1 Berkley Medical Excess Underwriters ERC ® Hospital Professional Liability: A Most Inhospitable...

51

1 Berkley Medical Excess Underwriters ERC ® Hospital Professional Liability: A Most Inhospitable Environment March 12, 2003 Matt Dolan, OneBeacon Insurance Daryl Douglas, GE ERC Sabrina Hart, Zurich North America Robin Maley, Maley Healthcare Strategies Kimberly Willis, Berkley Medical Medical Professional Liability Symposium

-

Upload

hector-ball -

Category

Documents

-

view

214 -

download

0

Transcript of 1 Berkley Medical Excess Underwriters ERC ® Hospital Professional Liability: A Most Inhospitable...

1Berkley Medical Excess Underwriters

ERC ®

Hospital Professional Liability: A Most Inhospitable Environment

March 12, 2003

Matt Dolan, OneBeacon InsuranceDaryl Douglas, GE ERC

Sabrina Hart, Zurich North AmericaRobin Maley, Maley Healthcare Strategies

Kimberly Willis, Berkley Medical

Medical Professional Liability Symposium

2

Agenda

Problem: Rising severity

Impact: Carrier results

Response: Reconsider underwriting architecture and risk management culture

3

Problem

Increasing severity of verdicts/settlements

– National and regional data

Trends driving the larger pay-outs

Strategies to reduce loss costs

ERC ®

4

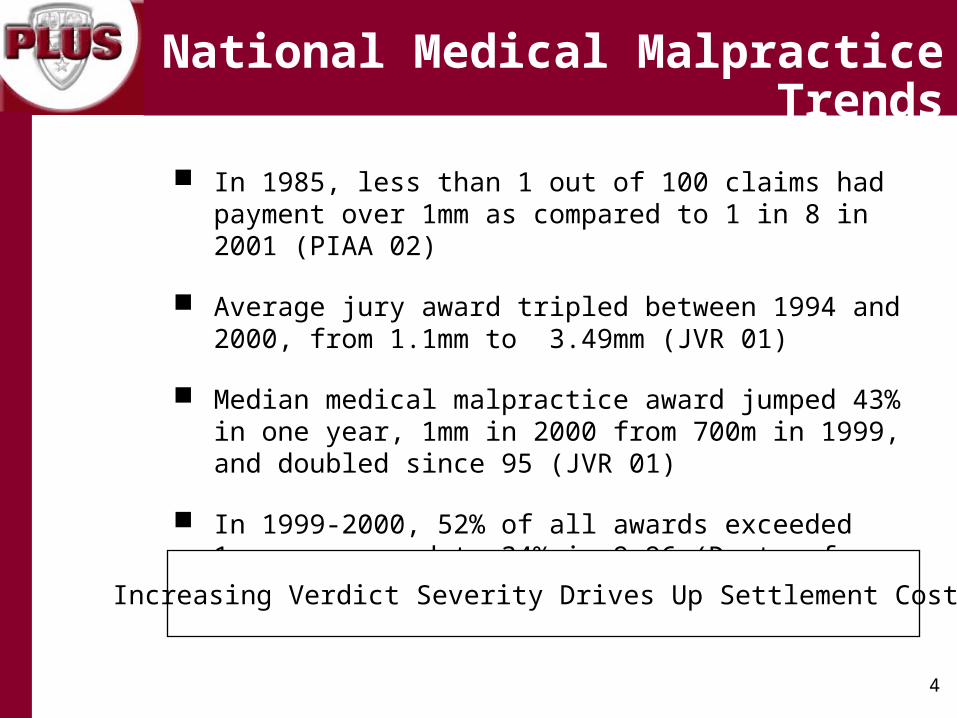

National Medical Malpractice Trends

In 1985, less than 1 out of 100 claims had payment over 1mm as compared to 1 in 8 in 2001 (PIAA 02)

Average jury award tripled between 1994 and 2000, from 1.1mm to 3.49mm (JVR 01)

Median medical malpractice award jumped 43% in one year, 1mm in 2000 from 700m in 1999, and doubled since 95 (JVR 01)

In 1999-2000, 52% of all awards exceeded 1mm as opposed to 34% in 9-96 (Dept. of Health, 7/02)

