1 Competitiveness in SEE and Prospects in the Catching-Up Process: A Regional Overview Peter...

34

1 Competitiveness in SEE and Prospects in the Catching-Up Process: A Regional Overview Peter Mooslechner Director Economic Analysis and Research Department Oesterreichische Nationalbank National Bank of the Republic of Macedonia Skopje – May 30, 2008

-

Upload

jewel-banks -

Category

Documents

-

view

217 -

download

1

Transcript of 1 Competitiveness in SEE and Prospects in the Catching-Up Process: A Regional Overview Peter...

1

Competitiveness in SEEand Prospects in the Catching-Up Process:

A Regional Overview

Peter Mooslechner

DirectorEconomic Analysis and Research Department

Oesterreichische Nationalbank

National Bank of the Republic of MacedoniaSkopje – May 30, 2008

2

Oesterreichische National bank

Overview

• The Starting Point:Initial income gap ….. but signs of catching-up

• Underlying factors • Elements of price and cost competitiveness• The importance of the regulatory framework

• Factors of SEE competitiveness within Europe:• Trade integration: Sectoral and geographical aspects • Current account balance: Structural issues• SEE: Attractiveness for foreign investors

• Where does the region go to?

…plus some facts on Euroization in SEE

3

Oesterreichische National bank

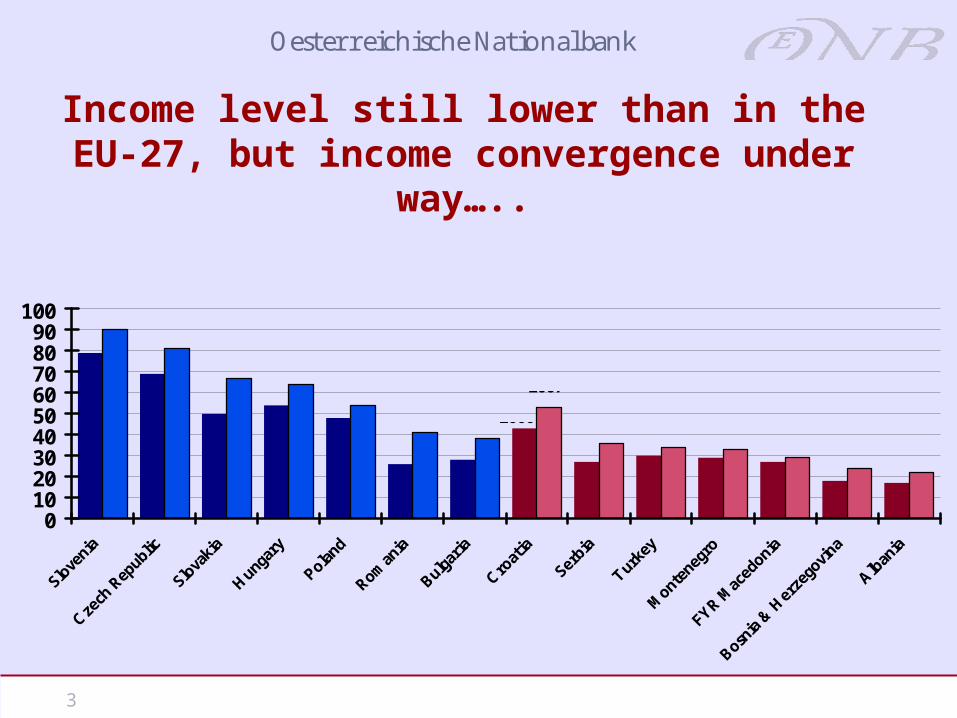

Income level still lower than in the EU-27, but income convergence under way…..

0102030405060708090

100

GDP per capita at PPPin % of EU-27

Source: wiiw.

2000

2007

4

Oesterreichische National bank

….. although it will take some time

GDP per capita in PPP terms: New EU Member States average as % of euro area average

Annual GDP growth in euro area assumed: 2.0%

40.0

50.0

60.0

70.0

80.0

90.0

100.0

20

04

20

08

20

12

20

16

20

20

20

24

20

28

20

32

20

36

20

40

Portugal (1986)

Greece (1981)

6% 5% 4%

Portugal (2004)

Greece (2004)

Source: Eurostat, OeNB.

5

Oesterreichische National bank

Most countries gained shares on world markets

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Poland Czech R. Hungary Slovakia Romania Slovenia Bulgaria Croatia BiH FYRMacedonia

Albania Serbia(incl.MNE)

Market Share in World Importsin %

Source: IMF.

