0 Bridgewater 0 Global Investment Management BRIDGEWATER ASSOCIATES Alpha Wars: Survival of the...

21

1 Bridgewater 1 Global Investment Management BRIDGEWATER ASSOCIATES Alpha Wars: Survival of the Fittest October 2005 One Glendinning Place Westport, CT 06880 (203) 226-3030 www.bwater.com Bob Prince Co-Chief Investment Officer

-

date post

20-Dec-2015 -

Category

Documents

-

view

219 -

download

1

Transcript of 0 Bridgewater 0 Global Investment Management BRIDGEWATER ASSOCIATES Alpha Wars: Survival of the...

1 Bridgewater 1 Global Investment Management

BRIDGEWATER ASSOCIATES

Alpha Wars: Survival of the Fittest

October 2005

One Glendinning PlaceWestport, CT 06880

(203) 226-3030www.bwater.com

Bob PrinceCo-Chief Investment Officer

2 Bridgewater 2 Global Investment Management

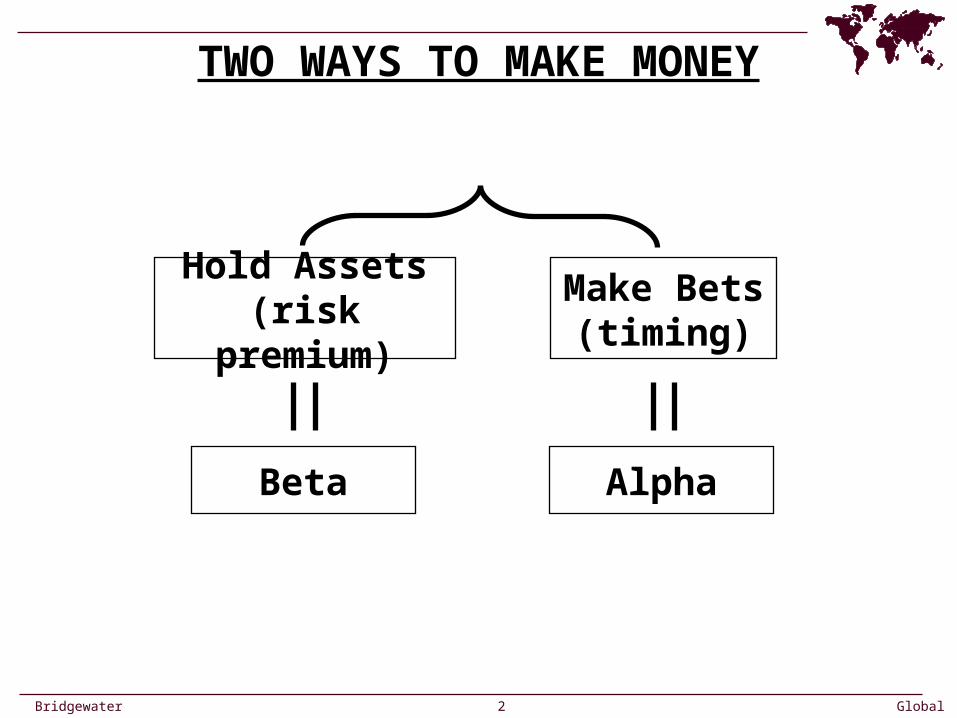

TWO WAYS TO MAKE MONEY

AlphaBeta

Hold Assets(risk premium)

Make Bets (timing)

3 Bridgewater 3 Global Investment Management

Beta +

Type of risk:

Alpha

Source of risk:

Correlation:

Return/Risk ratios:

Difficulty:

Cost:

Systematic Unsystematic

Asset class Manager skill

0.2 to 0.3

High

Unlimited

Low

ExpensiveCheap

HardEasy

Alpha vs. Beta

4 Bridgewater 4 Global Investment Management

THE ALPHA WORLDS ARE CONVERGING

Alpha is a zero sum game, no matter what you call it. Weaker players will lose to stronger players.

Active Management

Alpha Overlay

Traditional

Hedge Funds

5 Bridgewater 5 Global Investment Management

THE WINNERS WILL BE…

SMARTEST

BEST RISK MANAGERS

Make good bets

Portfolio theory applied to alpha

6 Bridgewater 6 Global Investment Management

APPLYING PORTFOLIO THEORY

Return

Risk

Ratio

1.0%

3.0%

0.3

Portfolio of 5

Ones and

Threes

…

…

…

1.0%

3.0%

0.3

…

…

…

1.0%

1.4%

0.7

…

…

…

1.0%

1.1%

0.9

…

…

…

1.0%

0.8%

1.3

Portfolio of 10

Portfolio of 40

7 Bridgewater 7 Global Investment Management

EXAMPLE OF COMBINING ALPHAS

-25%

0%

25%

50%

75%

100%

125%

150%

175%

200%

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02

US Bond Alpha JPY/USD Alpha Combined

Information Ratio:

