01 hoffmann applied solar expertise

32

PROSPECTS & CHALLENGES DURING INTRODUCTION OF NEW PRODUCTS IN THE PV MARKET Winfried Hoffmann Winfried Hoffmann President EPIA bifiPV Workshop Konstanz, 23rd April 2012

-

Upload

sandia-national-laboratories-energy-climate-renewables -

Category

Presentations & Public Speaking

-

view

347 -

download

0

Transcript of 01 hoffmann applied solar expertise

PROSPECTS & CHALLENGES DURING INTRODUCTION OF NEW PRODUCTS IN THE PV MARKET

Winfried HoffmannWinfried HoffmannPresident EPIA

bifiPV Workshop

Konstanz, 23rd April 2012

Applied Solar Expertise

Dr. Winfried Hoffmann – ASEPresident EPIA

SMA Management Board Representative to the EPIA

Member of the Supervisory Board of SMA Solar Technology AG

Member of Scientific Board of FhG-ISE and Supervisory Board of ISFH and Helmholtz

Customer Needs

… and market size from a GW perspective

on-grid off-grid consumer high efficiency

Small nichemainstream Small niche

3Bruxelles, 21 March 2012. 7th EPIA Market Workshop

€/kWh €/hr light W/m² g/W

Source: Fraunhofer ISE

€/m² / aesthetics €/W flexibility W/mm²

nicheSmall niche Small niche

Berlin 120419 Thin Film

c-Si Commercial Module Efficiency

Photon 2007 Module Survey Results

19.3

16.7

15.1

13.5 13.713.3

14.2 14.4 14.4 14.414.0 13.8

13.113.7

14.3

13.312.8

12

14

16

18

20

Effi

cien

cy (%

)

Error bars show mean efficiency for all products

specialized manufacturing Standard

Cells

4Bruxelles, 21 March 2012. 7th EPIA Market Workshop

0

2

4

6

8

10

12

Sun

pow

er

San

yo

BP

LG

BC BP

Sha

rp M

ono

Sha

rp M

ulti

Kyo

cera

Sun

tech

Mon

o

Sun

tech

Mul

ti

Mot

ech

Mon

o

Mot

ech

Mul

ti

Deu

tsch

e M

ono

Deu

tsch

e M

ulti

Mits

ubsh

i

JA

Sch

ott M

ulti

Sch

ott E

FG

Effi

cien

cy (%

)

7% B

deg

rada

tion

Source: Photon International, Mar-08

Crystalline Silicon PV Module Value Chain

Poly-SiFeedstockPoly-SiFeedstock

IngotProductionIngotProduction

CellProductionCellProduction

ModuleAssemblyModuleAssembly

Distribution,Integration &Installation

Distribution,Integration &Installation

MC

Wafer orSheetProduction

Wafer orSheetProduction

5Bruxelles, 21 March 2012. 7th EPIA Market Workshop

Cz

Berlin 120419 Thin Film

New products and processes for c-Si compared to mainstream products

Mainstream „new„new

Product“ orProcess“

Poly Si

Wafer

6Bruxelles, 21 March 2012. 7th EPIA Market Workshop

Cell

Module

New products and processes for c-Si compared to mainstream products

Mainstream „new„new

Product“ orProcess“

Poly Si Gas phasedestillation &Siemens reactor

- Same -

Fluidized Bed

mg-Si (no gas phase cleaning)