Increasing Verdict Severity Drives Up Settlement Costs

5

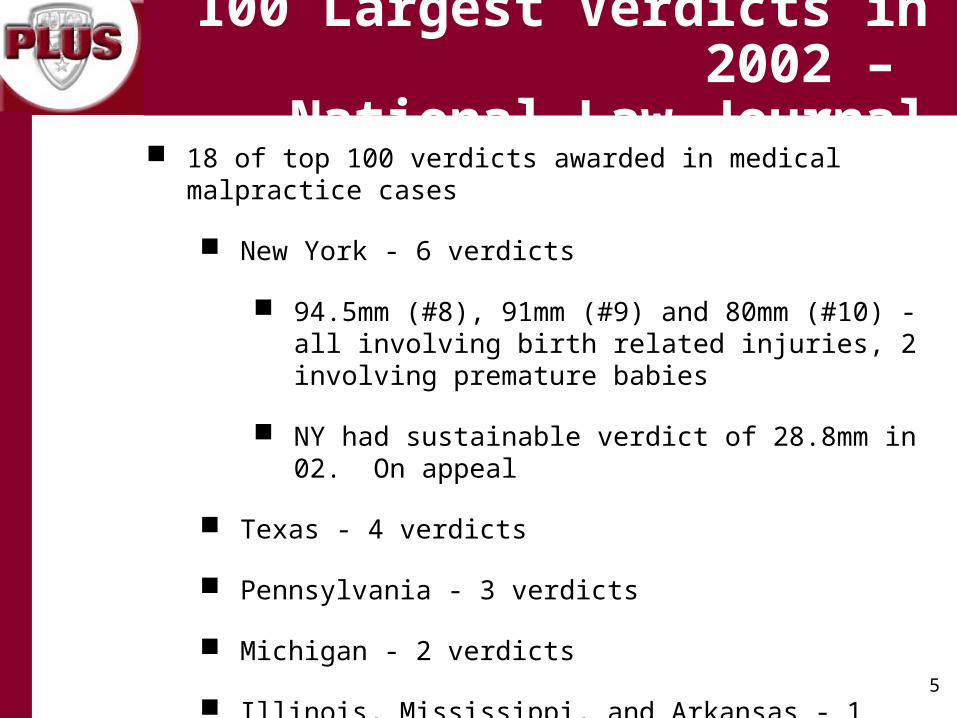

100 Largest Verdicts in 2002 – National Law Journal

18 of top 100 verdicts awarded in medical malpractice cases

New York - 6 verdicts

94.5mm (#8), 91mm (#9) and 80mm (#10) - all involving birth related injuries, 2 involving premature babies

NY had sustainable verdict of 28.8mm in 02. On appeal

Texas - 4 verdicts

Pennsylvania - 3 verdicts

Michigan - 2 verdicts

Illinois, Mississippi, and Arkansas - 1 verdict each

6

Chicago - 2002 Verdicts and Settlements

$30mm verdict - failure to timely deliver resulting in brain injury

$22.3mm verdict - failure to dx spinal cord impingement of 64 y/m resulting in quadriplegia

$22mm verdict - double amputation of cab driver

$20.25mm verdict - fail to dx fetal distress. 19 y/m spastic quad

$19.5mm settlement - death of mom and brain damaged infant

$19mm settlement - asphasia of former bond broker in 30’s

19mm settlement - young woman in vegetative state

18.4mm settlement - fail to dx fetal distress

17.5mm settlement - fail to prevent aneurysm of young female

7

Large Award Drivers - Common Jurisdictional Factors

Effective, aggressive, competitive, powerful and large plaintiffs’ bar

Failed or no tort reform measures

Limited mediation and counter-productive pre-trials

Demographics of the jury pool

History of large verdicts and settlements

Elected judiciary

8

Philadelphia

CAT Fund made record pay-outs in 02, rising to $348,000,000 from $321,600,000 in 01

In 02, 50% of CAT Fund pay-outs went toward Philadelphia cases

37 judgments for more than $1,000,000 in 2001

Other sample verdicts

2003- 24.6mm (failure to perform c/s leading to brain damage of infant)

