0201202LB04A-24 (Pack 4) - U.S. Career Institute

118

Explore the possibilities Bookkeeping Instruction Pack 4 Lessons 17-20 0201202LB04A-24

Transcript of 0201202LB04A-24 (Pack 4) - U.S. Career Institute

Explore the possibilities

BookkeepingInstruction Pack 4 Lessons 17-20

0201202LB04A-24

Bookkeeping

Instruction Pack 4

Lesson 17: Daily Bookkeeping Concepts

Lesson 18: Partnerships, Corporations and Non-profit Organizations

Lesson 19: Discounts, Reversing Entries and Allowances

Lesson 20: Sole Proprietorship Business Project

No part of this document may be reproduced or transmitted in any form or by any means, electronic or mechanical, for any purpose, without the express written permission of U.S. Career Institute.

Copyright © 2014, Weston Distance Learning, Inc. All Rights Reserved. 0201202LB04A-24

AcknowledgmentsAuthorsRobert James

Editorial StaffJanet PerryKimberly FieldsChristine DunlapElizabeth MunsonBrian KaufmanCarolina TownsendKaryn Madison

Design/LayoutConnie HunsaderSandy Petersen

U.S. Career InstituteFort Collins, CO 80525

www.uscareerinstitute.edu

Pack 4—Table of Contents

0201202LB04A-24 III

Table of Contents

Lesson 17: Daily Bookkeeping ConceptsStep 1: Learning Objectives for Lesson 17 ................................................................................................................... 1Step 2: Lesson Preview .................................................................................................................................................... 1Step 3: Terms You Will Need to Know ......................................................................................................................... 1Step 4: Daily Cash and Accounts ................................................................................................................................... 2Step 5: Cash Receipts Portion of the Summary ........................................................................................................... 4

Cash Sales .......................................................................................................................................................... 4Collections on Account ................................................................................................................................... 4Refunds .............................................................................................................................................................. 4

Step 6: Cash on Hand Section of the Summary........................................................................................................... 5Step 7: Petty Cash and Change Bank ............................................................................................................................ 5Step 8: Cash Short and Cash Over ................................................................................................................................ 5Step 9: Total Sales ............................................................................................................................................................ 6Step 10: Practice Exercise 17-1 ...................................................................................................................................... 8Step 11: Review Practice Exercise 17-1 ....................................................................................................................... 10Step 12: Handling the Petty Cash/Change Bank ....................................................................................................... 11

The Amount in the Petty Cash/Change Bank ............................................................................................ 11Petty Cash Slips (Vouchers) .......................................................................................................................... 12

Step 13: Journalizing Petty Cash Slips and Cash Over/Short .................................................................................. 12Step 14: Lesson Summary ............................................................................................................................................. 17Step 15: Quiz 17 ............................................................................................................................................................. 17

Lesson 18: Partnerships, Corporations and Non-profit OrganizationsStep 1: Learning Objectives for Lesson 18 ................................................................................................................... 1Step 2: Lesson Preview ................................................................................................................................................... 1Step 3: Terms You Will Need to Know ........................................................................................................................ 2Step 4: Partnerships ........................................................................................................................................................ 2

Co-ownership ................................................................................................................................................... 2

Bookkeeping

IV 0201202LB04A-24

Step 5: A Partner’s Interest ............................................................................................................................................ 3Transferring Interest ........................................................................................................................................ 3Goodwill ........................................................................................................................................................... 4Capital Accounts .............................................................................................................................................. 5Additional Investment .................................................................................................................................... 7Drawing Accounts ........................................................................................................................................... 8The Worksheet and Financial Statements .................................................................................................... 8Figuring Division of Income or Loss ............................................................................................................ 8Preparing a Distribution of Net Income Statement .................................................................................... 9

Step 6: Practice Exercise 18-1 ..................................................................................................................................... 10Step 7: Review Practice Exercise 18-1 ........................................................................................................................ 12Step 8: The Capital Statement ..................................................................................................................................... 13Step 9: Preparing Partnership Balance Sheets .......................................................................................................... 15Step 10: Closing Accounts in a Partnership .............................................................................................................. 15

Closing the Drawing Accounts .................................................................................................................... 17Step 11: Corporations .................................................................................................................................................. 18

Stocks and Stockholders ................................................................................................................................ 18Dividends and Retained Earnings ................................................................................................................ 19Types of Stock ................................................................................................................................................. 19Trading Stock .................................................................................................................................................. 20

Step 12: Practice Exercise 18-2 ................................................................................................................................... 20Step 13: Review Practice Exercise 18-2 ...................................................................................................................... 21Step 14: What is a Non-profit Organization? ............................................................................................................ 21

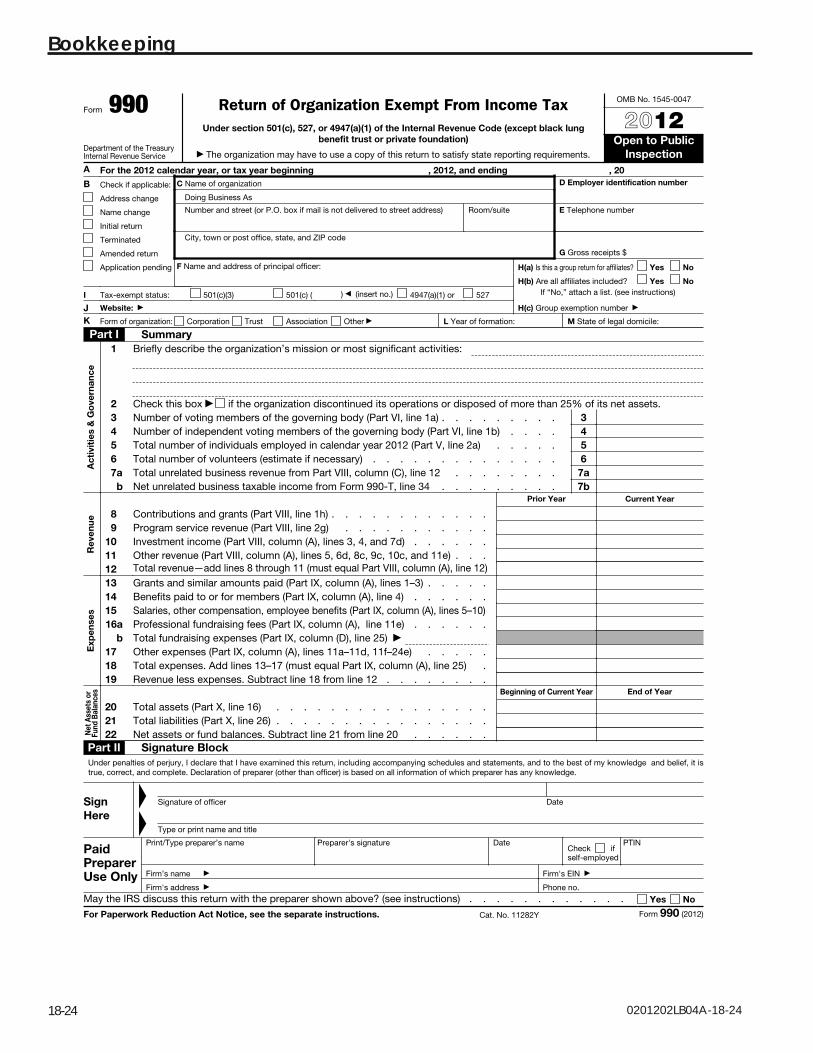

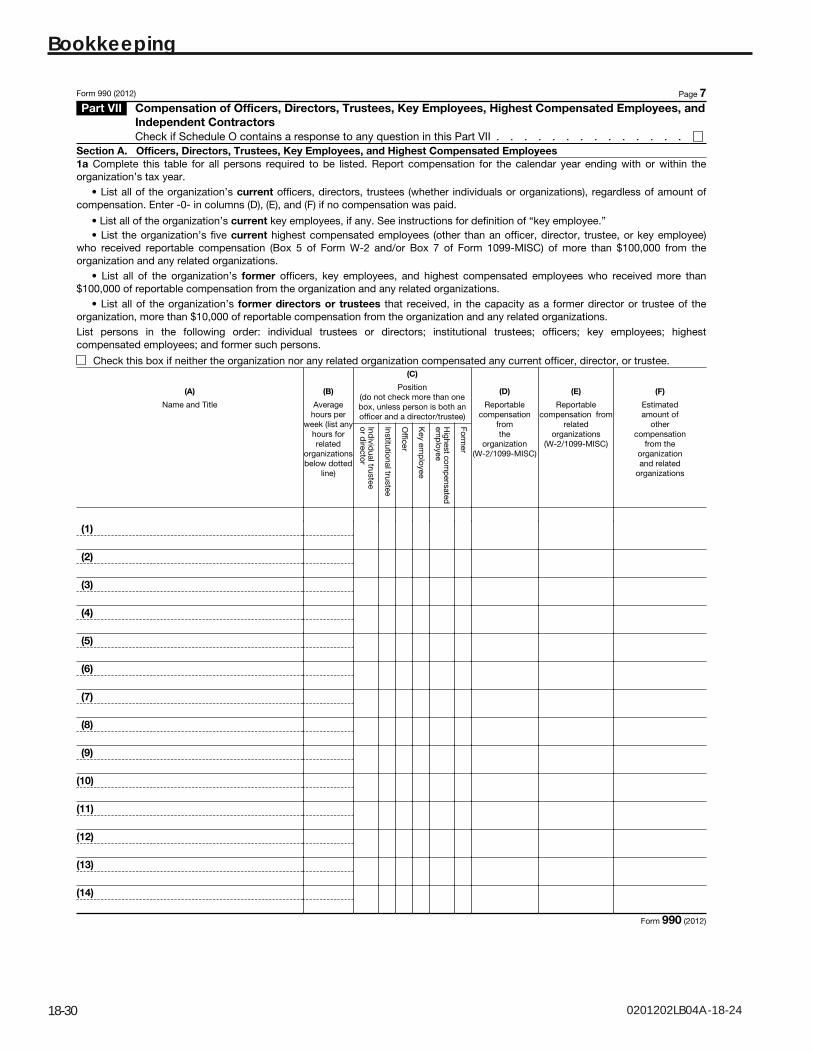

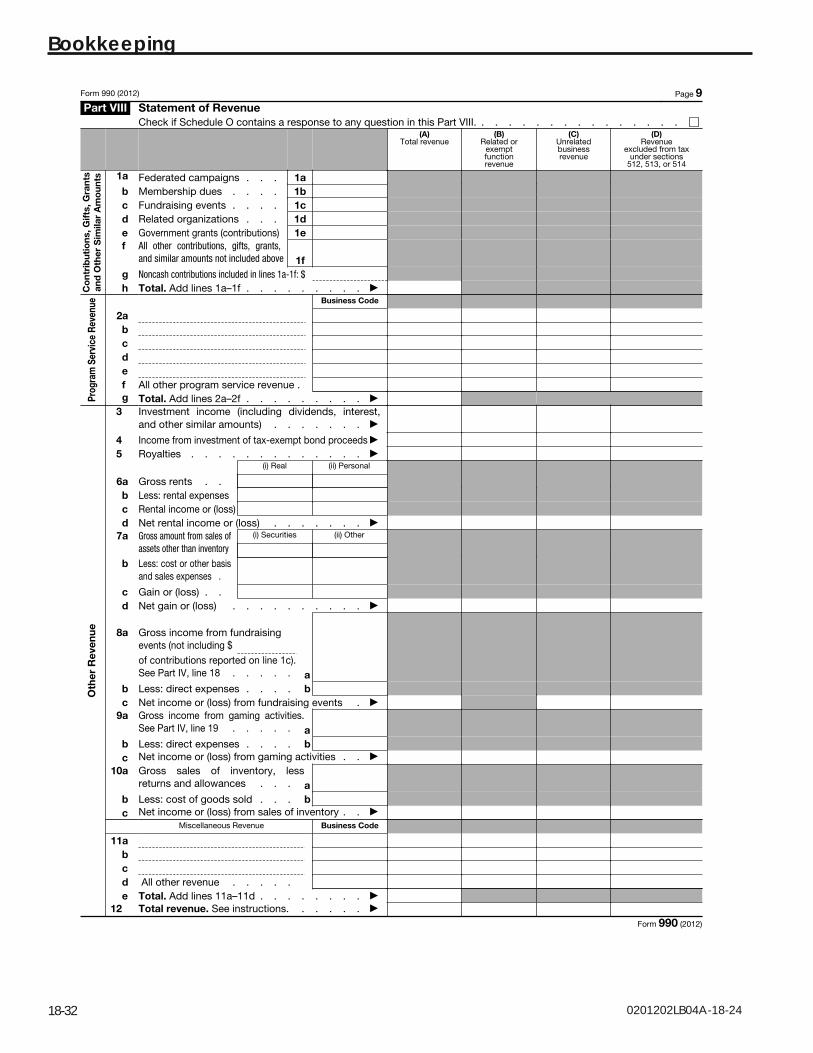

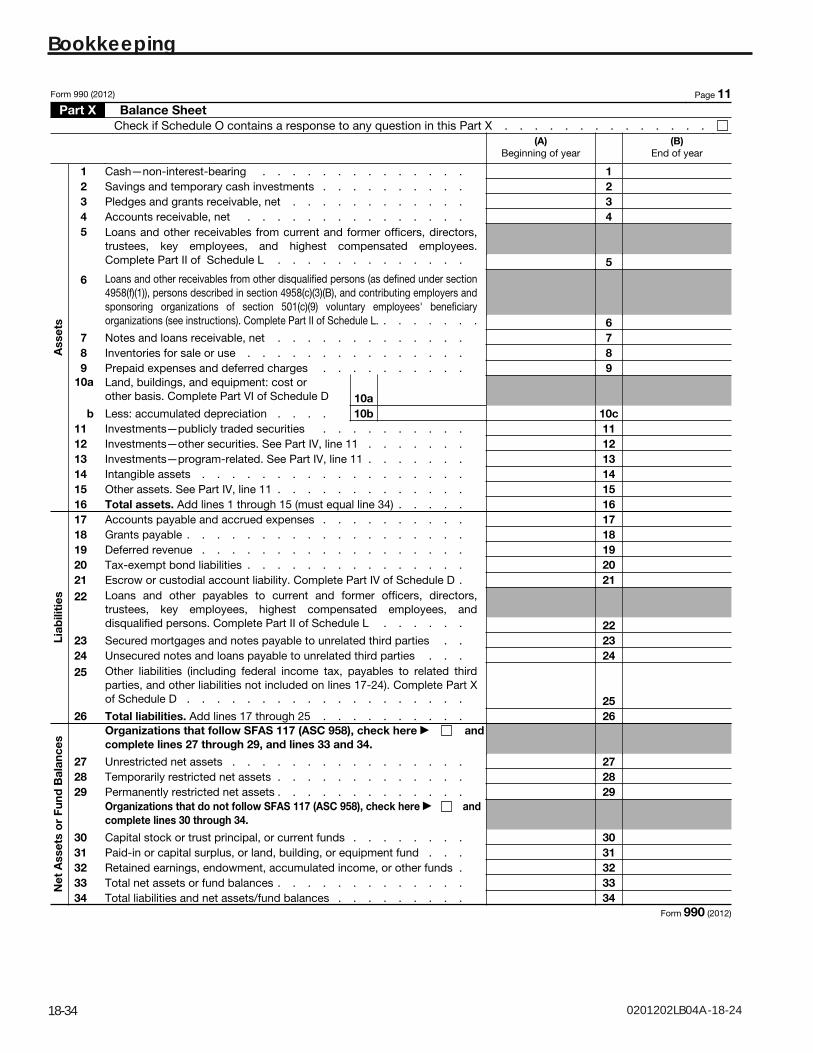

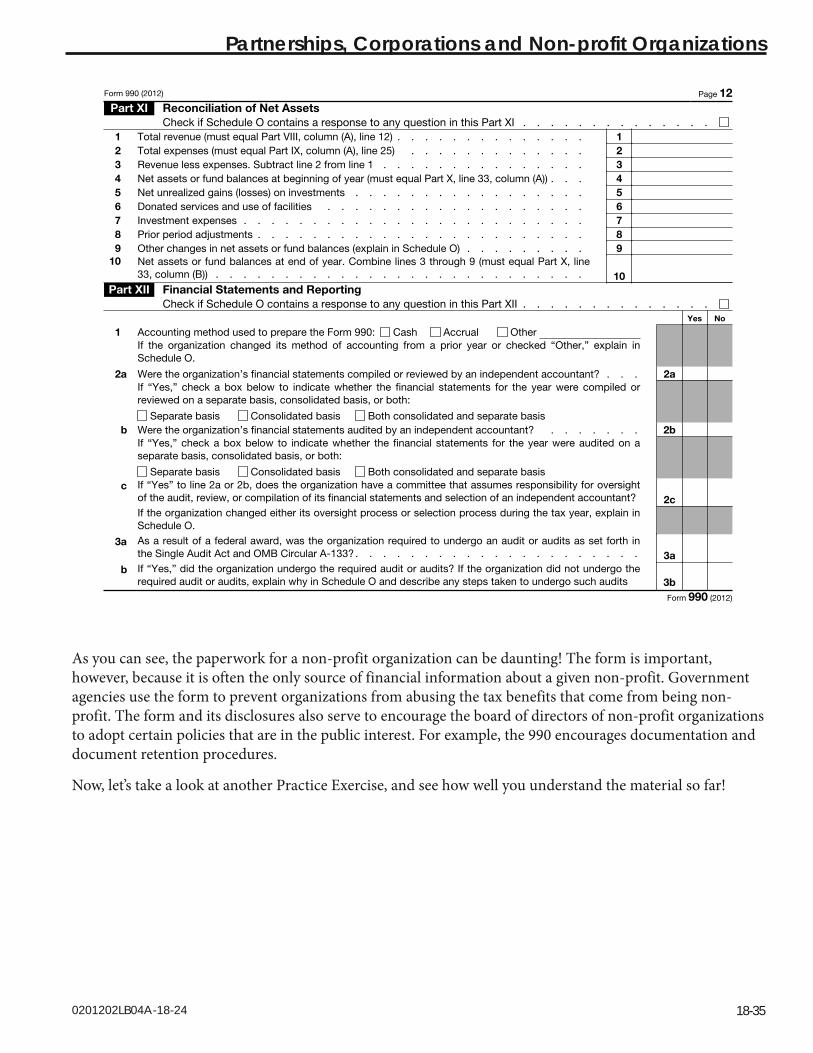

Non-profit Organizations and the Accounting ......................................................................................... 22Services Professional ..................................................................................................................................... 22Form 990 for Non-profit Organizations ..................................................................................................... 22

Step 15: Practice Exercise 18-3 ................................................................................................................................... 36Step 16: Review Practice Exercise 18-3 ...................................................................................................................... 36Step 17: Lesson Summary ............................................................................................................................................ 36Step 18: Quiz 18 ............................................................................................................................................................. 36

Pack 4—Table of Contents

0201202LB04A-24 V

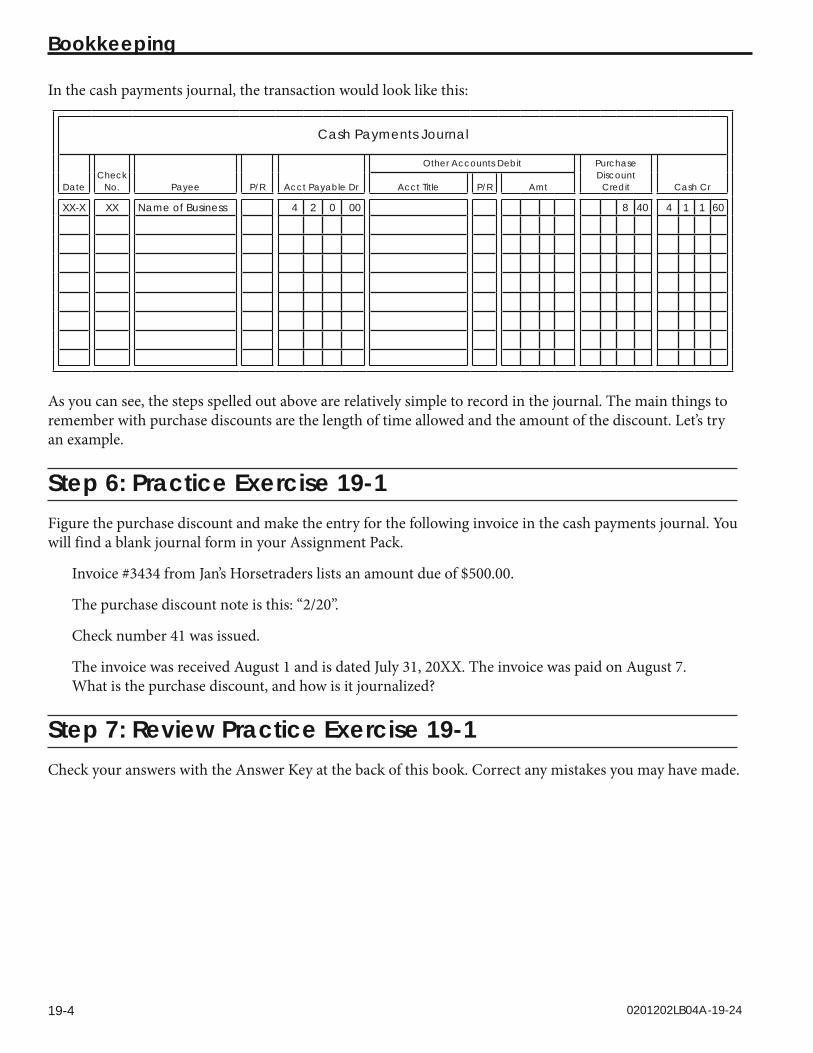

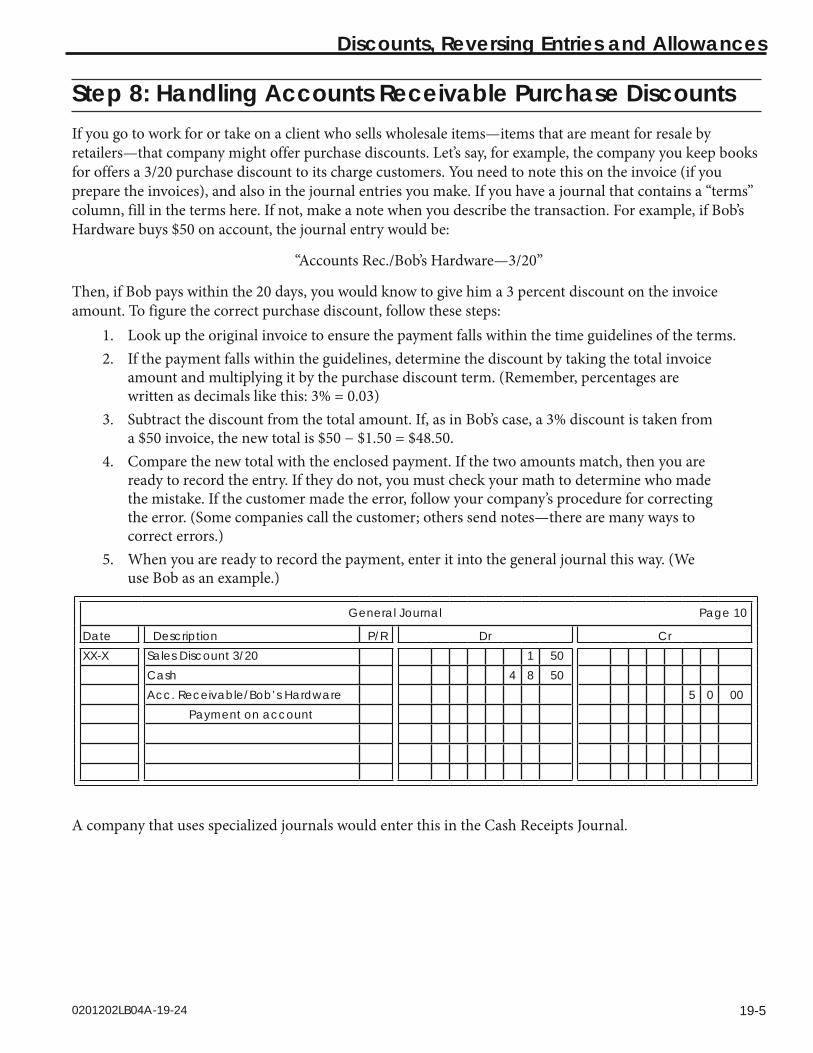

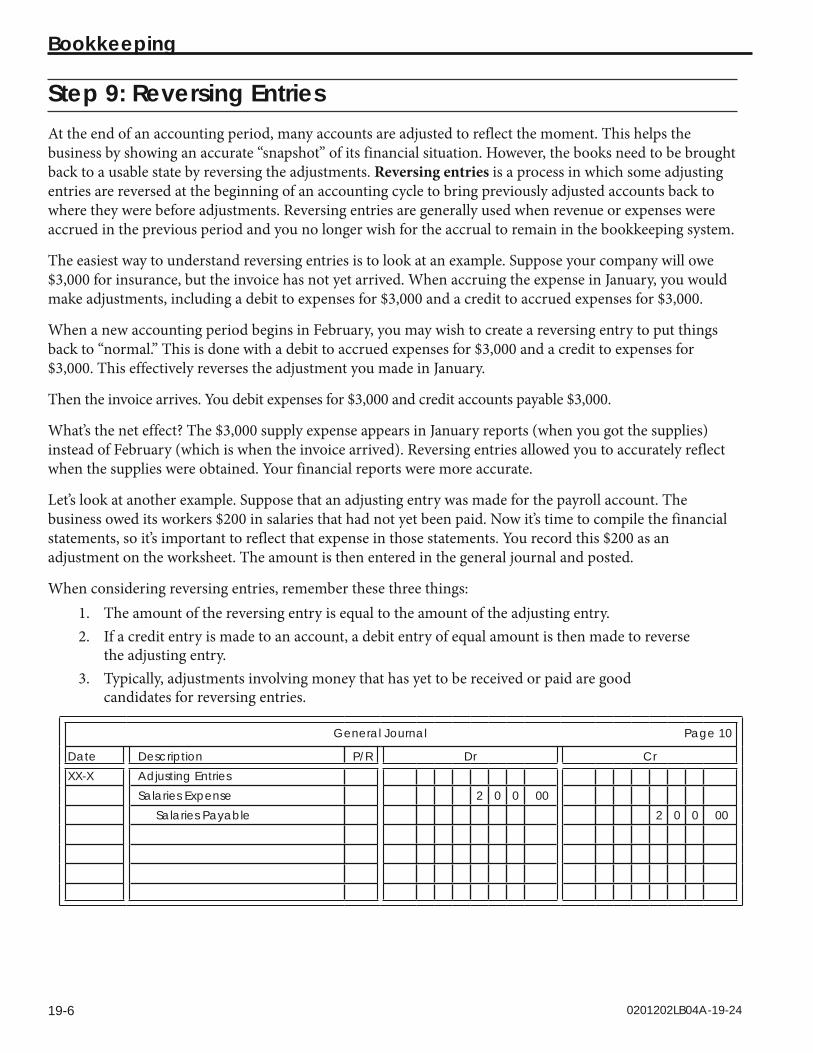

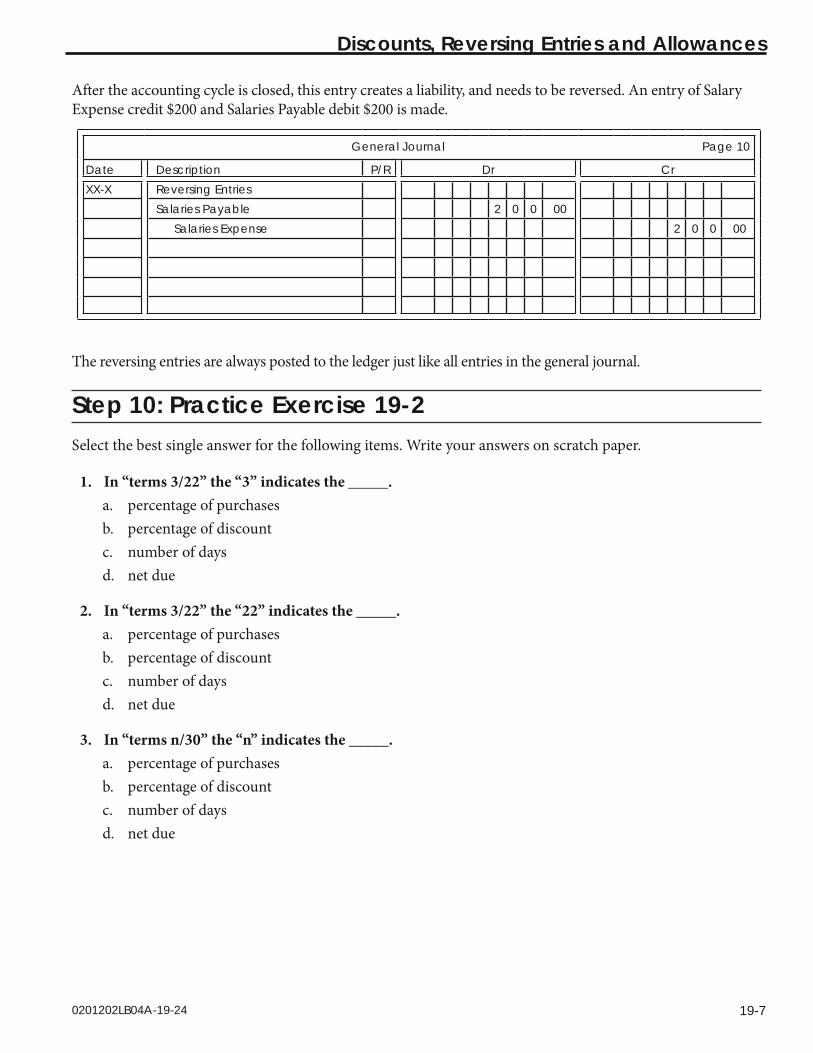

Lesson 19: Discounts, Reversing Entries and AllowancesStep 1: Learning Objectives for Lesson 19 ................................................................................................................... 1Step 2: Lesson Preview .................................................................................................................................................... 1Step 3: Terms You Will Need to Know ......................................................................................................................... 1Step 4: Purchase Discounts ............................................................................................................................................ 2Step 5: Journalizing Purchase Discounts ...................................................................................................................... 2Step 6: Practice Exercise 19-1 ........................................................................................................................................ 4Step 7: Review Practice Exercise 19-1 ........................................................................................................................... 4Step 8: Handling Accounts Receivable Purchase Discounts ............................................................................................5Step 9: Reversing Entries ................................................................................................................................................ 6Step 10: Practice Exercise 19-2 ...................................................................................................................................... 7Step 11: Review Practice Exercise 19-2 ......................................................................................................................... 8Step 12: Allowances for Uncollectible Accounts ......................................................................................................... 9Step 13: Getting Started a Bookkeeper ...................................................................................................................... 10Step 14: Practice Exercise 19-3 .................................................................................................................................... 13Step 15: Review Practice Exercise 19-3 ....................................................................................................................... 13Step 16: Lesson Summary ............................................................................................................................................. 14Step 17: Quiz 19 ............................................................................................................................................................. 14

Just for Fun ...................................................................................................................................................... 15

Lesson 20:Sole Proprietorship Business ProjectStep 1: Lesson Preview .................................................................................................................................................... 1Step 2: Completing the Project ...................................................................................................................................... 1Step 3: The Final Project ................................................................................................................................................. 2Step 4 Bright Ideas Light Center .................................................................................................................................... 4

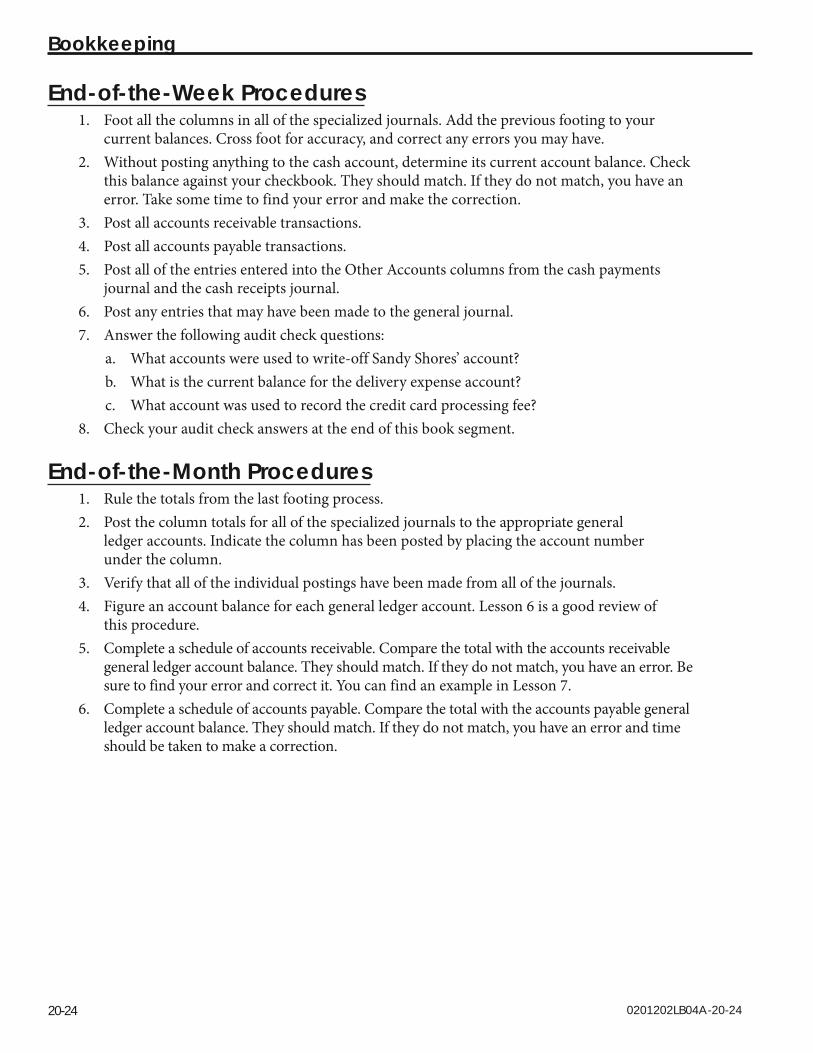

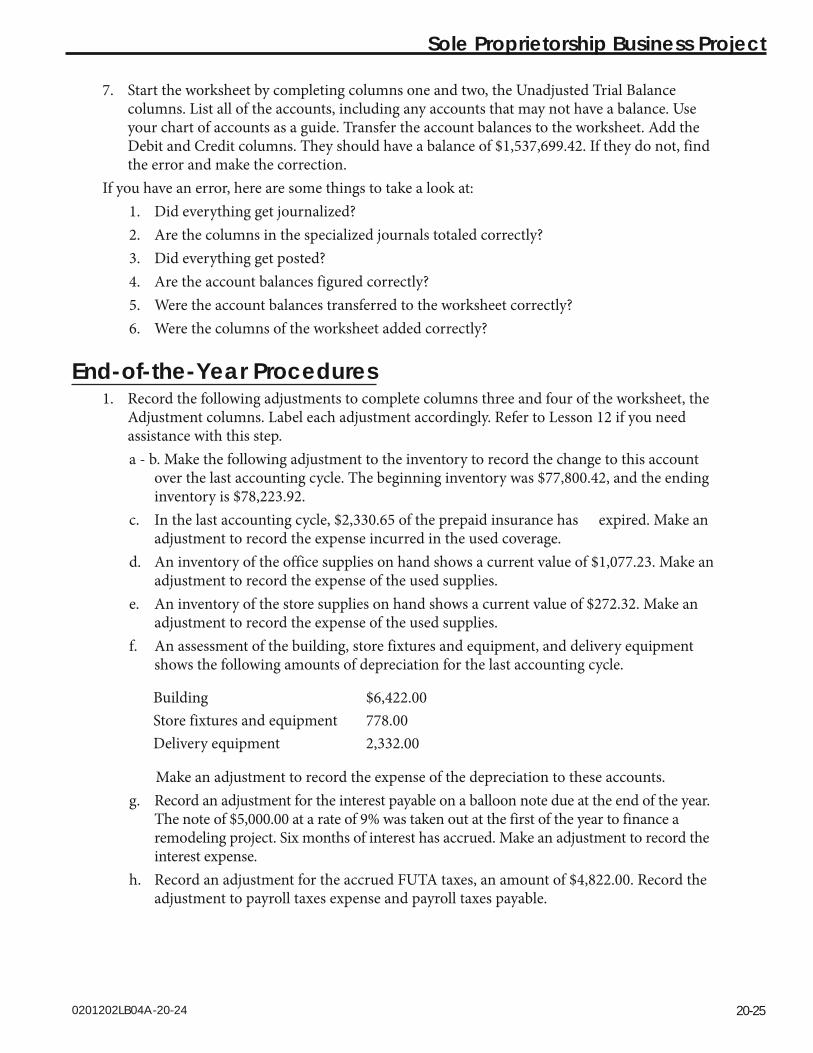

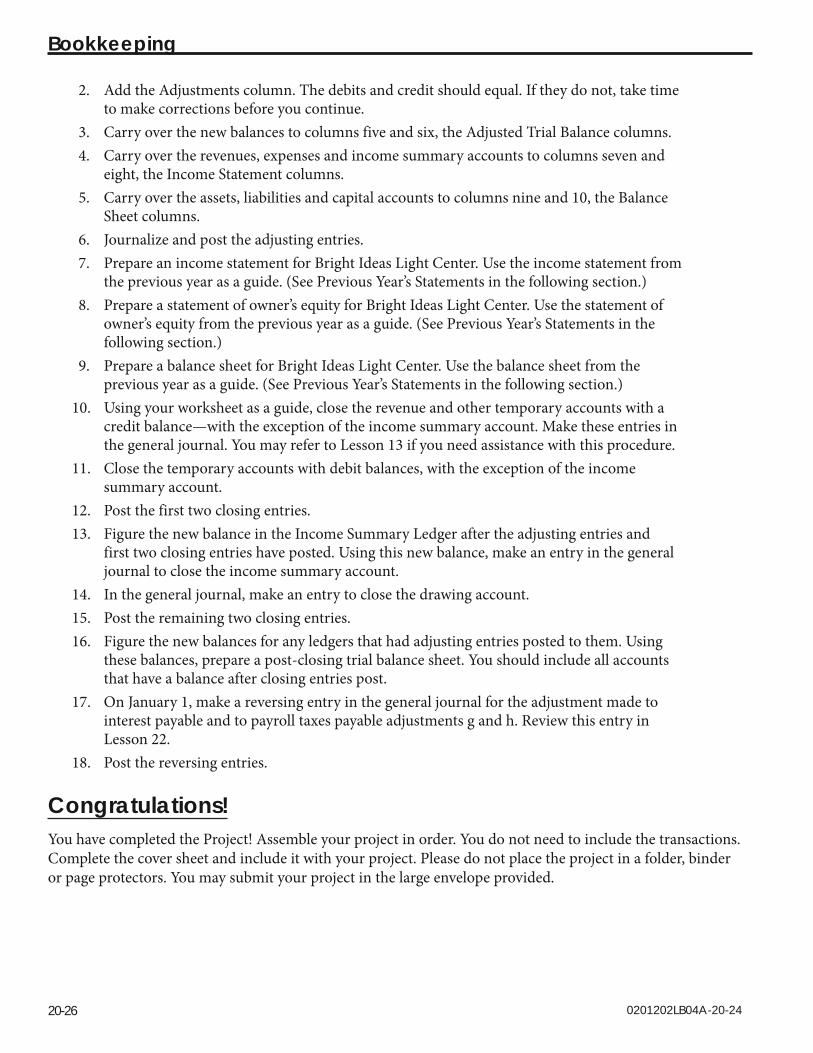

Background ....................................................................................................................................................... 4List of Transactions .......................................................................................................................................... 4End-of-the-Week Procedures ........................................................................................................................ 8End-of-the-Week Procedures ....................................................................................................................... 12End-of-the-Week Procedures ....................................................................................................................... 16End-of-the-Week Procedures ....................................................................................................................... 24End-of-the-Month Procedures .................................................................................................................... 24End-of-the-Year Procedures.......................................................................................................................... 25Congratulations! ............................................................................................................................................. 26

Bookkeeping

VI 0201202LB04A-24

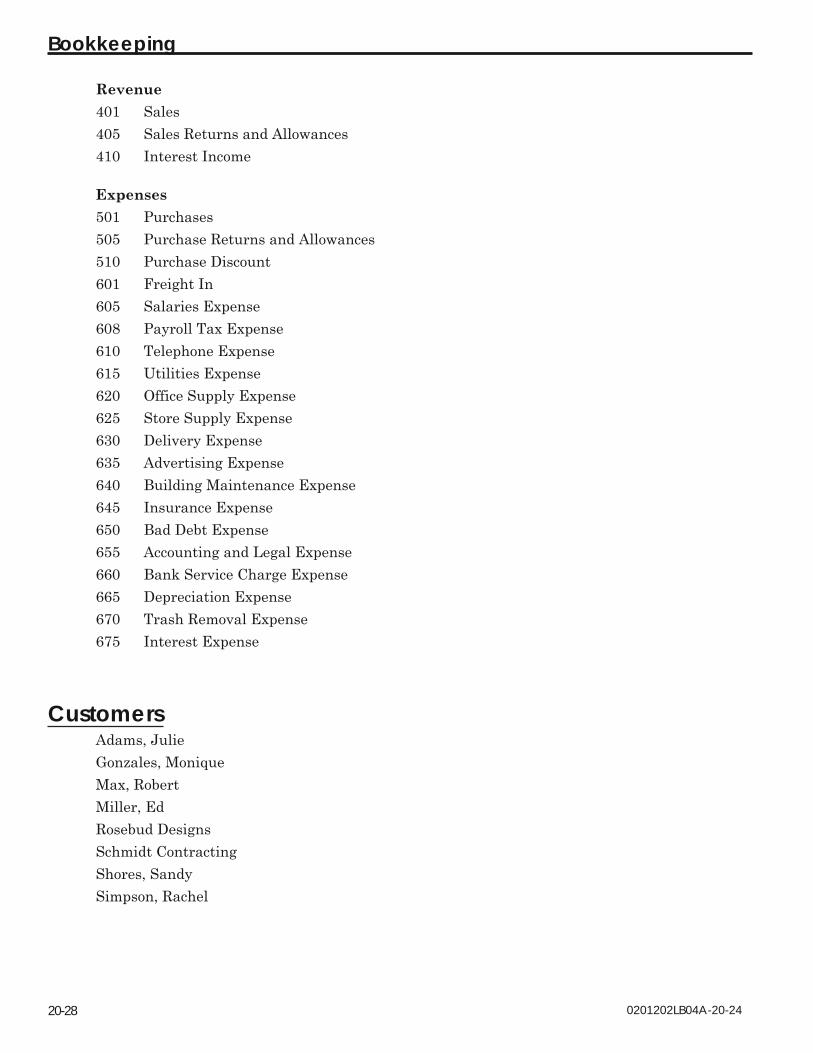

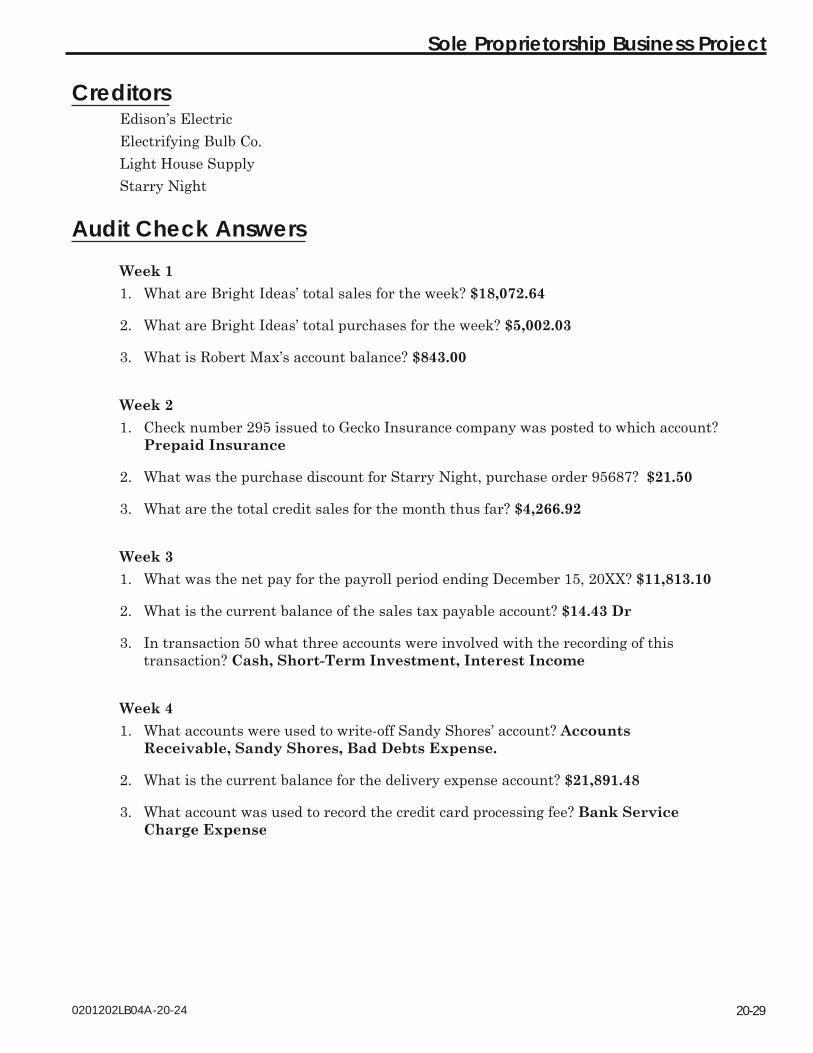

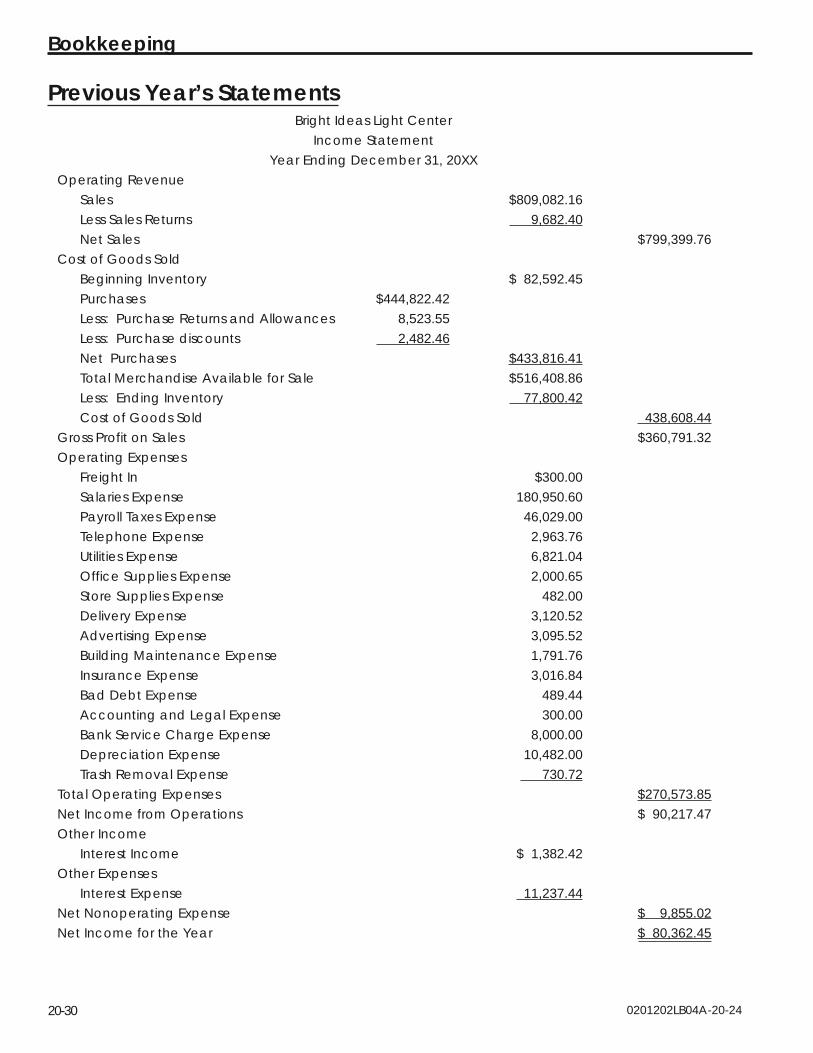

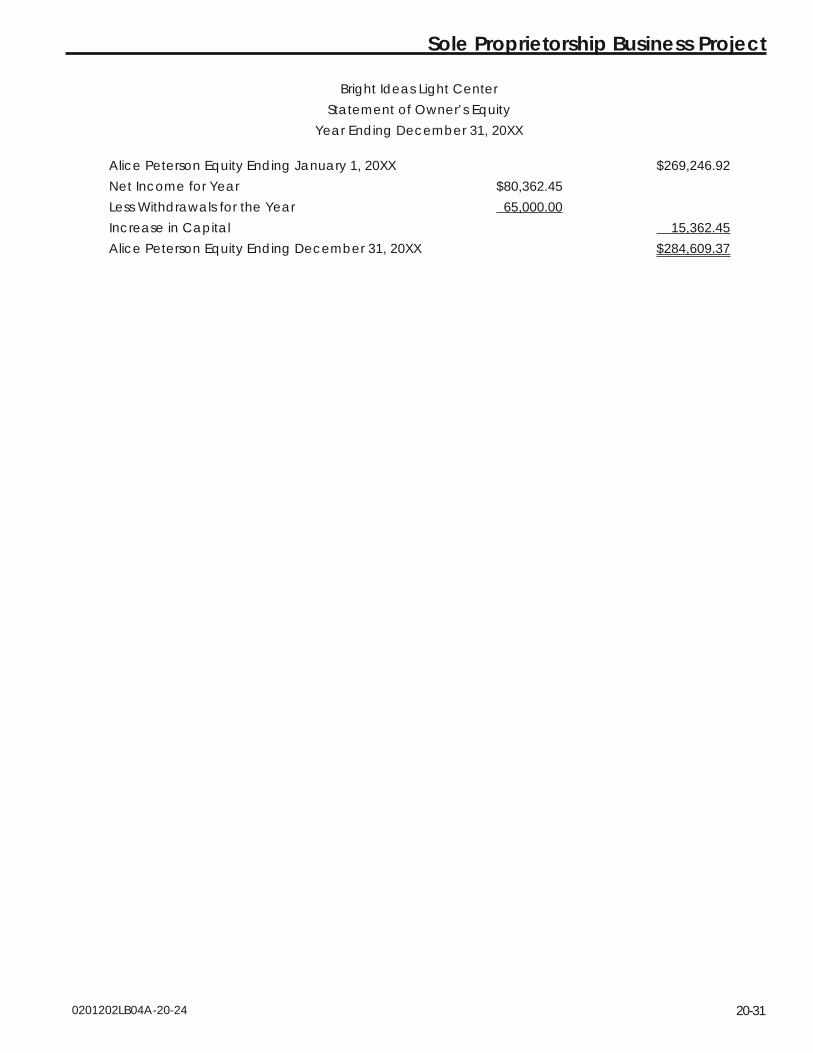

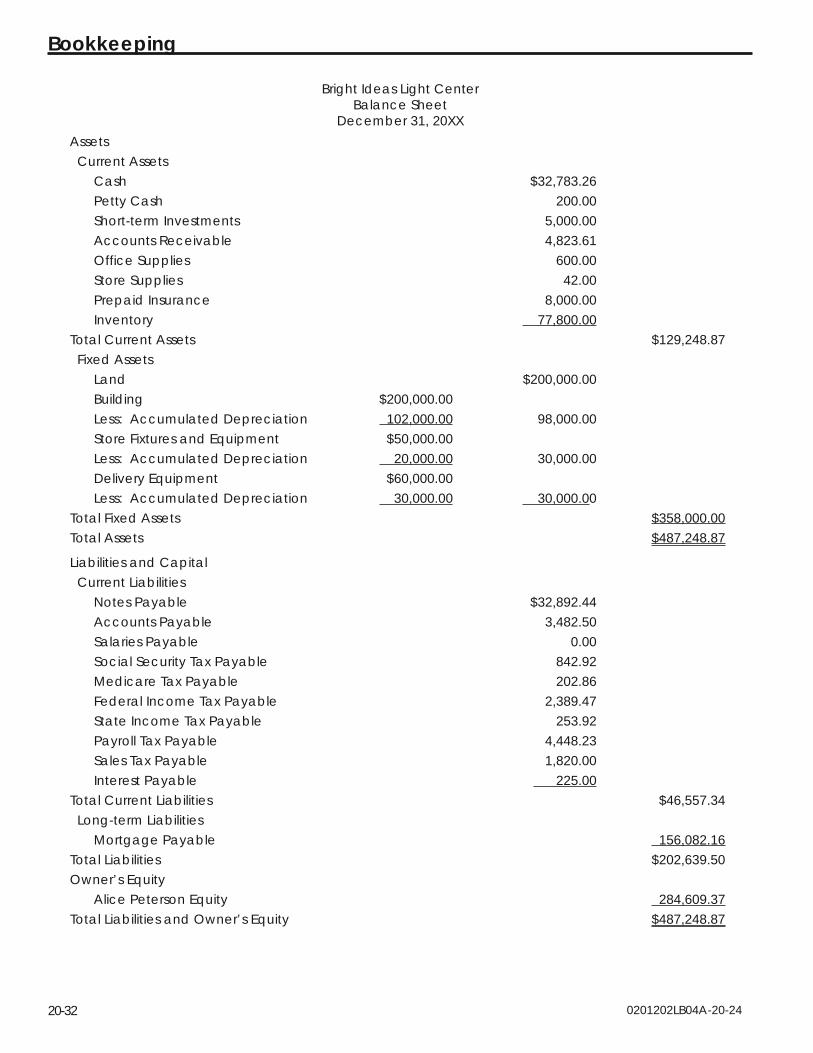

Chart of Accounts ........................................................................................................................................... 27Customers ........................................................................................................................................................ 28Creditors .......................................................................................................................................................... 29Audit Check Answers ..................................................................................................................................... 29Previous Year’s Statements ............................................................................................................................. 30

Answer KeyLesson 17 .......................................................................................................................................................................... 1

Practice Exercise 17-1 ...................................................................................................................................... 1Lesson 18 .......................................................................................................................................................................... 3

Practice Exercise 18-1 ...................................................................................................................................... 3Practice Exercise 18-2 ...................................................................................................................................... 4Practice Exercise 18-3 ...................................................................................................................................... 4

Lesson 19 .......................................................................................................................................................................... 5Practice Exercise 19-1 ...................................................................................................................................... 5Practice Exercise 19-2 ...................................................................................................................................... 6Practice Exercise 19-3 ...................................................................................................................................... 7Lesson 19 Just for Fun ...................................................................................................................................... 8

Lesson 17 Daily Bookkeeping Concepts

Step 1: Learning Objectives for Lesson 17After completing the instruction in this lesson, you will be trained to do the following:

● Work with the different daily accounts and receipts.

● Explain the difference between petty cash and change accounts.

● Prepare a daily summary of receipts.

● Journalize the daily summary.

Step 2: Lesson PreviewUp until now, we have discussed bookkeeping procedures as they apply to “specific accounting periods.” These accounting periods are usually months, quarters or years. There are, however, many businesses that must have some bookkeeping done every day. These daily bookkeeping procedures enable business owners, especially those in retail sales and service businesses, to keep a running tab on how their business is doing. You may be asked to prepare a daily summary of receipts for such an owner. This lesson will show you how to prepare that document. In addition, you will learn how to handle petty cash and change accounts, as well as cash receipts and sales. These items all work together to prepare the daily summary.

Step 3: Terms You Will Need to KnowHere are the bookkeeping terms you will learn about in this lesson:

● cash on hand

● cash receipts

● change bank

● petty cash fund

● petty cash slip

● cash over

● cash short

0201202LB04A-17-24

Bookkeeping

17-2

● collections on account

● total sales

● total cash on hand

● daily cash and sales summary

Step 4: Daily Cash and AccountsYou’ve probably had the experience of going into a store just minutes before closing to make a last minute purchase. You may have found that the clerk is busy with the end-of-the-day procedure—counting the cash in the register and recording and filing credit slips.

Keeping track of the daily cash and accounts is often the responsibility of the bookkeeper. This section will show you how to organize those receipts into a summary called the daily cash and sales summary.

You may wonder why a daily summary is so important. It is important for three reasons:1. It reconciles the daily sales with the amount of money brought in.2. It keeps employees honest—an employee who knows his or her cash drawer will be

reconciled at the end of the day will be careful to handle each sale accurately.3. It provides an easy-to-read source of information for journalizing the day’s transactions.

Let’s look at a sample daily cash and sales summary.

0201202LB04A-17-24

Daily Bookkeeping Concepts

17-3

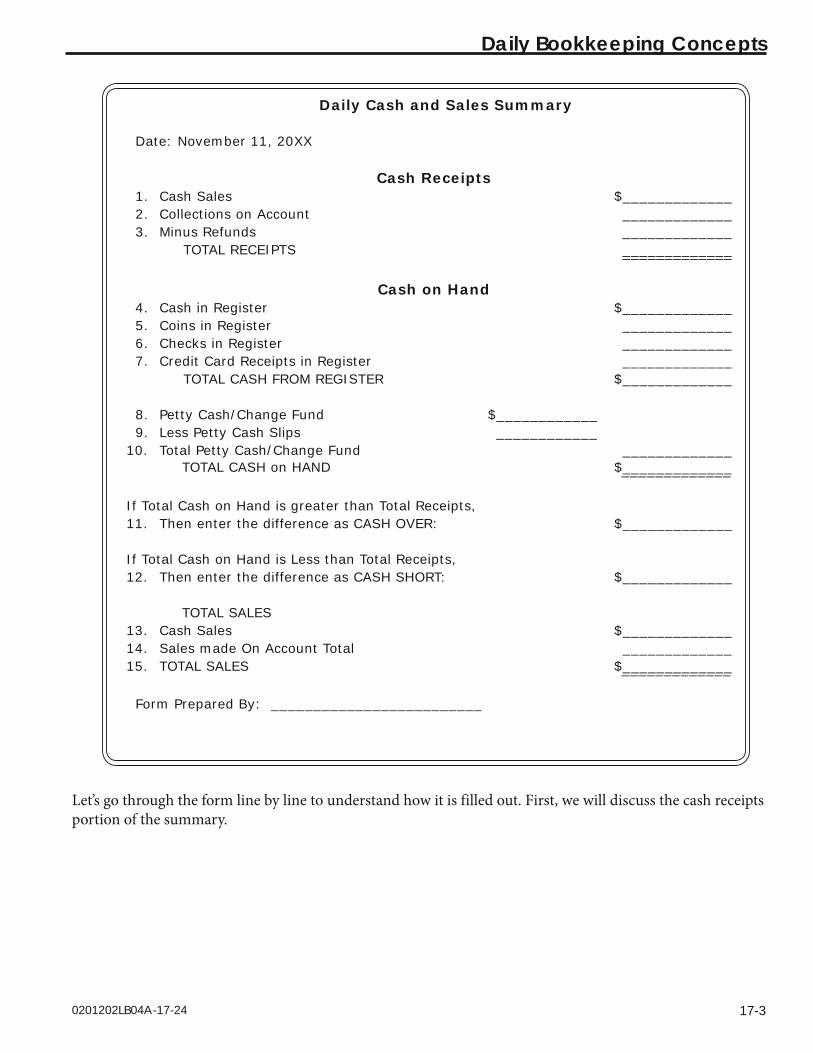

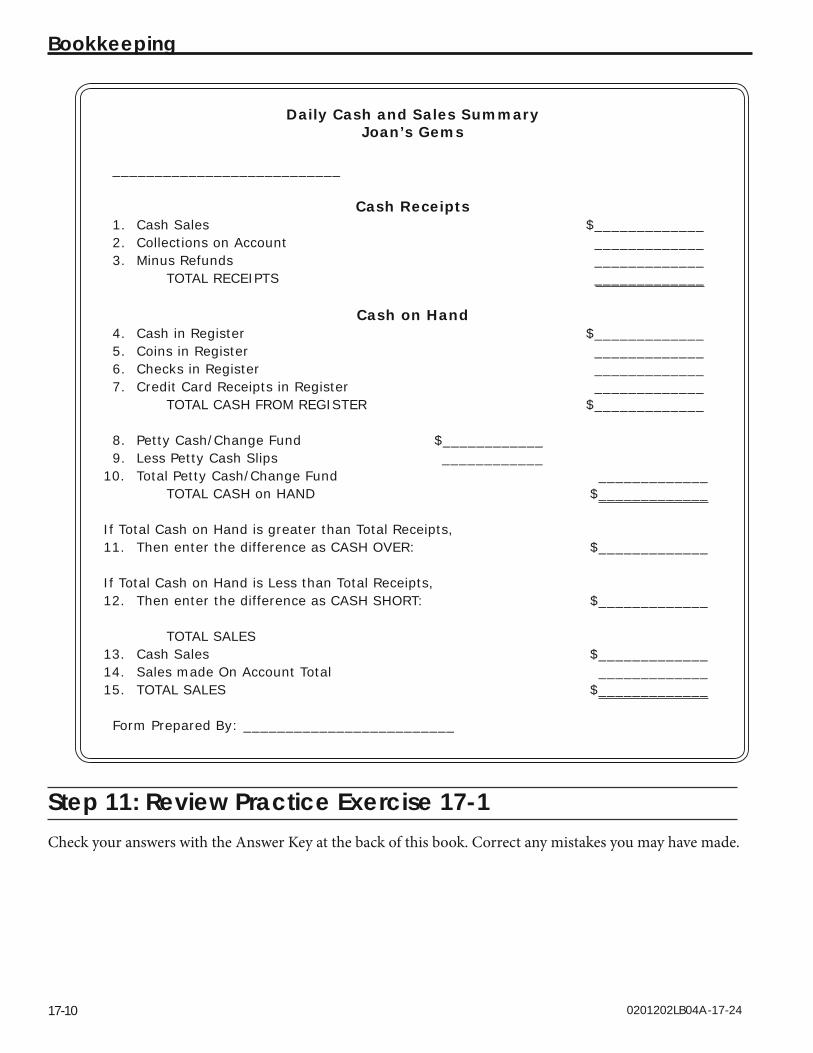

Daily Cash and Sales Summary

Date: November 11, 20XX

Cash Receipts1. Cash Sales $_____________2. Collections on Account _____________3. Minus Refunds _____________ TOTAL RECEIPTS _____________ _____________

Cash on Hand4. Cash in Register $_____________5. Coins in Register _____________6. Checks in Register _____________7. Credit Card Receipts in Register _____________ TOTAL CASH FROM REGISTER $_____________

8. Petty Cash/Change Fund $____________9. Less Petty Cash Slips ____________

10. Total Petty Cash/Change Fund _____________ TOTAL CASH on HAND $_____________ _____________

If Total Cash on Hand is greater than Total Receipts, 11. Then enter the difference as CASH OVER: $_____________

If Total Cash on Hand is Less than Total Receipts,12. Then enter the difference as CASH SHORT: $_____________

TOTAL SALES13. Cash Sales $_____________14. Sales made On Account Total _____________15. TOTAL SALES $_____________ _____________

Form Prepared By: _________________________

Let’s go through the form line by line to understand how it is filled out. First, we will discuss the cash receipts portion of the summary.

0201202LB04A-17-24

Bookkeeping

17-4

Step 5: Cash Receipts Portion of the SummaryThe cash receipts portion of the summary is where you list the total amount of money collected during the business day. The first line in this section is for listing the total amount of cash sales.

Cash SalesThe most common type of receipt for a cash sale is the paper receipt from a cash register. In many stores, the cash register tape records not only the exact item sold and its price, but also the time and date of the sale. Most cash registers keep a running total of everything rung up each day. At the end of the day, you can find the total amount of cash sales by pressing the correct button on the register. It will print out totals for items sold, cash refunds made and sales tax collected. Some smaller businesses may have a manual cash register or perhaps just a calculator. These businesses often issue handwritten receipts and keep carbon copies.

Whatever the method of recording the cash sales, the total must be calculated and entered on line 1 of the daily cash and sales summary at the end of each business day.

Cash sales (remember, cash sales include sales made with cash, checks or credit cards) are not the only transactions that require a receipt. Payments on accounts receivable must also be recorded.

Collections on AccountLine 2 of the daily cash and sales summary is for listing the amount of money collected on account. As discussed in the lesson on accounts receivable, some businesses extend credit to individuals and other businesses. Periodically, these customers who charge items from the shop will make payments on their accounts. They might pay by mail or they might come in and drop off a payment. Either way, any payment received must be accounted for on that day’s daily cash and sales summary as collections on account. To find this figure, simply total all the payments made on account for the day. In this case, you are not worried about who paid for which accounts. That will be listed in the accounts receivable ledgers. Here, you are looking simply for the total payments received for the day. Add up the receipts for these transactions and enter the amount on the appropriate line on the summary.

RefundsThe third item in the cash receipts section concerns refunds given during the day. If a customer buys an item and later returns it for a refund, the business deducts the amount of the refund from the cash receipts total. This is because when the customer returns the item, he is essentially unwinding the transaction—it’s as if the transaction never took place.

When a refund is issued, the business should fill out a credit slip (or ring up the refund on the cash register). Enter the total of all these refund receipts in the appropriate space on the daily summary.

Note: Do not include refunds made to accounts receivable accounts in this total. This section only concerns cash refunds.

Now that we have covered the cash receipts section of the daily summary. Let’s go on to the cash on hand section.

0201202LB04A-17-24

Daily Bookkeeping Concepts

17-5

Step 6: Cash on Hand Section of the Summary Cash on hand is the amount of money currently in the cash register, money drawer, safe or other storage area. This total includes all the cash and coins in the register, plus the total of the checks and credit card slips. The summary sheet has a space to enter each of these totals. The term “cash” on line 4 refers to the currency (paper money); “coins” refers to the change, such as quarters, dimes, nickels and pennies; “checks” refers to customers’ personal checks and money orders; “credit card receipts” refers to the total amount of credit card charge slips.

Simply total up all the items listed to calculate the total cash on hand, the amount of cash taken in on a single day. The next part of this section deals with petty cash and the change bank.

Step 7: Petty Cash and Change BankMost businesses have a standard change bank amount that is in the register each morning. This change bank is used for making change for customers during the day. Additionally, the business may have a certain amount of money designated for a petty cash fund. The petty cash fund is used by the business for incidental expenses during the day.

First, find out what the standard amounts for each of these are and enter the total amount on line 8 of the daily cash and sales summary. For example, the business may have $300 for the change bank and $200 for petty cash. You would then write $500 on line 8.

As mentioned above, the petty cash fund is used by the business to buy incidental items throughout the day. We will discuss the handling of petty cash in detail later in this lesson, but for now, let’s say that the business owner discovers she is out of staples for the stapler. She has ordered a large quantity from the local office supply store, but the order won’t be delivered until tomorrow. The business owner decides to use $2 from petty cash to buy enough staples to get through the day. She takes $2 out of the cash register and fills out a petty cash slip to indicate how much she took out.

At the end of the day, the total of the petty cash slips is entered on line 9 of the daily cash and sales summary.

Now deduct the amount of petty cash slips from the total petty cash/change fund amount you listed on line 8. Enter the result on line 10.

Now you deduct the amount on line 10 from the total cash from register amount. This gives you the total daily cash on hand. This amount should be the same as your total receipts in the cash receipts portion of the summary.

Step 8: Cash Short and Cash OverSometimes when you compare your total daily cash on hand with your total receipts, you will find the two numbers are different.

If the total daily cash on hand is greater than the total receipts, you have more money in the cash register or money drawer than you should (according to your receipts). This excess is called cash over.

0201202LB04A-17-24

Bookkeeping

17-6

If, on the other hand, your total daily cash on hand figure is less than the total receipts, you have less money in the cash register or money drawer than you should (according to your receipts). This shortfall is called cash short.

If you are over or short, the first step is to look for an error in one of four areas:1. The figures in the summary added incorrectly.2. A sale entered in the register incorrectly (check the cash register tape).3. Petty cash slips filled out or added incorrectly.4. Accounts receivable slips omitted or added incorrectly.

Another possible reason for a difference in these two amounts is that the clerk gave someone the wrong amount of change. This is difficult to discover.

If, after checking each of the items previously mentioned in the four steps discussed you are still over or short, enter the amount of the difference in the appropriate spot on the daily cash and sales summary.

The final section of the daily cash and sales summary concerns total sales, regardless of whether they were cash or on account.

Step 9: Total Sales Total sales is the combination of cash sales and sales made on account. To find the total sales for a business, take the cash sales and add to it any sales made on account. This allows you to see how many sales were made during the day. The sales made on account are usually recorded with some type of invoice or sales slip. Some cash registers will make a notation.

The reason the sales made on account are added in last is that these transactions do not affect your cash on hand. It is an important figure, however, and must be accounted for.

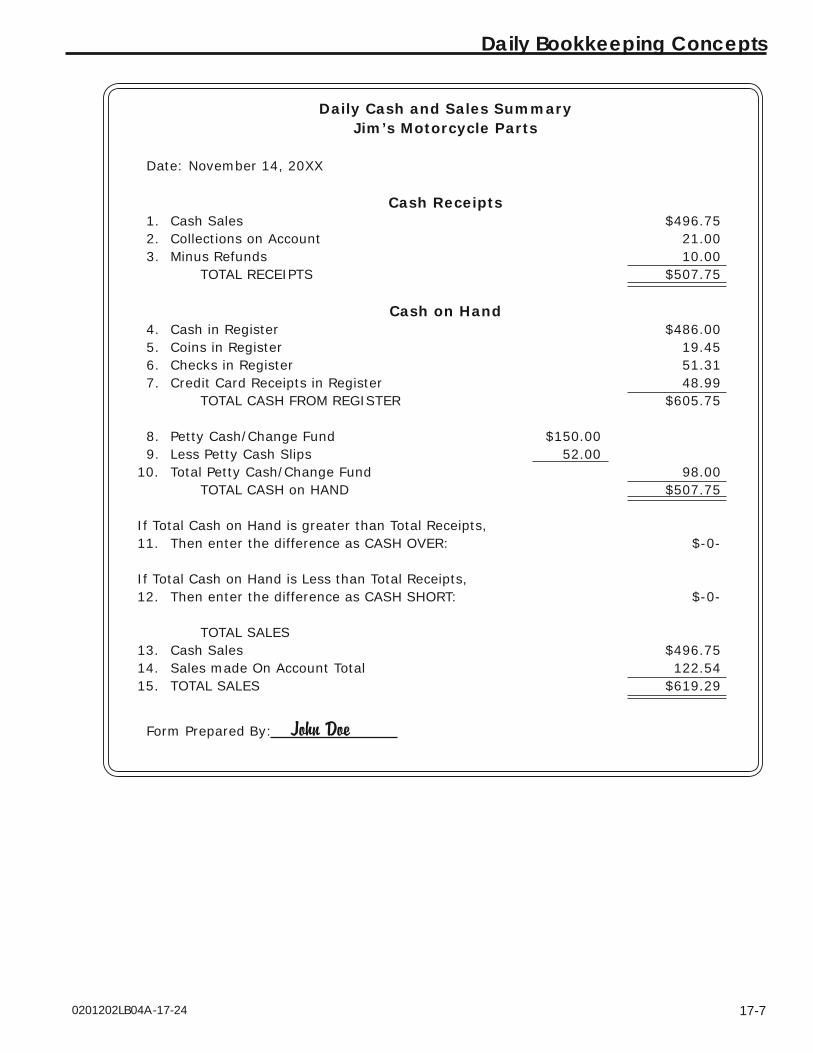

After you have figured total sales, the daily cash and sales summary is complete. Look at this sample of the completed daily cash and sales summary for Jim’s Motorcycle Parts.

0201202LB04A-17-24

Daily Bookkeeping Concepts

17-7

Daily Cash and Sales SummaryJim’s Motorcycle Parts

Date: November 14, 20XX

Cash Receipts1. Cash Sales $496.752. Collections on Account 21.003. Minus Refunds 10.00 TOTAL RECEIPTS $507.75

Cash on Hand4. Cash in Register $486.005. Coins in Register 19.456. Checks in Register 51.317. Credit Card Receipts in Register 48.99 TOTAL CASH FROM REGISTER $605.75

8. Petty Cash/Change Fund $150.00 9. Less Petty Cash Slips 52.00

10. Total Petty Cash/Change Fund 98.00 TOTAL CASH on HAND $507.75

If Total Cash on Hand is greater than Total Receipts, 11. Then enter the difference as CASH OVER: $-0-

If Total Cash on Hand is Less than Total Receipts,12. Then enter the difference as CASH SHORT: $-0-

TOTAL SALES13. Cash Sales $496.7514. Sales made On Account Total 122.5415. TOTAL SALES $619.29

Form Prepared By: John Doe

0201202LB04A-17-24

Bookkeeping

17-8

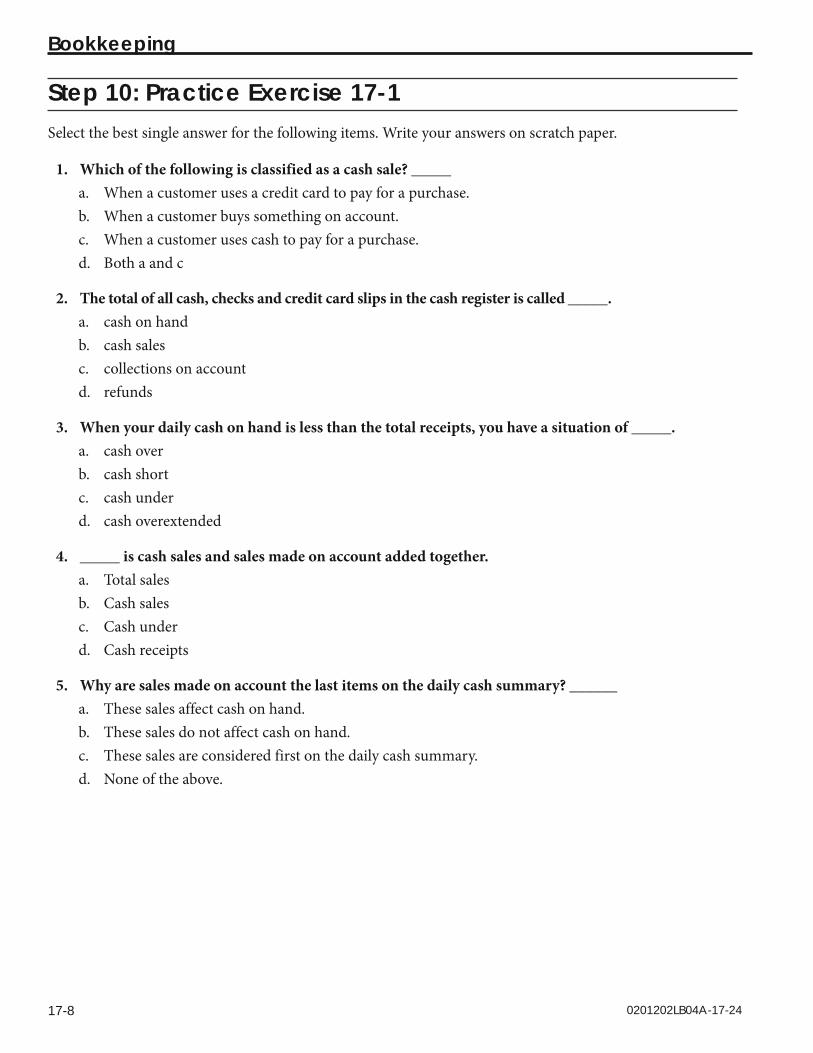

Step 10: Practice Exercise 17-1Select the best single answer for the following items. Write your answers on scratch paper.

1. Which of the following is classified as a cash sale? _____a. When a customer uses a credit card to pay for a purchase.b. When a customer buys something on account.c. When a customer uses cash to pay for a purchase.d. Both a and c

2. The total of all cash, checks and credit card slips in the cash register is called _____.a. cash on handb. cash salesc. collections on accountd. refunds

3. When your daily cash on hand is less than the total receipts, you have a situation of _____.a. cash overb. cash shortc. cash underd. cash overextended

4. _____ is cash sales and sales made on account added together.a. Total salesb. Cash salesc. Cash underd. Cash receipts

5. Why are sales made on account the last items on the daily cash summary? ______a. These sales affect cash on hand.b. These sales do not affect cash on hand.c. These sales are considered first on the daily cash summary.d. None of the above.

0201202LB04A-17-24

Daily Bookkeeping Concepts

17-9

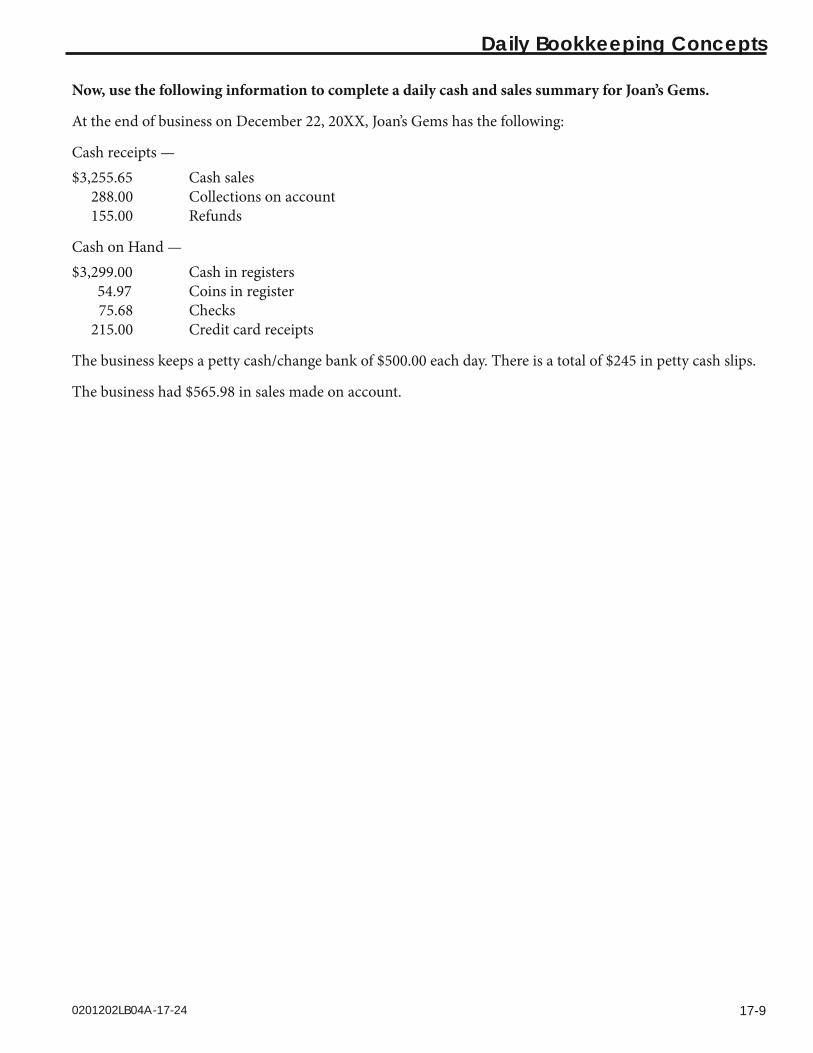

Now, use the following information to complete a daily cash and sales summary for Joan’s Gems.

At the end of business on December 22, 20XX, Joan’s Gems has the following:

Cash receipts —$3,255.65 Cash sales 288.00 Collections on account 155.00 Refunds

Cash on Hand —$3,299.00 Cash in registers 54.97 Coins in register 75.68 Checks 215.00 Credit card receipts

The business keeps a petty cash/change bank of $500.00 each day. There is a total of $245 in petty cash slips.

The business had $565.98 in sales made on account.

0201202LB04A-17-24

Bookkeeping

17-10

Daily Cash and Sales SummaryJoan’s Gems

___________________________

Cash Receipts1. Cash Sales $_____________2. Collections on Account _____________3. Minus Refunds _____________ TOTAL RECEIPTS _____________

Cash on Hand4. Cash in Register $_____________5. Coins in Register _____________6. Checks in Register _____________7. Credit Card Receipts in Register _____________ TOTAL CASH FROM REGISTER $_____________

8. Petty Cash/Change Fund $____________9. Less Petty Cash Slips ____________

10. Total Petty Cash/Change Fund _____________ TOTAL CASH on HAND $_____________

If Total Cash on Hand is greater than Total Receipts, 11. Then enter the difference as CASH OVER: $_____________

If Total Cash on Hand is Less than Total Receipts,12. Then enter the difference as CASH SHORT: $_____________

TOTAL SALES13. Cash Sales $_____________14. Sales made On Account Total _____________15. TOTAL SALES $_____________

Form Prepared By: _________________________

Step 11: Review Practice Exercise 17-1Check your answers with the Answer Key at the back of this book. Correct any mistakes you may have made.

0201202LB04A-17-24

Daily Bookkeeping Concepts

17-11

Step 12: Handling the Petty Cash/Change BankBusinesses often keep a small amount of cash on premises, to allow them to purchase miscellaneous supplies and keep change ready for the cash registers. The petty cash/change bank is a set amount of money kept on hand for this purpose. The petty cash/change bank is an important part of any business operation. There are three things to remember about these funds:

1. The petty cash/change bank must begin each day with the same amount of money in it.2. Whenever money is removed from petty cash, it must be accounted for with a petty cash slip

(also called a petty cash voucher).3. When change is made from the change bank, that money must be replaced. In other words,

clerks should “buy” change from the change bank—put in a $10 bill and remove two $5 bills, for example.

At the end of the day, the petty cash slips are used to journalize the money that went out from petty cash. Then the amount taken out is repaid by issuing a check to the person in charge of the petty cash fund so that the next day’s petty cash/change fund starts at the standard amount.

The Amount in the Petty Cash/Change BankAs we mentioned earlier, when a business opens each day, there will be a set amount of money that goes into the cash registers for making change and for making petty cash purchases. This money is known as the petty cash/change bank. Sometimes businesses have their petty cash in a separate place of its own—a box in the manager’s office, for example. Smaller businesses usually use the change bank as petty cash—if the business needs something and pays for it from petty cash, the clerk writes up a petty cash slip and takes the money from the register. In larger businesses, there is someone in charge of petty cash and change. If a clerk needs change, he must go to this person and “buy” it—putting in a $20 bill and getting back the change (a $10 and two $5 bills for example). In any case, at the end of the day, the petty cash/change bank must be brought back to its original amount.

It is important that the petty cash/change bank remains at a set amount. This makes it much easier to figure total cash on hand. By being able to subtract out the money you started the day with (the petty cash/change bank), you are able to figure how much money was taken in. For example, if you end the day with $600 in the register, and you know the petty cash/change bank is $100 every day, you are able to figure the total cash on hand as $500. Imagine if the petty cash/change bank was different each day. If you assumed it was $100, but today it was only $67, what would that do to your total cash on hand figures?

Another important part of managing the petty cash/change bank is keeping track of the amount of money that went out of the petty cash account during the day.

0201202LB04A-17-24

Bookkeeping

17-12

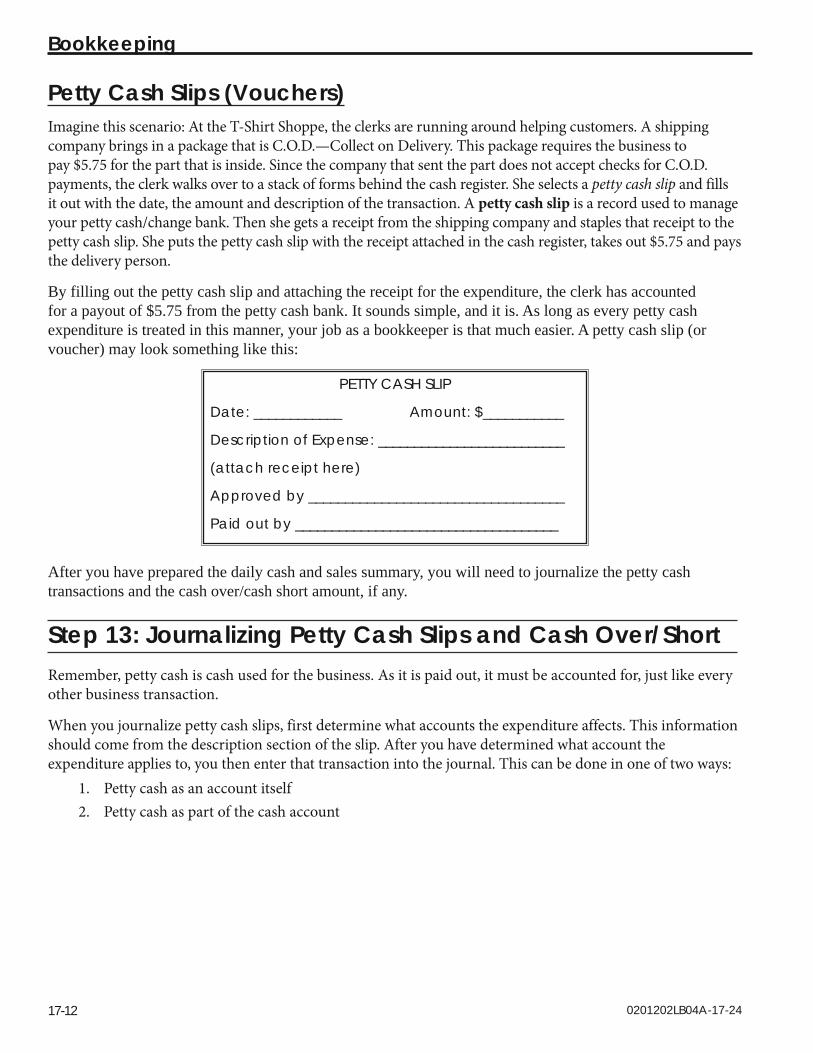

Petty Cash Slips (Vouchers)Imagine this scenario: At the T-Shirt Shoppe, the clerks are running around helping customers. A shipping company brings in a package that is C.O.D.—Collect on Delivery. This package requires the business to pay $5.75 for the part that is inside. Since the company that sent the part does not accept checks for C.O.D. payments, the clerk walks over to a stack of forms behind the cash register. She selects a petty cash slip and fills it out with the date, the amount and description of the transaction. A petty cash slip is a record used to manage your petty cash/change bank. Then she gets a receipt from the shipping company and staples that receipt to the petty cash slip. She puts the petty cash slip with the receipt attached in the cash register, takes out $5.75 and pays the delivery person.

By filling out the petty cash slip and attaching the receipt for the expenditure, the clerk has accounted for a payout of $5.75 from the petty cash bank. It sounds simple, and it is. As long as every petty cash expenditure is treated in this manner, your job as a bookkeeper is that much easier. A petty cash slip (or voucher) may look something like this:

PETTY CASH SLIP

Date: ____________ Amount: $___________

Description of Expense: __________________________

(attach receipt here)

Approved by ___________________________________

Paid out by ____________________________________

After you have prepared the daily cash and sales summary, you will need to journalize the petty cash transactions and the cash over/cash short amount, if any.

Step 13: Journalizing Petty Cash Slips and Cash Over/ShortRemember, petty cash is cash used for the business. As it is paid out, it must be accounted for, just like every other business transaction.

When you journalize petty cash slips, first determine what accounts the expenditure affects. This information should come from the description section of the slip. After you have determined what account the expenditure applies to, you then enter that transaction into the journal. This can be done in one of two ways:

1. Petty cash as an account itself2. Petty cash as part of the cash account

0201202LB04A-17-24

Daily Bookkeeping Concepts

17-13

If you have a system where there is a petty cash account, then you journalize the slips like this:

General Journal

Date Description P/R Dr Cr

Supplies 5 75 Petty Cash 5 75

Enter each slip individually, and pay close attention to the account each one affects.

You then repay your petty cash account by taking money from the cash account and putting it into the petty cash account. If you have a total of $75 in petty cash expenditures and the account normally has $150 in it, you need to repay the difference so the account stays at $150.

The journal entries for a petty cash purchase of $5.75 for office supplies would look like this:

General Journal

Date Description P/R Dr Cr

Office Supplies 5 75 Petty Cash 5 75Petty Cash 5 75

Cash 5 75

0201202LB04A-17-24

Bookkeeping

17-14

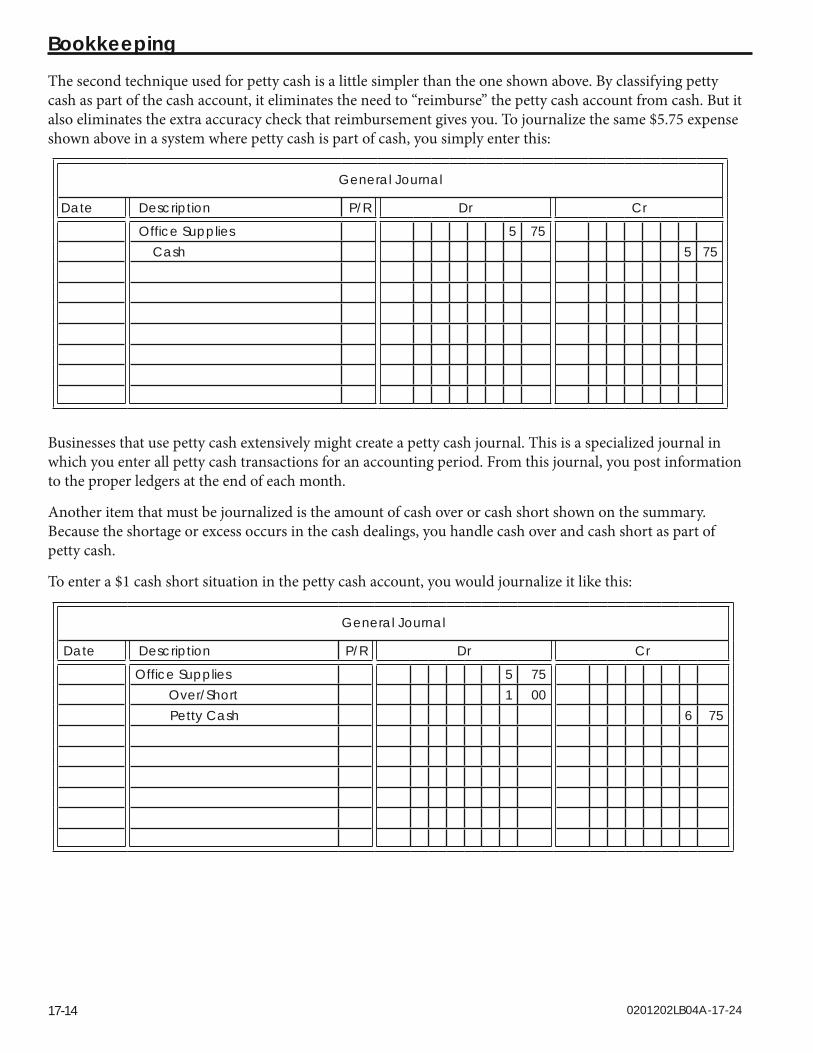

The second technique used for petty cash is a little simpler than the one shown above. By classifying petty cash as part of the cash account, it eliminates the need to “reimburse” the petty cash account from cash. But it also eliminates the extra accuracy check that reimbursement gives you. To journalize the same $5.75 expense shown above in a system where petty cash is part of cash, you simply enter this:

General Journal

Date Description P/R Dr Cr

Office Supplies 5 75 Cash 5 75

Businesses that use petty cash extensively might create a petty cash journal. This is a specialized journal in which you enter all petty cash transactions for an accounting period. From this journal, you post information to the proper ledgers at the end of each month.

Another item that must be journalized is the amount of cash over or cash short shown on the summary. Because the shortage or excess occurs in the cash dealings, you handle cash over and cash short as part of petty cash.

To enter a $1 cash short situation in the petty cash account, you would journalize it like this:

General Journal

Date Description P/R Dr Cr

Office Supplies 5 75 Over/Short 1 00 Petty Cash 6 75

0201202LB04A-17-24

Daily Bookkeeping Concepts

17-15

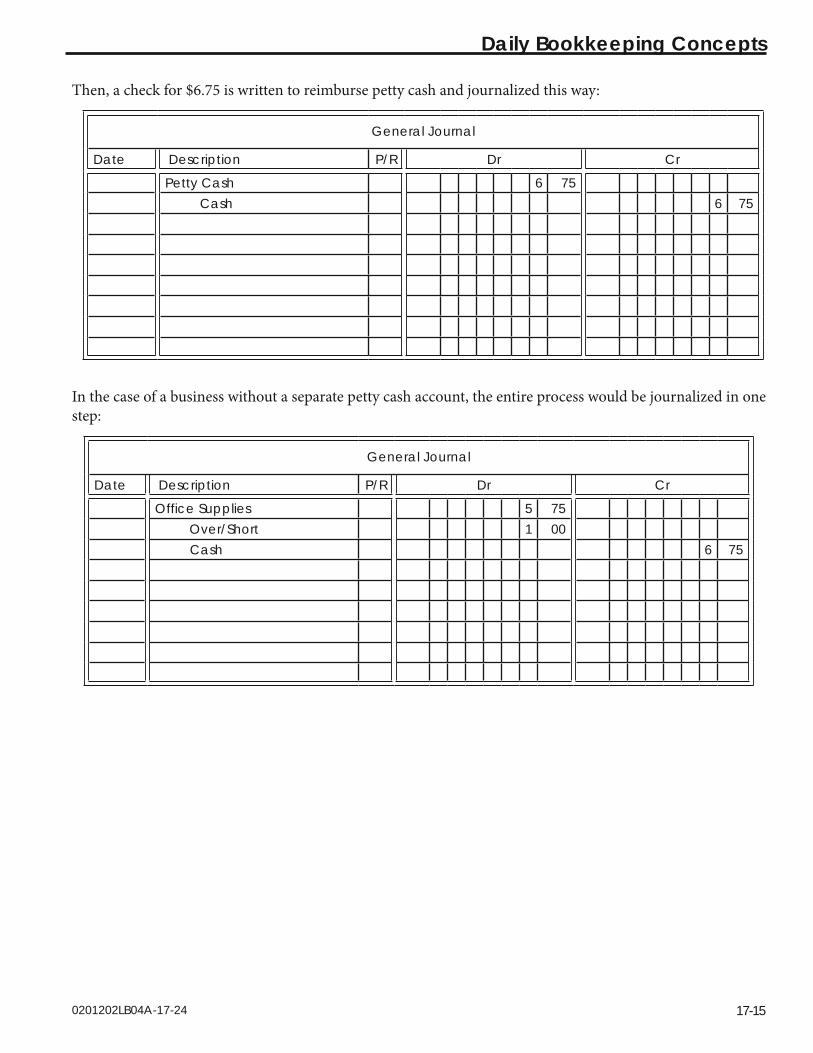

Then, a check for $6.75 is written to reimburse petty cash and journalized this way:

General Journal

Date Description P/R Dr Cr

Petty Cash 6 75 Cash 6 75

In the case of a business without a separate petty cash account, the entire process would be journalized in one step:

General Journal

Date Description P/R Dr Cr

Office Supplies 5 75 Over/Short 1 00 Cash 6 75

0201202LB04A-17-24

Bookkeeping

17-16

Now, in the case of a cash over entry, you would make the same entries, except you would change the entry on the over/short line to a credit. To find the total for cash reimbursement, you subtract the over amount from the expense. For example, in the case of a $5.75 office supply expense and a $1 cash over situation, your journal entry would look like this:

General Journal

Date Description P/R Dr Cr

Office Supplies 5 75 Over/Short 1 00 Cash 4 75

If there is a separate petty cash account, the entry would look like this:

General Journal

Date Description P/R Dr Cr

Office Supplies 5 75 Over/Short 1 00 Petty Cash 4 75

0201202LB04A-17-24

Daily Bookkeeping Concepts

17-17

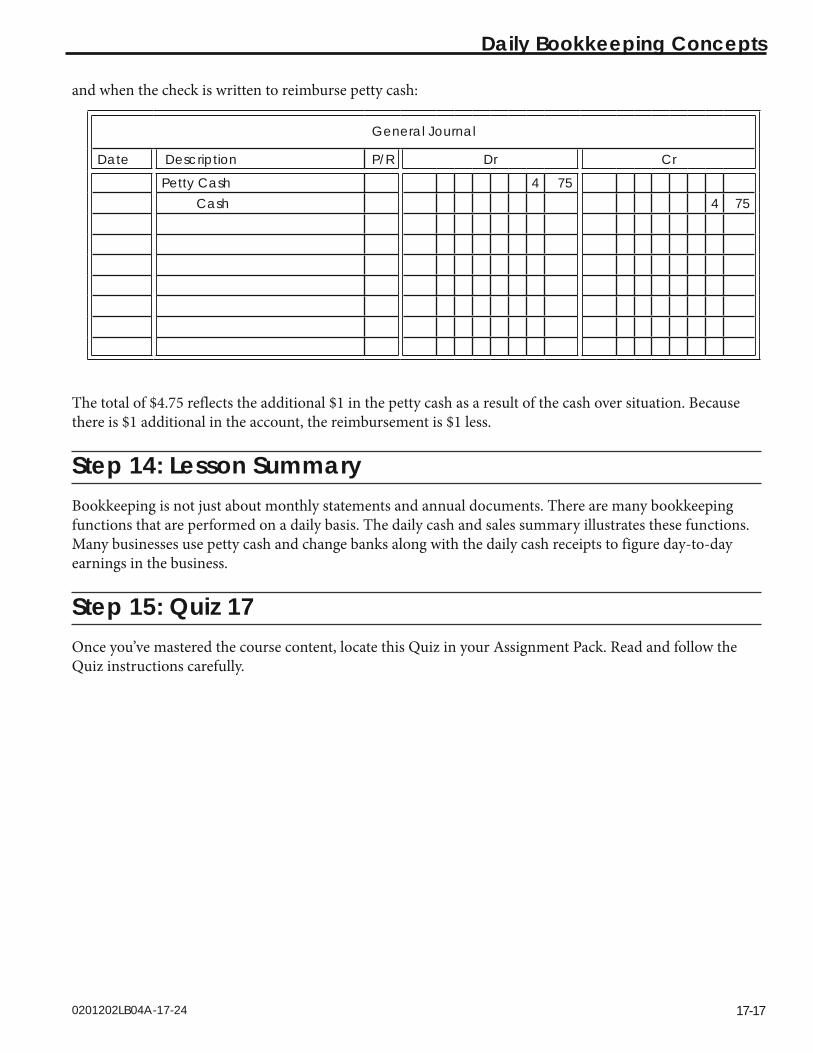

and when the check is written to reimburse petty cash:

General Journal

Date Description P/R Dr Cr

Petty Cash 4 75 Cash 4 75

The total of $4.75 reflects the additional $1 in the petty cash as a result of the cash over situation. Because there is $1 additional in the account, the reimbursement is $1 less.

Step 14: Lesson SummaryBookkeeping is not just about monthly statements and annual documents. There are many bookkeeping functions that are performed on a daily basis. The daily cash and sales summary illustrates these functions. Many businesses use petty cash and change banks along with the daily cash receipts to figure day-to-day earnings in the business.

Step 15: Quiz 17Once you’ve mastered the course content, locate this Quiz in your Assignment Pack. Read and follow the Quiz instructions carefully.

0201202LB04A-17-24

Bookkeeping

17-18

Lesson 18 Partnerships, Corporations and

Non-profit Organizations

Step 1: Learning Objectives for Lesson 18After completing the instruction in this lesson, you will be trained to do the following:

● Define partnerships, and explain the various characteristics of the partnership arrangement.

● Account for partners’ shares in assets and liabilities, as well as in drawing accounts.

● Explain the differences between a partnership and a corporation.

● Explain the characteristics of a non-profit organization and how it maintains tax-exempt status.

Step 2: Lesson Preview So far in this course, we have covered bookkeeping from the view of the sole proprietorship; that is, businesses with one owner and a single drawing account. This lesson will move into three more areas of ownership—partnerships, corporations and non -profit organizations.

A partnership is defined as the association of two or more persons who agree to run a business for profit. The partners in this agreement enter into the arrangement willingly. A corporation divides personal and business finances by establishing the company as a separate legal entity. Owners of a corporation are called shareholders because they own a “share” of the company.

Corporations have certain advantages over partnerships. A corporation is continuous (it doesn’t expire upon the death of shareholders). A partnership’s profit is taxed as personal income, and owners are subject to self-employment taxes. In a corporation, salaries (not profits) are taxed, which can result in a substantial tax savings. And, corporations have more options when trying to raise money. However, partnerships have some advantages not enjoyed by corporations. They are easier (and less costly) to establish. And partnerships aren’t required to carry unemployment insurance taxes (at the current rate, this can save partners up to $434 per partner per year).

A non-profit organization works for a public interest with no intent to earn a profit. Non-profits are structured similarly to corporations, but any profit earned is invested back in the company, rather than given to shareholders. For this reason, the non-profit enjoys certain tax advantages.

As you might imagine, bookkeeping procedures differ, depending on whether the company you work for is a partnership, corporation or non-profit organization. The lesson will cover bookkeeping concepts and procedures for all three business types.

0201202LB04A-18-24

Bookkeeping

18-2

Step 3: Terms You Will Need to Know Here are the bookkeeping terms you will learn about in this lesson:

● board of directors ● partnership ● checklist of required schedules ● par value ● chief executive officer (CEO) ● percentage interest ● common factor ● percentage method ● common stock ● preferred stock ● co-owners ● retained earnings ● corporations ● shareholders ● distribution of net income statement ● statement of program services accomplishments ● dividends ● statement regarding other IRS filings and tax compliance ● goodwill ● stock ● goodwill fee ● stock exchange ● incorporated ● stockholders ● mutual agents ● treasury stock ● non-profit organization

Step 4: Partnerships As explained in the introduction to this lesson, partnerships are agreements between two or more people who enter into a business for profit. Although every partnership agreement is unique, there is one main characteristic of a partnership that is always present—the concept of co-ownership.

Co-ownership When a partnership is formed, all parties in the partnership become co-owners of the business. That is, if two people decide to enter into a 50-50 partnership, they each own half of the business. The 50-50 refers to the percent owned by each partner. Percentages do not need to be equal. Every partner must own something, and the total must equal 100. For example, a 40-30-30 partnership gives a larger share of the business to the first partner and equal shares to the other two partners. The total adds up to 100 (signifying 100 percent of the company).

The amount of the business a partner owns is known as percentage interest. The percentage interest helps determine a partner’s share of profit and loss and liability. Percentage interest does not, however, affect the next characteristic—mutual agents.

No matter how much a partner owns (how big his or her percentage interest in the company is), each partner can make decisions for the entire firm. This is known as the concept of mutual agents. These decisions include entering into binding contracts, as long as the contracts lie in the normal scope of the firm’s business. A partner in the Rock Hard Gym and Health Club could sign a contract to purchase exercise equipment, for example. However, if the equipment was not normally used in a health club, the partner would not have the authority to enter into a binding contract.

0201202LB04A-18-24

Partnerships, Corporations and Non-profit Organizations

18-3

Because a partnership involves people, the length of the partnership agreement can vary. People change, and situations change. As changes occur, the establishment or dissolution of partnerships takes place.

There are some elements of the partnership that must always be in writing. These include percentage interest of each partner, pay-out information and the length of the partnership.

Having the agreement in writing ensures that the terms of the agreement are understood by all parties involved and eliminates possible misunderstandings.

Each partner in a business is personally liable for the debts the partnership incurs while that partner is associated with the business. This is a very important concept. Partners are not shielded by the business, and if a partner leaves the business, he or she is still personally responsible for the share of debt incurred by a business while he or she was a partner.

Additionally, when a partner leaves a firm, he must give adequate public notice of his departure. This is the only way he can keep from being held liable for debts incurred after he leaves.

As the bookkeeper for a partnership, you will be asked to figure each partner’s ownership of liabilities and assets.

Step 5: A Partner’s Interest As explained previously, percentage interest is the amount of a business owned by a partner. This is the figure that you, the bookkeeper, will use to figure how much each partner owes, earns and is responsible for as far as the business finances go.

The percent interest can be broken down into a ratio that is often used to determine division of net income or net loss in a partnership. To figure the ratio, you find the greatest common factor of the percent interest figures. In a 25-25-50 partnership, the greatest common factor (the largest number that can be evenly divided into each of the percentage interest figures) is 25. And 25 goes into 25 once and into 50 twice. The ratio, therefore, is 1:1:2.

Transferring Interest In a partnership, each partner owns some part of the business, and all the partners’ shares added up equal 100 percent of the business. That means there is no portion of the business available to new investors. This doesn’t stop new partners from being able to buy into the firm. Existing partners can sell a percentage of their percent interest. This allows new partners to join.

For example, say Company A has three partners: Bob, Jim and Chuck. Bob owns 50 percent of the company. Jim and Chuck own 25 percent each. Bob decides to sell Aaron half of his interest. Well, half of Bob’s 50 percent is 25 percent of the entire business. After Bob sells Aaron 25 percent of the business, all four partners are now equal.

Some partnership agreements require all partners to agree to allow new partners to buy into the company; some do not. Most of the time, partners are allowed to sell their percentage for whatever sum they wish, as long as the buyer pays at least what the percentage is worth to the partner. If Bob’s share of the business was worth $50,000, he wouldn’t want to sell half of his share for $10,000 (it’s worth $25,000).

0201202LB04A-18-24

Bookkeeping

18-4

Sometimes, new partners have to pay a fee to join a company. This goodwill fee reduces the amount of percentage interest they acquire. Let’s discuss this concept in more detail.

Goodwill When a company offers quality products or services, it doesn’t take long for the word to get around. Newspapers sometimes take surveys to find the best restaurant, the best night club or the best hardware store. When people think a company delivers quality, that increases that company’s reputation. Goodwill means that a company has a good reputation. It is an intangible asset that adds value to a company. Sometimes, a new partner might be charged a fee for joining a company with a good reputation. This fee is called a goodwill fee.

Franchises take advantage of goodwill. If you want a hamburger, there are several fast food outlets whose names might pop into your head. If you need building supplies or a plumber, the same thing might happen. Whatever company’s name pops into your head probably works the hardest to get your business. That may or may not be good, but it does increase sales.

For example, working harder for your business might mean all-out advertising blitzes designed to drive the company name into the customer’s head. On the other hand, it could be subtle and the result of local word of mouth (“The best at what you need is Company A.... My brother had them do some work, and it was excellent.”).

Many franchisers charge franchise fees. Whether a company charges goodwill fees or franchise fees, the fees for an initial investment must be entered into the books. Let’s look at how you would journalize this for the investor.

General Journal Page 1

Date Description P/R Dr Cr1 5 Cash 1 0 0 0 0 0 00

Goodwill 1 0 0 0 0 00I.M. Investor, Capital 9 0 0 0 0 00

Initial Investment

As you can see, the investor received $90,000 worth of capital for his $100,000 investment. He is relying on the company growing and making money for him to recoup the $10,000 goodwill fee.

0201202LB04A-18-24

Partnerships, Corporations and Non-profit Organizations

18-5

When the company receives a goodwill fee, the other partners see their capital increase. Suppose I.M. Investor bought into a company owned by Jon Dyer. Dyer’s journal would look something like this, if Dyer started out with $500,000 cash in the business:

General Journal Page 1

Date Description P/R Dr Cr1 5 Cash 5 0 0 0 0 0 00

Goodwill 1 0 0 0 0 00Dyer, Capital 5 1 0 0 0 0 00

Initial Investment

Many bookkeeping tasks are the same for sole proprietorships and partnerships. The main difference is the capital accounts.

Capital Accounts With partnerships, there are two or more people involved in a business. Each partner has contributed a different amount of equity or capital to the business. As the bookkeeper, you will need to keep track of the equity and capital amounts each partner holds in the business. This information is kept in individual capital accounts for each partner.

Note: When a business becomes a partnership, you should allow a bookkeeper to set up the different accounts for the business. The bookkeeper is better prepared to perform this task. Use the balance sheet provided by the bookkeeper to establish the amounts in each account, and then go from there.

0201202LB04A-18-24

Bookkeeping

18-6

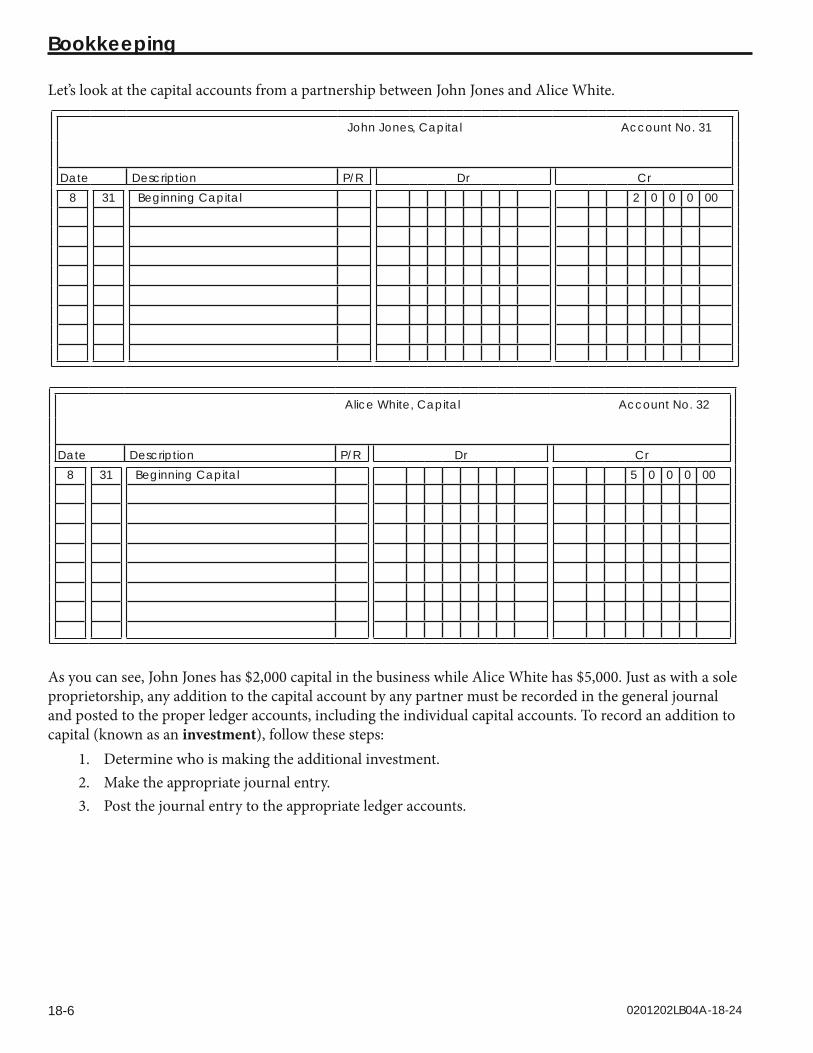

Let’s look at the capital accounts from a partnership between John Jones and Alice White.

John Jones, Capital Account No. 31

Date Description P/R Dr Cr8 31 Beginning Capital 2 0 0 0 00

Alice White, Capital Account No. 32

Date Description P/R Dr Cr8 31 Beginning Capital 5 0 0 0 00

As you can see, John Jones has $2,000 capital in the business while Alice White has $5,000. Just as with a sole proprietorship, any addition to the capital account by any partner must be recorded in the general journal and posted to the proper ledger accounts, including the individual capital accounts. To record an addition to capital (known as an investment), follow these steps:

1. Determine who is making the additional investment. 2. Make the appropriate journal entry. 3. Post the journal entry to the appropriate ledger accounts.

0201202LB04A-18-24

Partnerships, Corporations and Non-profit Organizations

18-7

Let’s take our previous example of initial capital investment by Mr. Jones and Ms White. Imagine that for this situation, the amounts invested represent additional capital. With that in mind, we would record Mr. Jones’ new investment like this:

General Journal Page 8

Date Description P/R Dr Cr1 31 Cash 2 0 0 0 00

John Jones, Capital 2 0 0 0 00Additional Investment

A company that uses specialized journals would enter this in the Cash Receipts Journal since cash is being taken by the company.

Additional Investment The journal entries would then be posted to the ledger. The first account is the cash account. You enter a $2,000 debit. Then, you go to John Jones’ capital account and credit it $2,000. Investments can take the form of cash, hardware, inventory or any number of things the company needs.

Other factors affect capital accounts. Net income and drawing accounts both need to be accounted for in individual capital accounts. This is done in the same manner as it would be in a sole proprietorship—through the closing of the books process. We’ll get to that process later in this lesson.

One difference between a partnership and a sole proprietorship is that a partnership changes the Assets = Liabilities + Capital equation. It doesn’t really change the numbers, but the order is a bit different. Remember, you have more than one person involved with the business, so now you have to account for as many partners as there are in the partnership. For example, if a business has three partners, the assets formula looks like this:

Assets = Liabilities + Capital Partner #1 + Capital Partner #2 + Capital Partner #3

0201202LB04A-18-24

Bookkeeping

18-8

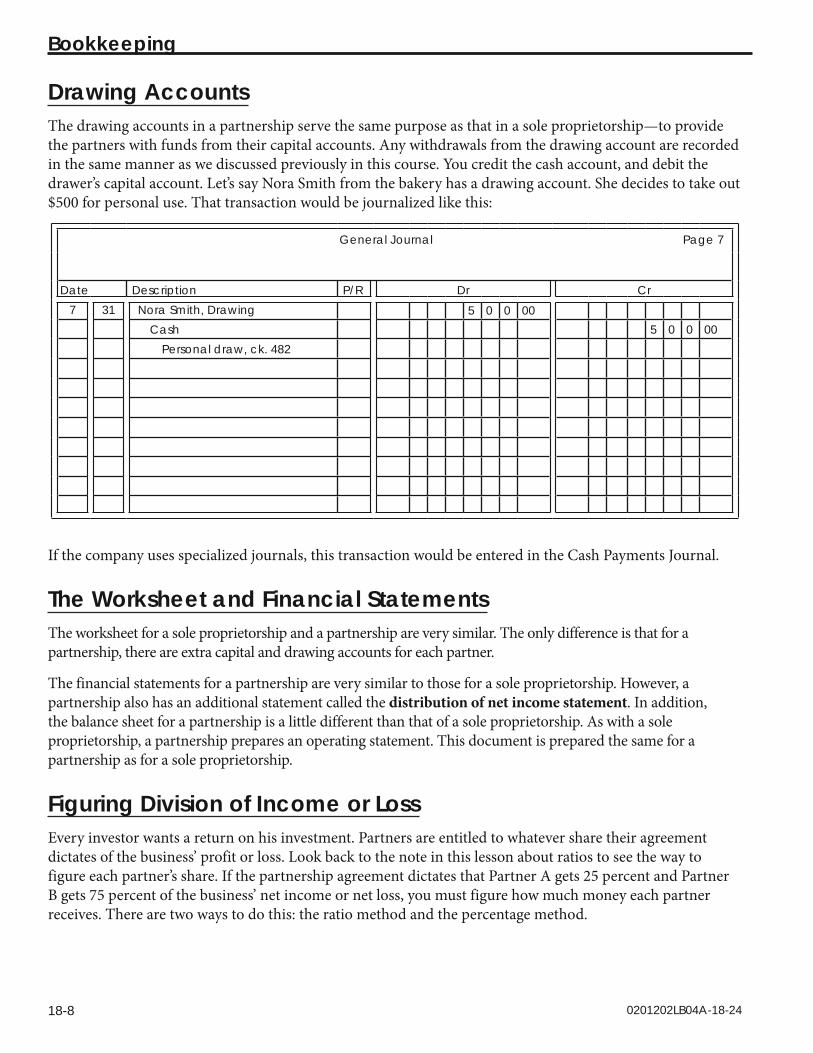

Drawing Accounts The drawing accounts in a partnership serve the same purpose as that in a sole proprietorship—to provide the partners with funds from their capital accounts. Any withdrawals from the drawing account are recorded in the same manner as we discussed previously in this course. You credit the cash account, and debit the drawer’s capital account. Let’s say Nora Smith from the bakery has a drawing account. She decides to take out $500 for personal use. That transaction would be journalized like this:

General Journal Page 7

Date Description P/R Dr Cr7 31 Nora Smith, Drawing 5 0 0 00

Cash 5 0 0 00Personal draw, ck. 482

If the company uses specialized journals, this transaction would be entered in the Cash Payments Journal.

The Worksheet and Financial Statements The worksheet for a sole proprietorship and a partnership are very similar. The only difference is that for a partnership, there are extra capital and drawing accounts for each partner.

The financial statements for a partnership are very similar to those for a sole proprietorship. However, a partnership also has an additional statement called the distribution of net income statement. In addition, the balance sheet for a partnership is a little different than that of a sole proprietorship. As with a sole proprietorship, a partnership prepares an operating statement. This document is prepared the same for a partnership as for a sole proprietorship.

Figuring Division of Income or Loss Every investor wants a return on his investment. Partners are entitled to whatever share their agreement dictates of the business’ profit or loss. Look back to the note in this lesson about ratios to see the way to figure each partner’s share. If the partnership agreement dictates that Partner A gets 25 percent and Partner B gets 75 percent of the business’ net income or net loss, you must figure how much money each partner receives. There are two ways to do this: the ratio method and the percentage method.

0201202LB04A-18-24

Partnerships, Corporations and Non-profit Organizations

18-9

The percentage method of figuring the division of income or loss simply takes the total net income or loss and multiplies it by the percentage of the company each partner owns. If Partner A’s and B’s combined net income is $50,000, then using the percentage method, we would figure their shares like this:

Partner A: Partner A is entitled to 25 percent of the $50,000. To find this, multiply $50,000 by 25% (0.25). This gives you Partner A’s share: $12,500.

Partner B: Partner B is entitled to 75 percent of the $50,000. Take $50,000 and multiply it by 75% (0.75). This gives you Partner B’s share: $37,500.

To check your work, take the total shares and add them together. The result should equal the total net income or loss of the company.

Partner A: $12,500

Partner B: + 37,500

Total $50,000

Preparing a Distribution of Net Income Statement As you can see from the previous section, the partners divide the net income of the business. You learned how to figure each partner’s share; now you will see how to record this information on a special document—the distribution of net income statement.

The distribution of net income statement spells out who received how much of the business’ net income. It looks like this:

Sue & Martha’s FlowersDistribution of Net Income Statement

Month ending Dec. 31, 20XX

Sue Miller 50% of Net Income ................. $2,500

Martha Jones 50% of Net Income ................... 2,500

Net Income .................................... $5,000

To complete the statement, follow these steps: 1. Use the operating statement to determine the share of net income for each partner. 2. Head up the distribution of net income statement with the business name, the words

“Distribution of Net Income Statement” and the dates the statement covers.

0201202LB04A-18-24

Bookkeeping

18-10

3. Fill out the statement by entering each partner’s name and that partner’s share (expressed as a percentage) of the business. This entry should be in this form:

Name of Partner Percentage Share of Net Income

4. In the column to the right of the “Percentage Share of Net Income” label, fill in the dollar amount that partner is entitled to. This amount can be found by completing the steps you learned in the previous section.

5. After all partners are entered on the statement, add up all the dollar amounts shown. The total of the partners’ interest should equal the total net income (or net loss) shown on the partnership’s statement.

6. If your figures are correct (the total on the distribution of net income statement matches the total on the operating statement), draw a double line under the total on the distribution of net income statement. You are finished with this document.

7. If the figures do not match, you have made an error. To find the error, first, check the percentage interest for each partner. Add up the percentages—they should total 100 percent. If they don’t, there is your error. If they do, check your math in figuring the dollar amounts due each partner. Then check your net income statement. The error must lie somewhere in one of these areas.

Now, take a few moments to review what you’ve learned.

Step 6: Practice Exercise 18-1

Part 1Select the best single answer for the following items. Write your answers on scratch paper.

1. When a partnership is formed, all partners become _____ of the business. a. sole owners b. co-owners c. equal co-owners d. all of the above

2. _____ interest refers literally to how much of the company a partner owns. a. Percentage b. Current c. Depreciating d. Asset

0201202LB04A-18-24

Partnerships, Corporations and Non-profit Organizations

18-11

3. The concept allowing each partner to enter into binding contracts for the firm is known as _____. a. depreciation b. mutual agents c. submissive contractual obligation d. underwritten law

4. The length of a partnership agreement _____. a. can varyb. must be in writing c. is never spelled out in the partnership agreement d. both a and b

5. When a partnership is formed, the professional bookkeeper must create a(n) _____ account for each partner. a. capital b. expense c. liability d. travel

6. To figure the ratio of percent interest, you must first determine the _____. a. highest common ratio b. single highest factor affecting net income c. greatest common factor d. business type

7. The _____ method of figuring the division of income or loss takes the total net income or loss and multiplies it by the percentage of the company each partner owns. a. percentage b. ratio c. net loss d. double declining balance

0201202LB04A-18-24

Bookkeeping

18-12

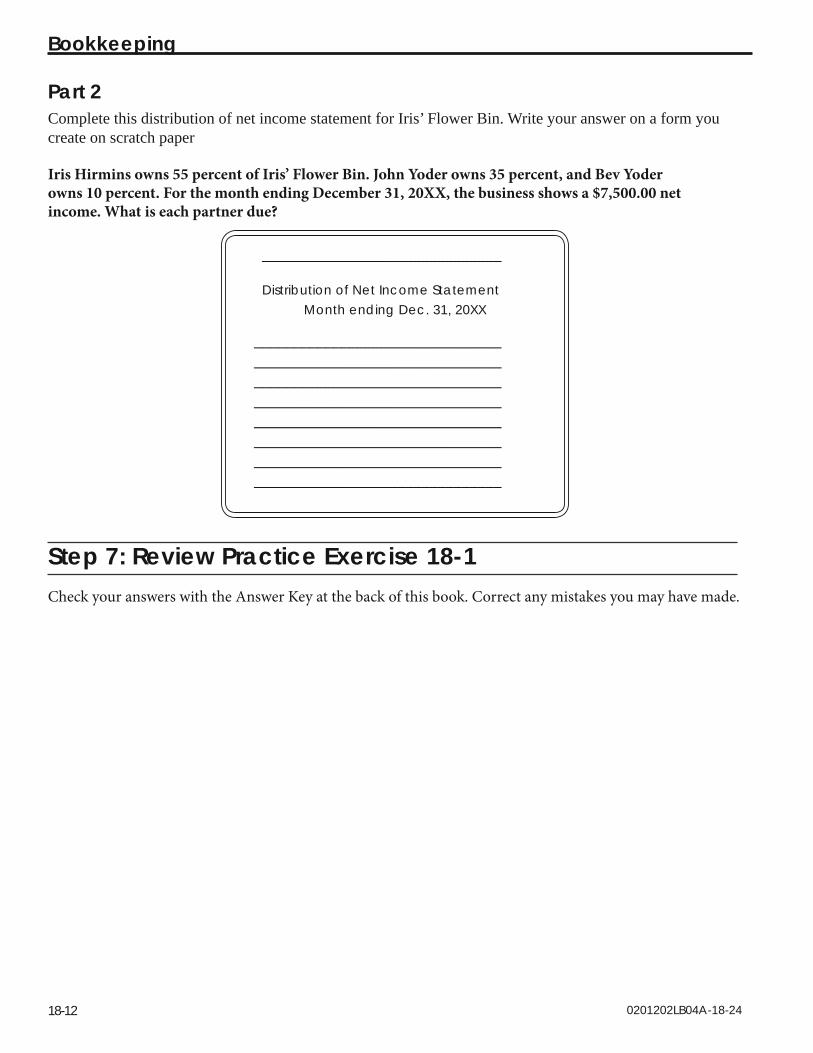

Part 2Complete this distribution of net income statement for Iris’ Flower Bin. Write your answer on a form you create on scratch paper

Iris Hirmins owns 55 percent of Iris’ Flower Bin. John Yoder owns 35 percent, and Bev Yoder owns 10 percent. For the month ending December 31, 20XX, the business shows a $7,500.00 net income. What is each partner due?

______________________________

Distribution of Net Income StatementMonth ending Dec. 31, 20XX

_______________________________ _______________________________ _______________________________ _______________________________ _______________________________ _______________________________ _______________________________ _______________________________

Step 7: Review Practice Exercise 18-1 Check your answers with the Answer Key at the back of this book. Correct any mistakes you may have made.

0201202LB04A-18-24

Partnerships, Corporations and Non-profit Organizations

18-13

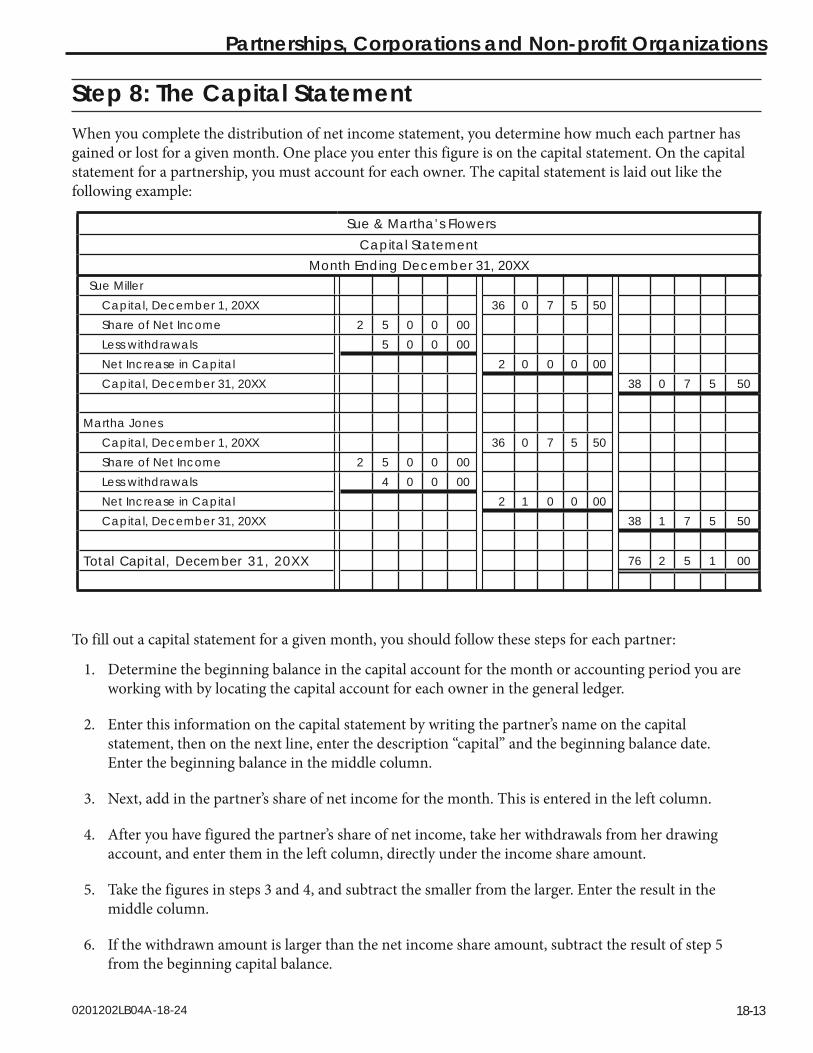

Step 8: The Capital Statement When you complete the distribution of net income statement, you determine how much each partner has gained or lost for a given month. One place you enter this figure is on the capital statement. On the capital statement for a partnership, you must account for each owner. The capital statement is laid out like the following example:

Sue & Martha’s FlowersCapital Statement

Month Ending December 31, 20XXSue Miller

Capital, December 1, 20XX 36 0 7 5 50Share of Net Income 2 5 0 0 00Less withdrawals 5 0 0 00Net Increase in Capital 2 0 0 0 00Capital, December 31, 20XX 38 0 7 5 50

Martha JonesCapital, December 1, 20XX 36 0 7 5 50Share of Net Income 2 5 0 0 00Less withdrawals 4 0 0 00Net Increase in Capital 2 1 0 0 00Capital, December 31, 20XX 38 1 7 5 50

Total Capital, December 31, 20XX 76 2 5 1 00

To fill out a capital statement for a given month, you should follow these steps for each partner:

1. Determine the beginning balance in the capital account for the month or accounting period you are working with by locating the capital account for each owner in the general ledger.

2. Enter this information on the capital statement by writing the partner’s name on the capital statement, then on the next line, enter the description “capital” and the beginning balance date. Enter the beginning balance in the middle column.

3. Next, add in the partner’s share of net income for the month. This is entered in the left column.

4. After you have figured the partner’s share of net income, take her withdrawals from her drawing account, and enter them in the left column, directly under the income share amount.

5. Take the figures in steps 3 and 4, and subtract the smaller from the larger. Enter the result in the middle column.

6. If the withdrawn amount is larger than the net income share amount, subtract the result of step 5 from the beginning capital balance.

0201202LB04A-18-24

Bookkeeping

18-14

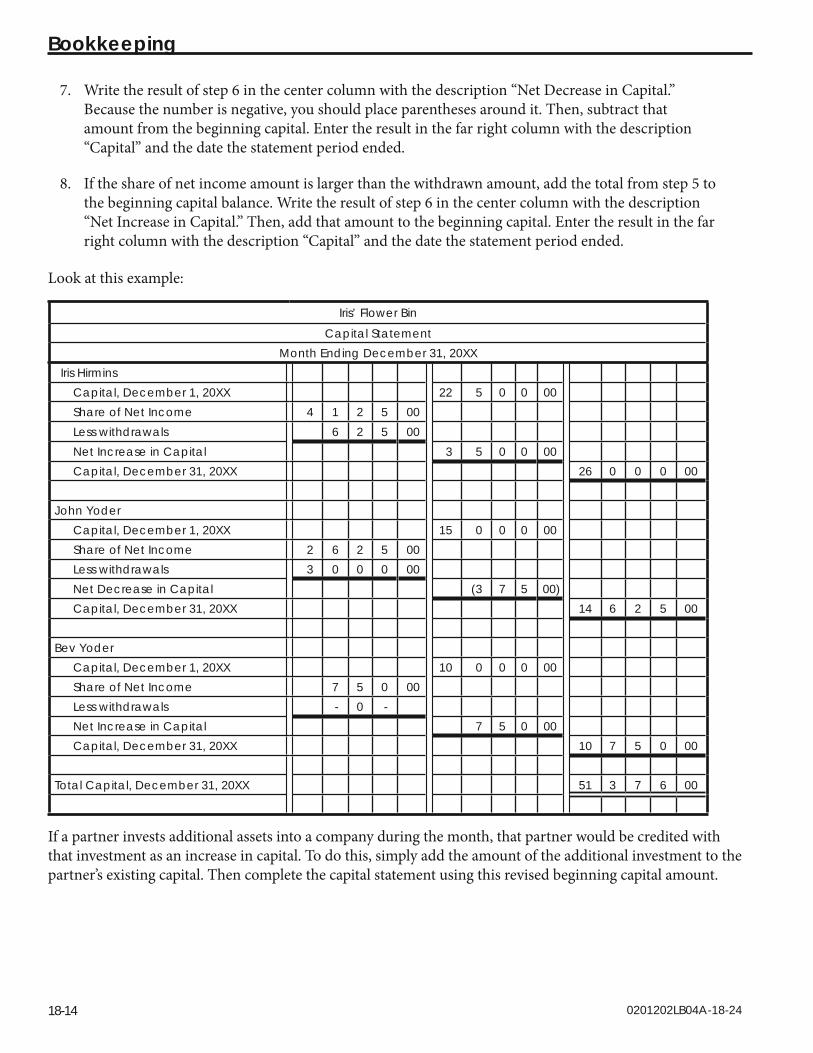

7. Write the result of step 6 in the center column with the description “Net Decrease in Capital.” Because the number is negative, you should place parentheses around it. Then, subtract that amount from the beginning capital. Enter the result in the far right column with the description “Capital” and the date the statement period ended.

8. If the share of net income amount is larger than the withdrawn amount, add the total from step 5 to the beginning capital balance. Write the result of step 6 in the center column with the description “Net Increase in Capital.” Then, add that amount to the beginning capital. Enter the result in the far right column with the description “Capital” and the date the statement period ended.

Look at this example:

Iris’ Flower Bin

Capital StatementMonth Ending December 31, 20XX

Iris HirminsCapital, December 1, 20XX 22 5 0 0 00Share of Net Income 4 1 2 5 00Less withdrawals 6 2 5 00Net Increase in Capital 3 5 0 0 00Capital, December 31, 20XX 26 0 0 0 00

John YoderCapital, December 1, 20XX 15 0 0 0 00Share of Net Income 2 6 2 5 00Less withdrawals 3 0 0 0 00Net Decrease in Capital (3 7 5 00)Capital, December 31, 20XX 14 6 2 5 00

Bev YoderCapital, December 1, 20XX 10 0 0 0 00Share of Net Income 7 5 0 00Less withdrawals - 0 -Net Increase in Capital 7 5 0 00Capital, December 31, 20XX 10 7 5 0 00

Total Capital, December 31, 20XX 51 3 7 6 00

If a partner invests additional assets into a company during the month, that partner would be credited with that investment as an increase in capital. To do this, simply add the amount of the additional investment to the partner’s existing capital. Then complete the capital statement using this revised beginning capital amount.

0201202LB04A-18-24

Partnerships, Corporations and Non-profit Organizations

18-15

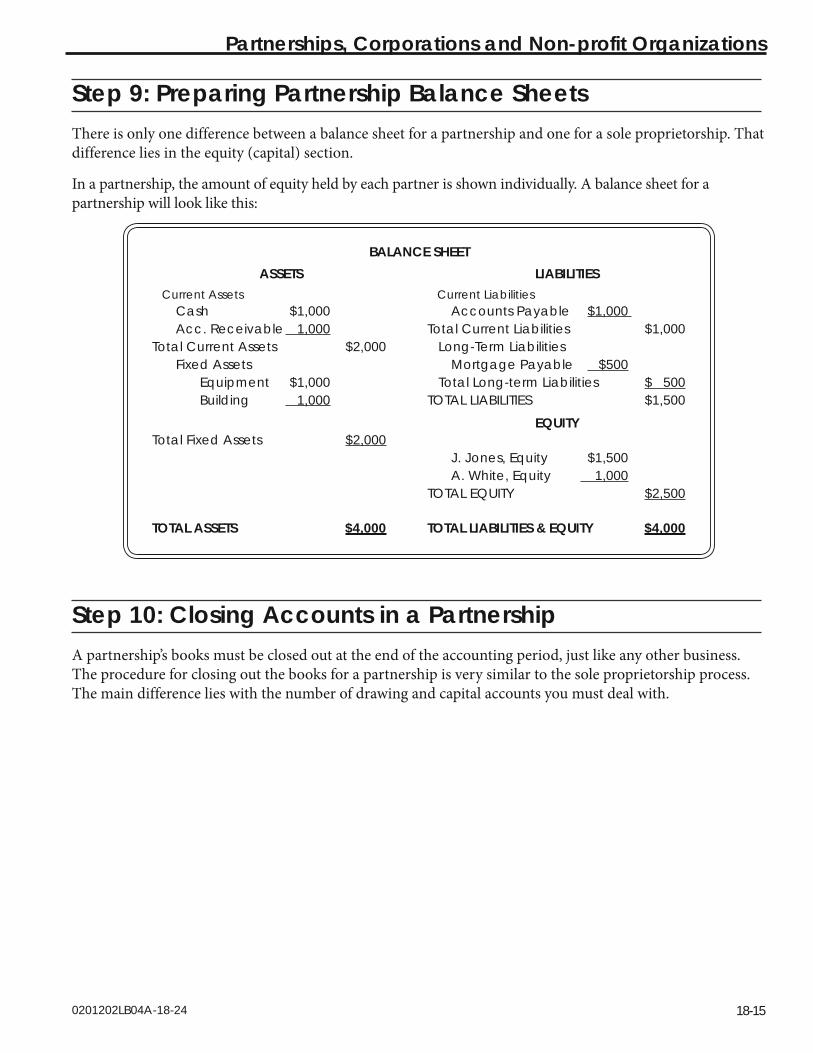

Step 9: Preparing Partnership Balance Sheets There is only one difference between a balance sheet for a partnership and one for a sole proprietorship. That difference lies in the equity (capital) section.

In a partnership, the amount of equity held by each partner is shown individually. A balance sheet for a partnership will look like this:

BALANCE SHEET ASSETS LIABILITIES

Current Assets Current Liabilities Cash $1,000 Accounts Payable $1,000 Acc. Receivable 1,000 Total Current Liabilities $1,000Total Current Assets $2,000 Long-Term Liabilities Fixed Assets Mortgage Payable $500 Equipment $1,000 Total Long-term Liabilities $ 500 Building 1,000 TOTAL LIABILITIES $1,500

EQUITYTotal Fixed Assets $2,000 J. Jones, Equity $1,500 A. White, Equity 1,000 TOTAL EQUITY $2,500

TOTAL ASSETS $4,000 TOTAL LIABILITIES & EQUITY $4,000

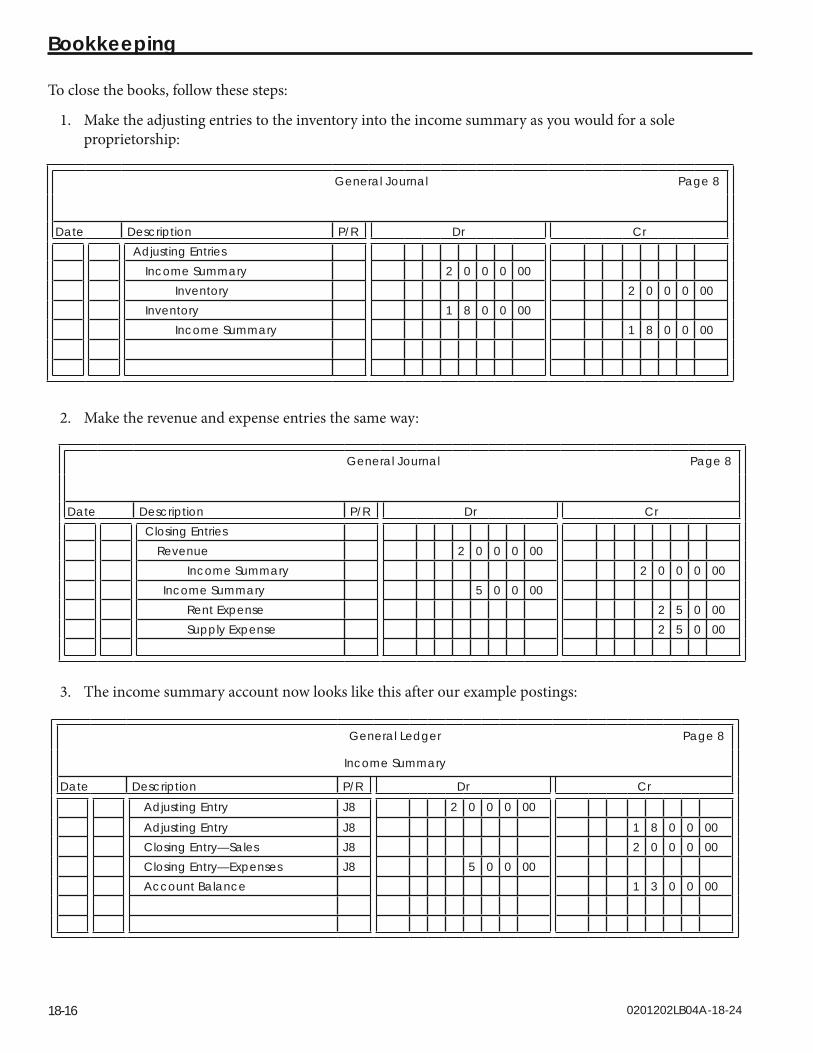

Step 10: Closing Accounts in a Partnership A partnership’s books must be closed out at the end of the accounting period, just like any other business. The procedure for closing out the books for a partnership is very similar to the sole proprietorship process. The main difference lies with the number of drawing and capital accounts you must deal with.

0201202LB04A-18-24

Bookkeeping

18-16

To close the books, follow these steps:

1. Make the adjusting entries to the inventory into the income summary as you would for a sole proprietorship:

General Journal Page 8

Date Description P/R Dr CrAdjusting Entries

Income Summary 2 0 0 0 00Inventory 2 0 0 0 00

Inventory 1 8 0 0 00Income Summary 1 8 0 0 00

2. Make the revenue and expense entries the same way:

General Journal Page 8

Date Description P/R Dr CrClosing Entries

Revenue 2 0 0 0 00Income Summary 2 0 0 0 00

Income Summary 5 0 0 00Rent Expense 2 5 0 00Supply Expense 2 5 0 00

3. The income summary account now looks like this after our example postings:

General Ledger Page 8

Income Summary

Date Description P/R Dr Cr

Adjusting Entry J8 2 0 0 0 00

Adjusting Entry J8 1 8 0 0 00Closing Entry—Sales J8 2 0 0 0 00Closing Entry—Expenses J8 5 0 0 00Account Balance 1 3 0 0 00

0201202LB04A-18-24

Partnerships, Corporations and Non-profit Organizations

18-17

When you complete this step, you should have your distribution of net income statement handy. In our example, we’ll say John Jones and Alice White each get 50 percent of the net income.

The account balance shown by the income summary should match the net income line of the distribution of net income statement. From that statement, determine how much each partner is entitled to. Then make the next entry to close the income summary:

General Journal Page 8

Date Description P/R Dr Cr

Income Summary 1 3 0 0 00John Jones, Capital 6 5 0 00Alice White, Capital 6 5 0 00

The $650 reflects the percentage shown on the distribution of net income statement.

Closing the Drawing Accounts After you have closed the income summary, the next step is closing the drawing accounts. To do this, take these steps:

1. Determine each partner’s balance in his or her drawing accounts either from the individual accounts or from the worksheet.

2. Next, close each account as you’ve learned previously. Remember, however, that now you have two or more drawing accounts to close. If, for example, Mr. Jones and Ms. White each had a $200 balance in the drawing accounts, the accounts would be closed this way:

General Journal Page 8

Date Description P/R Dr Cr

John Jones, Capital 2 0 0 00John Jones, Drawing 2 0 0 00

Alice White, Capital 2 0 0 00Alice White, Drawing 2 0 0 00

0201202LB04A-18-24

Bookkeeping

18-18

3. Finally, post all closing entries to the appropriate ledger accounts. In this case, capital accounts and drawing accounts for both John Jones and Alice White would be posted with the information from the journal.

Now let’s see how corporations differ from partnerships.

Step 11: Corporations If you look up business listings in the phone book, you may see the abbreviation “Inc.” This abbreviation stands for incorporated. Incorporated means the business is a corporation instead of a partnership or sole proprietorship. In the Lesson Preview, you were introduced to some of the differences between corporations and other business forms. In this segment, we’ll cover some of the aspects of the corporation in more detail. You’ll learn how corporations are owned, how profits are distributed and how some profits are kept within the organization for future investment. By the end of the segment, you’ll have a better grasp of businesses that incorporate!

It’s important to note that this segment is not designed to prepare you to work as a bookkeeper for a corporation. Corporations often employ certified accountants to keep their financial records. The additional training you need to work for a corporation is covered in more advanced accounting classes. You may consider taking advanced course work after you’ve accumulated some experience as a bookkeeper. Until then, keep the information from this Lesson Step in the back of your mind. It may come in handy as your career progresses!

Stocks and StockholdersYou already know how partnerships and sole proprietorships are owned. Corporations are different. They attain a legal separation of person and business assets and liabilities. What does this mean? Suppose you’re an owner of a sole proprietorship. Your company and your personal belongings are both part of your individual assets. If your company goes broke, you may have to sell your house or car to settle outstanding debts. A corporation is different. If the corporation goes broke, your house and car and other personal belongings are not affected, because a corporation is a separate legal entity.

So how does ownership of a corporation work? Generally, corporations issue stock in the company. Stock (also called shares) refers to a portion of a company that is sold to generate money for the business. People who own stock are called stockholders (or shareholders) because they own stock (a share of the company).

Small corporations can be owned by as few as two people. All of the available stock may be owned by a handful of friends or by the members of a family. Some corporations are large enough to list in the newspaper business section. People all around the world may own a small piece of these large businesses.

Now, imagine a company with thousands of stockholders. With so many owners, how does a corporation make basic day-to-day decisions? In general, the company is headed by a chief executive officer (CEO), who oversees company operations. Who supervises the CEO? The board of directors is a governing board that is responsible for hiring the CEO and evaluating the results of company policies. And the board of directors is elected by stockholders. If you own ten shares of stock in a company, you generally have 10 votes to apply to the election of board members.

0201202LB04A-18-24

Partnerships, Corporations and Non-profit Organizations

18-19

In general, when you purchase stock, the corporation issues you a certificate signifying that you own a specific portion of the company. This certificate entitles you to your share of company earnings. But how do you get paid? Let’s take a look at how corporations pay their stockholders.

Dividends and Retained EarningsIn a sole proprietorship or partnership, owners have a drawing account. Corporations are different. In exchange for the money invested in the company, stockholders are paid dividends. Dividends are money paid per share of stock by the company. Usually, the company limits its total dividend payout, so stocks do not automatically earn dividends. At the end of an accounting period, the company determines its net income and decides how much of that income to pass on to its stockholders. Dividends are paid on a per-share basis. That is, each stockholder receives an amount of money based on how many shares of stock are owned.

Even when a corporation has a profitable year, the company may not want to pay all of its profits out as dividends. Instead, the company will hold back some of the profit to reinvest in the company and help it grow. This reinvestment of profit is known as retained earnings. Retained earnings affect how large and how often dividends are paid.

Suppose a company earns a million dollars over the course of the year. The company decides to keep 90 percent of its profit as retained earnings and pass on the remaining 10 percent as dividends ($100,000). And imagine that the company has 10,000 shares of stock issued. This means that each share of stock earns a $10 dividend. If you own five shares of the company’s stock, you will get a check for $50.

Generally, that’s how dividends work. However, not all shares of stock work the same. In the next segment, we’ll look at the three major types of stock, and how they differ.

Types of StockCommon stock is an ordinary unit of ownership in a corporation. Each share is basically the same, no matter who owns it. The owners of common stock split profits equally and have equal voting rights. Preferred stock is a special kind of stock that gets first shot at dividends. Suppose a company wants to reinvest in a new location and limits the amount to be paid in dividends. Preferred stockholders are more likely to benefit from the available payout. In addition, if the corporation goes bankrupt, preferred stockholders are paid after creditors, but before common stockholders. However, there is often a tradeoff to owning this type of stock. Preferred stockholders don’t always have voting privileges.