03.09.2014 Mongolia banking system outlook: Mongolian banks face cyclical and structural challenges,...

26

1 Mongolia Banking System Outlook, September 2014 Mongolia Banking System Outlook Mongolian Banks Face Cyclical and Structural Challenges SEPTEMBER, 2014 Graeme Knowd, Associate Managing Director

-

Upload

the-business-council-of-mongolia -

Category

Business

-

view

214 -

download

0

Transcript of 03.09.2014 Mongolia banking system outlook: Mongolian banks face cyclical and structural challenges,...

1Mongolia Banking System Outlook, September 2014

Mongolia Banking System OutlookMongolian Banks Face Cyclical and Structural Challenges

SEPTEMBER, 2014Graeme Knowd, Associate Managing Director

2Mongolia Banking System Outlook, September 2014

Agenda

1. Executive Summary

2. Operating Environment

3. Key Credit Metrics

4. Systemic Support

5. Key Takeaways

3Mongolia Banking System Outlook, September 2014

Executive Summary1

4Mongolia Banking System Outlook, September 2014

Mongolian Banks Face Cyclical and Structural Challenges

» Subdued global commodity demand continues to pressure growth outlook.

» Policy-driven credit boom remains key systemic risk.

» Tight funding conditions to persist amidst strong credit growth.

Our negative outlook for Mongolia’s banking system remains unchanged from 2013

5Mongolia Banking System Outlook, September 2014

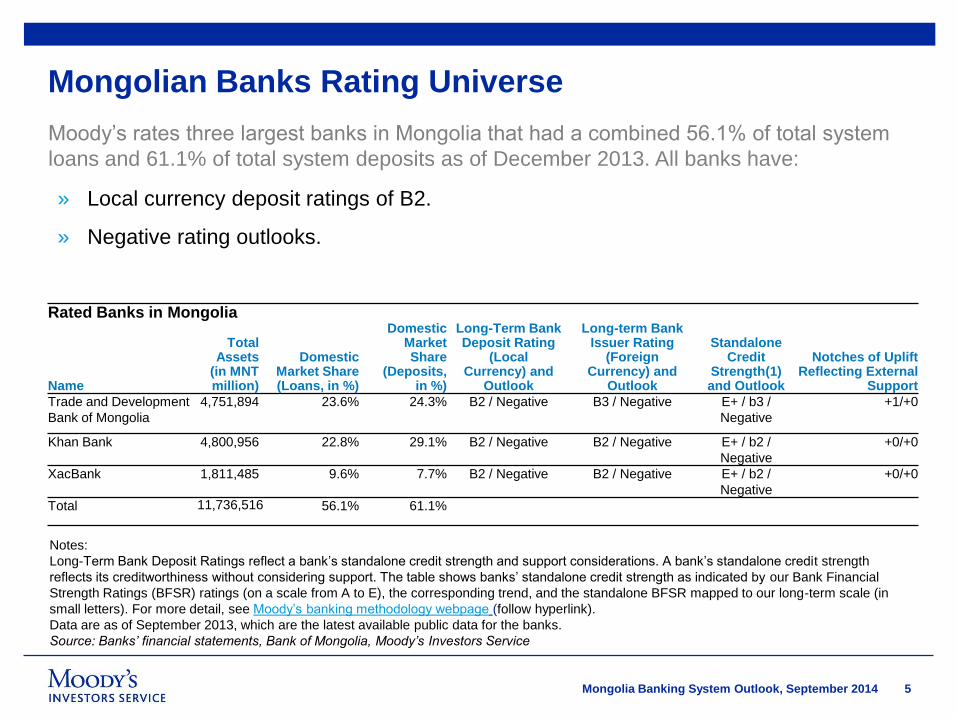

Mongolian Banks Rating Universe

Moody’s rates three largest banks in Mongolia that had a combined 56.1% of total system

loans and 61.1% of total system deposits as of December 2013. All banks have:

» Local currency deposit ratings of B2.

» Negative rating outlooks.

Rated Banks in Mongolia

Name

Total Assets

(in MNT million)

Domestic Market Share (Loans, in %)

Domestic Market Share

(Deposits, in %)

Long-Term Bank Deposit Rating

(Local Currency) and

Outlook

Long-term Bank Issuer Rating

(ForeignCurrency) and

Outlook

Standalone Credit

Strength(1)and Outlook

Notches of Uplift Reflecting External

Support

Trade and Development

Bank of Mongolia

4,751,894 23.6% 24.3% B2 / Negative B3 / Negative E+ / b3 /

Negative

+1/+0

Khan Bank 4,800,956 22.8% 29.1% B2 / Negative B2 / Negative E+ / b2 /

Negative

+0/+0

XacBank 1,811,485 9.6% 7.7% B2 / Negative B2 / Negative E+ / b2 /

Negative

+0/+0

Total 11,736,516 56.1% 61.1%

Notes:

Long-Term Bank Deposit Ratings reflect a bank’s standalone credit strength and support considerations. A bank’s standalone credit strength

reflects its creditworthiness without considering support. The table shows banks’ standalone credit strength as indicated by our Bank Financial

Strength Ratings (BFSR) ratings (on a scale from A to E), the corresponding trend, and the standalone BFSR mapped to our long-term scale (in

small letters). For more detail, see Moody’s banking methodology webpage (follow hyperlink).

