1 Budgeting the Project Faculty of Applied Engineering and Urban Planning Civil Engineering...

33

1 Budgeting the Project Faculty of Applied Engineering and Urban Planning Civil Engineering Department Lecture 18 + 19 2 nd Semester 2008/2009 UP Copyrights 2008 Construction Project Management Eng: Eyad Haddad

-

Upload

sara-powell -

Category

Documents

-

view

216 -

download

0

Transcript of 1 Budgeting the Project Faculty of Applied Engineering and Urban Planning Civil Engineering...

11

Budgeting the Project

Faculty of Applied Engineering and Urban Planning

Civil Engineering Department

Lecture 18 + 19

2nd Semester 2008/2009

UP Copyrights 2008

Const

ruct

ion P

roje

ct

Managem

ent

Eng: Eyad Haddad

22

IntroductionIntroduction

Budgets are plans for allocating organizational

resources to project activities. على الشركة مصادر لتوزيع كخطة تعتبر الميزانية

المشروع أنشطة

forecasting required resources, quantities needed,

when needed, and costs , احتياجها وزمن المطلوبة والكميات بالمصادر التنبؤ يتم وفيها

وتكلفتها

Budgets help tie project to overall organizational

objectives.

Budgets can be used as tool by upper management

to monitor and guide projects.

33

METHODS OF BUDGETINGMETHODS OF BUDGETING

1. Top-Down Budgeting

2. Bottom-Up Budgeting

44

1. Top-Down Budgeting1. Top-Down Budgeting

Based on collective judgments and experiences of top

and middle managers.

Overall project cost estimated by estimating costs of

major tasks

Advantages

accuracy of estimating overall budget لتقدير كبيرة لدقة تحتاج ال

العامة الميزانية

errors in funding small tasks need not be

individually identified الصغيرة األنشطة ميزانية تقدير عن الناجمة االخطاء عن بمعزل

55

2. Bottom-Up Budgeting2. Bottom-Up Budgeting

WBS or action plan identifies elemental tasks

Those responsible for executing these tasks estimate

resource requirements

Advantage

more accurate in the detailed tasks.

Disadvantage

risk of fail to consider tasks

66

2. Bottom-Up Budgeting2. Bottom-Up Budgeting

a work statement and set of drawings or specifications

are used to “take off” material quantities required to

perform each discrete task performed in accomplishing a

given operation or producing an equipment component.

From these quantities, direct labor, equipment, and

overhead costs are derived and added.

This technique is used as the level of detail increases as

the project develops.

77

COST ESTIMATINGCOST ESTIMATING

Data collection & normalization:

When estimating, cost data is collected.

Data may be collected from similar projects, data bases, and

published reports.

The basis of the cost data should be documented as part of the

detailed backup for the estimate.

The amount of data collected will depend on the time available to

perform the estimate and the type of estimate, as well as the

budget allocation for the estimate’s preparation.

88

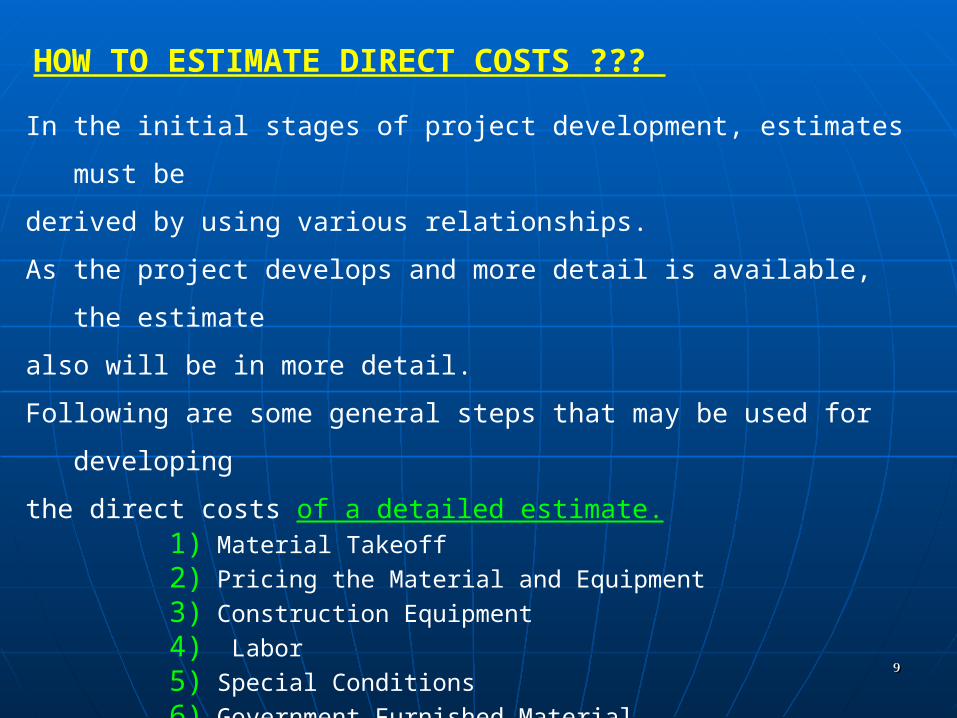

HOW TO ESTIMATE DIRECT COSTS ???

