1 Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved. Fernando Marchant B., Manager Supply...

14

1 Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved. Fernando Marchant B., Manager Supply Codelco: Strategic Sourcing Fernando Marchant B. Manager Supply Sept., 2010

-

date post

18-Dec-2015 -

Category

Documents

-

view

219 -

download

0

Transcript of 1 Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved. Fernando Marchant B., Manager Supply...

1

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Codelco: Strategic Sourcing

Fernando Marchant B.Manager SupplySept., 2010

2

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Codelco: Operations and Global Commercial Presence*

Codelco Norte DivisionCopper

Codelco Norte DivisionCopper

VentanasSmelter & Refinery

Division

VentanasSmelter & Refinery

Division

AndinaDivisionCopper

AndinaDivisionCopper

SantiagoHeadquarters

SantiagoHeadquarters

Salvador DivisionCopper

Salvador DivisionCopper

El TenienteDivisionCopper

El TenienteDivisionCopper

New York - USCodelco Group

Inc.

New York - USCodelco Group

Inc.

Düsseldorf - GermanyCodelco Kupferhandel

GMHB

Düsseldorf - GermanyCodelco Kupferhandel

GMHB

London - UKChile Copper

Ltd.

London - UKChile Copper

Ltd.

Shanghai - ChinaRepresentative

Office

Shanghai - ChinaRepresentative

Office

Gabriela Mistral Operation

Copper

Gabriela Mistral Operation

Copper

*: Commercial Subsidiaries.

3

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Codelco: World Leader in the Copper and Molybdenum Industry

FCX:10%

BHP Billiton:7%

Xstrata:6%

Rio Tinto:5%

Others:51%

Southern Copper:3%

Anglo American:4%

Antofagasta PLC:2%

Vale:1%

Codelco: 11%

Leadership in Copper Production

Source: Codelco, Companies Annual Reports, WBMS and USGS.

Others Chile:20%

Peru:12%

Mexico:7%United States:6%

Indonesia:6%

China:5%

Poland:5%

Russia:4%

Australia:4%

Other Countries:

20%

Codelco: 10%

Leadership in Copper Reserves

China JDC:8%

Thompson Creek:7%

FCX: 14%

Other China: 18%

Antofagasta Minerals:3%

China Molybdenum:

6%Anglo

American: 3%

Codelco: 10%

Others: 23%

Grupo Mexico: 7%

Second Largest Molybdenum Producer

4

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Our Commitment with the Owner: 1990 – 2009Profit before Taxes

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

US$ Million, nominal currency

5

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Investments: 1976 - 2010

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010*

US$ Million, nominal currency

Note: 1976-2009: Figures include projects, mine development and investments in related companies. *: Forecast.

6

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Evolution of Codelco’s Geological Resources, Mineral Resources and Reserves

252 259275

298318

81

119 125 127

36 46 54 54 49 48

327326328

122125120121

53 53

0

50

100

150

200

250

300

350

400

2003 2004 2005 2006 2007 2008 2009 2010

Geological ResourcesMineral ResourcesReserves

Note: Corresponds to Business and Development Plan. Since 2006, geological and mineral resources include stockpile and broken ore.

Milion fine metric tonnes

7

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Cooper Production per Division (%)

Total 2010-2104: 8,600 thousand fmt (approx.)

