1. 2 CABA Overview About CABA: CABA is the authoritative knowledge-based forum advancing the...

39

1

-

Upload

homer-kennedy -

Category

Documents

-

view

224 -

download

1

Transcript of 1. 2 CABA Overview About CABA: CABA is the authoritative knowledge-based forum advancing the...

1

2

CABA Overview

• About CABA: CABA is the authoritative knowledge-based forum

advancing the application and integration of automation in the residential and commercial building industry.

• Definition of Intelligent Building Technologies: The use of integrated technological building systems,

communications and controls to create a building and its infrastructure which provides the owner, operator and occupant with an environment which is flexible, effective, comfortable and secure.

3

CABA and the following CABA members funded this project

Ruby Sponsors

Emerald Sponsors

Diamond Sponsors

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

4

Background and ObjectivesLife Cycle Costing of Intelligent Buildings (LCCIB)

LCCIB Project – The objectives for undertaking this project should help to address the following:

• Challenges associated with LCC.

• Evaluate current LCC methodology.

• Evaluate LCC alternatives.

• Investigate the adequacy of training and education efforts.

• Explore collaboration efforts to bring LCC to the mainstream.

• Evaluate the development and incorporation of LCC with regard to technology changes.

• Match objectives in the development of the ideal intelligent building focused LCC tool.

• Lay out work streams for effective industry changes.

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

5

Frost & Sullivan’s Methodology

Frost & Sullivan’s approach and methodology combined primary and secondary research. The primary research sample categorization included the following:

Frost & Sullivan also undertook a targeted user research through a controlled 150 sample survey conducted among building owners and asset managers to evaluate their views on intelligent buildings, technology adoption, decision making factors and perceptions towards LCC.

Source: Frost & Sullivan, 2013

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

6

Key Takeaways

The key takeaways of this research are the following:

• Capital investment must be justified.

• LCC is used only sporadically.

• Simple payback is often used.

• LCC methodology is inconsistent.

• Tools are typically complex.

• Fragmented delivery chain.

• NIST model is the leader.

• A collaborative approach is necessary.

• Education and training are predominantly ad hoc.

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

7

Intelligent Buildings and Life Cycle Costing

Building Profile

System Integration Specialist

Integration Determinants Limiting Factors

Non-integrated

• Overtly dependent on contractors

• Availability• Low cost• Relationships• No open standards• Difficult to accomplish

system integration

• Long-term maintenance contracts of manufacturers

• Engineering by design not adopted as a norm

• Costly upgrade contracts

Partially integrated

• Dependency on contractors and system integrators

• Advocacy of open standards to some degree

• Cost still overrides decisions• Benefits of integration not

fully exploited

• Hardware intensive with multiple communication interfaces/gateways makes switch to full integration cumbersome

• Proprietary strongholds persist

Fully integrated

• Collaborative approach and accountability shared by multiple stakeholders with the building owner at the center of decision making

• Specs dictated by compatibility and interoperability

• Demonstrates lowest life cycle cost

• Variances in cost estimation• Perception issues with

regards to cost and time consumed

• Lack of skilled professionals

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

8

Key Inducement Factors to Move to LCC

•Initial costs comprise only a fraction of actual capital outlay a building owner/project manager has to provision for.•These costs are incapable of reflecting recurring and timeline oriented costs that get attached to a project’s life cycle.•LCC provides visibility into total cost of ownership over a 20 or 30 year life span.

Present costs do not equal future costs

Simple payback does not reflect full

value

•Beyond initial costs, LCC takes into consideration potential future costs that will ultimately be added to the total ownership costs for the building owner/project manager.•LCC converts all future costs into present value by discounting those in present value terms.•This allows for apples-to-apples comparison of costs over 20 or 30 years, irrespective of when they may get added to the life cycle of the project.

•Simple payback only offers a cursory glance to preliminary savings that could accrue in the early years of a project.•Initial costs and expected annual savings do not reflect variances in expected equipment lifetime.•Additionally, maintenance cost differences, periodic rebates and incentives, as well as other operational savings that could accrue beyond initial years has an impact on total cost of ownership.

