006508 - Guardian Life Insurance Company of America following text is derived from A.M. Best's...

33

006508 - Guardian Life Insurance Company of America Report Revision Date: 06/07/2017 Rating and Commentary 1 Best's Credit Rating: 06/07/2017 Rating Rationale: 06/07/2017 Report Commentary: 07/06/2016 Financial 2 Time Period: 2nd Quarter - 2017 Last Updated: 10/17/2017 Status: Quality Cross Checked General Information 3 Corporate Structure: 04/26/2017 States Licensed: 10/23/2001 Officers and Directors: 06/01/2017 Best's Credit Rating Methodology Disclaimer Best's Rating Guide Additional Online Resources Related News Archived AMB Credit Reports Rating Activity and Announcements Corporate Changes & Retirements Company Overview AMB Country Risk Reports - United States 1 The Rating and Commentary dates outline the most recent updates to the company's Best's Credit Rating, Rating Rationale, and Report Commentary for key rating and business changes. Report Commentary may include significant changes to the Business Profile, Risk Management, Operating Performance, Balance Sheet Strength, or Reinsurance sections of the report. 2 The Financial dates reflect the current status of the financial tables and charts found within the AMB Credit Report, including whether the data was loaded "As Received" or had been run through A.M. Best "Quality Cross Checks". 3 The General Information dates cover key changes made to Corporate Structure, States Licensed, or Officers and Directors. Page 1 of 33 Print Date: October 23, 2017

Transcript of 006508 - Guardian Life Insurance Company of America following text is derived from A.M. Best's...

006508 - Guardian Life Insurance Company ofAmerica

Report Revision Date: 06/07/2017

Rating and Commentary 1

Best's Credit Rating: 06/07/2017

Rating Rationale: 06/07/2017

Report Commentary: 07/06/2016

Financial 2

Time Period: 2nd Quarter - 2017

Last Updated: 10/17/2017

Status:Quality Cross Checked

General Information 3

Corporate Structure: 04/26/2017

States Licensed: 10/23/2001

Officers and Directors: 06/01/2017

Best's Credit Rating Methodology Disclaimer Best's Rating Guide

Additional Online Resources

Related News Archived AMB Credit Reports

Rating Activity and Announcements Corporate Changes & Retirements

Company Overview AMB Country Risk Reports - United States

1 The Rating and Commentary dates outline the most recent updates to the company's Best's Credit Rating, Rating Rationale, and Report Commentary for key rating andbusiness changes. Report Commentary may include significant changes to the Business Profile, Risk Management, Operating Performance, Balance Sheet Strength, or Reinsurancesections of the report.2 The Financial dates reflect the current status of the financial tables and charts found within the AMB Credit Report, including whether the data was loaded "As Received" orhad been run through A.M. Best "Quality Cross Checks".3 The General Information dates cover key changes made to Corporate Structure, States Licensed, or Officers and Directors.

Page 1 of 33 Print Date: October 23, 2017

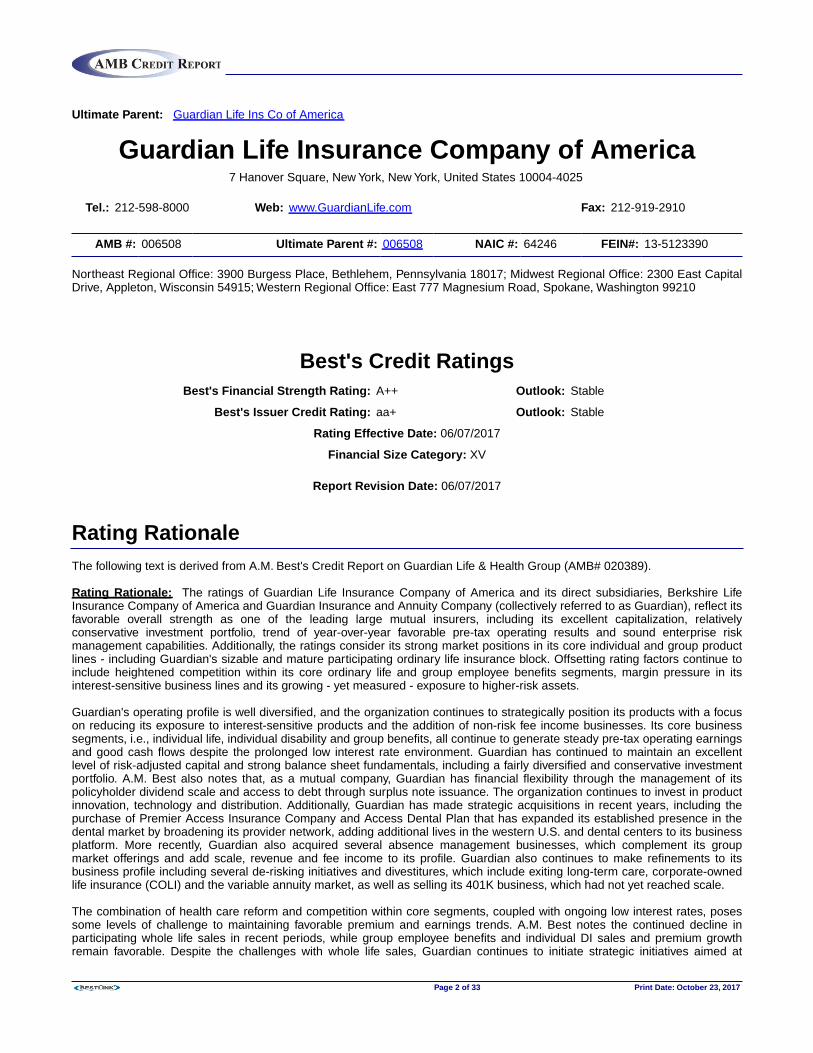

Ultimate Parent: Guardian Life Ins Co of America

Guardian Life Insurance Company of America7 Hanover Square, New York, New York, United States 10004-4025

Tel.: 212-598-8000 Web: www.GuardianLife.com Fax: 212-919-2910

AMB #: 006508 Ultimate Parent #: 006508 NAIC #: 64246 FEIN#: 13-5123390

Northeast Regional Office: 3900 Burgess Place, Bethlehem, Pennsylvania 18017; Midwest Regional Office: 2300 East CapitalDrive, Appleton, Wisconsin 54915; Western Regional Office: East 777 Magnesium Road, Spokane, Washington 99210

Best's Credit RatingsBest's Financial Strength Rating: A++ Outlook: Stable

Best's Issuer Credit Rating: aa+ Outlook: Stable

Rating Effective Date: 06/07/2017

Financial Size Category: XV

Report Revision Date: 06/07/2017

Rating RationaleThe following text is derived from A.M. Best's Credit Report on Guardian Life & Health Group (AMB# 020389).

Rating Rationale: The ratings of Guardian Life Insurance Company of America and its direct subsidiaries, Berkshire LifeInsurance Company of America and Guardian Insurance and Annuity Company (collectively referred to as Guardian), reflect itsfavorable overall strength as one of the leading large mutual insurers, including its excellent capitalization, relativelyconservative investment portfolio, trend of year-over-year favorable pre-tax operating results and sound enterprise riskmanagement capabilities. Additionally, the ratings consider its strong market positions in its core individual and group productlines - including Guardian's sizable and mature participating ordinary life insurance block. Offsetting rating factors continue toinclude heightened competition within its core ordinary life and group employee benefits segments, margin pressure in itsinterest-sensitive business lines and its growing - yet measured - exposure to higher-risk assets.

Guardian's operating profile is well diversified, and the organization continues to strategically position its products with a focuson reducing its exposure to interest-sensitive products and the addition of non-risk fee income businesses. Its core businesssegments, i.e., individual life, individual disability and group benefits, all continue to generate steady pre-tax operating earningsand good cash flows despite the prolonged low interest rate environment. Guardian has continued to maintain an excellentlevel of risk-adjusted capital and strong balance sheet fundamentals, including a fairly diversified and conservative investmentportfolio. A.M. Best also notes that, as a mutual company, Guardian has financial flexibility through the management of itspolicyholder dividend scale and access to debt through surplus note issuance. The organization continues to invest in productinnovation, technology and distribution. Additionally, Guardian has made strategic acquisitions in recent years, including thepurchase of Premier Access Insurance Company and Access Dental Plan that has expanded its established presence in thedental market by broadening its provider network, adding additional lives in the western U.S. and dental centers to its businessplatform. More recently, Guardian also acquired several absence management businesses, which complement its groupmarket offerings and add scale, revenue and fee income to its profile. Guardian also continues to make refinements to itsbusiness profile including several de-risking initiatives and divestitures, which include exiting long-term care, corporate-ownedlife insurance (COLI) and the variable annuity market, as well as selling its 401K business, which had not yet reached scale.

The combination of health care reform and competition within core segments, coupled with ongoing low interest rates, posessome levels of challenge to maintaining favorable premium and earnings trends. A.M. Best notes the continued decline inparticipating whole life sales in recent periods, while group employee benefits and individual DI sales and premium growthremain favorable. Despite the challenges with whole life sales, Guardian continues to initiate strategic initiatives aimed at

Page 2 of 33 Print Date: October 23, 2017

Rating Rationale (Continued...)supporting and growing its group dental, group life and disability business segments. Guardian had previously been impactedby the need to continue to invest in its retirement solutions business to reach critical mass and contribute meaningfully toconsolidated results. However, due to lack of scale the decision was ultimately made to exit this business via divestiture in2016. The company maintains a large block of variable and interest-sensitive life and annuity business, and the continued lowinterest rate environment is impacting these spread-based businesses and continuing to pressure Guardian's margins. Finally,A.M. Best notes that while Guardian's portfolio is mostly conservative and well diversified, the organization maintain a modestexposure to alternative higher-risk assets, including joint venture partnerships, high-yield bonds and real estate-linked assetsrelative to capital and surplus. Overall credit risk within the commercial real estate sector has been reduced and comparesfavorably to mutual peers.

A negative rating action could occur if Guardian were to experience a material decline in risk-adjusted capitalization, asustained decline in new business growth in its core individual and group insurance lines of business, and/or if operatingearnings deteriorate due to increased morbidity or mortality.

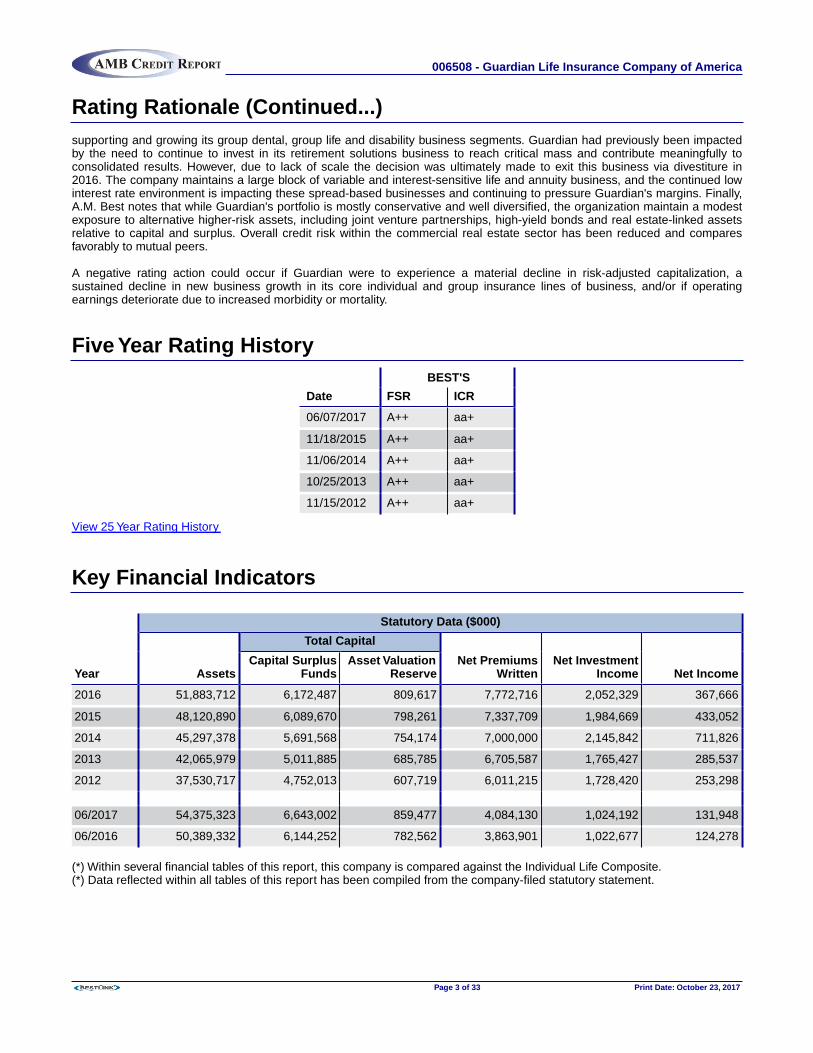

Five Year Rating HistoryBEST'S

Date FSR ICR

06/07/2017 A++ aa+

11/18/2015 A++ aa+

11/06/2014 A++ aa+

10/25/2013 A++ aa+

11/15/2012 A++ aa+

View 25 Year Rating History

Key Financial Indicators

Statutory Data ($000)

Total Capital

Year AssetsCapital Surplus

FundsAsset Valuation

ReserveNet Premiums

WrittenNet Investment

Income Net Income

2016 51,883,712 6,172,487 809,617 7,772,716 2,052,329 367,666

2015 48,120,890 6,089,670 798,261 7,337,709 1,984,669 433,052

2014 45,297,378 5,691,568 754,174 7,000,000 2,145,842 711,826

2013 42,065,979 5,011,885 685,785 6,705,587 1,765,427 285,537

2012 37,530,717 4,752,013 607,719 6,011,215 1,728,420 253,298

06/2017 54,375,323 6,643,002 859,477 4,084,130 1,024,192 131,948

06/2016 50,389,332 6,144,252 782,562 3,863,901 1,022,677 124,278

(*) Within several financial tables of this report, this company is compared against the Individual Life Composite.(*) Data reflected within all tables of this report has been compiled from the company-filed statutory statement.