Wafer

7Bruxelles, 21 March 2012. 7th EPIA Market Workshop

Cell

Module

Solar Grade

PhysicochemicalPurification Process

High-Purity Silicon For Photovoltaic Energy Conversion

8Bruxelles, 21 March 2012. 7th EPIA Market Workshop

Source: PV Silicon AG, 2006

Quarzite

CokeMG-Si

ChemicalReactionHCI

SiCl4

SiHCl3SiH2Cl2

PurificationConversion

SiHCl3

SiH4

ThermalDecompositionCVD

Mod. EG-Silicon

Grade Silicon

Berlin 120419 Thin Film

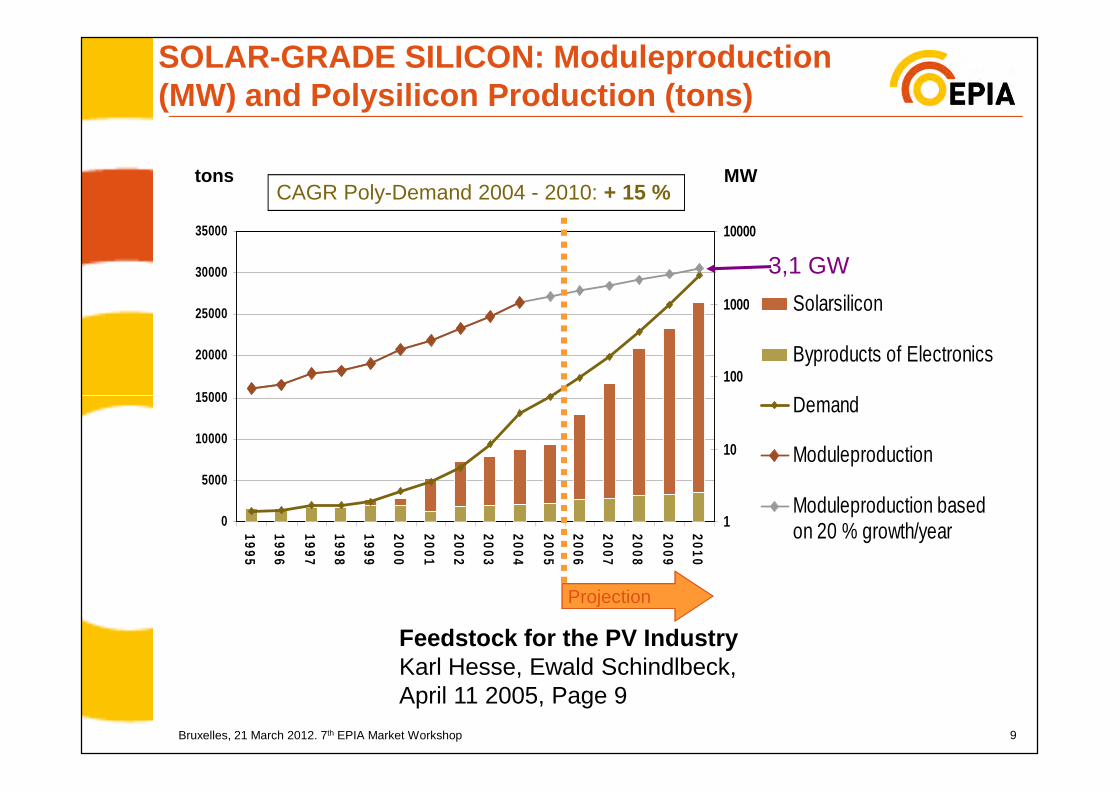

15000

20000

25000

30000

35000

100

1000

10000

Solarsilicon

Byproducts of Electronics

Demand

CAGR Poly-Demand 2004 - 2010: + 15 %

SOLAR-GRADE SILICON: Moduleproduction(MW) and Polysilicon Production (tons) AN NOT FOLLOW DEMAND – Perspectiv 2006.

tons MW

3,1 GW

9Bruxelles, 21 March 2012. 7th EPIA Market Workshop

Feedstock for the PV Industry Karl Hesse, Ewald Schindlbeck, April 11 2005, Page 9

0

5000

10000

15000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

1

10

Demand

Moduleproduction

Moduleproduction based on 20 % growth/year

Projection

New products and processes for c-Si compared to mainstream products

Mainstream „new„new

Product“ orProcess“

Poly Si Gas phasedestillation &Siemens reactor

- Same -

Fluidized Bed

mg-Si (no gas phase cleaning)

Wafer mc + Cz crystal & wire saw (slurry )

Multi goes monoDiamond coated

Ribbon

10Bruxelles, 21 March 2012. 7th EPIA Market Workshop

wire saw (slurry ) Diamond coatedwire (…TFX)