Data are as of September 2013, which are the latest available public data for the banks.

Source: Banks’ financial statements, Bank of Mongolia, Moody’s Investors Service

6Mongolia Banking System Outlook, September 2014

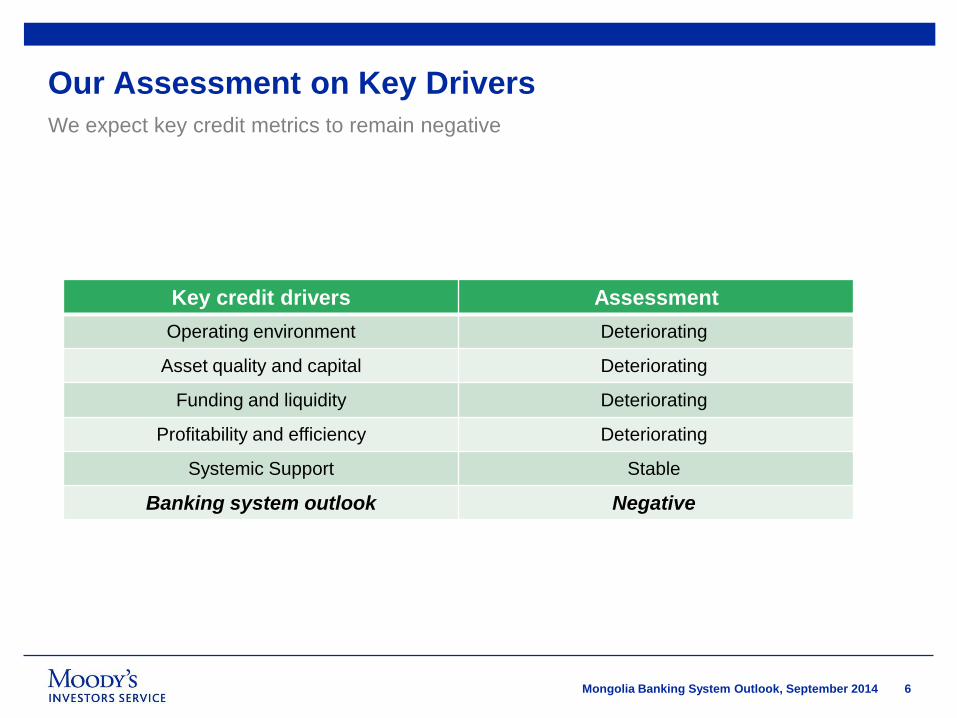

Our Assessment on Key Drivers

Key credit drivers Assessment

Operating environment Deteriorating

Asset quality and capital Deteriorating

Funding and liquidity Deteriorating

Profitability and efficiency Deteriorating

Systemic Support Stable

Banking system outlook Negative

We expect key credit metrics to remain negative

7Mongolia Banking System Outlook, September 2014

Operating Environment2

8Mongolia Banking System Outlook, September 2014

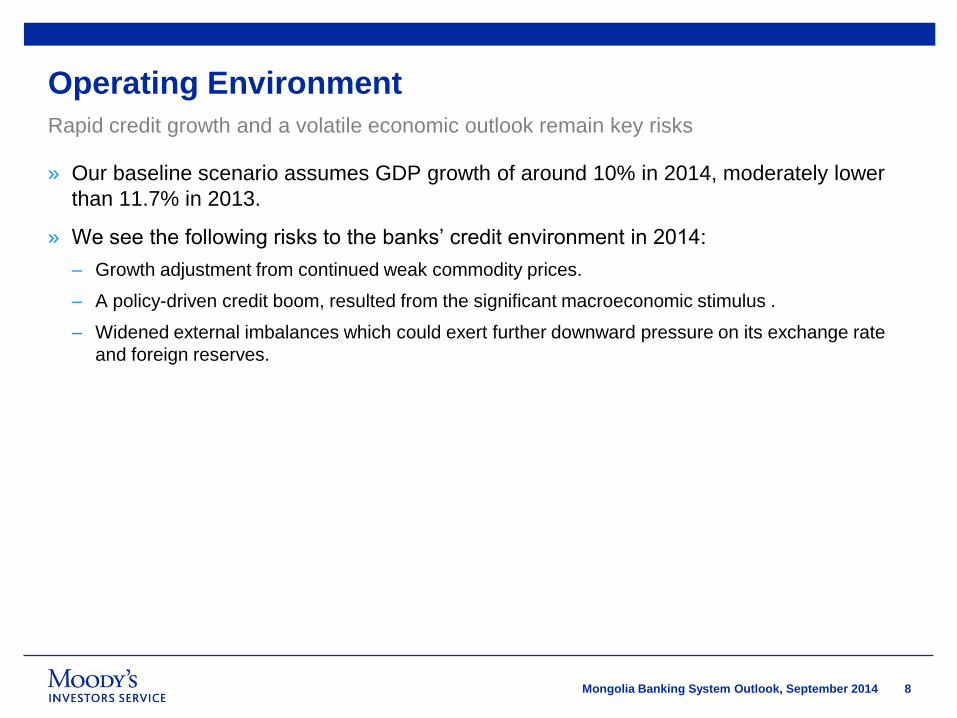

Operating Environment

» Our baseline scenario assumes GDP growth of around 10% in 2014, moderately lower

than 11.7% in 2013.

