: TOMM Committee Kangaroo Island...6 Figure 24: Visitors who were very satisfied with their...

117

Prepared for: TOMM Committee Kangaroo Island CB Contact: Ben Nitschke, Account Manager Phone: (08) 8373 3822 Email: [email protected] Issue Date: 3 September, 2018 Project number: TOMM0004 www.colmarbrunton.com

Transcript of : TOMM Committee Kangaroo Island...6 Figure 24: Visitors who were very satisfied with their...

Prepared for: TOMM Committee Kangaroo Island

CB Contact: Ben Nitschke, Account Manager

Phone: (08) 8373 3822

Email: [email protected]

Issue Date: 3 September, 2018

Project number: TOMM0004

www.colmarbrunton.com

2

Contents.

Addressing the TOMM Indicators ......................................................................... 9

Introduction ........................................................................................................... 15

Background .................................................................................................................................................... 15

Research Objectives ..................................................................................................................................... 16

Research Methodology ................................................................................................................................. 16

Weighting ........................................................................................................................................................ 16

Questionnaire Design ................................................................................................................................... 17

Restructuring & Reanalysis of Previous Wave Data ............................................................................... 17

Confidence Intervals ..................................................................................................................................... 17

Data cleaning ................................................................................................................................................. 18

Limitations of the Research ......................................................................................................................... 18

Recommendation of Kangaroo Island to others as a holiday destination (EC1e) ............................ 25

Average expenditure per visit (EC1f) ........................................................................................................ 26

Annual number of visitors (EC1g).............................................................................................................. 27

Satisfaction with customer service received (EC2c) .............................................................................. 28

Satisfaction with professionalism of tourism operators (EC2d) ........................................................... 29

Compliments and complaints (EC2e) ........................................................................................................ 30

Average spend per night over $200 (EC3c) ............................................................................................ 31

Viewed wildlife in natural environment (EX1b) ....................................................................................... 34

Experienced scenic variety without crowds (EX1c) ................................................................................ 35

Experienced cultural heritage and history of settlement (EX1d) ......................................................... 36

Experienced spectacular scenery and coastal landscapes (EX1e) ....................................................... 37

Experienced areas of untouched natural beauty (EX1f) ........................................................................ 38

Experienced farming and rural landscapes (EX1g) ................................................................................ 39

Experienced local Kangaroo Island produce (EX1h) .............................................................................. 40

Kangaroo Island offers one of Australia’s top three nature & wildlife experiences (EX1i) ............. 42

Kangaroo Island has a friendly local community (EX1j) ....................................................................... 43

Agreement with positioning statement (EX1k) ....................................................................................... 44

Matching expectation set by marketing materials (EX1l) ..................................................................... 45

Satisfaction with overall experience (EX1m) ........................................................................................... 46

Seeing native wildlife in its natural environment (EX2a) ...................................................................... 47

Opportunity to learn more about the Island’s natural environment (EX2b) ..................................... 48

Opportunity to learn more about the Island’s history (EX2c) .............................................................. 49

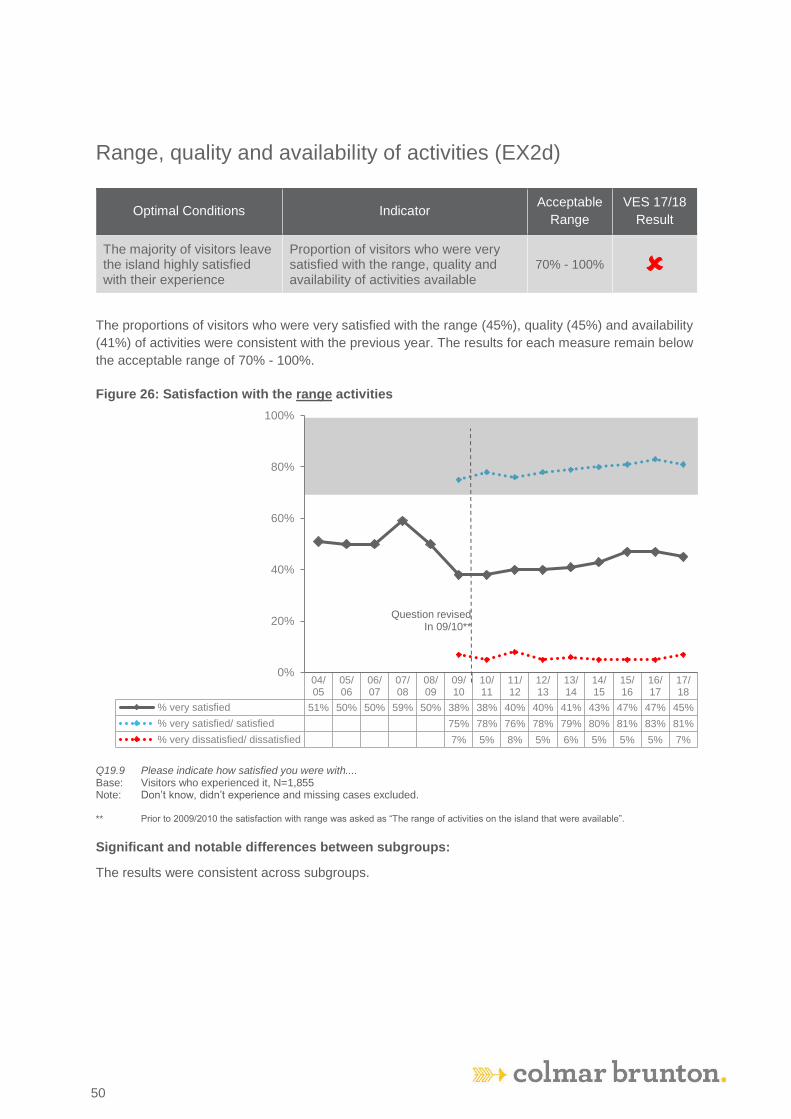

Range, quality and availability of activities (EX2d) ................................................................................ 50

3

Quality of accommodation (EX2e) ............................................................................................................. 53

Range, quality and availability of Kangaroo Island produce (EX2f) .................................................... 54

Quality of public tourism infrastructure (EX2h) ...................................................................................... 57

Recommendation of Kangaroo Island as holiday destination (EX2i) .................................................. 63

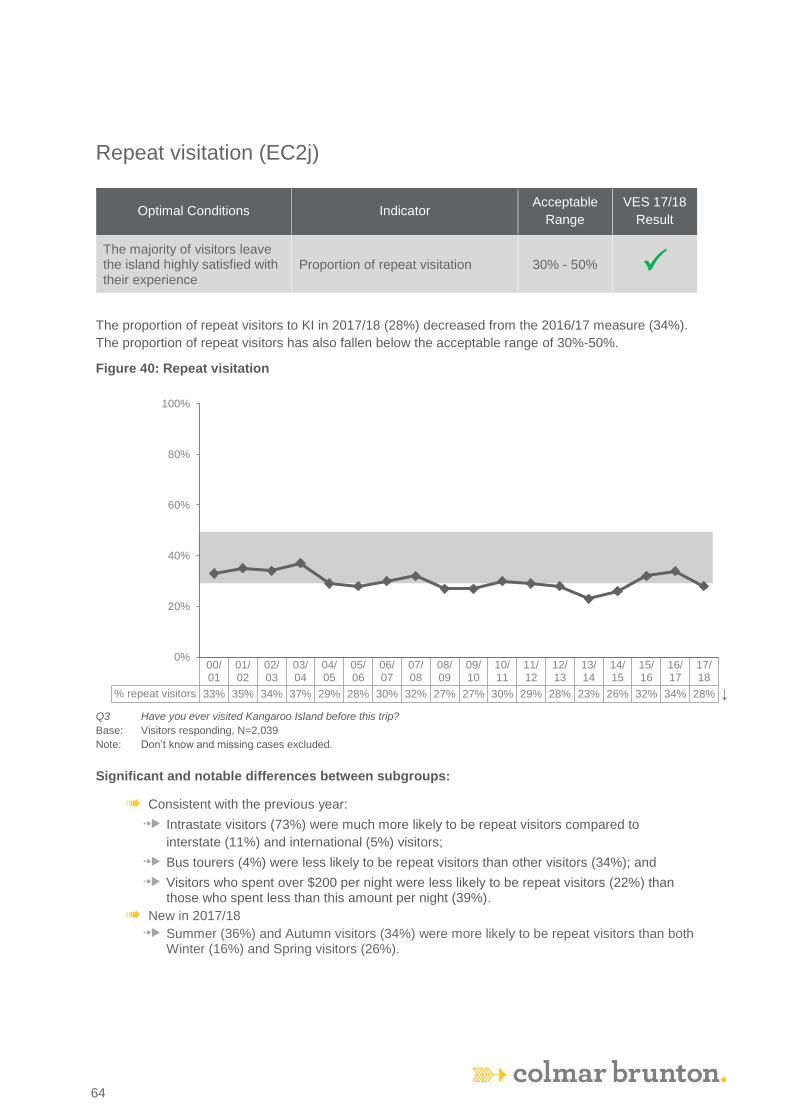

Repeat visitation (EC2j) ............................................................................................................................... 64

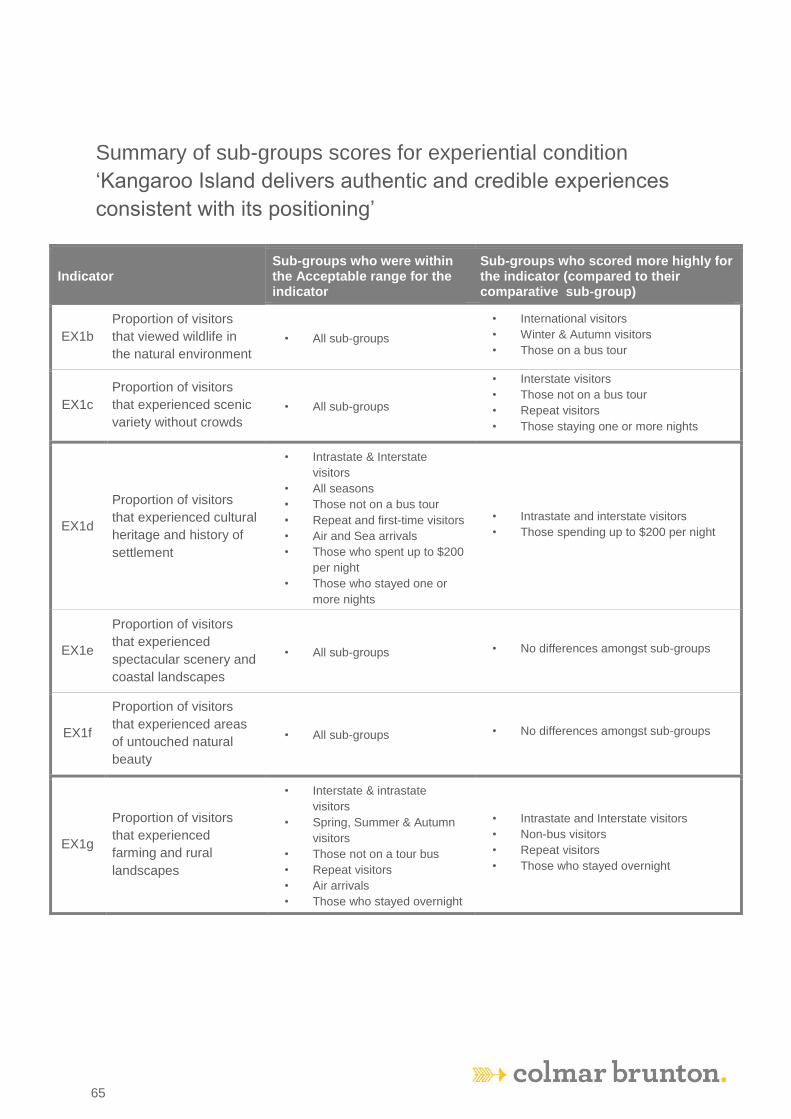

Summary of sub-groups scores for experiential condition ‘Kangaroo Island delivers authentic

and credible experiences consistent with its positioning’...................................................................... 65

Summary of sub-groups scores for experiential condition ‘Kangaroo Island delivers authentic

and credible experiences consistent with its positioning’ (continued) ............................................... 66

Summary of sub-groups scores for experiential condition ‘The majority of visitors leave the

Island highly satisfied with their experience’ .......................................................................................... 67

Summary of sub-groups scores for experiential condition ‘The majority of visitors leave the

Island highly satisfied with their experience’ (continued) .................................................................... 69

Visits to natural areas occurring on managed sites (EN2b) ................................................................. 71