Cell

Module

Wafer Production EFG Technology withRWE SCHOTT Solar (2003)

conventional Technology

solidification

melting &crystallisation

EFG Technology

Silicon ribbon pull

11Bruxelles, 21 March 2012. 7th EPIA Market Workshop 11

Wafer cuttingSi ribbonsgrowth

Laser cutting

Si ribbons (disruptive in 70ies) versus mainstream wafer cutting

� when Mobile started EFG ribbon technology, wafer cutting by ID saws used about 1 mm crystal (0.5mm kerf loss, 0.5mm waferthickness)

� with the advent of wire saws the kerf loss and the waferthickness decreased by continuous development (volume!)

12Bruxelles, 21 March 2012. 7th EPIA Market Workshop

� in addition the crystallization technology, both Cz and mc, developed further, thereby reducing the €/kg ingot significantly

� The huge expansion in poly Si production decreased the priceper kg significantly

� the small, yet existent efficiency gap (~0.5% abs) added to theend of EFG technology in 2010 (cumulative spending about 500 m€)

New products and processes for c-Si compared to mainstream products

Mainstream „new„new

Product“ orProcess“

Poly Si Gas phasedestillation &Siemens reactor

- Same -

Fluidized Bed

mg-Si (no gas phase cleaning)

Wafer mc + Cz crystal & wire saw (slurry)

Multi goes monoDiamond coated wire ribbon

13Bruxelles, 21 March 2012. 7th EPIA Market Workshop

wire saw (slurry) Diamond coated wire ribbon

Cell f-/b- screen printedcell

Selective emitterBifiMIS-IL

MWTBack cont.

Module

Main stream versus disruptive cell technology

StartStd pn

Screen printSiN passivation

Disruptive 1Bc cell(SunPower)

Disruptive 2HIT(Sanyo)

time

14Bruxelles, 21 March 2012. 7th EPIA Market Workshop

Selective emitter

New passivation, laser, …

Today cumulative experience ca 60 GW Ca 3 GWCa 2 GW

Example main stream versus disruptive

MIS-IL solar cell (ISFH/NUKEM)

� industrialization of PECVD process for SiN AR andpassivation, necessary for MIS-IL, boosted mainstream (R&R SINA)

15Bruxelles, 21 March 2012. 7th EPIA Market Workshop

� evaporation of Al was demonstrated at pilot scalebut could not be transferred to high volumeproduction (lack of equipment for cost efficientmetalization at that time … things have changed bynow!)

� … new approach with US start-up

16Bruxelles, 21 March 2012. 7th EPIA Market Workshop

High Efficiency Solar Cells

Back contact for highest current

17Bruxelles, 21 March 2012. 7th EPIA Market Workshop

n-type base

18Bruxelles, 21 March 2012. 7th EPIA Market Workshop

19Bruxelles, 21 March 2012. 7th EPIA Market Workshop

20Bruxelles, 21 March 2012. 7th EPIA Market Workshop

21Bruxelles, 21 March 2012. 7th EPIA Market Workshop

New products and processes for c-Si compared to mainstream products

Mainstream „new„new

Product“ orProcess“

Poly Si Gas phasedestillation &Siemens reactor

- Same -

Fluidized Bed

mg-Si (no gas phase cleaning)

Wafer mc + Cz crystal & wire saw (slurry)

Multi goes monoDiamond coated wire ribbon

22Bruxelles, 21 March 2012. 7th EPIA Market Workshop

wire saw (slurry) Diamond coated wire ribbon

Cell f-/b- screen printedcell

Selective emitterBifiMIS-IL

MWTBack cont.

