1 Announcement - Acq of TEB (final...

23

Page 1 of 23 CENSOF HOLDINGS BERHAD (“CENSOF” OR THE “COMPANY”) (I) PROPOSED ACQUISITION BY CENSOF OF 349,112,731 ORDINARY SHARES OF RM0.20 EACH IN TIME ENGINEERING BERHAD ("TEB") (“TEB SHARES”), REPRESENTING 45.03% EQUITY INTEREST IN TEB, FROM KHAZANAH NASIONAL BERHAD (“KHAZANAH”) FOR A CASH CONSIDERATION OF APPROXIMATELY RM69.82 MILLION (“PROPOSED ACQUISITION”); AND (II) PROPOSED MANDATORY TAKE-OVER OFFER BY CENSOF TO ACQUIRE ALL THE REMAINING TEB SHARES NOT ALREADY OWNED BY CENSOF UPON COMPLETION OF THE PROPOSED ACQUISITION (“OFFER SHARES”) (“PROPOSED MGO”) (COLLECTIVELY REFERRED TO AS THE “PROPOSALS”) 1. INTRODUCTION On behalf of the Board of Directors of Censof (“Board”), RHB Investment Bank Berhad (“RHBIB”) wishes to announce that Censof had, on 12 September 2013, entered into a conditional share sale and purchase agreement with Khazanah to acquire 349,112,731 TEB Shares, representing 45.03% of the issued and paid-up share capital of TEB for a cash consideration of approximately RM69.82 million (“SSA”). Upon completion of the Proposed Acquisition, Censof will emerge as the new controlling shareholder in TEB with 45.03% equity interest in TEB. Accordingly, pursuant to Section 218(2) of the Capital Markets & Services Act, 2007 (“CMSA”) and Section 9(1), Part III of the Malaysian Code on Take-Overs and Mergers, 2010 (“Code”), Censof will be obliged to extend a mandatory general offer to the shareholders of TEB other than Censof (“Non-Interested TEB Shareholders”) at a cash offer price of RM0.20 for every one (1) Offer Share. In relation thereto, Censof will serve the notice of the Proposed MGO to the Board of Directors of TEB in accordance with Section 11(7) of the Code (“Notice”) upon the SSA becoming unconditional. 2. INFORMATION ON TEB TEB was incorporated under the name of TIME Engineering Sdn Bhd on 12 October 1970 as a trading company distributing welding products and was subsequently converted into a public limited company on 24 June 1983 upon which it assumed its present name. The company was listed on the then Main Board of Bursa Malaysia Securities Berhad (“Bursa Securities”) on 12 September 1983.

Transcript of 1 Announcement - Acq of TEB (final...

Page 1 of 23

CENSOF HOLDINGS BERHAD (“CENSOF” OR THE “COMPANY”) (I) PROPOSED ACQUISITION BY CENSOF OF 349,112,731 ORDINARY SHARES OF RM0.20

EACH IN TIME ENGINEERING BERHAD ("TEB") (“TEB SHARES”), REPRESENTING 45.03% EQUITY INTEREST IN TEB, FROM KHAZANAH NASIONAL BERHAD (“KHAZANAH”) FOR A CASH CONSIDERATION OF APPROXIMATELY RM69.82 MILLION (“PROPOSED ACQUISITION”); AND

(II) PROPOSED MANDATORY TAKE-OVER OFFER BY CENSOF TO ACQUIRE ALL THE

REMAINING TEB SHARES NOT ALREADY OWNED BY CENSOF UPON COMPLETION OF THE PROPOSED ACQUISITION (“OFFER SHARES”) (“PROPOSED MGO”)

(COLLECTIVELY REFERRED TO AS THE “PROPOSALS”) 1. INTRODUCTION

On behalf of the Board of Directors of Censof (“Board”), RHB Investment Bank Berhad (“RHBIB”) wishes to announce that Censof had, on 12 September 2013, entered into a conditional share sale and purchase agreement with Khazanah to acquire 349,112,731 TEB Shares, representing 45.03% of the issued and paid-up share capital of TEB for a cash consideration of approximately RM69.82 million (“SSA”). Upon completion of the Proposed Acquisition, Censof will emerge as the new controlling shareholder in TEB with 45.03% equity interest in TEB. Accordingly, pursuant to Section 218(2) of the Capital Markets & Services Act, 2007 (“CMSA”) and Section 9(1), Part III of the Malaysian Code on Take-Overs and Mergers, 2010 (“Code”), Censof will be obliged to extend a mandatory general offer to the shareholders of TEB other than Censof (“Non-Interested TEB Shareholders”) at a cash offer price of RM0.20 for every one (1) Offer Share. In relation thereto, Censof will serve the notice of the Proposed MGO to the Board of Directors of TEB in accordance with Section 11(7) of the Code (“Notice”) upon the SSA becoming unconditional.

2. INFORMATION ON TEB TEB was incorporated under the name of TIME Engineering Sdn Bhd on 12 October 1970 as a trading company distributing welding products and was subsequently converted into a public limited company on 24 June 1983 upon which it assumed its present name. The company was listed on the then Main Board of Bursa Malaysia Securities Berhad (“Bursa Securities”) on 12 September 1983.

Page 2 of 23

The principal activity of TEB is that of investment holding whilst the principal activities of its principal subsidiaries are as follows:

(Source: Annual Report 2012 of TEB)

The remaining subsidiaries of TEB are currently dormant and have been placed under members’ voluntary liquidation. These subsidiaries are Toplink Advisory and Management Services Sdn Bhd, TIME Automation and Management Services Sdn Bhd and its subsidiary, TIME Spectrum Communication Sdn Bhd.

The principal business divisions of TEB Group are the:

(i) provision of e-commerce trade facilitation service by Dagang Net Technologies Sdn Bhd,

a 71.25%-owned subsidiary of TEB (“Dagang Net”). Dagang Net is the developer and operator of the national single window (“NSW”), a national initiative that provides a one-stop trade facilitation system linking federal statutory bodies and government agencies with trading communities. The NSW enables electronic exchange of data, submission of documents and transmission of messages for cargo clearance to support the country's strong international trade business;

(ii) provision of data centre services through the Integrated Enterprise Centre (“IEC”) which houses contact centre, data centre, disaster recovery centre, network operations centre and security operations centre under one roof in Cyberjaya. IEC is a Tier-3 Compliant data centre, Tier-4 Ready facility and will soon receive Green Building Index certification while its Security Operations Centre is now ISO 27001 certified. TEB is able to offer processing power and storage space via the Oracle Exadata machine thus becoming the first in ASEAN to provide Private Cloud Computing Managed Services and Secured Managed Services; and

(iii) systems integration service through TEB Systems Integrators Sdn Bhd (“TSI”) in the management of large IT projects, specifically to advise clients on computing and networking solutions, developing maintenance and application services for the public sector.

The statutory information of TEB and historical financial information of TEB Group for the past three (3) financial years ended (“FYE”) 31 December 2012 together with the unaudited financial information for the six (6)-month financial period ended (“FPE”) 30 June 2013 are set out in the Appendix of this Announcement.

TEB

Dagang Net Technologies Sdn Bhd

TEB Systems Integrators Sdn Bhd

Providing expertise in information technology project management and consultancy, supply and maintenance of information and communication technology hardware and equipment, and asset management.

TEB Quantum Technology Sdn Bhd

Providing IT solutions, cyber security services, managed services and supply of computer hardware, software and peripherals.

71.25% 100.00% 100.00%

Development, management and provision of business-to-government and business-to-business e-commerce and computerized transaction facilitation services.

Page 3 of 23

3. INFORMATION ON KHAZANAH Khazanah is the investment holding arm of the Government of Malaysia entrusted to manage the commercial assets held by the Government of Malaysia and to undertake strategic investments. Khazanah was incorporated on 3 September 1993 as a public limited company under the Companies Act 1965 (“Act”). Save for one (1) share owned by the Federal Land Commissioner, all the share capital of Khazanah is owned by the Minister of Finance Incorporated, a corporate body incorporated pursuant to the Minister of Finance (Incorporation) Act, 1957. The board of Directors of Khazanah as at the date of this Announcement is as follows:

Name Nationality

Direct Indirect

No. of shares held

% No. of shares held

%

Dato’ Seri Mohd Najib bin Tun Hj Abdul Razak

Malaysian - - - -

Tan Sri Dato’ Nor Mohamed Yakcop Malaysian - - - -

Dato’ Sri Ahmad Husni Hanadziah Malaysian - - - -

Tan Sri Md Nor Yusof Malaysian - - - -

Raja Tan Sri Dato’ Seri Arshad bin Raja Tun Uda

Malaysian - - - -

Tan Sri Mohamed Azman bin Yahya Malaysian - - - -

Dato’ Mohammed Azlan bin Hashim Malaysian - - - -

Tan Sri Andrew Sheng Malaysian - - - -

Tan Sri Dato’ Azman bin Hj Mokhtar Malaysian - - - -

(Source: www.khazanah.com.my)

4. DETAILS OF THE PROPOSALS 4.1 Details Of The Proposed Acquisition 4.1.1 Background Information

The Proposed Acquisition entails the acquisition by Censof of Khazanah’s entire equity interest in TEB of 349,112,731 TEB Shares (“Sale Shares”), representing approximately 45.03% equity interest in TEB, for a total cash consideration of RM69,822,546.20 (“Purchase Consideration”) or RM0.20 per Sale Share.