US Bond Alpha = 0.65

JPY/USD Alpha = 0.55

Combined = 0.87

8 Bridgewater 8 Global Investment Management

DIVERSIFIED ALPHA IS BETTERTHAN NONDIVERSIFIED ALPHA

Traditional Fixed Income Mandate

Fully Diversified Pure Alpha

Sources of Value Added: 77

Average Correlation: 0.04

IR per slice: 0.35

Implied IR: 1.40

Sources of Value Added: 6

Average correlation: 0.25

IR per slice: 0.35

Implied IR: 0.56

9 Bridgewater 9 Global Investment Management

Scaling an Information Ratio of 1.0

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Tracking Error/Volatility

Alp

ha/

Ret

urn

Active EquityBonds

Enhanced Cash Hedge Funds

Source: Bridgewater analysis

GTAA

SCALABILITY OF OVERLAY

Active

10 Bridgewater 10 Global Investment Management

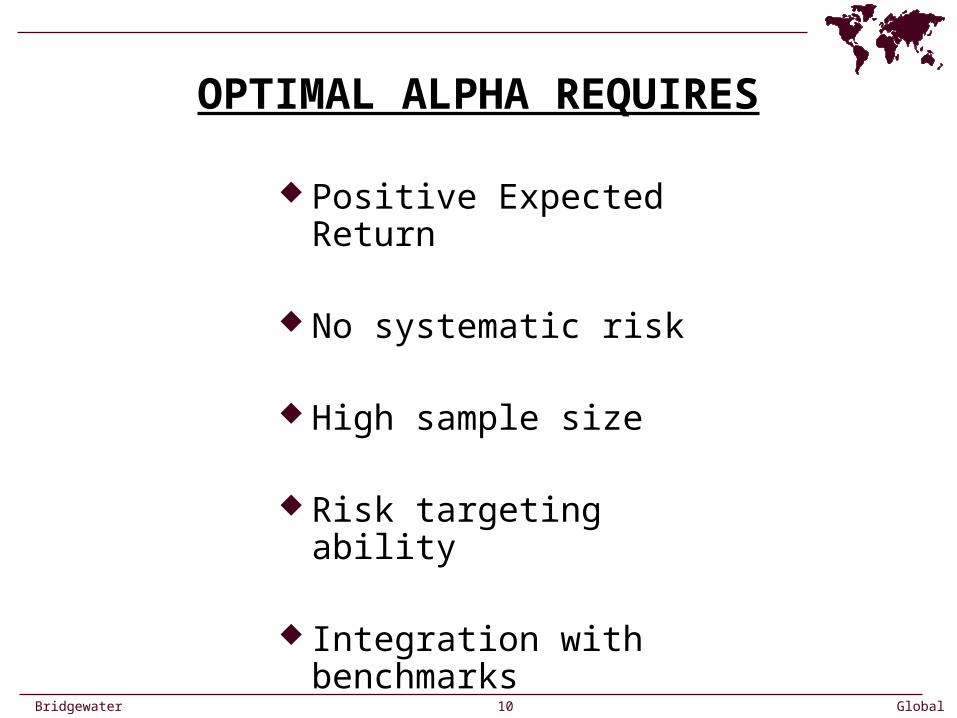

OPTIMAL ALPHA REQUIRES

Positive Expected Return

No systematic risk

High sample size

Risk targeting ability

Integration with benchmarks

11 Bridgewater 11 Global Investment Management

Hedge Funds: Alpha or Beta?

