0 CHAPTER 10 Long-Term (Capital Investment) Decisions © 2009 Cengage Learning.

36

1 CHAPTER 10 Long-Term (Capital Investment) Decisions © 2009 Cengage Learning

-

Upload

deborah-anderson -

Category

Documents

-

view

230 -

download

5

Transcript of 0 CHAPTER 10 Long-Term (Capital Investment) Decisions © 2009 Cengage Learning.

1

CHAPTER 10

Long-Term (Capital Investment) Decisions

© 2009 Cengage Learning

2

2

Introduction

Capital Investment Decisions•Which do I purchase?•What is the return on the investment?•What are the qualitative costs and benefits?•What are the quantitative costs and benefits?

3

3

Focus on Cash Flow

Long-term investment decisions require a consideration of the time value of money.

The time value of money is based on the concept of a

dollar received (paid) today being worth more (less) than a dollar received (paid) in the

future.

4

4

Focus on Cash Flow

•Original investment

•Repairs and maintenance

•Extra operating costs

•Incremental revenues

•Cost reductions in operating expenses

•Salvage value

•Release of working capital at the end

What cash flows should I

consider??

5

5

Focus on Cash Flow

Long-term investment decisions require a consideration of the time value of money. The time value of money is based on the concept that a dollar received today is worth more than a dollar received in the future.

Key Concept

6Discounted Cash Flow Analysis

The time value of money is considered in capital

investment decisions by using one of two techniques: the net present value (NPV) method or the internal rate of return

(IRR) method.

Key Concept

7Net Present Value

The cost of capital represents what the firm

would have to pay to borrow (issue funds) or

raise funds through equity (issue stock) in

the financial marketplace. In NPV, the discount rate serves as a hurdle rate or a minimum required rate of return.

What do I use for a discount

rate?

8

8

Net Present Value

If the present value of cash inflows is greater than or equal to the

present value of cash outflows (the NPV is greater than or equal to

zero), the investment provides a return at least equal to the discount rate (the minimum

required rate or return), and the investment is acceptable.

Key Concept

9

9

Net Present Value

•Cost: $50,000

•Net increase in cash flows (Revenues-Expenses): $14,000 for six years

•No salvage value

•MRR = 12% (use for discount rate)

Should B&R purchase a new

refrigerated delivery van?

10

10

Net Present Value

Cash Flow

Initial Investment

Annual Cash Income

Net Present Value

Year

Now

1-6

Amount

$(50,000)

14,000

12% Factor

1.0000

4.1114

Present Value

$(50,000.00)

57,559.60

$7,559.60

Because the NPV is positive, the delivery van

should be purchased.

11

11

Internal Rate of Return

The internal rate of return (IRR) is the actual yield or return earned by an investment. The IRR is the discount rate that makes the NPV = 0.

Key Concept

12

12

Internal Rate of Return

•IRR can be found by using a NPV table, financial calculator, or Excel

•When determining whether to accept a project, you must also consider the impact of uncertainty on the decision

•Changes in assumptions about future revenues and costs are likely to affect the decision