4.1.2 Salient terms of the SSA

(a) Consideration and payment of the Sale Shares

(i) Khazanah agrees to sell to Censof, and Censof agrees to purchase from Khazanah, the Sale Shares free from all encumbrances and together with all rights and benefits attaching thereto;

(ii) The Proposed Acquisition will be undertaken via two (2) tranches in the

following manner:

Tranches No. of Sale Shares

To be completed by

Tranche 1 178,956,773 Completion Date I (as defined below) Tranche 2 170,155,958 Completion Date II (as defined below) Total 349,112,731

Page 4 of 23

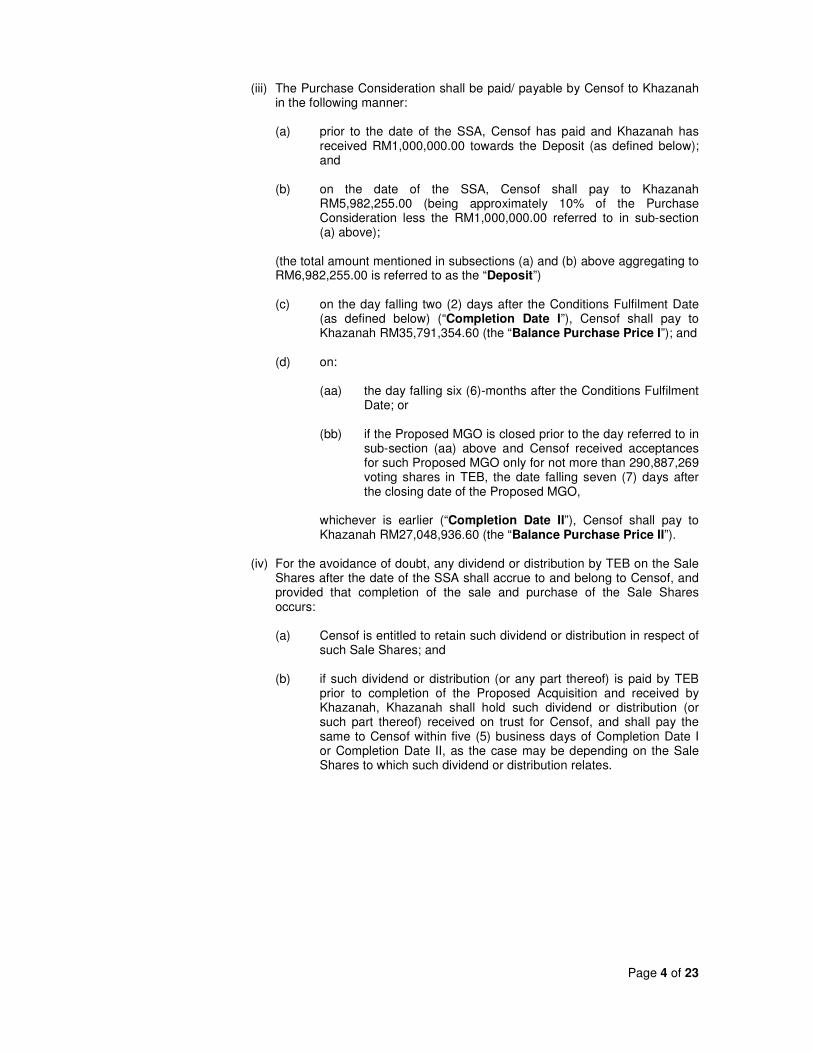

(iii) The Purchase Consideration shall be paid/ payable by Censof to Khazanah in the following manner:

(a) prior to the date of the SSA, Censof has paid and Khazanah has

received RM1,000,000.00 towards the Deposit (as defined below); and

(b) on the date of the SSA, Censof shall pay to Khazanah

RM5,982,255.00 (being approximately 10% of the Purchase Consideration less the RM1,000,000.00 referred to in sub-section (a) above);

(the total amount mentioned in subsections (a) and (b) above aggregating to RM6,982,255.00 is referred to as the “Deposit”)

(c) on the day falling two (2) days after the Conditions Fulfilment Date

(as defined below) (“Completion Date I”), Censof shall pay to Khazanah RM35,791,354.60 (the “Balance Purchase Price I”); and

(d) on:

(aa) the day falling six (6)-months after the Conditions Fulfilment

Date; or

(bb) if the Proposed MGO is closed prior to the day referred to in sub-section (aa) above and Censof received acceptances for such Proposed MGO only for not more than 290,887,269 voting shares in TEB, the date falling seven (7) days after the closing date of the Proposed MGO,

whichever is earlier (“Completion Date II”), Censof shall pay to Khazanah RM27,048,936.60 (the “Balance Purchase Price II”).

(iv) For the avoidance of doubt, any dividend or distribution by TEB on the Sale

Shares after the date of the SSA shall accrue to and belong to Censof, and provided that completion of the sale and purchase of the Sale Shares occurs:

(a) Censof is entitled to retain such dividend or distribution in respect of

such Sale Shares; and

(b) if such dividend or distribution (or any part thereof) is paid by TEB prior to completion of the Proposed Acquisition and received by Khazanah, Khazanah shall hold such dividend or distribution (or such part thereof) received on trust for Censof, and shall pay the same to Censof within five (5) business days of Completion Date I or Completion Date II, as the case may be depending on the Sale Shares to which such dividend or distribution relates.

Page 5 of 23

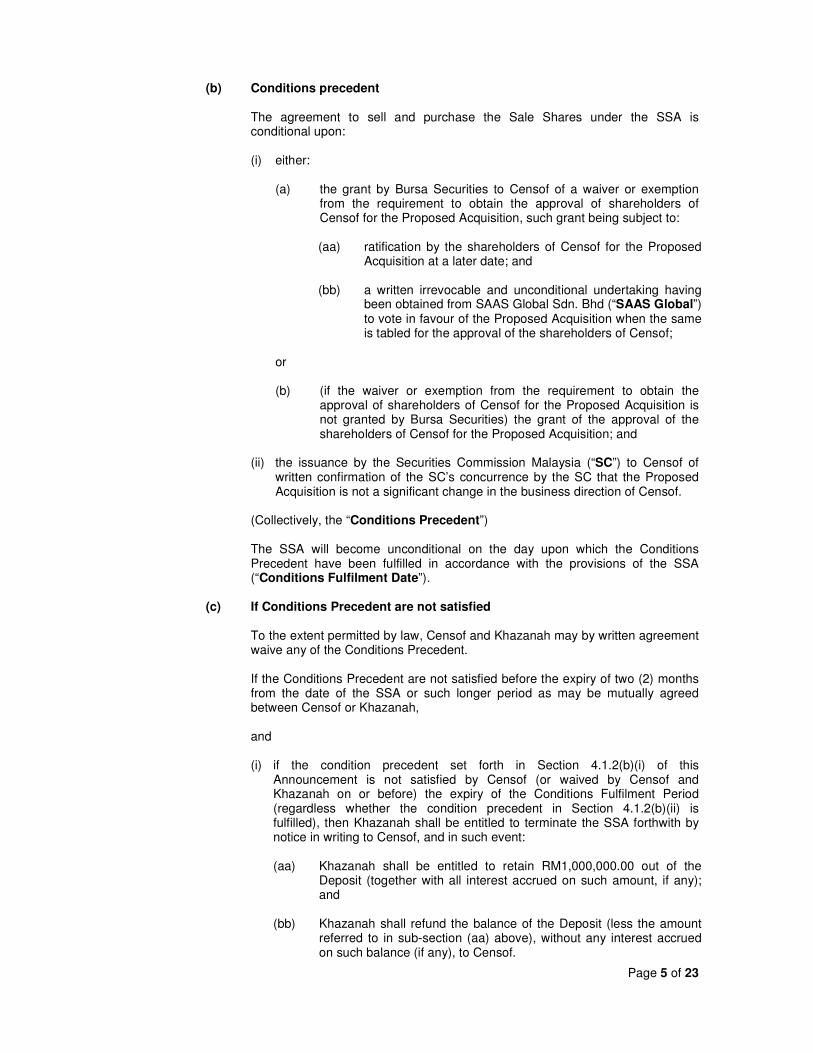

(b) Conditions precedent

The agreement to sell and purchase the Sale Shares under the SSA is conditional upon:

(i) either:

(a) the grant by Bursa Securities to Censof of a waiver or exemption

from the requirement to obtain the approval of shareholders of Censof for the Proposed Acquisition, such grant being subject to:

(aa) ratification by the shareholders of Censof for the Proposed

Acquisition at a later date; and

(bb) a written irrevocable and unconditional undertaking having been obtained from SAAS Global Sdn. Bhd (“SAAS Global”) to vote in favour of the Proposed Acquisition when the same is tabled for the approval of the shareholders of Censof;

or (b) (if the waiver or exemption from the requirement to obtain the

approval of shareholders of Censof for the Proposed Acquisition is not granted by Bursa Securities) the grant of the approval of the shareholders of Censof for the Proposed Acquisition; and

(ii) the issuance by the Securities Commission Malaysia (“SC”) to Censof of

written confirmation of the SC’s concurrence by the SC that the Proposed Acquisition is not a significant change in the business direction of Censof.