006508 - Guardian Life Insurance Company of America

Page 3 of 33 Print Date: October 23, 2017

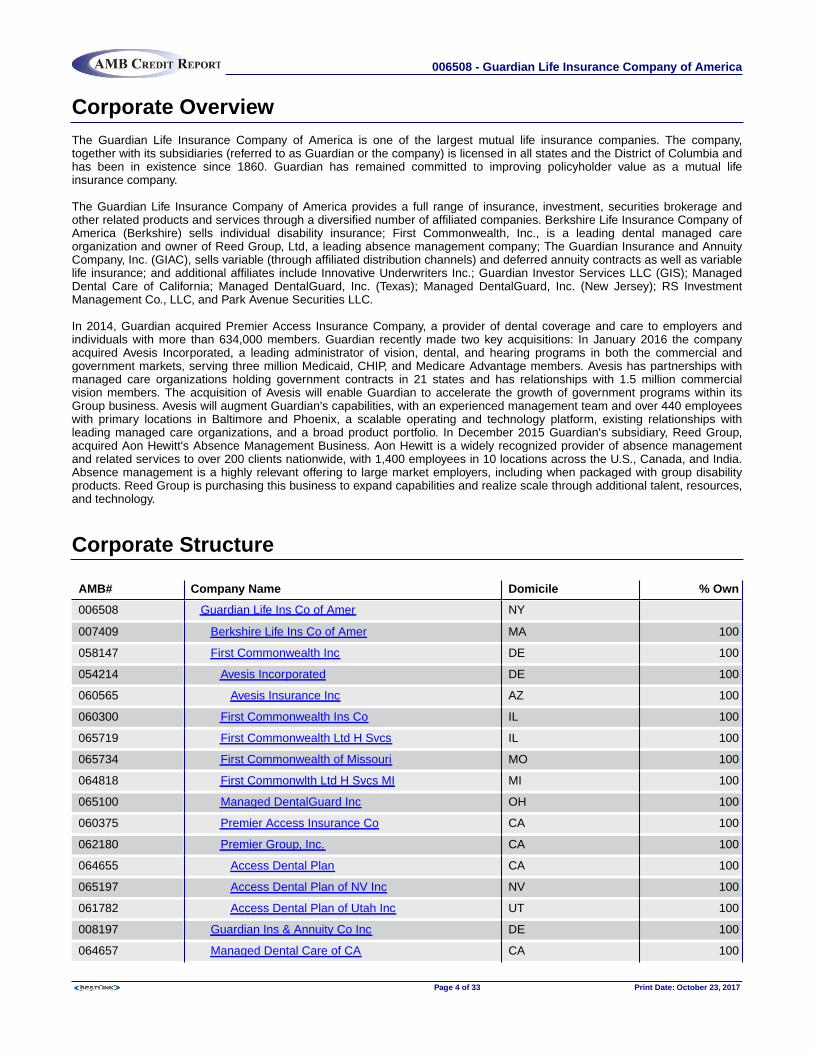

Corporate OverviewThe Guardian Life Insurance Company of America is one of the largest mutual life insurance companies. The company,together with its subsidiaries (referred to as Guardian or the company) is licensed in all states and the District of Columbia andhas been in existence since 1860. Guardian has remained committed to improving policyholder value as a mutual lifeinsurance company.

The Guardian Life Insurance Company of America provides a full range of insurance, investment, securities brokerage andother related products and services through a diversified number of affiliated companies. Berkshire Life Insurance Company ofAmerica (Berkshire) sells individual disability insurance; First Commonwealth, Inc., is a leading dental managed careorganization and owner of Reed Group, Ltd, a leading absence management company; The Guardian Insurance and AnnuityCompany, Inc. (GIAC), sells variable (through affiliated distribution channels) and deferred annuity contracts as well as variablelife insurance; and additional affiliates include Innovative Underwriters Inc.; Guardian Investor Services LLC (GIS); ManagedDental Care of California; Managed DentalGuard, Inc. (Texas); Managed DentalGuard, Inc. (New Jersey); RS InvestmentManagement Co., LLC, and Park Avenue Securities LLC.

In 2014, Guardian acquired Premier Access Insurance Company, a provider of dental coverage and care to employers andindividuals with more than 634,000 members. Guardian recently made two key acquisitions: In January 2016 the companyacquired Avesis Incorporated, a leading administrator of vision, dental, and hearing programs in both the commercial andgovernment markets, serving three million Medicaid, CHIP, and Medicare Advantage members. Avesis has partnerships withmanaged care organizations holding government contracts in 21 states and has relationships with 1.5 million commercialvision members. The acquisition of Avesis will enable Guardian to accelerate the growth of government programs within itsGroup business. Avesis will augment Guardian's capabilities, with an experienced management team and over 440 employeeswith primary locations in Baltimore and Phoenix, a scalable operating and technology platform, existing relationships withleading managed care organizations, and a broad product portfolio. In December 2015 Guardian's subsidiary, Reed Group,acquired Aon Hewitt's Absence Management Business. Aon Hewitt is a widely recognized provider of absence managementand related services to over 200 clients nationwide, with 1,400 employees in 10 locations across the U.S., Canada, and India.Absence management is a highly relevant offering to large market employers, including when packaged with group disabilityproducts. Reed Group is purchasing this business to expand capabilities and realize scale through additional talent, resources,and technology.

Corporate Structure

AMB# Company Name Domicile % Own

006508 Guardian Life Ins Co of Amer NY

007409 Berkshire Life Ins Co of Amer MA 100

058147 First Commonwealth Inc DE 100

054214 Avesis Incorporated DE 100

060565 Avesis Insurance Inc AZ 100

060300 First Commonwealth Ins Co IL 100

065719 First Commonwealth Ltd H Svcs IL 100

065734 First Commonwealth of Missouri MO 100

064818 First Commonwlth Ltd H Svcs MI MI 100

065100 Managed DentalGuard Inc OH 100

060375 Premier Access Insurance Co CA 100

062180 Premier Group, Inc. CA 100

064655 Access Dental Plan CA 100

065197 Access Dental Plan of NV Inc NV 100

061782 Access Dental Plan of Utah Inc UT 100

008197 Guardian Ins & Annuity Co Inc DE 100

064657 Managed Dental Care of CA CA 100

006508 - Guardian Life Insurance Company of America

Page 4 of 33 Print Date: October 23, 2017

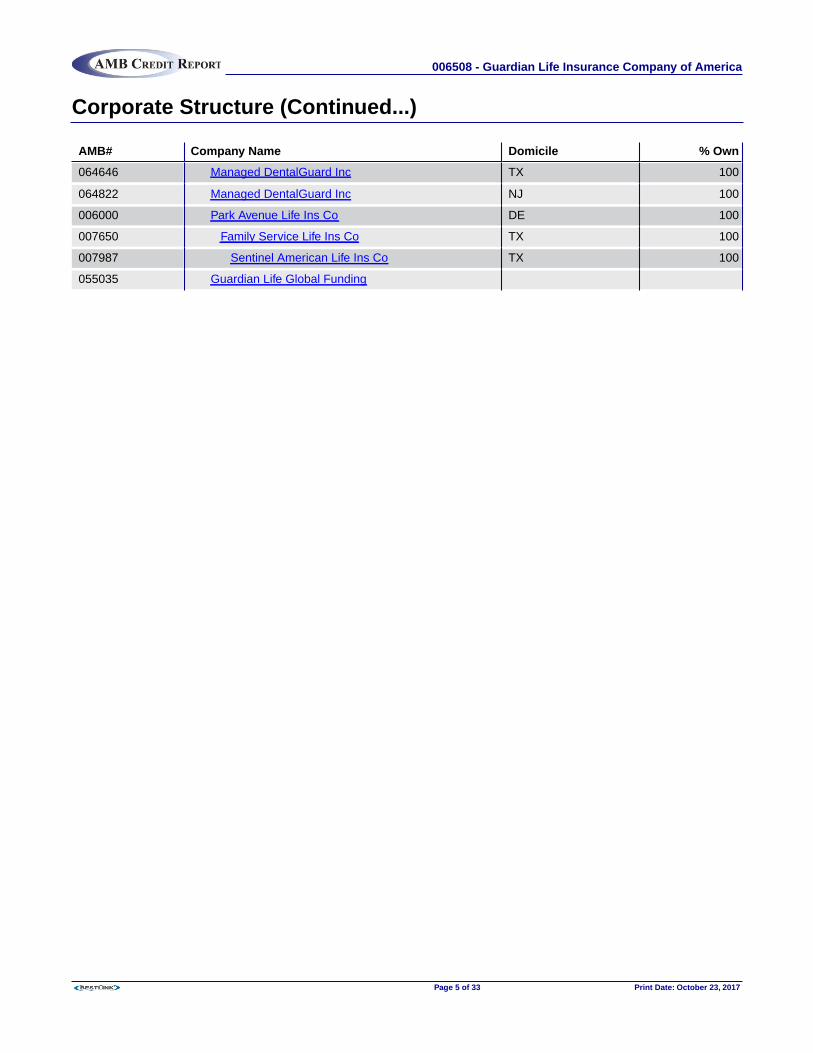

Corporate Structure (Continued...)

AMB# Company Name Domicile % Own

064646 Managed DentalGuard Inc TX 100

064822 Managed DentalGuard Inc NJ 100

006000 Park Avenue Life Ins Co DE 100

007650 Family Service Life Ins Co TX 100

007987 Sentinel American Life Ins Co TX 100

055035 Guardian Life Global Funding

006508 - Guardian Life Insurance Company of America

Page 5 of 33 Print Date: October 23, 2017

Business ProfileThe following text is derived from A.M. Best's Credit Report on Guardian Life & Health Group (AMB# 020389).

Guardian Life Group, (Guardian) through its subsidiaries, provides a full range of products and financial services to customersthroughout the United States. Its wide array of product offerings enables its client base to diversify its portfolio throughinsurance, investment, securities brokerage and other pertinent financial products and services. More specifically, productsand services include individual insurance (individual participating whole life, individual disability, multi-life), group life and healthinsurance, retirement solutions (annuities, 401(k), mutual funds), and other related products and services specifically targetingpension, retirement related investments and administration, asset management and securities brokerage. Guardian targets thesmall business owner, upper-income life insurance and disability income market and the employee benefits market. Thecompany's strategy for growth is focused on distribution, including the ongoing expansion and improvement of its careeragency system supplemented by growth in the independent agent and broker channels, and further development and supportof its worksite channel. Its distribution management team focuses on agent recruitment through turnkey solutions for start-upagencies and sales manager development through a portfolio of training programs and technology driven tools. Guardian'semployee benefits portfolio is distributed by the company's group representatives, who work both directly with clients andthrough brokers. Prior to 2012, its agency distribution was segregated from its core profit centers. In 2012, managementimplemented an organizational alignment and distribution was integrated into its respective profit centers. This alignmentprovides for fluent collaboration between the design and delivery of products and service to support its distribution whiledriving higher productivity, which is evident in the company's sales results.

Guardian recently made two key acquisitions: In January 2016, the company acquired Avesis Incorporated, a leadingadministrator of vision, dental, and hearing programs in both the commercial and government markets, serving three millionMedicaid, CHIP, and Medicare Advantage members. Avesis has partnerships with managed care organizations holdinggovernment contracts in 21 states and has relationships with 1.5 million commercial vision members. The acquisition of Avesiswill enable Guardian to accelerate the growth of government programs within its Group business. Avesis will augmentGuardian's capabilities, with an experienced management team and over 440 employees with primary locations in Baltimoreand Phoenix, a scalable operating and technology platform, existing relationships with leading managed care organizations,and a broad product portfolio. In December 2015, Guardian's subsidiary, Reed Group, acquired Aon Hewitt's AbsenceManagement Business. Aon Hewitt is a widely recognized provider of absence management and related services to over 200clients nationwide, with 1,400 employees in 10 locations across the U.S., Canada, and India. Absence management is a highlyrelevant offering to large market employers, including when packaged with group disability products. Reed Group is purchasingthis business to expand capabilities and realize scale through additional talent, resources, and technology.

Guardian's financial results are reported through its two primary businesses -- Individual Markets, which provides products andservices to individuals primarily through their general agency distribution channel, and Group and Worksite Markets whichprovides products and services through employers and other groups. Individual business includes life and disability (excludingCOLI and BOLI), Retirement Solutions (annuities and 401(k)) and RS Investments (a San Francisco-based investmentmanagement firm). RS is a mutual fund company specializing in growth and value mutual funds and institutional accounts, andoperates as an independent subsidiary of Guardian Investor Services, LLC. Park Avenue Securities (PAS), a broker-dealeraffiliate of Guardian Insurance and Annuity Company (GIAC), offers the RS funds, proprietary and non-proprietary variableannuity and variable life products, equity securities, investment advisory programs, and non-proprietary mutual funds. On7/1/16 Guardian announced its intent to sell the 401(k) business to Ameritas. This is part of Guardian's ongoing plan to focusefforts on businesses where they have core competencies and scale while evolving to a more customer- and market-segment-focused organization. The transaction is pending regulatory approval.

Both the insurance and investment products are marketed through the company's career agency force consisting of over 3,000field representatives. Guardian's career sales force has grown through actively recruiting general agents, regional directorsand sales managers, as well as through excellent agent retention. These efforts have helped contribute to the group's wholelife sales growth. The company continues to revamp its career training program with a focus on recruiting and successionplanning for key agencies to assure continued growth while maintaining talent within its distribution. This stability in the salesforce provides a competitive advantage in the upper-income market. The sales organization's strength and stability, as well asits focus on the upper-income market, are evidenced by the fact that Guardian's average case size, premium persistency,average face amount and average premium per policy are significantly higher than its peer group.

Within the individual risk segment, Guardian focuses its marketing efforts on the upper-income small business owner andprofessional life insurance and disability income market. Its broad product portfolio includes traditional participating whole life,universal life, level premium term, and pension trust products. To counteract the low interest rate environment within itsindividual risk segment, the company has de-risked its interest sensitive business lines (UL and Executive Benefits - BOLI),has exited its Executive Benefits - COLI and long-term care business lines and is limiting sales of variable annuity business tointernal distribution within the Retirement Solutions segment.

006508 - Guardian Life Insurance Company of America

Page 6 of 33 Print Date: October 23, 2017

Business Profile (Continued...)Traditional whole life insurance, Guardian's core product, represents the majority of ordinary life premium production for thegroup with individual term and universal life providing diversification benefits to its Individual Life profit center. Guardian's agentrecruiting and training initiatives, new and enhanced products, improved customer and producer support, and complementarydistribution outlets should also provide opportunities in the group's core market. A key initiative for the agency force is TheLiving Balance Sheet which provides a personal financial web site for each client with daily aggregation of financial informationfrom over 10,000 financial institutions. This real-time system provides a full financial overview for both the agent and the client.While A.M. Best views the success of the company's strategic initiatives positively, it believes the industry is highly competitive,and Guardian may be challenged to continue its growth trends in the individual marketplace. Guardian's response to achallenging environment includes profit center growth initiatives, product innovation, cost reductions, increased governmentrelations initiatives and new initiatives in Group Dental, Life and Disability businesses to mitigate the impact of health carereform. During 2013, Guardian introduced an accelerated death benefit rider for long term care (LTC) to its whole life productwhich allows the policyholder to accelerate a portion of the policy's death benefit if he or she becomes chronically ill and needsLTC services.

Another subsidiary of the group, Berkshire Life Insurance Company of America (Berkshire), offers individual disabilityinsurance (DI). The combined life insurance line is managed by Guardian, and the combined DI business is managed byBerkshire. The combined organization is now a leading writer of non-cancelable individual disability insurance in the country.DI products are sold primarily through the group's core field representative force, independent agents and outside brokers.Recent growth initiatives include expanding distribution capabilities through the use of wholesalers to attract brokers andexecutive benefit plan specialists. With the consolidation of this line through Berkshire, efforts to improve operatingfundamentals such as pricing, underwriting, and claims management have resulted in improved loss ratios, which havebecome more stable, and earnings continue to improve. The disability line strengthens Guardian's product offerings, and thecompany has placed DI specialists in agency offices to enhance sales efforts. Expanding upon its DI expertise and to provideadditional products to its representatives, Berkshire introduced a multi-life DI product for employees of small and medium-sizedbusinesses.

Guardian's group insurance segment focuses on the employee benefits market (generally employers less than 5,000employees). The company's balanced product portfolio includes dental (PPO and DHMO), vision, disability, life, critical illness,cancer, accident and stop loss coverage sold through the broker market, managed by over 250 group sales representatives in52 locations nationwide. In light of health care reform, Guardian has recently announced that it has developed a suite of dentalbenefit products which will be offered on 48 small business health (SHOP) exchanges which are being formed for companieswith 50 or less employees. Guardian participates in state and private exchanges with exchange certified dental programs, butthe longer term impact of health care reform remains uncertain at this time. The company previously marketed group medicalinsurance. The company began its exit from this market in 2000. In 2012, the company completed its exit from group medicalinsurance with a portion going to an unaffiliated insurer. The group medical line represented a declining percentage ofcompany-wide premiums and the company will be focusing primarily on its group non-medical business. Future growthinitiatives for the group segment include targeted customer growth, channel and worksite expansion and improving operationaland technology efficiencies to support its growth strategy.