2001 - 37mm, 25mm, 20.8mm

2000 - 100mm, 59mm, 49.6mm

9

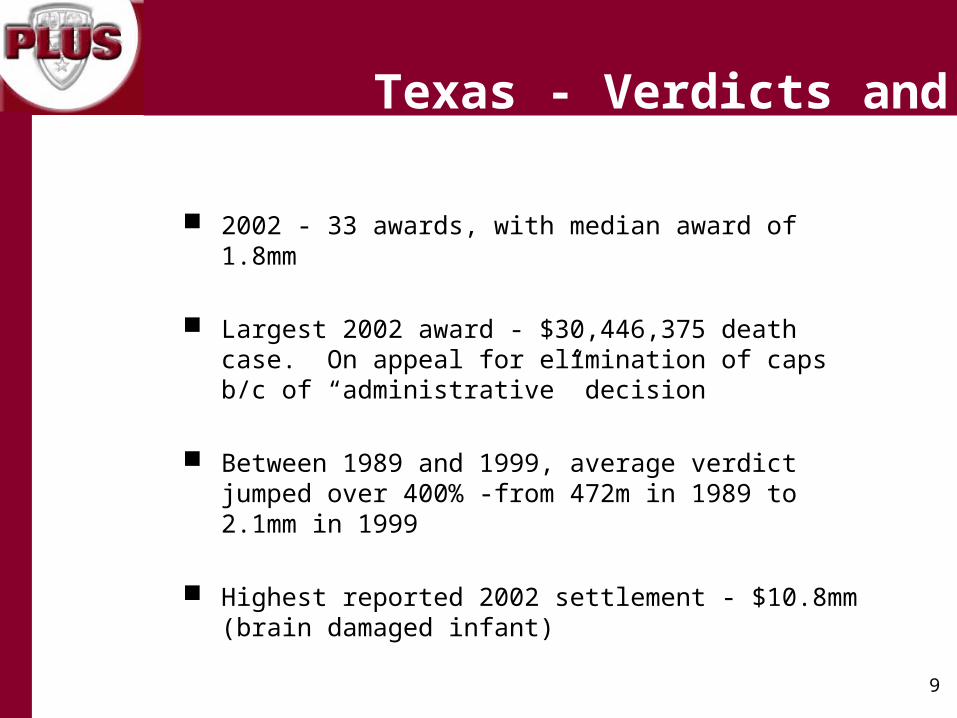

Texas - Verdicts and Settlements

2002 - 33 awards, with median award of 1.8mm

Largest 2002 award - $30,446,375 death case. On appeal for elimination of caps b/c of “administrative” decision

Between 1989 and 1999, average verdict jumped over 400% -from 472m in 1989 to 2.1mm in 1999

Highest reported 2002 settlement - $10.8mm (brain damaged infant)

10

Texas - Verdicts and Settlements

Other large Texas verdicts

$268 million wrongful death verdict in Dallas County in 2000 (settled pre-verdict for app. 2.5mm)

$67.5 million medical malpractice verdict in Dallas in 1999-above the knee amputation of child (settled app. 7mm)

$59 million medical malpractice verdict in Eagle Pass in 2000-impaired newborn (settled app. 30mm)

$40 million medical malpractice verdict in Houston in 2000-negligent credentialing case (reversed on appeal)

$20 million MCO E&O verdict in Corpus ChristiImproper de-selection of provider (settled app. 5mm)

11

Large Award Drivers - Sociological Factors

Monetary desensitization - sport/star salaries; lotteries; publication of large verdicts and medical errors

Emboldened plaintiffs’ lawyers - less willing to settle

Managed care backlash - staff reductions; reduced skill levels of providers; disgruntled health care staff

Jurors are experts and have access to more information

Advances in medicine

12

Large Award Drivers Medical/Legal Factors

Finger-pointing between doctors and hospital staff

Alleged altered records and late entries

Incomplete, inconsistent and outdated policies

used as a sword by plaintiffs

Lack of documentation

Shifting burden of proof: bad result = negligence

Apparent agency - ED, radiology, anesthesiology

13

Survey

Disagree Somewhat

1%Agree

Somewhat20%

Agree Strongly79%

A hospital is responsible for the actions of all medical professionals that practice at the hospital.

14

Survey

No28%

Yes72%

A doctor with privileges at a hospital (a doctor not on staff and not receiving salary from the hospital but able to admit patients and practice at the hospital) makes a mistake in treating a patient.

Is the hospital liable for the doctor’s actions?

15

So What Can We Do?

Support and lobby for tort reform

Focus on improving patient safety and error reduction

Focus on high risk areas - OB, ED

Hire the most respected and experienced trial lawyers

Cannot afford to defend on the cheap

16

Claims and Legal Management of Catastrophic Cases

Spend Money to Save Money - Bob Clifford, Chicago

But (claims specialists) won’t spend the dough. That’s where I’ve got an edge on you. Because my experience is that all these claims people who are watching this thing, they are cheap. They are penny wise and Tom Foolish…. I don’t have a budget on a case….They can … bury me in terms of their financial weight. But not on any one case….. I mean, here, it costs you $10,000 to $20,000 to do a focus group. Most defendants don’t do focus groups. And yet they’ll try the case and get wacked for an extra million bucks. Hello? What am I missing here?

17

So What Can We Do?

