1 Chapter 4: Time Value of Money Copyright, 2000 Prentice Hall ©Author Nick Bagley, bdellaSoft,...

41

1 Chapter 4: Time Chapter 4: Time Value of Money Value of Money Copyright, 2000 Prentice Hall ©Author Nick Bagley, bdellaSoft, Inc. Objective Explain the concept of compoundin and discounting and to provide examples of real life applications

-

date post

20-Dec-2015 -

Category

Documents

-

view

218 -

download

1

Transcript of 1 Chapter 4: Time Value of Money Copyright, 2000 Prentice Hall ©Author Nick Bagley, bdellaSoft,...

1

Chapter 4: Time Value of Chapter 4: Time Value of MoneyMoney

Copyright, 2000 Prentice Hall ©Author Nick Bagley, bdellaSoft, Inc.

ObjectiveExplain the concept of compounding

and discounting and to provide examples of real life

applications

2

Value of Investing $1Value of Investing $1

1 Year $1.1

2 Years $1.21

3 Years $1.331

4 Years $1.4641

– Continuing in this manner you will find Continuing in this manner you will find that the following amounts will be that the following amounts will be earnt:earnt:

3

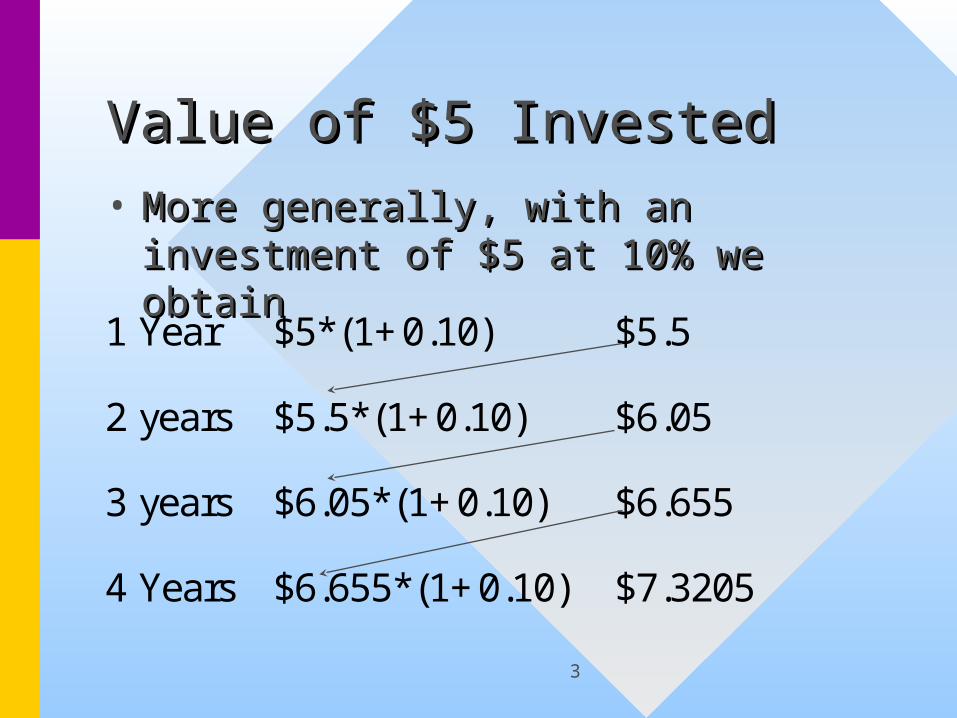

Value of $5 InvestedValue of $5 Invested

1 Year $5*(1+0.10) $5.5

2 years $5.5*(1+0.10) $6.05

3 years $6.05*(1+0.10) $6.655

4 Years $6.655*(1+0.10) $7.3205

• More generally, with an investment More generally, with an investment of $5 at 10% we obtainof $5 at 10% we obtain