While the dental line provides product and earnings diversification for Guardian, external factors, broker consolidations andcompetitive pricing and bundling are impacting the industry and resulting in premium declines for First Commonwealth. In late2012, Guardian's First Commonwealth subsidiary acquired 100% interest in Reed Group, Ltd. (Reed). Reed is a leadingprovider of absence management services and software to employers. In April 2014, Guardian acquired Premier AccessInsurance Company and its affiliates (Premier Access). Premier Access, based in Sacramento, California, is a provider ofdental coverage and care to employers and individuals with more than 634,000 members. The acquisition is expected tostrengthen Guardian's existing Dental Health Maintenance Organization (DHMO) network in several states including California,Utah, Nevada and Arizona. It also extends Guardian's reach into the state-run Medicaid and Children's Health InsuranceProgram (CHIP) markets which are expected to grow significantly due to expanded eligibility under the Affordable Care Act(ACA). Guardian also gained a presence on six individual state exchanges, complementing its existing offering on 48 of thesmall business health (SHOP) exchanges.

Guardian's key to transitioning from a medical focus to a multiple non-medical product marketing approach has been trainingand enhanced administrative support provided to the organization's group sales representatives. New product introductions,technological investments, and upgraded training and support of the company's group sales representatives should continue toprovide a platform for growth. The group sales representatives now offer employers complete benefits packages includingdental, vision, life and disability. The company's worksite marketing endeavors to work closely with independent brokers to sellvoluntary group term life, dental, and disability to employees of existing group clients. Worksite marketing now representsapproximately a third of total non-medical product sales. A.M. Best views favorably management's focus on a multi-productstrategy utilizing a combination of managed care arrangements, HSAs, its proprietary PPO and DHMO dental offering, and itsportfolio of non-medical products. In 2013, Guardian introduced a medical stop-loss product for companies who self-fund theiremployee medical coverage.

006508 - Guardian Life Insurance Company of America

Page 7 of 33 Print Date: October 23, 2017

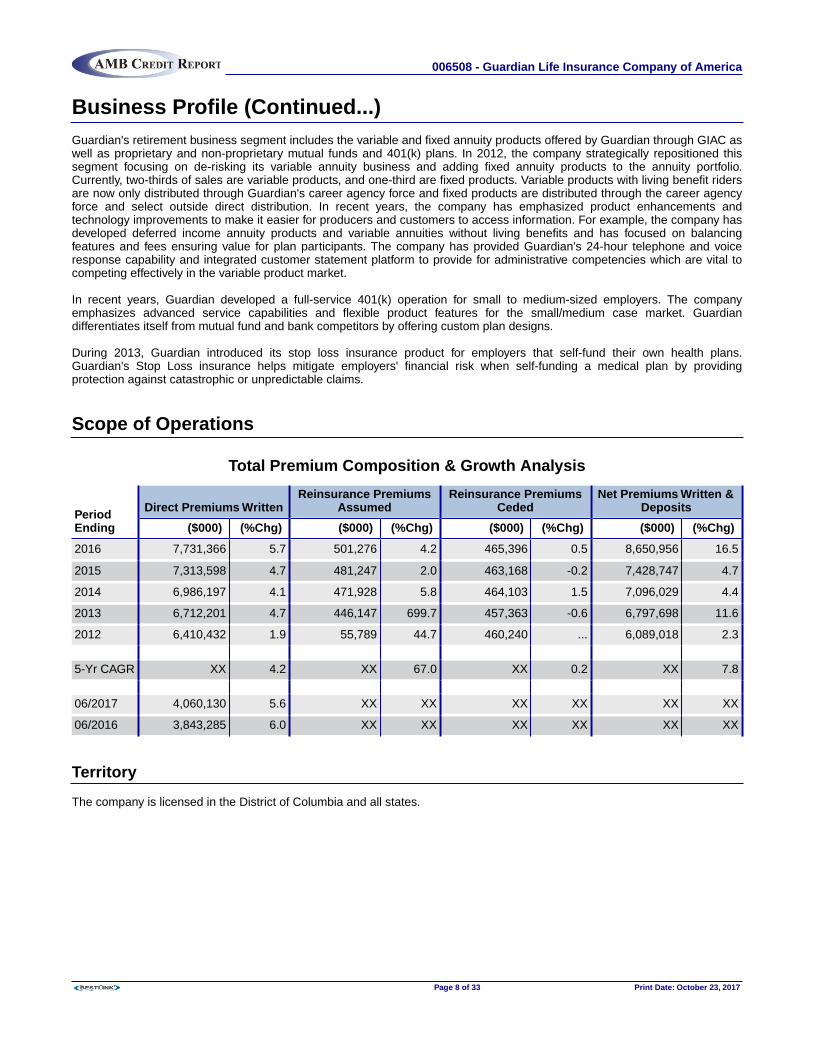

Business Profile (Continued...)Guardian's retirement business segment includes the variable and fixed annuity products offered by Guardian through GIAC aswell as proprietary and non-proprietary mutual funds and 401(k) plans. In 2012, the company strategically repositioned thissegment focusing on de-risking its variable annuity business and adding fixed annuity products to the annuity portfolio.Currently, two-thirds of sales are variable products, and one-third are fixed products. Variable products with living benefit ridersare now only distributed through Guardian's career agency force and fixed products are distributed through the career agencyforce and select outside direct distribution. In recent years, the company has emphasized product enhancements andtechnology improvements to make it easier for producers and customers to access information. For example, the company hasdeveloped deferred income annuity products and variable annuities without living benefits and has focused on balancingfeatures and fees ensuring value for plan participants. The company has provided Guardian's 24-hour telephone and voiceresponse capability and integrated customer statement platform to provide for administrative competencies which are vital tocompeting effectively in the variable product market.

In recent years, Guardian developed a full-service 401(k) operation for small to medium-sized employers. The companyemphasizes advanced service capabilities and flexible product features for the small/medium case market. Guardiandifferentiates itself from mutual fund and bank competitors by offering custom plan designs.

During 2013, Guardian introduced its stop loss insurance product for employers that self-fund their own health plans.Guardian's Stop Loss insurance helps mitigate employers' financial risk when self-funding a medical plan by providingprotection against catastrophic or unpredictable claims.

Scope of Operations

Total Premium Composition & Growth Analysis

PeriodEnding

Direct Premiums WrittenReinsurance Premiums

AssumedReinsurance Premiums

CededNet Premiums Written &

Deposits

($000) (%Chg) ($000) (%Chg) ($000) (%Chg) ($000) (%Chg)

2016 7,731,366 5.7 501,276 4.2 465,396 0.5 8,650,956 16.5

2015 7,313,598 4.7 481,247 2.0 463,168 -0.2 7,428,747 4.7

2014 6,986,197 4.1 471,928 5.8 464,103 1.5 7,096,029 4.4

2013 6,712,201 4.7 446,147 699.7 457,363 -0.6 6,797,698 11.6

2012 6,410,432 1.9 55,789 44.7 460,240 ... 6,089,018 2.3

5-Yr CAGR XX 4.2 XX 67.0 XX 0.2 XX 7.8

06/2017 4,060,130 5.6 XX XX XX XX XX XX

06/2016 3,843,285 6.0 XX XX XX XX XX XX

Territory

The company is licensed in the District of Columbia and all states.

006508 - Guardian Life Insurance Company of America

Page 8 of 33 Print Date: October 23, 2017

Business Trends

2016 By-Line Business ($000)

Product Line

Direct PremiumsWritten

ReinsurancePremiums Assumed

ReinsurancePremiums Ceded Net Premiums Written

($000) (%) ($000) (%) ($000) (%) ($000) (%)

Ordinary life 4,053,621 52.4 35,913 7.2 265,616 57.1 3,829,389 49.3

Group life 542,215 7.0 1,170 0.2 269 0.1 543,116 7.0

Individual annuities 16,396 0.2 ... ... ... ... 16,396 0.2

Individual A&H 196,516 2.5 464,172 92.6 189,305 40.7 471,383 6.1

Group A&H 2,922,619 37.8 21 ... 10,206 2.2 2,912,433 37.5

Total 7,731,366 100.0 501,276 100.0 465,396 100.0 7,772,716 100.0

2016 Top Product Lines of Business (Net Premiums Written)

49.3%

7.0%0.2%

6.1%

37.5%

Ordinary life Individual annuities Group A&H

Group life Individual A&H

5 Years of Net Premiums Written ($000)

0

1,500,000

3,000,000

4,500,000

6,000,000

7,500,000

2012

2013

2014

2015

2016

6,011,215

6,705,5877,000,000

7,337,7097,772,716

By-Line Reserves ($000)

Product Line 2016 2015 2014 2013 2012

Ordinary life 34,874,038 32,718,188 30,799,892 28,860,779 26,948,126

Group life 547,734 568,600 560,277 542,998 531,147

Supplementary contracts 20,417 23,467 26,587 30,307 32,551

Individual annuities 217,691 225,876 222,231 229,236 235,996

Group annuities 19,072 21,060 25,043 26,925 25,251

Deposit type contracts 1,209,718 406,752 401,466 389,554 384,723

Individual A&H 2,543,832 2,419,260 2,248,850 2,113,837 32,960

Group A&H 1,169,402 1,079,568 1,000,514 909,911 850,514

Total 40,601,905 37,462,770 35,284,860 33,103,545 29,041,267

006508 - Guardian Life Insurance Company of America

Page 9 of 33 Print Date: October 23, 2017

Business Trends (Continued...)

Life Policies Statistics

Year

Ordinary Policies Group Policies Group Certificates

Issued In Force Issued In Force Issued In Force

2016 42,438 976,237 7,185 46,916 453,793 2,914,676

2015 43,371 973,086 6,780 45,146 413,814 2,753,294

2014 45,224 1,122,532 6,861 43,648 421,040 2,603,980

2013 48,192 1,136,973 7,742 42,145 464,126 2,450,473

2012 47,268 1,155,954 6,883 39,579 517,247 2,231,056

Life Insurance In Force ($000)

Year

Whole Life &Endowment &

Additions Term Credit Group IndustrialTotal Insurance

In Force

2016 201,764,706 152,874,094 ... 236,177,629 ... 590,816,429

2015 196,006,313 140,090,486 ... 219,374,574 ... 555,471,373

2014 191,175,664 128,259,861 ... 199,623,255 ... 519,058,780

2013 185,345,325 116,927,888 ... 180,787,142 ... 483,060,355

2012 177,486,182 106,042,619 ... 160,460,257 ... 443,989,058

New Life Business Issued

Year

Whole Life &Endowment& Additions Term Credit Group Industrial

TotalInsurance

Issued

Non-Particpt.

(%)Particpt.

(%)

2016 11,881,314 21,719,321 ... 40,005,277 ... 73,605,912 ... 100.0

2015 11,679,401 20,530,270 ... 34,084,595 ... 66,294,266 ... 100.0

2014 12,055,217 20,005,557 ... 34,727,487 ... 66,788,261 ... 100.0

2013 13,744,701 19,753,847 ... 34,909,511 ... 68,408,059 ... 100.0

2012 13,236,192 17,594,553 ... 34,400,221 ... 65,230,967 ... 100.0

006508 - Guardian Life Insurance Company of America

Page 10 of 33 Print Date: October 23, 2017

Business Trends (Continued...)

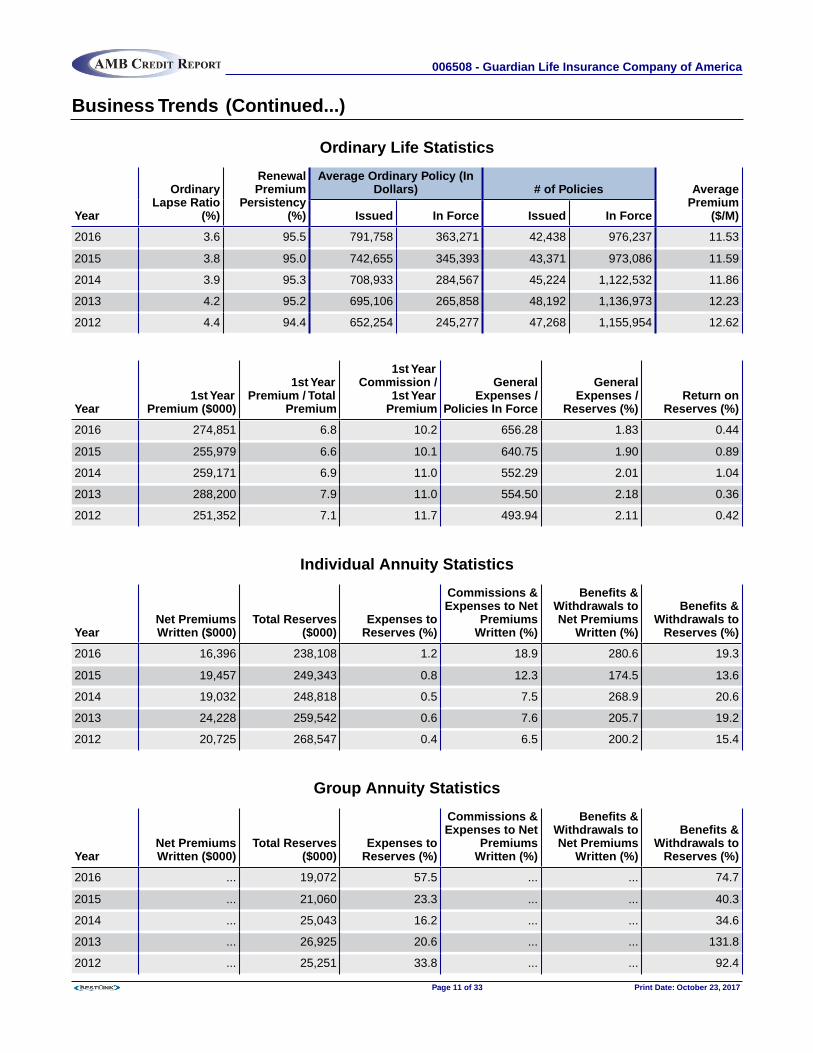

Ordinary Life Statistics

Year

OrdinaryLapse Ratio

(%)

RenewalPremium

Persistency(%)

Average Ordinary Policy (InDollars) # of Policies Average

Premium($/M)Issued In Force Issued In Force

2016 3.6 95.5 791,758 363,271 42,438 976,237 11.53

2015 3.8 95.0 742,655 345,393 43,371 973,086 11.59

2014 3.9 95.3 708,933 284,567 45,224 1,122,532 11.86

2013 4.2 95.2 695,106 265,858 48,192 1,136,973 12.23

2012 4.4 94.4 652,254 245,277 47,268 1,155,954 12.62

Year1st Year

Premium ($000)

1st YearPremium / Total

Premium

1st YearCommission /

1st YearPremium

GeneralExpenses /

Policies In Force

GeneralExpenses /

Reserves (%)Return on

Reserves (%)

2016 274,851 6.8 10.2 656.28 1.83 0.44

2015 255,979 6.6 10.1 640.75 1.90 0.89

2014 259,171 6.9 11.0 552.29 2.01 1.04

2013 288,200 7.9 11.0 554.50 2.18 0.36

2012 251,352 7.1 11.7 493.94 2.11 0.42

Individual Annuity Statistics

YearNet PremiumsWritten ($000)

Total Reserves($000)

Expenses toReserves (%)

Commissions &Expenses to Net

PremiumsWritten (%)

Benefits &Withdrawals toNet Premiums

Written (%)

Benefits &Withdrawals to

Reserves (%)

2016 16,396 238,108 1.2 18.9 280.6 19.3

2015 19,457 249,343 0.8 12.3 174.5 13.6

2014 19,032 248,818 0.5 7.5 268.9 20.6

2013 24,228 259,542 0.6 7.6 205.7 19.2

2012 20,725 268,547 0.4 6.5 200.2 15.4

Group Annuity Statistics

YearNet PremiumsWritten ($000)

Total Reserves($000)

Expenses toReserves (%)

Commissions &Expenses to Net

PremiumsWritten (%)

Benefits &Withdrawals toNet Premiums

Written (%)

Benefits &Withdrawals to

Reserves (%)

2016 ... 19,072 57.5 ... ... 74.7

2015 ... 21,060 23.3 ... ... 40.3

2014 ... 25,043 16.2 ... ... 34.6

2013 ... 26,925 20.6 ... ... 131.8

2012 ... 25,251 33.8 ... ... 92.4

006508 - Guardian Life Insurance Company of America

Page 11 of 33 Print Date: October 23, 2017

Business Trends (Continued...)