13

13

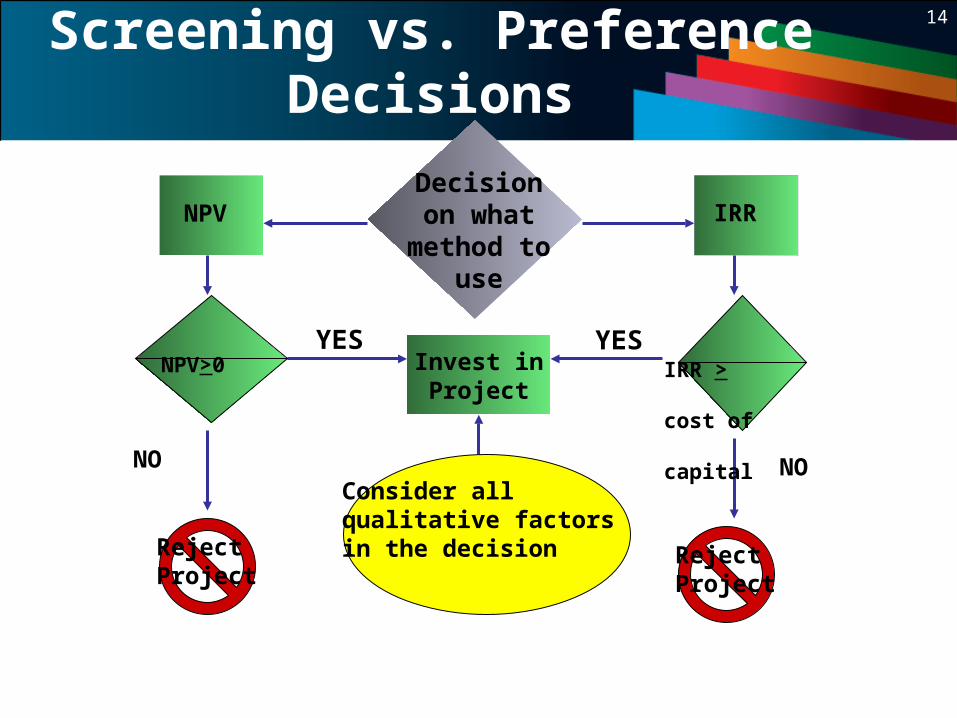

Screening and Preference Decisions

•Screening decisions involve deciding if an

investment meets some predetermined company

standard

•Preference decisions involve choosing among

alternatives

14

14

Screening vs. Preference Decisions

Invest inProject

Decisionon what

method touse

NPV

NO NO

YES YES

IRR

IRR > cost of capital

NPV>0

RejectProject

RejectProject

Consider allqualitative factorsin the decision

15

15

Screening and Preference Decisions

Profitability Index (PI): Calculated by dividing the present value of the cash flow by the initial investment.

A PI greater than 1.0 means that the NPV is positive and the project is acceptable.

16

16

The Impact of Taxes on Capital Investment

Decisions•Nonprofit organizations such as hospitals, museums, churches, and other organizations are structured as organizations exempt from federal and state income taxes

•Profit-making companies must consider the impact of income taxes on capital investment and other management decisions

17

17

The Impact of Taxes on Capital Investment

Decisions

Taxes are a major source of cash outflows for many

companies and must be taken into consideration in

calculations of the time value of money.

Key Concept

18

18

Extended Example

Amber Valley Ski Resort is considering installing another

chair lift for a new undeveloped area that would expand the amount of area

available for skiing.

The options are to put in a double, triple, or quadruple

chair lift to carry two, three, or four skiers on each chair.

19

19

The Impact of Uncertainty on Capital Investment Decisions

What if the number of skiers did not increase at

the rate that was projected?

Will the acquisition of the new lift still result in a sufficient return on the

investment?

20

20

The Impact of Uncertainty on Capital Investment Decisions

One way to adjust for risk is to increase the cost of capital used in the NPV calculations.

How do I try to

adjust for uncertain

ty?

21

21

Sensitivity Analysis

Sensitivity Analysis: Used to highlight decisions that may be affected by changes in expected cash flows. Uses what-if analysis to determine how sensitive capital investment decisions are to changes (number of skiers per day).

22

22

The Impact of the New Manufacturing Environment on Capital Investment Decisions

Automating a process is more extensive and expensive than just purchasing a piece of equipment. Other expenses include:

•Software needed

•Training of personnel and complementary machines

•Development of new processes

23

23

The Impact of the New Manufacturing Environment on Capital Investment Decisions

Benefits of automating production processes:

•Decreased labor costs

•Increase in the quality of the finished product

•Increased speed of production process

•Increased reliability of the finished product

•An overall reduction in the amount of inventory

24

24

The Impact of the New Manufacturing Environment on Capital Investment Decisions

Analyzing the costs and benefits of investments in automated and

computerized design and manufacturing equipment and

robotics requires careful consideration of both

quantitative and qualitative factors.