2000

2007

6

Oesterreichische National bank

Some Basic Factors Driving Competitiveness

7

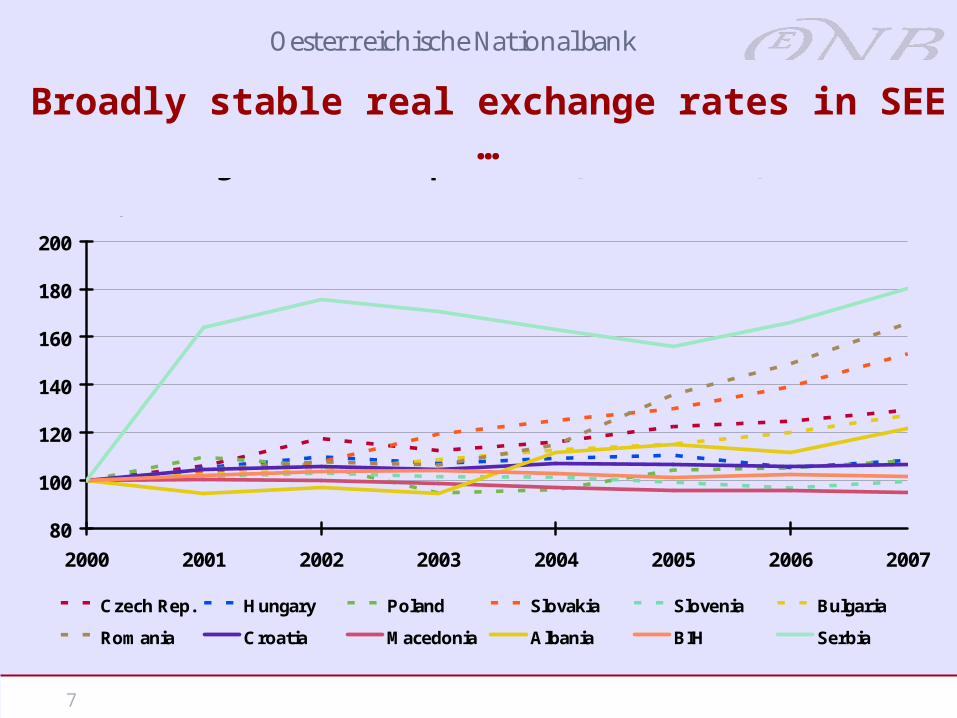

Oesterreichische National bank

80

100

120

140

160

180

200

2000 2001 2002 2003 2004 2005 2006 2007

Czech Rep. Hungary Poland Slovakia Slovenia Bulgaria

Romania Croatia Macedonia Albania BIH Serbia

Real exchange rates - EUR per NCU (PPI deflated) Index, 2000 = 100

Source: WIIW.

Broadly stable real exchange rates in SEE …

8

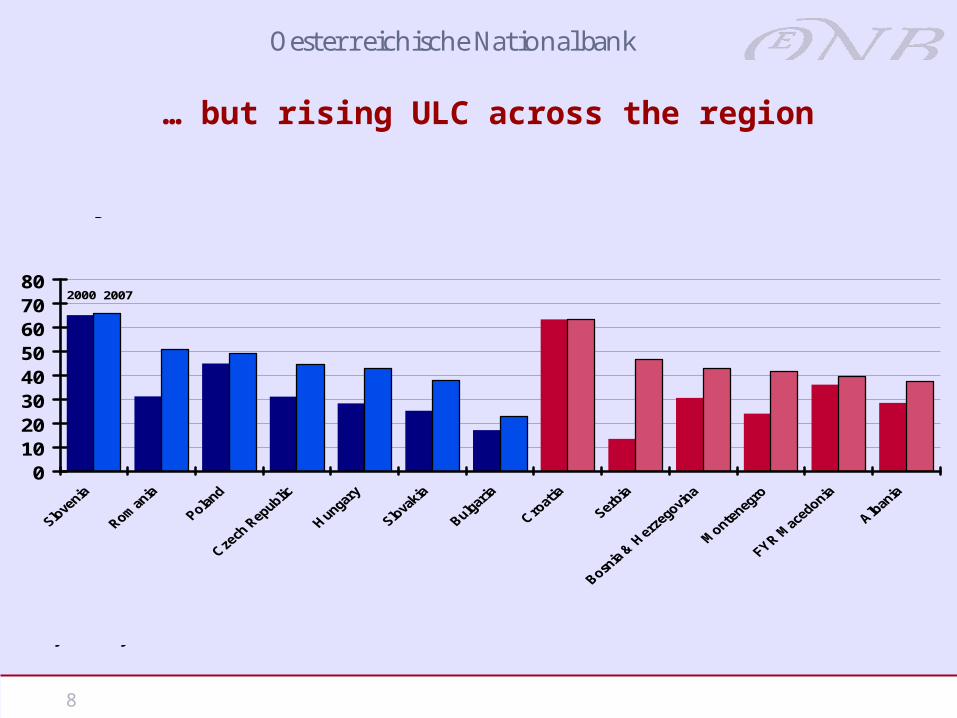

Oesterreichische National bank

2000 2007

01020304050607080

Unit Labor CostsPPP adjusted, Austria=100

Source: wiiw.

Data for Turkey not available.

… but rising ULC across the region

9

Oesterreichische National bank

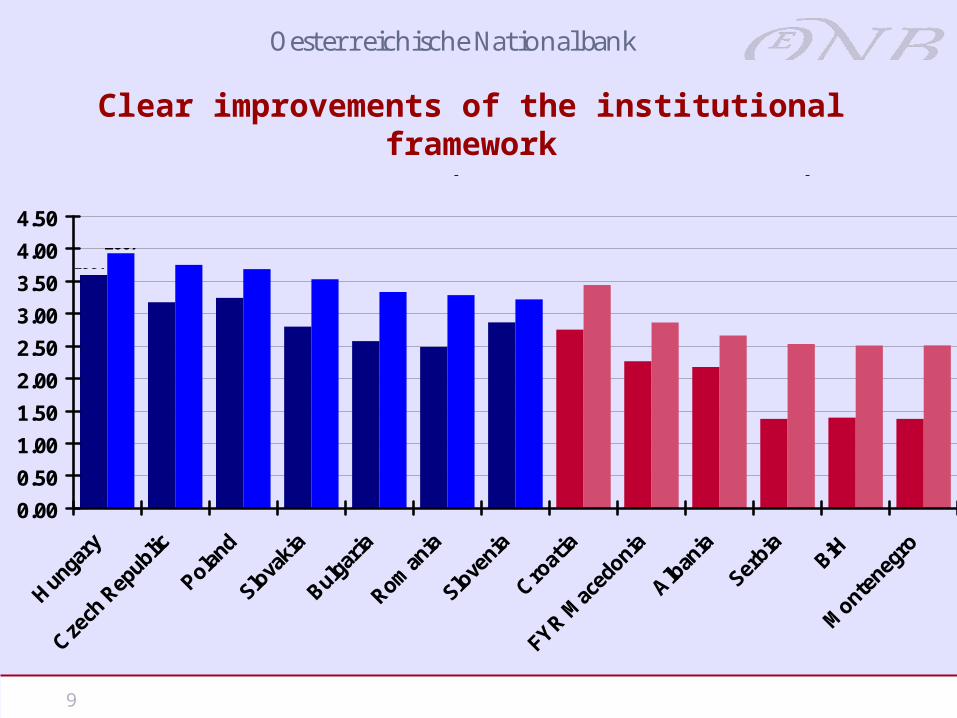

Clear improvements of the institutional framework

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

EBRD Transition Indicators (overall transition score)

Source: EBRD.