(Collectively, the “Conditions Precedent”) The SSA will become unconditional on the day upon which the Conditions Precedent have been fulfilled in accordance with the provisions of the SSA (“Conditions Fulfilment Date”).

(c) If Conditions Precedent are not satisfied

To the extent permitted by law, Censof and Khazanah may by written agreement waive any of the Conditions Precedent. If the Conditions Precedent are not satisfied before the expiry of two (2) months from the date of the SSA or such longer period as may be mutually agreed between Censof or Khazanah, and (i) if the condition precedent set forth in Section 4.1.2(b)(i) of this

Announcement is not satisfied by Censof (or waived by Censof and Khazanah on or before) the expiry of the Conditions Fulfilment Period (regardless whether the condition precedent in Section 4.1.2(b)(ii) is fulfilled), then Khazanah shall be entitled to terminate the SSA forthwith by notice in writing to Censof, and in such event:

(aa) Khazanah shall be entitled to retain RM1,000,000.00 out of the

Deposit (together with all interest accrued on such amount, if any); and

(bb) Khazanah shall refund the balance of the Deposit (less the amount

referred to in sub-section (aa) above), without any interest accrued on such balance (if any), to Censof.

Page 6 of 23

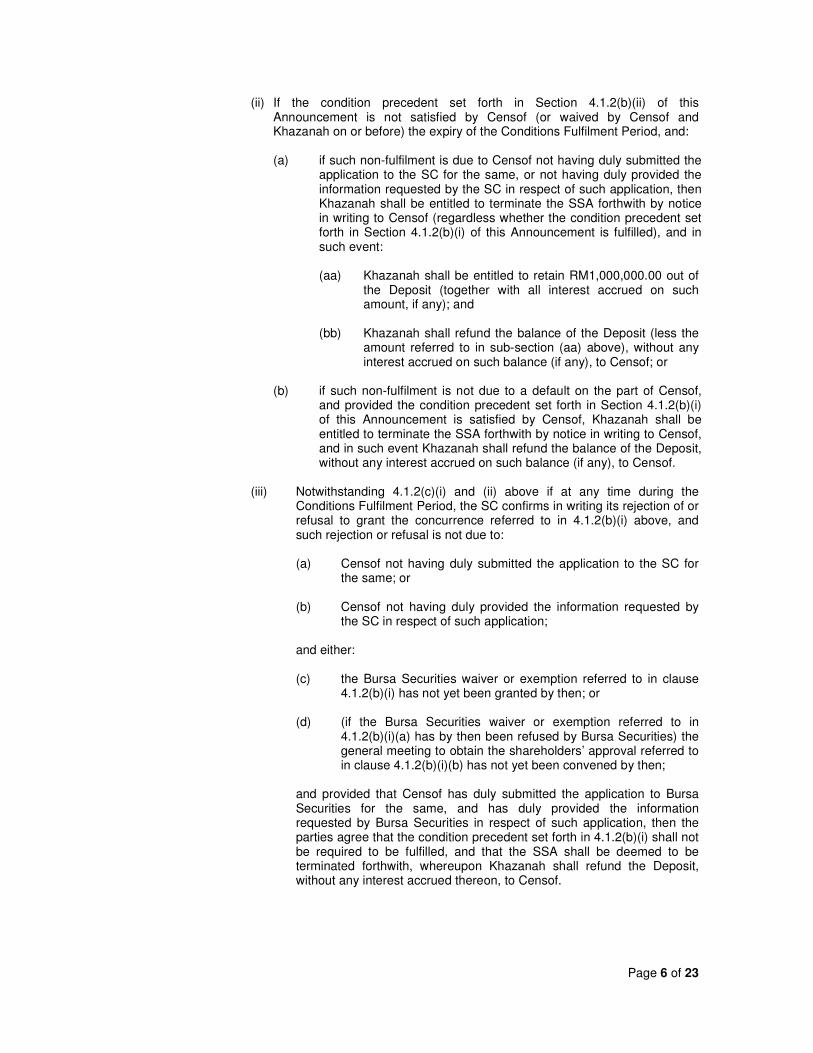

(ii) If the condition precedent set forth in Section 4.1.2(b)(ii) of this

Announcement is not satisfied by Censof (or waived by Censof and Khazanah on or before) the expiry of the Conditions Fulfilment Period, and:

(a) if such non-fulfilment is due to Censof not having duly submitted the

application to the SC for the same, or not having duly provided the information requested by the SC in respect of such application, then Khazanah shall be entitled to terminate the SSA forthwith by notice in writing to Censof (regardless whether the condition precedent set forth in Section 4.1.2(b)(i) of this Announcement is fulfilled), and in such event:

(aa) Khazanah shall be entitled to retain RM1,000,000.00 out of

the Deposit (together with all interest accrued on such amount, if any); and

(bb) Khazanah shall refund the balance of the Deposit (less the

amount referred to in sub-section (aa) above), without any interest accrued on such balance (if any), to Censof; or

(b) if such non-fulfilment is not due to a default on the part of Censof,

and provided the condition precedent set forth in Section 4.1.2(b)(i) of this Announcement is satisfied by Censof, Khazanah shall be entitled to terminate the SSA forthwith by notice in writing to Censof, and in such event Khazanah shall refund the balance of the Deposit, without any interest accrued on such balance (if any), to Censof.

(iii) Notwithstanding 4.1.2(c)(i) and (ii) above if at any time during the

Conditions Fulfilment Period, the SC confirms in writing its rejection of or refusal to grant the concurrence referred to in 4.1.2(b)(i) above, and such rejection or refusal is not due to:

(a) Censof not having duly submitted the application to the SC for

the same; or

(b) Censof not having duly provided the information requested by the SC in respect of such application;

and either:

(c) the Bursa Securities waiver or exemption referred to in clause 4.1.2(b)(i) has not yet been granted by then; or

(d) (if the Bursa Securities waiver or exemption referred to in

4.1.2(b)(i)(a) has by then been refused by Bursa Securities) the general meeting to obtain the shareholders’ approval referred to in clause 4.1.2(b)(i)(b) has not yet been convened by then;

and provided that Censof has duly submitted the application to Bursa Securities for the same, and has duly provided the information requested by Bursa Securities in respect of such application, then the parties agree that the condition precedent set forth in 4.1.2(b)(i) shall not be required to be fulfilled, and that the SSA shall be deemed to be terminated forthwith, whereupon Khazanah shall refund the Deposit, without any interest accrued thereon, to Censof.

Page 7 of 23

Upon such termination, the SSA shall be of no further force and effect and neither party to the SSA shall have any claim against each other except in respect of any right or obligation under the SSA which is expressed to apply after the termination of the SSA, and any right or obligation under the SSA which has accrued prior to such termination.

(d) Completion

Upon receiving the Balance Purchase Price I on Completion Date I, and Balance Purchase Price II on Completion Date II, Khazanah shall complete, execute and lodge with Khazanah’s authorised depository agent the transfer of securities request form as prescribed by Bursa Depository together with relevant supporting documents, for Sale Share Tranche I and Sale Share Tranche II, accordingly as soon as practicable after receipt thereof.

Provided that:

(i) the Deposit has been paid by Censof in accordance with the SSA; and

(ii) there shall have been no termination of the SSA pursuant to Section 4.1.2(e)

of this Announcement.