Key Concept

25

25

The Payback Method

The payback period is the length of time needed for a long-term

project to recapture or pay back the initial investment.

Payback Period =

Original Investment

Net Annual Cash Inflows

26

26

The Payback Method

The payback method can be useful as a quick

approximation of the discounted cash flow methods

when the cash flows follow similar patterns.

Key Concept

27

27

Appendix

Time Value of Money and Decision Making

•Future Value

•Present Value

•Annuities

28

28

Appendix: Time Value of Money and Decision

Making

The present value of cash flows is the amount of future cash flows discounted to their equivalent worth today. So how do we find the present value?

If I receive cash at different times, how do I determine the time value of money?

29

29

Appendix: Present and Future Value

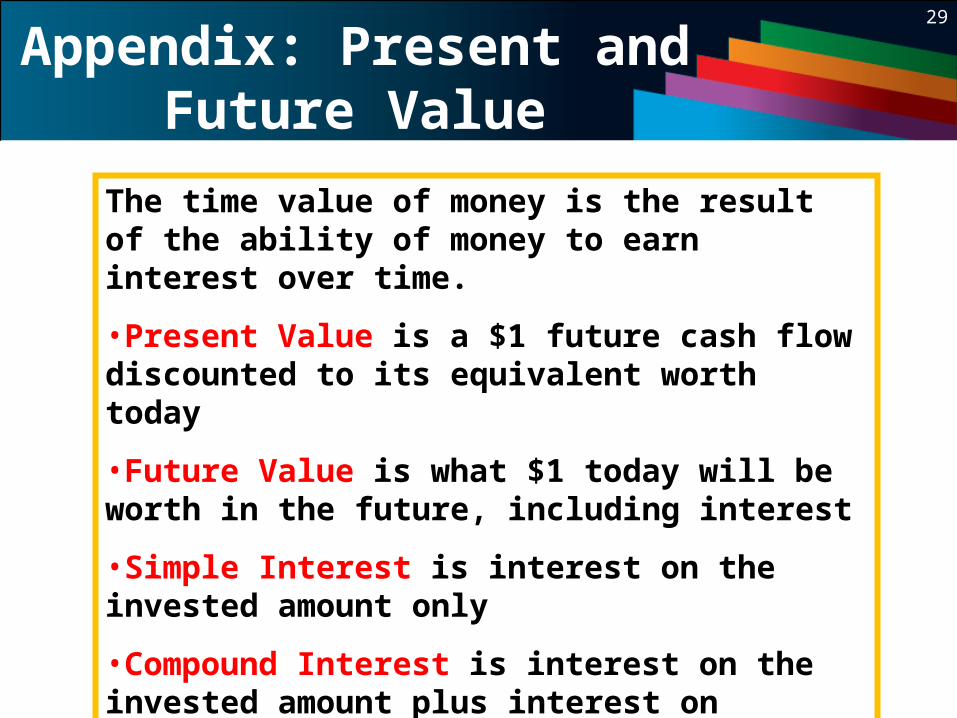

The time value of money is the result of the ability of money to earn interest over time.

•Present Value is a $1 future cash flow discounted to its equivalent worth today

•Future Value is what $1 today will be worth in the future, including interest

•Simple Interest is interest on the invested amount only

•Compound Interest is interest on the invested amount plus interest on previous interest earned but not withdrawn

30

30

Appendix: Future Value

How much will this $100 be worth three years from now if I invest it at 4%?

