00 Feldman FM.indd xvi 10/13/09 11:34:04...

30

-

Upload

nguyenquynh -

Category

Documents

-

view

214 -

download

0

Transcript of 00 Feldman FM.indd xvi 10/13/09 11:34:04...

00_Feldman_FM.indd xvi 10/13/09 11:34:04 PM

00_Feldman_FM.indd i 10/13/09 11:34:03 PM

Praise for the new edition of

Reverse Mergers And Other Alternatives to Traditional IPOs

By David N. Feldman With contributions by Steven Dresner

“ Reverse mergers and self-filings are important alternatives to traditional IPOs, but with recent rule changes and developments in the market, these transactions have become more complex than ever. David Feldman’s second edition of Reverse Mergers explains these important developments in plain English and is an invaluable resource [for] any participant involved in the business of taking small companies public.”

—Timothy J. Keating President, Keating Investments

“ David Feldman’s new edition of Reverse Mergers is a must for any practicing securities lawyer’s library—along with Romeo and Dye’s Section 16 treatise and Hick’s Resales of Restricted Securities. Once again, in clear and concise language, Feldman takes the reader through the often-tricky landscape of reverse mergers and alternative public offerings and, by way of illuminating real-world anecdotes, teaches the reader how to avoid the potholes and use this fi nancing technique to its fullest potential. A masterful book by the master in the reverse-merger area.”

—Mitchell C. Littman, Esq. Founding partner, Littman Krooks

“ David Feldman’s Reverse Mergers is the most current go-to source for dealmakers, investors, and entrepreneurs [interested in] going public without an IPO.”

—Chandra S. Mishra, Phd Eminent scholar and professor, Florida Atlantic University

00_Feldman_FM.indd ii 10/13/09 11:34:03 PM

“ Feldman’s Reverse Mergers should be required reading for any company planning to go public. It is the definitive source of information for issu-ers and for professionals involved in executing these transactions—and a roadmap for the industry to follow for many years to come.”

—Richard Rappaport, ceo WestPark Capital

“ Feldman has a unique ability to walk companies through the reversemerger process. His thorough understanding of all of the alternatives enables companies to make good business decisions. Reverse Mergers will prove to be invaluable for any company thinking of going public.”

—Charles Weinstein Managing partner, Eisner LLP

00_Feldman_FM.indd iii 10/13/09 11:34:03 PM

Reverse Mergers

00_Feldman_FM.indd iv 10/13/09 11:34:04 PM

Also available from Bloomberg Press

The Issuer’s Guide to PIPEs: New Markets, Deal Structures, and Global Opportunites

for Private Investments in Public Equity Edited by Steven Dresner

PIPEs: A Guide to Private Investments in Public Equity Revised and Updated Edition

Edited by Steven Dresner with E. Kurt Kim

Hedge Fund of Funds Investing: New Strategies for the Hedge Fund Marketplace

by Joseph G. Nicholas

Market-Neutral Investing: Long/Short Hedge Fund Strategies

by Joseph G. Nicholas

Due Diligence for Global Deal Making: The Defi nitive Guide to Cross-Border Mergers and Acquisitions,

Joint Ventures, Financings, and Strategic Alliances Edited by Arthur H. Rosenbloom

The Securitization Markets Handbook: Issuing and Investing in Mortgage- and Asset-Backed Securities

by Charles Austin Stone and Anne Zissu

A complete list of our titles is available at www.bloomberg.com/books

Attention Corporations

This book is available for bulk purchase at special discount. Special editions or chapter reprints can also be customized to specifications. For information,

please e-mail Bloomberg Press, [email protected], Attention: Director of Special Markets, or phone 212-617-7966.

00_Feldman_FM.indd v 10/13/09 11:34:04 PM

Reverse Mergers And Other Alternatives to

Traditional IPOs

Second Edition

David N. Feldman

With contributions by Steven Dresner

Bloomberg Press

New York

00_Feldman_FM.indd vi 10/13/09 11:34:04 PM

© 2006, 2009 by David N. Feldman. All rights reserved. Protected under the Berne Convention. Printed in the United States of America. No part of this book may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher except in the case of brief quotations embodied in critical articles and reviews. For information, please write to Permissions Department, Bloomberg Press, 731 Lexington Avenue, New York, NY 10022, or send an e-mail to [email protected].