12 Bridgewater 12 Global Investment Management

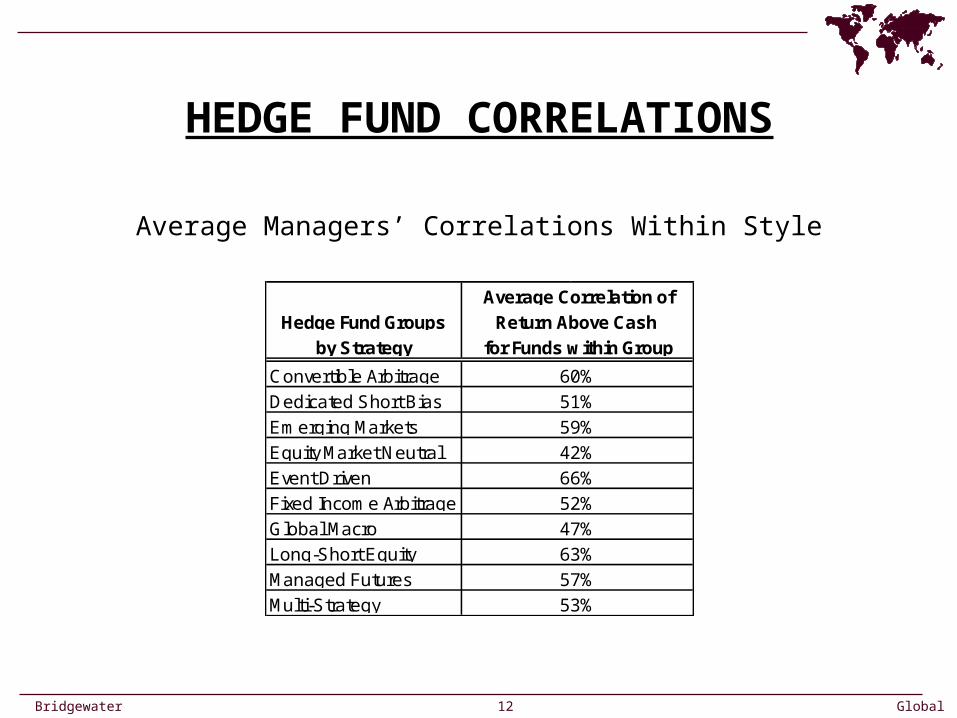

HEDGE FUND CORRELATIONS

Long-Short Equity

Managed Futures

Multi-Strategy

63%

57%

53%

Convertible Arbitrage

Dedicated Short Bias

Emerging Markets

Equity Market Neutral

Event Driven

Fixed Income Arbitrage

Global Macro

42%

66%

52%

47%

60%

51%

59%

Hedge Fund Groups

by Strategy

Average Correlation of

Return Above Cash

for Funds within Group

Average Managers’ Correlations Within Style

13 Bridgewater 13 Global Investment Management

BETAS IN HEDGE FUNDSFixed Income Arbitrage

-15%

-10%

-5%

0%

5%

10%

15%

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04

-25%

0%

25%

50%

75%

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04

Rolling 6-Month Excess Returns

Cumulative Excess Return

Correlation: 77%

Fixed Income Arbitrage Strategy Hedge Funds BW Simple Fixed Income Arbitrage Replication

14 Bridgewater 14 Global Investment Management

BETAS IN HEDGE FUNDSMerger Arbitrage

-15%

-10%

-5%

0%

5%

10%

15%

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04

-20%

0%

20%

40%

60%

80%

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04

Rolling 6-Month Excess Returns

Cumulative Excess Return

Correlation:56%

Merger Arbitrage Strategy Hedge Funds BW Simple Merger Arbitrage Replication

15 Bridgewater 15 Global Investment Management

BETAS IN HEDGE FUNDSEmerging Markets

-50%

-30%

-10%

10%

30%

50%

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04

-50%

-25%

0%

25%

50%

75%

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04

Rolling 6-Month Excess Returns

Cumulative Excess Return

Correlation:79%

Emerging Markets Strategy Hedge Funds BW Emerging Markets Strategy Replication

16 Bridgewater 16 Global Investment Management

BETAS IN HEDGE FUNDS

-50%

-30%

-10%

10%

30%

50%

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04

-50%-25%

0%25%50%75%

100%125%

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04

Rolling 6-Month Excess Returns

Cumulative Excess Return

Managed Futures

Correlation since Jan. 1999: 90%

Managed Futures Strategy Hedge Funds BW Simple Managed Futures Strategy Replication

17 Bridgewater 17 Global Investment Management

APPLYING HEDGE FUNDS

Are you getting alpha or beta?

Diversify.

Allocate based on alpha/beta targets.

Overlay HF alpha onto optimal beta.