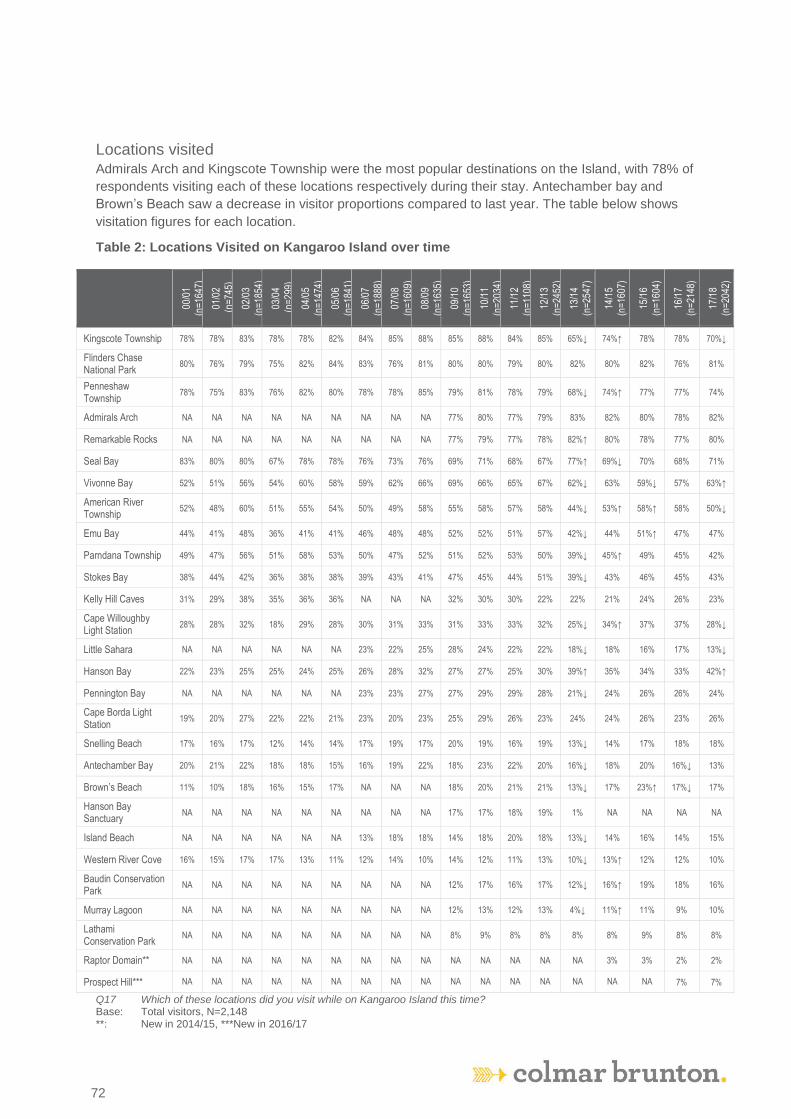

Locations visited ............................................................................................................................................ 72

Awareness of quarantine regulations prior to arriving (EN2e) ............................................................ 73

Visitor Profile ......................................................................................................... 78

Visitor Origin .................................................................................................................................................. 78

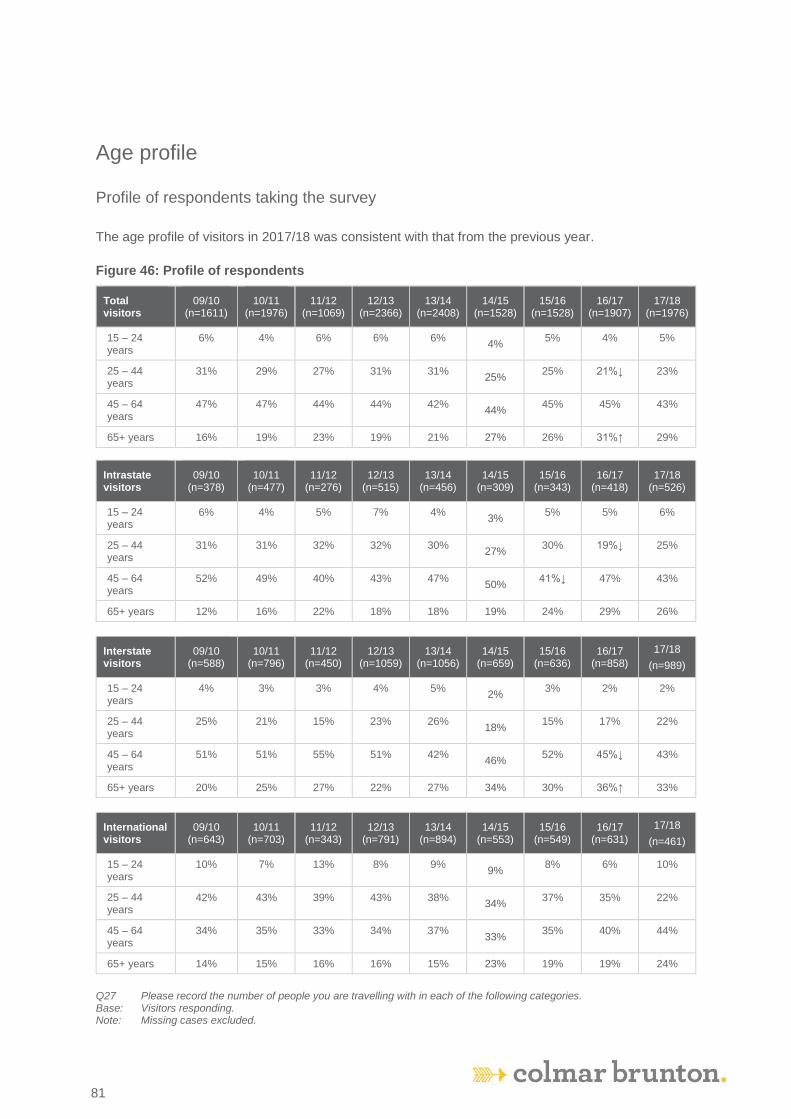

Age profile ...................................................................................................................................................... 81

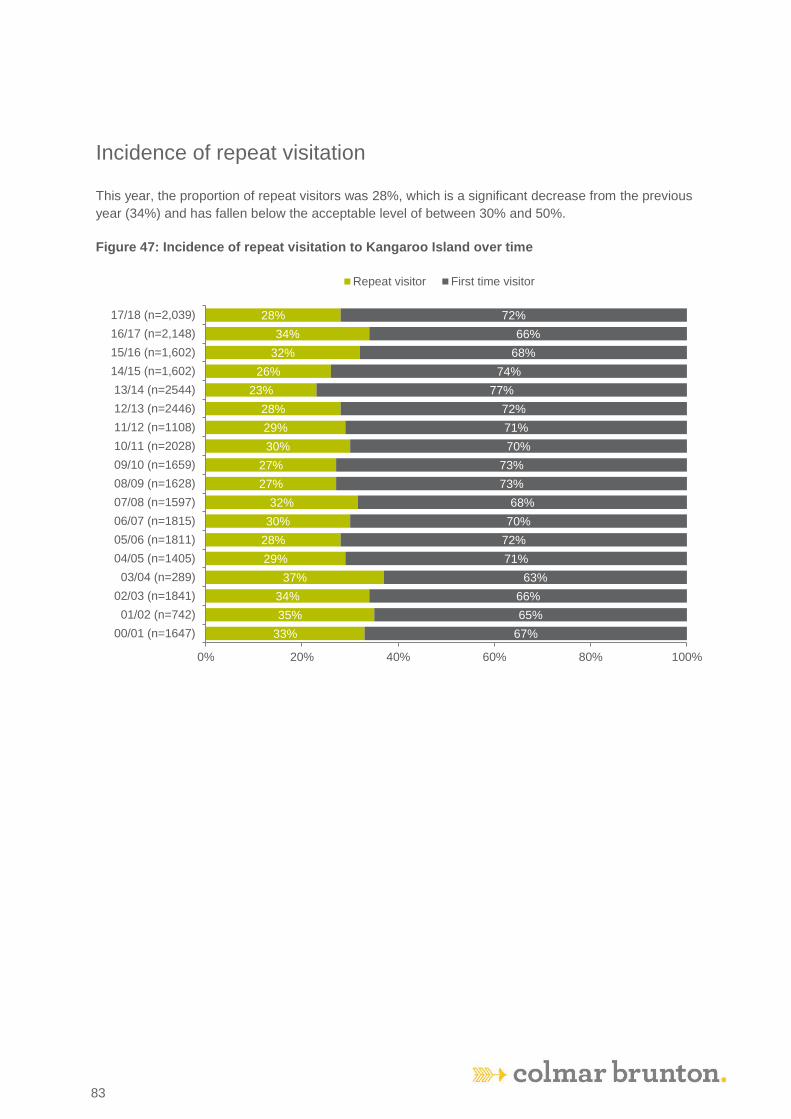

Incidence of repeat visitation ..................................................................................................................... 83

Travel party .................................................................................................................................................... 85

Types of Accommodation ............................................................................................................................ 87

Satisfaction with accommodation .............................................................................................................. 89

Credible vs. Experienced Attributes & Attractions .................................................................................. 91

Reasons for Dissatisfaction ......................................................................................................................... 93

Suggestions for Improvement .................................................................................................................... 94

Exploration of those dissatisfied overall ................................................................................................... 95

Seasonal variances ............................................................................................... 98

Proportion of visitors by season ................................................................................................................. 98

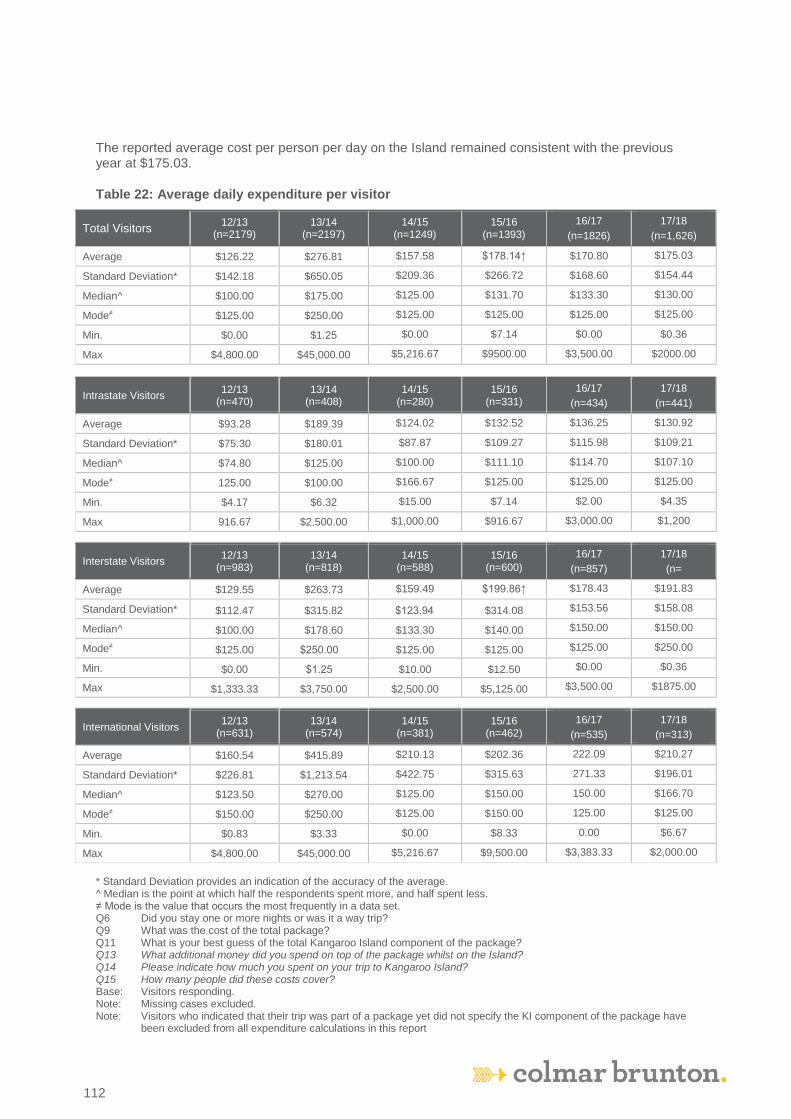

Appendix A: Visitor Expenditure ...................................................................... 109

Incidence of Package Bookings ................................................................................................................ 109

Expenditure per visitor ............................................................................................................................... 111

Appendix B: VES Questionnaire ....................................................................... 113

4

Index of Tables

Table 1: Margin of Error per number of responses 17

Table 2: Locations Visited on Kangaroo Island over time 72

Table 3: Awareness of quarantine regulations by first time and repeat visitors this wave 76

