. WAGES Hourly pay Anything over 40 hours must be paid overtime (time and a half) SALARIES Annual...

13

Your Money and the Bank UNIT VII – Personal Financial Literacy

-

Upload

dwight-newton -

Category

Documents

-

view

226 -

download

7

Transcript of . WAGES Hourly pay Anything over 40 hours must be paid overtime (time and a half) SALARIES Annual...

Your Money and the Bank

UNIT VII – Personal Financial Literacy

Your PayWAGES

Hourly pay Anything over

40 hours must be paid overtime (time and a half)

SALARIES Annual pay Get paid the

same regardless of how many hours you work

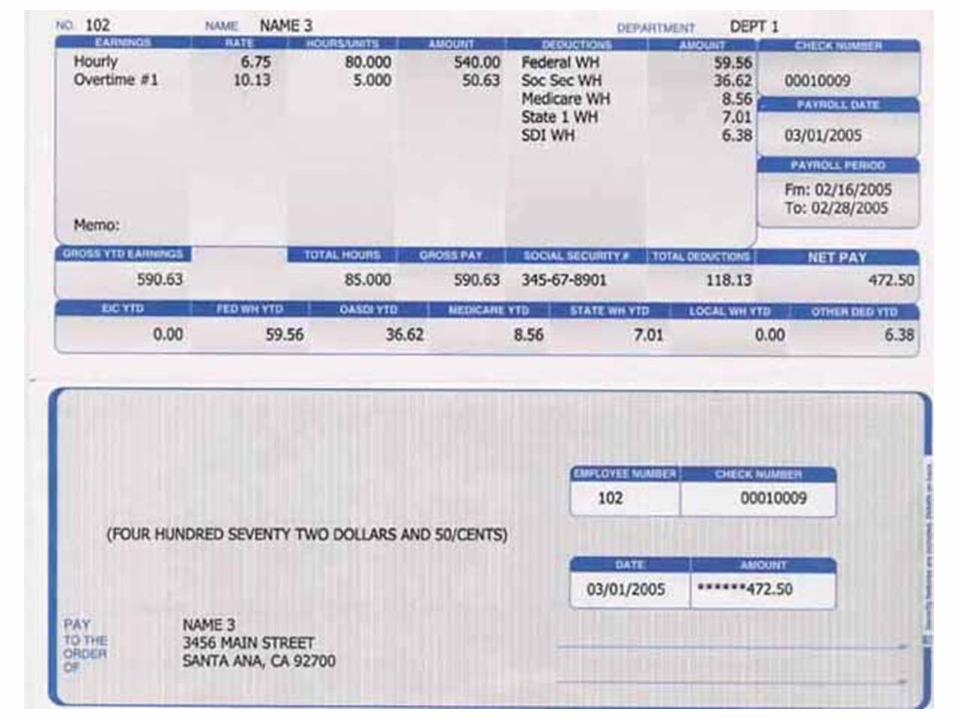

Your PayGROSS PAY

How much you make BEFORE taxes and other deductions are taken out

NET PAY How much you

make AFTER taxes and other deductions are taken out

Mandatory Deductions

Deduction

What do you get? Who pays?

Federal Income TaxState Income TaxFICA: Social SecurityFICA: Medicare

Pays for services provided by federal government

Pays for services provided by state government (not all state have, but NC does)