Year 1$100 @ 4%

$104

Year 2$104 @4%$108.16

Year 3$108.16 @ 4%

$112.19

31

31

Appendix: Future Value

FV = PV (1 + r)n

FV = Future Value

PV = The $ Amount

r = Interest Rate

n = Number of Compounding Periods

32

32

Appendix: Future Value

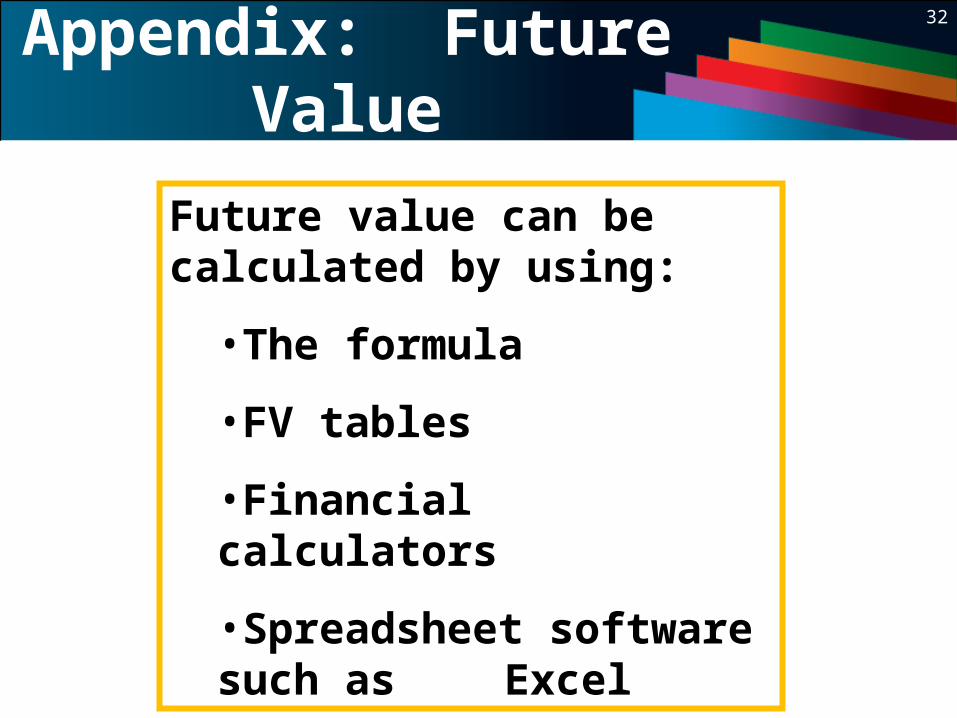

Future value can be calculated by using:

•The formula

•FV tables

•Financial calculators

•Spreadsheet software such as Excel

33

33

Appendix: Present Value

If I need $112.19 three years from now, and I can invest at 4%, how much do I have to invest now?