Initial cost can be

misleading

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

9

LCC Usage Trends

Industry StakeholderUsage Statistic

(Approximately %)*Trend

Building Owners/Developers/Project Managers

38%Sporadic Users

Neutral-to-increasing

Consultants 68%Heavy Users

Increasing

Contractors and Integrators 12%Negligent Users

Neutral

OEMs 40%Moderate Users

Increasing

Push Factors• There is a growing emphasis on proving business case.• Funding approvals increasingly requires a solid pre-project evaluation.• Thrust to evaluate cost-benefit analysis over an extended project life

span is advocated by some building owners.

Source: Frost & Sullivan, 2013* Percentage of total interviewed

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

10

Key Challenges

Segment Key Challenges Usage Characteristics

Building Owners/ Asset Managers

Reliance on consultants provide early acquaintance with LCC

CFOs and fund approvers emphasize more on individual financial metrics

Understanding LCC techniques is a hurdle Perceived extra costs

Have interest in adopting LCC

Customized tools preferred

Consultants and Suppliers

More attuned to using LCC Relatively little clarity on intelligent technology Meeting minimum project requirements is key More likely to use LCC where maximum risk with

performance guarantees are associated in projects

Tendency to use more in-house developed tools

Provide it for a fee, unless part of major contracts

Contractors/ Integrators

Little inclination towards offering project or technology evaluation

No incentive to keep up with the influx of intelligent technology

Mostly work to deliver to specifications Meeting minimum requirement is the sole criteria

Not open to spending on education and training

Some familiarity with LCC in integrated design delivery approach

Industry-led initiatives are necessary to bring them under compliance

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

11

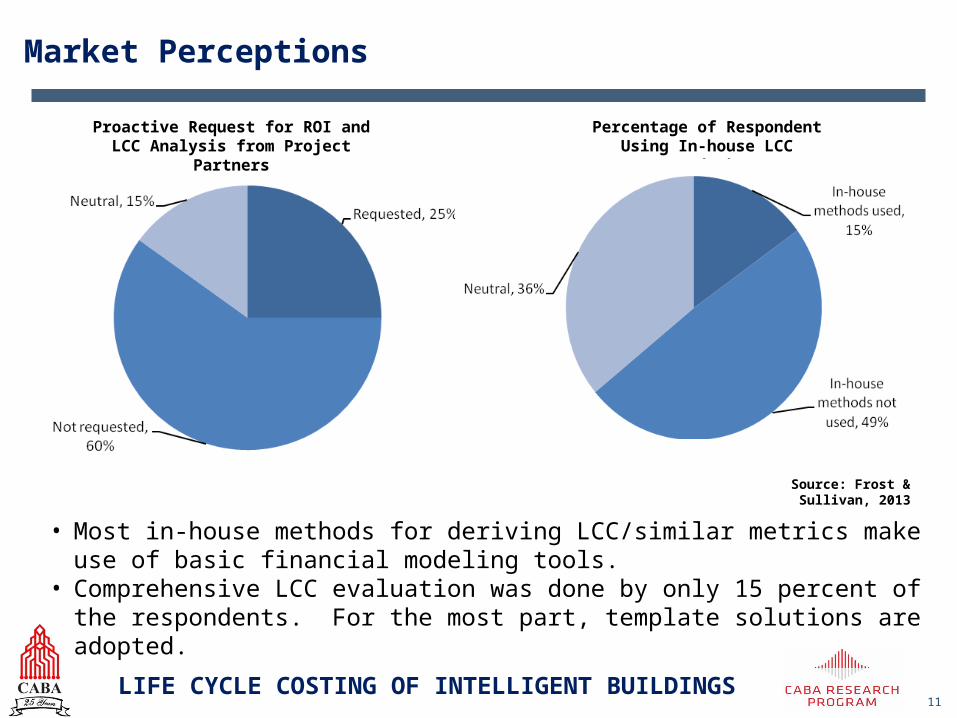

Market Perceptions

Proactive Request for ROI and LCC Analysis from Project Partners

Percentage of Respondent Using In-house LCC Methods

Source: Frost & Sullivan, 2013

• Most in-house methods for deriving LCC/similar metrics make use of basic financial modeling tools.

• Comprehensive LCC evaluation was done by only 15 percent of the respondents. For the most part, template solutions are adopted.