BLOOMBERG, BLOOMBERG ANYWHERE, BLOOMBERG.COM, BLOOMBERG MARKET ESSENTIALS, Bloomberg Markets, BLOOMBERG NEWS, BLOOMBERG PRESS, BLOOMBERG PROFESSIONAL, BLOOMBERG RADIO, BLOOMBERG TELEVISION, and BLOOMBERG TRADEBOOK are trademarks and service marks of Bloomberg Finance L.P. (“BFLP”), a Delaware limited partnership, or its subsidiaries. The BLOOMBERG PROFESSIONAL service (the “BPS”) is owned and distributed locally by BFLP and its subsidiaries in all jurisdictions other than Argentina, Bermuda, China, India, Japan, and Korea (the “BLP Countries”). BFLP is a wholly owned subsidiary of Bloomberg L.P. (“BLP”). BLP provides BFLP with all global marketing and operational support and service for these products and distributes the BPS either directly or through a non-BFLP subsidiary in the BLP Countries. All rights reserved.

This publication contains the authors’ opinions and is designed to provide accurate and authoritative information. It is sold with the understanding that the authors, publisher, and Bloomberg L.P. are not engaged in rendering legal, accounting, investment planning, or other professional advice. The reader should seek the services of a qualified professional for such advice; the authors, publisher, and Bloomberg L.P. cannot be held responsible for any loss incurred as a result of specific investments or planning decisions made by the reader.

First edition published 2006 Second edition published 2009

1 3 5 7 9 10 8 6 4 2

Library of Congress Cataloging-in-Publication Data

Feldman, David N. Reverse mergers : and other alternatives to traditional IPOs / David N. Feldman ; with

contributions by Steven Dresner. – 2nd ed. p. cm.

Includes bibliographical references and index. Summary: “The top expert in the field of reverse mergers provides an executive summary along

with nuts and bolts explanations showing how these deals are done. The revised edition addresses new regulations, SPACs, growth in China, and other key topics”–Provided by publisher.

ISBN 978-1-57660-340-6 (alk. paper) 1. Going public (Securities) 2. Going public (Securities)–Law and legislation–United States.

3. Corporations--United States--Finance. I. Dresner, Steven, 1970- II. Title.

HG4028.S7F45 2009 658.1’64–dc22 2009039854

00_Feldman_FM.indd vii 10/13/09 11:34:04 PM

I am thrilled to dedicate this second edition to the

three people that matter most to me in the world.

My amazing wife Barbra remains my sounding board,

best friend, and life partner. And, of course, my

kids: Sammi brings me great pride in her talent and

dedication to helping others, and Andrew never fails

to bring me joy and amazement at his extraordinary

intelligence and unbridled love for life.

00_Feldman_FM.indd viii 10/13/09 11:34:04 PM

C O N T E N T S

List of Illustrations .................................................................xv

Acknowledgments ................................................................ xvii

Introduction............................................................... 1 The Structure of This Book ................................................................... 4

1 Why Go Public?.......................................................... 9 Advantages of Being Public.................................................................... 9

Access to Capital ............................................................................... 9 Liquidity ..........................................................................................11 Growth Through Acquisitions or Strategic Partnerships ....................11 Stock Options for Executives ............................................................12 Confidence in Management ..............................................................13

Disadvantages of Being Public .......................................................... 13 Emphasis on Short-Term Results ......................................................14 Public Disclosure ..............................................................................14 Fraud and Greed (Even After Sarbanes-Oxley) ..................................15 It’s Expensive! ...................................................................................16 Public Companies Attract Lawsuits ...................................................17

Weighing the Pros and Cons ................................................................18

PART ONE | THE BUSINESS OF REVERSE

MERGERS

2 IPOs Versus Reverse Mergers ..................................... 23

Advantages of a Reverse Merger Versus an IPO ...................................27 Lower Cost .......................................................................................28 Speedier Process ...............................................................................29 Not Dependent on IPO Market for Success ......................................30 Not Susceptible to Changes from Underwriters Regarding Initial

Stock Price ...................................................................................32 Less Time-Consuming for Company Executives ................................32 Less Dilution ....................................................................................33 Underwriters Unnecessary ................................................................33

Disadvantages of a Reverse Merger Versus an IPO...............................34

00_Feldman_FM.indd ix 10/13/09 11:34:04 PM

Less Funding ....................................................................................34 Market Support Is Harder to Obtain ................................................34

3 Shells and Deal Structures......................................... 37

Public Shells ..........................................................................................37 Value of Shells ..................................................................................38