(e) Termination

(i) If, prior to Completion Date I, it shall be found that any of the warranties of Khazanah or Censof, as the case may be, was when given, or will be or would be, at Completion Date I, not complied with or is otherwise untrue or misleading in any material respect, the non-defaulting party shall be entitled to send a notice to the defaulting party requiring it to remedy such breach within fourteen Business Days after the defaulting party is in receipt of the said notice from the non-defaulting party (or prior to Completion Date I, whichever period is shorter), and in the event where such breach is still not remedied by the defaulting party as aforesaid, the non-defaulting party shall be entitled (in addition to and without prejudice to all other rights or remedies available to it) by notice in writing to the defaulting party to terminate the SSA and:

(a) if Khazanah is the defaulting party, then Khazanah shall refund to

Censof within ten (10) business days of such termination, the Deposit free of interest; and

(b) if Censof is the defaulting party, then Khazanah shall retain and be

entitled absolutely to the Deposit as agreed liquidated damages;

and thereafter neither party shall have any further liability with respect to the SSA.

(ii) If Khazanah fails or refuses to complete the Proposed Acquisition, Censof

shall be entitled to send a notice to Khazanah requiring it to remedy such breach within fourteen business days, failing which Censof shall be entitled to (a) terminate the SSA or (b) bring an action for specific performance of this SSA against Khazanah. If Censof elects to terminate the SSA pursuant to (a) above, Khazanah shall, within ten business days of receipt of Censof’s notice of termination, refund to Censof free of interest all moneys paid to Khazanah and thereafter the SSA shall be of no further force and effect and neither Censof nor Khazanah shall have claim against each other.

Page 8 of 23

(iii) If Censof fails to pay the payment of the Balance Purchase Price I, Balance

Purchase Price II or any part thereof, to Khazanah according to Section 4.1.2(a)(iii) of this Announcement, or fails to complete the Proposed Acquisition according to the SSA for reasons arising from any act, wilful omission, neglect or blameworthy conduct on the part of Censof, Khazanah shall be entitled to send a notice to Censof requiring it to remedy such breach within fourteen business days, failing which Khazanah shall be entitled to (a) terminate the SSA or (b) bring an action for specific performance of this SSA against Censof, or otherwise take such action in law to compel Censof to pay the Balance Purchase Price I and/or Balance Purchase Price II, as the case may be, and/or such part thereof that is outstanding.

If Khazanah elects to terminate the SSA pursuant to (a) above, it shall be entitled absolutely to the Deposit (including all interests accrued thereon) and thereafter the SSA shall be of no further force and effect and neither party shall have claim against each other.

THE REST OF THIS PAGE IS INTENTIONALLY LEFT BLANK

Page 9 of 23

4.1.3 Basis and justification for the Purchase Consideration The Purchase Consideration of RM0.20 per TEB Share was arrived at on a willing buyer-willing seller basis after taking into consideration the five (5)-day volume weighted average price (“VWAP”) of TEB Shares up to and including 11 September 2013 of RM0.28. The justifications of the Purchase Consideration of RM0.20 per TEB Shares are set out as follows: (i) the Purchase Consideration is at a discount of 28.57% to the prevailing market

price of TEB Shares on 11 September 2013, being the last Market Day prior to the execution of the SSA of RM0.28 per TEB Share.

(ii) price-to-book ratio (“PBR”) of 1.54 times based on the audited net assets (“NA”) of TEB and its group of companies (“TEB Group”) for the FYE 31 December 2012 of RM103.2 million.

In view that the TEB Group is mainly involved in provision of information and communications technology (“ICT”) solutions and e-commerce and computerized transaction facilitation services, for the purpose of assessing the Purchase Consideration, the management of Censof has selected several comparable companies which are currently listed on Bursa Securities to give an indication of the current market expectations in relation to the valuation of TEB Group. As there are no companies listed on Bursa Securities that are exactly similar or directly comparable to the TEB Group in terms of composition of business, scale of operations, track record, shareholders’ profile, marketability and liquidity of the shares and future prospects, the comparable companies selected by the management of Censof (“Selected Comparable Companies”) are based on the core business of the Selected Comparable Companies which the management of Censof deem to be comparable to TEB. We wish to highlight that the comparison made is only for illustrative purposes as the Selected Comparable Companies cannot be considered identical or directly similar to the TEB Group in terms of scale of operations, composition of business activities, future prospects, asset base, risk profile and other criteria.

For comparison purposes, we have considered the PBR. The PBR is a method used in the valuation of companies by comparing the company’s market value to its book value. A PBR of less than one (1) time would mean that the market value accorded to the company is less than the NA attributable to the shareholders of the company and may therefore indicate that the company is undervalued. It should be noted that for the purpose the comparable companies analysis, the Board has not considered other financial evaluation methods such as the price-to-earnings multiple of the Comparable Companies, as TEB is currently in a loss making position. The table below provides an illustration comparison of the PBR of TEB relative to that of the Selected Comparable Companies:

Page 10 of 23

Company Principal activities(1)

Audited FYE

Closing price as at 11 September

2013 (RM)

Market capitalisation

as at 11 September

2013

(RM’million)

NA per share

(3)

(RM) PBR

(3)

(times)

Formis Resources Berhad

Formis Resources Berhad is an investment holding company. Through its subsidiaries, the company distributes and maintains computer equipment and software, develops application software and system integration, and provides hardware and software maintenance, network, information, and system integration services. The company provides computer consultant and contractor services.

31 March 2013 (1)

0.705 248.29 0.40 1.76

Heitech Padu Berhad

HeiTech Padu Berhad provides total business solutions in IT which includes system integration, data center management, network related services, and disaster recovery services. The company, through its subsidiaries, also develops software, manages and maintains property, and develops centralized parts price database for the Malaysian insurance industry.

31 December 2012

(1)0.730 73.89 2.04 0.36

Dataprep Holdings Berhad

Dataprep Holdings Berhad is an investment holding company which provides management services. Through its subsidiaries, the company supports, markets, develops and maintains computer equipment, systems, and software. The company also provides computer related consulting and training services and internet application services.

31 March 2013 (1)

0.245 93.86 0.10 2.45

My E.G. Services Berhad

My E.G. Services Berhad provides e-services between the Government of Malaysia and its citizens and businesses. The company's services include electronic delivery of driver and vehicle registrations, licensing and summons services and utility bill payments.

30 June 2012 (1)

1.910

1,138.96 0.20 9.55

High 9.55

Low 0.36

Average 3.53

TEB (2)

0.20 155.04 0.13 1.54

Notes:

(1) As extracted from Bloomberg. (2) Based on the Purchase Consideration of RM0.20 per TEB Share. (3) Based on the latest annual reports of the respective companies.

Page 11 of 23

As illustrated above, based on the audited financial statements for the FYE 31 December 2012, the Purchase Consideration represents a PBR of 1.54 times which is within the range of the PBR of the Selected Comparable Companies of between 0.36 times and 9.55 times, and is below the average PBR of the Selected Comparable Companies of 3.53 times.

(iii) the Proposed Acquisition is for the purchase of a strategic controlling stake in TEB otherwise may not be able to acquire from the open market;

(iv) the potential future earnings, prospects and financial performance of TEB Group as disclosed in Section 7 of this Announcement; and

(v) potential synergistic benefits arising from the Proposed Acquisition to Censof

and its group of companies (“Censof Group” or “Group”) as disclosed in Section 5.1 of this Announcement.

4.1.4 Transactions with Khazanah There have been no transactions between our Group and Khazanah for the preceding twelve (12) months up to the date of this announcement.

4.2 Details of the Proposed MGO

Upon completion of the Proposed Acquisition, Censof will hold 45.03% equity interest in TEB. In relation thereto, Censof will be obliged to extend the Proposed MGO to Non-Interested TEB Shareholders at a cash offer price of RM0.20 for every one (1) Offer Share upon the SSA being unconditional in accordance with Section 218(2) of the CMSA and Section 9(1), Part III of the Code. The Proposed MGO will be conditional upon Censof and persons acting-in-concert with it (“PACs”) having received, on or before the closing date of the Proposed MGO, valid acceptances (provided that such acceptances are not, where permitted, subsequently withdrawn) in respect of the Offer Shares, which would result in Censof and its PACs holding in aggregate more than fifty percent (50%) of the total voting shares of TEB (“Acceptance Condition”). For avoidance of doubt, the Acceptance Condition shall be computed based on Censof’s deemed equity interest of 45.03% under the SSA plus any valid acceptances received of more than 4.97% equity interest in TEB through the Proposed MGO. The Offer Shares to be acquired pursuant to acceptances under the Proposed MGO shall be transferred free from all moratoriums, claims, charges, liens, pledges, options, rights of pre-emption, third party rights and other security interests and/or encumbrances and/or equities whatsoever from the date of valid acceptance and with all the rights, benefits and entitlements attached thereto from the date of the document, outlining the terms and conditions of the Proposed MGO including the right to all dividends and/or distributions declared, made or paid on or after the date of the Notice, subject to adjustment to the consideration under the Proposed MGO in the event TEB declares, makes or pays any dividend and/or other distributions on or after the date of the Notice but prior to the close of the Proposed MGO and the holder of the Offer Shares is entitled to retain such dividend and/or distributions where the consideration for each Offer Share shall be reduced by the quantum of the net dividend and/or distribution per TEB Share which such Non-Interested TEB Shareholder is entitled to.