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

12

Mandating and Incentivizing LCC - Feasibility

Elements for Achieving a Mandate for LCC

Feasibility Timeframe* and Steps Needed

Codification of LCC analysis as a norm by standard bodies (eg., ANSI, ASHRAE, others)

Medium-HighMake provisions in building and product specification codes; Long term

Mandating LCC as a prerequisite to obtain institutional project funding

MediumLobby with financial bodies to advocate the importance of LCC over other financial metrics; Mid term

Changing building owner’s perceptions

Medium-HighExtensively use education, training and other interactive processes; Short term

Redefining utility-led incentives and rebates

Medium-High

Lobby with utility commissions and regulators to improvise incentives and rebates supporting LCC; Mid-to-long term

Certification processes including LCC modules for tradespeople

Low-MediumPromote sponsorships from technology vendors for such certification/training processes; Short term

* Short term–2-3 years; Mid term–5-7 years; Long term–10 years or more

Source: Frost & Sullivan, 2013

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

13

Process Optimization

The following aspects need to be incorporated in the project delivery process:

• Supply Chain Collaboration – Collaborate throughout the design, construction, and

commissioning process; leverage building information modeling (BIM).

• Integrated Design and Delivery Approach – Move away from disjointed and

transactional approach; consortium approaches will lead to accountability and could help

enforce LCC adoption.

• Opt For Objective Evaluation Criteria – Competitive bids will continue in the industry.

An objective evaluation criterion is required, backed by lowest total cost of ownership.

• Avoid Cost Thresholds - Allow for the inclusion of more vendors and suppliers into the

selection process.

• Mandate a Feedback Loop - Can offer valuable insights into technology performance,

cost-benefit evaluation, and establish their importance in intelligent building projects.

• Educational and Training Efforts - Seeking out partnerships among industry stakeholder

groups and promoting training and sponsorship efforts to help achieve LCC adoption is

important.

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

14

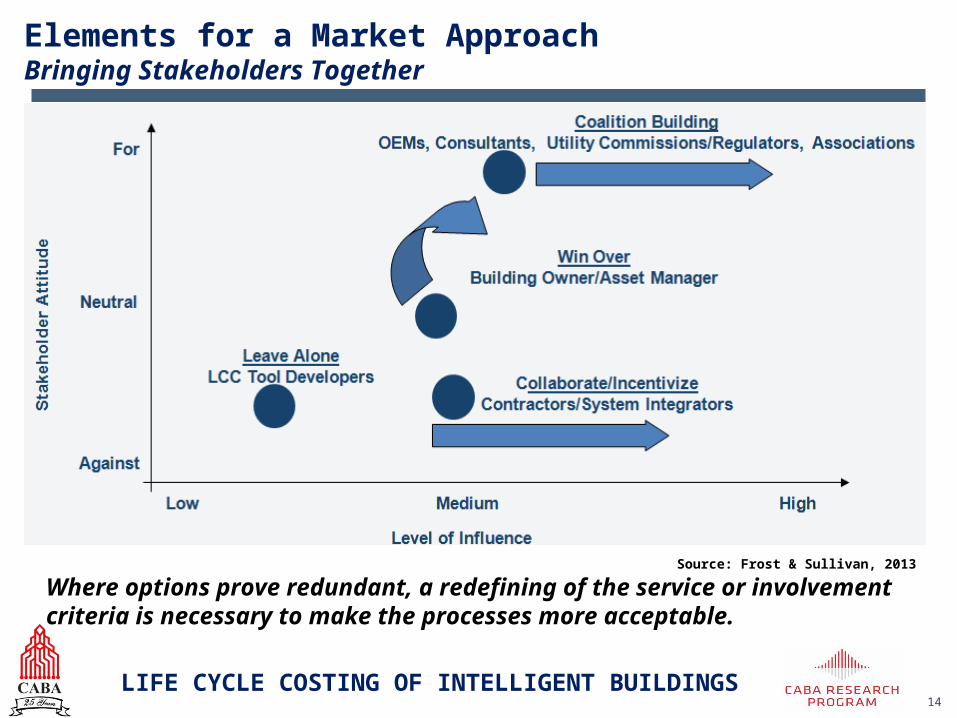

Elements for a Market Approach Bringing Stakeholders Together

Where options prove redundant, a redefining of the service or involvement criteria is necessary to make the processes more acceptable.