Reverse Merger Deal Structures ............................................................43 The Reverse Triangular Merger .........................................................44 Other Deal Structures.......................................................................46 Reverse Stock Splits ..........................................................................47

Doing a Deal ..........................................................................................48

4 Introduction to Rule 419 .......................................... 51 Rule 419..... ..........................................................................................51

Basics of Rule 419 ............................................................................52

Life After Passage of Rule 419 ..............................................................54 Grandfathered Shells ........................................................................54 Public Shells from Operating Companies ..........................................54 SPACs ..............................................................................................54 Form 10 Shells .................................................................................54 The Internet Boom (and Bust) .........................................................56

Today’s Reverse Merger Market ............................................................57

5 China: Land of the Panda, the Great Wall, and Reverse Mergers ................................................. 61

PRC Regulators Challenge, But Do Not Prohibit, Shell Mergers ....................................................................................62

Issues in Structuring Reverse Mergers with Chinese

Decrees in 2005 (Circulars 11, 29, and 75) .......................................62 Six Chinese Ministries Act Jointly in 2006 (Circular 10) ...................63 SAFE 106 .........................................................................................64 SAFE 142—August 2008 .................................................................65

Where Are We? ..............................................................................65 Due Diligence and Other Unique Challenges.................................. 66

Due Diligence ..................................................................................66 Language Barriers .............................................................................67 Cultural Barriers ...............................................................................68 Audit Issues ......................................................................................69

Companies ........................................................................................70

00_Feldman_FM.indd x 10/13/09 11:34:04 PM

Start with a WFOE ..........................................................................70

The Outlook: Good! ........................................................................ 72

6 Financing ................................................................. 75 How Not to Do It.................................................................................76

How Financing Drives the Deal ...........................................................79

Time and Money ..................................................................................86

7 Winning Market Support .......................................... 89

The Market Support Challenge ............................................................90 Limited Float ...................................................................................90 Concentration of Control of the Float ..............................................91 Weak Analyst Coverage of Penny Stocks ...........................................91 Minimal Support from Market Makers .............................................91 Short-Selling Pressure .......................................................................92 Thin Trading Reduces Ability to Raise Money Versus

Active Trading ..............................................................................93

Does an IPO Guarantee Strong Market Support? ................................93

How to Build Post–Reverse Merger Support........................................95 Get a New Attitude ..........................................................................95 The Importance of Investor Relations ...............................................95 Earn Your Support ............................................................................96 Movin’ On Up..................................................................................98 WestPark’s WRASP Structure: A Simple, Smart Idea .......................103

Ticker? What Ticker? ..........................................................................104

8 Shady Tactics .......................................................... 107

A Few “Bad Guy” Anecdotes ..............................................................108 Telltale Signs: Not Disclosing Biographical Information or Trying to Avoid Full Disclosure ......................................................109 One Company’s Search for a Clean Shell: A Case Study ..................110

“Bad Guy” Tactics ...............................................................................114 Inappropriate Expenses and Compensation .....................................114 Strange Money-Raising Activity ......................................................114 Insider Trading ...............................................................................114 Press Releases and Hype .................................................................115 Time Pressure .................................................................................115 Incomplete Disclosure ....................................................................116 Incomplete Insider Filings ..............................................................116

00_Feldman_FM.indd xi 10/13/09 11:34:04 PM

Refusal to Back Up Representations and Warranties ........................116 Messy Isn’t Dirty and “Not Nice” Doesn’t Mean “Bad” ...................117

Bad Investment Banker Tactics ...........................................................117 Lack of Due Diligence ....................................................................117 Nonregistration as Broker-Dealers ..................................................117 Accredited Investors or Not? ...........................................................119

Looking for Mr. Good Guy ................................................................119

PART TWO | LEGAL ISSUES AND TRAPS FOR

THE UNWARY

9 Deal Mechanics ...................................................... 125

Structural and Implementation Issues Relating to Shareholder Approval….. .................................................................................... 125

Structural Approaches to Avoiding Shareholder Approval ................127 Forward and Reverse Stock Splits ....................................................129 Changing the Charter to Allow for Issuance of More Shares ............131 Name Change of the Shell ..............................................................132 Schedule 14f-1: Board Changes ......................................................133 A Merger Isn’t an Offering. Or Is It? ...............................................136