It is the intention of Censof to maintain the listing status of TEB subsequent to the Proposed MGO and not to privatise TEB. In the event that Censof receives acceptance resulting in the public shareholding spread of TEB not being in compliance with Paragraph 8.02(1) of the Listing Requirements of Bursa Securities (“Listing Requirements”) (“Non-Compliance with Public Shareholding Spread”), the Board will undertake to place out TEB Shares in order to rectify the Non-Compliance with Public Shareholding Spread. It should be noted that the number of TEB Shares to be placed out

Page 12 of 23

will increase in tandem with the quantum of acceptances received by Censof under the Proposed MGO.

4.3 Liabilities To Be Assumed

Save for the existing liabilities incurred in the ordinary course of business of TEB, there are no liabilities, including contingent liabilities and guarantees, to be assumed by Censof pursuant to the Proposals.

4.4 Additional Financial Commitment

There are no additional financial commitments by Censof in putting the assets/businesses of TEB Group on-stream as TEB Group already has on-going businesses.

4.5 Source Of Funding

The Proposals will be satisfied entirely via cash which will be funded by internally-generated funds and/or external borrowings, the composition of which would be determined by the Board later.

5. RATIONALE FOR THE PROPOSALS

5.1 Proposed Acquisition

Censof believes in growing its business organically as well as through acquisitions. In line with Censof’s plan to continuously expand its business, the Company has been actively looking into avenues to strengthen their revenue source as well as to provide more value added services to its customers. Since its listing, Censof has acquired two (2) companies, namely PT Praisindo Technology, a 60%-owned subsidiary of Censof, and KnowledgeCom Corporation Sdn Bhd, a 80%-owned subsidiary of Censof. The Proposed Acquisition presents a good and rare opportunity for Censof to not only expand its business but also to leverage on TEB’s resources and infrastructure to create strategic benefits, which Censof believes will bring both Censof Group and TEB Group the next level of performance.

The Proposals are expected to result in synergistic benefits to the enlarged Censof Group, including but not limited to the following:

(i) Levaraging on TEB’s assets

In 2012, Century Software (M) Sdn Bhd, a wholly-owned subsidiary of Censof (“CSM”) commenced a new business model of offering financial management software solutions (“FMSS”) under a leasing arrangement named software-as-a-service (“SaaS”) (as opposed to outright sale of the FMSS software). SaaS allows CSM’s customers to reduce their cost of operation and capital expenditure by allowing customers to lease its FMSS software without the initial burden of a huge capital expenditure to purchase the FMSS software. In return, CSM charges its clients according to pay-per usage model based on usage pattern of the FMSS software. On the other hand, TEB currently owns the IEC which is a Tier-3 Compliant data centre, Tier-4 Ready facility offering services which include amongst others, private cloud computing managed services and secured managed services, hardware, hosting, warehousing and cloud computing services.

Page 13 of 23

Moving forward, Censof would be able to capitalise on the existing infrastructure of the IEC by bundling the services offered by IEC with the existing products or services of Censof. This is important as the management of Censof, vide CSM, is planning to move its current customers to the SaaS business model which includes more than 70 federal statutory bodies and government agencies. The management of Censof believes that the SaaS business model would be well received by these federal statutory bodies and government agencies as they would not have to incur capital expenditure to maintain their computer network, thus providing cost-savings for these federal statutory bodies and government agencies in relation to the purchase and maintenance of computer/ network equipment. In that light, Censof believes that the Proposals would enable the enlarged Censof Group to garner a competitive edge over its competitors due to the availability of a combined infrastructure, hardware and software solutions and readily available customer base to cross sell their products and services.

(ii) Payment gateway and payment aggregation solutions

T-Melmax Sdn Bhd’s (“TMX”), a wholly-owned subsidiary of Censof, payment aggregation software, Max-Paygate and its payment portal Cpay offer electronic payments and collections solutions for business-to-business (“B2B”), business-to-government (“B2G”) and consumer-to-business (“C2B”) transactions. Dagang Net’s payment gateway Financial Services Payment Gateway (“FSPG”) offers electronic payments for B2G transactions vide strategic collaboration with Financial Processing Exchange (“FPX”) a national project which facilitates online payments for e-commerce transactions in particular B2B and B2C transactions on a secure and multi-bank platform. Upon the completion of the Proposed Acquisition, Censof would be able to complement the FSPG used by Dagang Net with TMX’s Max-Paygate or integrate/merge Censof’s Max-Paygate with the existing FSPG.

(iii) System integration business

CSM and TMX perform software system which includes the provision of systems implementation in the area of payment gateway system, implementation of FPX as well as data security and financial application customisation services. TSI specialises in the hardware system integration which includes the provision of project management, from design, installation to commissioning. In most system integration projects, software system integrators such as CSM and TMX as well as hardware system integrators such as TSI are required in a system implementation or integration that largely comprised of both hardware and software requirements. Upon the completion of the Proposed Acquisition, Censof would be able to assign the hardware system integration projects which are currently outsourced to third parties to TSI for execution.

5.2 Proposed MGO

The Proposed MGO is undertaken pursuant to an obligation under Section 218(2) of the CMSA and Section 9(1), Part III of the Code when the shareholding of Censof in TEB increases more than 33% arising from the Proposed Acquisition.

Notwithstanding the above, the Proposed MGO provides an opportunity for Censof to further increase its shareholding in TEB after the Proposed Acquisition.

Page 14 of 23

6. FINANCIAL EFFECTS ON CENSOF GROUP PURSUANT TO THE PROPOSALS

The Proposals will not have any effect on the issued and paid-up share capital and substantial shareholders’ shareholdings of our Group as the Proposals will be fully satisfied in cash. The proforma effects on gearing, earnings and EPS of our Group arising from the Proposals are illustrated below based on the following scenarios: Scenario I: (a) Assuming that the proposed private placement of up to ten percent (10%) of the issued

and paid-up share capital of Censof to third party investor(s) announced by Kenanga Investment Bank Berhad on 28 June 2013 (“Proposed Private Placement”) is undertaken on the minimum scenario basis whereby only 34,420,000 new ordinary shares of RM0.10 each in Censof (“Censof Shares”) will be issued pursuant to the Proposed Private Placement (none of the outstanding warrants are exercised); and

(b) On the assumption that the Proposed Acquisition is completed but the Proposed MGO

fails to garner the Acceptance Condition, resulting in Censof holding only 45.03% equity interest of TEB.

Scenario II: (a) Assuming that the Proposed Private Placement is undertaken on the maximum scenario

basis whereby 38,722,500 new Censof Shares will be issued pursuant to the Proposed Private Placement (and all outstanding warrants are exercised); and

(b) On the assumption that the Proposed Acquisition is completed and all the Non-Interested

TEB Shareholders accept the Proposed MGO, resulting in Censof holding 100.00% equity interest of TEB.