In the initial stages of project development, estimates must be

derived by using various relationships.

As the project develops and more detail is available, the estimate

also will be in more detail.

Following are some general steps that may be used for developing

the direct costs of a detailed estimate.1) Material Takeoff 2) Pricing the Material and Equipment 3) Construction Equipment 4) Labor 5) Special Conditions 6) Government Furnished Material 7) Sampling and Analysis Costs 8) Transportation and Waste Disposal 9) Environmental Management Considerations

99

HOW TO ESTIMATE DIRECT COSTS ???

In the initial stages of project development, estimates must be

derived by using various relationships.

As the project develops and more detail is available, the estimate

also will be in more detail.

Following are some general steps that may be used for developing

the direct costs of a detailed estimate.1) Material Takeoff 2) Pricing the Material and Equipment 3) Construction Equipment 4) Labor 5) Special Conditions 6) Government Furnished Material 7) Sampling and Analysis Costs 8) Transportation and Waste Disposal 9) Environmental Management Considerations

1010

Detailed Estimates MethodologyDetailed Estimates Methodology

After most or all of the detail design work is complete, approximate

estimates are supplemented by detailed estimates

Stage 1: Quantity takeoffMeasurement of material & Labor quantities

Quantities usually recappedتتلخص by trade for control reasons

Stage 2: Direct Cost contributionΣ [Quantity] x [Unit Costs] = Estimated direct cost of

construction

1111

Detailed Estimates MethodologyDetailed Estimates Methodology

Notes on Detailed EstimatesHave differing ranges of uncertainties

Distributions typically asymmetric.

More an art than a science – or bookkeeping الدفاتر مسك لعلم قريبة

Detailed quantitative estimates possible– but ignore important

qualitative factors

Wealth وفرة of trade-specific and method specific.

detail complexity للحسابات المطلوبة بالتفاصيل التعقيد صفة تعطيها

Frequently depends heavily on subcontractor estimatesالفرعي المقاول تقديرات علي كبير بشكل تعتمد

1212

Cost Classification Cost Classification

1. Direct Cost

– Labor Cost

– Material Cost

– Equipment Cost

– Tests Expenses

2. Indirect Cost (“Overhead”)

– Interest on loans

– Trailer rental

– Office costs

– AC/heat

– Planning & logistics

– Supervision

1313

Suggestion table used for estimating your projectSuggestion table used for estimating your project