19972007

10

Oesterreichische National bank

Competitive Advantages of SEE Countries

• Critical issue: „Hard factors“ point more towards a certain loss in price competitiveness

• But „soft factors“ draw a more favourable picture:

• Continuously improving infrastructure supports trade with the EU markets

• Geographical location, closeness to the enlarged EU

• EU accession process

• Progress in regional cooperation and integration

• Attractiveness for FDI

11

Oesterreichische National bank

The Competitive Position of SEE within Europe:

Elements of a Dynamic View

12

Oesterreichische National bank

0102030405060708090

Exports of Goods and Services in % of GDP

Source: wiiw.

2000 2007

Note: Montenegro, FYR Macedonia, BiH, Serbia, Albania data of 2003 instead of 2000. In 2003, Serbia and Montenegro are not considered separately.

Progress in Trade Integration

13

Oesterreichische National bank

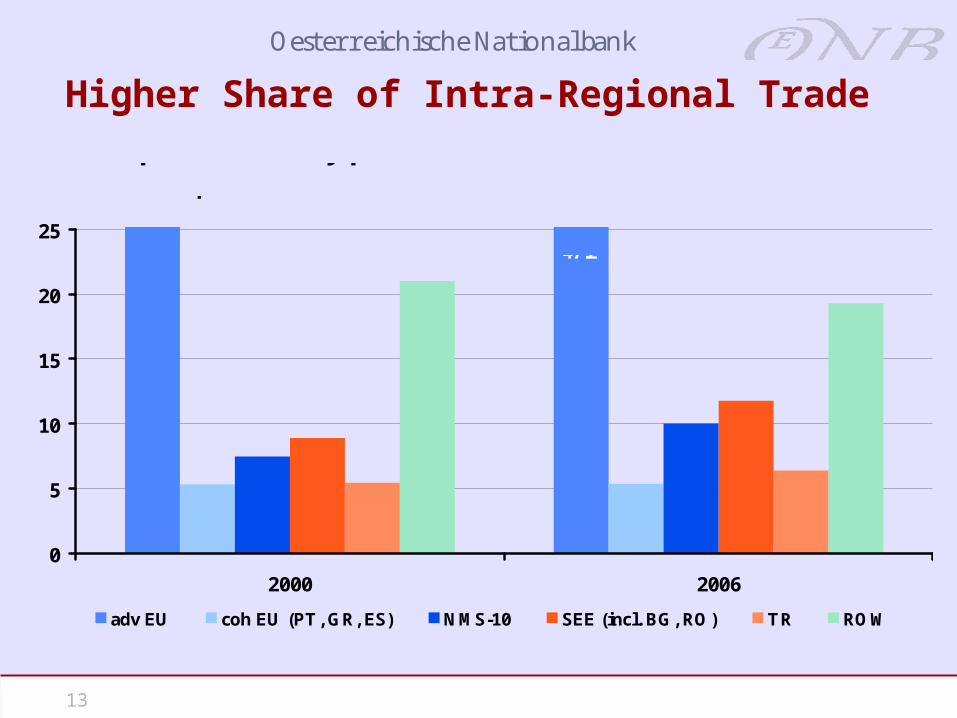

Higher Share of Intra-Regional Trade

0

5

10

15

20

25

2000 2006

adv EU coh EU (PT, GR, ES) NMS-10 SEE (incl. BG, RO) TR ROW

SEE export shares by partnersin % of total exports

Source: UN COMTRADE.

51.9 47.2

14

Oesterreichische National bank

0.0

0.5

1.0

1.5

2.0

2.5

Fuels,lubricants,

etc.

Chemicalproducts

Manufacturedgoods

Machines andtransportequipment

Misc.manufactured

articles

Total

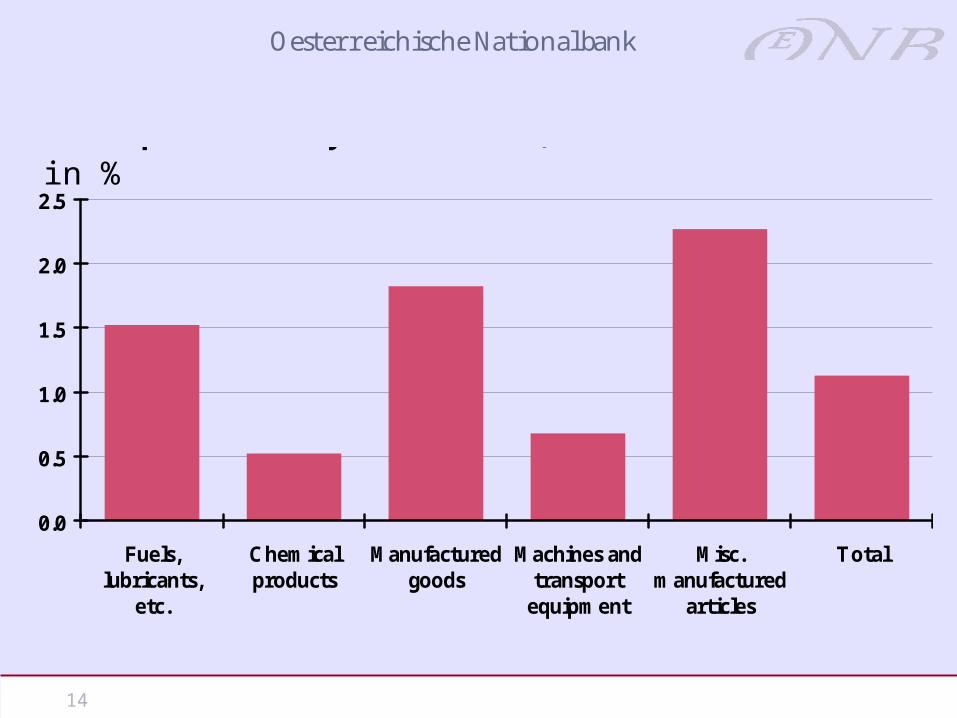

SEE export shares by commodities, 2006

Source: UN COMTRADE.