Source: Frost & Sullivan, 2013

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

15

Project Cases

Project/Arranger Details

Western Kentucky University,KentuckyArranged by Johnson Controls, Inc. and Western Kentucky University

Showcase of Energy Information System: Panoptix® platform that includes applications for utility tracking and reporting; fault detection and diagnostics; equipment performance analytics; and measurement and verification; and a public-facing energy information kiosk.

Adobe Systems Incorporated,West Tower 12 Smart Floor,CaliforniaArranged by WattStopper and IBS, Inc.

Showcase of digital lighting management solution by WattStopper and IBIS-centralized software interface responsible for integrated sequences of operation, optimizing control strategies, and reducing energy consumption.

Virginia Tech Campus,Blacksburg, VirginiaArranged by Siemens Industry, Inc.

Showcase of the development of an operations control center, centralizing the coordination and management of the campus HVAC infrastructure, improvement in operations efficiency and responsiveness, and effective management of BAS data to improve decision making.

Microsoft Corporation Headquarters, Redmond, Washington Arranged by Microsoft Corporation

Showcase of intelligent building system overlay, automating RCx program, optimizing campus portfolio (35,000 assets), improving labor efficiencies, and automating building performance reporting.

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

16

Recommendations

Source: Frost & Sullivan, 2013

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

17

Activity Areas

Source: Frost & Sullivan, 2013

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

18

Create a Focused Working Group/Task

Force

Process Step

Activity

Support

Create Foundation

• LCC format standardization

• Data reconciliation• Evaluation of best

practices

• Work with utilities and their public utility commissions/regulators

• Influence building rating tools/standards

Lobbying Efforts Educational/ Awareness Efforts Coalition Building

• Leverage IIBC membership and other CABA working groups to create participation format

• Assign end goals

Achieve Immediate Thrust

Create Knowledge Base

Foster Partnerships

Result

Recommended Action Items

• Help create proper certifications

• Integrate LCC techniques

• Collaborate at industry association level

• Redefine credits and incentives towards long term goals

• Institutionalize practices

• Integrate delivery approaches towards projects

LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

19

LCC and Solutions Business

•Lighting is undergoing a paradigm shift towards solutions due

the advent of inherently digitally controllable LEDs

•Systems, Solutions and Services related innovations

increasingly rely on Life Cycle Cost for assessing value of

different propositions.

•Large institutional customers such as federal Govt. (e.g.

DOD) are requiring LCC methodologies for decision making: The purpose of Life-Cycle Costing (LCC) is to help select the best energy and water

projects.

Properly implemented, LCC will help an energy manager meet or exceed energy goals

with the lowest possible investment.

20

Monetization of the Connected Home2013 Project Overview

21

Project Introduction

Research Aim

To provide clarity into the current and emerging connected home

ecosystem – from vendor to end-user - categorizing the value

chain across different products and services to allow further

understanding of revenue generation, positioning, and value

creation in the connected home market.

22

Phase 2b: ‘industry participant’ InterviewsPhase 2a: End-User/Consumer Survey

Research Methodology:

Phase 2: Interviews and Interim Update Meeting

• IHS conducted a web-survey of 1,000 consumers in North America to assess key topics including:

• Desirability of connected home device, features and services

• Willingness to pay for key devices/services

• Attitudes to connected home suppliers, i.e., preferred suppliers, etc.

• Assessment of each statement by demographic, etc.

• The aim of this survey was to determine what constitutes value in the mind of different consumer groups.

• No pre-qualifying questions were used, aside from excluding respondents under the age of 16 (as they are considered unlikely to be the key purchasers, although may influence the buying decision of others).

• Series of interviews (in the range of 20-30) to cover all key industry participants (as agreed with the Project Steering Committee) in the kick-off meeting, such as:

• Device Suppliers• Retailers• Contractors/Installers• Service Providers (including platform

providers)• Operators• Others

• Each 45-60 minute discussion was based on ‘discussion guides’, agreed with the Project Steering Committee

• The interviews were focussed on North American industry participants

• This primary research process supplemented IHS’s existing knowledge base, having recently completed a focussed ‘smart home’ study (which required >40 primary interviews).

Trends in the Connected Home

The range of existing companies offering connected home solutions

will increase, moving from specialist companies to general service

providers, retailers, etc.