Table 4: Interstate Visitor Origin over time 79

Table 5: International Visitor Origin over Time 80

Table 6: Age profile of visitors (includes entire travel party) 82

Table 7: Repeat Visitation to Kangaroo Island by Visitor Origin over time 84

Table 8: Travel party by visitor origin over time 86

Table 9: Accommodation used over time 87

Table 10: Accommodation Used by Visitor Origin 88

Table 11: Satisfaction with accommodation types across waves 89

Table 12: Satisfaction with accommodation types this wave 90

Table 13: Credible vs. experienced attributes and attractions 91

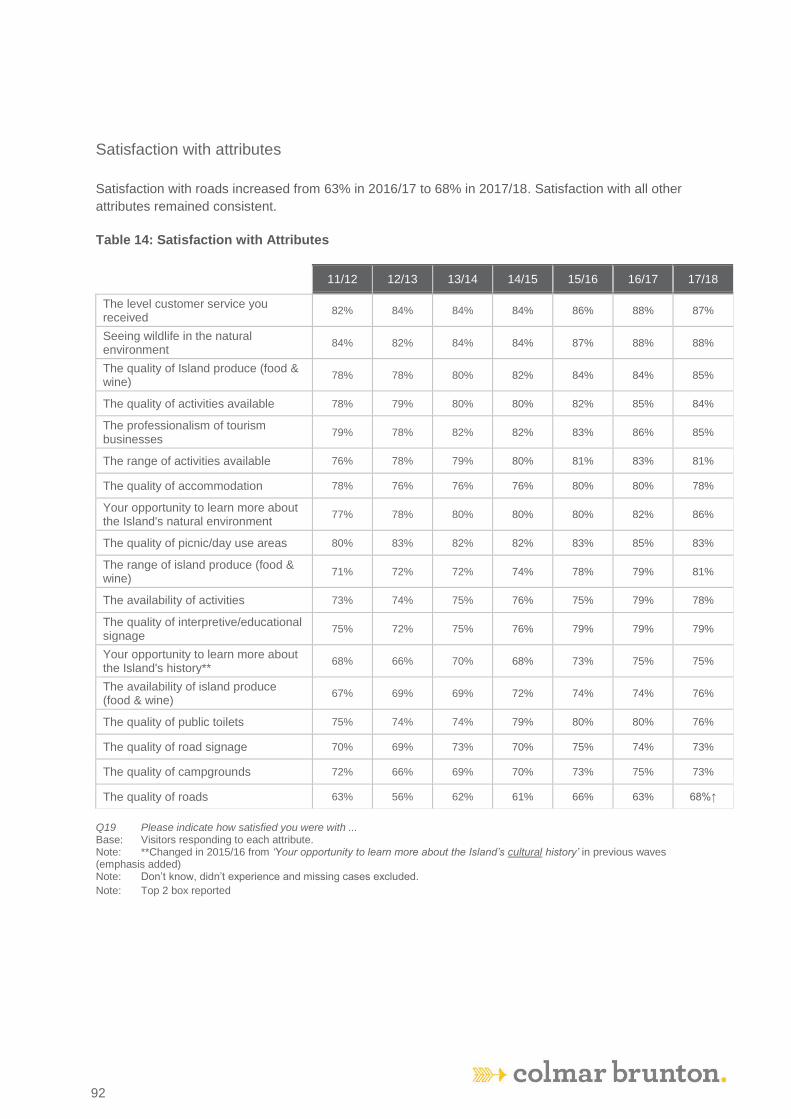

Table 14: Satisfaction with Attributes 92

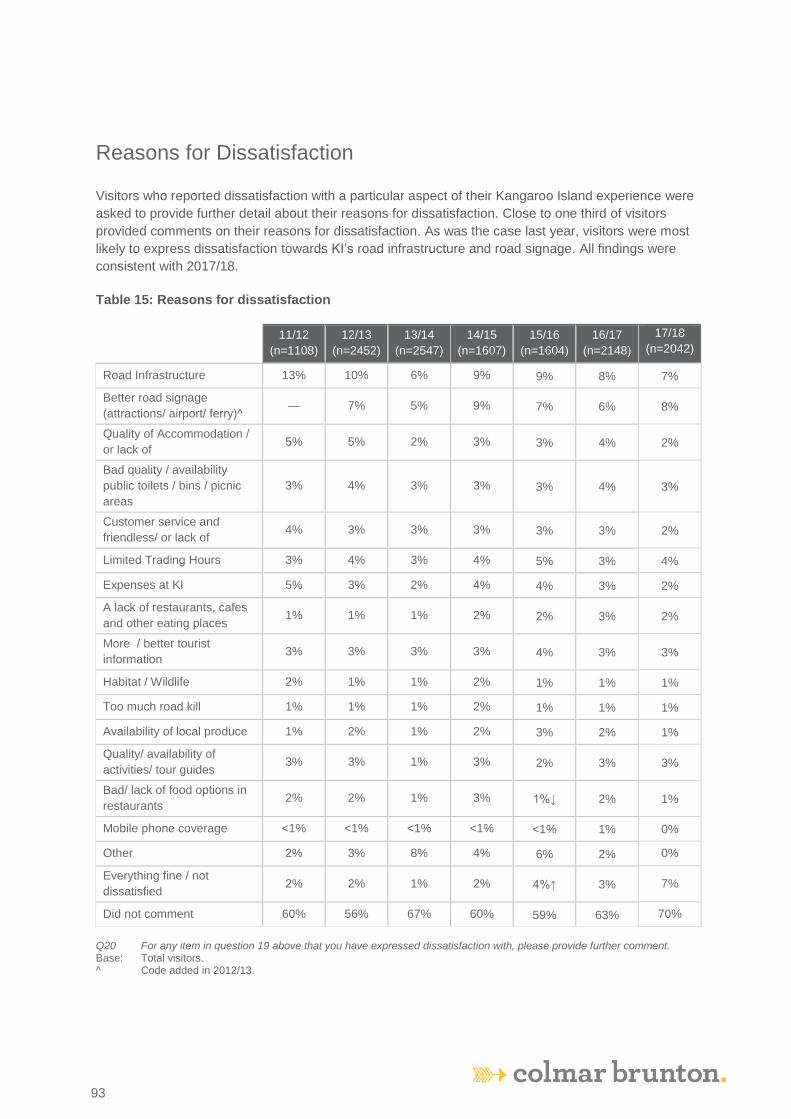

Table 15: Reasons for dissatisfaction 93

Table 16: Suggestions for improvement 94

Table 17: Who was dissatisfied? 95

Table 18: What were they dissatisfied with? 96

Table 19: Reasons for dissatisfaction (Q20) 97

Table 20: Booking Type by Visitor Origin 110

Table 21: Average expenditure per visitor 111

Table 22: Average daily expenditure per visitor 112

5

Index of Figures

Figure 1: Length of stay over time 22

Figure 2: Average Number of Nights over Time 23

Figure 3: Average number of nights by visitor origin over time 24

Figure 4: Willingness to recommend 25

Figure 5: Increase in average annual total expenditure per person per visit 26

Figure 6: Increase in annual number of visitors 27

Figure 7: Satisfaction with customer service received 28

Figure 8: Satisfaction with professionalism of tourism operators 29

Figure 9: Number of compliments and complaints received 30

Figure 10: Average spend per night over $200 31

Figure 11: Visitors that viewed Australia’s wildlife in natural surroundings 34

Figure 12: Visitors that experienced scenic variety without crowds 35

Figure 13: Visitors that experienced cultural heritage and history of settlement 36

Figure 14: Visitors that experienced spectacular scenery and coastal landscapes 37

Figure 15: Visitors that experienced areas of untouched natural beauty 38

Figure 16: Visitors that experienced farming and rural landscapes 39

Figure 17: Visitors that experienced local Kangaroo Island produce 40

Figure 18: Visitors that experienced Kangaroo Island as one of Australia’s top three nature &

wildlife experiences 42

Figure 19: Visitors that experienced a friendly local community on Kangaroo Island 43

Figure 20: Visitors who agree that Kangaroo Island is a wild and welcoming destination 44

Figure 21: Visitors stating that their experience matched or exceeded the expectation set by

marketing materials 45

Figure 22: Visitors who were very satisfied** with their overall experience on Kangaroo

Island 46

Figure 23: Visitors who were satisfied with seeing native wildlife in its natural environment 47

6

Figure 24: Visitors who were very satisfied with their opportunity to learn more about the

Island’s natural environment 48

Figure 25: Satisfaction with opportunity to learn more about the Island’s history 49

Figure 26: Satisfaction with the range activities 50

Figure 27: Satisfaction with the quality of activities 51

Figure 28: Satisfaction with the availability of activities 52

Figure 29: Satisfaction with quality of accommodation 53

Figure 30: Satisfaction with the range of local Kangaroo Island produce 54

Figure 31: Satisfaction with the quality of local Kangaroo Island produce 55

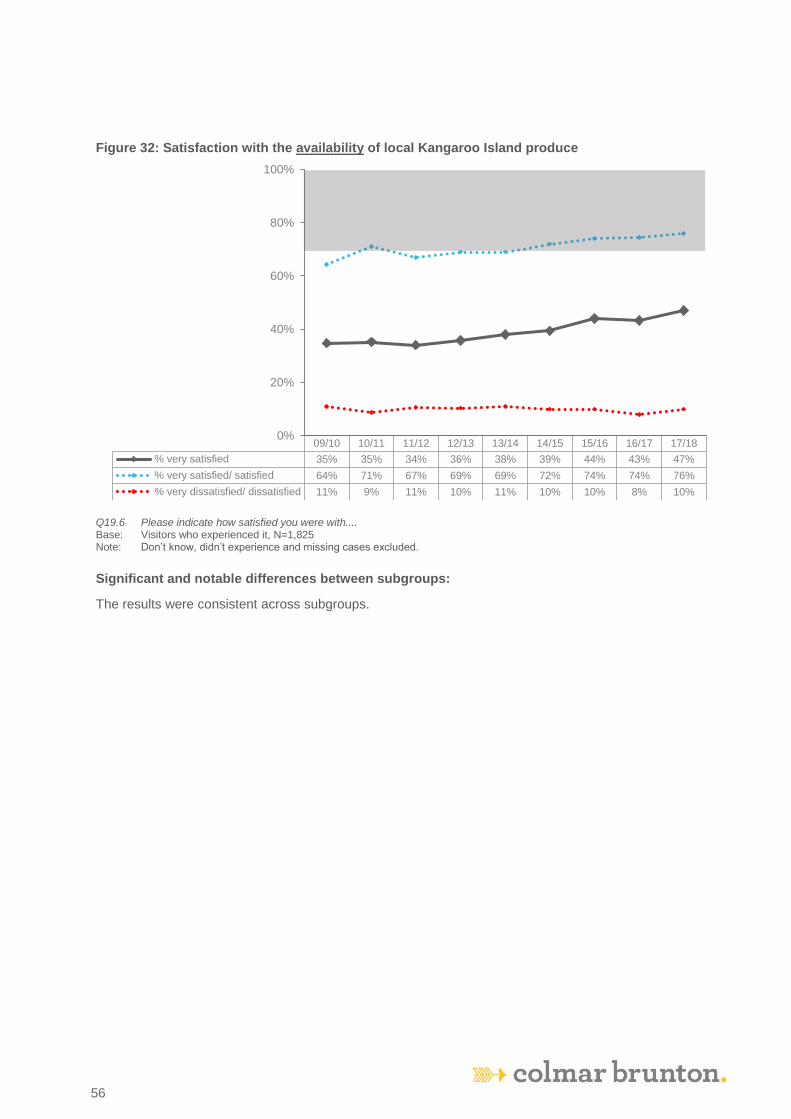

Figure 32: Satisfaction with the availability of local Kangaroo Island produce 56

Figure 33: Satisfaction with the quality of picnic & day use areas 57

Figure 34: Satisfaction with the quality of interpretive & educational signage 58