in %

15

Oesterreichische National bank

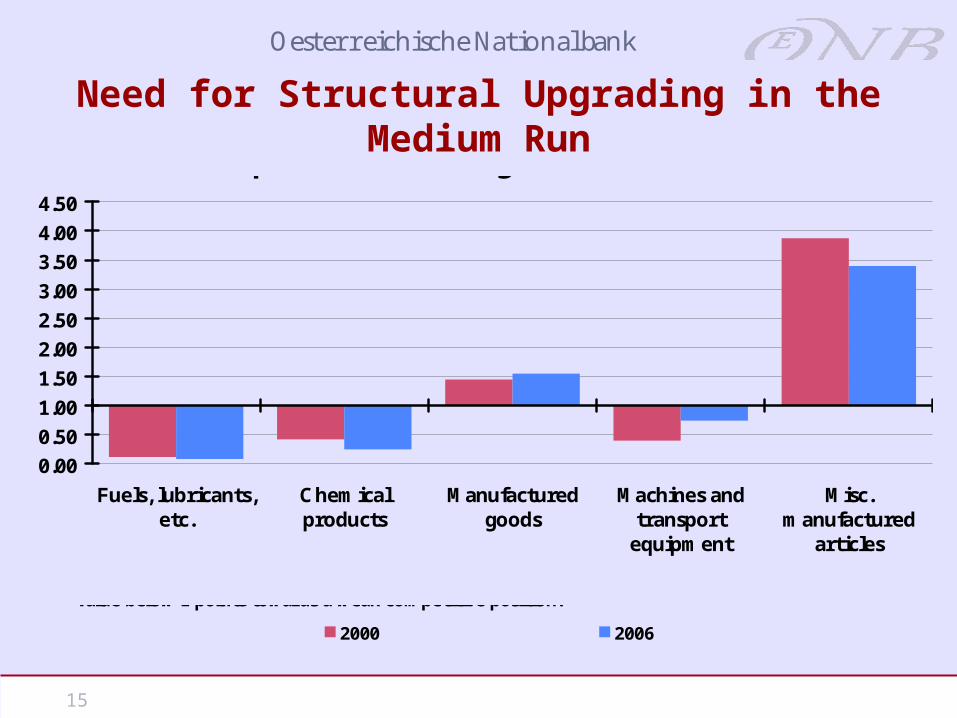

Need for Structural Upgrading in the Medium Run

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Fuels, lubricants,etc.

Chemicalproducts

Manufacturedgoods

Machines andtransportequipment

Misc.manufactured

articles

2000 2006

Revealed Comparative Advantages of SEE on advEU Market

Source: UN COMTRADE, own calculations.

A positive deviation from 1 implies a comparative advantage in the respective commodity group, a value below 1 points towards a weak competitive position.

16

Oesterreichische National bank

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

2000

2001

2002

2003

2004

2005

2006

2007

2000

2001

2002

2003

2004

2005

2006

2007

2000

2001

2002

2003

2004

2005

2006

2007

2000

2001

2002

2003

2004

2005

2006

2007

2000

2001

2002

2003

2004

2005

2006

2007

2000

2001

2002

2003

2004

2005

2006

2007

2000

2001

2002

2003

2004

2005

2006

2007

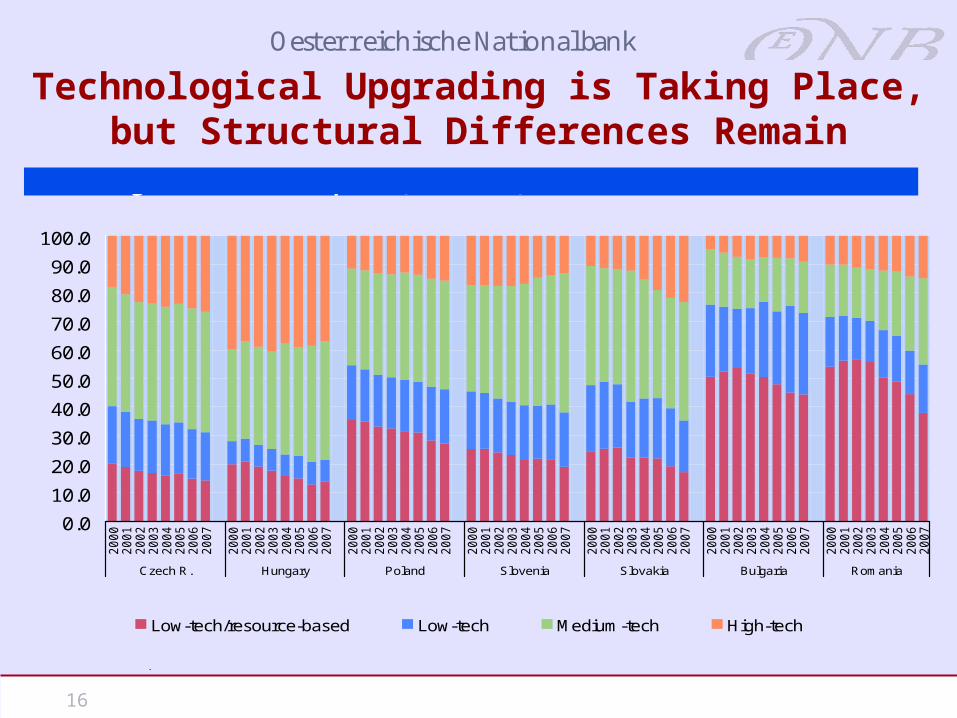

Czech R. Hungary Poland Slovenia Slovakia Bulgaria Romania

Low-tech/resource-based Low-tech Medium-tech High-tech

Technological content of exports (2000-2007)in % of classified exports (covering around 90% of total exports)

Source: Eurostat, OeNB.