Utilize jury consultants

Consider effect of settlement amounts driving future costs

Try the right cases

fine line between overpaying and gambling

Push mediation

Hire an experienced and skilled claims staff

Restoration Phase - Return of the Fundamentals

Phase of cycle expected to last well into 2004 - 2005

Interest Rate >1% lower than last year

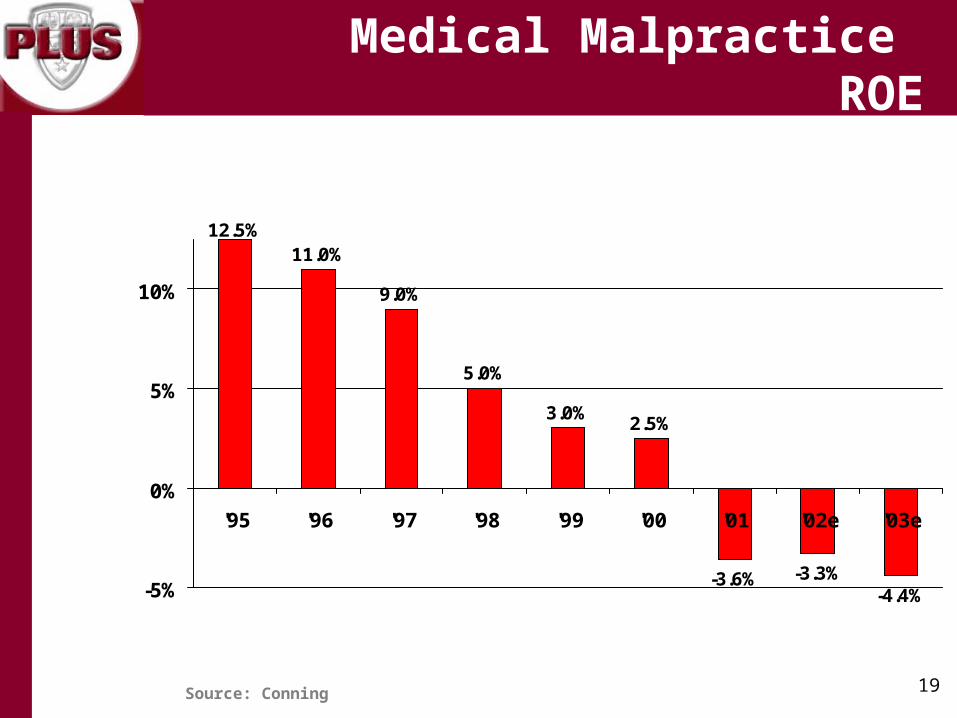

Lower Combined Needed for Same ROE

2002 interest rates95 Combined è13.5% ROE

2003 interest rates95 Combined è 12% ROE

Impact: Where Are We?

19

12.5%11.0%

9.0%

5.0%

3.0%2.5%

-3.6% -3.3%-4.4%-5%

0%

5%

10%

'95 '96 '97 '98 '99 '00 '01 '02e '03e

Source: Conning

Medical Malpractice ROE

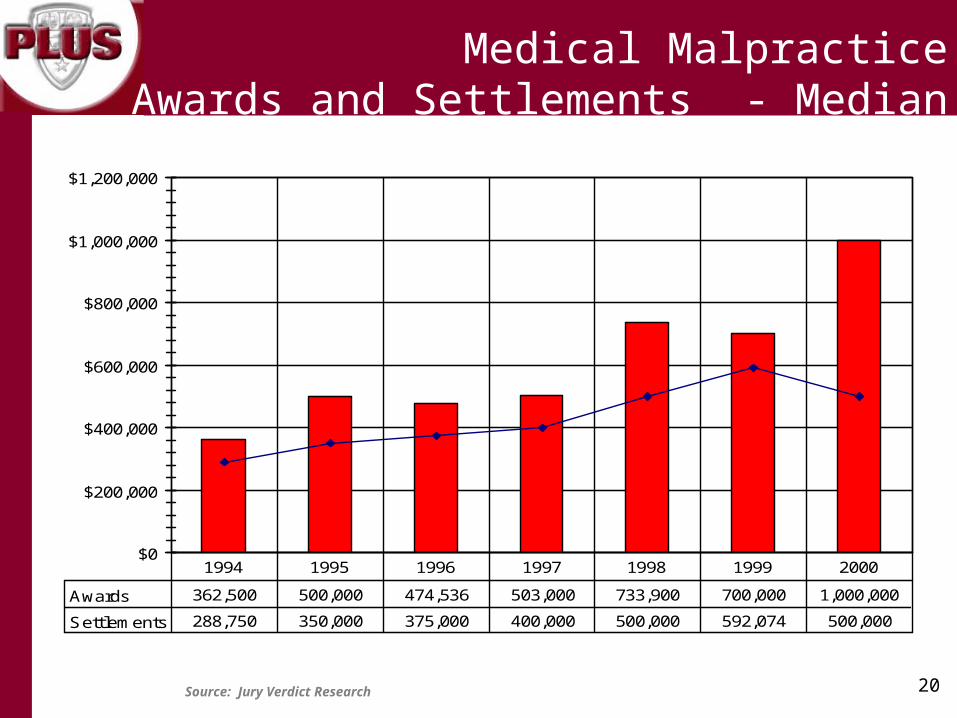

20Source: Jury Verdict Research

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

Awards 362,500 500,000 474,536 503,000 733,900 700,000 1,000,000

Settlements 288,750 350,000 375,000 400,000 500,000 592,074 500,000

1994 1995 1996 1997 1998 1999 2000

Medical MalpracticeAwards and Settlements - Median

21Source: Jury Verdict Research

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

Awards 1,139,862 2,039,037 1,900,870 1,970,872 2,981,796 3,429,019 3,481,876

Settlements 644,201 643,119 755,327 971,466 1,044,002 1,459,290 1,052,785

1994 1995 1996 1997 1998 1999 2000

Medical MalpracticeAwards and Settlements - Mean

Rate - What is Adequate?

