1 A MULTIPERIOD FIRM MODEL by Ralf Östermark. 2 Firm plan model – Key elements Input: Decision...

27

1 A MULTIPERIOD FIRM MODEL by Ralf Östermark

-

Upload

ross-christon -

Category

Documents

-

view

213 -

download

0

Transcript of 1 A MULTIPERIOD FIRM MODEL by Ralf Östermark. 2 Firm plan model – Key elements Input: Decision...

1

A MULTIPERIOD FIRM MODEL

by Ralf Östermark

2

Firm plan model – Key elements

Input: Decision variables Sales volume Production volume New debt etc.

Input: Given parameters Sales price/unit Production cost/unit Amortization ratio etc.

Input: Logical restrictions Inventory ≥ 0 Fixed assets ≥ 0 Debt ≥ 0 etc.

Computations/Output: Multi-period financial statements Balance sheet Statement of income Some elements of Cash flow statement

Output: Firm valuation:Sum of discounted future Net Income

Input: Historical accounts Balance sheet

3

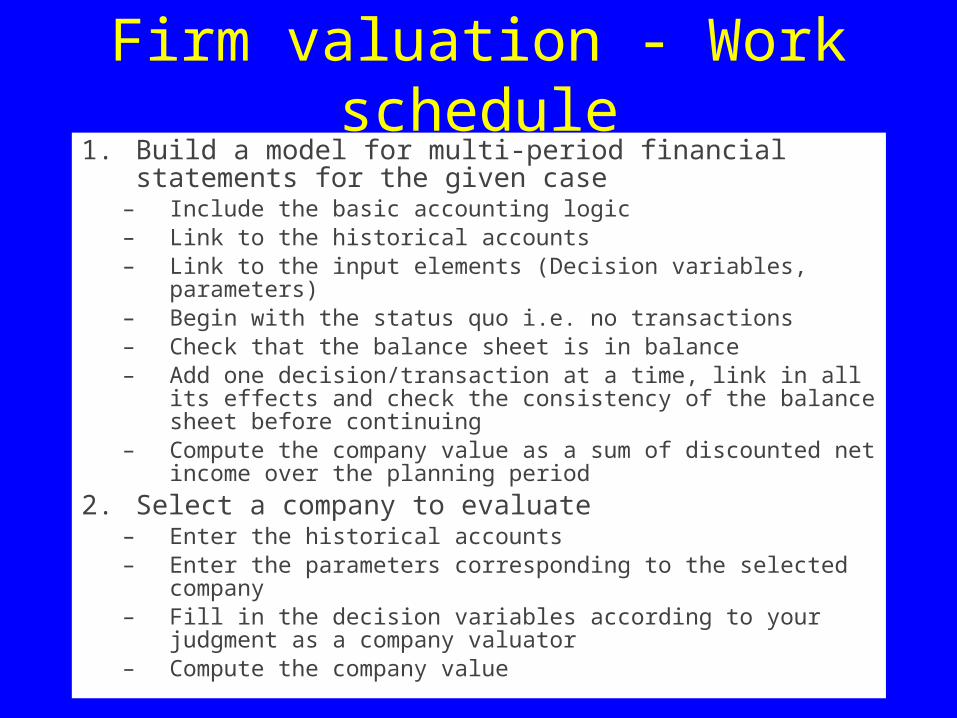

Firm valuation - Work schedule1. Build a model for multi-period financial statements for

the given case– Include the basic accounting logic– Link to the historical accounts– Link to the input elements (Decision variables, parameters)– Begin with the status quo i.e. no transactions– Check that the balance sheet is in balance– Add one decision/transaction at a time, link in all its effects and

check the consistency of the balance sheet before continuing– Compute the company value as a sum of discounted net income

over the planning period

2. Select a company to evaluate– Enter the historical accounts– Enter the parameters corresponding to the selected company– Fill in the decision variables according to your judgment as a

company valuator– Compute the company value

4

Large Scale Techno-Economic Firm Planning

Key elements

Optimal Firm Planning

Dynamic Firm Models(Monetary Process)

Real ProcessForecastingNeural Nets

Nonlinear Models

OptimizationFuzzy Sets

Genetic Algorithms

ComputationPC-applications (interface)

High Performance CPU (CSC)

Parallel Processing (1) MIMD / SUPER machines (2) Joint research CSC - support:

5

Key Features:

• The necessary financial relations included

• Free specification of planning horizon

• Simulation and optimization combined

• Guaranteed feasibility

• A flexible optimization module written as a dynamic link libary (DLL) in strict ANSI C.