4

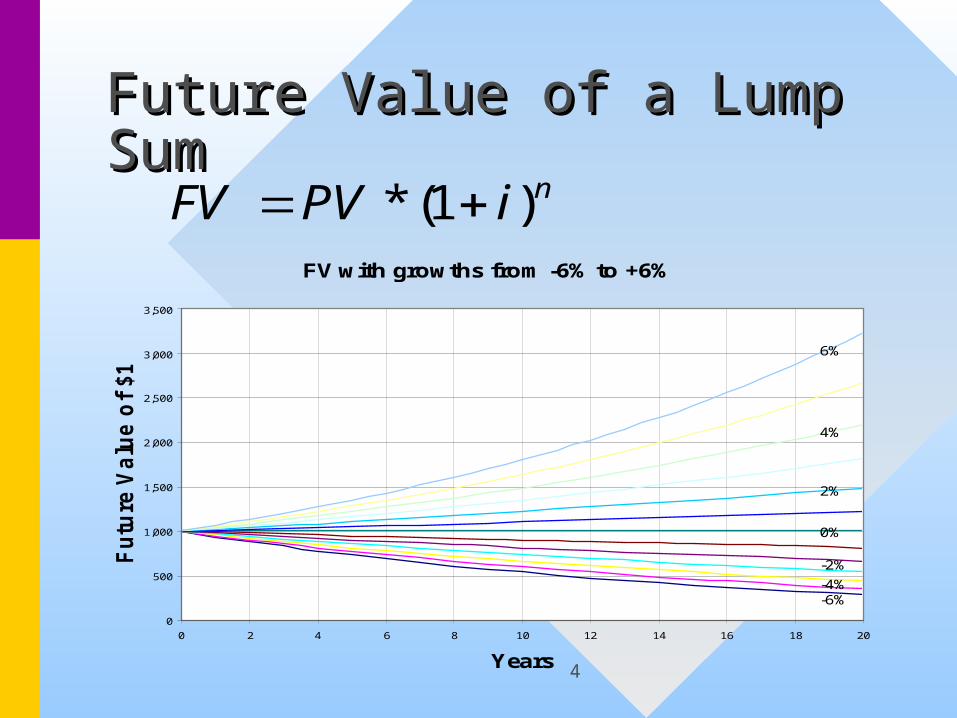

Future Value of a Lump Future Value of a Lump SumSum

niPVFV )1(* FV with growths from -6% to +6%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0 2 4 6 8 10 12 14 16 18 20

Years

Fu

ture

Va

lue

of

$1

00

0

6%

4%

2%

0%

-2%

-4%-6%

5

Example: Future Value of Example: Future Value of a Lump Suma Lump Sum• Your bank offers a

CD with an interest rate of 3% for a 5 year investments.

• You wish to invest $1,500 for 5 years, how much will your investment be worth?

1111145.1738$

)03.01(*1500$

)1(*5

niPVFV

n 5i 3%PV 1,500FV ?Result 1738.911111

6

Present Value of a Lump Present Value of a Lump SumSum

nn

n

n

iFVi

FVPV

i

iPVFV

)1(*)1(

:obtain to)1(by sidesboth Divide

)1(*

7

Example: Present Value of Example: Present Value of a Lump Suma Lump Sum

• You have been You have been offered $40,000 for offered $40,000 for your printing your printing business, payable business, payable in 2 years. Given in 2 years. Given the risk, you require the risk, you require a return of 8%. a return of 8%. What is the present What is the present value of the offer?value of the offer? today55.293,34$

55281.34293

)08.01(

000,40

)1(

2

ni

FVPV

8

Solving Lump Sum Cash Solving Lump Sum Cash Flow for Interest RateFlow for Interest Rate

1

)1(

)1(

)1(*

n

n

n

n

PVFV

i

PVFV

i

iPVFV

iPVFV

9

Example: Interest Rate on Example: Interest Rate on a Lump Sum Investmenta Lump Sum Investment

• If you invest If you invest $15,000 for ten $15,000 for ten years, you receive years, you receive $30,000. What is $30,000. What is your annual your annual return?return?

point) basisnearest the(to %18.7

071773463.0

121211500030000

1

101

1010

n

PVFV

i

10

Review of LogarithmsReview of Logarithms

• The basic properties of logarithms that The basic properties of logarithms that are used by finance are:are used by finance are:

)ln()ln(

)ln()ln()*ln(

)ln(

0,)ln(

xyx

yxyx

xe

xxe

y

x

x

11

Review of LogarithmsReview of Logarithms

• The following properties are easy to prove The following properties are easy to prove from the last ones, and are useful in financefrom the last ones, and are useful in finance

)ln(*)ln()ln(

)ln()ln()ln()**ln(

)ln()ln()/ln(

yxyx

zyxzyx

yxyx

12

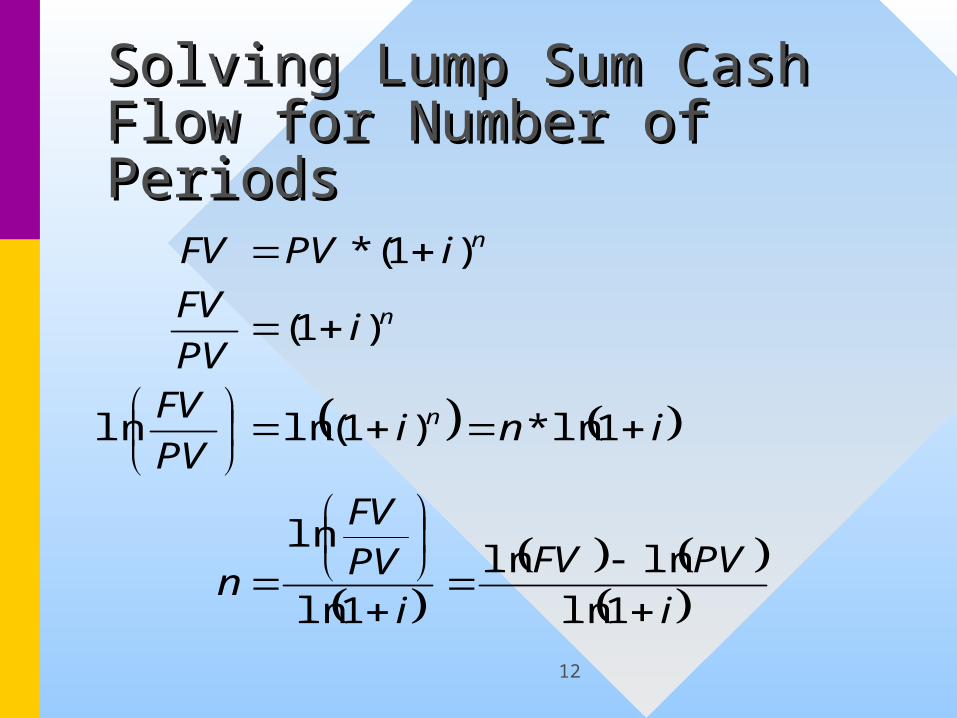

Solving Lump Sum Cash Solving Lump Sum Cash Flow for Number of Flow for Number of PeriodsPeriods

iPVFV

iPVFV

n

iniPV

FV

iPV

FV

iPVFV

n

n

n

1ln

lnln

1ln

ln

1ln*)1(lnln

)1(

)1(*

13

Effective Annual Rates of Effective Annual Rates of an APR of 18%an APR of 18%

AnnualPercentagerate

Frequency ofCompounding

AnnualEffective Rate

18 1 18.00

18 2 18.81

18 4 19.25

18 12 19.56

18 52 19.68

18 365 19.72

14

The Frequency of The Frequency of CompoundingCompounding• Note that as the frequency of Note that as the frequency of

compounding increases, so does the compounding increases, so does the annual effective rateannual effective rate

• What occurs as the frequency of What occurs as the frequency of compounding rises to infinity?compounding rises to infinity?