Module Glass – EVA –backfoil & lamination

Glass – new encaps– glass (1mm)

No laminationNo encapsmaterial

From Cell to Module Production

23Bruxelles, 21 March 2012. 7th EPIA Market Workshop

New products and processes for c-Si compared to mainstream products

Mainstream „new„new

Product“ orProcess“

Poly Si Gas phasedestillation &Siemens reactor

- Same -

Fluidized Bed

mg-Si (no gas phase cleaning)

Wafer mc + Cz crystal & wire saw (slurry )

Multi goes monoDiamond coated

Ribbon

24Bruxelles, 21 March 2012. 7th EPIA Market Workshop

wire saw (slurry ) Diamond coatedwire (…TFX)

Cell f-/b- screen printedcell

Selective emitterBifiMIS-IL

MWTBack cont.

Module Glass – EVA –backfoil & lamination

Glass – new encaps– glass (1mm)

No laminationNo encapsmaterial

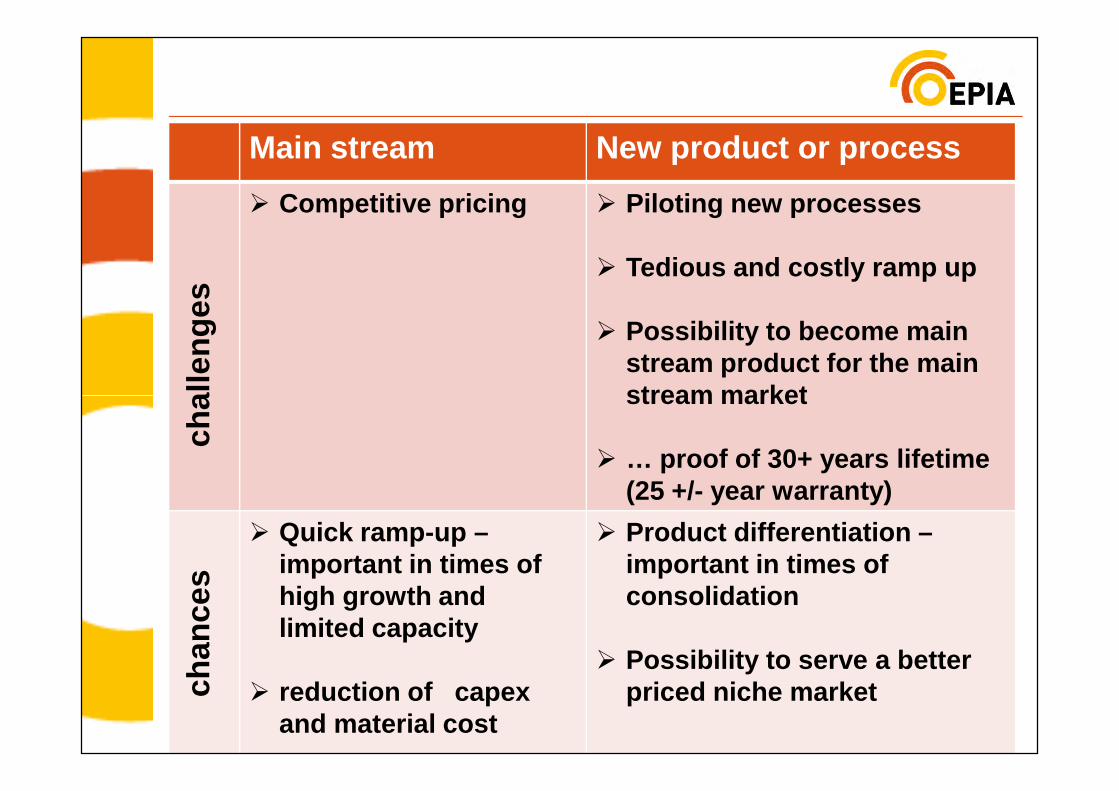

Main stream New product or process

chal

leng

es� Competitive pricing � Piloting new processes

� Tedious and costly ramp up

� Possibility to become mainstream product for the mainstream market

25Bruxelles, 21 March 2012. 7th EPIA Market Workshop

chal

leng

es

stream market

� … proof of 30+ years lifetime(25 +/- year warranty)