$375k in 2000

$635K in 2000 with just 2% inflation

70%

139% 2001E Combined

121% Breakeven, 105% to return desired ROE

34%

Theory 1 Theory 2

$500k in late 80’s

33%

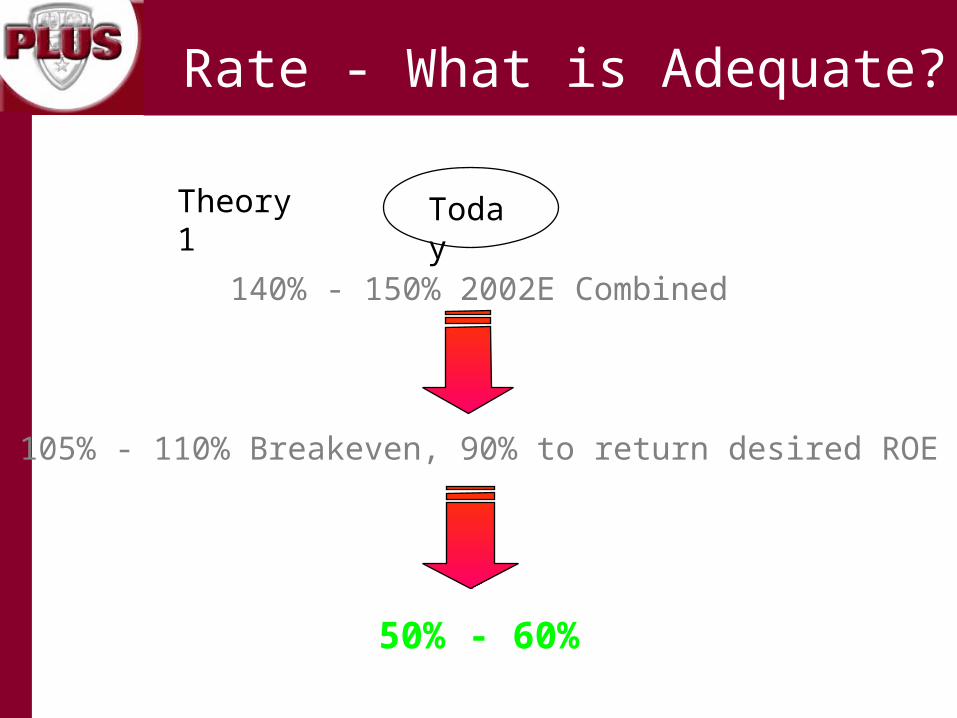

Rate - What is Adequate?

140% - 150% 2002E Combined

105% - 110% Breakeven, 90% to return desired ROE

50% - 60%

Theory 1 Today

Selection, Price, and Terms

• Risk Selection Commitment to holistic risk mgmt Risk Profiling Greater scrutiny of underlying