Page 15 of 23

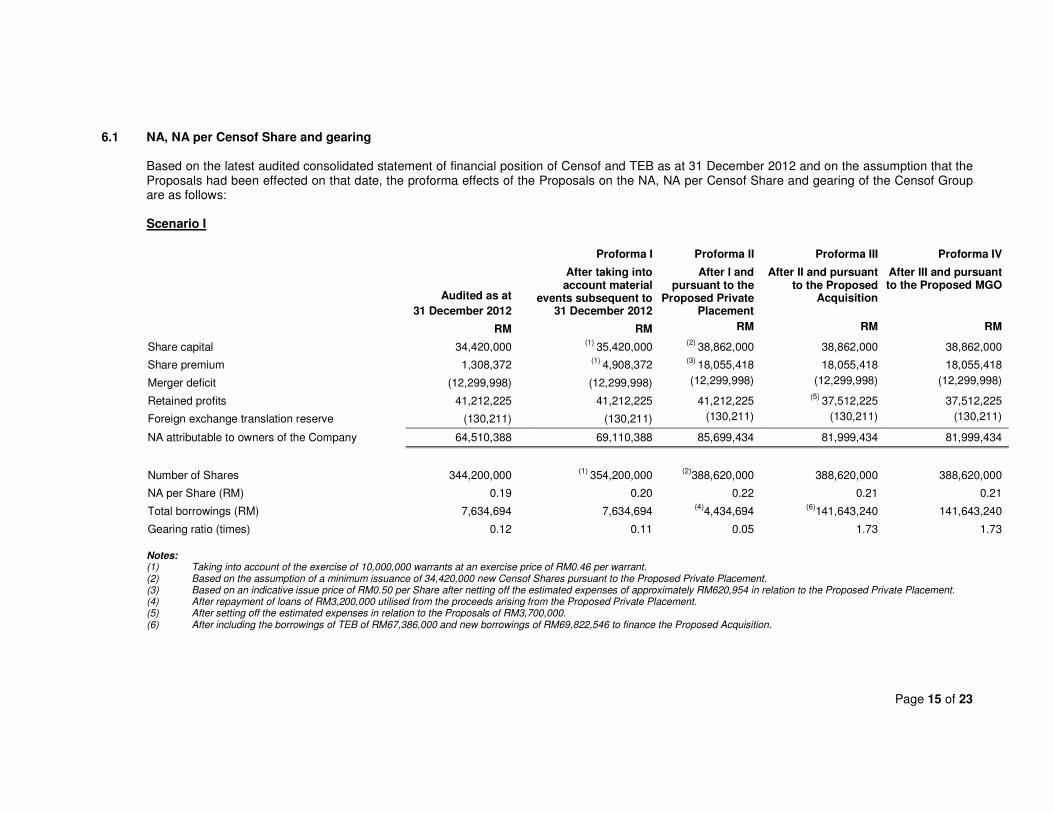

6.1 NA, NA per Censof Share and gearing

Based on the latest audited consolidated statement of financial position of Censof and TEB as at 31 December 2012 and on the assumption that the Proposals had been effected on that date, the proforma effects of the Proposals on the NA, NA per Censof Share and gearing of the Censof Group are as follows:

Scenario I

Proforma I Proforma II Proforma III Proforma IV

Audited as at

31 December 2012

After taking into account material

events subsequent to 31 December 2012

After I and pursuant to the

Proposed Private Placement

After II and pursuant to the Proposed

Acquisition

After III and pursuant to the Proposed MGO

RM RM RM RM RM

Share capital 34,420,000 (1)

35,420,000 (2)

38,862,000 38,862,000 38,862,000

Share premium 1,308,372 (1)

4,908,372 (3)

18,055,418 18,055,418 18,055,418

Merger deficit (12,299,998) (12,299,998) (12,299,998) (12,299,998) (12,299,998)

Retained profits 41,212,225 41,212,225 41,212,225 (5)

37,512,225 37,512,225

Foreign exchange translation reserve (130,211) (130,211) (130,211) (130,211) (130,211)

NA attributable to owners of the Company 64,510,388 69,110,388 85,699,434 81,999,434 81,999,434

Number of Shares 344,200,000 (1)

354,200,000 (2)

388,620,000 388,620,000 388,620,000

NA per Share (RM) 0.19 0.20 0.22 0.21 0.21

Total borrowings (RM) 7,634,694 7,634,694 (4)

4,434,694 (6)

141,643,240 141,643,240

Gearing ratio (times) 0.12 0.11 0.05 1.73 1.73

Notes:

(1) Taking into account of the exercise of 10,000,000 warrants at an exercise price of RM0.46 per warrant. (2) Based on the assumption of a minimum issuance of 34,420,000 new Censof Shares pursuant to the Proposed Private Placement. (3) Based on an indicative issue price of RM0.50 per Share after netting off the estimated expenses of approximately RM620,954 in relation to the Proposed Private Placement. (4) After repayment of loans of RM3,200,000 utilised from the proceeds arising from the Proposed Private Placement. (5) After setting off the estimated expenses in relation to the Proposals of RM3,700,000. (6) After including the borrowings of TEB of RM67,386,000 and new borrowings of RM69,822,546 to finance the Proposed Acquisition.

Page 16 of 23

Scenario II

Proforma I Proforma II Proforma III Proforma IV

Audited as at

31 December 2012

After taking into account material

events subsequent to 31 December 2012

After I and pursuant to the

Proposed Private Placement

After II and pursuant to the Proposed

Acquisition

After III and pursuant to the Proposed MGO

RM RM RM RM RM

Share capital 34,420,000 (1)

35,420,000 (2)

42,594,750 42,594,750 42,594,750

Share premium 1,308,372 (1)

4,908,372 (3)

31,665,418 31,665,418 31,665,418

Merger deficit (12,299,998) (12,299,998) (12,299,998) (12,299,998) (12,299,998)

Retained profits 41,212,225 41,212,225 41,212,225 (5)

37,512,225 37,512,225

Foreign exchange translation reserve (130,211) (130,211) (130,211) (130,211) (130,211)

NA attributable to owners of the Company 64,510,388 69,110,388 103,042,184 99,342,184 99,342,184

Number of Shares 344,200,000 (1)

354,200,000 (2)

425,947,500 425,947,500 425,947,500

NA per Share (RM) 0.19 0.20 0.24 0.23 0.23

Total borrowings (RM) 7,634,694 7,634,694 (4)

4,434,694 (6)

141,643,240 (7)

226,865,630

Gearing ratio (times) 0.12 0.11 0.04 1.43 2.28

Notes:

(1) Taking into account of the exercise of 10,000,000 warrants at an exercise price of RM0.46 per warrant. (2) Based on the assumption of a minimum issuance of 33,025,000 outstanding Warrants at an exercise price of RM0.46 per Warrant and maximum issuance of 38,722,500 new

Censof Shares pursuant to the Proposed Private Placement. (3) Based on an indicative issue price of RM0.50 per Share after netting off the estimated expenses of approximately RM620,954 in relation to the Proposed Private Placement. (4) After repayment of loans of RM3,200,000 utilised from the proceeds arising from the Proposed Private Placement. (5) After setting off the estimated expenses in relation to the Proposals of RM3,700,000. (6) After including the borrowings of TEB of RM67,386,000 and new borrowings of RM69,822,546 to finance the Proposed Acquisition. (7) After including the new borrowings of RM85,222,390 to finance the acquisition of the remaining 426,111,952 TEB Shares not owned by Censof pursuant to the Proposed MGO.

Page 17 of 23

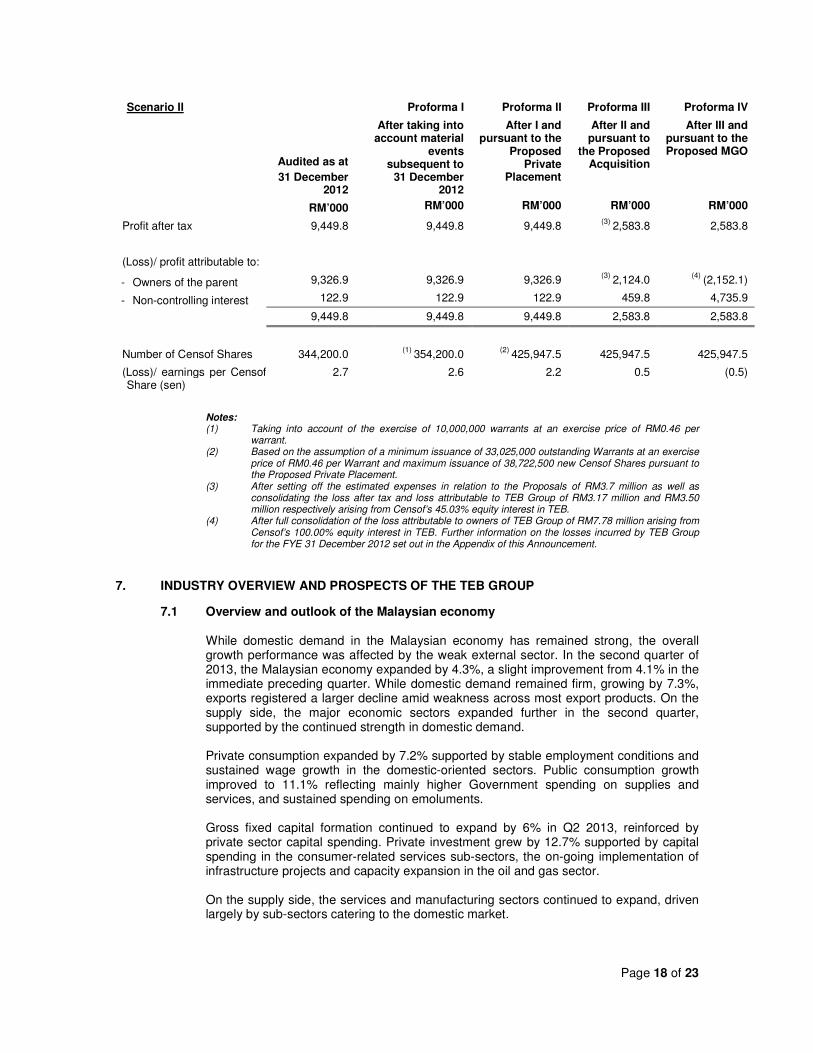

6.2 Earnings

The Board has noted that the TEB Group recorded a loss after tax (“LAT”) of approximately RM3.17 million for the FYE 31 December 2012. Notwithstanding the above, barring unforeseen circumstances and having considered the rationale and synergistic benefits for the Proposals as discussed in Section 5.1 of this announcement, the Board is of the opinion that the Proposals is expected to contribute positively to the earnings of the Censof Group in the future financial years.