Technological Upgrading is Taking Place, but Structural Differences Remain

17

Oesterreichische National bank

The Permanent Challenge of Trade and

Current Account Balances

18

Oesterreichische National bank

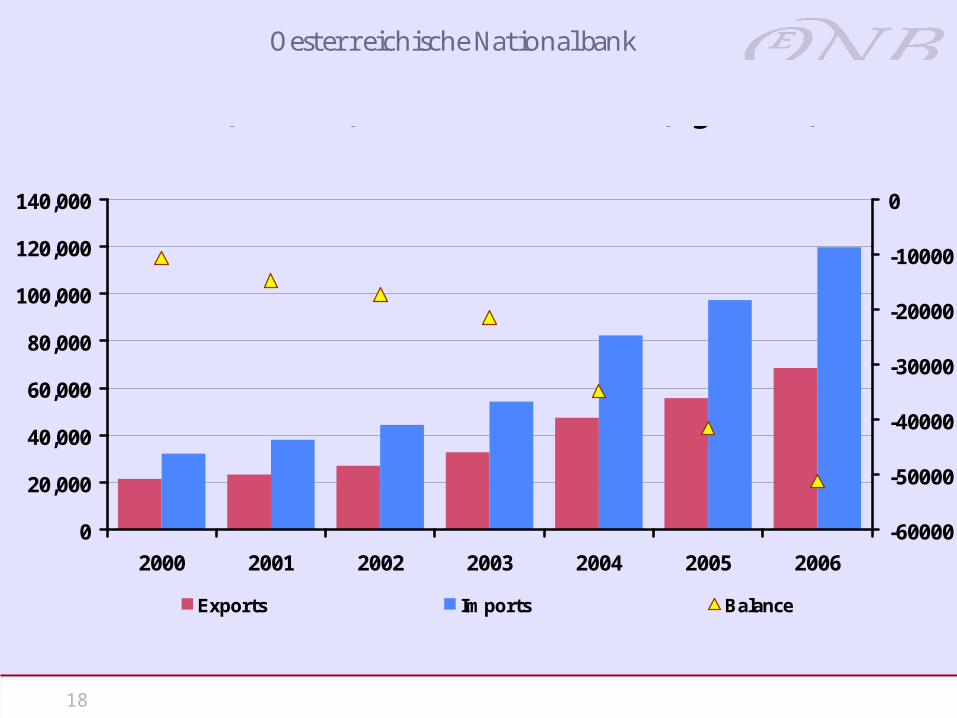

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2000 2001 2002 2003 2004 2005 2006

-60000

-50000

-40000

-30000

-20000

-10000

0

Exports Imports Balance

Trade Flows (left axis) and Trade Balance (right axis) of SEEin Mio USD

Source: UN COMTRADE.

19

Oesterreichische National bank

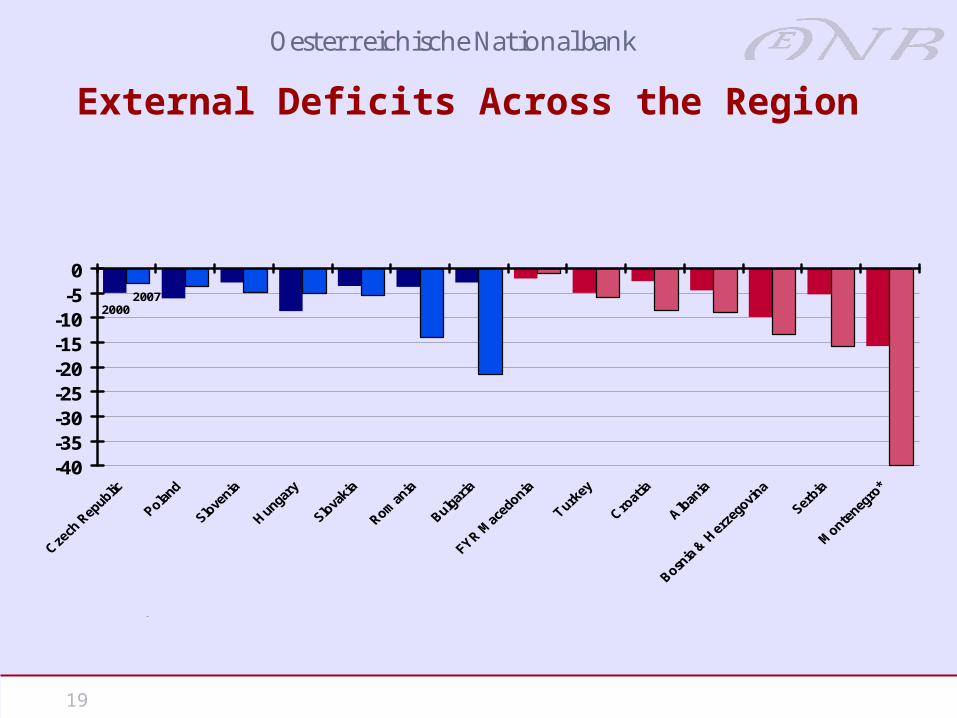

20002007

-40-35-30-25-20-15-10-50

Current Account Balancein % of GDP

Source: Eurostat, wiiw.