• Price Continued rate increases to ensure acceptable

ROE What is adequate? Minimum premiums

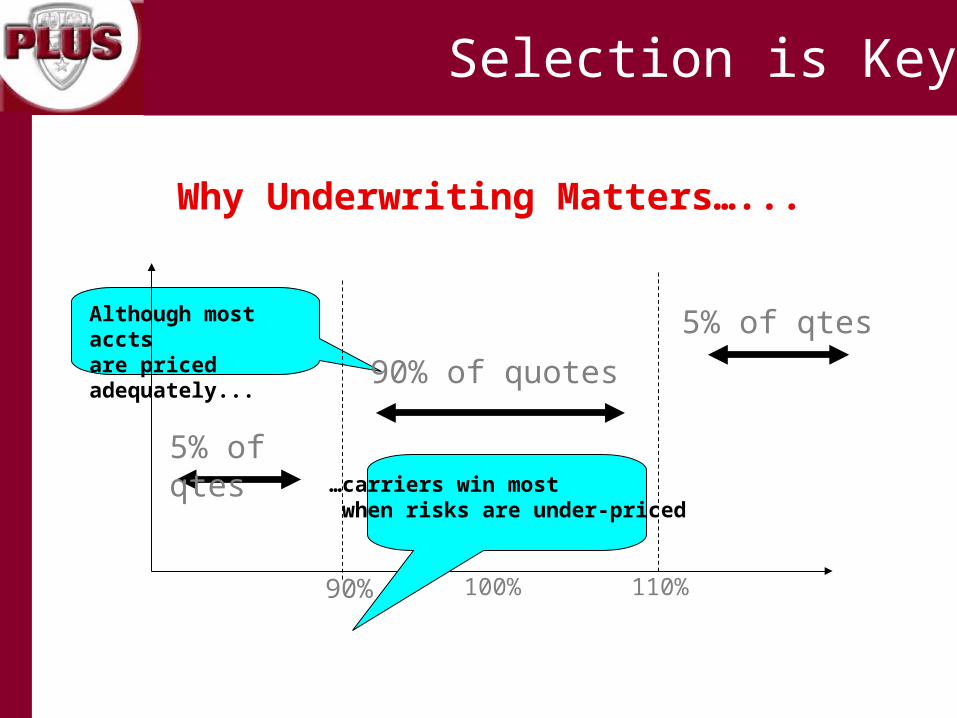

Selection is Key

Why Underwriting Matters…...

90% 100% 110%

5% of qtes

90% of quotes

5% of qtesAlthough most accts are priced adequately...

…carriers win most when risks are under-priced

Underwriting Matters

Misclassification of exposure units

Evaluation date of loss run > 90 days from eff date

Inadequate reserving

Failure to request/review excess loss runs

Failure to evaluate underlying coverage

Uninsured/under insured physicians

Insufficient attachment point

Inappropriate policy forms

Blanket named insureds

Incorrect retroactive date

Waiver of collateral

Terms

Adequate attachment point

Unaggregated attachment point

Maintenance retentions Reduced capacity Collateral Implied Warranty excl. Auto attachment points

Buffer layers/inner aggregates

ALAE within the limit of liability

Retroactive dates Punitive excl. Mold excl. Terrorism

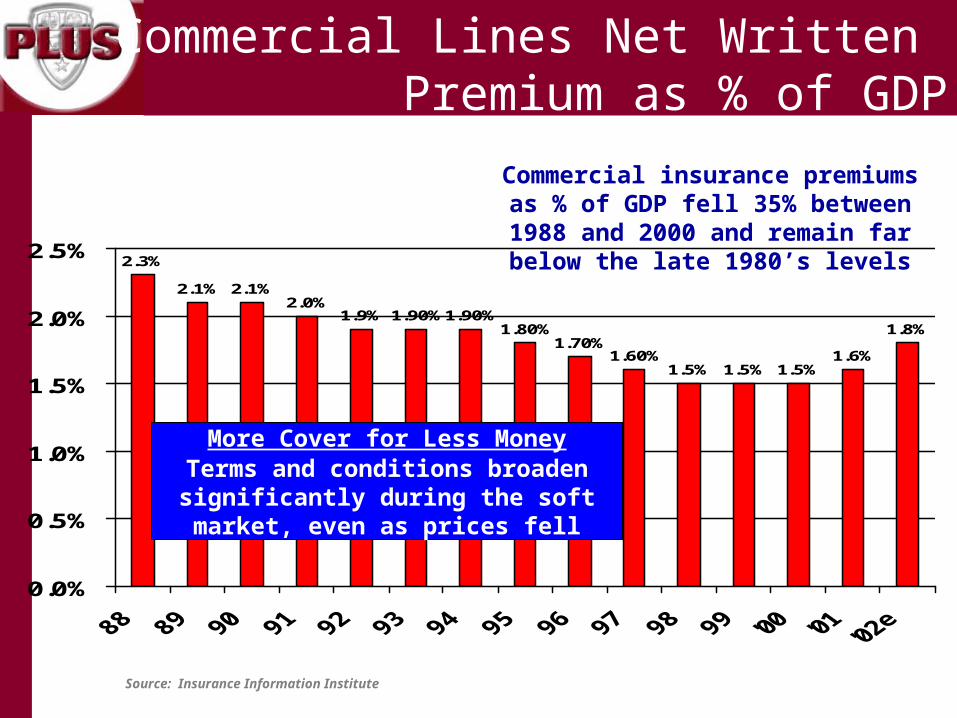

Source: Insurance Information Institute

2.3%

2.1%2.0%

1.9% 1.90%1.90%1.80%

1.70%1.60%

1.5% 1.5% 1.5%1.6%

1.8%

2.1%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Commercial insurance premiums as % of GDP fell 35% between 1988 and 2000 and remain far below the late 1980’s levels