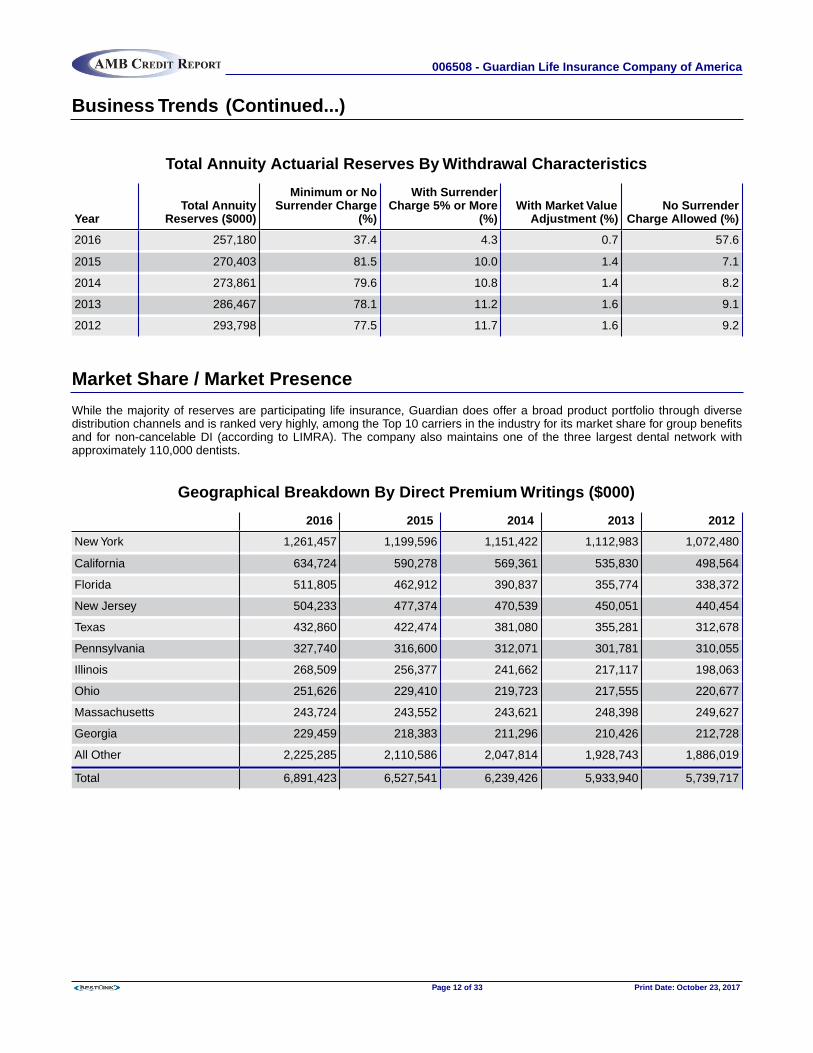

Total Annuity Actuarial Reserves By Withdrawal Characteristics

YearTotal Annuity

Reserves ($000)

Minimum or NoSurrender Charge

(%)

With SurrenderCharge 5% or More

(%)With Market Value

Adjustment (%)No Surrender

Charge Allowed (%)

2016 257,180 37.4 4.3 0.7 57.6

2015 270,403 81.5 10.0 1.4 7.1

2014 273,861 79.6 10.8 1.4 8.2

2013 286,467 78.1 11.2 1.6 9.1

2012 293,798 77.5 11.7 1.6 9.2

Market Share / Market Presence

While the majority of reserves are participating life insurance, Guardian does offer a broad product portfolio through diversedistribution channels and is ranked very highly, among the Top 10 carriers in the industry for its market share for group benefitsand for non-cancelable DI (according to LIMRA). The company also maintains one of the three largest dental network withapproximately 110,000 dentists.

Geographical Breakdown By Direct Premium Writings ($000)

2016 2015 2014 2013 2012

New York 1,261,457 1,199,596 1,151,422 1,112,983 1,072,480

California 634,724 590,278 569,361 535,830 498,564

Florida 511,805 462,912 390,837 355,774 338,372

New Jersey 504,233 477,374 470,539 450,051 440,454

Texas 432,860 422,474 381,080 355,281 312,678

Pennsylvania 327,740 316,600 312,071 301,781 310,055

Illinois 268,509 256,377 241,662 217,117 198,063

Ohio 251,626 229,410 219,723 217,555 220,677

Massachusetts 243,724 243,552 243,621 248,398 249,627

Georgia 229,459 218,383 211,296 210,426 212,728

All Other 2,225,285 2,110,586 2,047,814 1,928,743 1,886,019

Total 6,891,423 6,527,541 6,239,426 5,933,940 5,739,717

006508 - Guardian Life Insurance Company of America

Page 12 of 33 Print Date: October 23, 2017

Risk ManagementThe following text is derived from A.M. Best's Credit Report on Guardian Life & Health Group (AMB# 020389).

Guardian has a formal and disciplined structure to monitor and manage risk. Enterprise Risk Management (ERM) objectivesare to manage and aggregate risk on an enterprise-wide level, ensure robust risk management processes, and instill a riskmanagement culture throughout the organization. By accomplishing these objectives, Guardian's ERM efforts allow the entityto maintain excellent financial strength, favorable capitalization and provide its customers with products that optimize thebalance between financial risk and return for both policyholders and the enterprise.

Guardian operationalizes its enterprise risk management through various Committees all of which report to the Corporate RiskManagement Committee (CRMC). Committee's reporting to the CRMC includes Investment Risk, Compliance, Operational,Product and Business Unit/Distribution. The CRMC consists of CEO, CFO, COO and other senior executives and is chaired bythe Chief Risk Officer. The Chief Actuary functions as the Chief Risk Officer of the Company. Each Committee has a charterdefining its mission and how it operates.

The Board of Directors has ultimate responsibility to monitor enterprise risks and management's plans to manage those risks,and the Board and each of its principal Committees have written charters containing explicit statements of their responsibilitiesfor monitoring enterprise risks and the Company's plans to manage those risks. Specifically, the Audit and Risk Committee isresponsible for monitoring all risks and their related management plans not explicitly covered by other Board committees. TheInvestment Committee monitors all investment risks and the Product and Distribution Committee monitors product pricingrisks, reviews the annual policyholder dividend pay-out and all reinsurance policies.

The Company has defined and quantified its ERM practices through a Guardian Corporate Risk Appetite statement which isupdated on an annual basis. This statement is enterprise wide, developed in conjunction with the planning process, and isreviewed and approved at both the Corporate Risk Committee as well as the Board of Directors. It reflects all material risksincluding interest rate, equity market, credit, business and operational. Once the enterprise wide "risk budget" is determined itis then allocated to each profit center which in turn develops its own cascading risk appetite statement to ensure consistencyand compliance with the overall enterprise risk budget. The risk appetite statement includes quantitative risk tolerances whichmandate minimum RBC ratios, earnings requirements, and place constraints on earnings volatility and capital volatility. Inaddition, a number of qualitative tolerances are formulated to address operational, business, regulatory and reputational risks.The Company uses various tools to understand and evaluate risks including stress testing and economic capital modeling.Economic capital modeling is performed for all business segments utilizing a set of integrated scenarios which identify allmaterial business risks using a conditional tail expectation ratio of 99% (i.e. required capital is computed based on theoutcomes of the worst 1% scenarios). Finally, in addition to economic capital, the company has completed a review of its OwnRisk and Solvency Assessment (ORSA) which will be required by the NAIC in the future.

006508 - Guardian Life Insurance Company of America

Page 13 of 33 Print Date: October 23, 2017

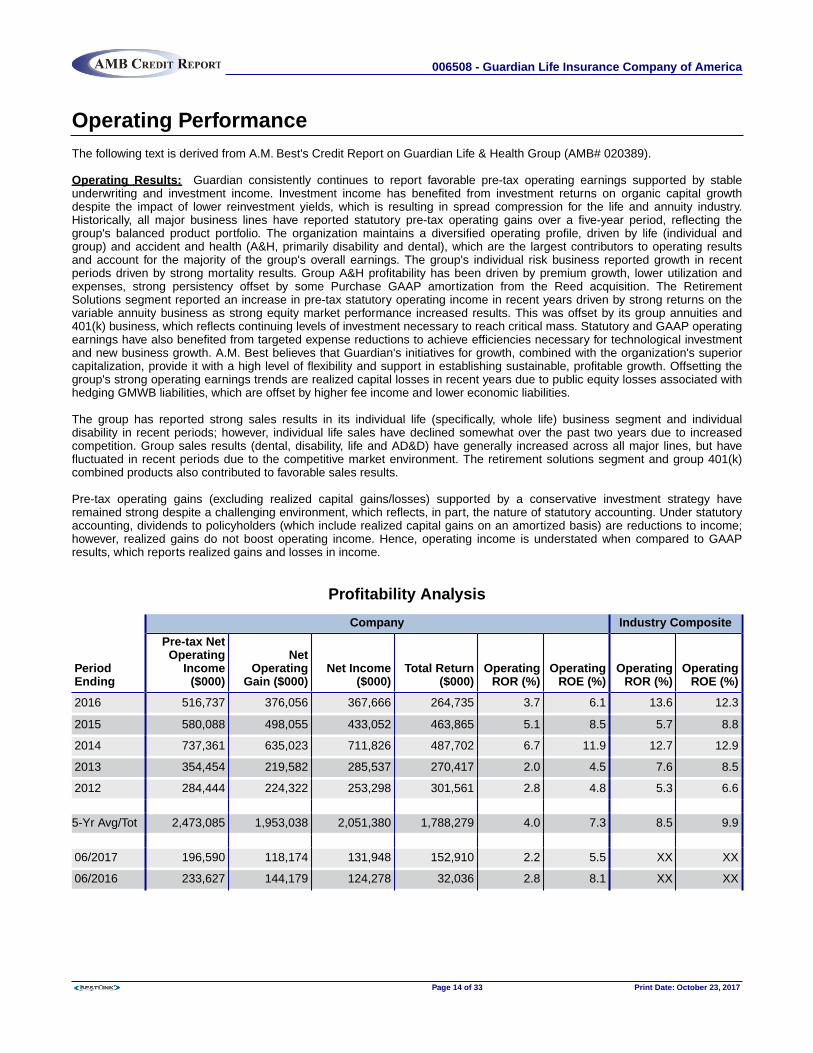

Operating PerformanceThe following text is derived from A.M. Best's Credit Report on Guardian Life & Health Group (AMB# 020389).

Operating Results: Guardian consistently continues to report favorable pre-tax operating earnings supported by stableunderwriting and investment income. Investment income has benefited from investment returns on organic capital growthdespite the impact of lower reinvestment yields, which is resulting in spread compression for the life and annuity industry.Historically, all major business lines have reported statutory pre-tax operating gains over a five-year period, reflecting thegroup's balanced product portfolio. The organization maintains a diversified operating profile, driven by life (individual andgroup) and accident and health (A&H, primarily disability and dental), which are the largest contributors to operating resultsand account for the majority of the group's overall earnings. The group's individual risk business reported growth in recentperiods driven by strong mortality results. Group A&H profitability has been driven by premium growth, lower utilization andexpenses, strong persistency offset by some Purchase GAAP amortization from the Reed acquisition. The RetirementSolutions segment reported an increase in pre-tax statutory operating income in recent years driven by strong returns on thevariable annuity business as strong equity market performance increased results. This was offset by its group annuities and401(k) business, which reflects continuing levels of investment necessary to reach critical mass. Statutory and GAAP operatingearnings have also benefited from targeted expense reductions to achieve efficiencies necessary for technological investmentand new business growth. A.M. Best believes that Guardian's initiatives for growth, combined with the organization's superiorcapitalization, provide it with a high level of flexibility and support in establishing sustainable, profitable growth. Offsetting thegroup's strong operating earnings trends are realized capital losses in recent years due to public equity losses associated withhedging GMWB liabilities, which are offset by higher fee income and lower economic liabilities.

The group has reported strong sales results in its individual life (specifically, whole life) business segment and individualdisability in recent periods; however, individual life sales have declined somewhat over the past two years due to increasedcompetition. Group sales results (dental, disability, life and AD&D) have generally increased across all major lines, but havefluctuated in recent periods due to the competitive market environment. The retirement solutions segment and group 401(k)combined products also contributed to favorable sales results.

Pre-tax operating gains (excluding realized capital gains/losses) supported by a conservative investment strategy haveremained strong despite a challenging environment, which reflects, in part, the nature of statutory accounting. Under statutoryaccounting, dividends to policyholders (which include realized capital gains on an amortized basis) are reductions to income;however, realized gains do not boost operating income. Hence, operating income is understated when compared to GAAPresults, which reports realized gains and losses in income.

Profitability Analysis

PeriodEnding

Company Industry Composite

Pre-tax NetOperating

Income($000)

NetOperating

Gain ($000)Net Income

($000)Total Return

($000)Operating

ROR (%)Operating

ROE (%)Operating

ROR (%)Operating

ROE (%)

2016 516,737 376,056 367,666 264,735 3.7 6.1 13.6 12.3

2015 580,088 498,055 433,052 463,865 5.1 8.5 5.7 8.8

2014 737,361 635,023 711,826 487,702 6.7 11.9 12.7 12.9

2013 354,454 219,582 285,537 270,417 2.0 4.5 7.6 8.5

2012 284,444 224,322 253,298 301,561 2.8 4.8 5.3 6.6

5-Yr Avg/Tot 2,473,085 1,953,038 2,051,380 1,788,279 4.0 7.3 8.5 9.9

06/2017 196,590 118,174 131,948 152,910 2.2 5.5 XX XX

06/2016 233,627 144,179 124,278 32,036 2.8 8.1 XX XX

006508 - Guardian Life Insurance Company of America

Page 14 of 33 Print Date: October 23, 2017

Operating Performance (Continued...)

