1 Budgeting in Greece Presentation at the annual meeting of Senior Budget Officials, Vienna, June...

24

1 Budgeting in Greece Presentation at the annual meeting of Senior Budget Officials, Vienna, June 2008 Ian Hawkesworth, Budgeting and Public Expenditures Division, GOV

-

Upload

jordan-mason -

Category

Documents

-

view

213 -

download

0

Transcript of 1 Budgeting in Greece Presentation at the annual meeting of Senior Budget Officials, Vienna, June...

1

Budgeting in GreecePresentation at the annual meeting of Senior Budget Officials, Vienna, June 2008

Ian Hawkesworth, Budgeting and Public Expenditures Division, GOV

2

Agenda

1. General overview2. Budget preparation3. Parliamentary approval4. Budget Execution5. Accounting and Audit

3

1. General overview2. Budget preparation3. Parliamentary approval4. Budget Execution5. Accounting and Audit

4

General Overview

• Founding member of OECD• Joined EC in 1981• 12th member of the euro zone• Per capita GDP at 89% of the euro zone

average• Services is the dominant contributor to

GDP• Rapid GDP per capita growth; on average

more than 4.0% per year during 2002-2007

5

6

General Overview

• Under the Stability and Growth Pact Excessive Deficit Procedure 2006/2007

• Successful in reducing the deficit below 3% of GDP in 2006

• Greece is projected to continue keep the deficit below recommended 3% of GDP

7

Source: OECD Economic Outlook, Vol.2007/2, No. 82, December

8

General Overview

• Future challenge lies in reducing government debt

• Currently, Greece has one of the highest general government debt ratios among OECD members (over 90% of GDP, Maastricht definition)

• Correspondingly Greece pays significant interest payments in terms of GDP share

9

Source: OECD Economic Outlook, Vol.2007/2, No. 82, December

10

11

General Overview• Situation is projected to be exacerbate with

growing current account balance deficit.• Explanations for the “dip”:

– Eurozone entry lowered borrowing costs which then led to consumer spending boom

– Surge of public and private investment increased demand for imported goods and services

* Because Greece is service-oriented economy, demand for durable goods translates to a current account balance deficit

12Source: IMF

13

1. General overview2. Budget preparation3. Parliamentary approval4. Budget Execution5. Accounting and Audit

14

Key Features

• Weak top-down budgeting• Lack of unitary budget process

(special accounts, capital budgeting)• Detailed input orientation• Little performance information• One year budgeting perspective• Program budget reform in pipeline