Figure 35: Satisfaction with the quality of public toilets 59

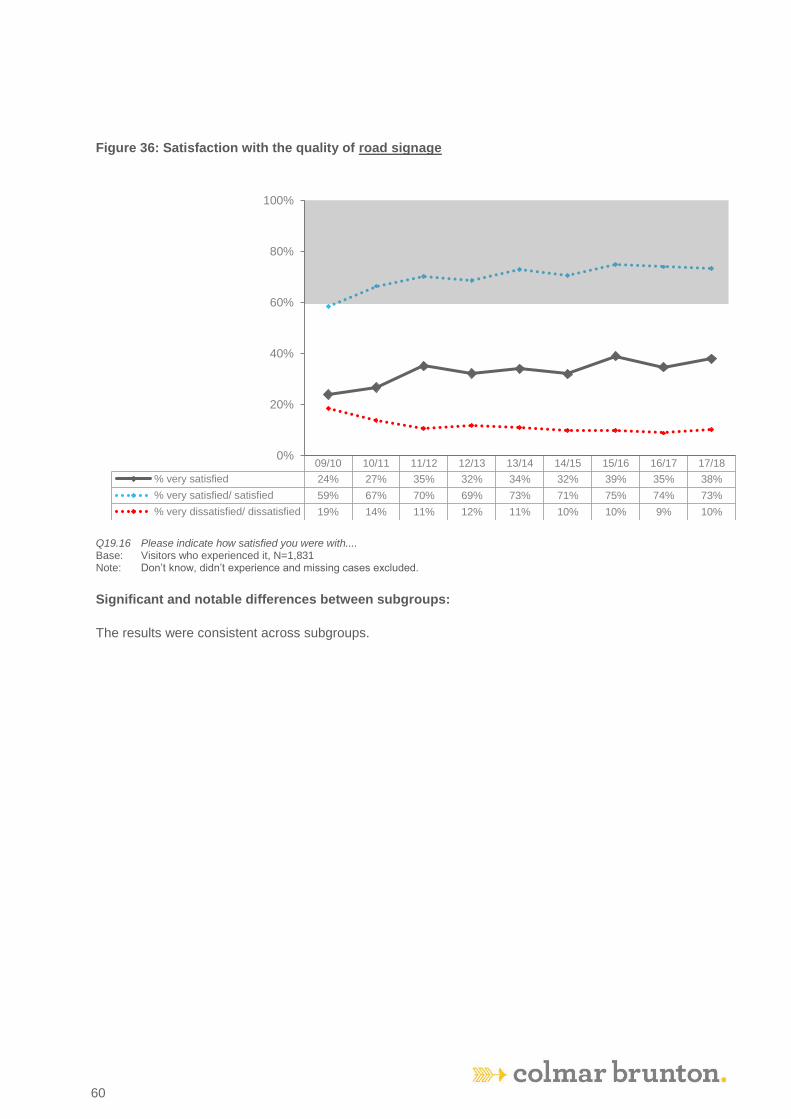

Figure 36: Satisfaction with the quality of road signage 60

Figure 37: Satisfaction with the quality of campgrounds 61

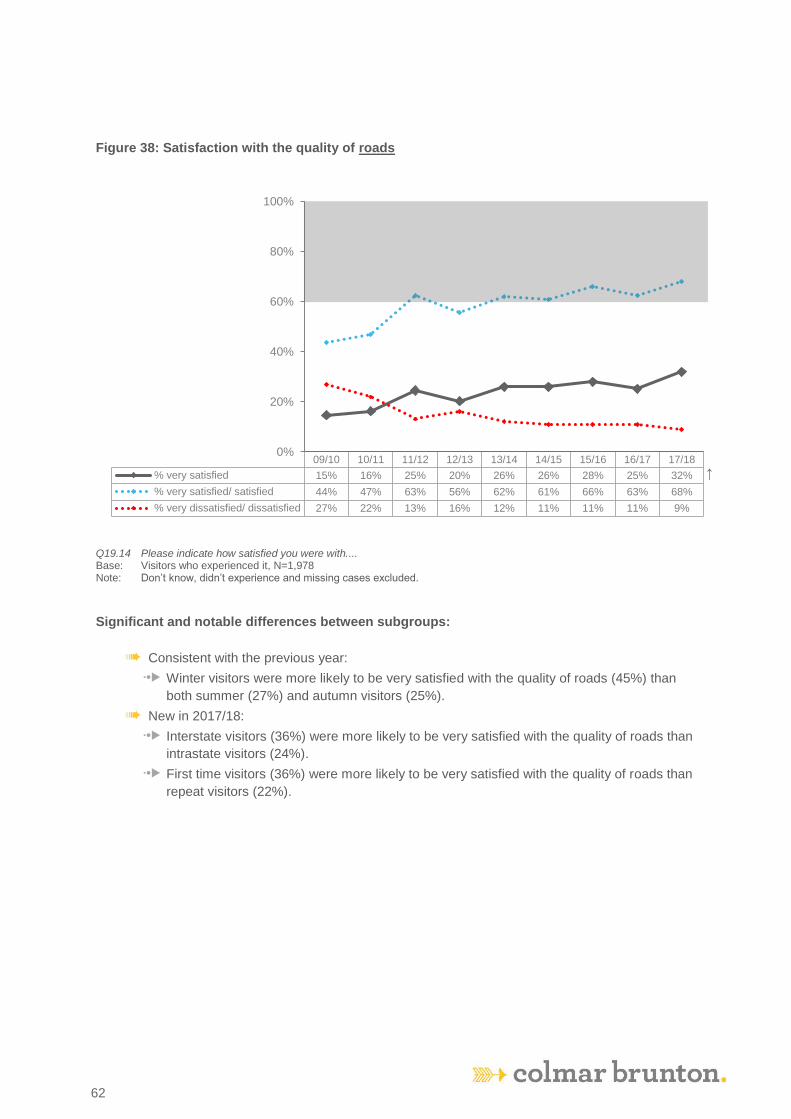

Figure 38: Satisfaction with the quality of roads 62

Figure 39: Willingness to recommend 63

Figure 40: Repeat visitation 64

Figure 41: Proportion of visitations to natural areas occurring on managed sites 71

Figure 42: Awareness of quarantine regulations 73

Figure 43: Awareness of any quarantine regulations by repeat and first time visitors 74

Figure 44: Awareness of Prohibited Items 75

Figure 45: Visitor Origin over time 78

Figure 46: Profile of respondents 81

Figure 47: Incidence of repeat visitation to Kangaroo Island over time 83

Figure 48: Travel party over Time 85

Figure 49: Proportion of visitors by season 98

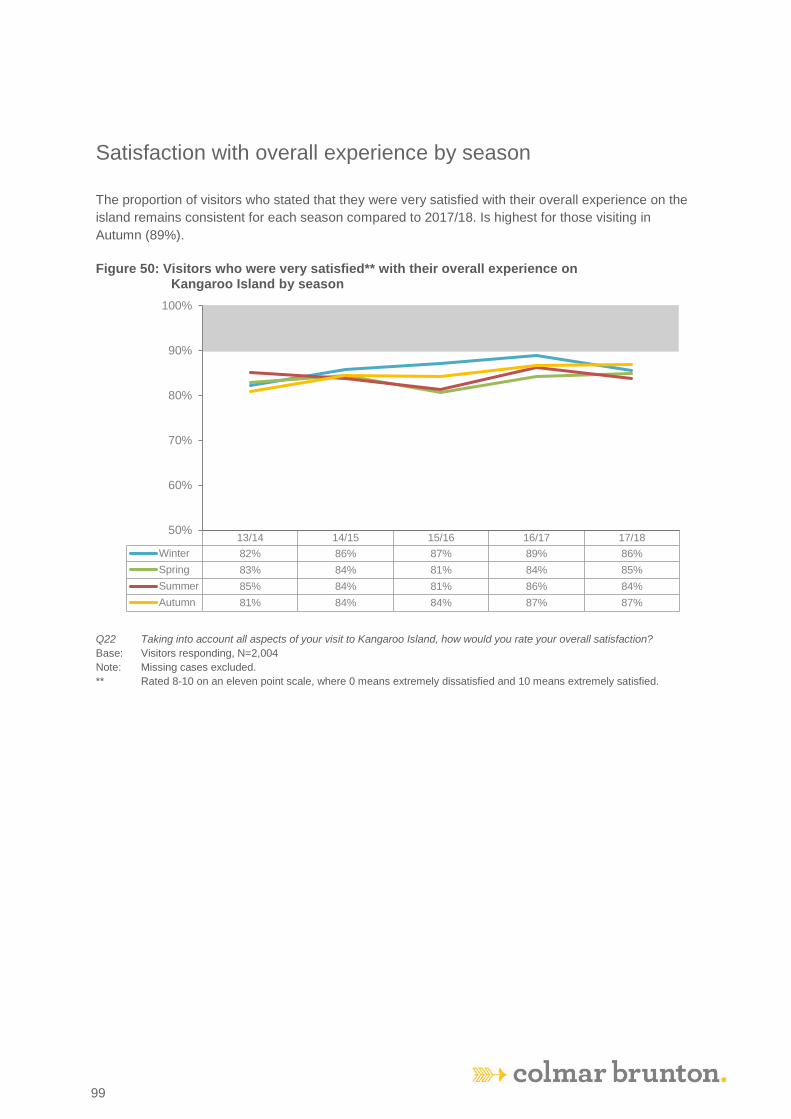

Figure 50: Visitors who were very satisfied** with their overall experience on Kangaroo

Island by season 99

7

Figure 51: Average number of nights stayed by season 100

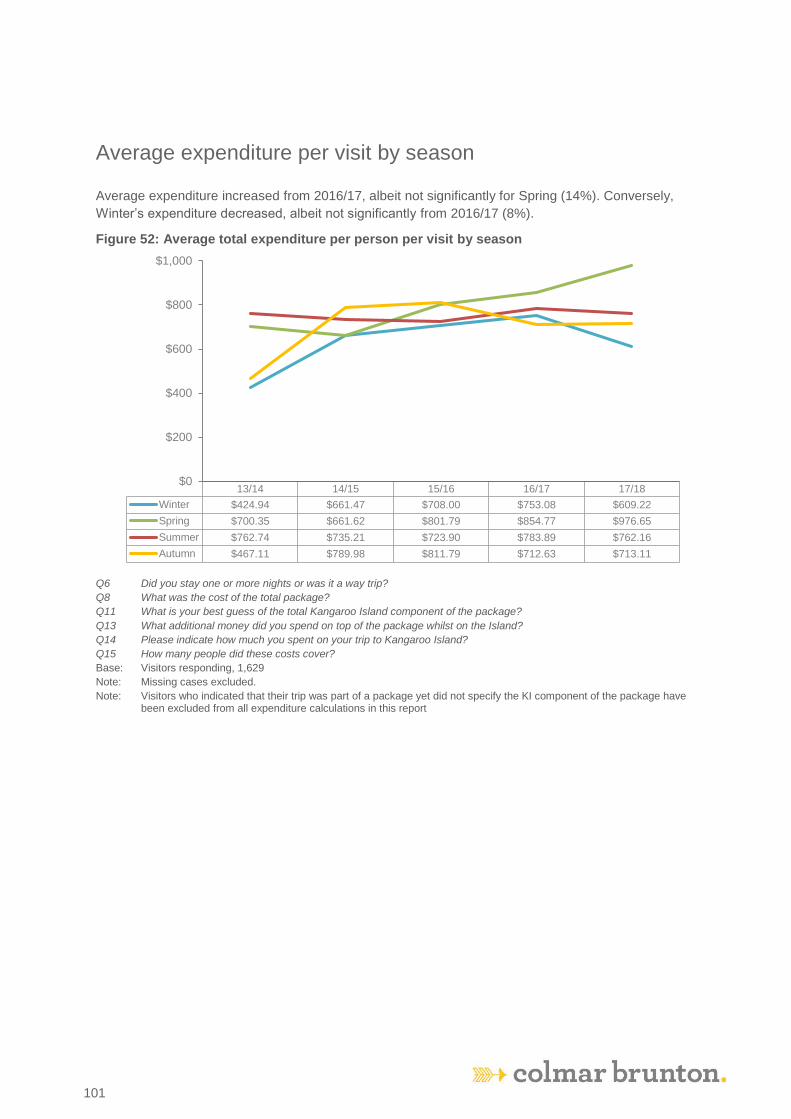

Figure 52: Average total expenditure per person per visit by season 101

Figure 53: Visitors who were very satisfied with customer service received by season 102

Figure 54: Visitors who spent $200+ per night by season 103

Figure 55: Visitors that experienced local Kangaroo Island produce by season 104

Figure 56: Visitors very satisfied with the range of local Kangaroo Island produce by season

105

Figure 57: Visitors very satisfied with the quality of local Kangaroo Island produce by season

106

Figure 58: Visitors very satisfied with the availability of local Kangaroo Island produce by

season 107

Figure 59: Repeat visitors by season 108

Figure 60: Trip to Kangaroo Island part of travel package 109

8

Disclaimer

TOMM does not represent or warrant that this information is correct, complete or suitable for the

purpose for which you wish to use it. By using this information, you acknowledge and agree to

release and indemnify the TOMM for any loss or damage that you may suffer as a result of your

reliance on this information.

9

Addressing the TOMM Indicators

At the core of TOMM is a practical set of indicators that monitor the status of tourism on Kangaroo

Island. A review of indicators was completed in the 2015/16 financial year to improve the monitoring

of the impact of tourism on Kangaroo Island. The indicators that relate to the visitor experience have

been measured through the annual Visitor Exit Survey since 2002.

This document outlines the findings of the 2017/18 Visitor Exit Survey (VES).