111

km

m

me

m

kLimEFF

15

The Frequency of The Frequency of CompoundingCompounding

11*

11

11

1

1

m

m

EFFmk

EFFm

k

m

kEFF

m

m

m

m

16

The Frequency of The Frequency of CompoundingCompounding

AnnualEffective Rate

CompoundingFrequency

AnnualPercentageRate

12 1 12.00

12 2 11.66

12 4 11.49

12 12 11.39

12 52 11.35

12 365 11.33

12 Infinity 11.33

17

Derivation of PV of Derivation of PV of Annuity Formula: Algebra. Annuity Formula: Algebra. 1 of 51 of 5

nn i

pmt

i

pmt

i

pmt

i

pmt

i

pmtPV

111

11

13

21

18

Derivation of PV of Derivation of PV of Annuity Formula: Algebra. Annuity Formula: Algebra. 2 of 52 of 5

}

1

1

1

1

1

1

1

1

1

1{*

13

21

nn iii

iipmtPV

19

Derivation of PV of Derivation of PV of Annuity Formula: Algebra. Annuity Formula: Algebra. 3 of 53 of 5

}

1

1

1

1

1

1

1

1

1

1{*)1(*)1(*

13

21

nn iii

iiipmtiPV

20

Derivation of PV of Derivation of PV of Annuity Formula: Algebra. Annuity Formula: Algebra. 4 of 54 of 5

nnnn

nnnn

ipmt

iiii

ipmt

ipmt

iiiii

iipmtiPV

1

1}

1

1

1

1

1

1

1

1

1

1{*

1

1*

]}1

1

1

1[

1

1

1

1

1

1

1

1

1

1{*)1(*

122

10

122

10

21

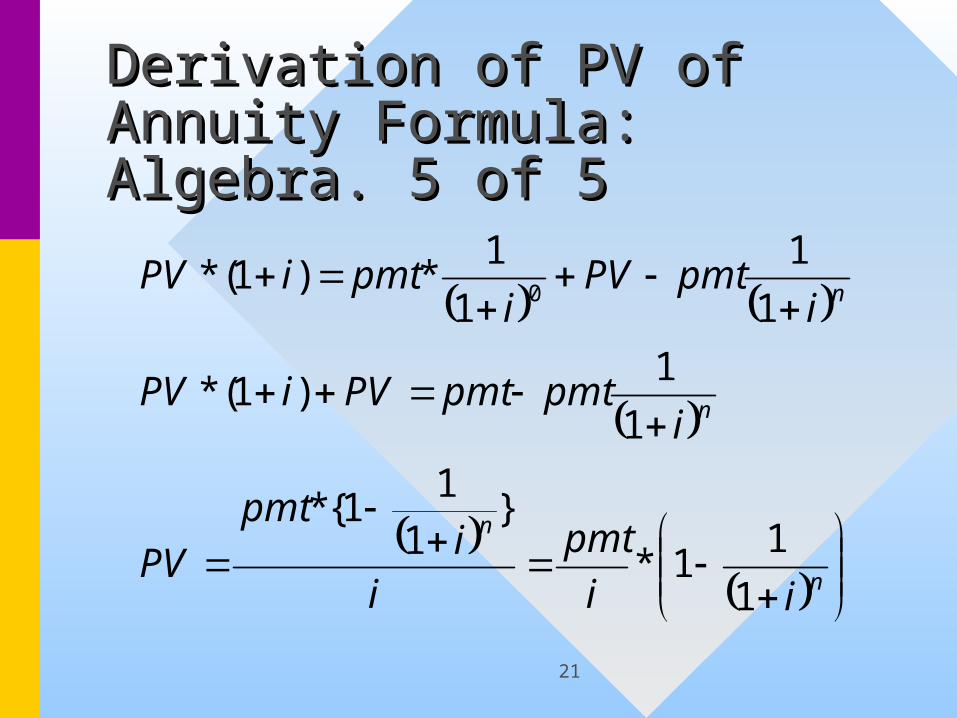

Derivation of PV of Derivation of PV of Annuity Formula: Algebra. Annuity Formula: Algebra. 5 of 55 of 5

n

n

n

n

ii

pmt

ii

pmt

PV

ipmtpmtPViPV

ipmtPV

ipmtiPV

1

11*

}1

11{*

1

1)1(*

1

1

1

1*)1(* 0

22

PV of Annuity FormulaPV of Annuity Formula

n

n

iipmt

ii

pmt

PV

1

11*

}1

11{*

23

PV Annuity Formula: PV Annuity Formula: PaymentPayment

n

n

n

i

iPVpmt

iipmt

iipmt

PV

11

*

11*

1

11*

24

PV Annuity Formula: PV Annuity Formula: Number of PaymentsNumber of Payments

ipmt

iPV

npmt

iPVi

pmtiPV

inpmt

iPVi

ipmt

iPVi

ipmt

PV

n

n

nn

1ln

*1ln

;*

11

*1ln1ln*;