There will be increased availability of connected

alternatives to traditionally non-connected products, and new

connected devices will emerge, with specialists developing

Solution-agnostic, third-party platform providers will be increasingly used by service providers and

device manufacturers

Some dedicated providers transition to platform

provision to align with market trend

Device Suppliers to begin offering connected home services, in some cases

as part of the upfront device cost

Increased opportunity for closely related business lines will develop (e.g. elderly monitoring or demand-response)

Features outside of cloud-based home control will play

an important role across customer segments (such as e-commerce or remote

diagnostics)

Connected Home Use-case24

56% of the 1,000 North American respondents would like to perform at least one of the connected home use-cases provided.

Use-cases around connected home monitoring functions, including intruder notification, hazard detection and door/window lock status, received the highest aggregate response, followed by climate control.

Typically respondents over the age of 51 showed significantly less interest in connected home functions, with more than half of these not selecting any use-cases at all.

An increase in household income yielded a higher propensity to have indicated an interest in a connected home use-case.

55% of respondents with a household income lower than $25,000 selected no use-cases, compared with just 29% with incomes of $150,000 or above.

Importantly, 76% of respondents owning a security system indicated an interest in at least one connected home use-cases, compared with just 49% that did not own a security system.

Desirability

Connected Home Use-case25

Connected Home Display Device Preference26

The way in which a consumer interfaces with the connected home can be key to the end-user experience.

For each use-case selected, at least 70% of respondents indicated they would like to use their smartphone to display information or control their connected home devices.

Tablet and web portal were second and third most prevalent in each use-case, except in lighting control were a control panel was preferred to a web portal.

Although respondents were able to select multiple devices, use of an in-car infotainment system to display information or control devices only received a maximum of 10% of responses. Generally, this was higher in ‘notification’ applications than in ‘control’ applications, where less interaction with an in-car infotainment system might be needed.

User Interface

Connected Home Display Device Preference

Respondents were asked to rate the value of using a single application over multiple apps to control multiple devices.

557 respondents were asked this question.

Key points of note:

• As more companies enter the connected home market, the market could develop in such a way that consumers have to open different apps to control different devices. This would be significantly detrimental to user experience and the development of the market, with more than a third of respondents selected that they would find it very valuable, only choosing a system which allows them to use a single app or program. A further third of respondents selected that they would find this valuable, and would prefer a single app or program.

Expanded Summarized Answers in Table AboveVery valuable – I would only choose a system which allows me to use a single app or programModerately valuable – I would prefer a single app or programNeutral – I’m happy with eitherNot of value – I would prefer separate apps or programs

Connected Home Display Device - Interface

IHS Technology

Connected Home Monthly Subscription Services

Overall, respondents preferred to pay a monthly fee for home monitoring-related services.

Entertainment and Convenience services were least selected for monthly

payments.

Service Provider Preference

While specialist home automation companies were the most commonly selected option, more than half of

respondents selected a company that already charges a subscription fee.

# RankFunctions Most Favoured for Monthly Cost

% of Respondents

# 1 Elderly Relative Monitoring 77%

# 2 Intruder Notification 69%

# 3 Hazard Detector Monitoring 68%

# 4 Viewing Camera Feed 66%

# 5 Relative Notification 64%

Source: IHS - Monetization in the Connected Home (2013)

# RankFunctions Least Favoured for Monthly Cost

% of Respondents

# 1 Home Entertainment Monitoring 40%

# 2 Window Dressing Control 46%

# 3 Pool Pump Monitoring 47%

# 4 Lighting Control 50%

Source: IHS - Monetization in the Connected Home (2013) # Rank Favoured Service Provider% of

Respondents

# 1 Specialist Home Automation Company 37%

# 2 Specialist Security Provider 24%

# 3 Telephone Provider 11%

# 4 Electricity Provider or Utility 9%

# 5 Cable/Satellite Provider 6%

Source: IHS - Monetization in the Connected Home (2013)

Willingness to Pay30

In all use-cases selected by respondents, at least 40% indicated that they intended to purchase a system or device to enable this functionality within the next five years. Crucially, a large number of respondents suggested some uncertainty regarding when or if they intended to purchase devices or systems, which would appear to contradict the high levels of interest and willingness to pay monthly fees.

