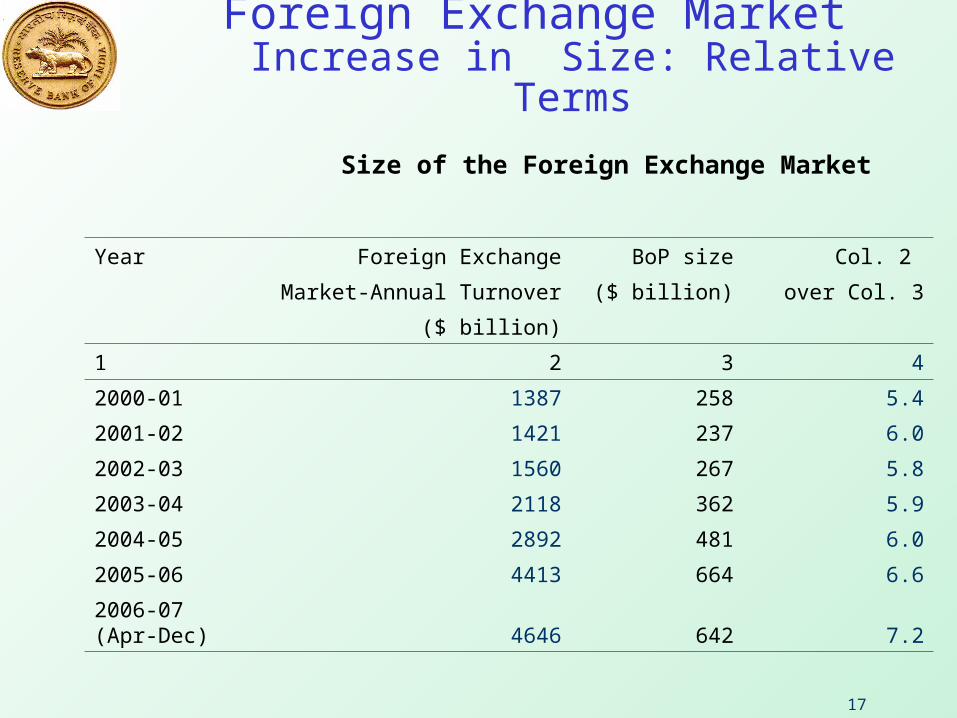

Foreign Exchange Market Increase in Size: Relative Terms

Size of the Foreign Exchange Market

Year Foreign Exchange BoP size Col. 2

Market-Annual Turnover ($ billion) over Col. 3

($ billion)