chan

ces

� Quick ramp-up –important in times ofhigh growth andlimited capacity

� reduction of capexand material cost

� Product differentiation –important in times ofconsolidation

� Possibility to serve a betterpriced niche market

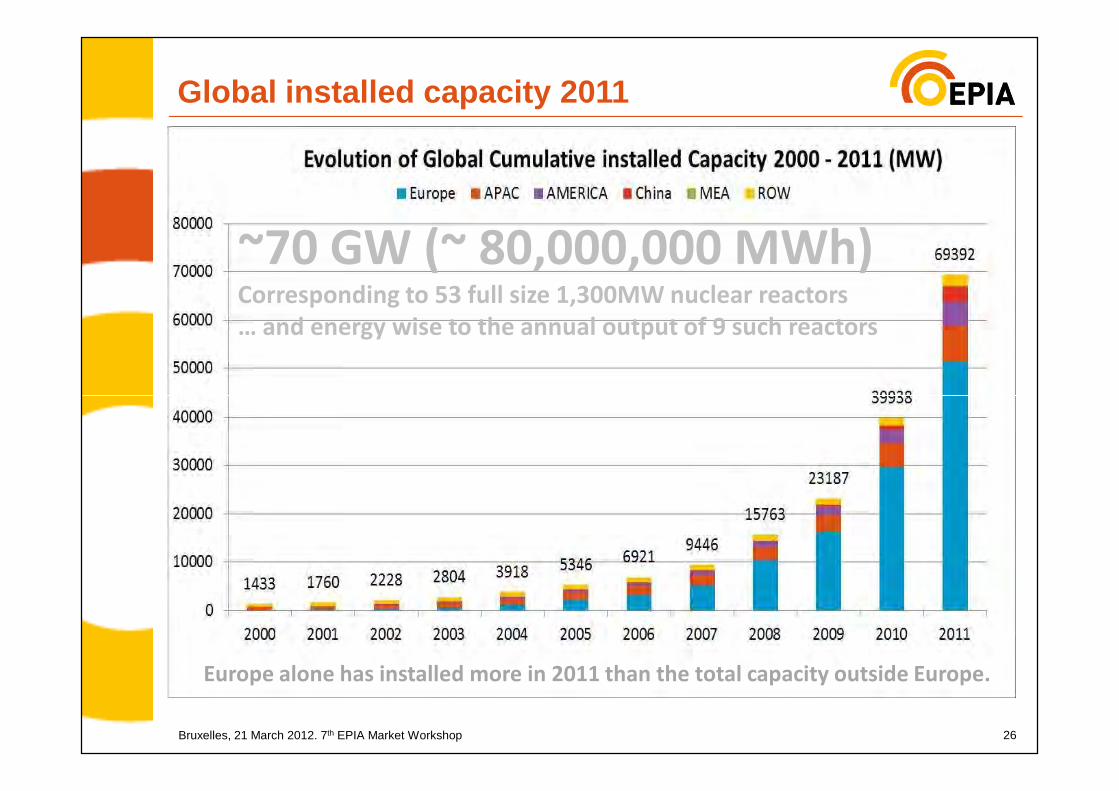

Global installed capacity 2011

~70 GW (~ 80,000,000 MWh)Corresponding to 53 full size 1,300MW nuclear reactors

… and energy wise to the annual output of 9 such reactors

26Bruxelles, 21 March 2012. 7th EPIA Market Workshop

Europe alone has installed more in 2011 than the total capacity outside Europe.