The effects on earnings of Censof Group are illustrated as follows:

Scenario I Proforma I Proforma II Proforma III Proforma IV

Audited as at

31 December 2012

After taking into account material

events subsequent to

31 December 2012

After I and pursuant to the

Proposed Private

Placement

After II and pursuant to

the Proposed Acquisition

After III and pursuant to the Proposed MGO

RM’000 RM’000 RM’000 RM’000 RM’000

Profit after tax 9,449.8 9,449.8 9,449.8 (3)

2,583.8 2,583.8

(Loss)/ profit attributable to:

- Owners of the parent 9,326.9 9,326.9 9,326.9 (3)

2,124.0 2,124.0

- Non-controlling interest 122.9 122.9 122.9 459.8 459.8

9,449.8 9,449.8 9,449.8 2,583.8 2,583.8

Number of Censof Shares (‘000)

344,200.0 (1)

354,200.0 (2)

388,620.0 388,620.0 388,620.0

(Loss)/ earnings per Censof Share (sen)

2.7 2.6 2.4 0.5 0.5

Notes:

(1) Taking into account of the exercise of 10,000,000 warrants at an exercise price of RM0.46 per warrant.

(2) Based on the assumption of a minimum issuance of 34,420,000 new Censof Shares pursuant to the Proposed Private Placement.

(3) After setting off the estimated expenses in relation to the Proposals of RM3.7 million as well as consolidating the loss after tax and loss attributable to TEB Group of RM3.17 million and RM3.50 million respectively arising from Censof’s 45.03% equity interest in TEB. Further information on the losses incurred by TEB Group for the FYE 31 December 2012 set out in the Appendix of this Announcement.

Page 18 of 23

Scenario II Proforma I Proforma II Proforma III Proforma IV

Audited as at

31 December 2012

After taking into account material

events subsequent to

31 December 2012

After I and pursuant to the

Proposed Private

Placement

After II and pursuant to

the Proposed Acquisition

After III and pursuant to the Proposed MGO

RM’000 RM’000 RM’000 RM’000 RM’000

Profit after tax 9,449.8 9,449.8 9,449.8 (3)

2,583.8 2,583.8

(Loss)/ profit attributable to:

- Owners of the parent 9,326.9 9,326.9 9,326.9 (3)

2,124.0 (4)

(2,152.1)

- Non-controlling interest 122.9 122.9 122.9 459.8 4,735.9

9,449.8 9,449.8 9,449.8 2,583.8 2,583.8

Number of Censof Shares 344,200.0 (1)

354,200.0 (2)

425,947.5 425,947.5 425,947.5

(Loss)/ earnings per Censof Share (sen)

2.7 2.6 2.2 0.5 (0.5)

Notes:

(1) Taking into account of the exercise of 10,000,000 warrants at an exercise price of RM0.46 per warrant.

(2) Based on the assumption of a minimum issuance of 33,025,000 outstanding Warrants at an exercise price of RM0.46 per Warrant and maximum issuance of 38,722,500 new Censof Shares pursuant to the Proposed Private Placement.

(3) After setting off the estimated expenses in relation to the Proposals of RM3.7 million as well as consolidating the loss after tax and loss attributable to TEB Group of RM3.17 million and RM3.50 million respectively arising from Censof’s 45.03% equity interest in TEB.

(4) After full consolidation of the loss attributable to owners of TEB Group of RM7.78 million arising from Censof’s 100.00% equity interest in TEB. Further information on the losses incurred by TEB Group for the FYE 31 December 2012 set out in the Appendix of this Announcement.

7. INDUSTRY OVERVIEW AND PROSPECTS OF THE TEB GROUP

7.1 Overview and outlook of the Malaysian economy

While domestic demand in the Malaysian economy has remained strong, the overall growth performance was affected by the weak external sector. In the second quarter of 2013, the Malaysian economy expanded by 4.3%, a slight improvement from 4.1% in the immediate preceding quarter. While domestic demand remained firm, growing by 7.3%, exports registered a larger decline amid weakness across most export products. On the supply side, the major economic sectors expanded further in the second quarter, supported by the continued strength in domestic demand. Private consumption expanded by 7.2% supported by stable employment conditions and sustained wage growth in the domestic-oriented sectors. Public consumption growth improved to 11.1% reflecting mainly higher Government spending on supplies and services, and sustained spending on emoluments. Gross fixed capital formation continued to expand by 6% in Q2 2013, reinforced by private sector capital spending. Private investment grew by 12.7% supported by capital spending in the consumer-related services sub-sectors, the on-going implementation of infrastructure projects and capacity expansion in the oil and gas sector. On the supply side, the services and manufacturing sectors continued to expand, driven largely by sub-sectors catering to the domestic market.

Page 19 of 23

Going forward, the global economy continues to face downside risks, emanating from developments in several major economies. Policy uncertainties surrounding the quantitative easing (QE) programme in the US and European sovereign debt concerns are expected to weigh on market sentiment and growth prospects. While overall growth performance in most emerging economies, including in Asia, will be affected by these developments, domestic demand will continue to support the overall growth performance. For the Malaysian economy, the prolonged weakness in the external environment has affected the overall growth performance of the economy going forward. While domestic demand is expected to remain firm, supported by sustained private consumption, capital spending in the domestic-oriented industries and the ongoing implementation of infrastructure projects, the weak external sector in the first half of this year will affect our overall growth performance for the year. The overall growth of the economy for 2013 is now revised to 4.5 – 5.0%. Going forward, domestic demand is expected to remain on its steady growth trajectory and will continue to be supported by an accommodative monetary policy. (Source: Economic and Financial Developments in Malaysia in the Second Quarter of 2013, Bank Negara Malaysia)

7.2 Overview and outlook of the ICT industry in Malaysia The ICT sector will continue to be a key focus for Malaysia and is expected to gain greater momentum driven by the convergence of industries due to digitalisation. The contribution of the ICT industry to GDP is targeted to increase to 10.2% by 2015. Greater use of ICT will not only support the growth of the sector but also boost productivity and raise the nation's overall competitiveness. However, to achieve growth, Malaysia needs to shift from being an average producer of general ICT products and services to a niche producer of selected ICT products and services, and progress from a net importer to a net exporter. Issues of lack of product acceptability, weak product branding and lack of cross-discipline expertise will be addressed. (Source: 10

th Malaysia Plan 2011–2015, Economic Planning Unit, Prime Minister's Department)

Under the nation's programme, namely, Digital Malaysia, the government aims to create an ecosystem which promotes the pervasive use of digital technology in all aspects of the economy to connect communities globally and interact in real time resulting in increased economic activity, productivity and standard of living. While Malaysia has built a strong ICT foundation, Digital Malaysia will focus on driving value-added services through digital technologies. One of the key goals to be achieved under Digital Malaysia is to raise Malaysia's ICT contribution from 9.8% of GDP in 2010 to 17% by 2020. (Source: Ministry of Finance Malaysia (2012). Economic Report 2012/ 2013 – Chapter 3: Economic

Performance and Prospects)

Digital Malaysia is the nation’s programme to advance Malaysia towards a developed digital economy by 2020 by creating an ecosystem that promotes the pervasive use of ICT in all aspects of the society, government and economy resulting in increased Gross National Income, enhanced productivity and improved standards of living. Founded on three strategic thrusts of (i) moving from Supply to Demand focused; (ii) from Consumption to Production Centric; and (iii) from Low Knowledge-Add to High Knowledge-Add, the move from the programme aims to:

• improve ICT contribution to the nation’s gross national income (GNI) to RM294 billion or 17%, an increase from the current 9.8%;

• create 160,000 high value jobs and an additional RM7,000 digital income per annum for over 350,000 citizens by the year 2020.