Other Legal Issues...............................................................................140 Unique Legal Opinion Issues ..........................................................140 Are Reps and Warranties from a Shell Meaningless? ........................141 Issues Relating to Fairness Opinions ...............................................144

Above All Else: Seek Competent and Experienced Advisers...............145

10 Due Diligence ........................................................ 147

The Basics.... .......................................................................................... 148

Clean, Dirty, and Messy Shells (and Footnote 32/172 Shells) ...........149 Messy Shells ...................................................................................149 Dirty Shells ....................................................................................154 Footnote 32/172 Shells ...................................................................154

Due Diligence Review of the Private Company .................................162 Minimize Surprises .........................................................................162

11 The Regulatory Regime .......................................... 165

Implementation of SOX .....................................................................165

June 2005 SEC Rule Changes: Reverse Mergers Are Further Legitimized (but Tougher to Consummate) ...................................167

00_Feldman_FM.indd xii 10/13/09 11:34:04 PM

Genesis of the June 2005 Rule Changes ..........................................168 The Rule Is Adopted ......................................................................170 Specifics of the Rule .......................................................................170 One Nice By-Product: Information ................................................174 Who Is Exempt? .............................................................................175 A Little More on Footnote 32 .........................................................176 So, Is It Good or Bad? ....................................................................176

2008 Rule 144 Amendments: Big Changes, Missed Opportunities .................................................................................177

PART THREE | OTHER WAYS TO GO

PUBLIC, MANUFACTURING

SHELLS, AND CURRENT

TRENDS

12 Self-Filings and Other IPO Alternatives ................... 183 How Do Shares of Stock Become Tradable? .......................................183

Registration of Shares .....................................................................184 Exemptions from Registration: Rule 144 ........................................185

Self-Filing Through Form S-1Resale Registration ..............................187 Private Offerings During Registration—Changes in 2007 ...............188

Mechanics of Form S-1 Self-Filing .....................................................190 Engaging Professionals ....................................................................190 Identifying Shareholders .................................................................191 Preparing and Filing the Document ................................................192 SEC (and FINRA) Comments and Revisions ..................................194 Establishing a Trading Market ........................................................196

Self-Filing Through Form 10 Registration .........................................197 Form 10 Versus Form S-1 (Exchange Act Versus Securities Act) ................................................................................197 Filing Form 10 and Automatic Effectiveness ...................................199 Developing a Market After Filing a Form 10 ...................................199

Brief Overview of Other Methods to Become Public.........................199 Regulation A ..................................................................................200 Intrastate Exemption ......................................................................201 Rule 504 ........................................................................................201 Regulation S ...................................................................................202

Which Way to Go? .............................................................................204

00_Feldman_FM.indd xiii 10/13/09 11:34:04 PM

13 Special Purpose Acquisition Companies (SPACs) ..... 205

Introduction to SPACs: The GKN Experience ..................................206

The SPAC Resurgence—Bubble and Bust .........................................209

What Is the Future of SPACs? ............................................................213

Wrap-up on SPACs.............................................................................215

14 Form 10 Shells........................................................ 217 Mechanics of Creating a Form 10 Shell..............................................218

Getting Started: Forming and Capitalizing the Entity .....................218 Preparing and Filing the Form 10 ...................................................221 Posteffective Responsibilities Prior to a Merger ...............................223

Raising Money and Finding Shareholders ..........................................224

Selling a Shell ......................................................................................224 Merging with a Form 10 Shell ........................................................225 Postmerger Registration—Rule 415 Limitation ...............................227 Preparation for Trading ...................................................................228

Legal Issues Regarding Form 10 Shells ...............................................229 The Worm/Wulff Letters—Mostly Gone ........................................229 Proper Capitalization ......................................................................231 Challenges in Postmerger Registration ............................................232

Advantages and Disadvantages of Form 10 Shells ..............................232 Advantages of Form 10 Shells .........................................................232 Disadvantages of Form 10 Shells .....................................................234

Endnote on SPACs and Form 10 Shells .............................................236

15 The Experts Speak (Again): A Look Ahead............... 237

Recent Market Volatility .....................................................................238

There are more “cash and carry” acquisitions of shells in reverse mergers that leave little or no equity behind for shell owners,

More companies are going public and deferring the

There is more interest now from Europe and Latin America,

Self-filings are more attractive as a result of the “evergreen”

What of the Predictions from the First Edition? ................................238