1 2 3 4

2000-01 1387 258 5.4

2001-02 1421 237 6.0

2002-03 1560 267 5.8

2003-04 2118 362 5.9

2004-05 2892 481 6.0

2005-06 4413 664 6.6

2006-07 (Apr-Dec) 4646 642 7.2

18

Foreign Exchange Market Improvement in Efficiency

Bid-Ask Spread of Select Currencies agains US Dollar

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1/3/

2000

5/3/

2000

9/3/

2000

1/3/

2001

5/3/

2001

9/3/

2001

1/3/

2002

5/3/

2002

9/3/

2002

1/3/

2003

5/3/

2003

9/3/

2003

1/3/

2004

5/3/

2004

9/3/

2004

1/3/

2005

5/3/

2005

9/3/

2005

1/3/

2006

5/3/

2006

9/3/

2006

1/3/

2007

per c

ent

INR GBP EUR JPY

19

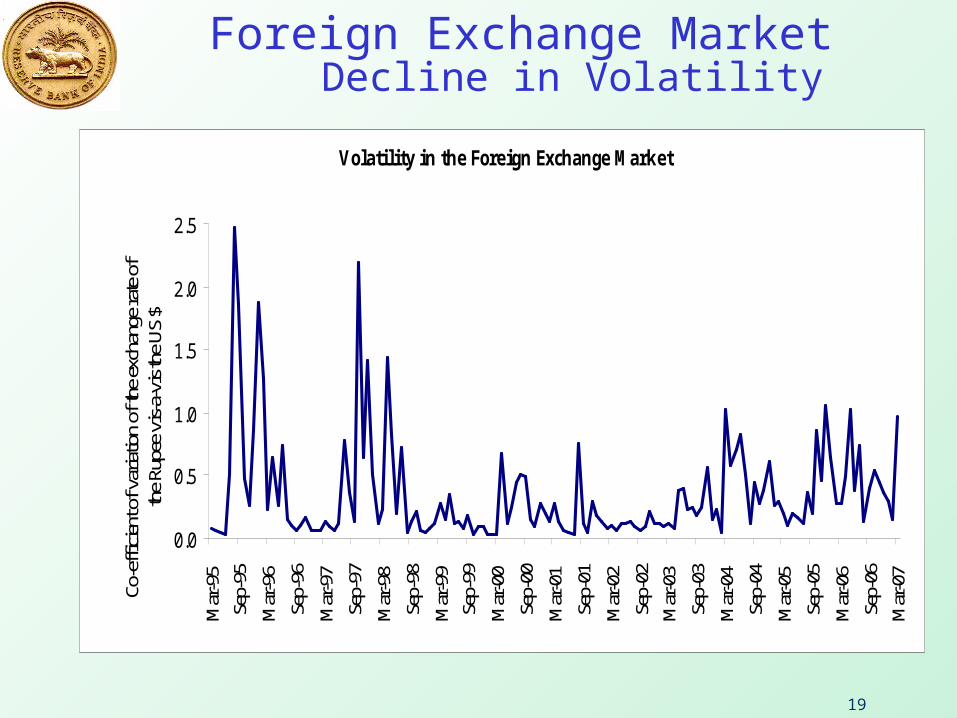

Foreign Exchange Market Decline in Volatility

Volatility in the Foreign Exchange Market

0.0

0.5

1.0

1.5

2.0

2.5M

ar-9

5Se

p-95

Mar

-96

Sep-

96M

ar-9

7Se

p-97

Mar

-98

Sep-

98M

ar-9

9Se

p-99

Mar

-00

Sep-

00M

ar-0

1Se

p-01

Mar

-02

Sep-

02M

ar-0

3Se

p-03

Mar

-04

Sep-

04M

ar-0

5Se

p-05

Mar

-06

Sep-

06M

ar-0

7

Co-e

ffic

ient

of v

aria

tion

of th

e ex

chan

ge ra

te o

f th

e Ru

pee

vis-

a-vi

s the

US

$

20

Financial Market Integration

Significance For monetary policy transmission framework

Evidence of stronger integration during the recent period (2000-2006) than the earlier period (1993-2000)

Correlation between the call rate and the reverse repo improved from 0.35 to 0.86

Correlation between the call rate and the 364-day Treasury Bills yield improved from 0.40 to 0.92

Correlation between the call rate and the 10-year yield improved from 0.46 to 0.88

Correlation between the call rate and the 6-months forward premia improved marginally from 0.61 to 0.62

Correlation between interest rates (the call rate) and the stock market improved from -0.10 to -0.23.

21

Financial Market Integration Interest Rates and Exchange Rate in India

-5

5

15

25

35A

pr-9

3

Feb-

94

Dec

-94

Oct

-95

Aug

-96

Jun-

97

Apr

-98

Feb-

99

Dec

-99

Oct

-00

Aug

-01

Jun-

02

Apr

-03

Feb-

04

Dec

-04

Oct

-05

Aug

-06In

tere

st R

ates

and

For

war

d Pr

emia

(Per

ce

nt)

0

10

20

30

40

50

Exc

hang

e R

ate

(Rs.

/US

$)