Page 20 of 23

These eight projects which are the first wave of the Digital Malaysia programme are (i) Asian eFulfillment Hub, (ii) Enabling e-Payment Services for SMEs and Micro Enterprises, (iii) Shared Enterprise Services, (iv) Develop On-Demand Customised Online Education, (v) Micro-sourcing to Generate Income for the B40, (vi) Facilitating Societal Upliftment, (vii) Establish a Trusted Mobile Digital Wallet Platform and (viii) Growing the Embedded Systems Industry. (Source: Multimedia Development Corporation (MDeC))

7.3 Prospects of TEB Group

The TEB Group is divided into three (3) main segments, namely the NSW, the IEC and the hardware system integration. Dagang Net is the developer and operator of the NSW, a national initiative that provides a one-stop trade facilitation system linking federal statutory bodies and government agencies with trading communities. The NSW enables electronic exchange of data, submission of documents and transmission of messages for cargo clearance to support the country's international trade business. In addition, Dagang Net’s trade portal and its payment module FSPG offers electronic payments via strategic collaboration with FPX for B2G

transactions. The NSW currently has a user base which accounts to over 13,000 users and this user base is expected to increase in view of Malaysia’s total external trade reaching RM1.3 trillion in 2012 (Source: Malaysia external trade statistics, Department of Statistics

Malaysia). The IEC houses the security operation centre, network operation centre, call centre and data centre under one roof, offering integrated and comprehensive niche value-add solutions to TEB’s clients. Hardware system integration is implemented by TSI, whereby TSI would provide project management, from design, installation to commissioning. TSI’s system integration services encompass enterprise network, which includes WAN and LAN implementation, designing and deployment of wireless solutions, installation and maintenance of structured cabling system (SCS), retro-fitting existing networks or implementing new networks to meet latest standards and specifications. Upon completion of the Proposals, the enlarged Censof Group would be to utilize the current offerings of the TEB Group to perform the following: (i) to offer comprehensive FMSS under the SaaS business model by bundling FMSS

solutions together with the services offered by IEC; (ii) to complement the FSPG used by Dagang Net with TMX’s Max-Paygate or

integrate TMX’s Max-Paygate with the existing FSPG used by NSW;

(iii) the NSW currently has a user base which accounts to over 13,000 users which will provide an immediate additional distribution channel for Censof to market and sell FMSS solutions vide SaaS; and

(iv) to combine the expertise of CSM and TMX in performing software system integration with the expertise of TSI in hardware system integration, which CSM and TMX are currently outsourcing to third party hardware system integrators.

Page 21 of 23

8. RISK FACTORS

The Proposals are not expected to materially change the risk profile of our Group’s business given that the nature of product and services of the Censof Group and TEB Group are complementary, intersected and related to each other. The combined and enlarged group is expected to provide more comprehensive services and solutions in their ICT economic sub-sectors. However, there may be additional risks arising from the Proposals as set out below which are non-exhaustive. Whilst the Company seeks to limit the impact of such risks, there can be no assurance that these factors will not have a material adverse effect on the business and operations of TEB Group and/or our Group:

(i) Integration risk

The various synergistic benefits to be reaped from the Proposals will depend largely on the success of the integration process to be implemented by the enlarged Censof Group. The Proposals may potentially expose our Group to new risks including those associated with the assimilation of new operations and personnel, the diversion of financial management resources from existing operations and the inability to successfully integrate TEB Group with our current business. As such, there is no assurance that the anticipated benefits from the Proposals will be realised, and that our Group will be able to generate sufficient revenue to offset the associated costs from the Proposed Acquisitions.

(ii) Impairment of goodwill

The Proposals would result in goodwill arising from Proposals upon the consolidation of TEB into our Group. Under prevailing accounting standards, the Board and external auditors of Censof are required to assess the carrying value for possible impairment of goodwill. There is no assurance that impairment to the original carrying value of the goodwill arising from the Proposals would not arise, and the financial position of your Group may be adversely affect if an impairment is deemed necessary in the future.

(iii) Non-completion of the Proposed Acquisition

The completion of the Proposed Acquisition is subject to conditions that are beyond the Company’s control such as the Condition Precedents as disclosed in Section 4.1.2 (b) of this Announcement.

Accordingly, there can be no assurance that the Proposed Acquisition will be completed as contemplated. In the event any of the Conditions Precedent as set out in Section 4.1.2 (b) of this Announcement are not fulfilled by the Conditions Fulfilment Date and in the event an extension of time is not agreed upon between Censof and Khazanah, the SSA may be terminated in the manner as set out in Section 4.1.2(c) of this Announcement.

(iv) Non-compliance with the Public Shareholding Spread

Censof and its PACs may receive acceptances pursuant to the Proposed MGO resulting in the public shareholding spread of TEB falling below 25%, in which case TEB will become Non-Compliant with Public Shareholding Spread. As disclosed in Section 4.2 of this Announcement, it is the intention of Censof to maintain the listing status of TEB subsequent to the Proposals. Consequently, the Board of Censof will endeavour to to place out sufficient number of TEB Shares or procure TEB to carry out a subsequent corporate exercise in order to rectify the Non-Compliance with Public Shareholding Spread. Amongst the possible measures that may be undertaken by Censof include, but not limited to, implementing an employee share scheme and placing out TEB Shares received vide the Proposed MGO to third-party investors. It should be noted that the quantum of TEB Shares to be place out may increase in tandem with the quantum of valid acceptances received by Censof under the Proposed MGO.

Page 22 of 23

However, there is no assurance that the TEB Shares will be successfully placed out or the Non-Compliance with Public Shareholding Spread will be successfully rectified. In the event that Censof is unable to rectify the Non-Compliance with Public Shareholding Spread, TEB may be delisted from the Official List of Bursa Securities and the TEB Shares held by our Group will end up being illiquid and not tradable on Bursa Securities.

9. ESTIMATED TIMEFRAME FOR COMPLETION

The tentative timeline in relation to the Proposals is as follow:

Tentative timeline Proposed events

End September 2013 Submission of the draft circular to shareholders of Censof to Bursa Securities for its approval

Middle October 2013 Despatch of the circular to shareholders in relation to the Proposals

Middle October 2013

SSA becomes unconditional and serving of the notice of take-over offer pursuant to the Proposed MGO

End October 2013 Extraordinary general meeting (“EGM”) to be convened in relation to the Proposals

End November 2013 Completion of the Proposals

We note the SSA provides for a timeline of two (2) months for Censof to fulfill the Conditions Precedent. As the Proposed Acquisition would be deemed a very substantial transaction pursuant to Paragraph 10.02(n) of the Listing Requirements where additional disclosures are required pursuant to Paragraph 10.10 of the Listing Requirements, the two (2) months period to obtain the shareholders’ approval would be insufficient for Censof to comply with Paragraph 8.29(1) of the Listing Requirements. On 9 September 2013, RHBIB, on behalf of Censof, had submitted an application to Bursa Securities seeking its approval for a waiver from complying with Paragraph 8.29(1) of the Listing Requirements. The approval from the said application is still pending. Nevertheless, Censof had, on 9 September 2013 secured the irrevocable and unconditional undertaking from its controlling shareholder, SaaS Global Sdn Bhd which currently holds 55.03% equity interest in Censof, to vote in favour of the ordinary resolutions pertaining to the Proposals at the EGM to be convened. Consequently, Censof shall on a later date, convene an EGM for purposes of ratifying the ordinary resolutions pertaining to the Proposals to comply with Paragraph 10.07 of the Listing Requirements. Barring any unforeseen circumstances, the Proposals are expected to be completed by the fourth quarter of calendar year 2013.

10. APPROVALS REQUIRED

The Proposals are subject to the following approvals: (a) Bursa Securities in respect of the waiver to comply with Paragraph 8.29(1) of the Listing

Requirements of Bursa Securities; (b) Securities Commission Malaysia in respect of the issuance of the offer document and

independent advice circular in relation to the Proposed MGO; and (c) Any other relevant authorities or parties, if required. The Proposals are inter-conditional upon each other. The Proposals are not conditional upon any other corporate exercise undertaken or to be undertaken by Censof.

Page 23 of 23

11. HIGHEST PERCENTAGE RATIO

The highest percentage ratio applicable to the Proposals pursuant to Paragraph 10.02(g) of the Main Market Listing Requirements of Bursa Securities is 294.37%.

12. INTERESTS OF DIRECTORS, MAJOR SHAREHOLDERS AND/OR PERSONS CONNECTED

None of the Directors, major shareholders of Censof and/or persons connected with them has any interest, direct or indirect, in the Proposals.

13. DIRECTORS’ STATEMENT The Board, after having considered all aspects of the Proposals, including the rationale and financial effects of the Proposals as well as the prospects of TEB as set out in Sections 5, 6 and 7 of this Announcement, are of the opinion that the Proposals are fair and reasonable and are in the best interest of the Company and its shareholders. Accordingly, the Board recommends that you vote in favour of the ordinary resolutions pertaining to the Proposals to be tabled at the forthcoming EGM to be convened.

14. ADVISERS

RHBIB has been appointed as the Principal Adviser to the Company for the Proposals.

15. DOCUMENT AVAILABLE FOR INSPECTION

The SSA is available for inspection at the registered office of the Company at Level 15-2, Bangunan Faber Imperial Court, Jalan Sultan Ismail, 50250 Kuala Lumpur during normal business hours from Mondays to Fridays (except public holidays) for a period of three (3) months from the date of this Announcement.

This Announcement is dated 12 September 2013.