The survey revealed that 30% of respondents were only made aware of connected home services or systems via the examples given in the survey itself. This may explain respondents’ uncertainty around their intention to purchase a device or system. Ultimately, if consumers are unaware that these systems and devices exist, they are unlikely to know where to purchase them from or indeed have a timeframe for doing so.

This result is of paramount importance, emphasizing the need to increase awareness amongst consumers to meet their desire and willingness to pay for the services or systems.

Purchase Intentions

Respondents that selected at least one use-case, selected on average six use-cases. This highlights the potential for multi-function systems or ‘bundling’ opportunities.

In contrast to the single application responses, a much lower percentage of respondents that selected more than one individual use-case (21%) indicated they would not be prepared to pay for all of their selections combined. 41% of these respondents suggested they would be prepared to pay $16 or more per month.

With an average of six use-cases selected by each of the respondents in this sample frame, this indicates that respondents would expect a level of discount for a bundle package when compared with purchasing multiple standalone services.

Bundled Functions

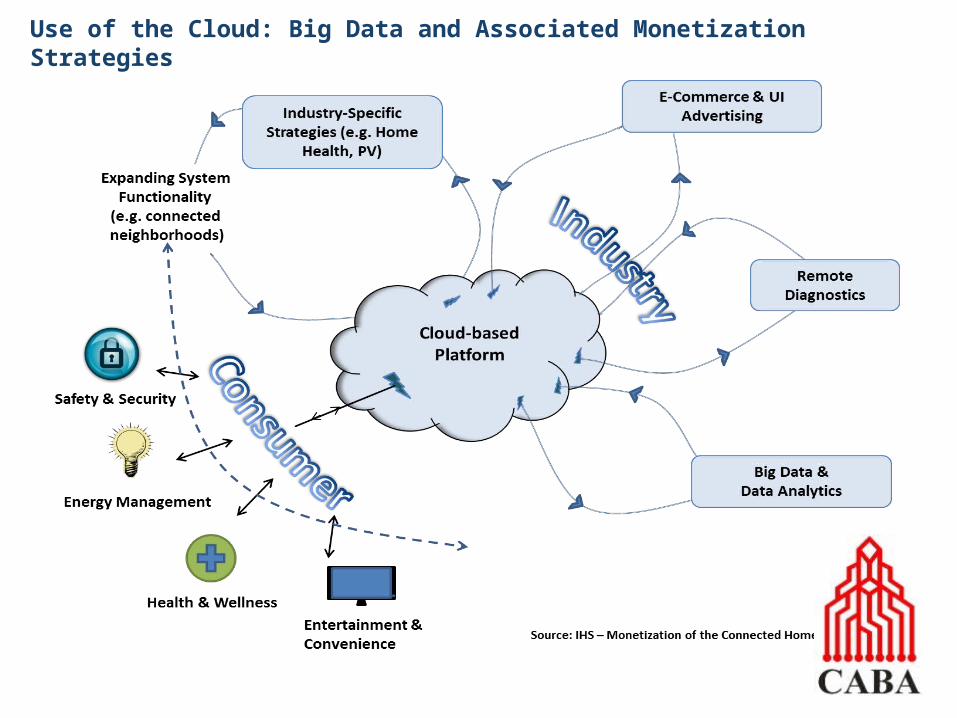

Use of the Cloud: Big Data and Associated Monetization Strategies

32

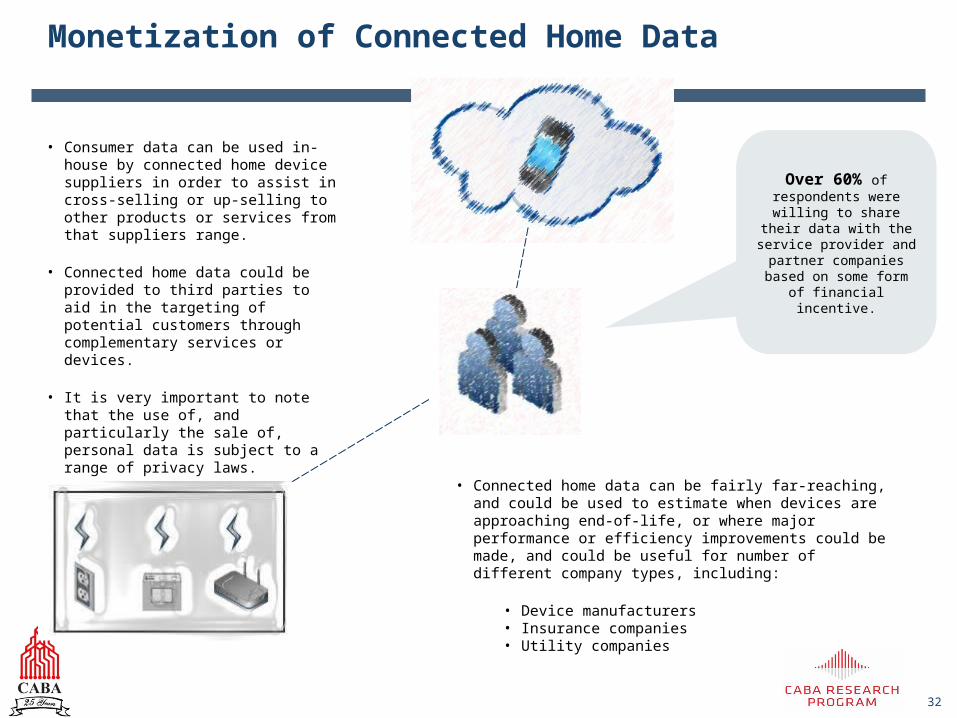

Monetization of Connected Home Data

• Consumer data can be used in-house by connected home device suppliers in order to assist in cross-selling or up-selling to other products or services from that suppliers range.

• Connected home data could be provided to third parties to aid in the targeting of potential customers through complementary services or devices.

• It is very important to note that the use of, and particularly the sale of, personal data is subject to a range of privacy laws.

Over 60% of respondents were willing to

share their data with the service provider and

partner companies based on some form of financial

incentive.

• Connected home data can be fairly far-reaching, and could be used to estimate when devices are approaching end-of-life, or where major performance or efficiency improvements could be made, and could be useful for number of different company types, including:

• Device manufacturers• Insurance companies• Utility companies

33

User Interface Advertising & E-Commerce Solutions

User Interface Advertising