CALL 91-TBills FR3 CP

CD 10-Year G-Sec RREPO EXCH

22

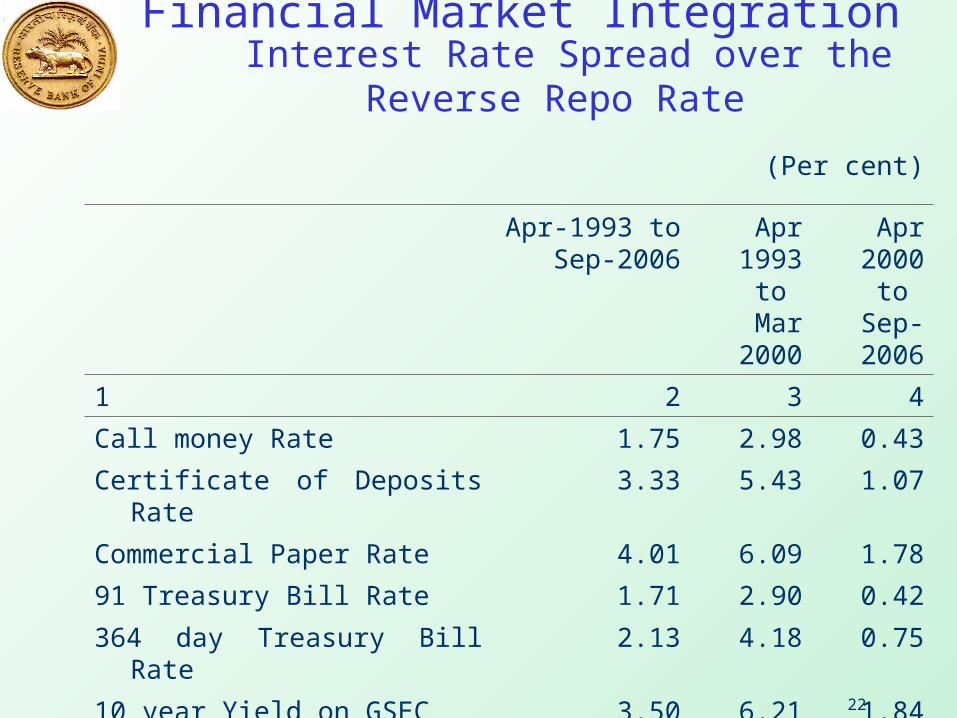

Financial Market Integration Interest Rate Spread over the Reverse Repo Rate

(Per cent)

Apr-1993 to Sep-2006

Apr 1993 to

Mar 2000

Apr 2000 to

Sep-2006

1 2 3 4

Call money Rate 1.75 2.98 0.43

Certificate of Deposits Rate 3.33 5.43 1.07

Commercial Paper Rate 4.01 6.09 1.78

91 Treasury Bill Rate 1.71 2.90 0.42

364 day Treasury Bill Rate 2.13 4.18 0.75

10 year Yield on GSEC 3.50 6.21 1.84

23

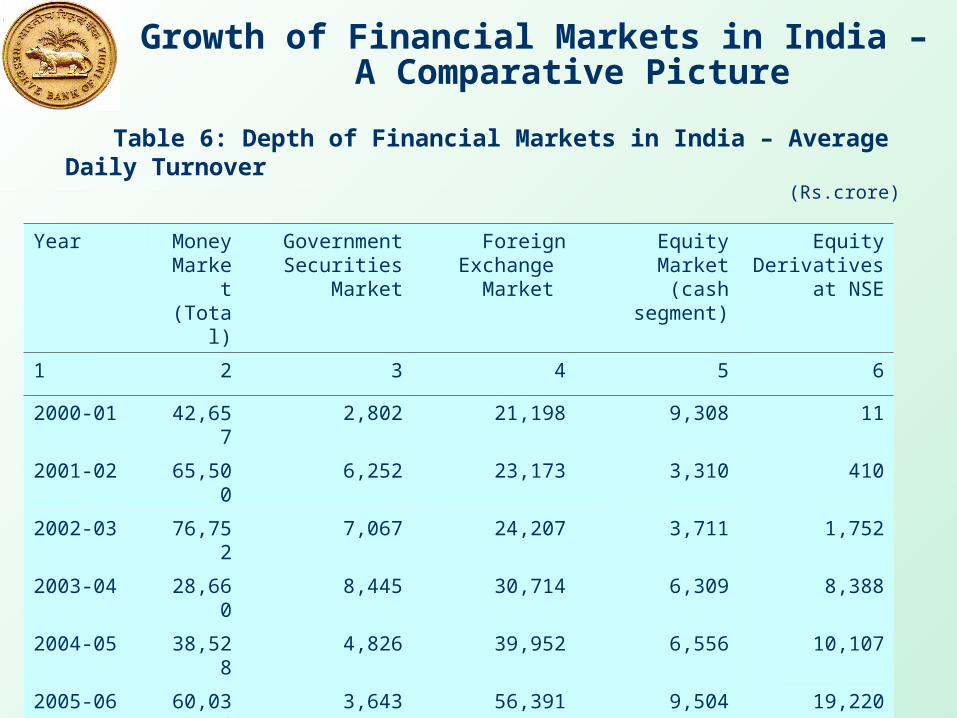

Growth of Financial Markets in India – A Comparative Picture

Table 6: Depth of Financial Markets in India – Average Daily Turnover(Rs.crore)