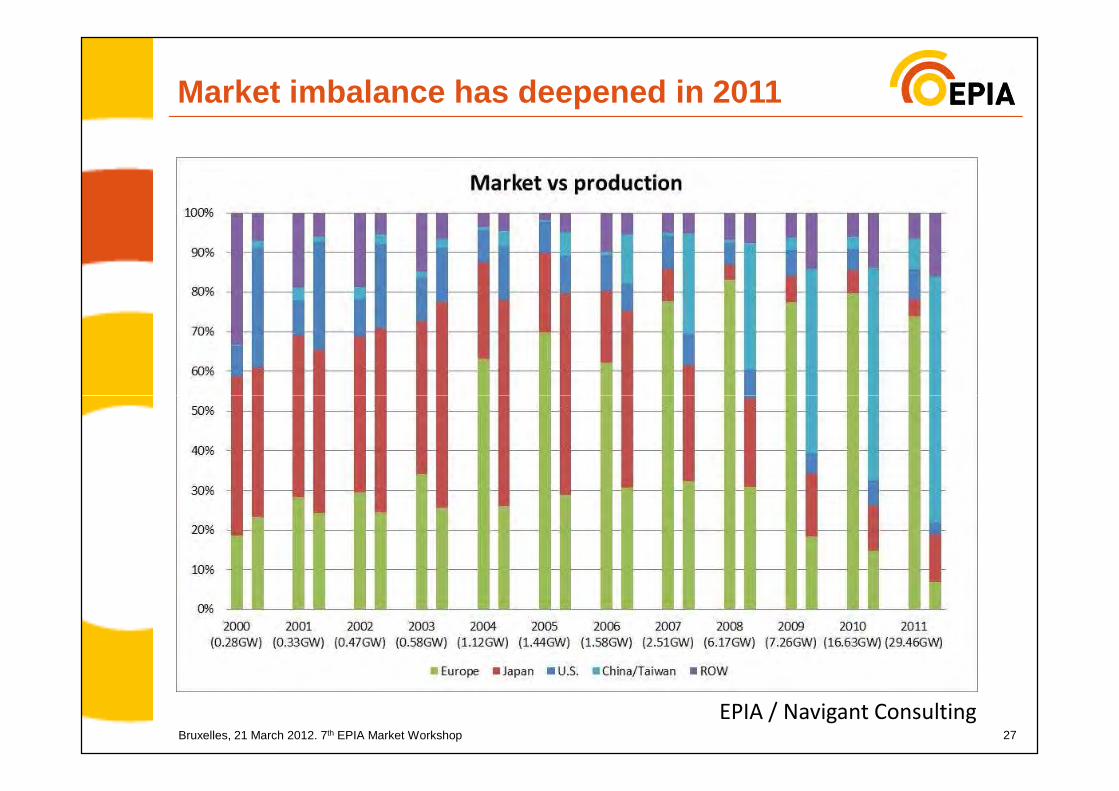

Market imbalance has deepened in 2011

27Bruxelles, 21 March 2012. 7th EPIA Market Workshop

EPIA / Navigant Consulting

1001980 2005 20081990 2000

Price Experience Curve

Photovoltaic

1. PEC for c-Si will continue

2. Reason for different PEC and PEF for Thin Film PV

28Bruxelles, 21 March 2012. 7th EPIA Market Workshop28

1

10

1,E+00 1,E+01 1,E+02 1,E+03 1,E+04 1,E+05

MW accumulated

AS

P in

$/W

PEF 20%

source: NAVIGANT

Thin Film

and PEF for Thin Film PV

3. Different growth rates forglobal PV installations asparameter

4. Different fraction of TF/c-Si as parameter

10,0

AS

P in

$/W

Case A – cSi 20%

PEC ScenarioCase A: BaselineTF share 15% constTF PEF 20%

Case B:Paradigm ShiftTF share 15% → 35%TF PEF 25%

10,0

AS

P in

$/W

Case B – cSi 20%c-Si Technology

price expectation in 2020

Photovoltaic –Future Price Development… with “healthy” module prices …

as of 2011/12

29Bruxelles, 21 March 2012. 7th EPIA Market Workshop

0,1

1,0

1,E+03 1,E+04 1,E+05 1,E+06

MW accumulated

AS

P in

$/W

Case A – TF 20%

0,1

1,0

1,E+03 1,E+04 1,E+05 1,E+06

MW accumulated

AS

P in

$/W

Case B – TF 25%

price expectation in 2020 ca. 60 – 80 $ct/W

Thin Film Technologyprice expectation in 2020

ca. 30 – 70 $ct/W

Technology Evolution

75

100

todayc-Si

TF

a-Si-pin/pin, II-VI

r/mgmc

Cz

+ (4 to 5) years *

SiIII -V

Mod

ule

pric

e (r

el. U

nits

)