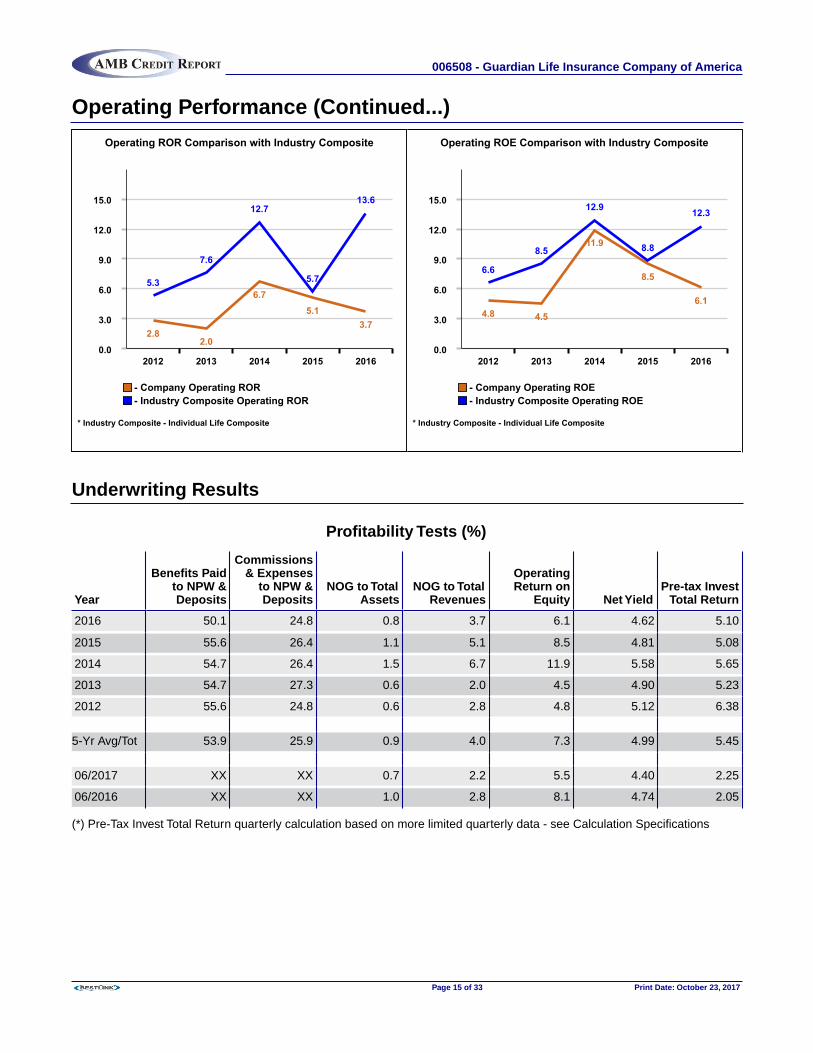

Operating ROR Comparison with Industry Composite

0.0

3.0

6.0

9.0

12.0

15.0

2012 2013 2014 2015 2016

2.82.0

6.75.1

3.7

5.3

7.6

12.7

5.7

13.6

- Company Operating ROR - Industry Composite Operating ROR

* Industry Composite - Individual Life Composite

Operating ROE Comparison with Industry Composite

0.0

3.0

6.0

9.0

12.0

15.0

2012 2013 2014 2015 2016

4.8 4.5

11.9

8.5

6.1

6.6

8.5

12.9

8.8

12.3

- Company Operating ROE - Industry Composite Operating ROE

* Industry Composite - Individual Life Composite

Underwriting Results

Profitability Tests (%)

Year

Benefits Paidto NPW &Deposits

Commissions& Expenses

to NPW &Deposits

NOG to TotalAssets

NOG to TotalRevenues

OperatingReturn on

Equity Net YieldPre-tax Invest

Total Return

2016 50.1 24.8 0.8 3.7 6.1 4.62 5.10

2015 55.6 26.4 1.1 5.1 8.5 4.81 5.08

2014 54.7 26.4 1.5 6.7 11.9 5.58 5.65

2013 54.7 27.3 0.6 2.0 4.5 4.90 5.23

2012 55.6 24.8 0.6 2.8 4.8 5.12 6.38

5-Yr Avg/Tot 53.9 25.9 0.9 4.0 7.3 4.99 5.45

06/2017 XX XX 0.7 2.2 5.5 4.40 2.25

06/2016 XX XX 1.0 2.8 8.1 4.74 2.05

(*) Pre-Tax Invest Total Return quarterly calculation based on more limited quarterly data - see Calculation Specifications

006508 - Guardian Life Insurance Company of America

Page 15 of 33 Print Date: October 23, 2017

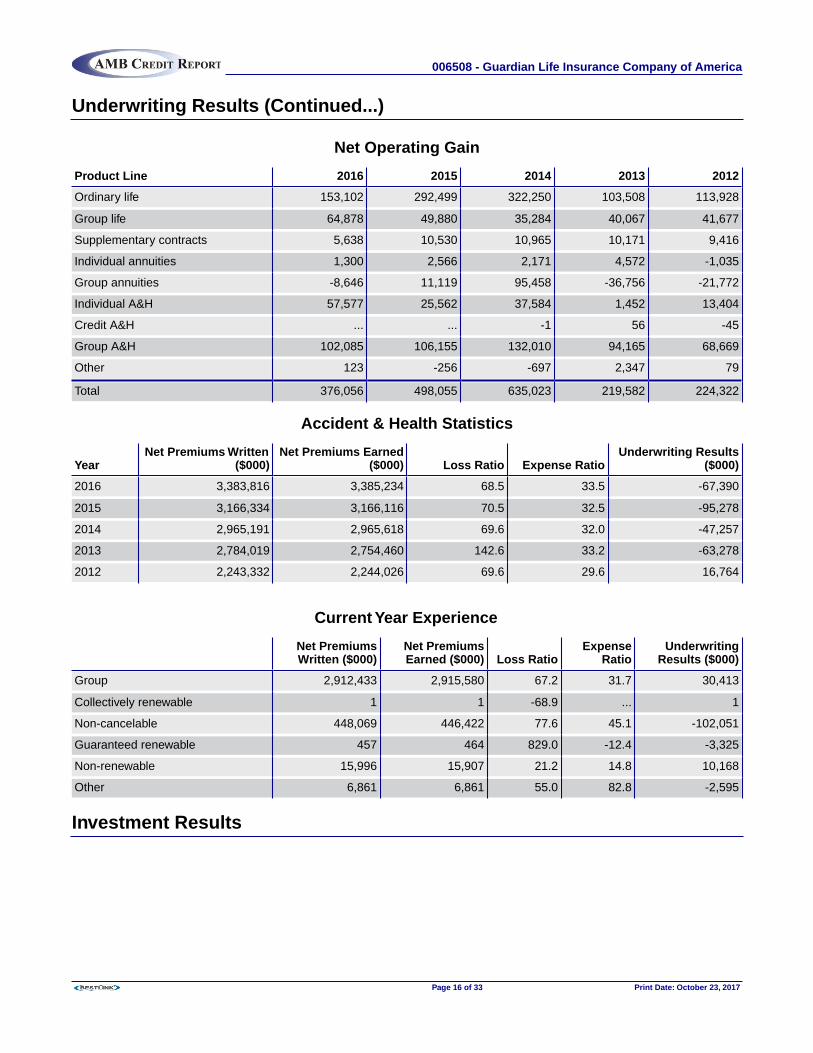

Underwriting Results (Continued...)

Net Operating Gain

Product Line 2016 2015 2014 2013 2012

Ordinary life 153,102 292,499 322,250 103,508 113,928

Group life 64,878 49,880 35,284 40,067 41,677

Supplementary contracts 5,638 10,530 10,965 10,171 9,416

Individual annuities 1,300 2,566 2,171 4,572 -1,035

Group annuities -8,646 11,119 95,458 -36,756 -21,772

Individual A&H 57,577 25,562 37,584 1,452 13,404

Credit A&H ... ... -1 56 -45

Group A&H 102,085 106,155 132,010 94,165 68,669

Other 123 -256 -697 2,347 79

Total 376,056 498,055 635,023 219,582 224,322

Accident & Health Statistics

YearNet Premiums Written

($000)Net Premiums Earned

($000) Loss Ratio Expense RatioUnderwriting Results

($000)

2016 3,383,816 3,385,234 68.5 33.5 -67,390

2015 3,166,334 3,166,116 70.5 32.5 -95,278

2014 2,965,191 2,965,618 69.6 32.0 -47,257

2013 2,784,019 2,754,460 142.6 33.2 -63,278

2012 2,243,332 2,244,026 69.6 29.6 16,764

Current Year Experience

Net PremiumsWritten ($000)

Net PremiumsEarned ($000) Loss Ratio

ExpenseRatio

UnderwritingResults ($000)

Group 2,912,433 2,915,580 67.2 31.7 30,413

Collectively renewable 1 1 -68.9 ... 1

Non-cancelable 448,069 446,422 77.6 45.1 -102,051

Guaranteed renewable 457 464 829.0 -12.4 -3,325

Non-renewable 15,996 15,907 21.2 14.8 10,168

Other 6,861 6,861 55.0 82.8 -2,595

Investment Results

006508 - Guardian Life Insurance Company of America

Page 16 of 33 Print Date: October 23, 2017

Investment Results (Continued...)Investment Gains

Year

CompanyIndustry

Composite

Net Invest.Income ($000)

RealizedCapital Gains

($000)

UnrealizedCapital Gains

($000)

Invest.IncomeGrowth

(%)

Invest.Yield

(%)

Return onInvested

Assets(%)

Pre-taxInvestTotal

Return(%)

Invest.IncomeGrowth

(%)

Invest.Yield

(%)

2016 2,052,329 -8,390 -102,932 3.4 4.6 5.1 5.10 1.5 4.9

2015 1,984,669 -65,003 30,813 -7.5 4.8 4.8 5.08 -11.2 5.0

2014 2,145,842 76,803 -224,125 21.5 5.6 6.2 5.65 15.5 5.9

2013 1,765,427 65,955 -15,121 2.1 4.9 5.2 5.23 3.9 5.2

2012 1,728,420 28,976 48,264 0.8 5.1 6.0 6.38 -6.7 5.0

5-Yr Avg/Tot 9,676,687 98,341 -263,100 3.6 5.0 5.4 5.45 0.2 5.2

06/2017 1,024,192 13,773 20,963 0.1 4.4 4.5 2.25 XX XX

06/2016 1,022,677 -19,901 -92,242 6.8 4.7 4.2 2.05 XX XX

(*) Pre-Tax Invest Total Return quarterly calculation based on more limited quarterly data - see Calculation Specifications

Investment Income Growth vs Industry

-15.0

-7.5

0.0

7.5

15.0

22.5

2012 2013 2014 2015 2016

0.8

2.1

21.5

-7.5

3.4

-6.7

3.9

15.5

-11.2

1.5

- Company Investment Income Growth (%) - Industry Composite Investment Income Growth (%)

* Industry Composite - Individual Life Composite

Investment Yield vs Industry

0.0

1.3

2.6

3.9

5.2

6.5

2012 2013 2014 2015 2016

5.1

4.9

5.6

4.8 4.65.0

5.25.9

5.0 4.9

- Company Investment Yield (%) - Industry Composite Investment Yield (%)

* Industry Composite - Individual Life Composite

006508 - Guardian Life Insurance Company of America

Page 17 of 33 Print Date: October 23, 2017

Balance Sheet Strength

Capitalization

The following text is derived from A.M. Best's Credit Report on Guardian Life & Health Group (AMB# 020389).

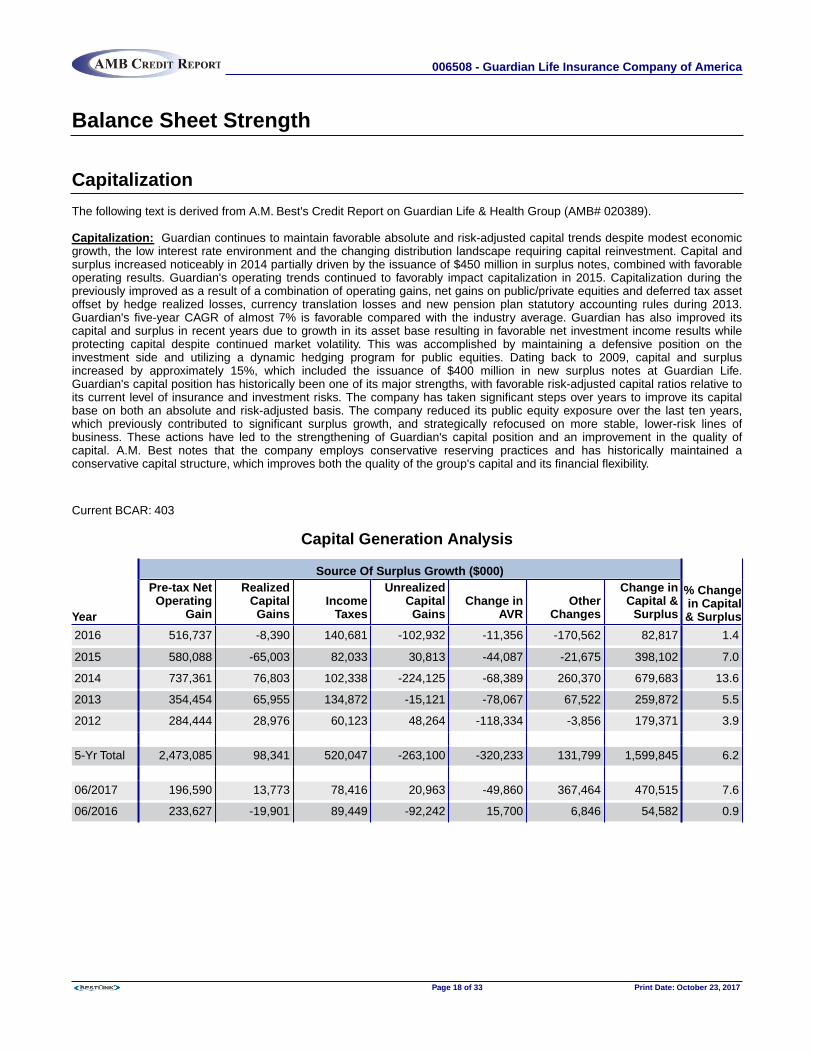

Capitalization: Guardian continues to maintain favorable absolute and risk-adjusted capital trends despite modest economicgrowth, the low interest rate environment and the changing distribution landscape requiring capital reinvestment. Capital andsurplus increased noticeably in 2014 partially driven by the issuance of $450 million in surplus notes, combined with favorableoperating results. Guardian's operating trends continued to favorably impact capitalization in 2015. Capitalization during thepreviously improved as a result of a combination of operating gains, net gains on public/private equities and deferred tax assetoffset by hedge realized losses, currency translation losses and new pension plan statutory accounting rules during 2013.Guardian's five-year CAGR of almost 7% is favorable compared with the industry average. Guardian has also improved itscapital and surplus in recent years due to growth in its asset base resulting in favorable net investment income results whileprotecting capital despite continued market volatility. This was accomplished by maintaining a defensive position on theinvestment side and utilizing a dynamic hedging program for public equities. Dating back to 2009, capital and surplusincreased by approximately 15%, which included the issuance of $400 million in new surplus notes at Guardian Life.Guardian's capital position has historically been one of its major strengths, with favorable risk-adjusted capital ratios relative toits current level of insurance and investment risks. The company has taken significant steps over years to improve its capitalbase on both an absolute and risk-adjusted basis. The company reduced its public equity exposure over the last ten years,which previously contributed to significant surplus growth, and strategically refocused on more stable, lower-risk lines ofbusiness. These actions have led to the strengthening of Guardian's capital position and an improvement in the quality ofcapital. A.M. Best notes that the company employs conservative reserving practices and has historically maintained aconservative capital structure, which improves both the quality of the group's capital and its financial flexibility.