Commercial Lines Net Written Premium as % of GDP

More Cover for Less MoneyTerms and conditions broaden

significantly during the soft market, even as prices fell

A Picture Is Worth A Thousand Words

30

The Price/Placement Framework Reconsidered

Capacity movement along the Price/Quality curve

The need to reconsider ROE expectations

The volatility factor

Trend and its impact on excess limits

The cost of capacity

Response: Underwriting Architecture

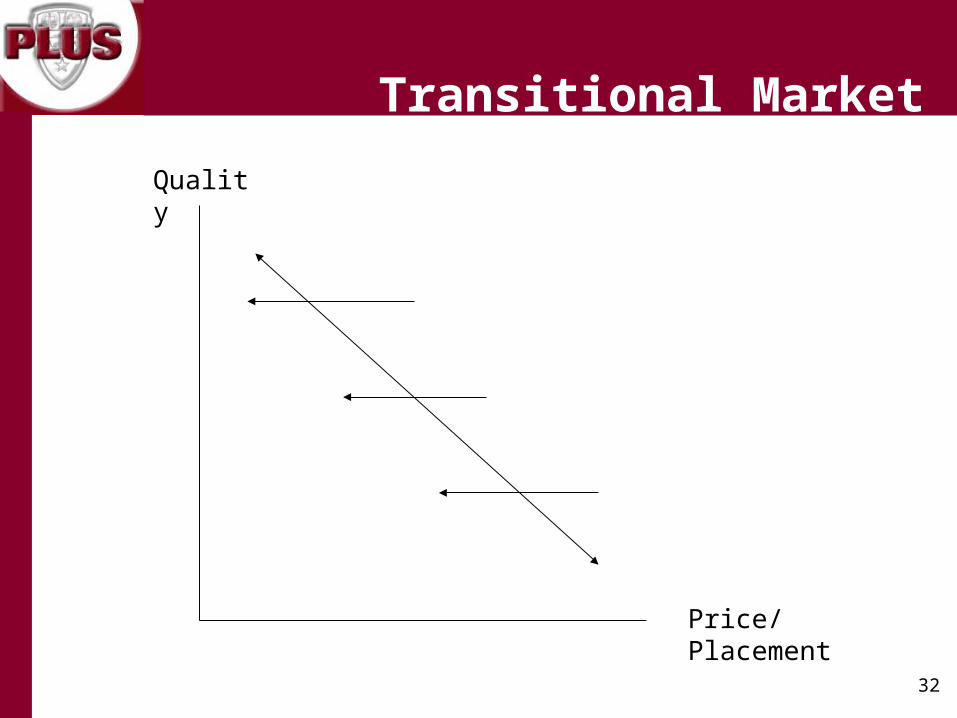

31

Quality

Price/Placement

Hard Market

32

Quality

Price/Placement

Transitional Market

33

Quality

Price/Placement

Soft Market

34

“Show Me the Money!”

Reimbursement/cash flow

Liability insurance premiums

HIPAA and corporate compliance expenditures

Increased ER patient flow

Patient safety/QI efforts

Disaster/emergency preparedness

Financial Challenges

35

Quality

Price/Placement

36

Pricing/ROE Assumptions

Industry-demonstrated propensity for loss

2001 CY loss > $2 billion

Risk loads must be imbedded in ROE targets

15%-17% > risk-free rate

Premium-to-surplus ratio must contemplate volatility of business and specific risk portfolio

37

The Volatility Issue

Example:

Account purchases $15 million in limit:

$ 900,000 for primary $5,000,000

$ 400,000 for $10,000,000 excess $5,000,000

Total: $1,400,000

Account experiences a loss of $12,500,000

Loss ratios:

Carrier writing entire $15,000,000 limit: 892% Carrier writing $5,000,000 primary layer: 555% Carrier writing $10,000,000 excess layer: 1,875%