» We see the following risks to the banks’ credit environment in 2014:

– Growth adjustment from continued weak commodity prices.

– A policy-driven credit boom, resulted from the significant macroeconomic stimulus .

– Widened external imbalances which could exert further downward pressure on its exchange rate

and foreign reserves.

Rapid credit growth and a volatile economic outlook remain key risks

9Mongolia Banking System Outlook, September 2014

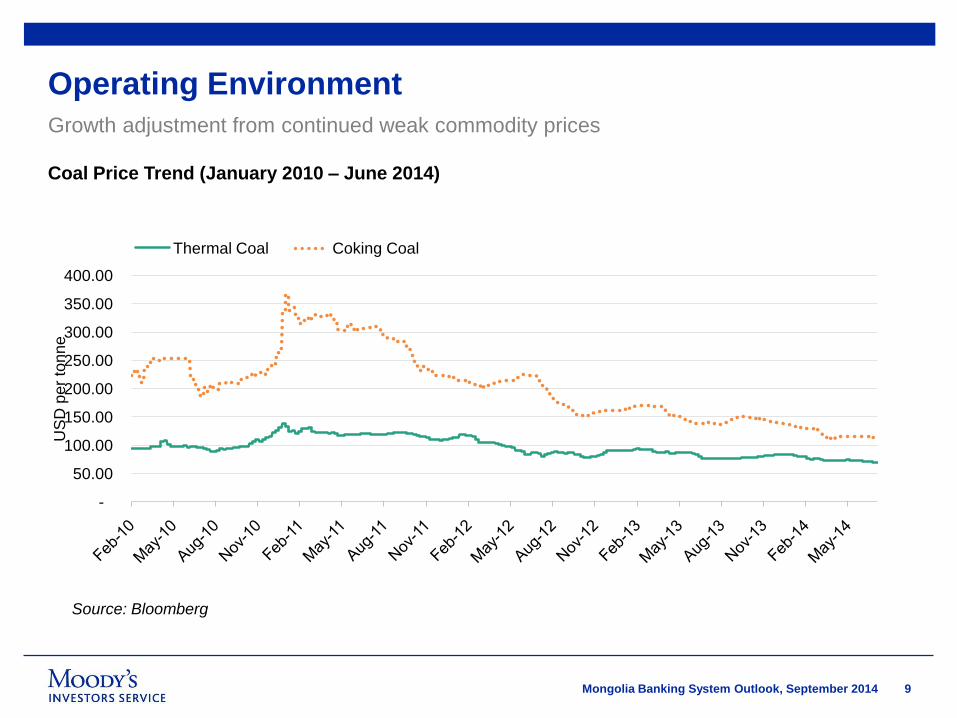

Operating Environment

Growth adjustment from continued weak commodity prices

Coal Price Trend (January 2010 – June 2014)

Source: Bloomberg

-

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

US

D p

er

ton

ne

Thermal Coal Coking Coal

10Mongolia Banking System Outlook, September 2014

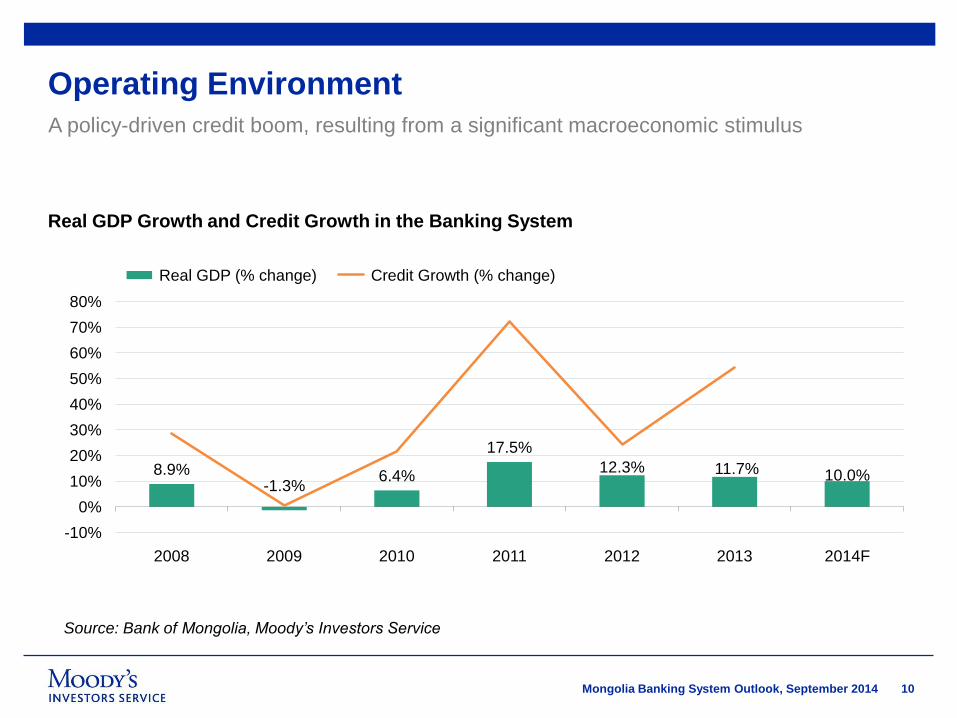

Operating Environment

A policy-driven credit boom, resulting from a significant macroeconomic stimulus

Source: Bank of Mongolia, Moody’s Investors Service

Real GDP Growth and Credit Growth in the Banking System

8.9%-1.3%

6.4%

17.5%

12.3% 11.7% 10.0%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2008 2009 2010 2011 2012 2013 2014F