6

Problem formulation:

MAXx c x A x b

x c b A

ttT

t t t t

t tn

tm

tmn

, ,

7

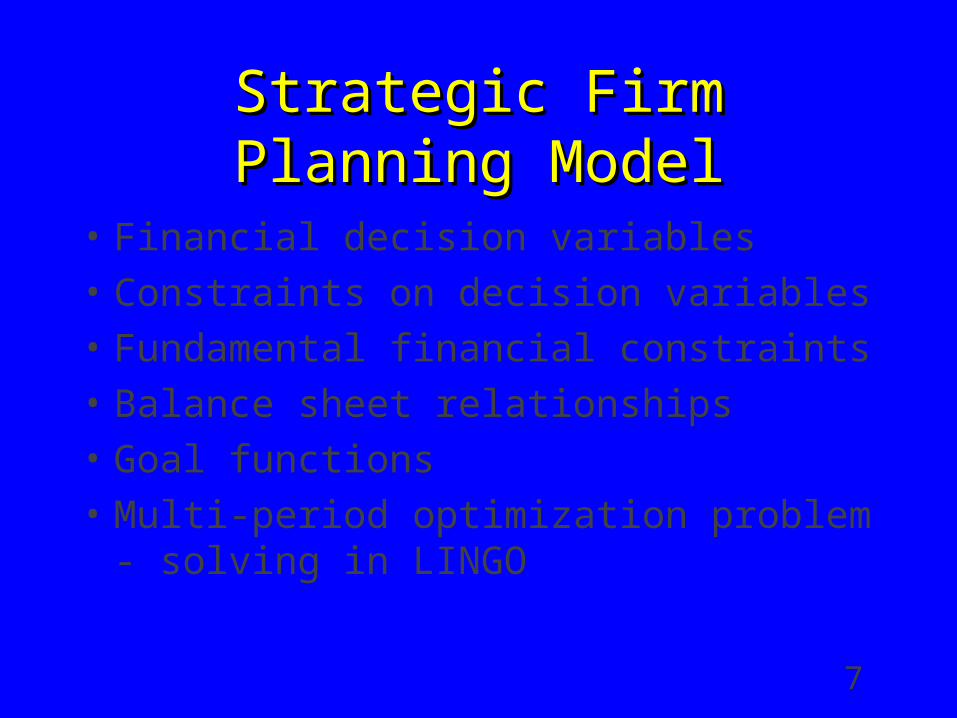

Strategic Firm Planning ModelStrategic Firm Planning Model

• Financial decision variables

• Constraints on decision variables

• Fundamental financial constraints

• Balance sheet relationships

• Goal functions

• Multi-period optimization problem - solving in LINGO

8

Decision variables

• Sales volume (SALEVOL)

• Production volume (PRODVOL)

• New debt (NEWDEBT)

• Repayment (REPAY)

• Investments (INV)

• New issues (NEWISSUE)

• Dividends (DIV)

• Depreciation (DEP)

9

Deviation variables

• Min dividend deviation (DIVDIFF)

• Max dividend deviation (MAXDIVDIFF)

• Equity deviation (EQUITYDIFF)

• Debt/Equity deviation (DEDIFF)

• Repayment deviation (REPDIFF)

10

FinancialFinancial statementstatement

• Fixed assets

• Value items

• Inventory

• Sales receivable

• Cash

• Other financial items

• Shareholders´equity

• Other restricted equity

• Net income of the year

• Other unrestricted equity

• Value items

• Accumulated depreciation difference

• Reservations

• Current liabilities

• Long-term debt

11

Statement of incomeStatement of income+ Turnover- Operating costs - Changes in inventory- Depreciation- Interest expenses+ Other financial income+ Extraordinary income and expenses+ Allocations- Taxes= Net income

12

Constraints on decision variablesConstraints on decision variablesConstraints on decision variablesConstraints on decision variables

1. Turnover - upper bound = f(production capacity)

TurnO Capacity TurnO FIXASSETFactor P prog

Machineprice progt t tt

* _

_

FIXED ASSETS

Factor * FIXASSETS

13

Factor * FIXASSETS

UNIT

PRICESALES

UNITCOSTMACHINE

FIXASSETSFactor

VOLUMEPRODUCTIONOFVALUESALES

capacityoductionUNIT

COSTMACHINECOSTPURCHASEMACHINE

*

Pr*

1. Turnover - upper bound (cont.)

14

Constraints on decision variablesConstraints on decision variables

2. Repayment level

MINIMIZE

h

1h

1tt

h

1tt0hhh REPAYDIFFREPAYNEWDEBTDEBTrepREPAYDEBT*repREPAY

15

Constraints on decision variablesConstraints on decision variablesConstraints on decision variablesConstraints on decision variables