Copper Production : 2010 - 2014

OPEN PIT UNDERGROUND

8

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Expenditures in Goods

- 500 1,000 1,500 2,000 2,500

Others

Lime

Tires

Chemical Products

Acid

Steel

Spare Parts

Fuel

Expenditures in Services

- 1,000 2,000 3,000 4,000

Cleaning and food services

Services of engineering

Rental

Administration Cost

Transportation

Mining Development

Mining Support Services

Maintenance

Electric Power

Business Opportunities: 2010 - 2014US$ Million

9

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

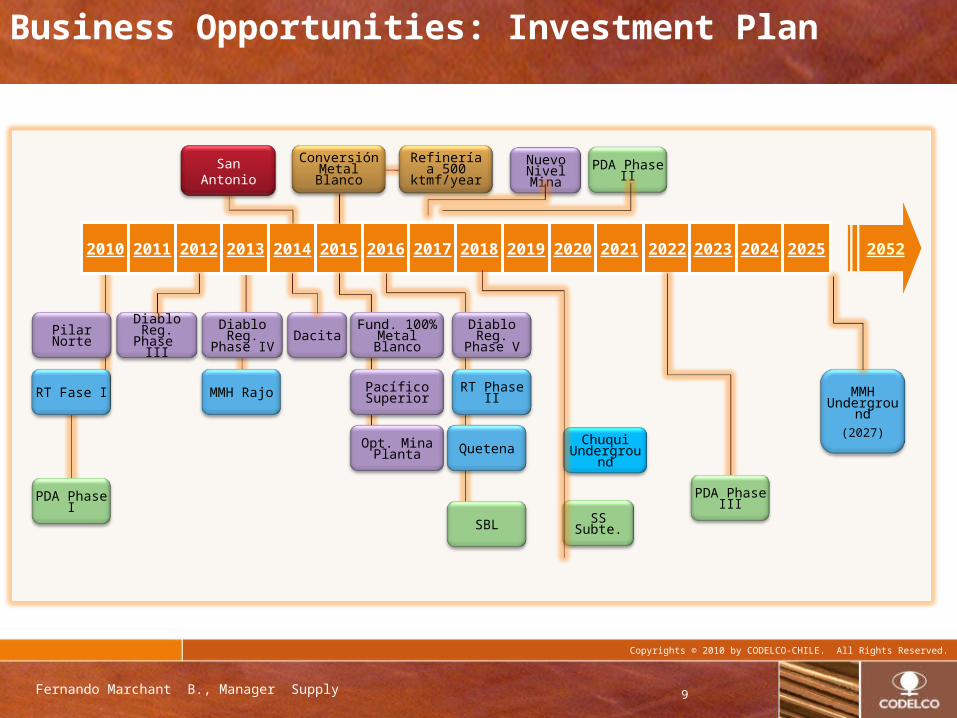

20522010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Diablo Reg.Phase III

Diablo Reg.Phase IVPilar Norte Dacita

RT Fase I MMH Rajo MMHUnderground

(2027)

PDA Phase I

Fund. 100%Metal Blanco

Pacífico Superior

Opt. Mina Planta

Diablo Reg.Phase V

RT Phase II

Quetena

PDA Phase II

SBL

PDA Phase III

San AntonioRefinería a

500 ktmf/yearConversión

Metal BlancoNuevo Nivel

Mina

SS Subte.

Chuqui Underground

Business Opportunities: Investment Plan

10

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

2017

Andina Phase IAndina DivisionInv: MUS$ 1,125

Prod: 60,000 tonnes / year

2nd Q2010

RT SulphidesCodelco Norte Division

Inv: MUS$ 370Prod: 160,000 tonnes / year

3rd Q

2010

2013

MMHMMH Division

Inv.: MUS$ 2,333 Prod: 170,000 tonnes / year

Andina Phase IIAndina Division

Inv: MUS$ 4,390 Prod: 318,000 tonnes / year

New Mine LevelEl Teniente Division

Inv: MUS$ 1,718Prod: 445,000 tonnes / year

2018

Chuqui UndergroundCodelco Norte Division

Inv: MU$ 2,006Prod: 315,000 tonnes/year

Under Commissioning

In Feasibility Study

Codelco: Major Projects

Pilar NorteEl Teniente Division

Inv: MUS$ 140

Prod: 60,000 tonnes / year

20122011

Note: Figures in 2010 US$. Annual production represents first 10-year average.

11

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

EQUIPMENTS

Year of Requirement

2012 2013 2014 2017After 2017

Total

Crushers 15 3 1 42 61

Feeders 15 88 103

Conveyor Belts 1 1 12 108 122

Mills 10 2 2 14

Slurry Pumps 9 9

Substations 26 12 38

Electric Rooms & Switchgears

5 5

Power Transformers 5 3 8

Screens 16 2 18

SAG & Mill Ring Motor 1 2 3

Main Equipment Requirements

12

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Investment Summary 2010 – 2014: US$ 15,000 Millions

13

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Codelco: An Interesting Business Opportunity

• Significant business volume

• Important foreign and domestic offer

• Productivity of service providers

• Innovation (technology)

• Suppliers development (new stage)

14

Copyrights © 2010 by CODELCO-CHILE. All Rights Reserved.

Fernando Marchant B., Manager Supply

Codelco: Strategic Sourcing

Fernando Marchant B.Manager SupplySept., 2010