• One of the key trends anticipated for the future connected home is the ability for companies to utilize user interfaces, such as control panels, smartphones, or tablets to advertise additional products and services, warranty discounts, and other up-sell services to the consumer.

• Vendors could monetize this by leasing or renting advertising space on connected home user interfaces to third-parties to promote relevant products, as well as use these displays to cross-sell their own products and services.

Just under 50% of the respondents surveyed found the opportunity for automatic

ordering of ancillary products for their devices

via their systems as valuable.

E-Commerce

• E-commerce can be implemented as part of the service for add-on or auxiliary devices, so that device offers can be linked to payment details stored on the system to enable easy, or even automatic (based on preset preferences) ordering of devices.

34

Remote Diagnostics

• Connected devices can, with the owner’s permission, use remote diagnostics features to allow information about the device performance to be communicated back to, for example, an appliance manufacturer.

• Vendors can remotely pre-empt expensive repairs by analyzing device diagnostic information, letting the consumer know that a device needs servicing or a part may need to be replaced.

• It could also be used as a tool to upsell extended warrantees or service contracts, for example by highlighting the parts of the device at risk of failure over the coming warrantee period.

• Remote diagnostics can enable the consumer to stay informed regarding the status of their device, warranty and other potential information. This enables consumers to make informed decisions about purchasing new devices or renewing warranties.

78% of respondents indicated remote software upgrades to

be valuable.

Similarly,

a staggering 80% of consumers surveyed found

remote diagnostic solutions to be valuable

• In addition, remote diagnostics capabilities can save time and associated costs for both the vendor and the consumer by automatically diagnosing a fault, without needed to send out a repairman to assess the problem before ordering and returning on a separate day with the required parts or tools.

• As with some of the other features outlined above, such as e-commerce, remote diagnostics can create an additional link between the consumer and the vendor. In some cases, the additional functionality and convenience can help to differentiate the device vendor, and also build further brand loyalty.

35

Other Monetization Considerations

Connected Neighborhoods

• There is an opportunity to expand the connected home network to create a connected neighborhood, driving a number of value-adding features and associated service revenues.