3. New issues - upper bound

MINIMIZE

tt EQUITYDIFFEQUITYnNEWISSUE 0*

16

Constraints on decision variablesConstraints on decision variables

4. Dividends

MINIMIZE

h

h

tt

h

tth

hh

MAXDIVDIFFDIVNETINCOMET.EQUITYFREE.UNRESDIV

TR.EQUITYFREE.UNRESDIVUpperbound

1

110

h

h

tth

hh

MINDIVDIFFNEWISSUEEQUITYdivDIV

div*EQUITYDIV:Lowerbound

10

17

Constraints on decision variablesConstraints on decision variables

5. Depreciation - lower bound

h

t

h

ttt

hhh

DEPINVFIXASSETdep

DEPFIXASSETdepDEP

1

1

10

*

18

Fundamental Financial Fundamental Financial Constraints Constraints

Fundamental Financial Fundamental Financial Constraints Constraints

1. Cash - nonnegative

Cash flow:+ Turnover - Change in sales revenues- Costs - Change in other financial assets- Interest expenses + Change in current liabilities+ Other financial income + New debt+ Extraordinary income - Repayment- Dividends - Investments

h

tth CashCashCash

00 00

19

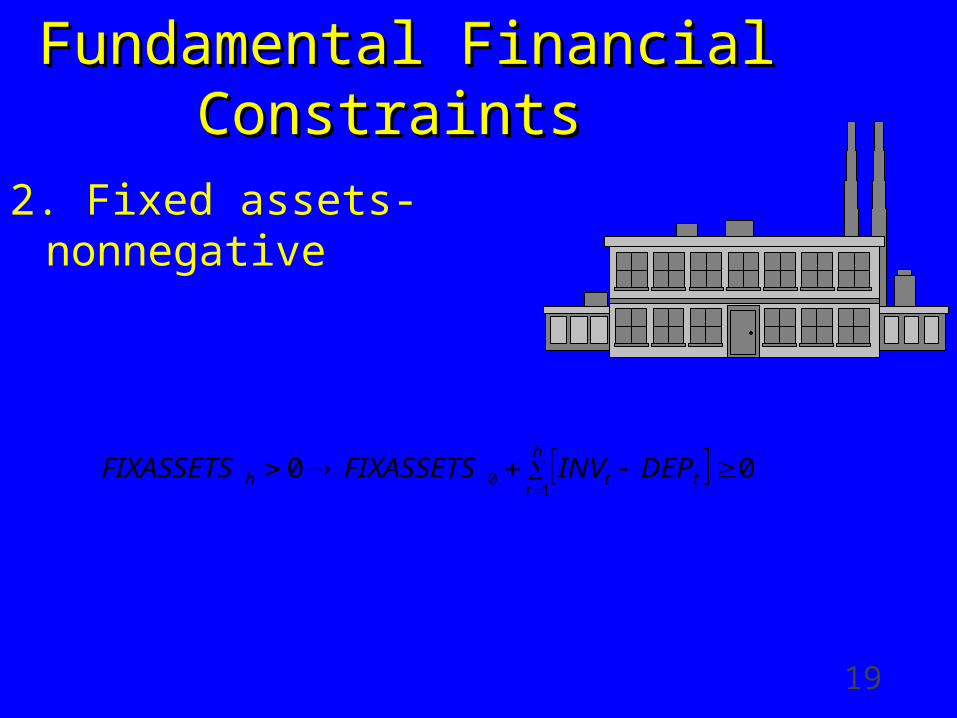

Fundamental Financial Fundamental Financial Constraints Constraints

Fundamental Financial Fundamental Financial Constraints Constraints

2. Fixed assets- nonnegative

001

0

h

ttth DEPINVFIXASSETSFIXASSETS

20

Fundamental Financial Fundamental Financial Constraints Constraints

Fundamental Financial Fundamental Financial Constraints Constraints

3. Long-term debt- nonnegative

001

0

h

ttth REPAYNEWDEBTDEBTDEBT

21

Fundamental Financial Fundamental Financial Constraints Constraints

Fundamental Financial Fundamental Financial Constraints Constraints

4. Capital structure

MINIMIZE

hh

h

tttt

hh

DEDIFFLIABdeDIVNETINCOMENEWISSUE

EQUITYLIABdeEQUITY

*

*

1

0

22

Financial relationships

Costs: c * TurnOInterests: i * DEBTOt. fin. costs. o *

OTH.FIN.ASS.Sales receivable s * TurnOCurrent liabilities cl * Costs

23

Alternative Objective functions Alternative Objective functions Alternative Objective functions Alternative Objective functions