Current Developments .......................................................................240

but are paid for in cash. ..............................................................240

commencement of trading..........................................................241

while China remains strong. .......................................................242 SPACs are struggling—will they return? ..........................................242

requirement and the longer postmerger 144 holding period. .......243

00_Feldman_FM.indd xiv 10/13/09 11:34:04 PM

Notwithstanding the above, the benefits of being public and even of reverse mergers are mostly greater than before, thanks to Rule 144 reform. .........................................................244

There is more confidence in Form 10 shells as a vehicle for certain types of transactions. The price for trading shells has dropped from a few years ago................................................245

Footnote 32/172 shells have proliferated despite efforts by British Columbia and FINRA to address them. ...........................246

The WRASP structure is having a real impact. ................................247 Reverse mergers between two operating companies are

becoming more popular. .............................................................248

And So It Goes....................................................................................249

Glossary ............................................................................... 251

Index .................................................................................. 271

00_Feldman_FM.indd xv 10/13/09 11:34:04 PM

I L L U S T R A T I O N S

Figures

I.1 Closed Reverse Mergers by Year ..................................................3

3.1 Flowchart of a Reverse Triangular Merger.................................45

7.1 Recent IPO Deal Activity..........................................................94

7.2 NYSE Amex Initial Listing Requirements.................................99

7.3 Nasdaq Global and Capital Market Initial Listing Requirements........................................................................... 101

xv

00_Feldman_FM.indd xvi 10/13/09 11:34:04 PM

00_Feldman_FM.indd xvii 10/13/09 11:34:04 PM

A C K N O W L E D G M E N T S

I really can’t believe it. Way back in 2003 when talk fi rst started about a book, I had no idea of the impact it would have, and I am humbled and grateful for the outpouring of support and appreciation I have received as the first edition sailed through its first three printings. And now, the second edition! There are many to thank (but more succinctly than last time)!

First are those who helped with this new edition. As always, at the top of the list is my contributor Steven Dresner. Steven was directly responsible for bringing me to Bloomberg Press. His contributions, charts, and data were critically important. Over at Bloomberg Press, thanks to Stephen Isaacs, Judy Sjo-Gaber, and their team for doing a tremendous job on every level, from marketing to content. Thanks to my “experts” for their contributions in the last chapter, and special thanks to lawyer and friend Richard Anslow for providing guidance on certain aspects of the new China chapter.

Let me also thank all my incredible colleagues at Feldman LLP. I especially wish to thank my senior counsel Scott Miller for all your hard work and talent.

Thanks also to Sam Katz of TZP Group for his continued extraordinary leadership of Youth Renewal Fund, Peter Boneparth, formerly of Jones Apparel Group and president of the board of Lawrence Woodmere Academy, and Alan Bernstein, its headmaster. To Bobby Blumenfeld and everyone at the Association for Corporate Growth, thanks for the opportunities you have provided. And one more shoutout to Jeff Meshel and all my friends at the Strategic Forum.

On a personal level, my wife, Barbra, and children, Sammi and Andrew, are truly amazing. Barbra, we make it together through all life throws at us and I’m constantly amazed at your poise and patience. You are an awesome wife and mother and I am so proud of your accomplishments in

xvii

00_Feldman_FM.indd xviii 10/13/09 11:34:04 PM

xviii Acknowledgments

the community. Sammi and Andrew, thanks for being such a source of pride and happiness in my life.

To all my clients, business friends, and referral sources, I truly owe my success to you, and I thank you very much for all your business, your friendship, your support, and the joy of being able to use my brain every day to assist you. I look forward to coming into work each morning.

00_Feldman_FM.indd xix 10/13/09 11:34:04 PM

Reverse Mergers

00_Feldman_FM.indd xx 10/13/09 11:34:04 PM

01_Feldman_Introduction.indd 1 10/13/09 11:08:49 PM

Introduction

Over the last decade, Wall Street has discovered that there are more ways to go public than through the traditional initial public offering (IPO), making it easier for more companies

to reap the benefits of public status. Public companies find it easier to attract investors than private ones do because investments in public companies are more liquid. Because of this liquidity, public companies can also use their stock more effectively to fund acquisitions and reward executives. Having various options for going public is good news to the vast majority of smaller companies, most of which do not fi t the typical profile investment banks use when deciding which companies can successfully accomplish an IPO.