*11

11*

;11*

25

Annuity Formula: PV Annuity Formula: PV Annuity DueAnnuity Due

}1)1{(*

)1(*}11{*

)1(*

1 n

n

regdue

iiipmt

iiipmt

iPVPV

26

Derivation of FV of Derivation of FV of Annuity Formula: AlgebraAnnuity Formula: Algebra

11*

1*1

11*FV

sum) (lump 1*FV

annuity) (reg. 1

11*

n

n

n

n

n

iipmt

iii

pmt

iPV

iipmt

PV

27

FV Annuity Formula: FV Annuity Formula: PaymentPayment

11

*

11*

n

n

i

iFVpmt

iipmt

FV

28

FV Annuity Formula: FV Annuity Formula: Number of PaymentsNumber of Payments

ipmt

iFV

n

pmtiFV

ini

ipmt

iFV

iipmt

FV

n

n

n

1ln

*1ln

*1ln1ln*1ln

1*

1

11*

29

Perpetual Annuities / Perpetual Annuities / PerpetuitiesPerpetuities

• Recall the annuity formula:Recall the annuity formula:

niipmt

PV1

11*

• Let n -> infinity with i > 0:

ipmt

PV

30

Mortgage: The paymentMortgage: The payment

• We will examine this problem using a We will examine this problem using a financial calculatorfinancial calculator

• The first quantity to determine is the The first quantity to determine is the amount of the loan and the pointsamount of the loan and the points

500,13$

03.0*)1.01(*500000$Points

000,450$

)1.01(*500000$Loan

31

Calculator SolutionCalculator Solution

n i PV FV PMT Result

360 0.5% 450,000 0 ? -2,697.98

This is the monthly repayment

32

Calculator SolutionCalculator Solution

n i PV FV PMT Result

360 .5% 450,000 0 ? -2,697.98

300 .5% ? 0 -2,697.98 418,745

Outstanding @ 60 Months

33

Summary of PaymentsSummary of Payments

• The family has made 60 payments = The family has made 60 payments = $2687.98*12*5 = $161,878.64$2687.98*12*5 = $161,878.64

• Their mortgage repayment =Their mortgage repayment = 450,000 - 418,744.61 = $31,255.39450,000 - 418,744.61 = $31,255.39

• Interest = payments - principle Interest = payments - principle reduction = 161,878.64 - 31,255.39 = reduction = 161,878.64 - 31,255.39 = $130,623.25$130,623.25

34

Amortization of Principal

0.00

50000.00

100000.00

150000.00

200000.00

250000.00

300000.00

350000.00

400000.00

450000.00

0 24 48 72 96 120 144 168 192 216 240 264 288 312 336 360

Months

Ou

tsta

nd

ing

Bal

ance

35

After Tax Cash Flow

$1,500

$1,700

$1,900

$2,100

$2,300

$2,500

$2,700

$2,900

0 24 48 72 96 120 144 168 192 216 240 264 288 312 336 360

Monthly Cash Flow

Mo

nth

36

Percent of Interest and Principal

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 24 48 72 96 120 144 168 192 216 240 264 288 312 336 360

Months

Per

cen

t

% Interest

% Principal

37

10% Aditional Payments

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

0 24 48 72 96 120 144 168 192 216 240 264 288 312 336 360

Months

Pri

nci

pal

Ou

tsta

nd

ing

38

$10,000

$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥ / ¥

? $/¥

U.S.A.

Japan

39

$10,000

$11,124$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥/¥

0.0108 $/¥

U.S.A.

Japan

40

$10,000

$10,918 ¥$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥ / ¥

0.0106 $/¥

U.S.A.

Japan

41

$10,000

$11,000 ¥$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥ / ¥

0.01068 $/¥

U.S.A.

Japan