Provides for old-age, survivors, and disability insurance

Provides hospital insurance for the elderly

Employee; Amount taken is based on pay and W-4

Employee and Employer

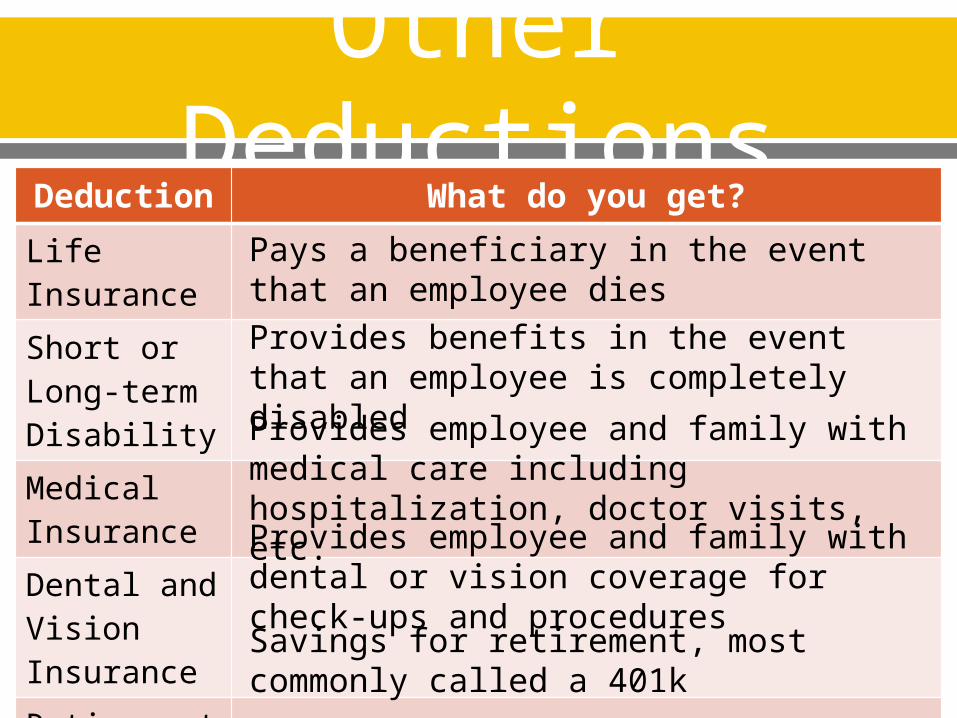

Other Deductions

Deduction What do you get?

Life Insurance

Short or Long-term Disability

Medical Insurance

Dental and Vision Insurance

Retirement Savings Plan

Pays a beneficiary in the event that an employee diesProvides benefits in the event that an employee is completely disabled

Provides employee and family with medical care including hospitalization, doctor visits, etc.Provides employee and family with dental or vision coverage for check-ups and proceduresSavings for retirement, most commonly called a 401k

Where should you put your money?

Financial Institution Description

Commercial Bank

Credit Union

Savings & Loan AssociationBrokerage Firm

Typical bank that offers checking, savings, and credit accounts – ex: Wells FargoMember owned cooperative, has same type of accounts as commercial but usually with better rates – ex: SECU

Today offer most types of accounts but specialize in saving and mortgage loansSpecialize in buying and selling stocks.

Deposit Services Checking Account

o Used for daily transactions, money flows in and out often

Savings Accounto Used for saving moneyo Money can be withdrawn anytimeo Interest is given to increase money in account

CDs (Certificate of Deposits)o aka – Time Deposito Money saved for a certain period of timeo Receives a higher interest rate

Managing Deposits and

Spending Making a Deposito To make a deposit into your checking or savings

account you must fill out a deposit slip

PRACTICE: Deposit check #123 for $300 and receive $75 back in cash.

Managing Deposits and

Spending Withdrawing Moneyo Can be done in person at the bank with a withdrawal

form or at an ATM

PRACTICE: Withdrawal $100 from account number 001336413

Managing Deposits and

Spending Spending Moneyo Today this can usually be done by using a debit card

attached to the accounto Checks can also be written, these are mostly used for

payments to people or for bills

PRACTICE: Write a check for $125.00 to

the U.S. Department of

Education

Managing Deposits and

Spending Keeping Track of Your Accounto It is INCREDIBLY important that you keep up with

the transactions (deposits, withdrawals, and spending) of your checking account

o Banks today offer online banking to help you with this but this is NOT always reliable because transactions can take a while to process so your account may have more/less than the online banking says

o Due to this, it is important to ALWAYS keep a paper record of transactions in your check register

o Each month you will receive a statement of the previous month’s activities. ALWAYS balance your checkbook and look for any mistakes you may have made.

Managing Deposits and

Spending Starting balance: $649.52

Deposit on 12/2: $54.96

ATM Withdrawal on 12/4: $20.00

Debit Card Purchase on 12/5: Food Lion for $ 13.75

Bill Payment on 12/9: Check #149 to Time Warner Cable for $183.15