r ribbon

mg metallurgicalgrade Silicon

mc multicrystalline

Cz Czochralski

30Bruxelles, 21 March 2012. 7th EPIA Market Workshop

ref: W. Hoffmann personal estimates

0 5 10 15 20 250

0 5 10 15 20 250

25

Module Efficiency [%]

a-Si/µc-Si,dye a-Si-pin

II-VI

r/mgmc

Cz+ (10 to 13) years *

50

30

Mod

ule

pric

e (r

el. U

nits

)

@ - (8 to 10) %price decrease per year

Beyond 20 years

OPV

Cz Czochralski

CPV concentrated PV

OPV organic PV

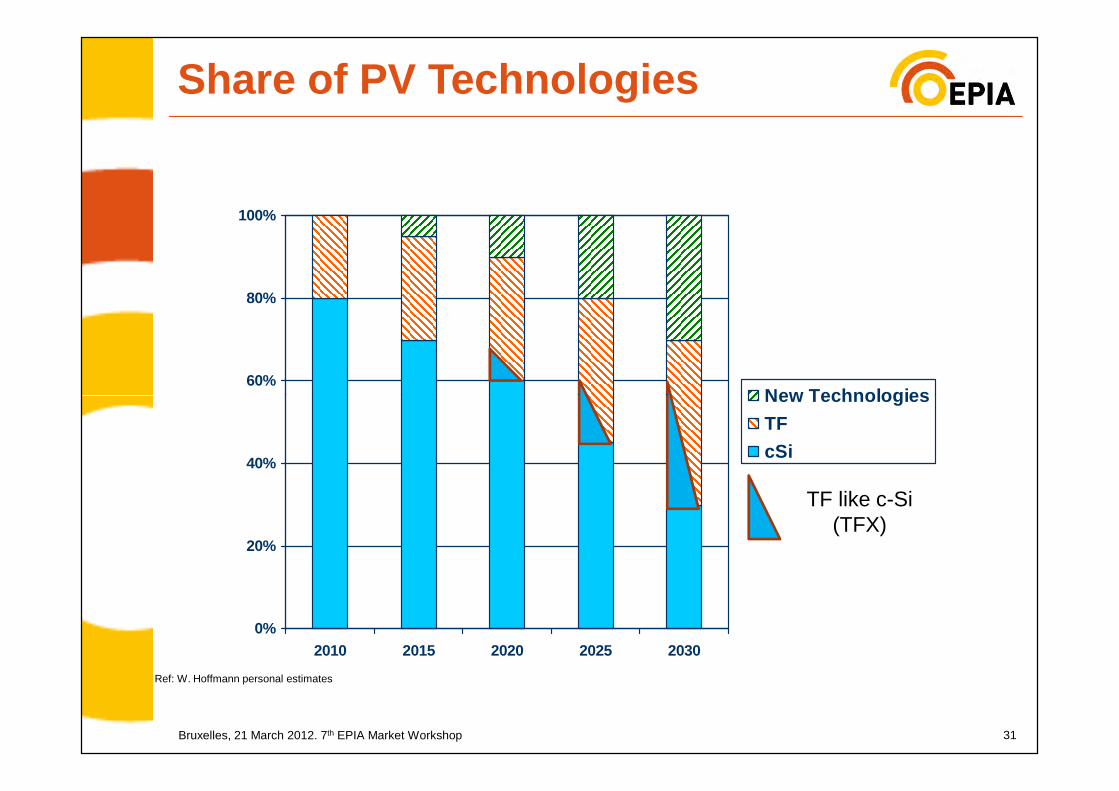

Share of PV Technologies

60%

80%

100%

New Technologies

31Bruxelles, 21 March 2012. 7th EPIA Market Workshop

0%

20%

40%

2010 2015 2020 2025 2030

New Technologies

TF

cSi

Ref: W. Hoffmann personal estimates

TF like c-Si(TFX)

www.epia.org