Current BCAR: 403

Capital Generation Analysis

Year

Source Of Surplus Growth ($000)

% Changein Capital& Surplus

Pre-tax NetOperating

Gain

RealizedCapitalGains

IncomeTaxes

UnrealizedCapitalGains

Change inAVR

OtherChanges

Change inCapital &

Surplus

2016 516,737 -8,390 140,681 -102,932 -11,356 -170,562 82,817 1.4

2015 580,088 -65,003 82,033 30,813 -44,087 -21,675 398,102 7.0

2014 737,361 76,803 102,338 -224,125 -68,389 260,370 679,683 13.6

2013 354,454 65,955 134,872 -15,121 -78,067 67,522 259,872 5.5

2012 284,444 28,976 60,123 48,264 -118,334 -3,856 179,371 3.9

5-Yr Total 2,473,085 98,341 520,047 -263,100 -320,233 131,799 1,599,845 6.2

06/2017 196,590 13,773 78,416 20,963 -49,860 367,464 470,515 7.6

06/2016 233,627 -19,901 89,449 -92,242 15,700 6,846 54,582 0.9

006508 - Guardian Life Insurance Company of America

Page 18 of 33 Print Date: October 23, 2017

Capitalization (Continued...)

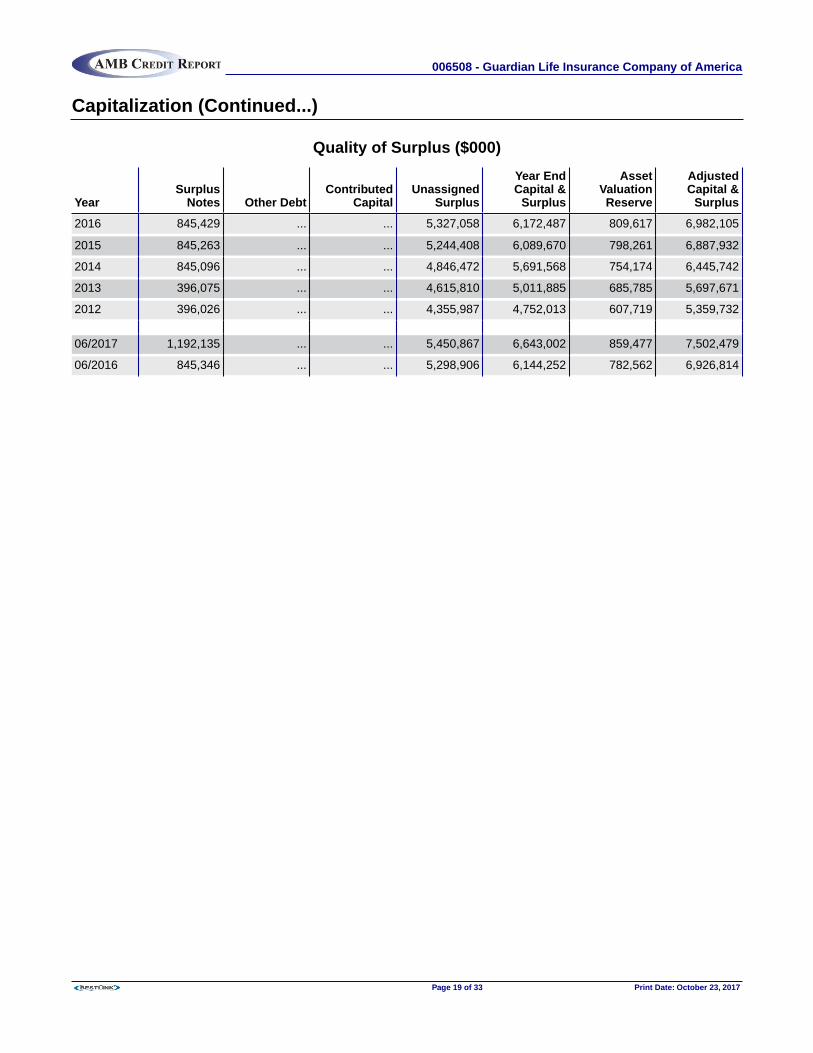

Quality of Surplus ($000)

YearSurplus

Notes Other DebtContributed

CapitalUnassigned

Surplus

Year EndCapital &

Surplus

AssetValuationReserve

AdjustedCapital &

Surplus

2016 845,429 ... ... 5,327,058 6,172,487 809,617 6,982,105

2015 845,263 ... ... 5,244,408 6,089,670 798,261 6,887,932

2014 845,096 ... ... 4,846,472 5,691,568 754,174 6,445,742

2013 396,075 ... ... 4,615,810 5,011,885 685,785 5,697,671

2012 396,026 ... ... 4,355,987 4,752,013 607,719 5,359,732

06/2017 1,192,135 ... ... 5,450,867 6,643,002 859,477 7,502,479

06/2016 845,346 ... ... 5,298,906 6,144,252 782,562 6,926,814

006508 - Guardian Life Insurance Company of America

Page 19 of 33 Print Date: October 23, 2017

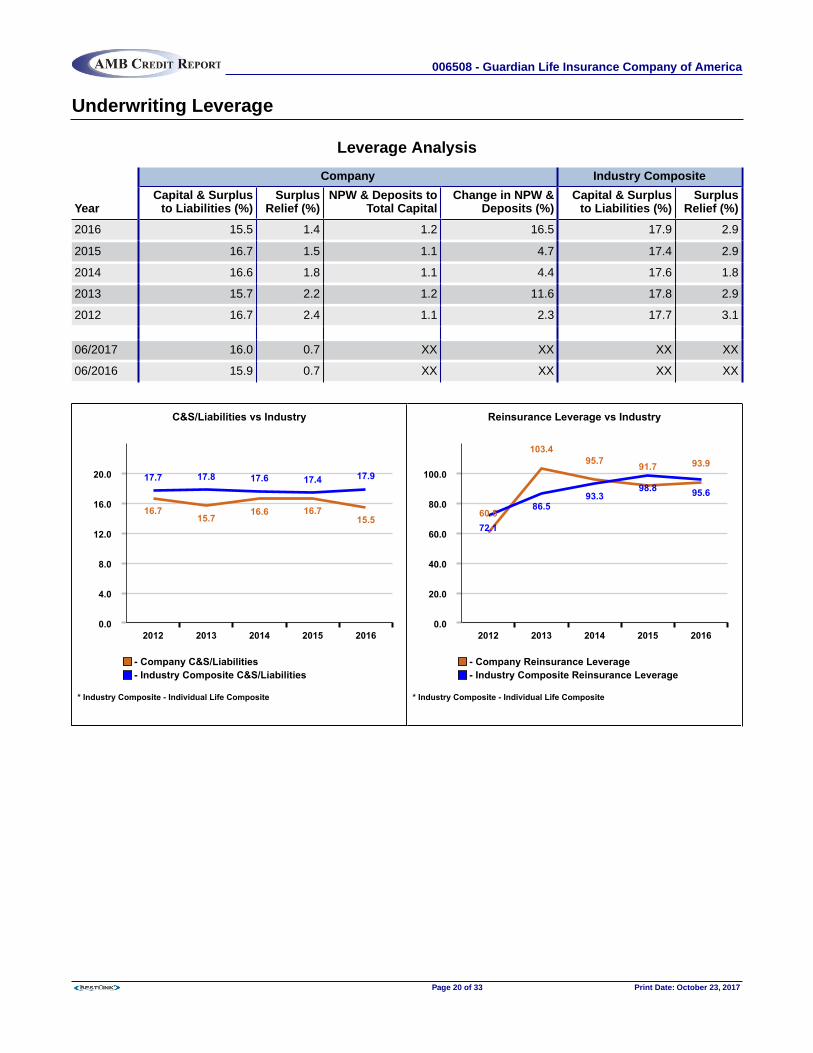

Underwriting Leverage

Leverage Analysis

Year

Company Industry Composite

Capital & Surplusto Liabilities (%)

SurplusRelief (%)

NPW & Deposits toTotal Capital

Change in NPW &Deposits (%)

Capital & Surplusto Liabilities (%)

SurplusRelief (%)

2016 15.5 1.4 1.2 16.5 17.9 2.9

2015 16.7 1.5 1.1 4.7 17.4 2.9

2014 16.6 1.8 1.1 4.4 17.6 1.8

2013 15.7 2.2 1.2 11.6 17.8 2.9

2012 16.7 2.4 1.1 2.3 17.7 3.1

06/2017 16.0 0.7 XX XX XX XX

06/2016 15.9 0.7 XX XX XX XX

C&S/Liabilities vs Industry

0.0

4.0

8.0

12.0

16.0

20.0

2012 2013 2014 2015 2016

16.715.7

16.6 16.715.5

17.7 17.8 17.6 17.4 17.9

- Company C&S/Liabilities - Industry Composite C&S/Liabilities

* Industry Composite - Individual Life Composite

Reinsurance Leverage vs Industry

0.0

20.0

40.0

60.0

80.0

100.0

2012 2013 2014 2015 2016

60.5

103.495.7 91.7 93.9

72.1

86.593.3

98.8 95.6

- Company Reinsurance Leverage - Industry Composite Reinsurance Leverage

* Industry Composite - Individual Life Composite

006508 - Guardian Life Insurance Company of America

Page 20 of 33 Print Date: October 23, 2017

Underwriting Leverage (Continued...)

Ceded Reinsurance Analysis

Year

Company Industry Composite

Face AmountReinsurance

Ceded

AffiliatedReinsuranceRecoverable

/ Capital &Surplus

UnaffiliatedReinsuranceRecoverable

/ Capital &Surplus

TotalReinsuranceRecoverable

/ Capital &Surplus

SurplusRelief

ReinsuranceLeverage

TotalReinsuranceRecoverable

/ Capital &Surplus

ReinsuranceLeverage

2016 149,453,849 0.7 0.8 1.5 1.4 93.9 2.9 95.6

2015 139,157,222 0.6 0.6 1.2 1.5 91.7 2.9 98.8

2014 130,039,866 0.6 1.1 1.7 1.8 95.7 2.9 93.3

2013 120,505,357 0.7 1.2 1.8 2.2 103.4 2.7 86.5

2012 114,093,169 0.6 1.2 1.8 2.4 60.5 2.8 72.1

Liquidity

The following text is derived from A.M. Best's Credit Report on Guardian Life & Health Group (AMB# 020389).

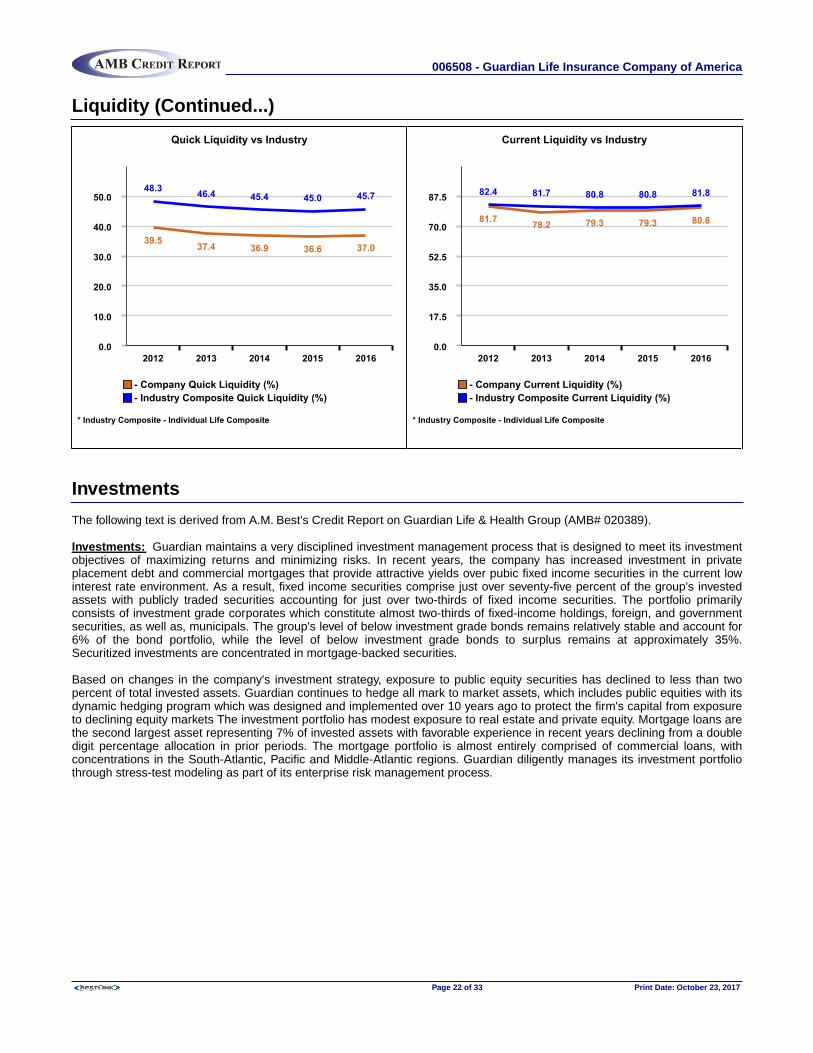

Liquidity: According to the A.M. Best Liquidity model for U.S. Life Insurers, Guardian maintains a high level of liquiditysuitable for its diversified risk profile. Both its short-term (30 days) and longer term (six to 12 months) ratios which measurescash needs positions under stressed scenarios exceed 100%. A ratio that exceeds 100% indicates that a higher comfort levelexists that a company's exposure to liquidity risk is acceptable. This high degree of liquidity also enables Guardian to meetunexpected needs for cash without the untimely sale of investments, which could result in realized gains/losses due to marketvolatility. Guardian's quick and current liquidity ratio's measures the proportion of liabilities covered by cash and investmentsthat can be converted quickly to cash are within expectations and are comparable to industry composites. Guardian's non-investment grade fixed-income securities, mortgage and real estate, and affiliated investments relative to capital areconsidered favorable when compared to the total industry and mutual company composites.

Liquidity Analysis

Year

Company Industry Composite

OperatingCash Flow

($000)Quick

LiquidityCurrent

Liquidity

Non-Investment

GradeBonds /Capital

Delinq &ForeclosedMortgage /

Capital

Mortgage& Real

Estate toCapital

AffiliatedInvestment

to CapitalQuick

LiquidityCurrent

Liquidity

2016 2,706,781 37.0 80.8 33.1 ... 55.1 27.5 45.7 81.8

2015 2,585,843 36.6 79.3 29.5 ... 55.4 23.9 45.0 80.8

2014 2,561,836 36.9 79.3 32.8 ... 49.6 27.2 45.4 80.8

2013 2,126,844 37.4 78.2 34.6 ... 52.4 29.8 46.4 81.7

2012 2,040,746 39.5 81.7 33.9 ... 60.2 29.2 48.3 82.4

06/2017 1,149,523 XX 81.5 28.6 ... 53.7 24.5 XX XX

06/2016 1,245,464 XX 80.3 38.4 ... 54.6 27.3 XX XX

006508 - Guardian Life Insurance Company of America

Page 21 of 33 Print Date: October 23, 2017

Liquidity (Continued...)