Real GDP (% change) Credit Growth (% change)

11Mongolia Banking System Outlook, September 2014

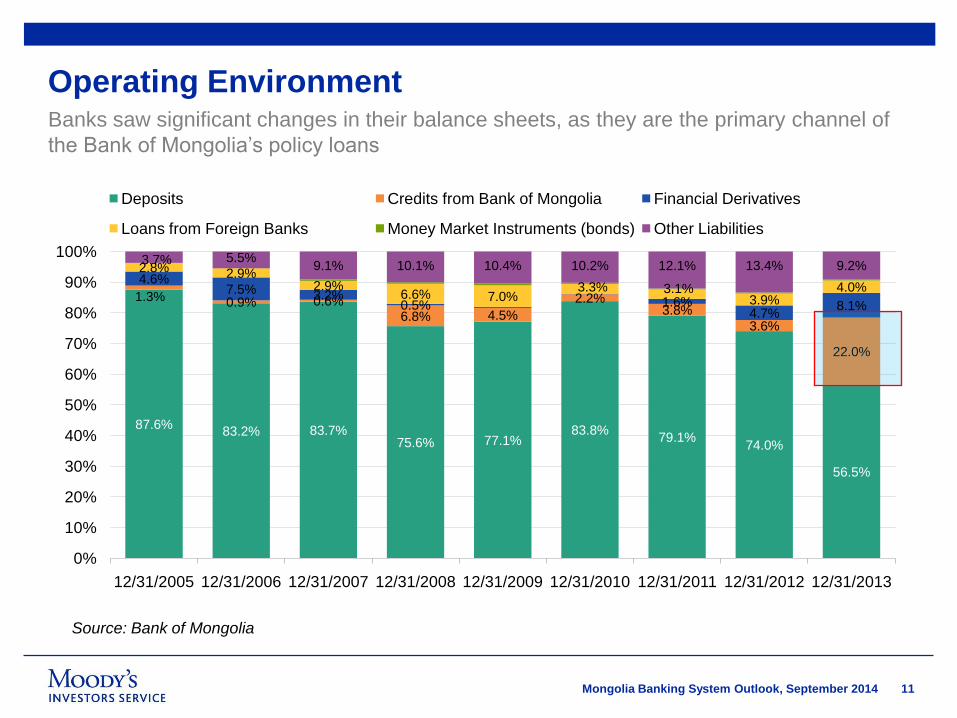

Operating EnvironmentBanks saw significant changes in their balance sheets, as they are the primary channel of

the Bank of Mongolia’s policy loans

87.6%83.2% 83.7%

75.6% 77.1%83.8%

79.1%74.0%

56.5%

1.3% 0.9% 0.6%6.8% 4.5%

2.2%3.8%

3.6%

22.0%

4.6%7.5% 3.2%

0.5% 1.6%4.7%

8.1%

2.8% 2.9%2.9%

6.6% 7.0%3.3% 3.1%

3.9%4.0%

3.7% 5.5%9.1% 10.1% 10.4% 10.2% 12.1% 13.4% 9.2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

12/31/2005 12/31/2006 12/31/2007 12/31/2008 12/31/2009 12/31/2010 12/31/2011 12/31/2012 12/31/2013