Summary of TOMM Indicators

Summary of Economic Indicators

Optimal Conditions Ref Indicators Acceptable Range VES 17/18 Results

Tourism optimises

economic benefits for

Kangaroo Island

EC1d Annual average number of nights stayed 4-7 nights 4.6 nights

EC1e Proportion of visitors that would recommend Kangaroo Island to others as a holiday destination

90% - 100% 95%

EC1f Average annual total expenditure per visit 5% - 10%↑ $722.70

[7.3% decrease]

EC1g Annual number of visitors to Kangaroo Island 0-20%*↑ 5.7%

Tourism operators excel in

their business

professionalism

EC2c Proportion of visitors that are very satisfied with the level of customer service they receive

65% - 100% 60%

EC2d Proportion of customers that are highly satisfied with the professionalism of tourism operators

65% - 100% 55%

EC2e The number of compliments and complaints received from visitors

↑ in positive comments

↓ in negative comments

↑ in positive comments

↓ in negative comments Island attracts Kangaroo its

high yield target markets EC3c

Proportion of visitors whose average spend per night exceeds $200

40% - 60% 34%

11

Summary of Experiential Indicators

Optimal Conditions Ref Indicators Acceptable Range VES 17/18 Results

Kangaroo Island delivers

authentic and credible

experiences consistent

with its positioning

EX1a Proportion of visitors that believe they

experienced an authentic wilderness holiday 80% - 100% Question removed in 2013/14

EX1b Proportion of visitors that viewed wildlife in the

natural environment 90% - 100% 97%

EX1c Proportion of visitors that experienced scenic

variety without crowds 90% - 100% 97%

EX1d Proportion of visitors that experienced cultural

heritage and history of settlement 70% - 100% 72%

EX1e Proportion of visitors that experienced

spectacular scenery and coastal landscapes 90% - 100% 99%

EX1f Proportion of visitors that experienced areas of

untouched natural beauty 90% - 100% 97%

EX1g Proportion of visitors that experienced farming

and rural landscapes 90% - 100% 88%

* Acceptable range changed from 0-3% to 0-20% in 2016.

12

Optimal Conditions Ref Indicators Acceptable Range VES 17/18 Results

Kangaroo Island delivers

authentic and credible

experiences consistent

with its positioning

EX1h Proportion of visitors that experienced local

Kangaroo Island produce 80% - 100% 83%

EX1i

Proportion of visitors that believe Kangaroo

Island offers one of Australia’s top three nature

& wildlife experiences

70% - 100% 81%

EX1j Proportion of visitors that believe Kangaroo

Island has a friendly local community 80% - 100% 93%

EX1k

Proportion of visitors who agree that Kangaroo

Island is a wild and welcoming destination, that

will surprise and amaze you, relax your mind,

refresh your spirit and make you feel totally

alive. It provides an opportunity to view and to

discover all the scenic variety of mainland

Australia

70% - 100% 85%

EX1l

Proportion of visitors that state that their

experience matched or exceeded the

expectation set by marketing materials

80% - 100% 94%

EX1m Proportion of visitors very satisfied with their

overall experience on Kangaroo Island 90% - 100% 85%

13

Optimal Conditions Ref Indicators Acceptable Range VES 17/18 Results

The majority of visitors

leave the island highly

satisfied with their

experience

EX2a Proportion of visitors who were very satisfied with seeing native wildlife in its natural environment

70% - 100% 69%

EX2b Proportion of visitors who were very satisfied with their opportunity to learn more about the Island’s natural environment

70% - 100% 49%

EX2c Proportion of visitors who were very satisfied with their opportunity to learn more about the Island’s history

70% - 100% 41%

Ex2d Proportion of visitors who were very satisfied with the range, quality and availability of activities available

70% - 100% 41%-45%

EX2e Proportion of visitors who were very satisfied with the quality of accommodation

70% - 100% 50%

EX2f Proportion of visitors who were very satisfied with the range, quality and availability of Kangaroo Island produce

70% - 100% 47% - 54%

EX2g Proportion of visitors that are very satisfied with the level of customer service they receive

80% - 100% 60%

EX2h

Proportion of visitors that are very satisfied with the quality of public tourism infrastructure (toilets, roads, campgrounds, picnic areas and signage) provided on Kangaroo Island

60% - 100% 32% - 48%

EX2i Proportion of visitors that would recommend Kangaroo Island as a holiday destination to others as a result of their experience

90% - 100% 95%

EX2j Proportion of repeat visitation 30% - 50% 28%

14

Summary of Environmental Indicators

Optimal Conditions Ref Indicators Acceptable Range VES 17/18 Results

Visitor activity has minimal

negative impacts on the

natural environment

EN2b Proportion of visitations to natural areas

occurring on managed sites 70% - 100% 74%

EN2e Proportion of visitors aware of quarantine

regulations prior to arriving on Kangaroo Island 70% - 100% 63%

KI TOMM: Visitor Exit Survey Report 2016-2017

15

15

Introduction

Background

Tourism is a key contributor to economic growth and development on Kangaroo Island, next to

agriculture, with both boosting productivity and providing a source of stable employment for residents.

TOMM (the Tourism Optimisation Management Model) was developed to monitor the effect of tourism

from a variety of perspectives (including environmental, economic, socio-cultural and visitor

experience) in the interests of both residents and visitors. The model is a community-based initiative

responsible for monitoring and managing the long-term sustainability of tourism on the island. The

initiative is overseen by a Management Committee with support and representatives from the

community, industry and Government agencies.

At the core of TOMM is a practical set of indicators that monitor tourism on Kangaroo Island. These

indicators measure changes in the economic, environmental, socio cultural and experiential

environments. A review of indicators was completed in the 2015/16 financial year.

The Visitor Exit Survey (VES) is a critical source of information with respect to measuring and

monitoring the TOMM indicators each year as well as collecting a raft of other information about

tourism on the Island. Trends demonstrated through these indicators are provided to agencies in

order to facilitate strategic planning for Kangaroo Island.

Colmar Brunton Research Services (CBRS) has carried out research with Kangaroo Island visitors as

part of the Tourism Optimisation Management Model (TOMM) monitor for the past fourteen financial

years. The following report details findings from the TOMM Visitor Exit Survey conducted throughout

the 2017/18 period. Where possible, tracking has been performed on questions that have been kept

comparable across the past fourteen years of the Visitor Exit Survey.

KI TOMM: Visitor Exit Survey Report 2016-2017

16

16

Research Objectives

Research Aim

The main aim of this research project is to monitor the effects of tourism on Kangaroo Island.

Specific Research Objectives

The specific objectives of the Visitor Exit Survey are to assess the following:

6 Profiles of origin and seasonality of visitors to the island;

6 Travel behaviour and experiences on the island;

6 Reasons for visiting Kangaroo Island;

6 Expectations and important factors influencing the decision to visit Kangaroo Island;

6 Valued aspects and visitor satisfaction with those aspects;

6 Overall satisfaction with Kangaroo Island experience;

6 Transportation;

6 Expenditure on Kangaroo Island;

6 Awareness of Kangaroo Island’s quarantine regulations; and

6 Demographic profile of visitors.

Research Methodology

The methodology for this project consisted of a self-completion survey, which visitors were able to

pick up at entry and exit points to the Island (airport and ferry departure points) across a full year

period from July 2018 to June 2018. This methodology was consistent with that employed for the last

fourteen Visitor Exit Surveys.

From approximately midway through the 2013/14 data collection period surveys were also distributed

on tour buses on the island in addition to the entry and exit points (airport and ferry departure points).

The aim of this was to increase data collection from day trip visitors.

A prize incentive of $500 worth of local Kangaroo Island produce was employed to increase

respondent participation. On receipt of all completed questionnaires, CBR edited, coded and entered

the data. Questionnaires that had a number of questions incomplete were ignored. Analysis consisted

predominantly of frequencies, cross tabulations and general tables.

Weighting

It was recognised from previous reports that there are significant differences between those visitors

reaching the Island by air and ferry, as well as between bus tour visitors and non-bus-tour visitors.

This year’s data was therefore weighted based on visitor population figures for air, sea, and tour bus

departures.

Weighting is the procedure to correct the distributions in the sample data to approximate those of the

population from which it is drawn. This is partly a matter of expansion and partly a matter of correction

or adjustment for both non-response and non-coverage. It serves the purpose of providing data that

represents the population rather than the sample.

KI TOMM: Visitor Exit Survey Report 2016-2017

17

17

The total population figures have not been provided to CBSR. Instead, the Kangaroo Island Council

was provided with a file that automatically calculates weights based on population data that is filled in.

The Council filled in the commercially sensitive information and provided CBSR with the resulting

weights. The population figures are not provided to CBSR or included in this report due to the

commercial sensitivity of this information.

Unless otherwise specified, all analysis has been based on weighted data.

Questionnaire Design

The 2017/18 questionnaire was identical to the 2016/17 questionnaire.

Restructuring & Reanalysis of Previous Wave Data

The reader should be aware that before analysis was conducted for the survey data for 2004/2005

year, the TOMM committee expressed their desire to restructure previous data in accordance with

each financial year. The board requested this to allow for more accurate trending and tracking

information to be obtained. In response to this request, CBSR agreed to restructure previous wave’s

data (2001 and 2002) to fit into financial years.

Confidence Intervals

Overall findings from a sample of n=2,042 can be reported within a +/-2.2% margin of error (‘n’ in

statistics refers to the size of the sample, i.e. the number of respondents). This means that if 50% of

visitors say they stayed on the island overnight, the ‘real’ response would fall between 48.8% and

52.2%. There are many cross tabulations included within the report with differing base sample sizes.

The table below illustrates the different margins of error associated with a series of sample sizes. The

reader should be mindful of these margins for error when analysing specific questions and trended

information within this report. Additionally, figures presented in this report are subjected to rounding

errors.

Table 1: Margin of Error per number of responses

Number of

responses per cell

Margin of Error

95% Confidence

2000 ±2.2%

1500 ±2.5%

1000 ±3.1%

500 ±4.4%

KI TOMM: Visitor Exit Survey Report 2016-2017

18

18

Data cleaning

In some cases, the data has been cleaned to improve the overall quality of the data. In case of

incomplete filled in questions by a respondent, the results for the incomplete question for that

respondent has been removed from the data. This is particularly evident for the expenses data where

calculations of total expenses are based on all the questions on the financial subject. Respondents

that have left out information might influence the overall result resulting in less accurate overall

analysis. For example, respondent’s expenditure data was excluded in rare cases where they

indicated that they travelled to the Island as part of a travel package, yet failed to specify the

Kangaroo Island component of the travel package. In order to make more valid comparisons over

time, this data cleaning procedure was applied to not only the 2016/17 wave, but the prior seven

waves as well.

Limitations of the Research

The current methodology employed for the Visitor Exit Survey involves visitors being able to collect

self-completion questionnaires at exit points from Kangaroo Island. Self-completion questionnaires

are cost effective and allow for ample distribution to the sample but often suffer from respondent bias

as there is less control over how it is completed.

Trained staff are not present to ensure accurate interpretation of the questions and individuals will

often skip over sections resulting in non-response bias while also requiring the questionnaire to be

short and simple potentially leaving out important information. Furthermore, self-completion surveys

often suffer from low response rates as the encouragement to complete the survey is not often there.

This results in additional respondent bias as certain demographics are more likely to complete self-

completion surveys than others (e.g. females).

Whilst the data in the research was weighted to account for differentiation of ferry, air, and tour bus

sample sizes from the actual figures, the findings must be considered with regard to the overall

reasonably low response rate.

There were significant differences in the methodology used between 00/01, 01/02 and subsequent

years. Again, trends should be considered indicative only, as many of the questions or code frames

have differed overtime, along with the methodology used to collect data. Unlike the methodology

currently used, surveys in 00/01 and 01/02 were not distributed throughout the financial year meaning

that statistical consistency is lost when trying to compare datasets from current years.

Finally, the reader should also be aware that some tracked results in this report will differ from the

results in previous reports. This is primarily due to the restructuring of the datasets into financial years

and the adaptation of analysis techniques for consistency across years.

KI TOMM: Visitor Exit Survey Report 2016-2017

19

19

Key Findings

2017/18 in a nutshell

The results of the 2017/18 Kangaroo Island Visitor Exit Survey show that key experiential indicators,

satisfaction and annual visitation numbers have been maintained at a high level or have increased

slightly on the previous year. However, average total expenditure per person per visit has declined in

2017/18 which may be linked to a decline in the proportion of overnight visitation. Overall satisfaction

is one of only two experiential measures which fell short of the acceptable range, yet it is nearing its

highest level since 2002/2003.

Economic indicators: 2017/18 saw decline in average annual total expenditure per person per

visit, and fewer visitors are staying overnight.

Average annual total expenditure per person per visit slowed in 2016/17, increasing by only 1.2%.

This year the trend has worsened, with a decrease of 7.3% in average total expenditure per visit to

$722.70, which nears spending in 2014/15 ($726.90).

The proportion of overnight visitors has decreased since last financial year. In 2017/18, 80% of

visitors stayed overnight which is significantly less than the 2016/17 measure (94%). This decrease in

overnight visitation has been driven by both interstate visitors (79%, down from 97% in 2016/17) and

international visitors (60%, down from 84% in 2016/17).

Only one of the measure pertaining to ‘Tourism operators excelling in their business professionalism’

fell within the acceptable range. However, the results were an improvement upon last year for each of

the indicators. The indicator which fell within its acceptable range was the number of compliments and

complaints received which saw an increase in complements and a significant decrease in complaints.

The proportion of those who were very satisfied with the customer service they received was 60%,

falling 5% short of the acceptable range (65%-100%). This is the highest result since the measure

commenced in 2009/10.