Year Money Market(Total)

GovernmentSecurities Market

Foreign Exchange

Market

Equity Market(cash segment)

EquityDerivatives

at NSE

1 2 3 4 5 6

2000-01 42,657 2,802 21,198 9,308 11

2001-02 65,500 6,252 23,173 3,310 410

2002-03 76,752 7,067 24,207 3,711 1,752

2003-04 28,660 8,445 30,714 6,309 8,388

2004-05 38,528 4,826 39,952 6,556 10,107

2005-06 60,034 3,643 56,391 9,504 19,220

2006-07 88,803 4,863 83,984 11,760 29,803

24

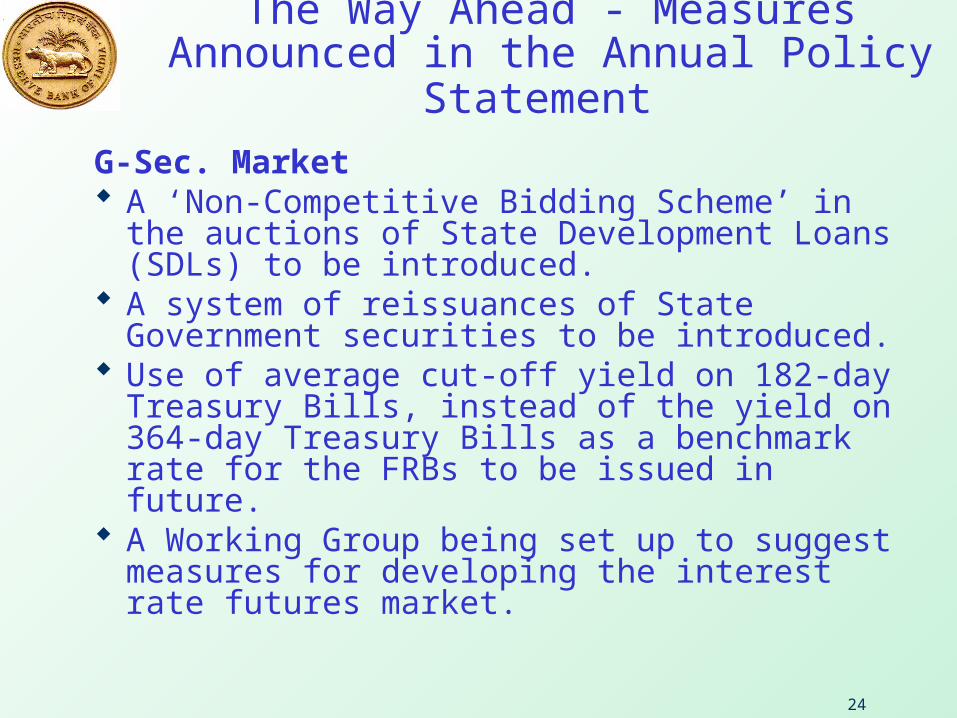

The Way Ahead - Measures Announced in the Annual Policy Statement

G-Sec. Market A ‘Non-Competitive Bidding Scheme’ in the

auctions of State Development Loans (SDLs) to be introduced.

A system of reissuances of State Government securities to be introduced.

Use of average cut-off yield on 182-day Treasury Bills, instead of the yield on 364-day Treasury Bills as a benchmark rate for the FRBs to be issued in future.

A Working Group being set up to suggest measures for developing the interest rate futures market.

25

The Way Ahead - Measures Announced in the Annual Policy Statement

Foreign Exchange Market Further liberalisation of foreign exchange facilities

in view of CFCAC Overseas investment limit to be enhanced Portfolio investment abroad limit to be enhanced Increase in the existing limit for prepayment of ECBs The limit for remittance scheme for individuals to be

enhanced Expanded the range of hedging tools available to the

market participants as also facilitate dynamic hedging by the residents

A Working Group on Currency Futures to be set up

26

Thank

You