Deposits Credits from Bank of Mongolia Financial Derivatives

Loans from Foreign Banks Money Market Instruments (bonds) Other Liabilities

Source: Bank of Mongolia

12Mongolia Banking System Outlook, September 2014

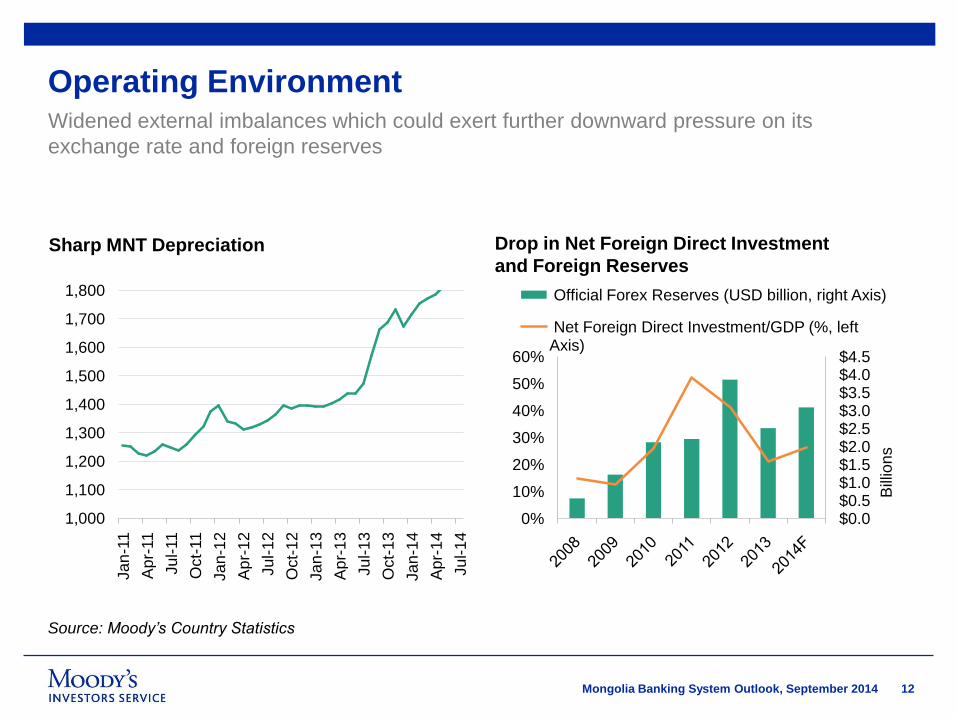

Operating EnvironmentWidened external imbalances which could exert further downward pressure on its

exchange rate and foreign reserves

Sharp MNT Depreciation Drop in Net Foreign Direct Investment

and Foreign Reserves

Source: Moody’s Country Statistics

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

Ja

n-1

1

Ap

r-11

Ju

l-11

Oct-

11

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oct-

12

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oct-

13

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

$0.0$0.5$1.0$1.5$2.0$2.5$3.0$3.5$4.0$4.5

0%

10%

20%

30%

40%

50%

60%

Bill

ion

s

Official Forex Reserves (USD billion, right Axis)

Net Foreign Direct Investment/GDP (%, left Axis)

13Mongolia Banking System Outlook, September 2014

Regulatory Environment

» Still-developing supervision, regulations as well as weak corporate governance

– The July 2013 failure of Savings Bank underscores the high cross-ownership linkage between the

banks and industrial companies, which have resulted in related-party lending and which have

increased the risks of spillovers.

» We expect the government’s latest legislation to result in some improvements in the

investment and capital market environments towards the latter part of this outlook:

– A new Foreign Investment Law

– A new Securities Market Law

– The Mongolia Mortgage Corporation (MIK)’s expanding its capacity to purchase mortgage loans.

Regulatory environment will remain challenging for Mongolian banks

14Mongolia Banking System Outlook, September 2014

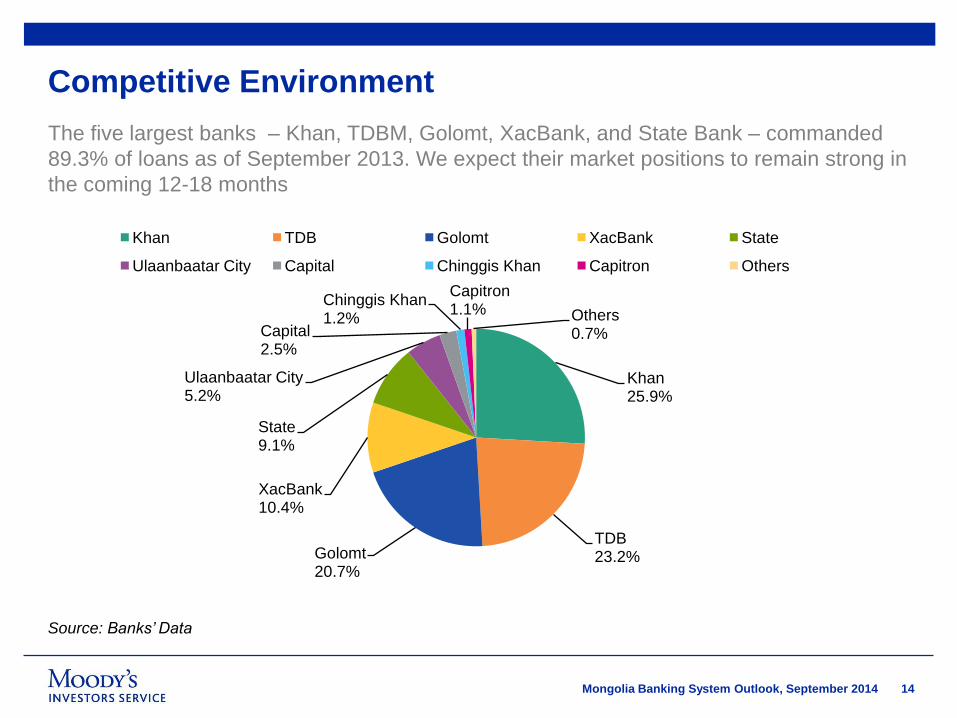

Competitive Environment

The five largest banks – Khan, TDBM, Golomt, XacBank, and State Bank – commanded

89.3% of loans as of September 2013. We expect their market positions to remain strong in

the coming 12-18 months

Khan25.9%

TDB23.2%Golomt

20.7%

XacBank10.4%

State9.1%

Ulaanbaatar City5.2%

Capital2.5%

Chinggis Khan1.2%

Capitron1.1% Others

0.7%

Khan TDB Golomt XacBank State

Ulaanbaatar City Capital Chinggis Khan Capitron Others

Source: Banks’ Data

15Mongolia Banking System Outlook, September 2014

Key Credit Metrics3

16Mongolia Banking System Outlook, September 2014

Asset Quality

We expect asset quality to be most vulnerable in Mining, Manufacturing, Construction, and