1414

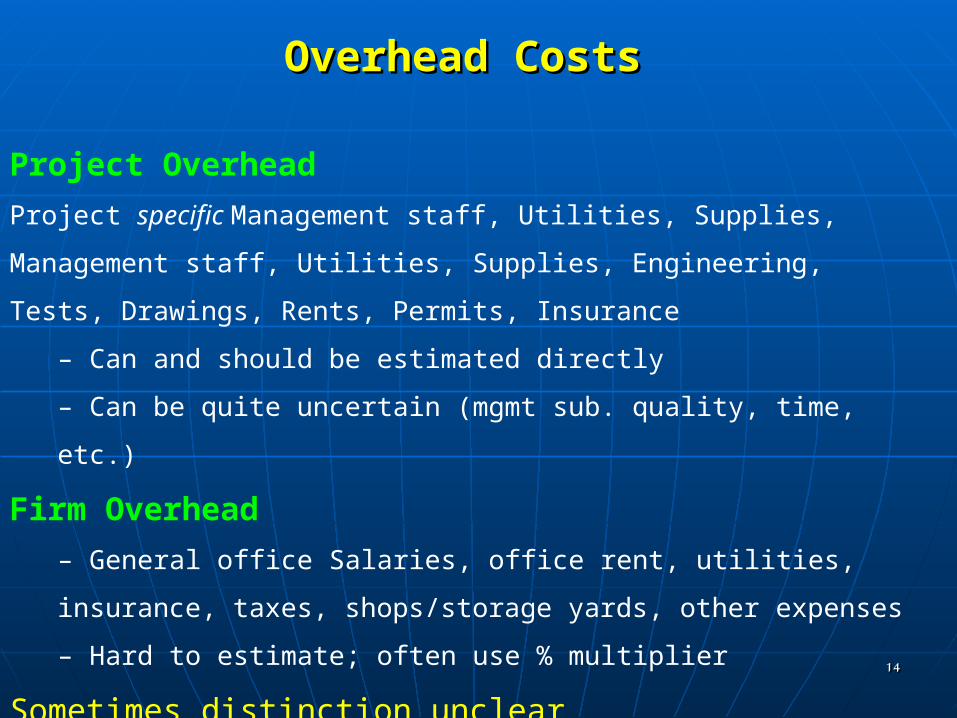

Overhead CostsOverhead Costs

Project Overhead

Project specific Management staff, Utilities, Supplies, Management

staff, Utilities, Supplies, Engineering, Tests, Drawings, Rents,

Permits, Insurance

– Can and should be estimated directly

– Can be quite uncertain (mgmt sub. quality, time, etc.)

Firm Overhead

– General office Salaries, office rent, utilities, insurance, taxes,

shops/storage yards, other expenses

– Hard to estimate; often use % multiplier

Sometimes distinction unclear

1515

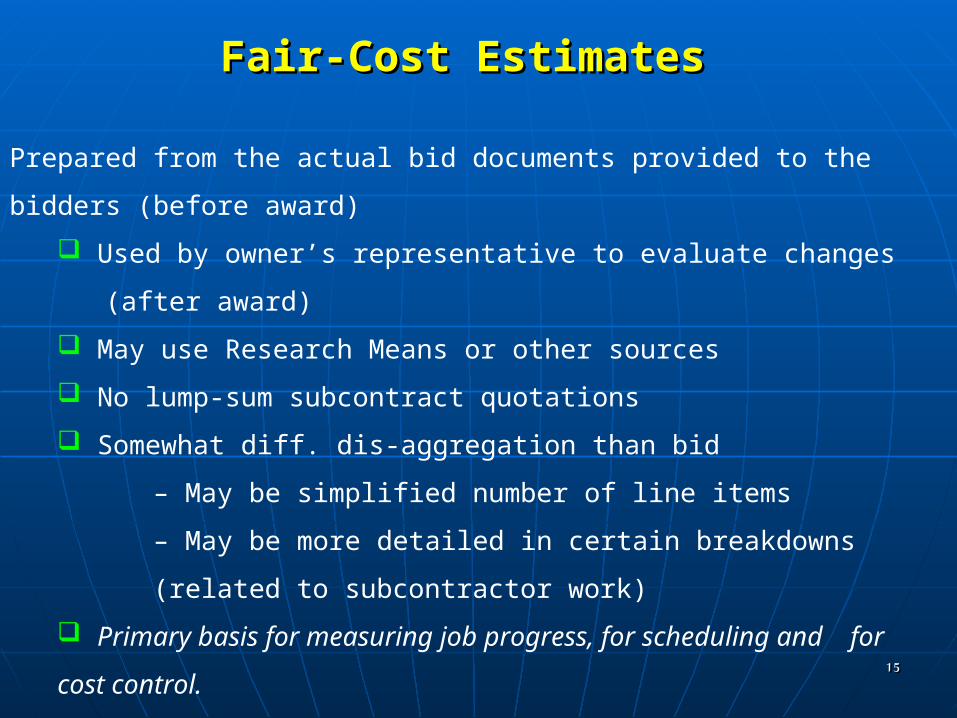

Fair-Cost EstimatesFair-Cost Estimates

Prepared from the actual bid documents provided to the bidders

(before award)

Used by owner’s representative to evaluate changes

(after award)

May use Research Means or other sources

No lump-sum subcontract quotations

Somewhat diff. dis-aggregation than bid

– May be simplified number of line items

– May be more detailed in certain breakdowns (related to

subcontractor work)

Primary basis for measuring job progress, for scheduling and

for cost control.

1616

Contractor’s Bid EstimateContractor’s Bid Estimate

Low enough to obtain the work, yet high enough to make profit

Often relies on

– Historical productivity data for company

– Intuition on speed of movement

– Quantity takeoff for most important items

Sometimes less detailed than fair cost estimates -

subcontractors from 30% to 80% of the project

Is estimating a streamlined process?