The two most popular alternatives to IPOs are reverse mergers (including mergers with special purpose acquisition companies, or SPACs) and self-filings. The following well-known companies have gone public through reverse mergers:

❑ Texas Instruments Inc. ❑ Jamba Juice, Inc. ❑ Berkshire Hathaway Inc. ❑ Tandy Corporation (Radio Shack Corporation) ❑ Occidental Petroleum Corporation ❑ Muriel Siebert & Co., Inc. ❑ Blockbuster Entertainment ❑ The New York Stock Exchange

1

01_Feldman_Introduction.indd 2 10/13/09 11:08:49 PM

2 Reverse Mergers

Less well-known deals are no less interesting:

❑ In 2006, Cougar Biotechnology merged with a shell company and raised $50 million. In 2009, it was sold for $1 billion.

❑ In February 2005, an investor group led by billionaire Robert F. X. Sillerman, former owner of well-known concert promoter SFX Entertainment, raised $46.5 million contemporaneously with the acquisition of a public shell company called Sports Entertainment Enterprises, Inc. and the acquisition of an 85 percent interest in Elvis Presley’s name, image, and likeness, and the operations of his home at Graceland. Since then the company, now known as CKX, Inc., has completed several more acquisitions including the proprietary rights to the American Idol television show. In April 2006, it paid $50 million for an 80 percent interest in boxer Muhammad Ali’s name, likeness, and image. Recently, Sillerman offered to take the company private, but that transaction was terminated as a result of the fi nancial turmoil in the fall of 2008.

❑ In 2002, RAE Systems went public in a reverse merger at $0.20 a share. As of this writing in early 2009 the stock was trading at around $4.

❑ Global Sources Ltd. reverse merged into The Fairchild Corporation. As of this writing, it has a market capitalization of approximately $430 million.

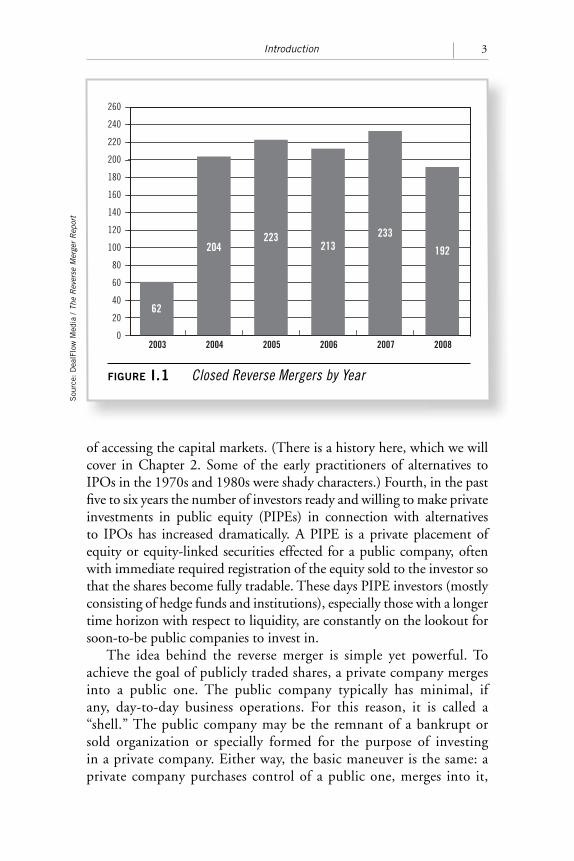

Alternatives to IPOs have grown in popularity over the last ten years. The number of closed reverse mergers has increased very dramatically since 2000, although activity levels dropped off markedly in late 2008 because of the significant and sudden stock market meltdown. (See FIGURE I.1, Closed Reverse Mergers by Year.) The recession and market uncertainty of late 2008 and early 2009 has hit all sectors of the economy. But many signs indicate that this fast-paced growth will resume and continue in the near future.

There are several reasons for this growth. First, the IPO market effectively closed, seemingly permanently, to all smaller companies in late 2000 following the dot-com bust. Those seeking to go public were forced to fi nd other ways to accomplish their goals. Second, the alternatives to IPOs offer benefits that traditional IPOs do not, especially to companies interested in raising capital in the $5 million to $50 million range. Third, a series of SEC regulations and enforcement policies have turned reverse mergers and self-filings into completely aboveboard, legitimate methods

01_Feldman_Introduction.indd 3 10/13/09 11:08:49 PM

Introduction 3

Sou

rce:

Dea

lFlo

w M

edia

/ Th

e R

ever

se M

erge

r R

epor

t

FIGURE I.1 Closed Reverse Mergers by Year

62

204 223

213 233

192

0

20

40

60

80

100

120

140

160

180

200

220

240

260

2003 2004 2005 2006 2007 2008

of accessing the capital markets. (There is a history here, which we will cover in Chapter 2. Some of the early practitioners of alternatives to IPOs in the 1970s and 1980s were shady characters.) Fourth, in the past five to six years the number of investors ready and willing to make private investments in public equity (PIPEs) in connection with alternatives to IPOs has increased dramatically. A PIPE is a private placement of equity or equity-linked securities effected for a public company, often with immediate required registration of the equity sold to the investor so that the shares become fully tradable. These days PIPE investors (mostly consisting of hedge funds and institutions), especially those with a longer time horizon with respect to liquidity, are constantly on the lookout for soon-to-be public companies to invest in.

The idea behind the reverse merger is simple yet powerful. To achieve the goal of publicly traded shares, a private company merges into a public one. The public company typically has minimal, if any, day-to-day business operations. For this reason, it is called a “shell.” The public company may be the remnant of a bankrupt or sold organization or specially formed for the purpose of investing in a private company. Either way, the basic maneuver is the same: a private company purchases control of a public one, merges into it,

01_Feldman_Introduction.indd 4 10/13/09 11:08:50 PM

4 Reverse Mergers

and when the merger is complete becomes a publicly traded company in its own right.

Self-filings, which provide another alternative to an IPO—one that does not utilize a shell—take advantage of the SEC regulation that allows private companies to become public by voluntarily following the same rules (and filing the same documents) that public companies follow. After agreeing to mandatory compliance with the SEC reporting regime, a company earns public status and can then offer securities to the public market or complete a PIPE.

This book is written for seasoned pros and beginners alike. It is—as of this writing—and has been since the publication of the fi rst edition in 2006, the fi rst and only book to explain the business and legal issues specific to reverse mergers and self-filings. My goal was to create a text that would be useful to company CEOs and CFOs as well as the professionals who advise them—lawyers, accountants, consultants, and investment bankers. Please note: I wrote this not just for lawyers. It covers legal issues in plain English.

This book is my best effort to codify what I have learned about alternatives to IPOs over the nineteen years since Feldman LLP, the boutique law firm I founded, and a predecessor firm, began this part of our practice. During that time we have worked with hundreds of clients contemplating reverse mergers and self-filings. Steven Dresner, my friend and contributor to this book, has enriched the text with the wisdom he has gleaned in his capacities as editor of PIPEs: A Guide to Private Investments in Public Equity (Bloomberg Press, 2005), and as the organizer of numerous business conferences on PIPEs and reverse mergers through his company, DealFlow Media.

The Structure of This Book Chapter 1 discusses the pros and cons of going public. After Chapter 1, the book is divided into three parts. Part One covers the business of reverse mergers. Chapter 2 compares the benefits of a reverse merger to the benefits of an IPO. Chapter 3 presents an overview of the market for shells, how they are formed, and basic reverse merger deal structures. The shell market is ever changing, in no small part due to rule changes by the SEC. Chapter 4 reviews the history behind the famous SEC Rule 419, which for a while in the early 1990s all but stopped the market for creating shells from scratch and taking them public. Chapter 5, added for the first time in this second edition, covers the dramatic presence of Chinese companies in the reverse

01_Feldman_Introduction.indd 5 10/13/09 11:08:50 PM

5 Introduction

merger market. It discusses legal and cultural challenges as well as the excitement that any market bubble brings.

Chapter 6 covers the financings that typically accompany a reverse merger, especially those done as PIPE investments. It includes examples of a few specific transactions from the fields of biotechnology, entertainment, technology, and sports, which are analyzed in depth. Issues of disclosure and valuation are discussed. An acknowledged challenge following a reverse merger is building and obtaining support for the company’s newly trading stock. Chapter 7 covers this issue in depth, with the goal of changing attitudes toward the issue. Rather than seeking an immediate “pop” in a stock, as sometimes happens after an IPO, reverse merged companies require patience for support to build over time.