Experiential indicators: Repeat visitation and overall satisfaction has decreased even though

those visited feel that KI provides authentic and credible experiences. The proportion of repeat

visitation decreased from last year and has fallen just below the acceptable range. Almost all

indicators pertaining to ‘delivering authentic and credible experiences consistent with its

positioning’ fell within their acceptable ranges. The only indictors which fell short was the

proportion who were satisfied with their overall experience, and the proportion of visitors who

experienced farming and rural landscapes.

2015/16 marked the first time that the proportion of repeat visitors (32%) fell within the acceptable

range of 30%-50% since 2010/11. This wave (2017/18), repeat visitation has decreased significantly,

to 28% and now falls below this acceptable range.

Almost all the indicators surrounding ‘Kangaroo Island delivers authentic and credible experiences

consistent with its positioning’, fell within their respective acceptable ranges in 2017/18. The indicators

which did not fall within their acceptable ranges were:

• the proportion of visitors who experienced farming and rural landscapes which decreased

significantly from 2016/17 (from 92% to 88%); and

• the proportion of visitors who were very satisfied with their overall experience on Kangaroo

Island.

KI TOMM: Visitor Exit Survey Report 2016-2017

20

20

However, it should be noted that satisfaction with overall experience (85%) is high in comparison to

previous measures and nearing the highest recorded level (86%). The trend over the last five years

continues to show a steady increase in the proportion of visitors who are very satisfied / satisfied, and

a decrease in the proportion of those who are very dissatisfied / dissatisfied. Recommendation of KI as

a holiday destination also remained high, with 95% of visitors surveyed indicating that they would

recommend KI as a holiday destination to others as a result of their experience.

KI TOMM: Visitor Exit Survey Report 2016-2017

21

21

Economic Indicators

Overview

In 2017/18, indicators relating to the first economic condition ‘Tourism optimises economic benefits

for Kangaroo Island’ were generally consistent with the previous year, although the growth in

average annual total expenditure per person and the proportion of overnight visitors have both

declined. The average number of nights stayed (4.6), the proportion willing to recommend KI as a

holiday destination (95%), and the increase in the annual number of visitors to KI (5.7%) were all

within the acceptable range. Average annual total expenditure per person per visit decreased by 7.3%

to $722.70 which is well outside of the acceptable range of 5%-10%.

In the second condition, ‘Tourism operators excel in their business professionalism’, only one of

the indicators fell within the acceptable range. However, the results were an improvement upon last

year’s results for each of the indicators. The indicator which fell within its acceptable range was the

number of compliments and complaints received which saw an increase in complements and a

significant decrease in complaints. The proportion of those who were very satisfied with the customer

service they received was 60%, falling 5% short of the acceptable range (65%-100%). This is the

highest result since the measure commenced in 2009/10.

Finally, the third economic condition ‘Kangaroo Island attracts its high yield target markets’ also

remained consistent with the previous year and remains below the ideal level of 40%-60%, with 34%

of visitors spending more than $200 per night.

KI TOMM: Visitor Exit Survey Report 2016-2017

22

22

↓

↑

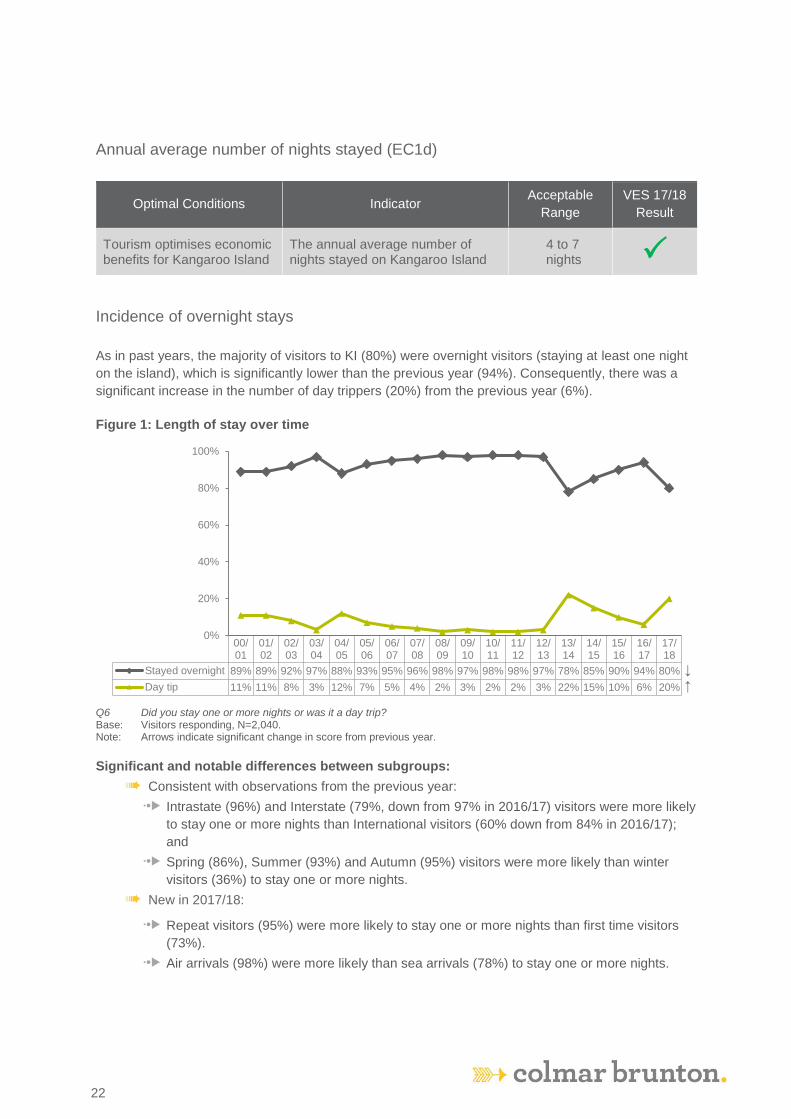

Annual average number of nights stayed (EC1d)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Tourism optimises economic benefits for Kangaroo Island

The annual average number of nights stayed on Kangaroo Island

4 to 7 nights

Incidence of overnight stays

As in past years, the majority of visitors to KI (80%) were overnight visitors (staying at least one night

on the island), which is significantly lower than the previous year (94%). Consequently, there was a

significant increase in the number of day trippers (20%) from the previous year (6%).

Figure 1: Length of stay over time

Q6 Did you stay one or more nights or was it a day trip? Base: Visitors responding, N=2,040. Note: Arrows indicate significant change in score from previous year.

Significant and notable differences between subgroups:

6 Consistent with observations from the previous year:

7 Intrastate (96%) and Interstate (79%, down from 97% in 2016/17) visitors were more likely

to stay one or more nights than International visitors (60% down from 84% in 2016/17);

and

7 Spring (86%), Summer (93%) and Autumn (95%) visitors were more likely than winter

visitors (36%) to stay one or more nights.

6 New in 2017/18:

7 Repeat visitors (95%) were more likely to stay one or more nights than first time visitors

(73%).

7 Air arrivals (98%) were more likely than sea arrivals (78%) to stay one or more nights.

00/01

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

17/18

Stayed overnight 89% 89% 92% 97% 88% 93% 95% 96% 98% 97% 98% 98% 97% 78% 85% 90% 94% 80%

Day tip 11% 11% 8% 3% 12% 7% 5% 4% 2% 3% 2% 2% 3% 22% 15% 10% 6% 20%

0%

20%

40%

60%

80%

100%

KI TOMM: Visitor Exit Survey Report 2016-2017

23

23

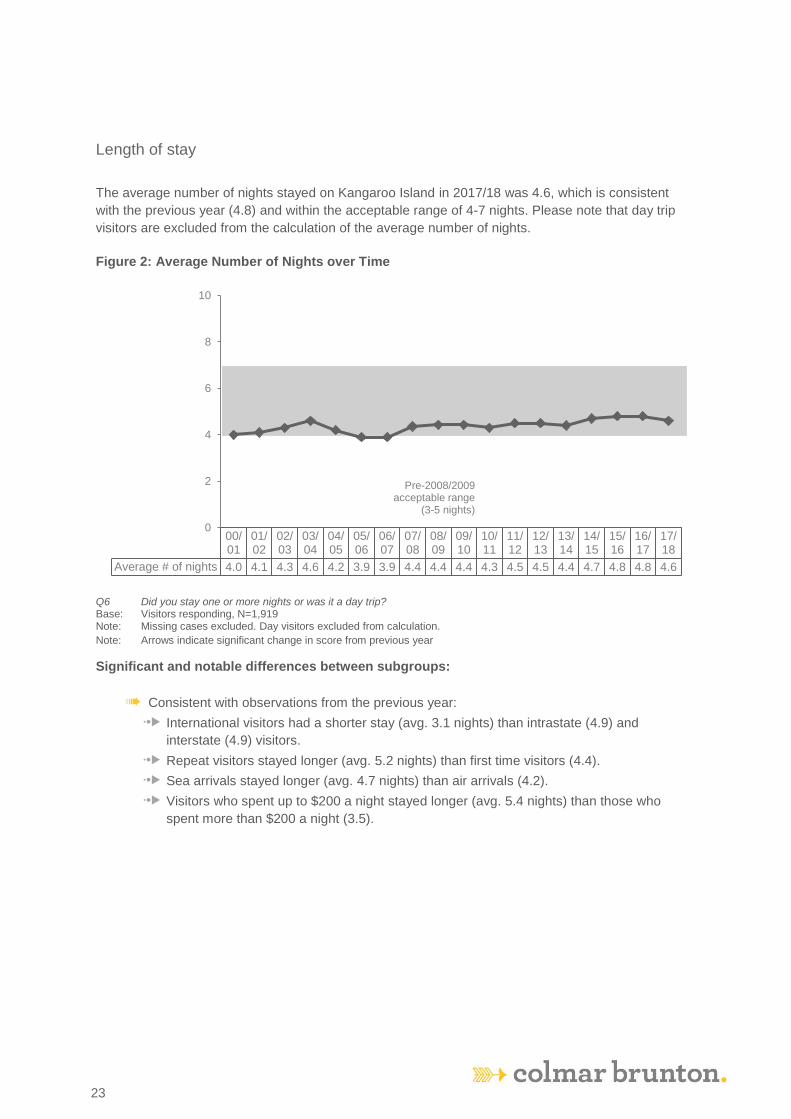

Length of stay

The average number of nights stayed on Kangaroo Island in 2017/18 was 4.6, which is consistent

with the previous year (4.8) and within the acceptable range of 4-7 nights. Please note that day trip

visitors are excluded from the calculation of the average number of nights.

Figure 2: Average Number of Nights over Time

Q6 Did you stay one or more nights or was it a day trip? Base: Visitors responding, N=1,919 Note: Missing cases excluded. Day visitors excluded from calculation.

Note: Arrows indicate significant change in score from previous year

Significant and notable differences between subgroups:

6 Consistent with observations from the previous year:

7 International visitors had a shorter stay (avg. 3.1 nights) than intrastate (4.9) and

interstate (4.9) visitors.

7 Repeat visitors stayed longer (avg. 5.2 nights) than first time visitors (4.4).

7 Sea arrivals stayed longer (avg. 4.7 nights) than air arrivals (4.2).

7 Visitors who spent up to $200 a night stayed longer (avg. 5.4 nights) than those who

spent more than $200 a night (3.5).

00/01

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

17/18

Average # of nights 4.0 4.1 4.3 4.6 4.2 3.9 3.9 4.4 4.4 4.4 4.3 4.5 4.5 4.4 4.7 4.8 4.8 4.6

0

2

4

6

8

10

Pre-2008/2009acceptable range

(3-5 nights)

KI TOMM: Visitor Exit Survey Report 2016-2017

24

24

Average number of nights by visitor origin

Length of stay was consistent by over time for visitor origin. Intrastate and interstate visitors had the

lengthiest stays at an average of 4.9 nights while international visitors had a shorter stay, at an

average of 3.1 nights.

Figure 3: Average number of nights by visitor origin over time

Q6 Did you stay one or more nights or was it a day trip?

Base: Intrastate visitors responding n=505, Interstate visitors responding n=980, International visitors responding n=434

Note: Missing cases excluded.

Note: Arrows indicate significant change in score from previous year.

00/01

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

17/18

Intrastate 4.6 4.8 4.2 4.8 4.8 4.5 4.9 5.0 4.8 4.9 4.8 4.6 4.9 4.8 5.2 4.9 5.0 4.9

Interstate 4.9 4.9 4.9 5.1 5.0 4.6 4.4 4.8 4.8 4.8 4.7 5.1 5.0 4.9 5.0 5.5 5.1 4.9

International 2.3 2.3 3.2 3.7 2.7 2.6 2.5 3.1 3.4 3.1 2.8 3.4 3.2 2.9 3.4 3.1 3.4 3.1

0

2

4

6

8

10

KI TOMM: Visitor Exit Survey Report 2016-2017

25

25

Recommendation of Kangaroo Island to others as a holiday

destination (EC1e)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Tourism optimises economic benefits for Kangaroo Island

Proportion of visitors that would recommend Kangaroo Island to others as a holiday destination

90% - 100%

Willingness to recommend scores in 2016/17 remained consistent with scores from the previous 4

years at 95%. This result is within the acceptable range of 90-100%.