Quick Liquidity vs Industry

0.0

10.0

20.0

30.0

40.0

50.0

2012 2013 2014 2015 2016

39.5 37.4 36.9 36.6 37.0

48.3 46.4 45.4 45.0 45.7

- Company Quick Liquidity (%) - Industry Composite Quick Liquidity (%)

* Industry Composite - Individual Life Composite

Current Liquidity vs Industry

0.0

17.5

35.0

52.5

70.0

87.5

2012 2013 2014 2015 2016

81.7 78.2 79.3 79.3 80.8

82.4 81.7 80.8 80.8 81.8

- Company Current Liquidity (%) - Industry Composite Current Liquidity (%)

* Industry Composite - Individual Life Composite

Investments

The following text is derived from A.M. Best's Credit Report on Guardian Life & Health Group (AMB# 020389).

Investments: Guardian maintains a very disciplined investment management process that is designed to meet its investmentobjectives of maximizing returns and minimizing risks. In recent years, the company has increased investment in privateplacement debt and commercial mortgages that provide attractive yields over pubic fixed income securities in the current lowinterest rate environment. As a result, fixed income securities comprise just over seventy-five percent of the group's investedassets with publicly traded securities accounting for just over two-thirds of fixed income securities. The portfolio primarilyconsists of investment grade corporates which constitute almost two-thirds of fixed-income holdings, foreign, and governmentsecurities, as well as, municipals. The group's level of below investment grade bonds remains relatively stable and account for6% of the bond portfolio, while the level of below investment grade bonds to surplus remains at approximately 35%.Securitized investments are concentrated in mortgage-backed securities.

Based on changes in the company's investment strategy, exposure to public equity securities has declined to less than twopercent of total invested assets. Guardian continues to hedge all mark to market assets, which includes public equities with itsdynamic hedging program which was designed and implemented over 10 years ago to protect the firm's capital from exposureto declining equity markets The investment portfolio has modest exposure to real estate and private equity. Mortgage loans arethe second largest asset representing 7% of invested assets with favorable experience in recent years declining from a doubledigit percentage allocation in prior periods. The mortgage portfolio is almost entirely comprised of commercial loans, withconcentrations in the South-Atlantic, Pacific and Middle-Atlantic regions. Guardian diligently manages its investment portfoliothrough stress-test modeling as part of its enterprise risk management process.

006508 - Guardian Life Insurance Company of America

Page 22 of 33 Print Date: October 23, 2017

Investments (Continued...)

Investment Yields (%)

Year Net Yield Bonds Stocks MortgagesCash &

Short Term

Real Estate InvestmentExpense

RatioGross Net

2016 4.62 4.60 1.43 4.94 0.53 18.14 2.90 8.67

2015 4.81 4.82 2.80 4.93 0.35 25.69 4.42 8.70

2014 5.58 4.93 21.20 5.62 0.21 16.82 5.25 5.76

2013 4.90 4.98 1.62 6.46 0.38 17.18 4.93 5.88

2012 5.12 5.28 1.50 6.23 0.60 17.58 5.68 5.74

Investments - Bond Portfolio

2016 Distribution By Maturity

Years YearsAverageMaturity0-1 1-5 5-10 10-20 20+

Government 1.6 1.6 0.5 0.2 2.3 11.3

Government Agencies ... 0.3 1.2 1.7 4.8 19.4

Industrial & Miscellaneous 1.7 16.0 30.8 10.1 26.6 12.9

Affiliated 0.4 ... ... ... ... 0.5

Hybrid Securities ... ... ... ... 0.1 19.9

Total 3.8 17.9 32.5 12.0 33.8 13.3

006508 - Guardian Life Insurance Company of America

Page 23 of 33 Print Date: October 23, 2017

Investments - Bond Portfolio (Continued...)

Bond Distribution By Issuer Type

2016 2015 2014 2013 2012

Bonds ($000) 35,447,351 31,715,928 29,652,862 27,379,870 25,186,382

US Government 4.5 5.2 4.4 5.2 4.5

Foreign Government 0.1 0.5 1.8 1.4 1.8

State, Municipal & Special Revenue - US 8.2 8.9 9.2 10.8 13.6

Industrial & Miscellaneous - US 87.2 85.4 84.6 82.6 80.2

2016 Bond Distribution By Issuer Type

4.5%

0.1%

8.2%

87.2%

US Government Foreign Government State, Municipal & Special Revenue - US Industrial & Miscellaneous - US

Bond Percent Private vs Public

2016 2015 2014 2013 2012

Private Issues 34.2 34.2 33.1 31.4 29.9

Public Issues 65.8 65.8 66.9 68.6 70.1

Bond Quality

2016 2015 2014 2013 2012

Class 1 52.2 52.2 49.2 48.2 49.5

Class 2 41.4 41.6 43.9 44.7 43.4

Class 3 3.3 3.1 3.5 3.1 3.4

Class 4 2.8 2.7 3.1 3.6 3.3

Class 5 0.3 0.4 0.3 0.3 0.4

006508 - Guardian Life Insurance Company of America

Page 24 of 33 Print Date: October 23, 2017

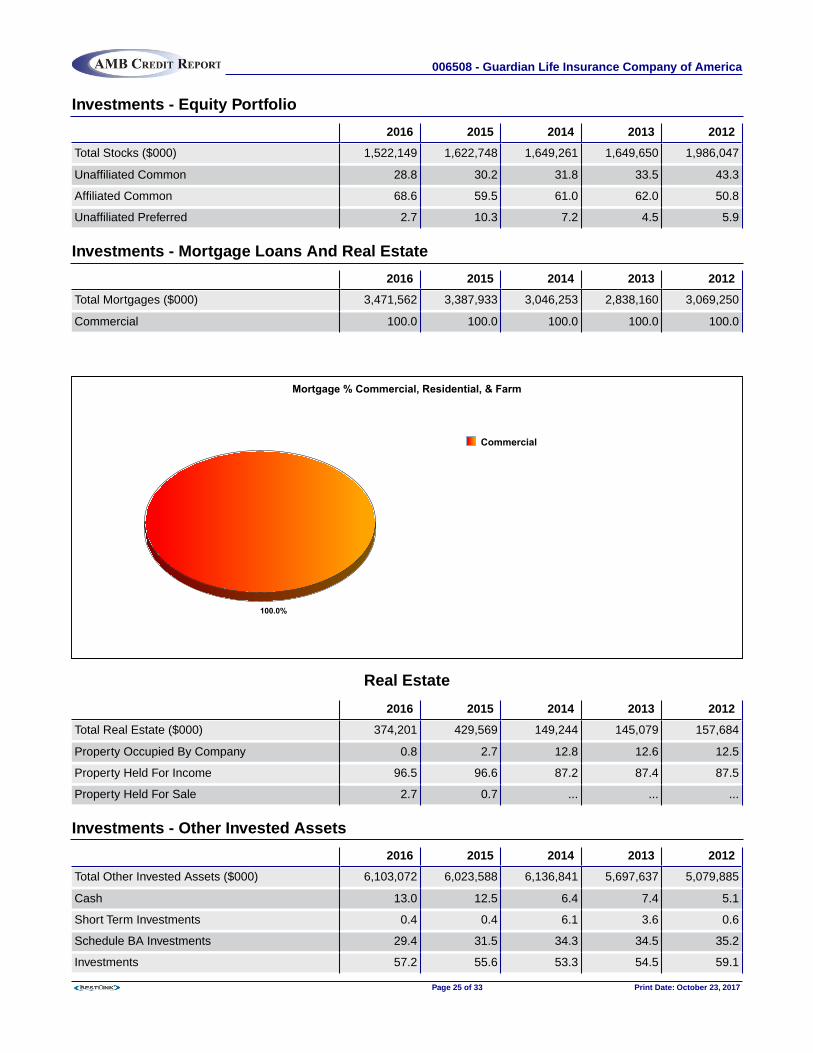

Investments - Equity Portfolio

2016 2015 2014 2013 2012

Total Stocks ($000) 1,522,149 1,622,748 1,649,261 1,649,650 1,986,047

Unaffiliated Common 28.8 30.2 31.8 33.5 43.3

Affiliated Common 68.6 59.5 61.0 62.0 50.8

Unaffiliated Preferred 2.7 10.3 7.2 4.5 5.9

Investments - Mortgage Loans And Real Estate

2016 2015 2014 2013 2012

Total Mortgages ($000) 3,471,562 3,387,933 3,046,253 2,838,160 3,069,250

Commercial 100.0 100.0 100.0 100.0 100.0

Mortgage % Commercial, Residential, & Farm

100.0%

Commercial

Real Estate

2016 2015 2014 2013 2012

Total Real Estate ($000) 374,201 429,569 149,244 145,079 157,684

Property Occupied By Company 0.8 2.7 12.8 12.6 12.5

Property Held For Income 96.5 96.6 87.2 87.4 87.5

Property Held For Sale 2.7 0.7 ... ... ...

Investments - Other Invested Assets

2016 2015 2014 2013 2012

Total Other Invested Assets ($000) 6,103,072 6,023,588 6,136,841 5,697,637 5,079,885

Cash 13.0 12.5 6.4 7.4 5.1

Short Term Investments 0.4 0.4 6.1 3.6 0.6

Schedule BA Investments 29.4 31.5 34.3 34.5 35.2

Investments 57.2 55.6 53.3 54.5 59.1

006508 - Guardian Life Insurance Company of America

Page 25 of 33 Print Date: October 23, 2017

History

Date Incorporated: 04/10/1860 Date Commenced: 07/16/1860 Domicile: NY

Originally incorporated as Germania Life Insurance Company, the present title was adopted in 1918. The company was fullymutualized during 1945.

Mergers: Berkshire Life Insurance Company, Massachusetts, 2001.

RS Investments (65% stake) 2006

Officers And Directors

OfficersPresident and CEO: Deanna M. MulliganEVP and CFO: Marc CostantiniEVP and Chief Investment Officer: Thomas G. SorellEVP and General Counsel: Tracy L. RichEVP: Michael N. Ferik (Individual Markets)SVP and CFO: Michael B. Cefole (Group and WorksiteMarkets)

SVP and Secretary: Harris OlinerSVP, Chief Actuary and Chief Risk Officer: MichaelSlipowitzSVP and Controller: John H. FlanniganSVP and Chief Human Resource Officer: Jay E.Rosenblum

DirectorsJohn J. BrennanLloyd E. CampbellRichard E. CavanaghNancy E. CooperDeborah L. Duncan

William C. FredaChristopher T. JennyDeanna M. MulliganStephen J. SqueriDonald C. Waite III

Regulatory

An examination of the financial condition was made as of December 31, 2008, by the insurance department of New York. The2016 annual independent audit of the company was conducted by PricewaterhouseCoopers, LLP. The annual statement ofactuarial opinion is provided by Michael Slipowitz, FSA, CERA, MAAA, Senior Vice President, Corporate Chief Actuary & ChiefRisk Officer.

Reserve Basis: (Current ordinary business): 2001 CSO 3.5%; Commissioners Reserve Valuation Method for most plans.(Current group business): 1960 CSG 4 1/2%; One year term valuation.

Reinsurance

The following text is derived from A.M. Best's Credit Report on Guardian Life & Health Group (AMB# 020389).

The company limits its exposure to loss by maintaining ceding agreements with several major reinsurers under various types oftreaties. Maximum net retention on any one life is $15 million for ordinary life and $1 million for group life.

006508 - Guardian Life Insurance Company of America

Page 26 of 33 Print Date: October 23, 2017

Balance Sheet ($000)

Admitted Assets YE 2016 YE 2015

Bonds 35,447,351 31,715,928

Preferred Stocks 40,487 166,835

Common Stocks 1,481,662 1,455,913

Mortgage Loans 3,471,562 3,387,933

Real Estate 374,201 429,569

Contract Loans 3,405,118 3,337,426

Cash & short-term Investments 821,843 778,064

Other Invested Assets 1,793,047 1,896,606

Funds held by reinsurance companies 2,478,728 2,377,467

Premiums & Consideration Due 1,057,513 1,020,721

Investment income due & accrued 384,281 366,715

Other Assets 1,127,921 1,187,713

Total Assets 51,883,712 48,120,890

Liabilities & Surplus YE 2016 YE 2015

+ Net Policy Reserves 39,392,187 37,056,018

Liabilities for deposit type contracts 1,209,718 406,752

Policy Claims 783,716 708,466

Dividend Reserve ... ...

Interest maintenance reserve 463,529 373,157

Commissions, taxes and expenses 1,172,846 917,394

Asset Valuation Reserve 809,617 798,261

Contingency Reserve ... ...

Other Liabilities 1,879,612 1,771,172

Total Liabilities 45,711,225 42,031,220

YE 2016: + Analysis of reserves; Life $34,093,413; annuities $236,763; supplementary contracts with life contingencies$20,417; accidental death benefits $5,291; disability active lives $129,587; disability disabled lives $344,893; miscellaneousreserves $848,587; accident & health $3,713,234.

YE 2015: + Analysis of reserves; Life $31,986,720; annuities $246,936; supplementary contracts with life contingencies$23,467; accidental death benefits $5,402; disability active lives $122,612; disability disabled lives $364,837; miscellaneousreserves $807,216; accident & health $3,498,828.

Capital & Surplus YE 2016 YE 2015

Surplus Notes 845,429 845,263

Contingency Reserve 3,007 3,007

Unassigned Surplus 5,323,051 5,205,498

Special Reserve 1,000 1,000

Other Surplus ... 34,903

Total Liabilities & Surplus 51,883,712 48,120,890

006508 - Guardian Life Insurance Company of America

Page 27 of 33 Print Date: October 23, 2017

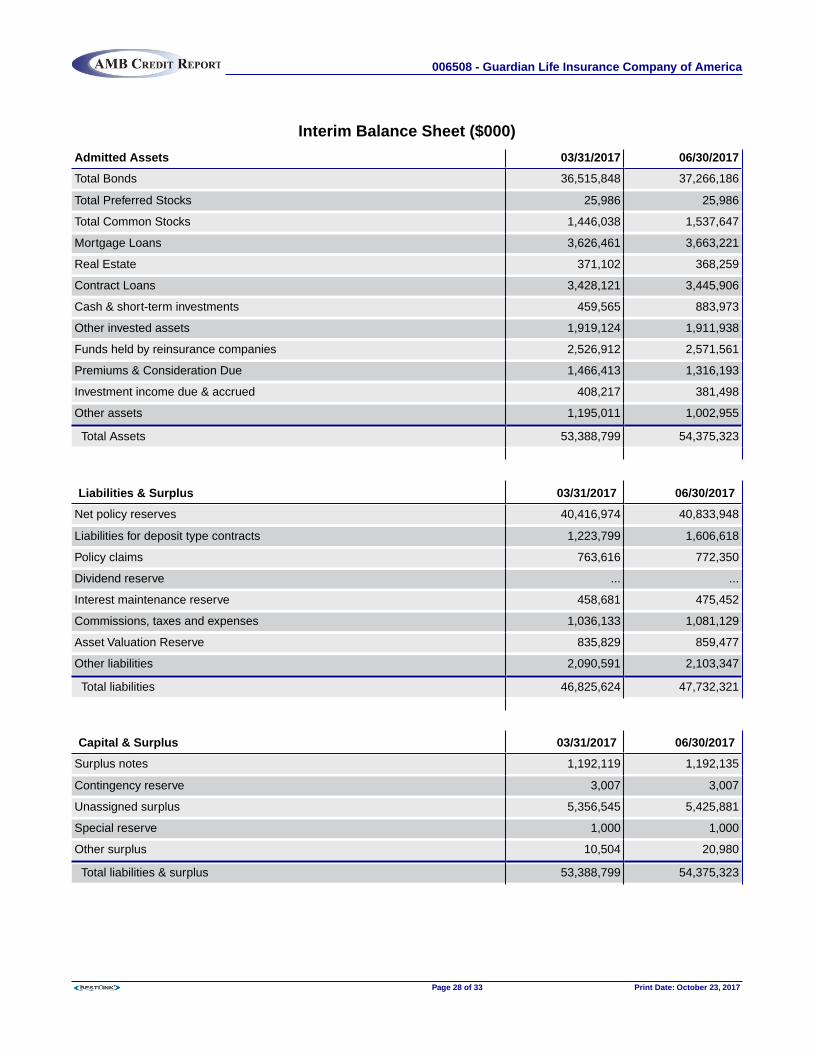

Interim Balance Sheet ($000)

Admitted Assets 03/31/2017 06/30/2017

Total Bonds 36,515,848 37,266,186

Total Preferred Stocks 25,986 25,986

Total Common Stocks 1,446,038 1,537,647

Mortgage Loans 3,626,461 3,663,221

Real Estate 371,102 368,259

Contract Loans 3,428,121 3,445,906

Cash & short-term investments 459,565 883,973

Other invested assets 1,919,124 1,911,938

Funds held by reinsurance companies 2,526,912 2,571,561

Premiums & Consideration Due 1,466,413 1,316,193

Investment income due & accrued 408,217 381,498

Other assets 1,195,011 1,002,955

Total Assets 53,388,799 54,375,323

Liabilities & Surplus 03/31/2017 06/30/2017

Net policy reserves 40,416,974 40,833,948

Liabilities for deposit type contracts 1,223,799 1,606,618

Policy claims 763,616 772,350

Dividend reserve ... ...