Mortgages

NPLs in

Mining, Manufacturing, Construction, an

d Mortgages

NPL Ratio by Industries

Source: Bank of Mongolia

NPL: Non-performing loan

0%

5%

10%

15%

20%

25%

30%

35%

2008 2009 2010 2011 2012 2013 1Q 2014

Mining and quarrying Manufacturing

Construction Mortgage

Total NPL ratio

0

50

100

150

200

250

300

MN

T B

illio

ns

2009 2010 2011 2012 2013 1Q 2014

17Mongolia Banking System Outlook, September 2014

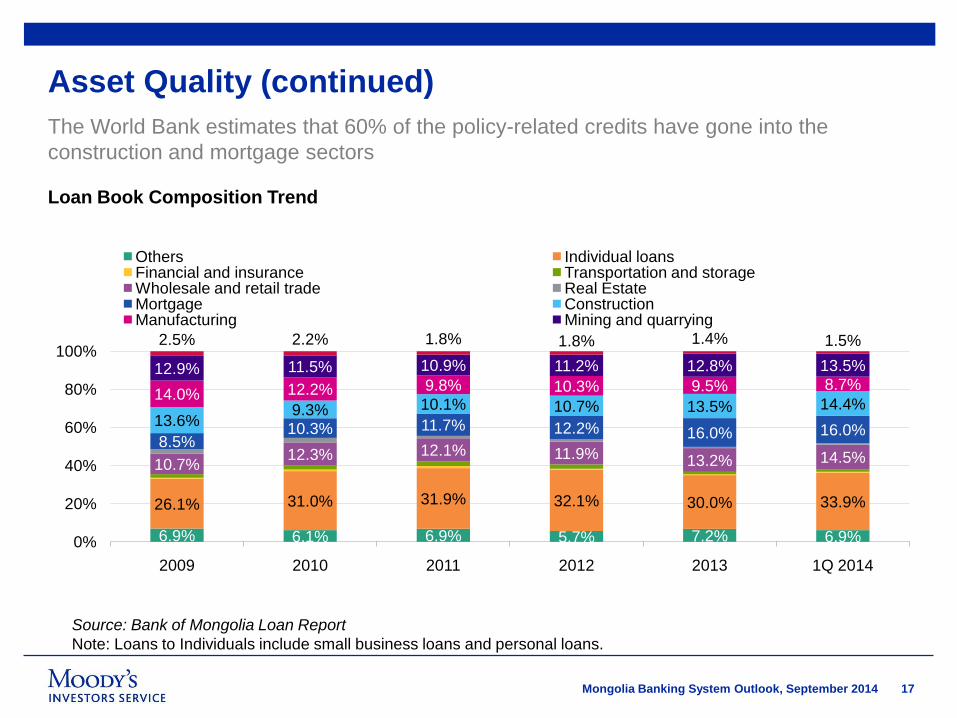

Asset Quality (continued)

The World Bank estimates that 60% of the policy-related credits have gone into the

construction and mortgage sectors

Loan Book Composition Trend

Source: Bank of Mongolia Loan Report

Note: Loans to Individuals include small business loans and personal loans.

6.9% 6.1% 6.9% 5.7% 7.2% 6.9%

26.1% 31.0% 31.9% 32.1% 30.0% 33.9%

10.7%12.3% 12.1% 11.9% 13.2% 14.5%

8.5%10.3% 11.7% 12.2% 16.0% 16.0%

13.6%9.3% 10.1% 10.7% 13.5% 14.4%

14.0% 12.2% 9.8% 10.3% 9.5% 8.7%12.9% 11.5% 10.9% 11.2% 12.8% 13.5%

2.5% 2.2% 1.8% 1.8% 1.4% 1.5%

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 1Q 2014

Others Individual loansFinancial and insurance Transportation and storageWholesale and retail trade Real EstateMortgage ConstructionManufacturing Mining and quarrying

18Mongolia Banking System Outlook, September 2014

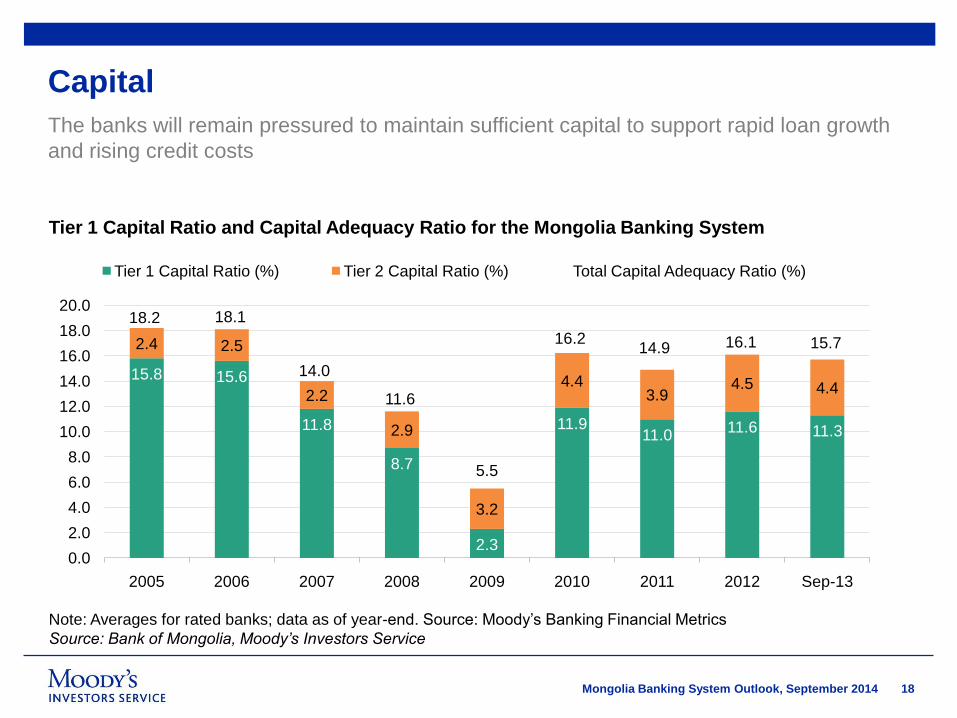

Capital

The banks will remain pressured to maintain sufficient capital to support rapid loan growth

and rising credit costs

Tier 1 Capital Ratio and Capital Adequacy Ratio for the Mongolia Banking System

Note: Averages for rated banks; data as of year-end. Source: Moody’s Banking Financial Metrics

Source: Bank of Mongolia, Moody’s Investors Service

15.8 15.6

11.8

8.7

2.3

11.911.0

11.6 11.3

2.4 2.5

2.2

2.9

3.2

4.43.9

4.5 4.4

18.2 18.1

14.0

11.6

5.5

16.214.9 16.1 15.7

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2005 2006 2007 2008 2009 2010 2011 2012 Sep-13

Tier 1 Capital Ratio (%) Tier 2 Capital Ratio (%) Total Capital Adequacy Ratio (%)

19Mongolia Banking System Outlook, September 2014

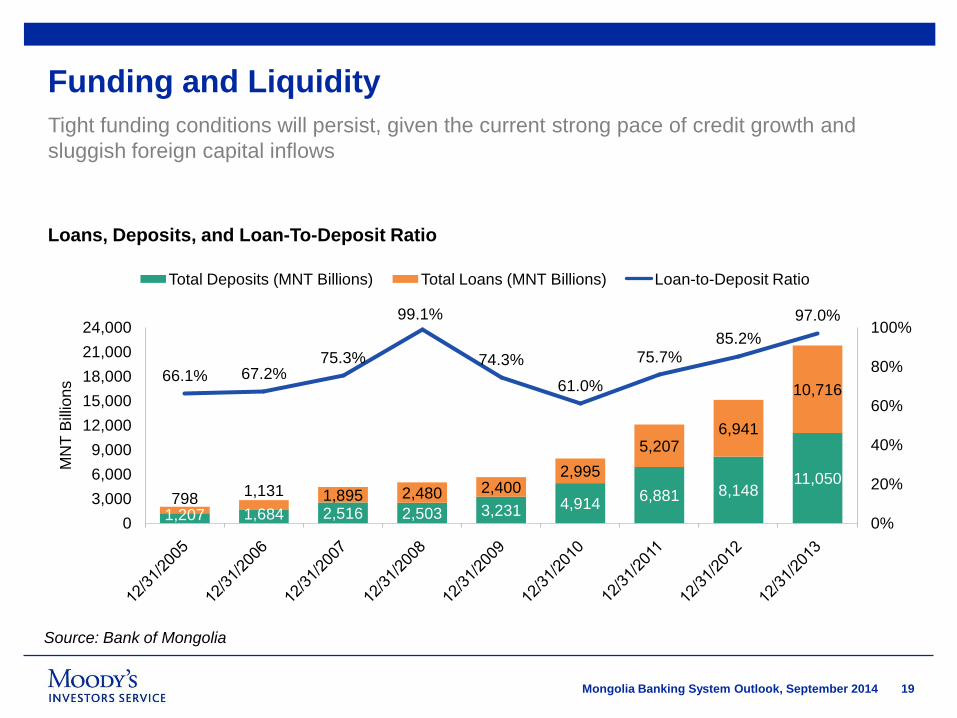

Funding and Liquidity

Tight funding conditions will persist, given the current strong pace of credit growth and