Figure 4: Willingness to recommend

Q23 Would you recommend Kangaroo Island as a holiday destination to others based on this trip? Base: Visitors responding, N=2,014 Note: Missing cases excluded. Note: Arrows indicate significant change in score from previous year.

Significant and notable differences between subgroups:

6 Consistent with observations from the previous year:

7 Air arrivals were more likely to indicate that they would recommend Kangaroo Island as a holiday destination (97%) compared to Sea arrivals (94%).

7 Intrastate visitors were more likely to indicate that they would recommend Kangaroo Island as a holiday destination (97%) compared to Interstate visitors (93%).

6 New in 2018/19:

7 Spring visitors (97%) were more likely to recommend Kangaroo Island as a holiday destination compared to summer (93%) and Autumn visitors (93%).

7 Repeat visitors were more likely to indicate that they would recommend Kangaroo Island as a holiday destination (97%) compared to first time visitors (94%).

00/01

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

17/18

% willing to recommend 98% 97% 99% 98% 98% 98% 98% 97% 95% 90% 94% 92% 93% 93% 93% 93% 95% 95%

0%

20%

40%

60%

80%

100%

KI TOMM: Visitor Exit Survey Report 2016-2017

26

26

↓

7 Those who spent up to $200 per night were more likely to indicate that they would recommend Kangaroo Island as a holiday destination (96%) compared to those who spent $201 or more (92%).

Average expenditure per visit (EC1f)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Tourism optimises economic benefits for Kangaroo Island

Average annual total expenditure per visit

5% - 10% increase

After increasing by 1.2% in 2016/17 to $779.59, average total expenditure per person per visit

decreased significantly, to $722.70 in 2017/18. This reflects a 7.3% decrease in expenditure, which is

outside of the acceptable range of 5%-10%.

Figure 5: Increase in average annual total expenditure per person per visit

Q6 Did you stay one or more nights or was it a way trip?

Q8 What was the cost of the total package?

Q11 What is your best guess of the total Kangaroo Island component of the package?

Q13 What additional money did you spend on top of the package whilst on the Island?

Q14 Please indicate how much you spent on your trip to Kangaroo Island?

Q15 How many people did these costs cover?

Base: Visitors responding, 1,633

Note: Missing cases excluded.

Note: Visitors who indicated that their trip was part of a package yet did not specify the KI component of the package have been excluded from all expenditure calculations in this report

Significant and notable differences between subgroups:

6 Consistent with observations from the previous year:

7 Per person expenditure was higher for interstate visitors ($939.67) compared to both

intrastate ($650.79) and international visitors ($585.65).

7 Air arrivals spent more than sea arrivals ($1297.87 vs. $740.70).

09/10(n=1450)

10/11(n=1811)

11/12(n=1000)

12/13(n=2179)

13/14(n=2197)

14/15(n=1,414)

15/16(n=1,412)

16/17(n=1,826)

17/18(n=1,634)

Avg. total expenditureper person per visit

$623.00 $633.65 $684.31 $609.52 $601.92 $726.90 $770.06 $779.59 $722.70

$0

$200

$400

$600

$800

$1,000

KI TOMM: Visitor Exit Survey Report 2016-2017

27

27

7 As to be expected, those who stayed one or more nights spent more than day visitors

($848.01 vs. $312.65).

7 Those on a bus tour ($326.18) spent less than those not on a tour ($835.10).

Annual number of visitors (EC1g)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Tourism optimises economic benefits for Kangaroo Island

Annual number of visitors to Kangaroo Island

0% - 20% increase

The annual number of visitors to Kangaroo Island increased from 213,933 in 2016/17 to 226,051 in

2017/18. This represents a 5.7% rise which is within the acceptable range of 0-20%.

Figure 6: Increase in annual number of visitors

Note: Data provided by TOMM Committee.

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

17/18

% increase innumber of visitors

2.3% 2.7% -2.0 -3.6 26.0 -5.4 5.6% 1.2% 3.0% 0.6% -0.4 1.2% 1.8% 4.4% 3.6% 5.7%

-30%

-20%

-10%

0%

10%

20%

30%

KI TOMM: Visitor Exit Survey Report 2016-2017

28

28

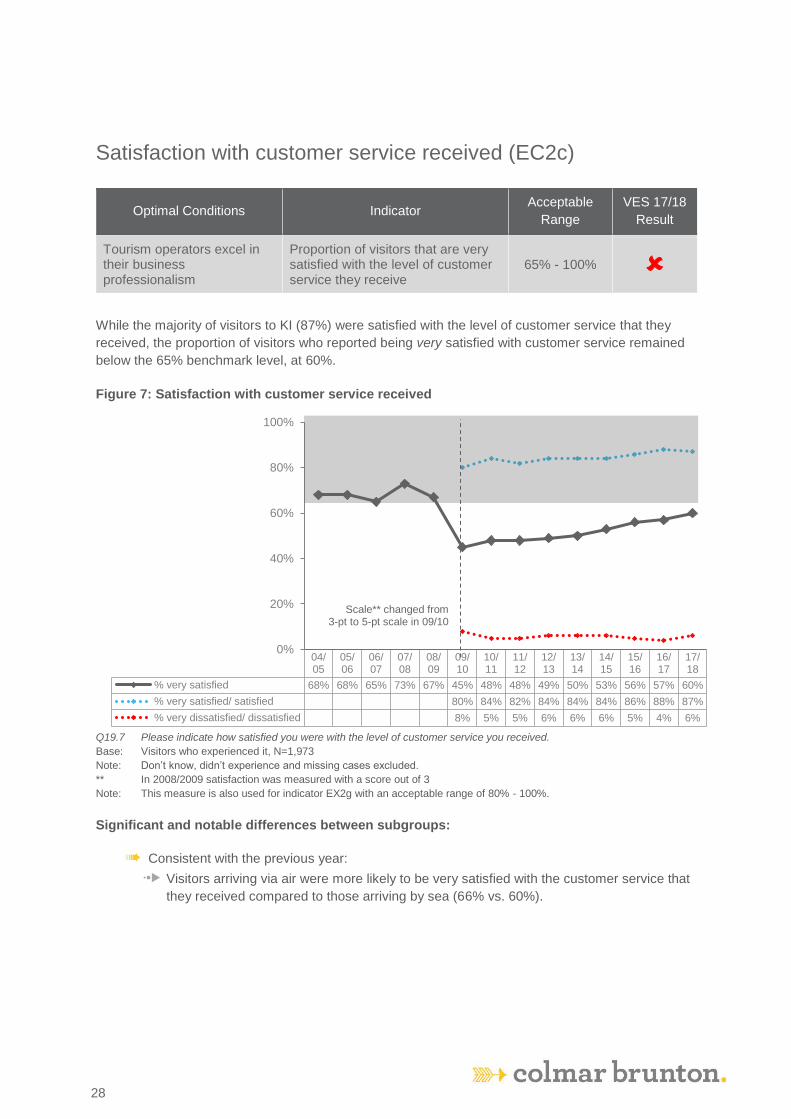

Satisfaction with customer service received (EC2c)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Tourism operators excel in their business professionalism

Proportion of visitors that are very satisfied with the level of customer service they receive

65% - 100%

While the majority of visitors to KI (87%) were satisfied with the level of customer service that they

received, the proportion of visitors who reported being very satisfied with customer service remained

below the 65% benchmark level, at 60%.

Figure 7: Satisfaction with customer service received

Q19.7 Please indicate how satisfied you were with the level of customer service you received.

Base: Visitors who experienced it, N=1,973

Note: Don’t know, didn’t experience and missing cases excluded.

** In 2008/2009 satisfaction was measured with a score out of 3

Note: This measure is also used for indicator EX2g with an acceptable range of 80% - 100%.

Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 Visitors arriving via air were more likely to be very satisfied with the customer service that

they received compared to those arriving by sea (66% vs. 60%).

04/05

05/06

06/07

07/08

08/09

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

17/18

% very satisfied 68% 68% 65% 73% 67% 45% 48% 48% 49% 50% 53% 56% 57% 60%

% very satisfied/ satisfied 80% 84% 82% 84% 84% 84% 86% 88% 87%

% very dissatisfied/ dissatisfied 8% 5% 5% 6% 6% 6% 5% 4% 6%

0%

20%

40%

60%

80%

100%

Scale** changed from 3-pt to 5-pt scale in 09/10

KI TOMM: Visitor Exit Survey Report 2016-2017

29

29

Satisfaction with professionalism of tourism operators (EC2d)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Tourism operators excel in their business professionalism

Proportion of customers that are highly satisfied with the professionalism of tourism operators

65% - 100%

This year, the proportion of visitors to Kangaroo Island who reported that they were very satisfied with

the professionalism of tourism operators was 5%, which is consistent with the previous year (52%)

and below the acceptable range of 65-100%. It is, however, the highest proportion since the measure

commenced in 2009/10.

Figure 8: Satisfaction with professionalism of tourism operators

Q19.12 Please indicate how satisfied you were with the professionalism of tourism businesses. Base: Visitors who experienced it, N=1,815 Note: Don’t know, didn’t experience and missing cases excluded.

Significant and notable differences between subgroups:

6 Results were consistent between subgroups.

09/10

10/11

11/12

12/13

13/14

14/15

15/16

16/17

17/18

% very satisfied 41% 40% 43% 41% 48% 51% 52% 52% 55%

% very satisfied/ satisfied 77% 77% 79% 78% 82% 82% 83% 86% 85%

% very dissatisfied/ dissatisfied 9% 7% 7% 7% 6% 6% 5% 5% 6%

0%

20%

40%

60%

80%

100%

KI TOMM: Visitor Exit Survey Report 2016-2017

30

30

↓

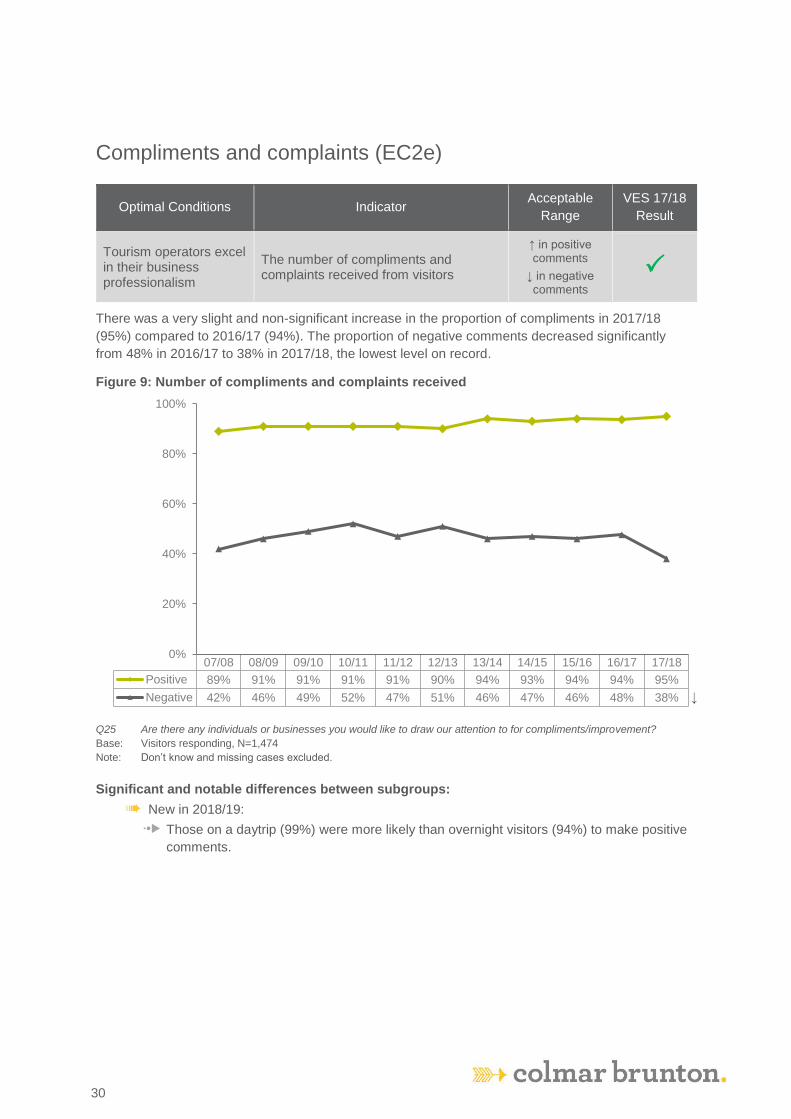

Compliments and complaints (EC2e)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Tourism operators excel in their business professionalism

The number of compliments and complaints received from visitors

↑ in positive comments

↓ in negative comments

There was a very slight and non-significant increase in the proportion of compliments in 2017/18

(95%) compared to 2016/17 (94%). The proportion of negative comments decreased significantly

from 48% in 2016/17 to 38% in 2017/18, the lowest level on record.