* 2001

External Deficits Across the Region

20

Oesterreichische National bank

-40

-30

-20

-10

0

10

20

30

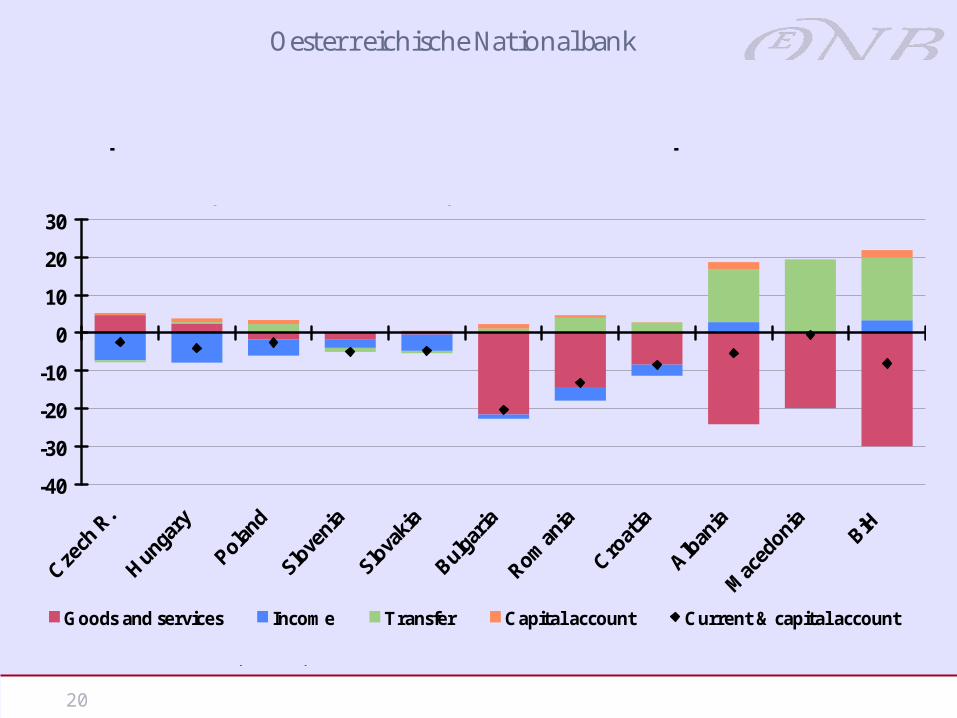

Goods and services Income Transfer Capital account Current & capital account

Composition of the combined current and capital account

% of GDP, 2007 (AL, MK and BIH 2006)

Source: National central banks, Eurostat, OeNB.

21

Oesterreichische National bank

-500500

1500250035004500550065007500

FDI Stock per Capitain EUR

Source: wiiw.

2003 2007

High and increasing FDI stock

22

Oesterreichische National bank

0

10

20

30

40

50

60

70

80

90

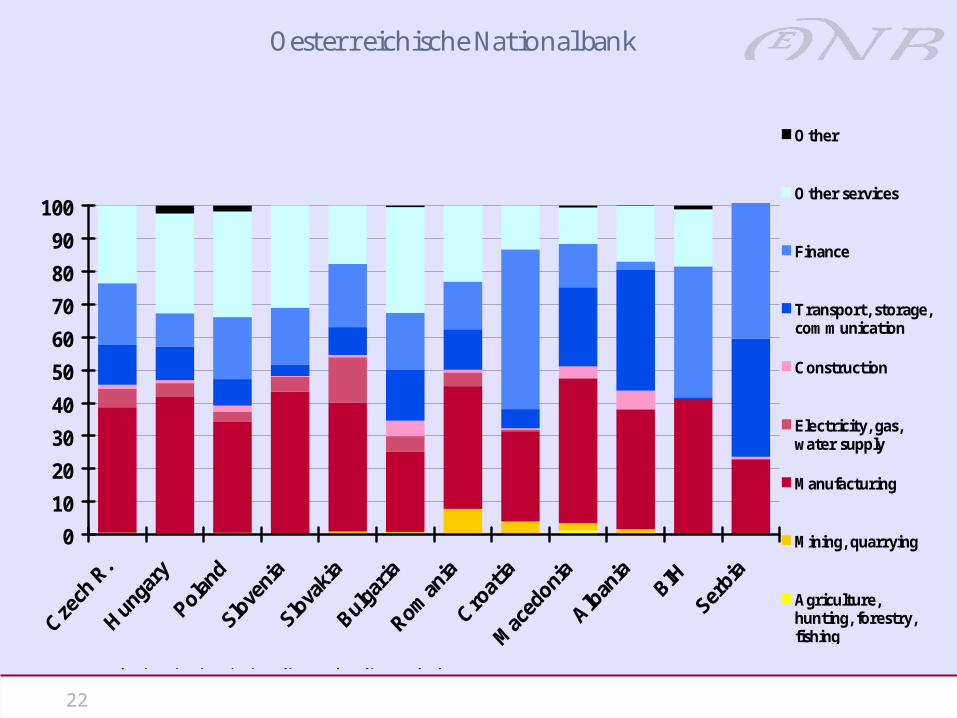

100

Other

Other services

Finance

Transport, storage,communication

Construction

Electricity, gas,water supply

Manufacturing

Mining, quarrying

Agriculture,hunting, forestry,fishing

Sectoral structure of inward FDI stock, latest available data

in % of total inward FDI stock

Note: 2006 (CZ, HU, PL, RO, SI, MK), 2005 (BIH), 2004 (AL)

23

Oesterreichische National bank

Where does the region go to?

• SEE still with significant cost/price advantage compared to the European Union

• EU is main trading partner - but low share in total EU imports points to considerable growth potential

• Trade with the CEE-5 region as well as interregional trade is rising (and these regions show stronger growth than the rest of the EU)

• Specialisation of production on low-tech and basic goods sector faces strong competition from Asian countries (in particular China)

• Obvious need for technological upgrading to gain in long-term competitiveness

24

Oesterreichische National bank

Euroization as a particularFeature of SEE?