38

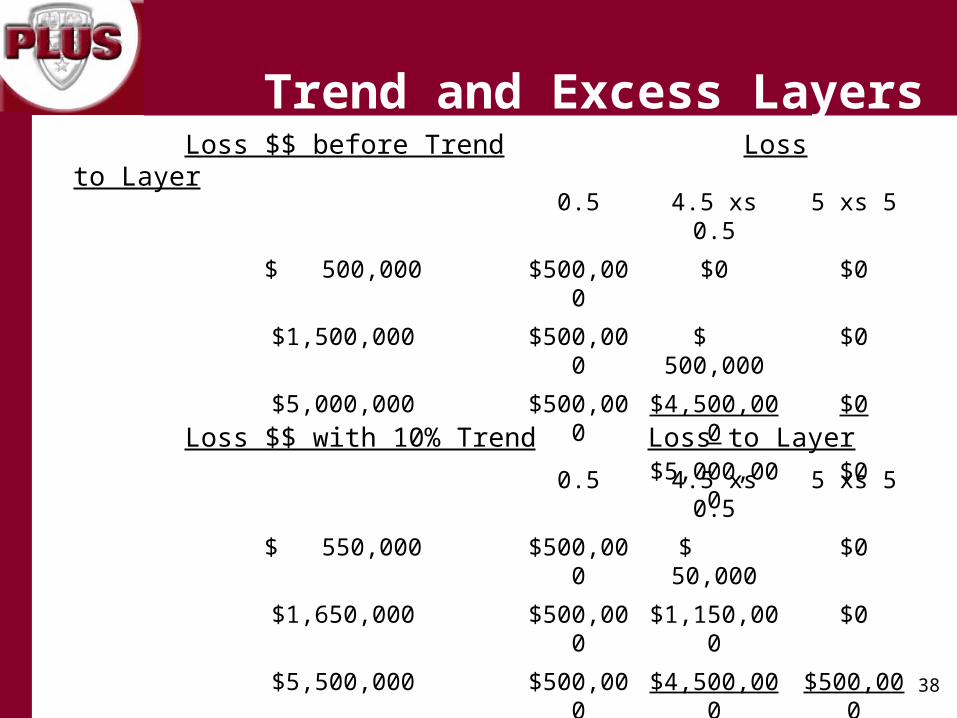

Loss $$ before Trend Loss to Layer

0.5 4.5 xs 0.5 5 xs 5

$ 500,000 $500,000 $0 $0

$1,500,000 $500,000 $ 500,000 $0

$5,000,000 $500,000 $4,500,000 $0

$5,000,000 $0

Loss $$ with 10% Trend Loss to Layer

0.5 4.5 xs 0.5 5 xs 5

$ 550,000 $500,000 $ 50,000 $0

$1,650,000 $500,000 $1,150,000 $0

$5,500,000 $500,000 $4,500,000 $500,000

$5,700,000 $500,000

Trend and Excess Layers

39

Trend to the Layer:

$500,000 = 0%

$4,500,000 xs $500,000 = 40%

$5,000,000 xs $5,000,000 = 100%

40

Attachment Rate per Million

Implied Funding

Implied Frequency

$15mm –$24mm

$12,000 136 0.7%

$25mm –$34mm

$10,000 163 0.6%

$35mm –$49mm

$ 8,500 191 0.5%

$50mm –Over

$ 7,500 217 0.5%

Cost of Capacity

41

It’s a Whole New Game!

Evaluating Risk in Healthcare Organizations

Response: Changing Risk Management Culture

42

Knowing your opponent and what risks prevail

Economic downturn Financial challenges Massive corporate restructuring Increased monitoring and reporting requirements Human resource dilemmas Safety emphasis Technology advancements Changing role of the Risk Manager

Key Factors - Impacting Risk Management Strategies

43

Strike Three – The Ten Pound Gorillas

Reimbursement/revenue Increasing unemployment and decreasing healthcare

benefits/insurance Discontent providers + patients = claims increases

Economic Downturn

44

Who’s on First?

Elimination or restriction on services, treatments and locations for financial or liability insurance reasons

Inconsistent leadership

Mixed industry and internal messages

Communication obstacles and disconnects

New, untried strategies

Massive Corporate Restructuring

45

More Referees and Umpires!

Unflattering “newsmagazine” profiles (e.g., 60 Minutes, 20/20)

Legislative mandates/proposals

Increase in regulatory requirements (e.g., HIPAA, EMTALA)

New and increased accreditation standards

Increased Monitoring and Reporting Requirements

46

Fielding a “Competitive” Team

Continuing nursing shortage

New providers are fewer

More providers retiring (e.g., liability/insurance)

Education and training

Fraud and whistleblowers

Human Resource Dilemmas

47

MTXE: Mental Toughness, Extra Effort

Medical errors

Patient rights

Public perception; branding and advertising

Maintenance/improvement of care locations

Disaster/emergency preparedness

Employee safety

Safety Emphasis

48

“12th Man”

Data abundance

Quicker decision timeframes

New education requirements

Third-party vendors and tools

Improved resource efficiency

Technology Advancements

49

Broadened responsibilities•Environment•Mold/air quality•Homeland security•Construction wrap-up•Institutional Review Boards•Advertising•Media Relations

Expanded knowledge base•More complex risks

Faster turnaround times•Adverse event resolution

Credentialing Greater interactions with

brokers/insureds Increased accountability

Changing Role of the Risk Manager

50

Developing an Effective Game Plan

Creative risk management solutions

Patient-centric focus

Strong leadership/accountability

Sharp, intuitive and skilled Risk Manager

Risk awareness at the grass-roots level

Risk management metrics/outcome measurements

Willingness to work collaboratively

Open door and communication

Sizing Up Risk

51

Score, Defend and Win!

Matching Insurance Solutions vs. Strategic Plans