• Connected home systems could be extended to enable users to create ‘connected home networks’ with their friends, family or neighbors, such that an alert is also shown on other pre-defined connected home users’ interfaces (whether a smartphone, tablet, Smart TV, etc.) if an alarm is triggered.

• This sort of neighborhood intelligence could be offered as a value-added service for consumers.

Warranties and Insurance• The majority of industry experts interviewed in

the process of this research were dismissive of the suggestion of dedicated connected home system insurance, partly as it may to some extent be covered under existing programs.

• The recent consumer survey from IHS revealed that more than 63% of respondents that would like to be able to perform connected home functions would like the option to purchase insurance on a connected home system, with younger age groups more likely to select this response. This presents a further monetization avenue for companies in the connected home market, from device suppliers to system or service providers, through to retailers or installation companies.

• Additionally, connected home service or system providers may partner with insurance providers to help reduce the value of insurance claims, creating a further avenue for revenue generation either directly from the insurance provider or indirectly via discounted insurance premiums to customers.

Leverage Trends in Other MarketsConnected home systems will need to evolve to take into account growing consumer trends, integrating new applications and functions as lifestyles, behaviors and households change.

For example, as the trend towards renewables grows, and certain parts of North America provide attractive incentives, connected home providers can leverage consumer interest in residential PV systems. Independent living offers an interesting opportunity as much of the core hardware and software functionality can be enabled with familiar solutions. Alternatively, leveraging the ‘connected car’ may provide further monetization opportunities.

36

Industry-Specific Connected Home Services

Demand Response and Peak Load Control

• Connected home service providers could obtain consumer permission to remotely, incrementally, adjust device operation at times of peak demand through offers such as rebates or discounts and act as demand response aggregators.

• This becomes even more of an interesting concept once electric vehicles begin to become more commonplace, as there is the potential for an electric vehicle to be used as an energy storage device – for example, charging to capacity when electricity demand is low (for example, at 3am), using this stored electricity at peak times.

Telehealth, Consumer Health Monitoring & Independent Living

• Independent living systems are considered by IHS to be an appropriate extension of current connected home capabilities, as much of the core hardware and software functionality can be enabled with familiar solutions.

• As interest in consumer-driven health monitoring grows, there could be the potential to have a common platform across the wider ‘connected home’, adding a further application strand, and becoming more entrenched in consumer lifestyles.

• Companies entering this market will need to be aware of the stringent, and often country-specific, regulations impacting this market (e.g. HIPAA)

Residential Photovoltaic (PV) Integration• IHS expects that the relative increase in uptake of

residential PV systems via incentive schemes will increase awareness of ‘smart’ alternatives to connected home energy management systems, where the PV system can be directly linked into a utility-led residential load control solution and can act as an determinant for demand-response activities.

• Service providers can work with PV providers to leverage the growing interest in residential PV installation through improved services driven by integration into a connected home system.

Connected Car• There is the potential for the integration of the connected

car into the connected home system, using an in-car infotainment system to display notifications or enable the control of connected home devices. An example may include the ability to control a connected HVAC system, via an in-car infotainment system, whilst driving back to your home.

• Connected home service and system providers could collaborate with in-car infotainment device suppliers to develop software solutions and ensure the relevant connectivity technologies are included within these devices to enable connected car integration with the connected home.

37

Connected Consumer Roadmap: Driven by the Internet of Things

Intelligent Buildings and Big Data

Current CABA Research Projects

38

38

Intelligent and Integrated Building Technologies: Market Size N.A. version 2 (MSNA v2)

Zero Net Energy Buildings: Building Intelligent Controls Driving Success

Current CABA Research Projects

39

1173 Cyrville Road, Suite 210Ottawa, ON K1J 7S6

613.686.1814Toll free: 888.798.CABA (2222) Fax: 613.744.7833

TO RECEIVE A COMPLIMENTARY LIFE CYCLE COSTING OF INTELLIGENT BUILDINGS

REPORT GO TO:

http://www.CABA.org/LCCIB

http://www.twitter.com/caba_newshttp://www.linkedin.com/groups?gid=2121884

http://www.CABA.org

Your Information Source for Home & Building Automation

For More Information Please Contact: