01 techtrends 0408 v2 3/20/09 2:10 PM Page 1 RETAIL 19TH · PDF file16 Merchandising & Supply...

15

Presented By A SUPPLEMENT TO RIS NEWS APRIL 2009 3 Who Responded 5 Year of Reassessment & Reallocation 8 Gauging Economy’s Impact 10 Strategy & Transformation 12 Point of Service 16 Merchandising & Supply Chain 20 Integration Across Channels RETAIL 19TH ANNUAL TECHNOLOGY STUDY Innovate Execute Adapt Strategies and technologies for surgically adjusting to today’s challenges and widening the gap when the economy rebounds. FINDINGS RETAIL 19TH ANNUAL PRODUCED BY: Innovate Execute Adapt Presented By:

Transcript of 01 techtrends 0408 v2 3/20/09 2:10 PM Page 1 RETAIL 19TH · PDF file16 Merchandising & Supply...

Presented By

A S U P P L E M E N T T O R I S N E W S A P R I L 2 0 0 9

3 Who Responded

5 Year of Reassessment & Reallocation

8 Gauging Economy’s Impact

10 Strategy & Transformation

12 Point of Service

16 Merchandising & Supply Chain

20 Integration Across Channels

RETAIL1 9 T H A N N U A L

T E C H N O L O G Y S T U D Y InnovateExecute

AdaptStrategies and technologies for surgically

adjusting to today’s challenges and widening the gap when the economy rebounds.

FIN

DIN

GS

RETAIL1 9 T H A N N U A L

PRODUCED BY:

InnovateExecute

Adapt

Presented By:

01_techtrends_0408_v2 3/20/09 2:10 PM Page 1

RETAIL TECHNOLOGY TRENDSSupplement to RIS News

April 2009

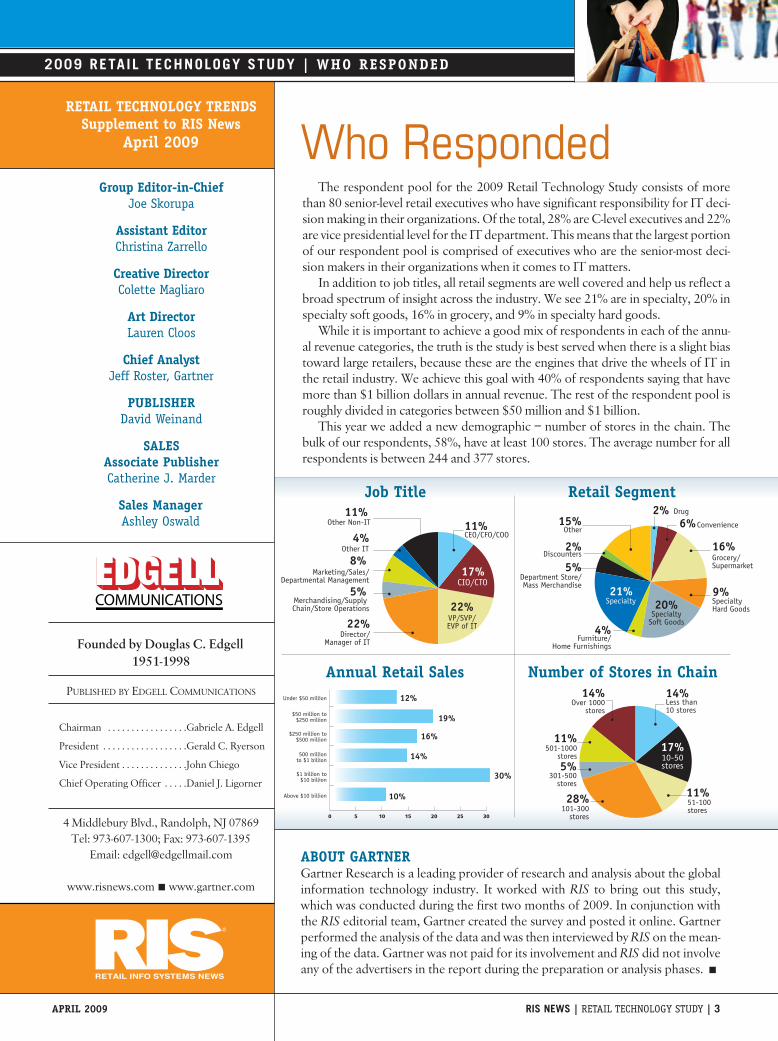

The respondent pool for the 2009 Retail Technology Study consists of morethan 80 senior-level retail executives who have significant responsibility for IT deci-sion making in their organizations. Of the total, 28% are C-level executives and 22%are vice presidential level for the IT department. This means that the largest portionof our respondent pool is comprised of executives who are the senior-most deci-sion makers in their organizations when it comes to IT matters.

In addition to job titles, all retail segments are well covered and help us reflect abroad spectrum of insight across the industry. We see 21% are in specialty, 20% inspecialty soft goods, 16% in grocery, and 9% in specialty hard goods.

While it is important to achieve a good mix of respondents in each of the annu-al revenue categories, the truth is the study is best served when there is a slight biastoward large retailers, because these are the engines that drive the wheels of IT inthe retail industry. We achieve this goal with 40% of respondents saying that havemore than $1 billion dollars in annual revenue. The rest of the respondent pool isroughly divided in categories between $50 million and $1 billion.

This year we added a new demographic – number of stores in the chain. Thebulk of our respondents, 58%, have at least 100 stores. The average number for allrespondents is between 244 and 377 stores.

12%Under $50 million

$50 million to$250 million

$250 million to$500 million

500 millionto $1 billion

$1 billion to$10 billion

Above $10 billion

0 5 10 15 20 25 30

19%

16%

14%

30%

10%

2009 RETAIL TECHNOLOGY STUDY | WHO RESPONDED

Less than10 stores

14%

10-50stores

17%

51-100stores

11%101-300

stores

28%

501-1000stores

301-500stores

5%

Over 1000stores

14%

11%

Who RespondedGroup Editor-in-Chief

Joe Skorupa

Assistant EditorChristina Zarrello

Creative DirectorColette Magliaro

Art DirectorLauren Cloos

Chief AnalystJeff Roster, Gartner

PUBLISHERDavid Weinand

SALESAssociate Publisher Catherine J. Marder

Sales Manager Ashley Oswald

Founded by Douglas C. Edgell1951-1998

PUBLISHED BY EDGELL COMMUNICATIONS

Chairman . . . . . . . . . . . . . . . . .Gabriele A. Edgell

President . . . . . . . . . . . . . . . . . .Gerald C. Ryerson

Vice President . . . . . . . . . . . . . .John Chiego

Chief Operating Officer . . . . .Daniel J. Ligorner

4 Middlebury Blvd., Randolph, NJ 07869Tel: 973-607-1300; Fax: 973-607-1395

Email: [email protected]

www.risnews.com ■ www.gartner.com

ABOUT GARTNERGartner Research is a leading provider of research and analysis about the globalinformation technology industry. It worked with RIS to bring out this study,which was conducted during the first two months of 2009. In conjunction withthe RIS editorial team, Gartner created the survey and posted it online. Gartnerperformed the analysis of the data and was then interviewed by RIS on the mean-ing of the data. Gartner was not paid for its involvement and RIS did not involveany of the advertisers in the report during the preparation or analysis phases. ■

CEO/CFO/COO11%

17%

22%22%

Merchandising/Supply Chain/Store Operations

5%

Marketing/Sales/Departmental Management

8%Other IT

4%Other Non-IT

11%

VP/SVP/EVP of IT

CIO/CTO

Director/Manager of IT

Job Title

Drug2%

Retail Segment

Convenience6%

Grocery/Supermarket

16%

SpecialtyHard Goods

9%

SpecialtySoft Goods

20%

Furniture/Home Furnishings

4%

Specialty21%

Department Store/Mass Merchandise

5%Discounters

2%Other

15%

Annual Retail Sales

Job Title Retail Segment

Number of Stores in Chain

APRIL 2009 RIS NEWS | RETAIL TECHNOLOGY STUDY | 3

03_toc.rts0409_v2 3/23/09 9:56 AM Page 1

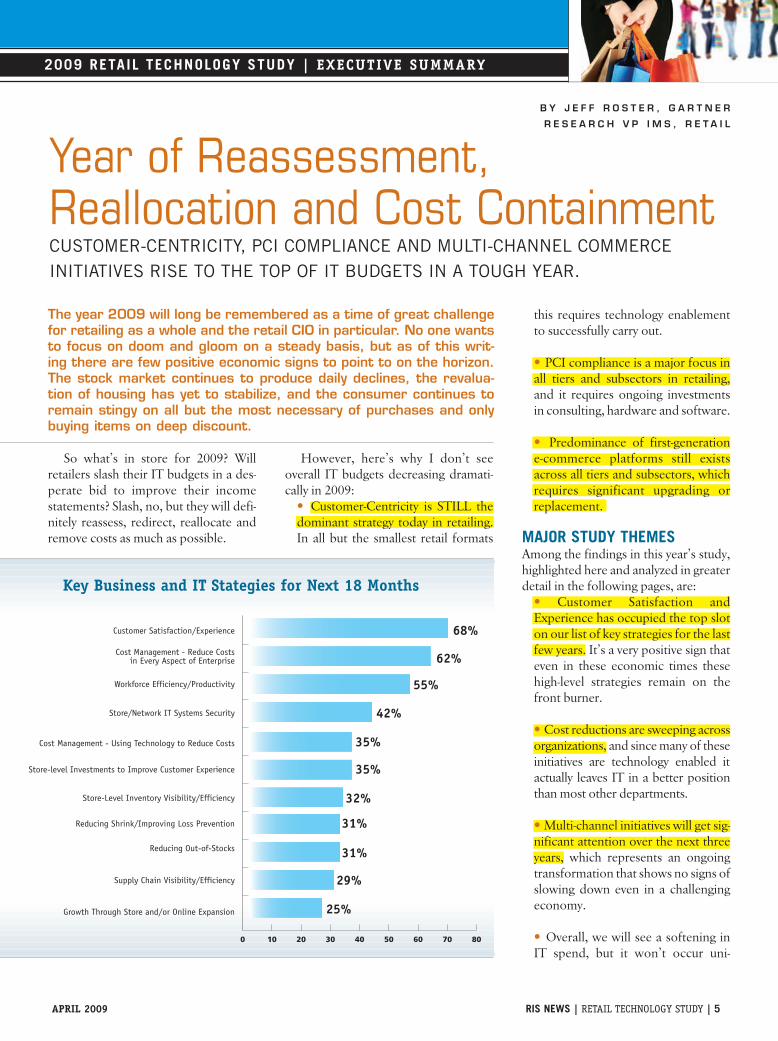

So what’s in store for 2009? Willretailers slash their IT budgets in a des-perate bid to improve their incomestatements? Slash, no, but they will defi-nitely reassess, redirect, reallocate andremove costs as much as possible.

However, here’s why I don’t seeoverall IT budgets decreasing dramati-cally in 2009:

• Customer-Centricity is STILL thedominant strategy today in retailing.In all but the smallest retail formats

this requires technology enablementto successfully carry out.

• PCI compliance is a major focus inall tiers and subsectors in retailing,and it requires ongoing investmentsin consulting, hardware and software.

• Predominance of first-generation e-commerce platforms still existsacross all tiers and subsectors, whichrequires significant upgrading orreplacement.

MAJOR STUDY THEMESAmong the findings in this year’s study,highlighted here and analyzed in greaterdetail in the following pages, are:

• Customer Satisfaction andExperience has occupied the top sloton our list of key strategies for the lastfew years. It’s a very positive sign thateven in these economic times thesehigh-level strategies remain on thefront burner.

• Cost reductions are sweeping acrossorganizations, and since many of theseinitiatives are technology enabled itactually leaves IT in a better positionthan most other departments.

• Multi-channel initiatives will get sig-nificant attention over the next threeyears, which represents an ongoingtransformation that shows no signs ofslowing down even in a challengingeconomy.

• Overall, we will see a softening inIT spend, but it won’t occur uni-

2009 RETAIL TECHNOLOGY STUDY | EXECUTIVE SUMMARY

The year 2009 will long be remembered as a time of great challengefor retailing as a whole and the retail CIO in particular. No one wantsto focus on doom and gloom on a steady basis, but as of this writ-ing there are few positive economic signs to point to on the horizon.The stock market continues to produce daily declines, the revalua-tion of housing has yet to stabilize, and the consumer continues toremain stingy on all but the most necessary of purchases and onlybuying items on deep discount.

Year of Reassessment,Reallocation and Cost ContainmentCUSTOMER-CENTRICITY, PCI COMPLIANCE AND MULTI-CHANNEL COMMERCE INITIATIVES RISE TO THE TOP OF IT BUDGETS IN A TOUGH YEAR.

B Y J E F F R O S T E R , G A R T N E R

R E S E A R C H V P I M S , R E T A I L

0 10 20 30 40 50 60 70 80

Store/Network IT Systems Security 42%

Supply Chain Visibility/Efficiency 29%

Store-Level Inventory Visibility/Efficiency 32%

Growth Through Store and/or Online Expansion 25%

Cost Management - Using Technology to Reduce Costs 35%

Store-level Investments to Improve Customer Experience 35%

Cost Management - Reduce Costsin Every Aspect of Enterprise 62%

Reducing Shrink/Improving Loss Prevention 31%

Reducing Out-of-Stocks 31%

Workforce Efficiency/Productivity 55%

Customer Satisfaction/Experience 68%

Key Business and IT Stategies for Next 18 Months

APRIL 2009 RIS NEWS | RETAIL TECHNOLOGY STUDY | 5

05_exec summary_rts0409_v3 3/19/09 5:09 PM Page 1

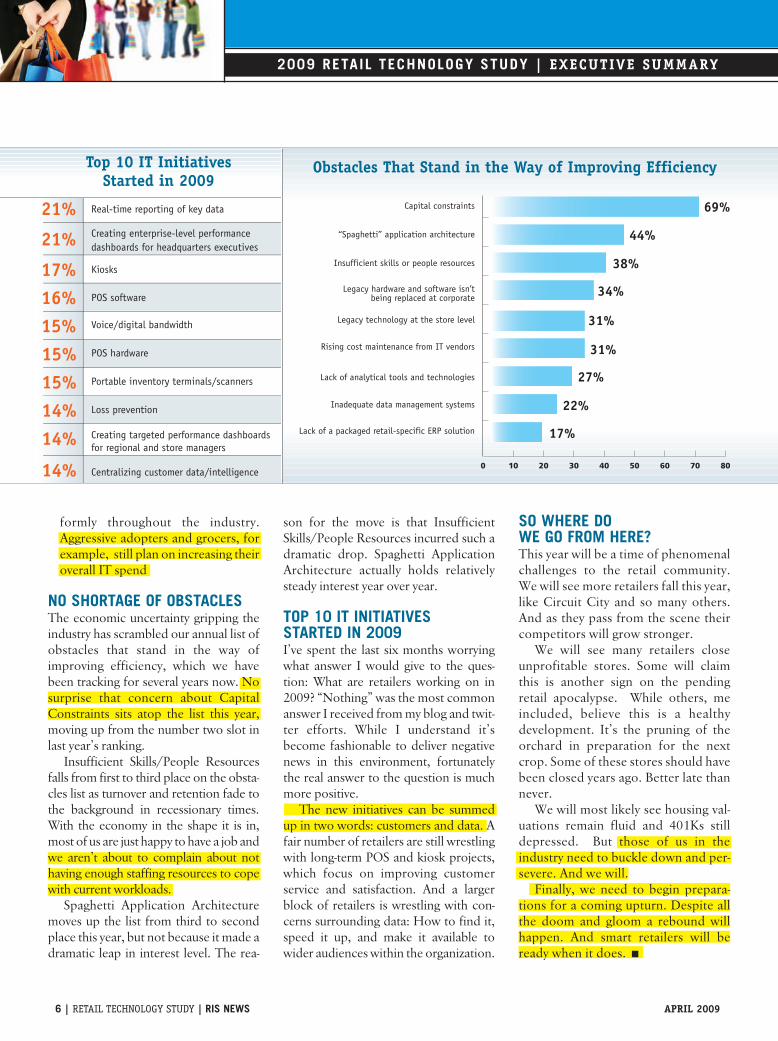

formly throughout the industry.Aggressive adopters and grocers, forexample, still plan on increasing theiroverall IT spend

NO SHORTAGE OF OBSTACLESThe economic uncertainty gripping theindustry has scrambled our annual list ofobstacles that stand in the way ofimproving efficiency, which we havebeen tracking for several years now. Nosurprise that concern about CapitalConstraints sits atop the list this year,moving up from the number two slot inlast year’s ranking.

Insufficient Skills/People Resourcesfalls from first to third place on the obsta-cles list as turnover and retention fade tothe background in recessionary times.With the economy in the shape it is in,most of us are just happy to have a job andwe aren’t about to complain about nothaving enough staffing resources to copewith current workloads.

Spaghetti Application Architecturemoves up the list from third to secondplace this year, but not because it made adramatic leap in interest level. The rea-

son for the move is that InsufficientSkills/People Resources incurred such adramatic drop. Spaghetti ApplicationArchitecture actually holds relativelysteady interest year over year.

TOP 10 IT INITIATIVES STARTED IN 2009I’ve spent the last six months worryingwhat answer I would give to the ques-tion: What are retailers working on in2009? “Nothing” was the most commonanswer I received from my blog and twit-ter efforts. While I understand it’sbecome fashionable to deliver negativenews in this environment, fortunatelythe real answer to the question is muchmore positive.

The new initiatives can be summedup in two words: customers and data. Afair number of retailers are still wrestlingwith long-term POS and kiosk projects,which focus on improving customerservice and satisfaction. And a largerblock of retailers is wrestling with con-cerns surrounding data: How to find it,speed it up, and make it available towider audiences within the organization.

SO WHERE DO WE GO FROM HERE?This year will be a time of phenomenalchallenges to the retail community.We will see more retailers fall this year,like Circuit City and so many others.And as they pass from the scene theircompetitors will grow stronger.

We will see many retailers closeunprofitable stores. Some will claimthis is another sign on the pendingretail apocalypse. While others, meincluded, believe this is a healthydevelopment. It’s the pruning of theorchard in preparation for the nextcrop. Some of these stores should havebeen closed years ago. Better late thannever.

We will most likely see housing val-uations remain fluid and 401Ks stilldepressed. But those of us in theindustry need to buckle down and per-severe. And we will.

Finally, we need to begin prepara-tions for a coming upturn. Despite allthe doom and gloom a rebound willhappen. And smart retailers will beready when it does. ■

0 10 20 30 40 50 60 70 80

Lack of a packaged retail-specific ERP solution 17%

Rising cost maintenance from IT vendors 31%

Legacy technology at the store level 31%

Capital constraints 69%

Legacy hardware and software isn’tbeing replaced at corporate 34%

“Spaghetti” application architecture 44%

Inadequate data management systems 22%

Insufficient skills or people resources 38%

Lack of analytical tools and technologies 27%

Obstacles That Stand in the Way of Improving Efficiency

2009 RETAIL TECHNOLOGY STUDY | EXECUTIVE SUMMARY

Real-time reporting of key data21%Creating enterprise-level performancedashboards for headquarters executives21%Kiosks17%POS software16%Voice/digital bandwidth15%POS hardware15%Portable inventory terminals/scanners15%Loss prevention14%Creating targeted performance dashboardsfor regional and store managers

14%

Centralizing customer data/intelligence14%

Top 10 IT Initiatives Started in 2009

6 | RETAIL TECHNOLOGY STUDY | RIS NEWS APRIL 2009

05_exec summary_rts0409_v3 3/19/09 5:10 PM Page 2

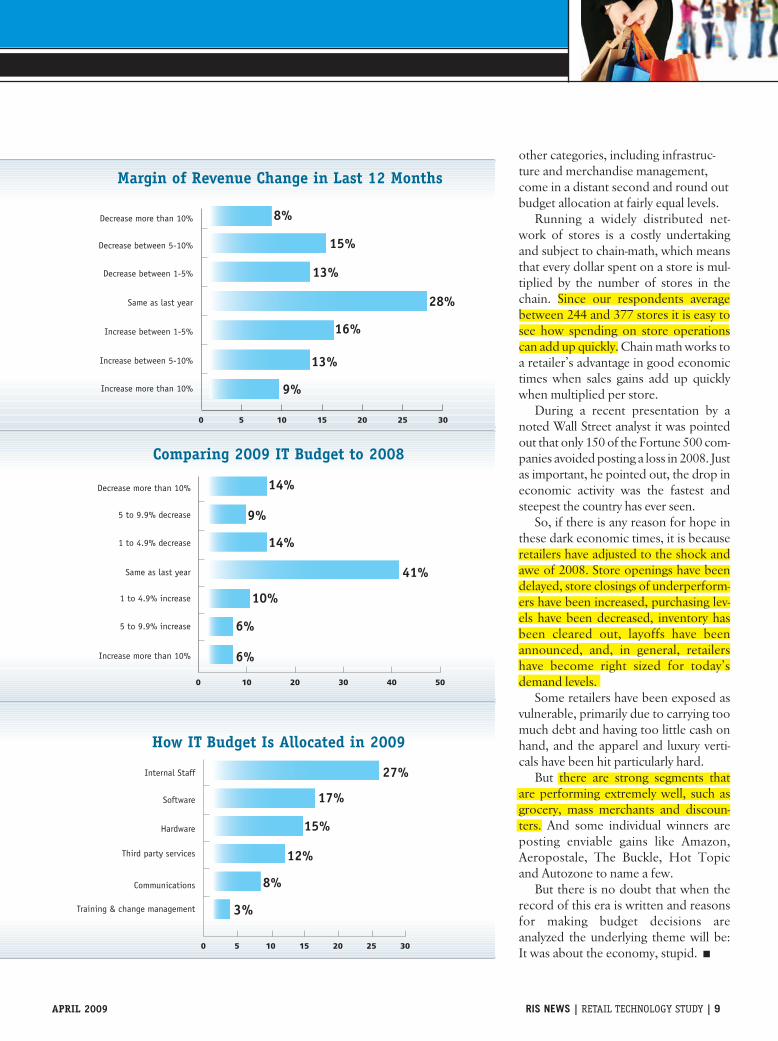

Still, 38% of respondents were up inrevenue year over year and the restrecorded flat sales. Will this happenagain in 2009? Not likely. The reason islast year’s nosedive was faster and steep-er than anything ever seen before, and itoccurred just as retailers headed intothe holiday season. Even retailers withreal-time systems could not adjust thatquickly. No one could.

The whipsawing of shoppers by acredit meltdown, massive Wall Street

bailouts, and frightening headlinesripped right out of the Great Depressionhad a chilling effect on consumer confi-dence. But here’s an interesting insight:Replace these once-in-a-lifetime circum-stances with normal recessionary forces,which are typically slower moving thanwhat we are now experiencing, and therevenue figures probably would havelooked similar to previous years with thetotal number of retailers reportingdecreases in the mid-teens.

Is this a reason for optimism in2009? As far as profits go, the answer is“yes.” Revenue? Not so much. It willtake a few years to reverse the econom-ic contraction occurring today throughstore closings and a sharp consumerreluctance to spend, but smart retailershave now caught up with the trend andare now fully prepared to adjust to cur-rent demand levels while at the sametime focusing on productivity and effi-ciency to protect margins.

IMPACT ON IT SPENDINGThe fourth quarter also is a time whenCIOs plan the following year’s technol-ogy budgets, so the economic gyrationslast fall likely had a major impact on ITplans. One logical area to feel thesqueeze is capital investment.Compared to last years’ study cap-exspending is down 10%, a sharp butexpected decline.

Overall, we find that 63% of retailerseither increased their IT budgets for

2009 or stayed the same as last year.This is a solid majority for a politicalelection, but it is far from par comparedto previous years. Typically, we findretailers report year-over-year IT budgetdecreases in the single digits. This yearthe figure is a whopping 36%, whichclosely corresponds to those whoreported depressed revenue in 2008.

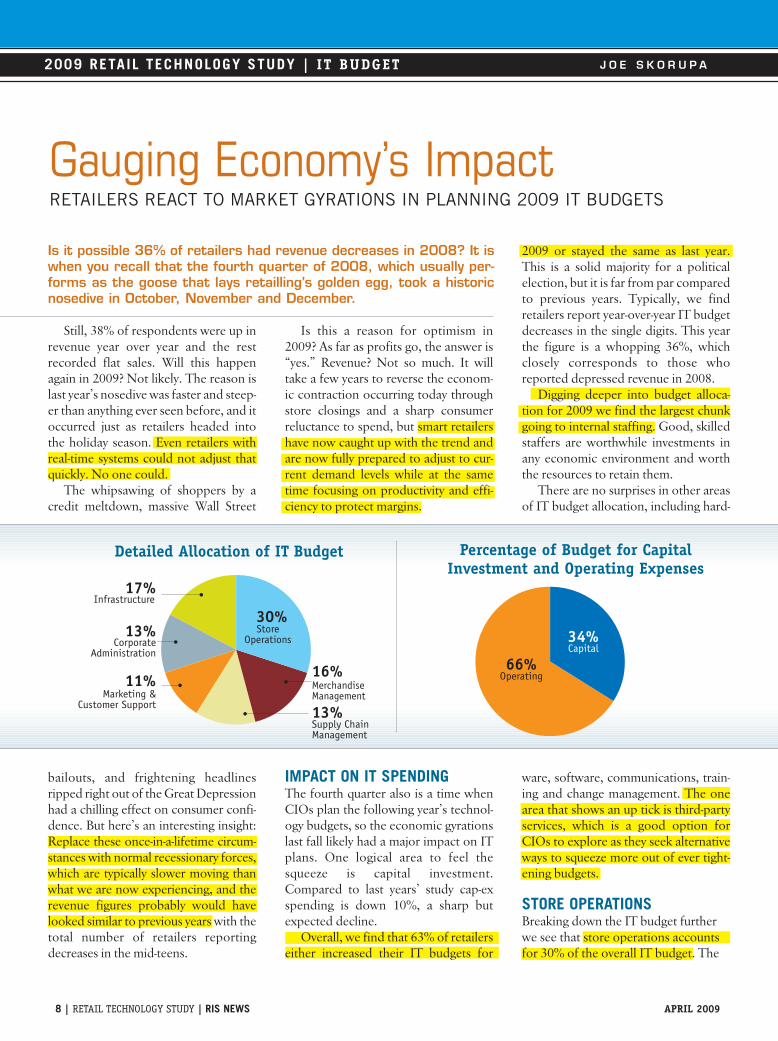

Digging deeper into budget alloca-tion for 2009 we find the largest chunkgoing to internal staffing. Good, skilledstaffers are worthwhile investments inany economic environment and worththe resources to retain them.

There are no surprises in other areasof IT budget allocation, including hard-

ware, software, communications, train-ing and change management. The onearea that shows an up tick is third-partyservices, which is a good option forCIOs to explore as they seek alternativeways to squeeze more out of ever tight-ening budgets.

STORE OPERATIONS Breaking down the IT budget furtherwe see that store operations accountsfor 30% of the overall IT budget. The

8 | RETAIL TECHNOLOGY STUDY | RIS NEWS APRIL 2009

Infrastructure17%

D

MerchandiseManagement

16%

Supply ChainManagement

13%Marketing &

Customer Support

11%

StoreOperations

30%Corporate

Administration

13%

2009 RETAIL TECHNOLOGY STUDY | IT BUDGET J O E S K O R U P A

Detailed Allocation of IT Budget

Capital34%

Operating66%

Percentage of Budget for CapitalInvestment and Operating Expenses

Is it possible 36% of retailers had revenue decreases in 2008? It iswhen you recall that the fourth quarter of 2008, which usually per-forms as the goose that lays retailling’s golden egg, took a historicnosedive in October, November and December.

Gauging Economy’s ImpactRETAILERS REACT TO MARKET GYRATIONS IN PLANNING 2009 IT BUDGETS

08_budget_rts0409_v2 3/19/09 5:10 PM Page 1

APRIL 2009 RIS NEWS | RETAIL TECHNOLOGY STUDY | 9

other categories, including infrastruc-ture and merchandise management,come in a distant second and round outbudget allocation at fairly equal levels.

Running a widely distributed net-work of stores is a costly undertakingand subject to chain-math, which meansthat every dollar spent on a store is mul-tiplied by the number of stores in thechain. Since our respondents averagebetween 244 and 377 stores it is easy tosee how spending on store operationscan add up quickly. Chain math works toa retailer’s advantage in good economictimes when sales gains add up quicklywhen multiplied per store.

During a recent presentation by anoted Wall Street analyst it was pointedout that only 150 of the Fortune 500 com-panies avoided posting a loss in 2008. Justas important, he pointed out, the drop ineconomic activity was the fastest andsteepest the country has ever seen.

So, if there is any reason for hope inthese dark economic times, it is becauseretailers have adjusted to the shock andawe of 2008. Store openings have beendelayed, store closings of underperform-ers have been increased, purchasing lev-els have been decreased, inventory hasbeen cleared out, layoffs have beenannounced, and, in general, retailershave become right sized for today’sdemand levels.

Some retailers have been exposed asvulnerable, primarily due to carrying toomuch debt and having too little cash onhand, and the apparel and luxury verti-cals have been hit particularly hard.

But there are strong segments thatare performing extremely well, such asgrocery, mass merchants and discoun-ters. And some individual winners areposting enviable gains like Amazon,Aeropostale, The Buckle, Hot Topicand Autozone to name a few.

But there is no doubt that when therecord of this era is written and reasonsfor making budget decisions are analyzed the underlying theme will be: It was about the economy, stupid. ■

0 5 10 15 20 25 30

Decrease more than 10% 8%

Decrease between 5-10% 15%

Decrease between 1-5% 13%

Increase between 5-10% 13%

Same as last year 28%

Increase between 1-5% 16%

Increase more than 10% 9%

Margin of Revenue Change in Last 12 Months

0 10 20 30 40 50

Decrease more than 10% 14%

1 to 4.9% decrease 14%

1 to 4.9% increase 10%

5 to 9.9% decrease 9%

5 to 9.9% increase 6%

Increase more than 10% 6%

Same as last year 41%

Training & change management 3%

Communications 8%

Third party services 12%

Software 17%

Hardware 15%

Internal Staff 27%

0 5 10 15 20 25 30

Comparing 2009 IT Budget to 2008

How IT Budget Is Allocated in 2009

08_budget_rts0409_v2 3/20/09 11:24 AM Page 2

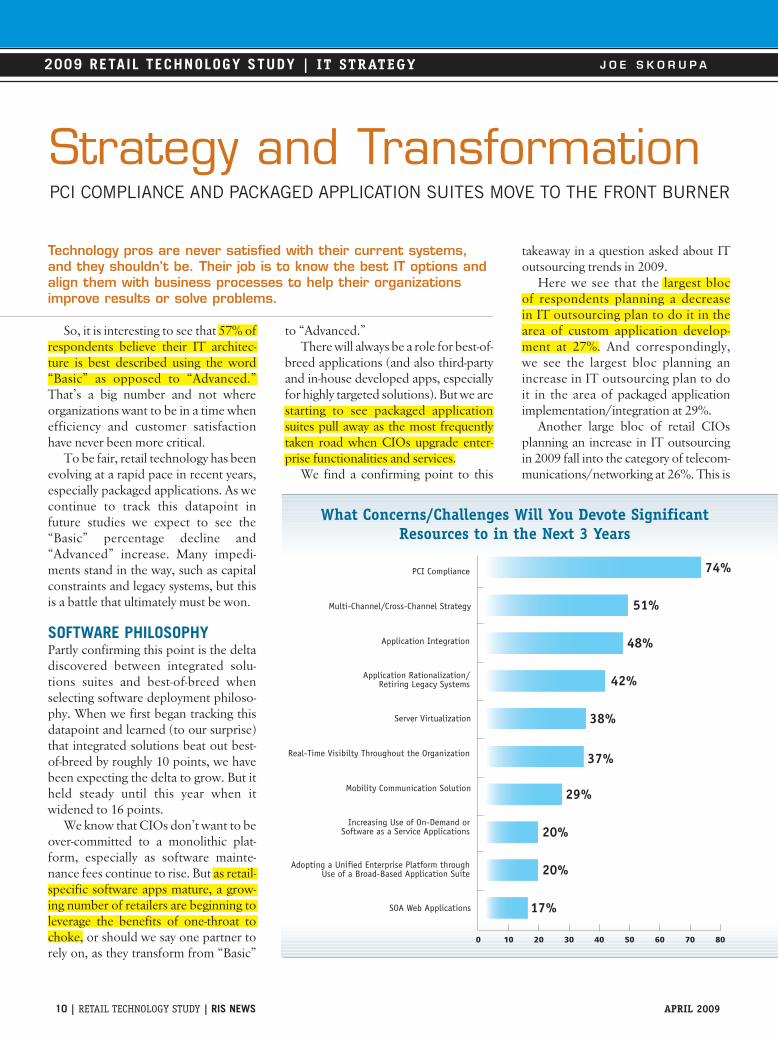

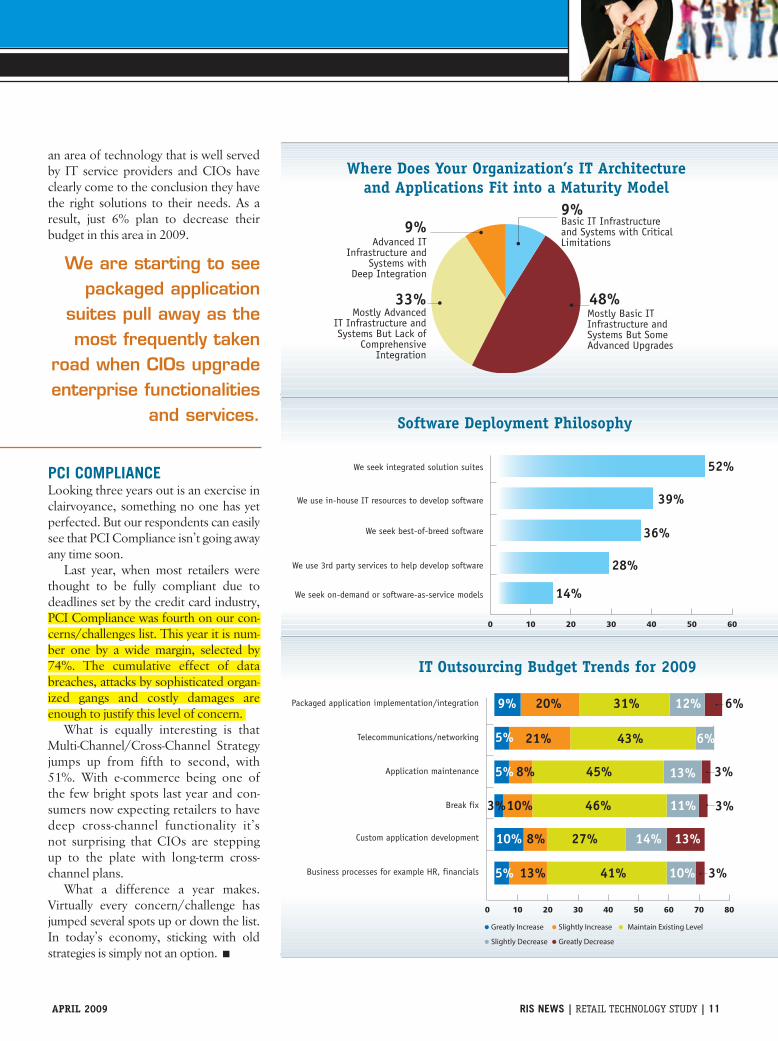

So, it is interesting to see that 57% ofrespondents believe their IT architec-ture is best described using the word“Basic” as opposed to “Advanced.”That’s a big number and not whereorganizations want to be in a time whenefficiency and customer satisfactionhave never been more critical.

To be fair, retail technology has beenevolving at a rapid pace in recent years,especially packaged applications. As wecontinue to track this datapoint infuture studies we expect to see the“Basic” percentage decline and“Advanced” increase. Many impedi-ments stand in the way, such as capitalconstraints and legacy systems, but thisis a battle that ultimately must be won.

SOFTWARE PHILOSOPHYPartly confirming this point is the deltadiscovered between integrated solu-tions suites and best-of-breed whenselecting software deployment philoso-phy. When we first began tracking thisdatapoint and learned (to our surprise)that integrated solutions beat out best-of-breed by roughly 10 points, we havebeen expecting the delta to grow. But itheld steady until this year when itwidened to 16 points.

We know that CIOs don’t want to beover-committed to a monolithic plat-form, especially as software mainte-nance fees continue to rise. But as retail-specific software apps mature, a grow-ing number of retailers are beginning toleverage the benefits of one-throat tochoke, or should we say one partner torely on, as they transform from “Basic”

to “Advanced.”There will always be a role for best-of-

breed applications (and also third-partyand in-house developed apps, especiallyfor highly targeted solutions). But we arestarting to see packaged applicationsuites pull away as the most frequentlytaken road when CIOs upgrade enter-prise functionalities and services.

We find a confirming point to this

takeaway in a question asked about IToutsourcing trends in 2009.

Here we see that the largest blocof respondents planning a decreasein IT outsourcing plan to do it in thearea of custom application develop-ment at 27%. And correspondingly,we see the largest bloc planning anincrease in IT outsourcing plan to doit in the area of packaged applicationimplementation/integration at 29%.

Another large bloc of retail CIOsplanning an increase in IT outsourcingin 2009 fall into the category of telecom-munications/networking at 26%. This is

10 | RETAIL TECHNOLOGY STUDY | RIS NEWS APRIL 2009

2009 RETAIL TECHNOLOGY STUDY | IT STRATEGY J O E S K O R U P A

Technology pros are never satisfied with their current systems,and they shouldn’t be. Their job is to know the best IT options andalign them with business processes to help their organizationsimprove results or solve problems.

Strategy and TransformationPCI COMPLIANCE AND PACKAGED APPLICATION SUITES MOVE TO THE FRONT BURNER

0 10 20 30 40 50 60 70 80

SOA Web Applications 17%

Increasing Use of On-Demand orSoftware as a Service Applications 20%

Adopting a Unified Enterprise Platform throughUse of a Broad-Based Application Suite 20%

Server Virtualization 38%

Real-Time Visibilty Throughout the Organization 37%

Mobility Communication Solution 29%

Multi-Channel/Cross-Channel Strategy 51%

Application Integration 48%

Application Rationalization/Retiring Legacy Systems 42%

PCI Compliance 74%

What Concerns/Challenges Will You Devote SignificantResources to in the Next 3 Years

10_strategy_rts0409_v3 3/19/09 5:12 PM Page 1

APRIL 2009 RIS NEWS | RETAIL TECHNOLOGY STUDY | 11

an area of technology that is well servedby IT service providers and CIOs haveclearly come to the conclusion they havethe right solutions to their needs. As aresult, just 6% plan to decrease theirbudget in this area in 2009.

PCI COMPLIANCELooking three years out is an exercise inclairvoyance, something no one has yetperfected. But our respondents can easilysee that PCI Compliance isn’t going awayany time soon.

Last year, when most retailers werethought to be fully compliant due todeadlines set by the credit card industry,PCI Compliance was fourth on our con-cerns/challenges list. This year it is num-ber one by a wide margin, selected by74%. The cumulative effect of databreaches, attacks by sophisticated organ-ized gangs and costly damages areenough to justify this level of concern.

What is equally interesting is thatMulti-Channel/Cross-Channel Strategyjumps up from fifth to second, with51%. With e-commerce being one ofthe few bright spots last year and con-sumers now expecting retailers to havedeep cross-channel functionality it’snot surprising that CIOs are steppingup to the plate with long-term cross-channel plans.

What a difference a year makes.Virtually every concern/challenge hasjumped several spots up or down the list.In today’s economy, sticking with oldstrategies is simply not an option. ■

0 10 20 30 40 50 60

We use in-house IT resources to develop software 39%

28%We use 3rd party services to help develop software

We seek on-demand or software-as-service models 14%

We seek integrated solution suites 52%

We seek best-of-breed software 36%

Software Deployment Philosophy

Packaged application implementation/integration 9% 20% 31% 12% 6%

0 10 20 30 40 50 60 70 80

Custom application development 27% 14% 13%8%10%

Telecommunications/networking 5% 21% 43% 6%

Business processes for example HR, financials 5% 13% 41% 10% 3%

Application maintenance 5% 8% 45% 3%13%

Break fix 3%10% 46% 11% 3%

Greatly Increase

Slightly Decrease Greatly Decrease

Slightly Increase Maintain Existing Level

IT Outsourcing Budget Trends for 2009

Basic IT Infrastructureand Systems with CriticalLimitations

9%

Advanced ITInfrastructure and

Systems withDeep Integration

9%

Mostly Basic ITInfrastructure and Systems But Some Advanced Upgrades

48%Mostly Advanced

IT Infrastructure andSystems But Lack of

ComprehensiveIntegration

33%

Where Does Your Organization’s IT Architecture and Applications Fit into a Maturity Model

We are starting to seepackaged application

suites pull away as themost frequently taken

road when CIOs upgradeenterprise functionalities

and services.

10_strategy_rts0409_v3 3/19/09 5:12 PM Page 2

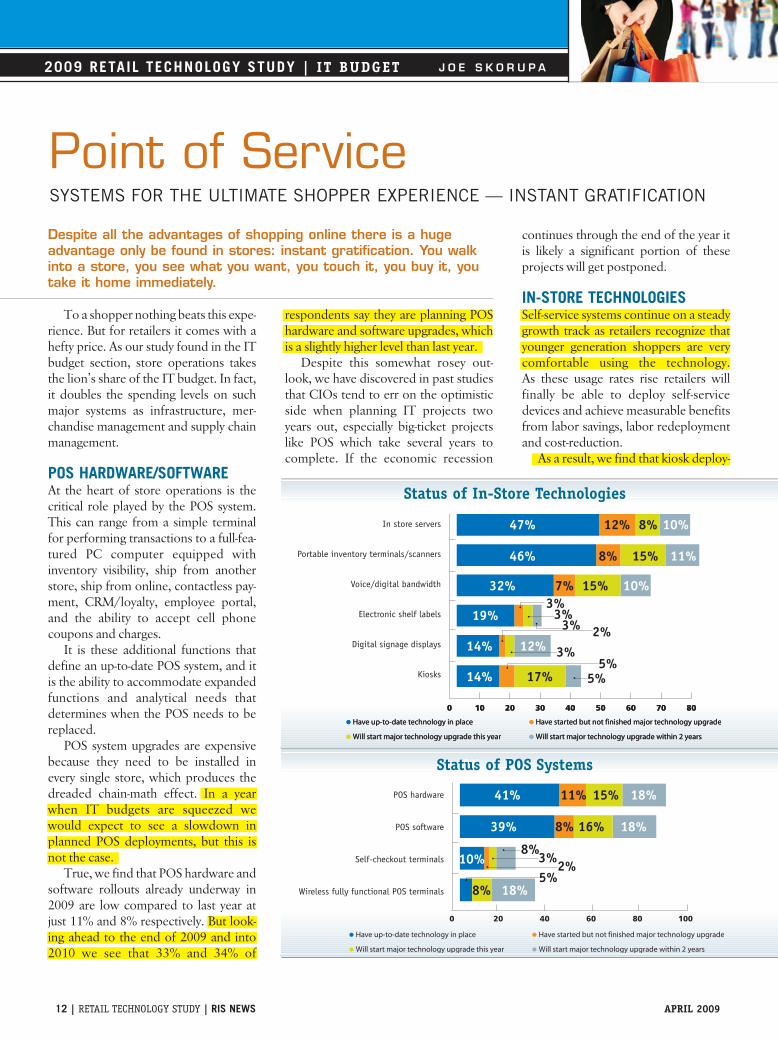

To a shopper nothing beats this expe-rience. But for retailers it comes with ahefty price. As our study found in the ITbudget section, store operations takesthe lion’s share of the IT budget. In fact,it doubles the spending levels on suchmajor systems as infrastructure, mer-chandise management and supply chainmanagement.

POS HARDWARE/SOFTWAREAt the heart of store operations is thecritical role played by the POS system.This can range from a simple terminalfor performing transactions to a full-fea-tured PC computer equipped withinventory visibility, ship from anotherstore, ship from online, contactless pay-ment, CRM/loyalty, employee portal,and the ability to accept cell phonecoupons and charges.

It is these additional functions thatdefine an up-to-date POS system, and itis the ability to accommodate expandedfunctions and analytical needs thatdetermines when the POS needs to bereplaced.

POS system upgrades are expensivebecause they need to be installed inevery single store, which produces thedreaded chain-math effect. In a yearwhen IT budgets are squeezed wewould expect to see a slowdown inplanned POS deployments, but this isnot the case.

True, we find that POS hardware andsoftware rollouts already underway in2009 are low compared to last year atjust 11% and 8% respectively. But look-ing ahead to the end of 2009 and into2010 we see that 33% and 34% of

respondents say they are planning POShardware and software upgrades, whichis a slightly higher level than last year.

Despite this somewhat rosey out-look, we have discovered in past studiesthat CIOs tend to err on the optimisticside when planning IT projects twoyears out, especially big-ticket projectslike POS which take several years tocomplete. If the economic recession

continues through the end of the year itis likely a significant portion of theseprojects will get postponed.

IN-STORE TECHNOLOGIESSelf-service systems continue on a steadygrowth track as retailers recognize thatyounger generation shoppers are verycomfortable using the technology. As these usage rates rise retailers willfinally be able to deploy self-servicedevices and achieve measurable benefitsfrom labor savings, labor redeploymentand cost-reduction.

As a result, we find that kiosk deploy-

12 | RETAIL TECHNOLOGY STUDY | RIS NEWS APRIL 2009

2009 RETAIL TECHNOLOGY STUDY | IT BUDGET J O E S K O R U P A

Despite all the advantages of shopping online there is a hugeadvantage only be found in stores: instant gratification. You walkinto a store, you see what you want, you touch it, you buy it, youtake it home immediately.

Point of ServiceSYSTEMS FOR THE ULTIMATE SHOPPER EXPERIENCE — INSTANT GRATIFICATION

POS hardware

POS software

Self-checkout terminals

Wireless fully functional POS terminals

9%

41% 11% 15% 18%

39% 8% 16% 18%

10%

18%8%

2%8%

3%5%

0 20 40 60 80 100

Have up-to-date technology in place

Will start major technology upgrade this year Will start major technology upgrade within 2 years

Have started but not finished major technology upgrade

Status of POS Systems

0 10 20 30 40 50 60 70 80

I

Have up-to-date technology in place

Will start major technology upgrade this year Will start major technology upgrade within 2 years

Have started but not finished major technology upgrade

0 10 20 30 40 50 60 70 80

In store servers

Portable inventory terminals/scanners

Voice/digital bandwidth

Electronic shelf labels

Digital signage displays

Kiosks

9%

47%

46% 8% 15% 11%

12% 8% 10%

32% 7% 15% 10%

19%3%3%3% 2%

3%12%14%

14%5%

17% 5%

Have up-to-date technology in place

Will start major technology upgrade this year Will start major technology upgrade within 2 years

Have started but not finished major technology upgrade

Status of In-Store Technologies

12_posStore_rts0409_v2 3/19/09 5:16 PM Page 1

ment at 22% over the next two yearsshows strong growth plans and only getsbeaten among in-store technologies bysuch necessities as voice/digital band-width (25%) and portable inventory ter-minals (26%).

Not all retail verticals today embraceself-service technology, but as someonepointed out recently, if Wegman’s isfinally piloting self-service POS then wehave crossed a major threshold and wide-spread acceptance can’t be too far away.(Wegman’s, a high-touch, up-scale region-al grocer with a strong emphasis on a per-

sonalized customer experience, has beenfamous for resisting any technology thatsits between its well trained staff and itsbeloved shoppers.)

For a number of years we categorizedbiometric payments as an emerging tech-nology, but its growth track has stalledjust as surely as has RFID in the supplychain. It didn’t help that a major biomet-ric vendor suddenly went bankrupt lastyear, but the larger issue is lack of shop-per acceptance. In the future we may feelmore comfortable relying on fingerprint,iris, palm or facial scans for identity

recognition, but that day is still severalyears ahead of us.

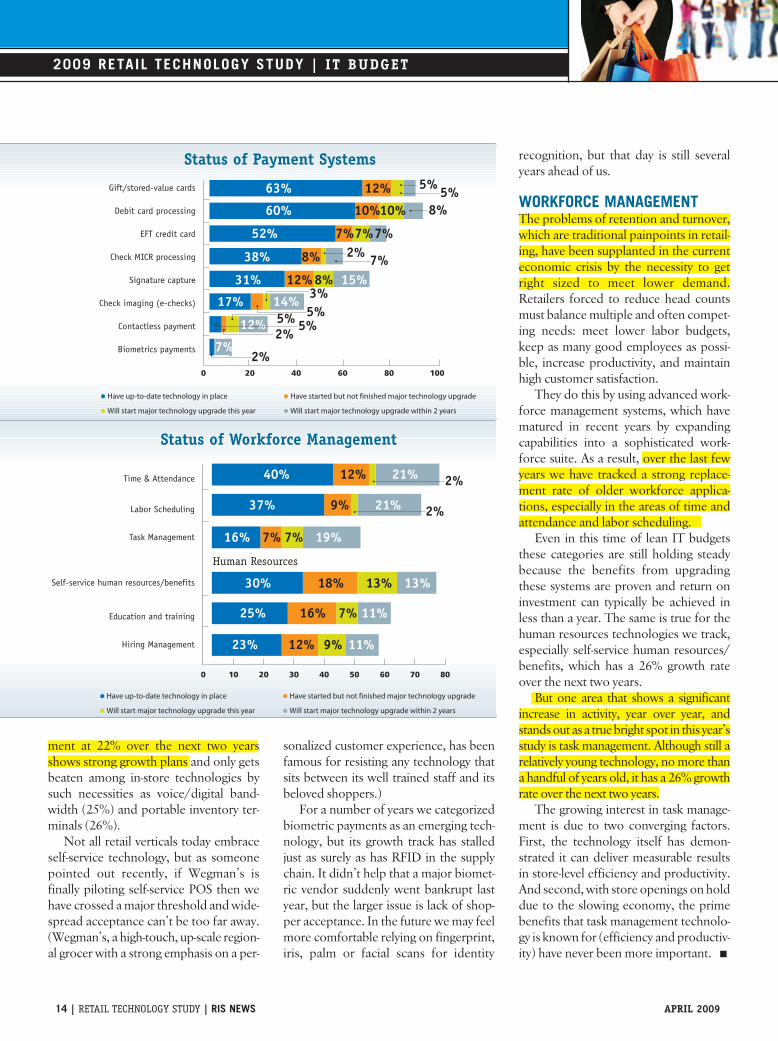

WORKFORCE MANAGEMENTThe problems of retention and turnover,which are traditional painpoints in retail-ing, have been supplanted in the currenteconomic crisis by the necessity to getright sized to meet lower demand.Retailers forced to reduce head countsmust balance multiple and often compet-ing needs: meet lower labor budgets,keep as many good employees as possi-ble, increase productivity, and maintainhigh customer satisfaction.

They do this by using advanced work-force management systems, which havematured in recent years by expandingcapabilities into a sophisticated work-force suite. As a result, over the last fewyears we have tracked a strong replace-ment rate of older workforce applica-tions, especially in the areas of time andattendance and labor scheduling.

Even in this time of lean IT budgetsthese categories are still holding steadybecause the benefits from upgradingthese systems are proven and return oninvestment can typically be achieved inless than a year. The same is true for thehuman resources technologies we track,especially self-service human resources/benefits, which has a 26% growth rateover the next two years.

But one area that shows a significantincrease in activity, year over year, andstands out as a true bright spot in this year’sstudy is task management. Although still arelatively young technology, no more thana handful of years old, it has a 26% growthrate over the next two years.

The growing interest in task manage-ment is due to two converging factors.First, the technology itself has demon-strated it can deliver measurable resultsin store-level efficiency and productivity.And second, with store openings on holddue to the slowing economy, the primebenefits that task management technolo-gy is known for (efficiency and productiv-ity) have never been more important. ■

Gift/stored-value cards

Debit card processing

EFT credit card

Check MICR processing

Signature capture

Check imaging (e-checks)

Contactless payment

Biometrics payments

0 20 40 60 80 100

63% 12%

60% 10%10%

52% 7%7%7%

38% 8%

31% 12%8% 15%

17%

5%

8%5%

2% 7%

3%5%

14%

12% 5%2%

5%

2%7%

Have up-to-date technology in place

Will start major technology upgrade this year Will start major technology upgrade within 2 years

Have started but not finished major technology upgrade

Status of Payment Systems

2009 RETAIL TECHNOLOGY STUDY | IT BUDGET

14 | RETAIL TECHNOLOGY STUDY | RIS NEWS APRIL 2009

Time & Attendance

Labor Scheduling

Self-service human resources/benefits

63%

0 10 20 30 40 50 60 70 80

40%

37%

12% 21% 2%

30% 18% 13% 13%

Education and training 25% 16% 7% 11%

Hiring Management17%

23% 12% 9% 11%

Task Management 16% 7% 7% 19%

2%9% 21%

Human Resources

Have up-to-date technology in place

Will start major technology upgrade this year Will start major technology upgrade within 2 years

Have started but not finished major technology upgrade

Status of Workforce Management

12_posStore_rts0409_v2 3/19/09 5:17 PM Page 2

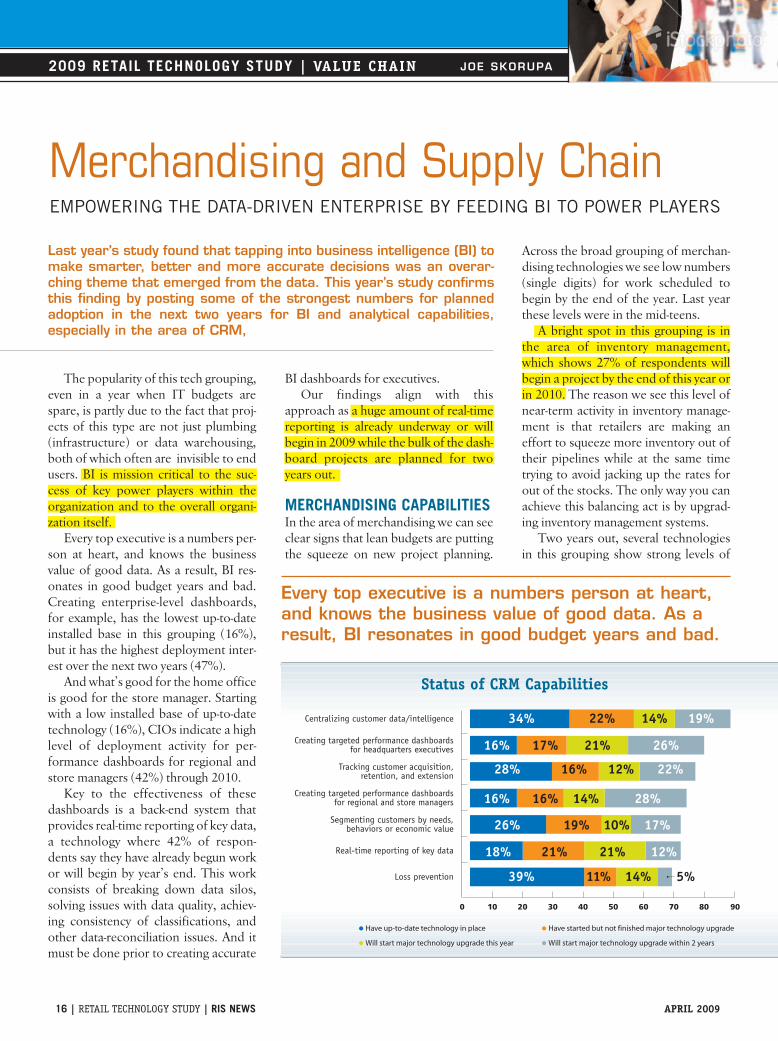

The popularity of this tech grouping,even in a year when IT budgets arespare, is partly due to the fact that proj-ects of this type are not just plumbing(infrastructure) or data warehousing,both of which often are invisible to endusers. BI is mission critical to the suc-cess of key power players within theorganization and to the overall organi-zation itself.

Every top executive is a numbers per-son at heart, and knows the businessvalue of good data. As a result, BI res-onates in good budget years and bad.Creating enterprise-level dashboards,for example, has the lowest up-to-dateinstalled base in this grouping (16%),but it has the highest deployment inter-est over the next two years (47%).

And what’s good for the home officeis good for the store manager. Startingwith a low installed base of up-to-datetechnology (16%), CIOs indicate a highlevel of deployment activity for per-formance dashboards for regional andstore managers (42%) through 2010.

Key to the effectiveness of thesedashboards is a back-end system thatprovides real-time reporting of key data,a technology where 42% of respon-dents say they have already begun workor will begin by year’s end. This workconsists of breaking down data silos,solving issues with data quality, achiev-ing consistency of classifications, andother data-reconciliation issues. And itmust be done prior to creating accurate

BI dashboards for executives. Our findings align with this

approach as a huge amount of real-timereporting is already underway or willbegin in 2009 while the bulk of the dash-board projects are planned for twoyears out.

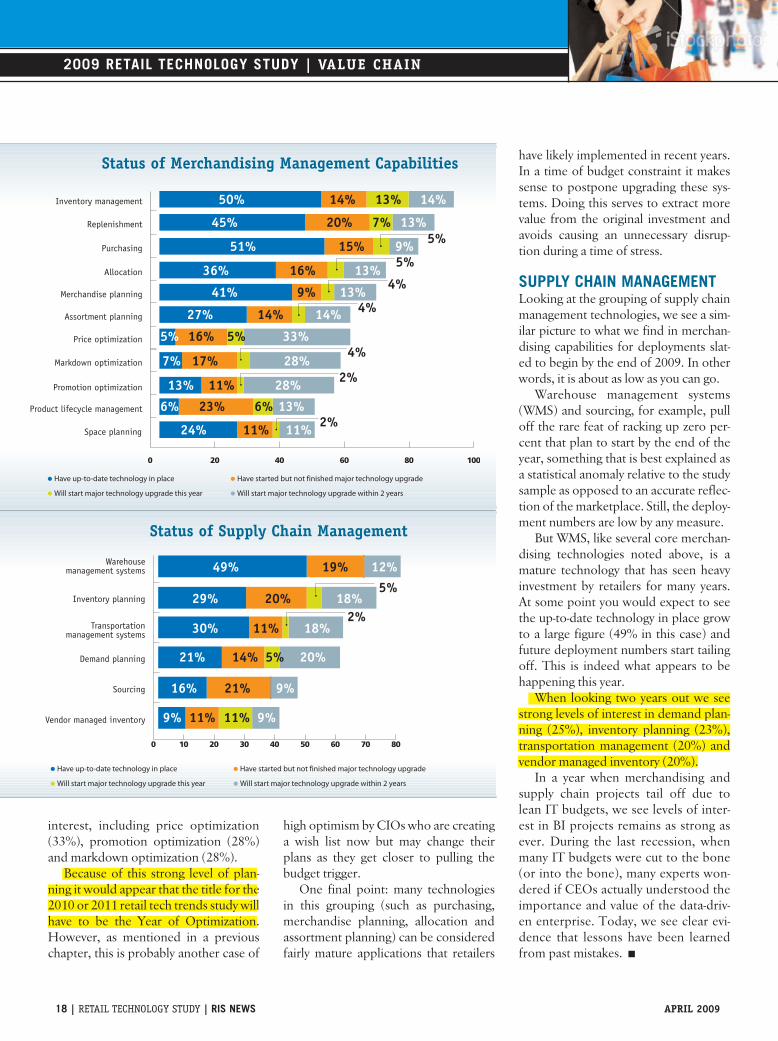

MERCHANDISING CAPABILITIESIn the area of merchandising we can seeclear signs that lean budgets are puttingthe squeeze on new project planning.

Across the broad grouping of merchan-dising technologies we see low numbers(single digits) for work scheduled tobegin by the end of the year. Last yearthese levels were in the mid-teens.

A bright spot in this grouping is inthe area of inventory management,which shows 27% of respondents willbegin a project by the end of this year orin 2010. The reason we see this level ofnear-term activity in inventory manage-ment is that retailers are making aneffort to squeeze more inventory out oftheir pipelines while at the same timetrying to avoid jacking up the rates forout of the stocks. The only way you canachieve this balancing act is by upgrad-ing inventory management systems.

Two years out, several technologiesin this grouping show strong levels of

16 | RETAIL TECHNOLOGY STUDY | RIS NEWS APRIL 2009

2009 RETAIL TECHNOLOGY STUDY | VALUE CHAIN JOE SKORUPA

Last year’s study found that tapping into business intelligence (BI) tomake smarter, better and more accurate decisions was an overar-ching theme that emerged from the data. This year’s study confirmsthis finding by posting some of the strongest numbers for plannedadoption in the next two years for BI and analytical capabilities,especially in the area of CRM,

Merchandising and Supply ChainEMPOWERING THE DATA-DRIVEN ENTERPRISE BY FEEDING BI TO POWER PLAYERS

Every top executive is a numbers person at heart,and knows the business value of good data. As aresult, BI resonates in good budget years and bad.

Have up-to-date technology in place

Will start major technology upgrade this year Will start major technology upgrade within 2 years

Have started but not finished major technology upgrade

0 10 20 30 40 50 60 70 80 90

Creating targeted performance dashboardsfor headquarters executives 16% 17% 21% 26%

Creating targeted performance dashboardsfor regional and store managers 16% 16% 14% 28%

Real-time reporting of key data 18% 21% 21% 12%

Segmenting customers by needs,behaviors or economic value 26% 19% 10% 17%

Tracking customer acquisition,retention, and extension 28% 16% 12% 22%

Centralizing customer data/intelligence 34% 22% 14% 19%

Loss prevention 39% 11% 14% 5%

Status of CRM Capabilities

16_merch_rts0409_v3 3/20/09 11:26 AM Page 1

interest, including price optimization(33%), promotion optimization (28%)and markdown optimization (28%).

Because of this strong level of plan-ning it would appear that the title for the2010 or 2011 retail tech trends study willhave to be the Year of Optimization.However, as mentioned in a previouschapter, this is probably another case of

high optimism by CIOs who are creatinga wish list now but may change theirplans as they get closer to pulling thebudget trigger.

One final point: many technologiesin this grouping (such as purchasing,merchandise planning, allocation andassortment planning) can be consideredfairly mature applications that retailers

have likely implemented in recent years.In a time of budget constraint it makessense to postpone upgrading these sys-tems. Doing this serves to extract morevalue from the original investment andavoids causing an unnecessary disrup-tion during a time of stress.

SUPPLY CHAIN MANAGEMENTLooking at the grouping of supply chainmanagement technologies, we see a sim-ilar picture to what we find in merchan-dising capabilities for deployments slat-ed to begin by the end of 2009. In otherwords, it is about as low as you can go.

Warehouse management systems(WMS) and sourcing, for example, pulloff the rare feat of racking up zero per-cent that plan to start by the end of theyear, something that is best explained asa statistical anomaly relative to the studysample as opposed to an accurate reflec-tion of the marketplace. Still, the deploy-ment numbers are low by any measure.

But WMS, like several core merchan-dising technologies noted above, is amature technology that has seen heavyinvestment by retailers for many years.At some point you would expect to seethe up-to-date technology in place growto a large figure (49% in this case) andfuture deployment numbers start tailingoff. This is indeed what appears to behappening this year.

When looking two years out we seestrong levels of interest in demand plan-ning (25%), inventory planning (23%),transportation management (20%) andvendor managed inventory (20%).

In a year when merchandising andsupply chain projects tail off due tolean IT budgets, we see levels of inter-est in BI projects remains as strong asever. During the last recession, whenmany IT budgets were cut to the bone(or into the bone), many experts won-dered if CEOs actually understood theimportance and value of the data-driv-en enterprise. Today, we see clear evi-dence that lessons have been learnedfrom past mistakes. ■

0 20 40 60 80 100

Product lifecycle management 6% 23% 6% 13%

Price optimization 5% 16% 33%5%

Replenishment 45% 20% 7% 13%

Inventory management 50% 14% 13% 14%

Purchasing5%51% 15% 9%

Merchandise planning 41% 9% 13% 4%Allocation 36% 16% 13%

5%

Assortment planning 27% 14% 14% 4%

Space planning 24% 11% 11% 2%

Promotion optimization 13% 11% 28% 2%Markdown optimization 7% 17% 28%

4%

Have up-to-date technology in place

Will start major technology upgrade this year Will start major technology upgrade within 2 years

Have started but not finished major technology upgrade

Status of Merchandising Management Capabilities

0 10 20 30 40 50 60 70 80

Vendor managed inventory 9% 11% 11% 9%

Sourcing 16% 21% 9%

Demand planning 21% 14% 5% 20%

Transportationmanagement systems

2%30% 11% 18%

Warehousemanagement systems 49% 19% 12%

Inventory planning 29% 20% 18%5%

Have up-to-date technology in place

Will start major technology upgrade this year Will start major technology upgrade within 2 years

Have started but not finished major technology upgrade

2009 RETAIL TECHNOLOGY STUDY | VALUE CHAIN

18 | RETAIL TECHNOLOGY STUDY | RIS NEWS APRIL 2009

Status of Supply Chain Management

16_merch_rts0409_v3 3/19/09 5:18 PM Page 2

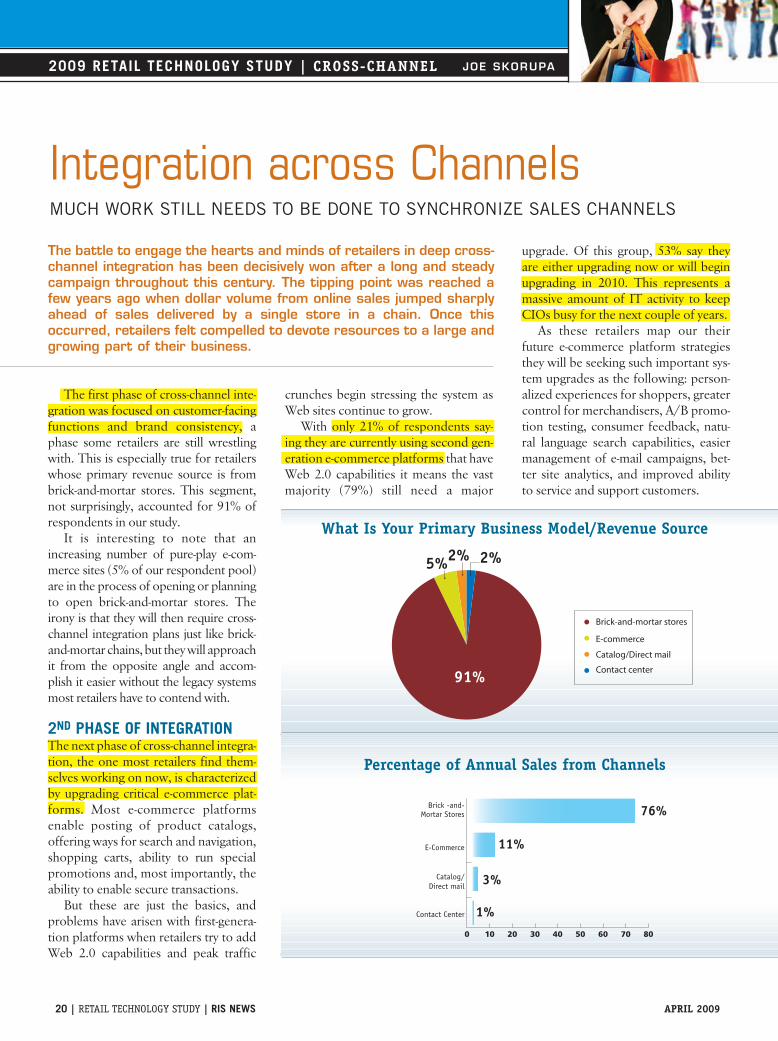

The first phase of cross-channel inte-gration was focused on customer-facingfunctions and brand consistency, aphase some retailers are still wrestlingwith. This is especially true for retailerswhose primary revenue source is frombrick-and-mortar stores. This segment,not surprisingly, accounted for 91% ofrespondents in our study.

It is interesting to note that anincreasing number of pure-play e-com-merce sites (5% of our respondent pool)are in the process of opening or planningto open brick-and-mortar stores. Theirony is that they will then require cross-channel integration plans just like brick-and-mortar chains, but they will approachit from the opposite angle and accom-plish it easier without the legacy systemsmost retailers have to contend with.

2ND PHASE OF INTEGRATIONThe next phase of cross-channel integra-tion, the one most retailers find them-selves working on now, is characterizedby upgrading critical e-commerce plat-forms. Most e-commerce platformsenable posting of product catalogs,offering ways for search and navigation,shopping carts, ability to run specialpromotions and, most importantly, theability to enable secure transactions.

But these are just the basics, andproblems have arisen with first-genera-tion platforms when retailers try to addWeb 2.0 capabilities and peak traffic

crunches begin stressing the system asWeb sites continue to grow.

With only 21% of respondents say-ing they are currently using second gen-eration e-commerce platforms that haveWeb 2.0 capabilities it means the vastmajority (79%) still need a major

upgrade. Of this group, 53% say theyare either upgrading now or will beginupgrading in 2010. This represents amassive amount of IT activity to keepCIOs busy for the next couple of years.

As these retailers map our theirfuture e-commerce platform strategiesthey will be seeking such important sys-tem upgrades as the following: person-alized experiences for shoppers, greatercontrol for merchandisers, A/B promo-tion testing, consumer feedback, natu-ral language search capabilities, easiermanagement of e-mail campaigns, bet-ter site analytics, and improved abilityto service and support customers.

20 | RETAIL TECHNOLOGY STUDY | RIS NEWS APRIL 2009

2009 RETAIL TECHNOLOGY STUDY | CROSS-CHANNEL JOE SKORUPA

The battle to engage the hearts and minds of retailers in deep cross-channel integration has been decisively won after a long and steadycampaign throughout this century. The tipping point was reached afew years ago when dollar volume from online sales jumped sharplyahead of sales delivered by a single store in a chain. Once thisoccurred, retailers felt compelled to devote resources to a large andgrowing part of their business.

Integration across ChannelsMUCH WORK STILL NEEDS TO BE DONE TO SYNCHRONIZE SALES CHANNELS

91%

5%2% 2%

E-commerce

Catalog/Direct mail

Contact center

Brick-and-mortar stores

What Is Your Primary Business Model/Revenue Source

Brick -and-Mortar Stores

E-Commerce

Catalog/Direct mail

Contact Center

76%

11%

3%

1%0 10 20 30 40 50 60 70 80

Percentage of Annual Sales from Channels

20_crossch_rts0409_v4 3/20/09 11:27 AM Page 1

THIRD PHASE OF INTEGRATIONAs previously noted, the dollar volumefrom e-commerce sales caught the atten-tion of C-level executives a few years agowhen it surpassed sales by a single store.Today, according to our respondents,the e-commerce figure is about 11% oftotal sales, with another 4% comingfrom catalog, direct mail and contactcenter sales.

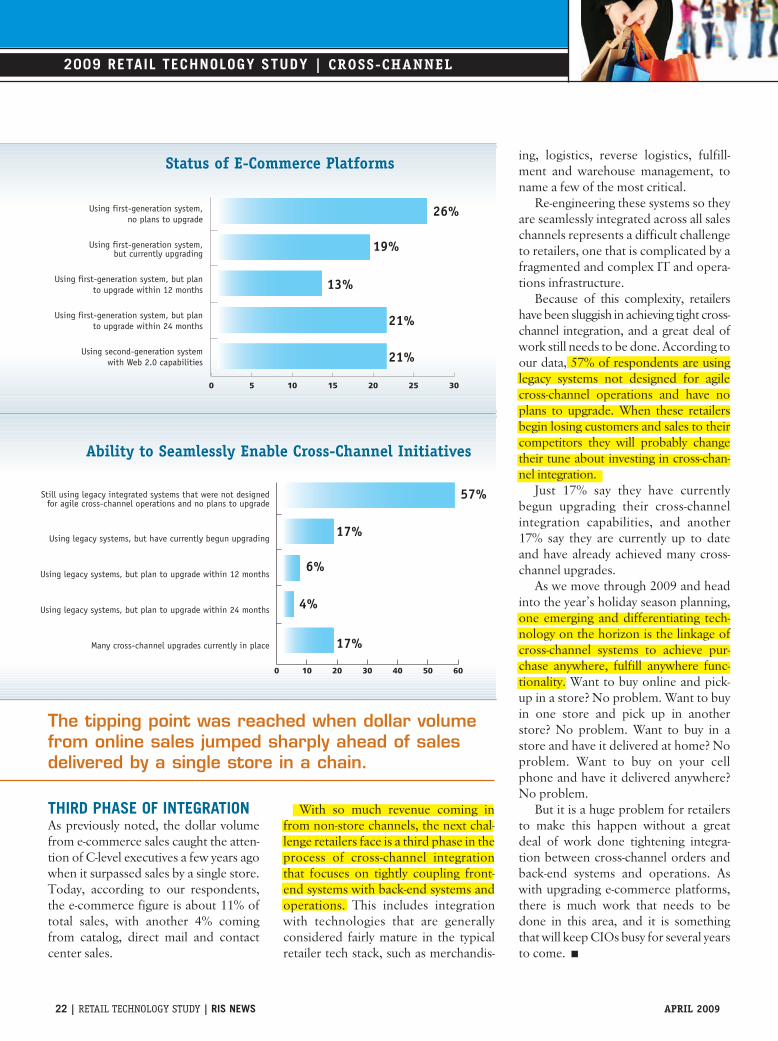

With so much revenue coming infrom non-store channels, the next chal-lenge retailers face is a third phase in theprocess of cross-channel integrationthat focuses on tightly coupling front-end systems with back-end systems andoperations. This includes integrationwith technologies that are generallyconsidered fairly mature in the typicalretailer tech stack, such as merchandis-

ing, logistics, reverse logistics, fulfill-ment and warehouse management, toname a few of the most critical.

Re-engineering these systems so theyare seamlessly integrated across all saleschannels represents a difficult challengeto retailers, one that is complicated by afragmented and complex IT and opera-tions infrastructure.

Because of this complexity, retailershave been sluggish in achieving tight cross-channel integration, and a great deal ofwork still needs to be done. According toour data, 57% of respondents are usinglegacy systems not designed for agilecross-channel operations and have noplans to upgrade. When these retailersbegin losing customers and sales to theircompetitors they will probably changetheir tune about investing in cross-chan-nel integration.

Just 17% say they have currentlybegun upgrading their cross-channelintegration capabilities, and another17% say they are currently up to dateand have already achieved many cross-channel upgrades.

As we move through 2009 and headinto the year’s holiday season planning,one emerging and differentiating tech-nology on the horizon is the linkage ofcross-channel systems to achieve pur-chase anywhere, fulfill anywhere func-tionality. Want to buy online and pick-up in a store? No problem. Want to buyin one store and pick up in anotherstore? No problem. Want to buy in astore and have it delivered at home? Noproblem. Want to buy on your cellphone and have it delivered anywhere?No problem.

But it is a huge problem for retailersto make this happen without a greatdeal of work done tightening integra-tion between cross-channel orders andback-end systems and operations. Aswith upgrading e-commerce platforms,there is much work that needs to bedone in this area, and it is somethingthat will keep CIOs busy for several yearsto come. ■

Using first-generation system,no plans to upgrade

Using first-generation system,but currently upgrading

Using first-generation system, but planto upgrade within 12 months

Using first-generation system, but planto upgrade within 24 months

Using second-generation systemwith Web 2.0 capabilities

0 5 10 15 20 25 30

26%

19%

13%

21%

21%

Status of E-Commerce Platforms

Still using legacy integrated systems that were not designedfor agile cross-channel operations and no plans to upgrade

Using legacy systems, but have currently begun upgrading

Using legacy systems, but plan to upgrade within 12 months

Using legacy systems, but plan to upgrade within 24 months

Many cross-channel upgrades currently in place

57%

17%

17%

0 10 20 30 40 50 60

6%

4%

2009 RETAIL TECHNOLOGY STUDY | CROSS-CHANNEL

Ability to Seamlessly Enable Cross-Channel Initiatives

22 | RETAIL TECHNOLOGY STUDY | RIS NEWS APRIL 2009

The tipping point was reached when dollar volumefrom online sales jumped sharply ahead of salesdelivered by a single store in a chain.

20_crossch_rts0409_v4 3/19/09 5:19 PM Page 2

Presented By

T H A N K Y O U T O T H E S P O N S O R S O F T H E S T U D YT H A N K Y O U T O T H E S P O N S O R S O F T H E S T U D Y

T I T L E S P O N S O R

S U P P O R T I N G S P O N S O R S

01_techtrends_0408_v2 3/23/09 10:00 AM Page 2