Interest maintenance reserve 458,681 475,452

Commissions, taxes and expenses 1,036,133 1,081,129

Asset Valuation Reserve 835,829 859,477

Other liabilities 2,090,591 2,103,347

Total liabilities 46,825,624 47,732,321

Capital & Surplus 03/31/2017 06/30/2017

Surplus notes 1,192,119 1,192,135

Contingency reserve 3,007 3,007

Unassigned surplus 5,356,545 5,425,881

Special reserve 1,000 1,000

Other surplus 10,504 20,980

Total liabilities & surplus 53,388,799 54,375,323

006508 - Guardian Life Insurance Company of America

Page 28 of 33 Print Date: October 23, 2017

Summary Of 2016 Operations ($000)

Income 2016 Disbursements 2016

Premiums: Death benefits 1,022,009

Ordinary life premiums 3,829,389 Claims incurred (PC) ...

Individual annuities premiums 16,396 Matured endowments 1,628

Credit life premiums ... Annuity & old age benefits 5,670

Group life premiums 543,116 Disability & Accident & Health benefits 22,267

Group annuities premiums ... Coupons, annual endowments & similarbenefits

...

Accident & Health group premiums 2,912,433 Surrender benefits 1,140,509

Accident & Health credit premiums ... Group conversion 1,418

Accident & Health other premiums 471,383 Accident & Health benefits 2,101,617

Industrial life premiums ... Interest on contract or deposit-type funds 32,896

Miscellaneous premiums ... Payments on supplemental contracts 2,451

Premiums & annuity considerations ... Accumulated coupon payments ...

Fraternal premiums ... Total benefits recodes 125

Aviation reinsurance premiums ... Increase in life reserves 2,121,762

Deposit type funds ... Increase in accident & health reserves 206,141

Employee benefits plan premiums ... Increase in liabilities for premium depositfunds

...

Deposit administration funds ... Change in reserves ...

Other premiums ... Reserve adjustment on reinsuranceassumed

3,465

Reinsurance premiums ... Other reserves ...

Total net premiums 7,772,716 Claim adjustment (PC only) ...

Supplementary contracts 2,376 Administrative expenses (PC only) ...

Coupon accum interest ... Commissions on premiums & annuityconsiderations

501,390

Net investment income 2,052,329 Commissions & expenses on reinsuranceassumed

214,024

Amortization of Interest MaintenanceReserve

121,995 Other commissions & expenses 5

Net operating gain from separate accounts ... Reinsurance expenses ...

Commissions & expense allowance on reinceded

86,222 Interest expenses 18,629

Reserve adjustment on reinsurance ceded ... Insurance taxes, licenses & fees 236,791

Reinsurance income 58,829 General insurance expenses 1,257,372

Other income 150,554 Net transfer to separate accounts ...

Difference between net earned & net written(PC only)

... Other expenses 764

Management and/or service fees 1,251 Miscellaneous operating expenses ...

Other disbursements ...

Total operating income 10,246,272 Total disbursements 8,890,932

006508 - Guardian Life Insurance Company of America

Page 29 of 33 Print Date: October 23, 2017

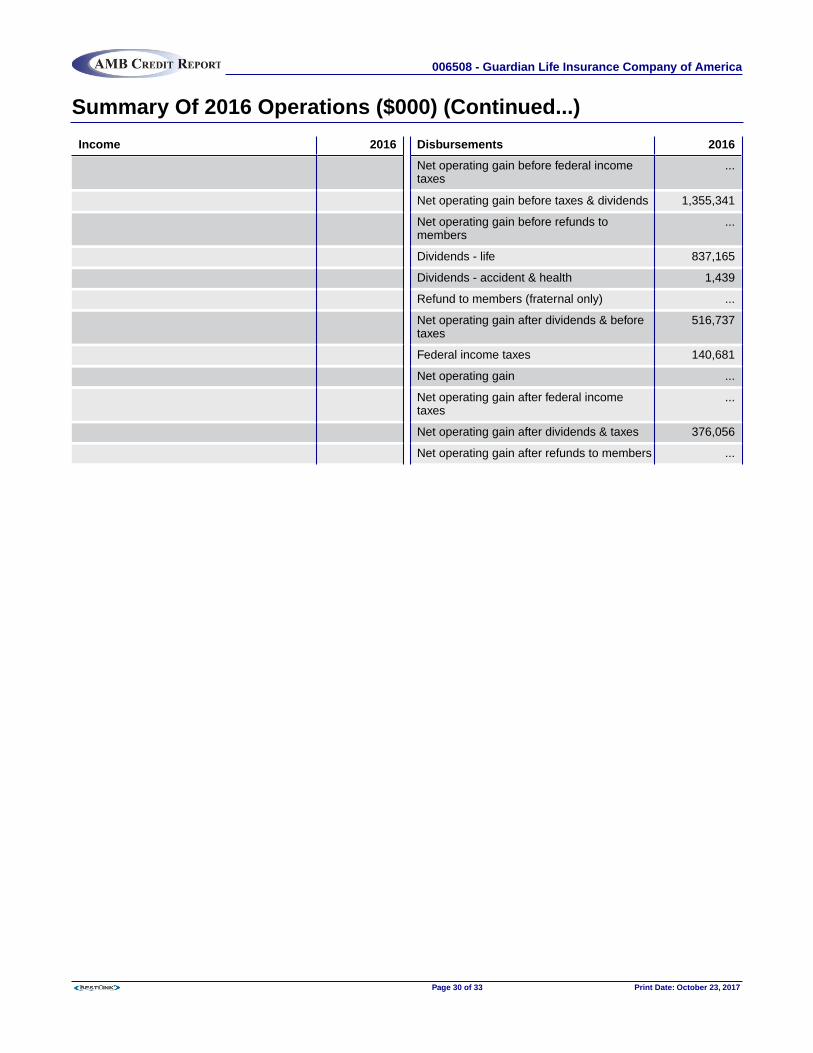

Summary Of 2016 Operations ($000) (Continued...)

Income 2016 Disbursements 2016

Net operating gain before federal incometaxes

...

Net operating gain before taxes & dividends 1,355,341

Net operating gain before refunds tomembers

...

Dividends - life 837,165

Dividends - accident & health 1,439

Refund to members (fraternal only) ...

Net operating gain after dividends & beforetaxes

516,737

Federal income taxes 140,681

Net operating gain ...

Net operating gain after federal incometaxes

...

Net operating gain after dividends & taxes 376,056

Net operating gain after refunds to members ...

006508 - Guardian Life Insurance Company of America

Page 30 of 33 Print Date: October 23, 2017

Interim Summary Of Operations ($000)

Period Ended06/30/2017

Period Ended06/30/2016

Increase /Decrease

Premiums & annuity considerations 4,084,130 3,863,901 220,229

Aviation reinsurance premiums ... ... ...

Deposit type funds ... ... ...

Employee benefits plan premiums ... ... ...

Deposit administration funds ... ... ...

Other premiums ... ... ...

Reinsurance premiums ... ... ...

Total premiums 4,084,130 3,863,901 220,229

Supplementary contracts 1,160 1,124 36

Coupon accum interest ... ... ...

Net investment income 1,024,192 1,022,677 1,515

Amortization of Interest Maintenance Reserve 48,592 53,643 -5,051

Net operating gain from separate accounts ... ... ...

Commissions & expense allowance on rein ceded 44,699 43,058 1,641

Reserve adjustment on reinsurance ceded ... ... ...

Other income 123,097 89,675 33,422

Difference between net earned & net written (PC only) ... ... ...

Total operating income 5,325,870 5,074,079 251,791

Death benefits 556,401 505,026 51,375

Claims incurred (PC) ... ... ...

Matured endowments 548 437 112

Annuity and old age benefits 3,029 2,980 49

Disability & Accident & Health benefits 1,091,569 1,074,130 17,439

Coupons, annual endowments & similar benefits ... ... ...

Surrender benefits 598,137 536,156 61,981

Group conversion 716 698 18

Interest on contract or deposit-type funds 22,120 14,443 7,677

Payments on supplemental contracts 804 1,620 -817

Accumulated coupon payments ... ... ...

Total benefits recodes -163 62 -225

Increase in liabilities for premium deposit funds ... ... ...

Change in reserves 1,441,762 1,342,193 99,568

Claim adjustment (PC only) ... ... ...

Administrative expenses (PC only) ... ... ...

Commissions on premiums & annuity considerations 260,016 246,370 13,647

Commissions & expenses on reinsurance assumed 105,092 97,438 7,653

Insurance taxes, licenses & fees 99,201 132,799 -33,598

General insurance expenses 502,488 471,642 30,846

006508 - Guardian Life Insurance Company of America

Page 31 of 33 Print Date: October 23, 2017

Interim Summary Of Operations ($000) (Continued...)

Period Ended06/30/2017

Period Ended06/30/2016

Increase /Decrease

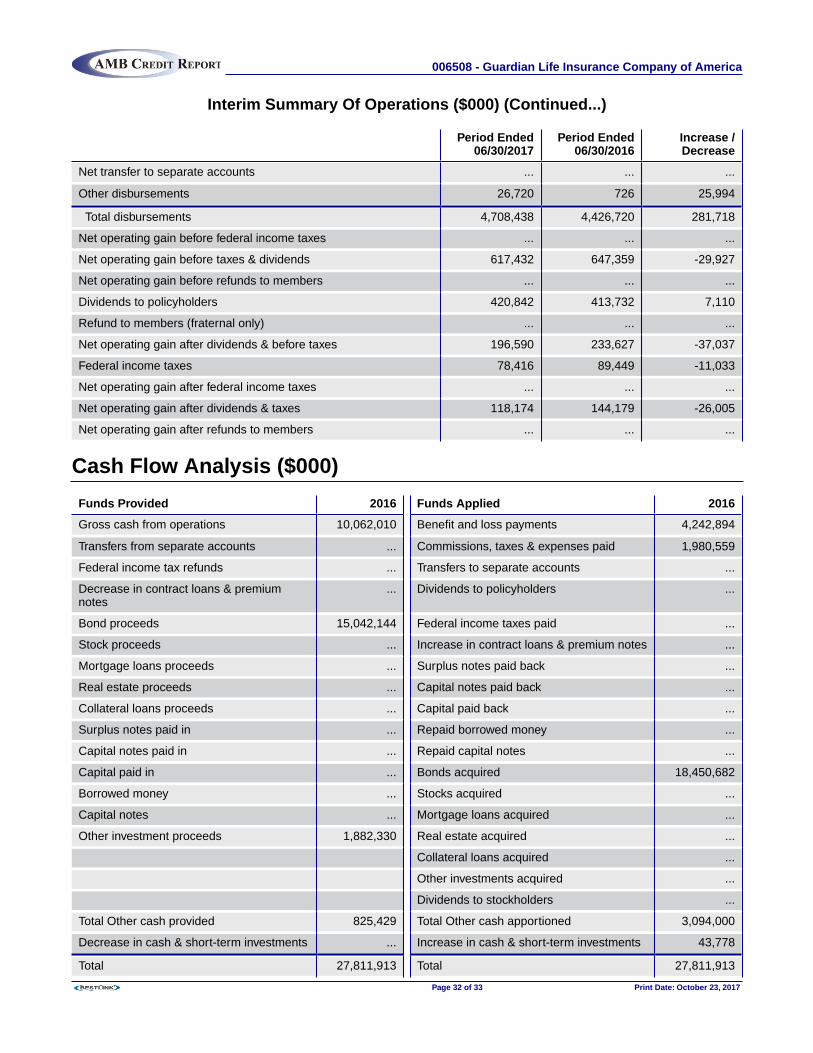

Net transfer to separate accounts ... ... ...

Other disbursements 26,720 726 25,994

Total disbursements 4,708,438 4,426,720 281,718

Net operating gain before federal income taxes ... ... ...

Net operating gain before taxes & dividends 617,432 647,359 -29,927

Net operating gain before refunds to members ... ... ...

Dividends to policyholders 420,842 413,732 7,110

Refund to members (fraternal only) ... ... ...

Net operating gain after dividends & before taxes 196,590 233,627 -37,037

Federal income taxes 78,416 89,449 -11,033

Net operating gain after federal income taxes ... ... ...

Net operating gain after dividends & taxes 118,174 144,179 -26,005

Net operating gain after refunds to members ... ... ...

Cash Flow Analysis ($000)

Funds Provided 2016 Funds Applied 2016

Gross cash from operations 10,062,010 Benefit and loss payments 4,242,894

Transfers from separate accounts ... Commissions, taxes & expenses paid 1,980,559

Federal income tax refunds ... Transfers to separate accounts ...

Decrease in contract loans & premiumnotes

... Dividends to policyholders ...

Bond proceeds 15,042,144 Federal income taxes paid ...

Stock proceeds ... Increase in contract loans & premium notes ...

Mortgage loans proceeds ... Surplus notes paid back ...

Real estate proceeds ... Capital notes paid back ...

Collateral loans proceeds ... Capital paid back ...

Surplus notes paid in ... Repaid borrowed money ...

Capital notes paid in ... Repaid capital notes ...

Capital paid in ... Bonds acquired 18,450,682

Borrowed money ... Stocks acquired ...

Capital notes ... Mortgage loans acquired ...

Other investment proceeds 1,882,330 Real estate acquired ...

Collateral loans acquired ...

Other investments acquired ...

Dividends to stockholders ...

Total Other cash provided 825,429 Total Other cash apportioned 3,094,000

Decrease in cash & short-term investments ... Increase in cash & short-term investments 43,778

Total 27,811,913 Total 27,811,913

006508 - Guardian Life Insurance Company of America

Page 32 of 33 Print Date: October 23, 2017