– A look at bids received for a typical project in a competitive

area will sometimes show more than 50% difference between

the low and the high bidders

1717

Definitive EstimatesDefinitive Estimates

There comes a time when a definitive estimate can be prepared that

will forecast the final project cost with little margin for error…

This error can be minimized through the proper addition of an

evaluated contingency

Four categories for purposes of reviewing definitive estimates:

– Traditional

– Design-Build

– Professional CM

– Unit-price

1818

Definitive Estimates - TraditionalDefinitive Estimates - Traditional

Lump-sum - definitive estimate = low bidder’s quotation +

evaluated contingency

•Fast track guaranteed maximum price, cost- plus-a-fee

•Definitive estimate will need

– Detailed project and specifications

– Firm material quotations

– Subcontractor quotes

– Prices for major equipment

1919

Definitive Estimates – Design-BuildDefinitive Estimates – Design-Build

Lump-sum, guaranteed maximum price, cost plus-a-fee

• Lump-sum can be misleading to an unknowledgeable owner.

– The cost is known but the facility that is going to be delivered is

unknown

• In guaranteed maximum price and cost plus-a- fee contracts

the definite estimates can be obtained earlier if compared to the

traditional approach because one entity is performing both

design and construction

2020

Definitive Estimates - CMDefinitive Estimates - CM

The definitive estimate can be accurately prepared about the same

time as the guaranteed-maximum or cost maximum or cost- plus-a-

fee option under traditional approach

• Examples show that is possible to develop definitive

estimates after the detailed design is about 95% complete.

2121

Definitive Estimates – Unit PriceDefinitive Estimates – Unit Price

Unit Price Projects:

• Usually heavy construction projects like dams, tunnels,

highways, and airports Prices constants while quantities vary within

limits inherent in the nature of work.

• Quantities may overrun or underrun owing to a number of

potential causes such as additional foundation, excavation to solid

rock, poor ground conditions, etc.

• Without reliable geological information the final cost may not

be known accurately until the end of the

project

2222

Quantity TakeoffQuantity Takeoff

Really requires thinking!

• Systematic identification of quantities of materials

and work required

• Key features sought

– Exhaustive

– Mutually exclusive

• Used to calculate several factors

– Amount of material (e.g. concrete CY)

– Equipment utilization

– Labor

• Breakdown often uses WBS

2323

Labor EstimationLabor Estimation

Most difficult, tricky

• For easy transferability, should separate into - Q: Unit

(Quantity)

– P: $/hour (Labor Price per hour)

– W: hour/unit (Labor hours per unit -- productivity)

• Total cost $ = Q * P * W

2424

Labor Price Estimation (P)Labor Price Estimation (P)

Components

– Wages (varies by area, Law, seniority, …)

– Insurance (varies w/contractor record, work type)

– Social security (insurance)

– Unemployment tax (state)

– Fringe benefits (holiday, retirement, health…)

– Wage premiums(prize)

2525

Wage PremiumsWage Premiums

For shift work

– Sometimes adjust hours

• Overtime

– 1.5-3x for overtime

– Some crafts paid overtime if over 32 hours

• Hazardous/difficult work

– Larger crane

– Underground work

2626

Labor Productivity Estimation (W)Labor Productivity Estimation (W)

Difficult but critical

• High importance of qualitative factors

(environment, morale, fatigue, learning, etc)

• The primary means by which to control labor costs

• Historical data available

– Department of Labor, professional orgs, state govs..)

2727

Productivity ConsiderationsProductivity Considerations

Considerations

• Location of jobsite (local skill base, Law rules)

• Learning curves

• Work schedule (overtime, shift work)

• Weather

– Elaborate work-difficult, costs

• Environment

– Location on jobsite, noise, proximity to matereials

• Management style

• Worksite rules

2828

Learning CurvesLearning Curves

2929

BUDGETBUDGET UNCERTAINTY AND RISK UNCERTAINTY AND RISK

MANAGEMENT MANAGEMENT

3030

EstimateEstimate of Project Cost: of Project Cost: Estimate Made at Project StartEstimate Made at Project Start

3131

Three Basic Causes for Change in ProjectsThree Basic Causes for Change in Projects

Errors made by cost estimator about how to achieve tasks.

• New knowledge about the nature of the performance goal or

setting.

• A mandate.

3232

Risk ManagementRisk Management

Risk Management Planning

• Risk Identification

• Qualitative Risk Analysis

• Risk Response Planning

• Risk Monitoring and Control

3333

Failure Mode and Effect Analysis (FMEA)Failure Mode and Effect Analysis (FMEA)

List ways project might fail

• Evaluate severity (S) of each failure

• Estimate likelihood (L) of each failure occurring

• Estimate ability to detect each failure (D)

• Calculate Risk Priority Number (RPN)

• Sort potential failures by their RPNs