- Optimize discounted dividend

- Optimize discounted net income

Max w

DIV

rDIFFt

tt

h

1

1

Max w

NETINCOME

rDIFFt

tt

h

1

1

24

Example: optimization in LINGOThe optimization module of the firm planning system is written as a dynamic link

library (DLL) in strict ANSI C by the author. However, in smaller optimization formulations like the one in analys.xls, the optimization can be carried out by Excel. We illustrate the solution process by a small system written for LINGO:

13] ! Objectivefunction 3 ;14] MAX = +.8696*Div(1)-10000.*MinDivdiff(1)-10000.*EQUITYdiff(1)-10000.*DEdiff(1)15] -10000.*REPdiffm(1)-30000.*MAXdivdf(1);16] !AMATRIX * X < b-vector;17] !Cash;18] +3.135*Oms(1)+.91*Nylan(1)-.91*Amort(1)-1.*Inv(1)19] +1.*Emiss(1)-1.*Div(1)+.1*Avskr(1)>3137.551;20] !Turnover;21] +1.*Oms(1)-.5*Inv(1)+.5*Avskr(1)<2950.4;22] !Fixed assets;23] +1.*Inv(1)-1.*Avskr(1)>-5900.8;24] !Long-term debt;25] +1.*Nylan(1)-1.*Amort(1)>-2353.9;26] !Minimal depreciation;27] -.03*Inv(1)+1.*Avskr(1)>177.024;28] !Debt-Equity ratio;

25

29] -2.375*Oms(1)-1.09*Nylan(1)+1.09*Amort(1)+1.*Emiss(1)30] -1.*Div(1)-.9*Avskr(1)+1.*DEdiff(1)>-3012.849;31] !New Issues;32] +1.*Emiss(1)-1.*EQUITYdiff(1)<111.572;33] !Minimal Dividend;34] -.01*Emiss(1)+1.*Div(1)+1.*MinDivdiff(1)>13.777;35] !Maximal Dividend;36] -.45*Oms(1)+.09*Nylan(1)-.09*Amort(1)+1.*Div(1)37] +.9*Avskr(1)-1.*MAXdivdf(1)<1450.449;38] !Minimal Debt Repayments;39] -.15*Nylan(1)+1.*Amort(1)+1.*REPdiffm(1)=353.085;

26

Related ResearchRelated ResearchRelated ResearchRelated Research

Östermark R: "Pitkän tähtäyksen strateginen tilinpäätössunnittelumalli" (A long term strategic planning model). Presented at European IFPS User's Group Meeting, Amsterdam 1983. In: European IFPS User's Group Proceedings, 11, 1983, 14 p.

Östermark, R. and E. Kasanen: "A graphical decision support system for multi-objective financial modeling", Turku School of Economics, 1985. Presented at the EURO VII Conference in Lisbon, Portugal 09/1986.

Östermark, R.: "A graphical DSS for conflict zone analysis of commercial bank environment", In: DSS Transactions 1987, 15 p. Presented at the DSS-87 Conference in San Fransisco, California.

Östermark, R.: "Optimal compromising within a multi-criterial conflict zone", European Journal of Operational Research 35, 1988, pp. 255-262.

Östermark, R. and K. Söderlund: "A multi-period firm model for strategic decision support", Kybernetes 28:5, 1999, pp. 538-556.

Östermark, R., H. Skrifvars, and T. Westerlund: "A nonlinear mixed integer multi-period firm model", International Journal of Production Economics 67, 2000, pp. 183-199.

27

Related Research…Related Research…Related Research…Related Research…

Booth, Bessler, Foote.”Managing interest-rate risk in banking institutions” European Journal of Operational Research 41(1989) 302-313.

Reid, Bradford.”A Farm Firm Model of Machinery Investment Decisions” American Journal of Agricultural Economics (1987) 64-77.

Bessler, Booth. “An interest rate risk management model for commercial banks” European Journal of Operational Research 74 (1994) 243-256

Korhonen’s Bank Model [EJOR, around 1989]

The derivative firm model (Choi et al, Man. and Decision Economics [1993])