25

Oesterreichische National bank

Why Euroization in SEE Countries?

• Competitiveness is not only a question of wages, prices and productivity – it is also a question of the exchange rate

• Under certain (specific) conditions: Expectations are stabilized by fixed exchange-rate policies

• Historical experience: Austria’s “hard currency policy” – a particular example of pegging a country’s currency

• Today: ERM II and Monetary Union

• For most SEE countries the introduction of the Euro is still a long way to go

• People and policy makers might chose different ways to go

• Euroization is a peculiarity of this region

26

Oesterreichische National bank

Survey conducted since 1997Initially 5 Countries (Czech Republic, Hungary, Slovakia,

Slovenia and Croatia) reduced to 4 Countries after Slovenia joining the Euro Area

NEW Geographical scope from autumn 2007 on 6 EU Member States:

Bulgaria, Czech Republic, Hungary, Poland, Romania and Slovakia

5 Southeastern European Countries: Albania, Bosnia and Herzegovina, Croatia, Former Yugoslav

Republic of Macedonia (FYR Macedonia) and Serbia

The Use of the Euro in Central, Eastern and Southeastern Europe – Survey Design (I)

27

Oesterreichische National bank

The Use of the Euro in Central, Eastern and Southeastern Europe – Survey Design (II)

In each country about 1000 persons over the age of 14 are interviewed (in Poland only the population of the 10 largest cities); 2 waves per year (spring and autumn)

Overall 26 questions plus socio-demographics, including also nonregular questions on specific topics (for example on foreign currency loans)

Central questions:■ amounts and composition of foreign currency cash holdings■ foreign currency denominated deposits■ as well as motives for holding them

28

Oesterreichische National bank

0

10

20

30

40

50

60

Hungary Poland Slovakia CzechRepublic

Bulgaria Romania Bosnia-Herzegovina

Croatia Albania Serbia FYRMacedonia

EURUSDGBPOTHER

Share of respondents holding foreign cash

in % of respondents (multiple answers possible)

Quelle: Source: OeNB Euro Survey 2007.

Note: GBP only asked in Poland.

29

Oesterreichische National bank

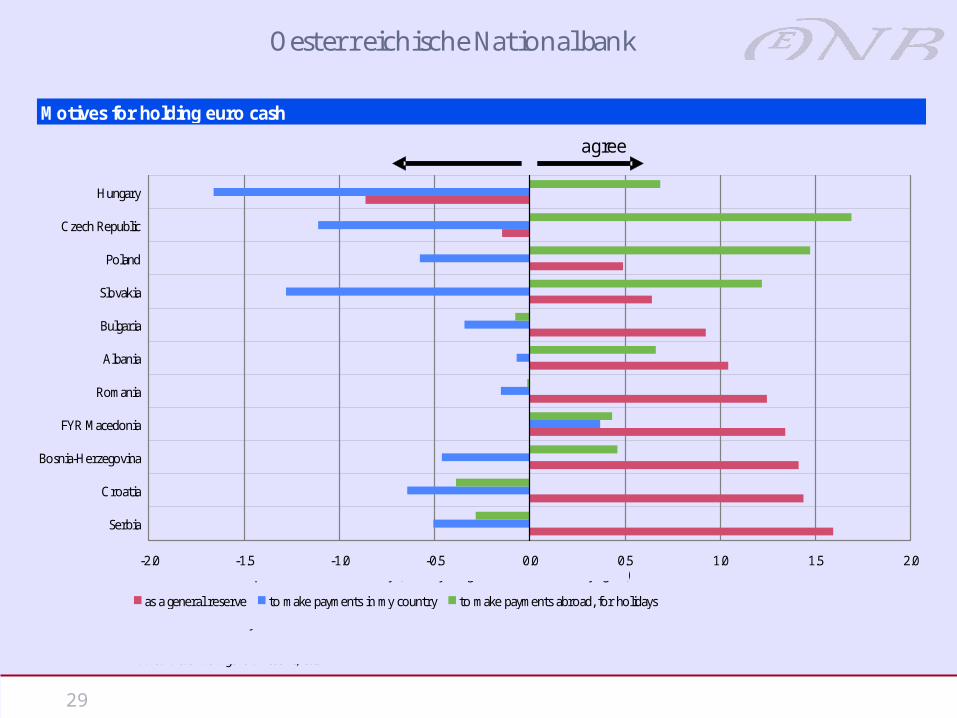

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Serbia

Croatia

Bosnia-Herzegovina

FYR Macedonia

Romania

Albania

Bulgaria

Slovakia

Poland

Czech Republic

Hungary

as a general reserve to make payments in my country to make payments abroad, for holidays

Motives for holding euro cash

normalized sample means for each country (-3.5 fully disagree, 0 neutral, +3.5 fully agree)

Source: OeNB Euro Survey 2007.

Note: Respondents who held euro cash were asked whether they agree or disagree on a scale from 1 (fully agree) to 6 (fully disagree) to the statement that they hold euro cash as a general reserve, etc.