sluggish foreign capital inflows

Loans, Deposits, and Loan-To-Deposit Ratio

Source: Bank of Mongolia

1,207 1,684 2,516 2,503 3,231 4,9146,881 8,148

11,050

7981,131 1,895 2,480 2,400

2,995

5,2076,941

10,71666.1% 67.2%

75.3%

99.1%

74.3%

61.0%

75.7%85.2%

97.0%

0%

20%

40%

60%

80%

100%

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

24,000

MN

T B

illio

ns

Total Deposits (MNT Billions) Total Loans (MNT Billions) Loan-to-Deposit Ratio

20Mongolia Banking System Outlook, September 2014

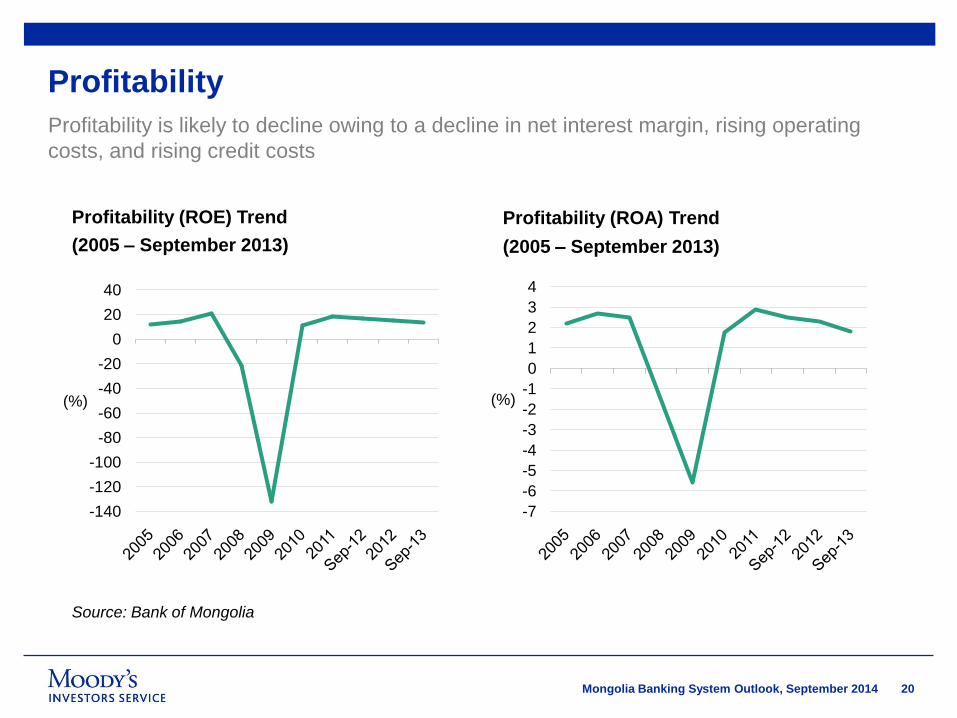

Profitability

Profitability is likely to decline owing to a decline in net interest margin, rising operating

costs, and rising credit costs

Profitability (ROE) Trend

(2005 – September 2013)

Profitability (ROA) Trend

(2005 – September 2013)

Source: Bank of Mongolia

-140

-120

-100

-80

-60

-40

-20

0

20

40

(%)

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

(%)

21Mongolia Banking System Outlook, September 2014

Systemic Support4

22Mongolia Banking System Outlook, September 2014

Systemic Support

» In our assessment, Mongolia has a low-support system.

» No uplift has been incorporated in the deposit ratings of Khan Bank and XacBank as

their current BCAs of b2 and deposit ratings of B2 are the same as Mongolia’s sovereign

rating.

» We have incorporated one notch of systemic support to the local currency deposit of

TDBM, which has a BCA of b3.

We expect the Mongolian government to be selective and to restrict its support to

systemically important banks

23Mongolia Banking System Outlook, September 2014

Key Takeaways5

24Mongolia Banking System Outlook, September 2014

Our Negative Outlook for Mongolia’s Banking System Remains Unchanged from 2013

» Subdued global commodity demand continues to pressure growth outlook.

» Policy-driven credit boom remains key systemic risk.

» Ongoing pressure on banks to maintain enough capital to support their rapid loan

growth.

» Tight funding conditions will persist amidst strong credit growth.

» Profitability will fall on declining margins and rising costs.

25Mongolia Banking System Outlook, September 2014

Graeme Knowd

Associate Managing Director - Japan

Corporate & Financial Institutions Group

Associate Managing Director - Korea/Mongolia

Financial Institutions Group

Moody’s Investors Service

Tel. +81.3.5408.4149

26Mongolia Banking System Outlook, September 2014

© 2014 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, ―MOODY’S‖). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. (―MIS‖) AND ITS AFFILIATES ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF

ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (―MOODY’S PUBLICATIONS‖) MAY

INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT

RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT.

CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S

OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED

ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE

OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR

HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S

ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN

STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS FOR RETAIL INVESTORS TO CONSIDER

MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS IN MAKING ANY INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL

ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE

REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN

WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all

information contained herein is provided ―AS IS‖ without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from

sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate

information received in the rating process or in preparing the Moody’s Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any

indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if

MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss

of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to

any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part

of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information

contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR

OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned credit rating agency subsidiary of Moody’s Corporation (―MCO‖), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and

commercial paper) and preferred stock rated by MIS have, prior to assignment of any rating, agreed to pay to MIS for appraisal and rating services rendered by it fees ranging from $1,500 to approximately

$2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors

of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com

under the heading ―Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.‖

For Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399

657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to ―wholesale clients‖ within the meaning of

section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a

―wholesale client‖ and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to ―retail clients‖ within the meaning of section 761G of the Corporations Act

2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail clients. It would

be dangerous for ―retail clients‖ to make any investment decision based on MOODY’S credit rating. If in doubt you should contact your financial or other professional adviser.