18 Bridgewater 18 Global Investment Management

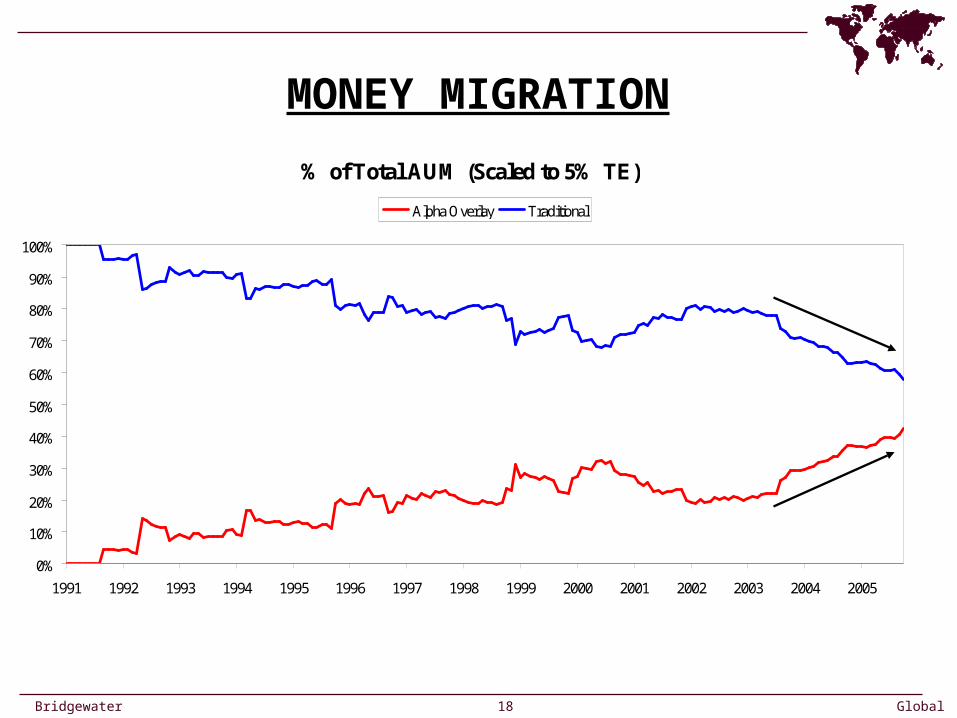

MONEY MIGRATION

% of Total AUM (Scaled to 5% TE)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Alpha Overlay Traditional

19 Bridgewater 19 Global Investment Management

MANAGER MIGRATION Traditional Fund Mangers Who Switched to HF/Alpha Overlay:

1. Jack Meyer Harvard Mgt Alpha Overlay2. Brian Posner Warburg Pincus Hygrove Partners3. Michael DiCarlo John Hancock DFS Advisors HF4. Leon Cooperman Goldman Omega HF5. Jeffrey Vinik Fidelity Vinik Asset Mgmt6. Rob Donahue Solomon Brothers Own fund7. Greg Jackson Oakmark Global Blum Capital HF8. David Glancy Fidelity Own fund9. Peter Trapp Needham Own fund10. Warren Lammert Janus Granite Point Capital11. Nicholas Tiller Fidelity Hedge fund12. Chirstopher Zepf Fidelity Hedge fund13. Dan Szemis Merrill Lynch Hedge fund14. Gary Schlarbaum Morgan Stanley Schlarbaum Capital

20 Bridgewater 20 Global Investment Management

Global Macro Funds

Global Macro

WorldInterest Rates

OutrightDuration

RelativeInterest Rates

RelativeCountryDuration

(diffs)

WorldEquity Prices

OutrightEquity

CurrencyForwards

Currency

RelativeReal Yields

RelativeCountryInflationIndexedBonds

RelativeEquity Prices

RelativeCountry &

SectorEquity

CommoditiesExposure

CommodityPrices

Nominal vs.

Inflation-IndexedBonds

BreakevenInflation Rates

EMD CreditSpreads

DevelopedBonds

vs.Emerging

MarketDebt

Process Example:

• Global macro managers take views on a variety of asset classes (e.g., equities, fixed income, currencies, commodities, etc.) by studying cause-effect relationships between macro economic variables and assessing how these are being (mis)priced in markets

• Example of macro economic variables: growth, inflation, central bank policy (e.g., intervention), political events, balance of payments, capital flows

• The implementation of these views takes many different shapes and forms:

• Systematic – cause-effect are studied and programmed into a logical code

• Discretionary – views are typically implemented through directional and concentrated bets

21 Bridgewater 21 Global Investment Management

Fixed Income Arbitrage

• Fixed Income Arbitrage managers are trying to capture spreads and positive carry in various forms, from simple strategies to more complex ones:

Emerging market credit spread - the managers try to time exposure to EMD spreads (duration hedged spread against US treasury), with bias towards being long the spread Mortgage-backed securities - similar to EMD spreads, the managers are biased

towards capturing the spread between MBS/ABS/CMBS and US treasuries by applying models for calculating prepayment risk (the option embedded in MBS). They tend to take the exposure in the less liquid/traded CMO trenches were they think mis-pricing of the prepayment option exists Volatility trading - the managers take views on volatility and skews and are biased towards being short options and collecting the difference between implied and actual volatility Carry/yield curve trades - try to capture positive carry (the difference between cash and longer-term rates) and implement views on the shape of the yield curve applying interest-rate models. These views are applied to the short-end of the curve (Euro$) and the long-end (Bonds) Currency - managers take some active views on currencies, primarily based on

interest rate diffs between countries