Year 3$112.19

1.04$108.16

Year 2$108.16

1.04$104.00

Year 1$104.00

1.04$100.00

34

34

Appendix: Present Value

FV

(1+r)n

PV =FV = Future Value

r = Interest Rate

n = Number of

Compounding Periods

35

35

Appendix: Present Value

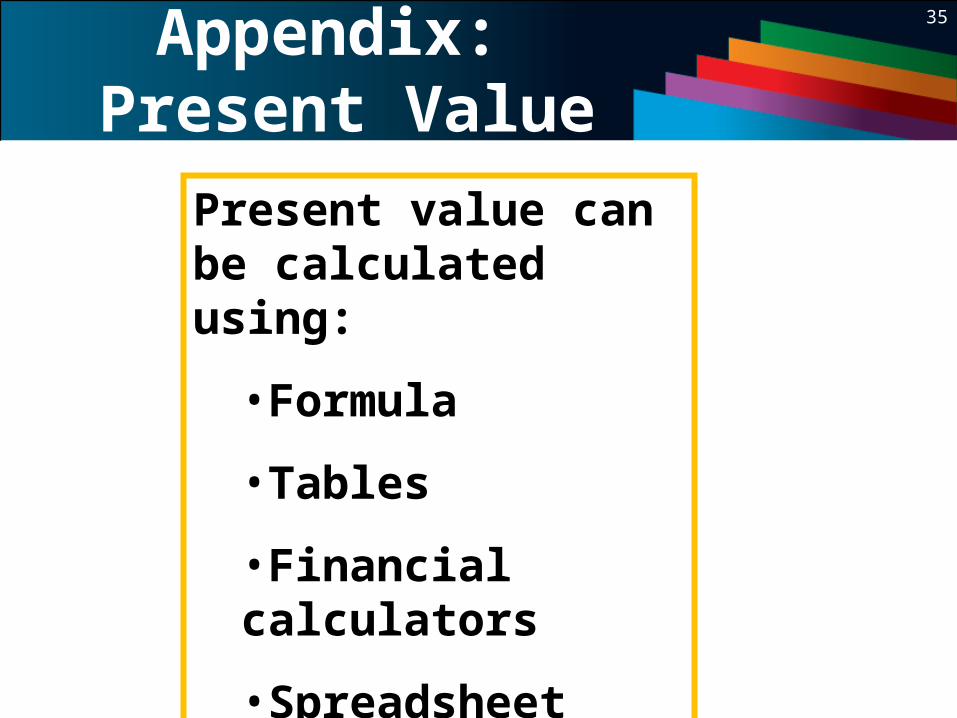

Present value can be calculated using:

•Formula

•Tables

•Financial calculators

•Spreadsheet software such as Excel

36

36

Appendix: Annuities

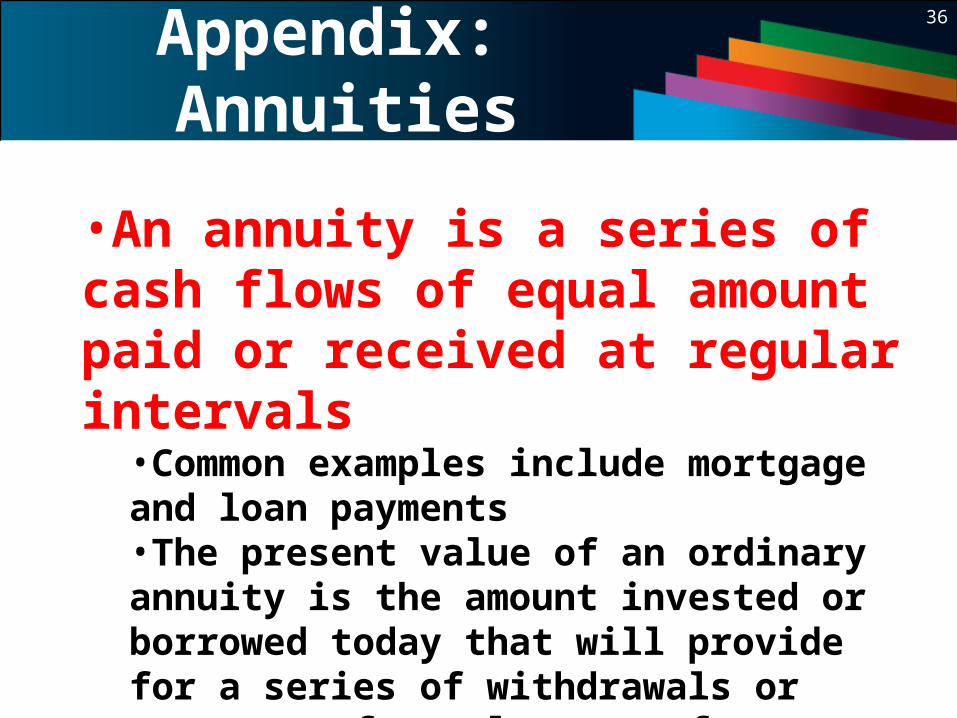

•An annuity is a series of cash flows of equal amount paid or received at regular intervals

•Common examples include mortgage and loan payments•The present value of an ordinary annuity is the amount invested or borrowed today that will provide for a series of withdrawals or payments of equal amount for a set number of periods