Chapter 8, the last chapter of Part One, provides a road map for those of us (I hope all of us) who seek to steer clear of unsavory and illegitimate activity in this field. Covered here are bad shell owner tactics and bad investment banker tactics. A list of signs that are consistent with behavior of a credible, legitimate player is included. As in all things Wall Street, it is difficult to go anywhere without finding some bad guys. Indeed, the venerable IPO suffered a black eye when state and federal regulators fined IPO underwriters over $2 billion for illegal excesses in the IPOs of the late 1990s. But reverse mergers also have a checkered past, something that has been almost entirely reversed in terms of both perception and reality.

Part Two covers legal issues and traps. Chapter 9 describes deal structures and issues in completing merger agreements. The famous “reverse triangular merger” is examined. Issues in a shell’s capital structure and availability of shares are also discussed. How parties back up their statements and promises is another issue, as is changing the name of the shell after a deal.

Chapter 10 covers a critically important issue in reverse mergers: due diligence. This involves “scrubbing” a shell that may have a history of prior operations, as well as working to avoid or minimize risks from dirty or messy shells (these are two different things). So-called Footnote 32/172 shells, which were targeted by the SEC in its 2005 rulemaking as being of questionable validity and, unfortunately, were made more attractive in the SEC’s amendments to its Rule 144 in 2008, are discussed. These are particularly thorny shells to examine, because they appear to be real businesses that went public, when in fact they are either fake start-ups or very small real businesses that will be stripped out or shut down upon a merger wherein no disclosure of the promoter’s real intent is made.

01_Feldman_Introduction.indd 6 10/13/09 11:08:50 PM

6 Reverse Mergers

Chapter 11 discusses the regulatory regime in greater depth. In particular, the chapter explores the sweeping and dramatic legislation, known as the Sarbanes-Oxley Act, which was passed in 2002 following the Enron and WorldCom debacles. This law mandated many changes— most of them for the good—in how public companies act. But, among other things, it has led to increases in the cost of being public. This chapter also reviews the SEC rulemaking of June 2005 that imposed signifi cant new disclosure requirements immediately following a reverse merger. By means of these rules, the SEC sought to eliminate more bad players at the same time as it affirmed that these techniques are a perfectly legitimate means of structuring companies. In addition, this chapter reviews SEC rule changes in 2008 relating to the availability of Rule 144 as a way for shares to become tradable without registration with the SEC.

Part Three covers other ways to go public without an IPO, manufacturing shells, and current trends. It starts with Chapter 12, which covers self-filings in depth and gives an overview of a few other methods of going public without an IPO or reverse merger. There are two ways to go about a self-filing: either by means of a resale registration to allow existing shares to start trading, or through filing a Form 10, which simply puts the company on the mandatory SEC reporting list. Once it is fully reporting, if shareholders have the ability to sell without having their shares individually registered with the SEC, trading can commence.

Chapter 13, which looks at SPACs, continues to be the only primer on a technique that had exploded in recent years before the creation of new vehicles stopped in early 2008. A SPAC, or special purpose acquisition company, is a public shell created specifically to enable a company to go public. It raises large amounts of money that can then be given to the private company it merges with. A SPAC’s shares are permitted to trade (most other manufactured shells’ stock does not trade), and investors in the SPAC get to review and approve the proposed merger. Each SPAC generally has an industry or geographic focus, and has a management team experienced in that sector to review potential merger candidates. As of this writing in early 2009, over 150 SPACs have been formed since 2003. Of these, approximately seventy have completed business combinations and over sixty are public and still awaiting a merger candidate. These shell vehicles had been raising anywhere from $20 million to hundreds of millions of dollars.

The next intense area of current activity, covered in Chapter 14, is manufacturing Form 10 shells. The SEC appears to favor these over some other types of shells (such as those created under Rule 419). Well over 150 of these shells have been formed by clients of my law fi rm alone!

01_Feldman_Introduction.indd 7 10/13/09 11:08:50 PM

7 Introduction

The last chapter of the book, Chapter 15, reviews a variety of other current issues: the growth in so-called “cash and carry” acquisitions of shell companies, the growing interest in companies from Latin America and Eastern Europe, the SPAC market influx, the growing attractiveness of self-filings, and the dramatic impact of the mostly positive, but also negative, changes to Rule 144. This chapter includes extensive quotes and thoughts from a number of leading industry players, from accountants to investment bankers to attorneys and others.

01_Feldman_Introduction.indd 8 10/13/09 11:08:50 PM

![My Updated CV as a Saidshoo [5807]](https://static.fdocuments.in/doc/165x107/5879941f1a28ab95318b62c9/my-updated-cv-as-a-saidshoo-5807.jpg)