15

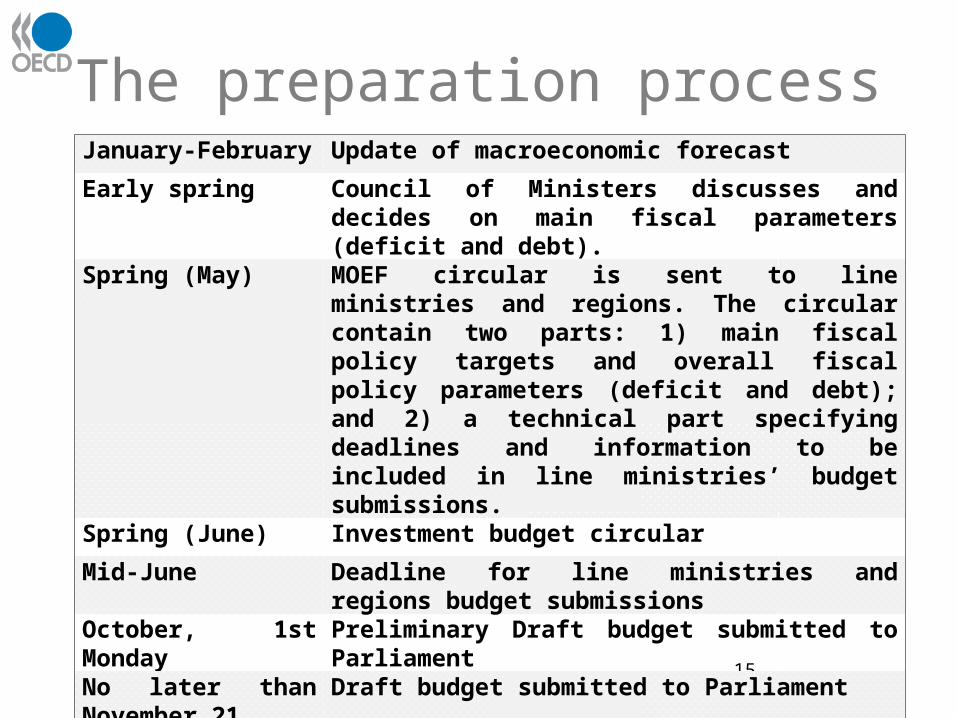

The preparation processJanuary-February Update of macroeconomic forecast

Early spring Council of Ministers discusses and decides on main fiscal parameters (deficit and debt).

Spring (May) MOEF circular is sent to line ministries and regions. The circular contain two parts: 1) main fiscal policy targets and overall fiscal policy parameters (deficit and debt); and 2) a technical part specifying deadlines and information to be included in line ministries’ budget submissions.

Spring (June) Investment budget circular

Mid-June Deadline for line ministries and regions budget submissions

October, 1st Monday Preliminary Draft budget submitted to Parliament

No later than November 21

Draft budget submitted to Parliament

No later than December 31

Budget is voted on in Parliament

16

1. General overview2. Budget preparation3. Parliamentary approval4. Budget Execution5. Accounting and Audit

17

Institutional features

• Unicameral legislature with 300 members elected for a four-year term by proportional representation.

• Presently a centre right majority• Traditionally majority governments• No independent research capacity

18

Parliamentary process

• Pre-budget consultation (early October)• Tabling• Committee on Economic Affairs

examination • Plenary debate• Approval of the budget – block vote (end

of December)• In-year oversight – weak• The definition of “Significant”

19

1. General overview2. Budget preparation3. Parliamentary approval4. Budget Execution5. Accounting and Audit

20

Key Features

• Extensive focus on ensuring the legality and propriety of expenditure

• Very extensive use of ex ante control• Execution involves a large amount of actors

which confuses responsibility• Reallocation very time consuming (6650 in

2007, half < € 5000) which burdens MOEF• New framework law places more emphasis

on ex post control, reducing the FAOs role, but effect too early to say

21

Ministry of Finance

Fiscal Audit Office

Tax and Payment

Office

Supreme Audit Court

Body(Ministry,Region,

etc)

Execution process

3rd Party

* Excludes Salaries and Pensions

22

1. General overview2. Budget preparation3. Parliamentary approval4. Budget Execution5. Accounting and Audit

23

Accounting

• On a cash basis, no plans for accruals• Responsibility for central government

accounting is centralized in GAO’s Directorate of Public Accounts

• Five different accounting systems for public sector: hospitals, social security funds, municipalities, public law entities, central government

• Modernization project

24

The Hellenic Court of Audit • Inspired by French Cour des Comptes• About 650 staff• Ex ante and as ex post control take up the

same amount of resources • Less than 1 pct. of ex ante controls result in

changes • No performance or value for money audits• Some defense and foreign affairs expenditure

is excluded from HCA audit• Little dialogue with Parliament on basis of

HCA’s annual report

![CAPITAL BUDGETING [Read-Only] - c.ymcdn.comc.ymcdn.com/.../CAPITAL_BUDGETING.pdf · CAPITAL BUDGETING Capital expenditures purchase physical assets to provide future services Yields](https://static.fdocuments.in/doc/165x107/5b15f7ab7f8b9a00708c252e/capital-budgeting-read-only-cymcdncomcymcdncomcapital-capital.jpg)

![CAPITAL BUDGETING [Read-Only] › ... › CAPITAL_BUDGETING.pdf · 2018-04-01 · CAPITAL BUDGETING Capital expenditures purchase physical assets to provide future services Yields](https://static.fdocuments.in/doc/165x107/5f2455918348e27b03790872/capital-budgeting-read-only-a-a-capital-2018-04-01-capital-budgeting.jpg)