agreedisagree

30

Oesterreichische National bank

0

10

20

30

40

50

60

70

80

90

Hungary Poland Slovakia CzechRepublic

Romania FYRMacedonia

Bulgaria Albania Serbia Bosnia-Herzegovina

Croatia

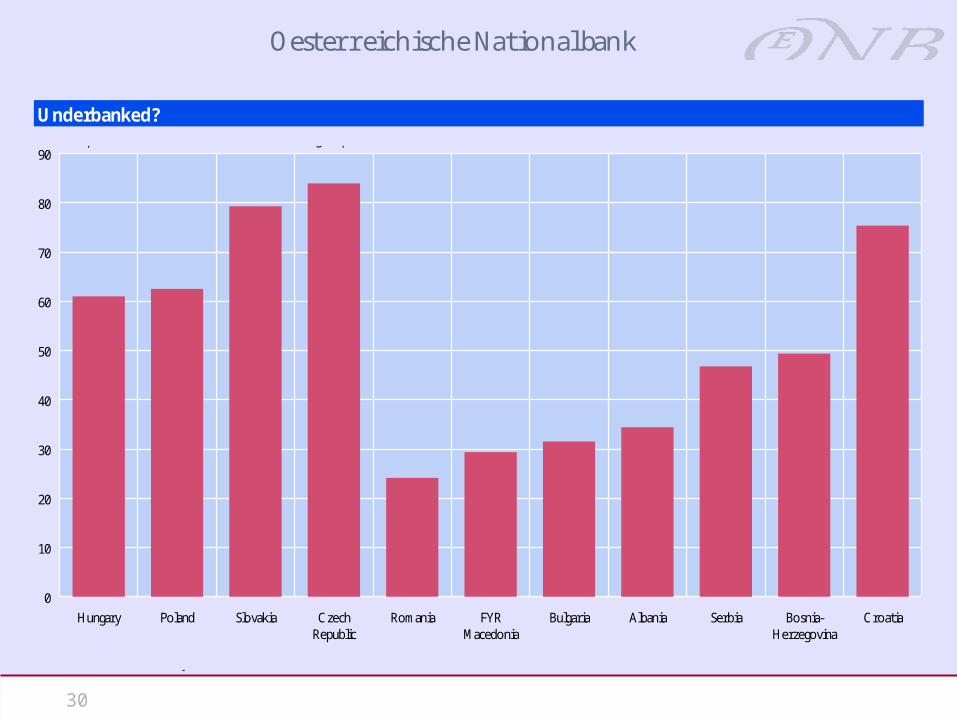

Underbanked? % of respondents with a transaction account or savings deposit

Source: OeNB Euro Survey 2007.

31

Oesterreichische National bank

0

10

20

30

40

50

60

Hungary Poland Slovakia CzechRepublic

Bulgaria Romania Croatia Albania FYRMacedonia

Serbia Bosnia-Herzegovina

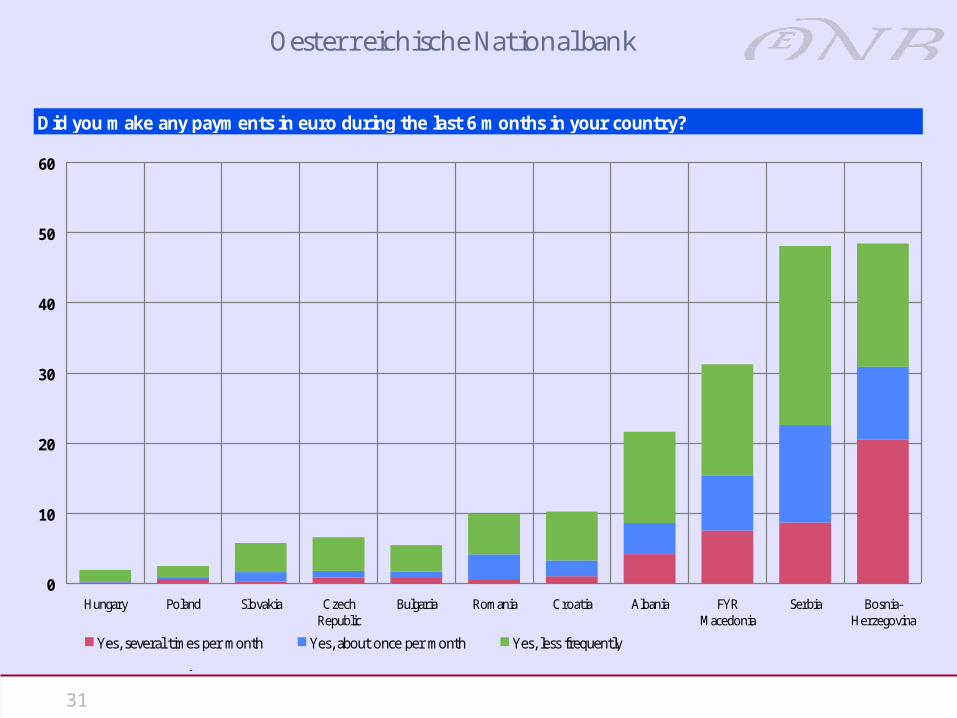

Yes, several times per month Yes, about once per month Yes, less frequently

Did you make any payments in euro during the last 6 months in your country?in % of respondents

Source: OeNB Euro Survey 2007.

32

Oesterreichische National bank

Summary of First Survey Results

• The euro plays a predominant role in foreign currency denominated assets held by residents throughout the region.

• In general, euro cash holdings are more important in Southeastern European Countries than in EU Member States.

• Key motives to hold euro cash: – Southeastern Europe, BU and RO as a store of value, – other EU Member States for holidays and shopping

purposes abroad.

33

Oesterreichische National bank

■ Focus on European Economic IntegrationMain results will be provided in an article on a regularly basis (semi-annual); first one in FEEI 1/2008 (July)

■ Research and information platform on the internet (July 2008) Details on the Survey, sample, technical report, questionnaire Selected results and complete list of publications www.oenb.at, ceec.oenb.at

■ The International Role of the EuroBox prepared for the European Central Bank’s report

■ Occasional newsletter on special topics

■ Ongoing research activities■ Stix, H. 2008. Euroization: What Factors Drive its Persistence?

Household Data Evidence for Croatia, Slovenia and Slovakia. OeNB Working Paper No. 140.

■ Presentation of papers by Doris Ritzberger-Gruenwald and Helmut Stix at the Annual Meeting of the Austrian Economic Association 2008

Where to find more information…..

34

Oesterreichische National bank

Thank you very Thank you very much for your much for your

Attention!Attention!