Figure 9: Number of compliments and complaints received

Q25 Are there any individuals or businesses you would like to draw our attention to for compliments/improvement?

Base: Visitors responding, N=1,474

Note: Don’t know and missing cases excluded.

Significant and notable differences between subgroups:

6 New in 2018/19:

7 Those on a daytrip (99%) were more likely than overnight visitors (94%) to make positive

comments.

07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

Positive 89% 91% 91% 91% 91% 90% 94% 93% 94% 94% 95%

Negative 42% 46% 49% 52% 47% 51% 46% 47% 46% 48% 38%

0%

20%

40%

60%

80%

100%

KI TOMM: Visitor Exit Survey Report 2016-2017

31

31

Average spend per night over $200 (EC3c)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island attracts its high yield target markets

Proportion of visitors for whom average spend per night exceeds $200

40% - 60%

The proportion of visitors who reported an average spend of over $200 per night was 37%, which is

consistent with the result from the previous year and below the acceptable range of 40-60%.

Figure 10: Average spend per night over $200

Q6 Did you stay one or more nights or was it a day trip?

Q8 What was the cost of the total package?

Q11 What is your best guess of the total Kangaroo Island component of the package?

Q13 What additional money did you spend on top of the package whilst on the Island? Q14 Please indicate how much you spent on your trip to Kangaroo Island? Q15 How many people did these costs cover? Base: Visitors responding, N=1,555 Note: Day trippers excluded. Note: Missing cases excluded. Note: Visitors who indicated that their trip was part of a package yet did not specify the KI component of the package have

been excluded from all expenditure calculations in this report

Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 International visitors (44%) and Interstate visitors (36%) were more likely to spend over

$200 per night than Intrastate visitors (25%).

7 Those arriving by air were more likely to spend over $200 per night (65%) than those

arriving by sea (70%).

7 First time visitors were more likely to spend over $200 per night (39%) than repeat visitors

(22%).

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% spend$200+ per night

28% 28% 26% 25% 30% 37% 35% 37% 34%

0%

20%

40%

60%

80%

100%

KI TOMM: Visitor Exit Survey Report 2016-2017

32

32

Summary of sub-group scores for economic indicators

Indicator Sub-groups who were within the Acceptable range for the indicator

Sub-groups who scored more highly for the indicator (compared to their comparative sub-group)

EC1d Annual average number of nights stayed

• Intrastate & interstate visitors • Spring, summer & autumn visitors • Those not on a bus tour • Sea and air arrivals • First time visitors & repeat visitors • Those who spent up to $200 a

night

• Interstate and intrastate visitors • Repeat visitors • Sea arrivals • Those who spent up to $200 a

night • Those not on a tour bus

EC1e

Proportion of visitors that would recommend Kangaroo Island to others as a holiday destination

• All subgroups

• Intrastate visitors • Repeat visitors • Air arrivals • Those who spent up to $200 a

night

EC1f Average annual total expenditure per visit

• Interstate visitors • Non-bus visitors • Over-night visitors

• Interstate visitors • Air arrivals • Those who stayed overnight • Those not on a bus tour

EC2c

Proportion of visitors that are very satisfied with the level of customer service they receive

• Air arrivals • Air arrivals

EC2d

Proportion of customers that are highly satisfied with the professionalism of tourism operators

• None • None

EC2e

The number of compliments and complaints received from visitors

• Air & sea arrivals • Interstate & International visitors • Repeat & First-time visitors • Summer, Autumn & Winter visitors • Those spending $200 or more per

night • Day-trippers & overnight visitors • Bus and non-bus visitors

• Those on a bus tour (Compliments)

• Day trippers (Compliments)

EC3c

Proportion of visitors whose average spend per night exceeds $200

• International visitors • Air arrivals

• Interstate and international visitors

• Air arrivals • First time visitors

KI TOMM: Visitor Exit Survey Report 2016-2017

33

33

Experiential Indicators

Overview

Almost all of the ‘Kangaroo Island delivers authentic and credible experiences consistent with

its positioning’ indicators fell within their respective acceptable ranges in 2017/18.

The indicators which did not fall within their acceptable ranges were the proportion of visitors who

experienced farming and rural landscapes which decreased significantly from 2016/17 (from 92% to

88%), and the proportion of visitors who were very satisfied with their overall experience on Kangaroo

Island. However, it should be noted that satisfaction with overall experience (85%) is high in

comparison to previous measures and nearing the highest recorded level (86%). The trend over the

last five years continues to show a steady increase in the proportion of visitors who are very satisfied /

satisfied, and a decrease in the proportion of those who are very dissatisfied / dissatisfied.

Recommendation of KI as a holiday destination also remained high, with 95% of visitors surveyed

indicated that they would recommend KI as a holiday destination to others as a result of their

experience.

Other notable results include an increase in the proportion of visitors who were very satisfied with the

quality of the roads (32% up from 25% in 2016/17) however remains well below the acceptable range

of 60%-100%.

KI TOMM: Visitor Exit Survey Report 2016-2017

34

34

Viewed wildlife in natural environment (EX1b)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that viewed wildlife in the natural environment

90% - 100%

The vast majority (97%) of visitors in 2017/18 viewed Australia’s wildlife in natural surroundings. This

result is consistent with last year’s measure and is within the acceptable range of 90-100%.

Figure 11: Visitors that viewed Australia’s wildlife in natural surroundings

Q18.2 For each of the following please indicate whether experienced this while on Kangaroo Island? Base: Visitors responding, N=1,876 Note: Missing cases excluded. * Figure reflects response to the question “please indicate whether you believe that Kangaroo Island provides you this

while on Kangaroo Island.

Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 Those on a bus tour (100%) were more likely to see view Australian wildlife in natural

surroundings than those not on a bus tour (96%).

7 International visitors were more likely to view Australian wildlife in natural surroundings

than both interstate (96%) and intrastate visitors (95%).

6 New in 2017/18:

7 Winter visitors (99%) and Autumn visitors (98%) were more likely to view Australian

wildlife in natural surroundings than summer visitors (95%).

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 92% 93% 93% 93% 96% 96% 96% 97% 97%

0%

20%

40%

60%

80%

100%

98% of visitors believedthat KI provides this*

KI TOMM: Visitor Exit Survey Report 2016-2017

35

35

Experienced scenic variety without crowds (EX1c)

Optimal Conditions Indicator Acceptable

Range

VES 16/17

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that experienced scenic variety without crowds

90% - 100%

Almost all visitors (97%) to Kangaroo Island experienced scenic variety without crowds, which is

consistent with last year’s measure (97%) and within the acceptable range of 90%-100%.

Figure 12: Visitors that experienced scenic variety without crowds

Q18.3 For each of the following please indicate whether experienced this while on Kangaroo Island? Base: Visitors responding, N=1,864 Note: Missing cases excluded. * Figure reflects response to the question “please indicate whether you believe that Kangaroo Island provides you this

while on Kangaroo Island. Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 Intrastate visitors (98%) were more likely to experience scenic variety without crowds of

people than international visitors (93%).

7 Day trippers were less likely to have experienced this (91%) than those who stayed

overnight (98%).

7 Those who did not come on a bus tour (98%) were more likely to have experienced this

than those who came as part of a bus tour (91%).

7 Repeat visitors were more likely to have experience this (99%) than first time visitors

(96%).

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 95% 97% 97% 96% 94% 97% 97% 97% 97%

0%

20%

40%

60%

80%

100%

96% of visitors believed that KI provides this*

KI TOMM: Visitor Exit Survey Report 2016-2017

36

36

Experienced cultural heritage and history of settlement (EX1d)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that experienced cultural heritage and history of settlement

70% - 100%

This year, the proportion of visitors who experienced cultural heritage and history of settlement (72%)

was consistent with 2016/17 (74%). This is within the acceptable range of 70-100%.

Figure 13: Visitors that experienced cultural heritage and history of settlement

Q18.4 For each of the following please indicate whether you experienced this while on Kangaroo Island? Base: Visitors responding, N=1,821 Note: Missing cases excluded. * Figure reflects response to the question “please indicate whether you believe that Kangaroo Island provides you this

while on Kangaroo Island. Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 International visitors were less likely to experience cultural heritage and the history of

settlement (54%) compared to both intrastate (74%) and interstate (77%) visitors.

6 New in 2018/19

7 Those spending less than $200 per night (75%) were more likely than those spending $201 or more per night (68%) to experience cultural heritage and the history of settlement.

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 68% 70% 71% 67% 71% 74% 76% 74% 72%

0%

20%

40%

60%

80%

100%

80% of visitors believed that KI provides this*

KI TOMM: Visitor Exit Survey Report 2016-2017

37

37

Experienced spectacular scenery and coastal landscapes

(EX1e)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that experienced spectacular scenery and coastal landscapes

90% - 100%

Almost all (99%) visitors experienced spectacular scenery and coastal landscapes in 2016/17. This

result is comparable to that of 2017/18 (99%) and is within the acceptable range of 90%-100%.

Figure 14: Visitors that experienced spectacular scenery and coastal landscapes

Q18.5 For each of the following please indicate whether you experienced this while on Kangaroo Island? Base: Visitors responding, N=1,865 Note: Missing cases excluded. * Figure reflects response to the question “please indicate whether you believe that Kangaroo Island provides you this

while on Kangaroo Island.

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 98% 98% 98% 98% 99% 99% 99% 99% 99%

0%

20%

40%

60%

80%

100%

99% of visitors believed that KI provides this*

KI TOMM: Visitor Exit Survey Report 2016-2017

38

38

Experienced areas of untouched natural beauty (EX1f)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that experienced areas of untouched natural beauty

90% - 100%

The proportion of visitors that reported experiencing areas of untouched natural beauty (97%) is

consistent with previous years. This result is within the acceptable range of 90-100%.

Figure 15: Visitors that experienced areas of untouched natural beauty

Q18.6 For each of the following please indicate whether you experienced this while on Kangaroo Island? Base: Visitors responding, N=1,989 Note: Missing cases excluded. * Figure reflects response to the question “please indicate whether you believe that Kangaroo Island provides you this

while on Kangaroo Island.

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 95% 95% 95% 95% 96% 95% 96% 97% 97%

0%

20%

40%

60%

80%

100%

98% of visitors believed that KI provides this*.

KI TOMM: Visitor Exit Survey Report 2016-2017

39

39

Experienced farming and rural landscapes (EX1g)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that experienced farming and rural landscapes

90% - 100%

The proportion of visitors who experienced farming and rural landscapes in 2017/18 (88%) decreased

significantly from 2016/17 (92%). This is now outside of the acceptable range of 90-100% after being

within the acceptable range for the previous two years.

Figure 16: Visitors that experienced farming and rural landscapes

Q18.7 For each of the following please indicate whether you experienced this while on Kangaroo Island?

Base: Visitors responding, N=1,860 Note: Missing cases excluded.

* Figure reflects response to the question “please indicate whether you believe that Kangaroo Island provides you this while on Kangaroo Island.

Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 Day trippers were less likely to have experienced farming and rural landscapes (67%)

than those staying one or more nights (92%); and

7 Bus tour visitors (67%) were less likely than others (92%) to experience this.

7 International visitors (72%) were less likely to experience this than both Interstate (91%)

and intrastate visitors (91%).

6 New in 2016/17:

7 Winter visitors (73%) were less likely to have experienced farming and rural landscapes

than spring (92%), summer (91%), and autumn (91%) visitors

7 Repeat visitors (92%) were less likely to experience this than first time visitors (86%).

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 88% 89% 89% 89% 88% 88% 90% 92% 88%

0%

20%

40%

60%

80%

100%

94% of visitors believed that KI provides this*

↓

KI TOMM: Visitor Exit Survey Report 2016-2017

40

40

Experienced local Kangaroo Island produce (EX1h)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that experienced local Kangaroo Island produce

80% - 100%

The proportion of visitors who experienced local Kangaroo Island produce in 2017/18 was 83%, which

is consistent with the previous measure (87%) and within the acceptable range of 80-100%.

Figure 17: Visitors that experienced local Kangaroo Island produce

Q18.8 For each of the following please indicate whether you experienced this while on Kangaroo Island? Base: Visitors responding, N=1,976. Note: Missing cases excluded.

* Figure reflects response to the question “please indicate whether you believe that Kangaroo Island provides you this while on Kangaroo Island.

Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 International visitors (67%) were less likely to experience local Kangaroo Island produce

than intrastate (93%) and interstate (83%) visitors;

7 Day trippers (46%) were less likely to experience this than those staying overnight (91%);

7 Repeat visitors to KI (94%) were more likely to experience this than first time visitors

(78%); and

7 Those on a bus tour (45%) were less likely to experience this than those not on a bus tour

(90%).

6 New in 2018/19:

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 79% 82% 82% 81% 75% 80% 83% 87% 83%

0%

20%

40%

60%

80%

100%

91% of visitors believed that KI provides this*

KI TOMM: Visitor Exit Survey Report 2016-2017

41

41

7 Intrastate visitors (93%) were more likely to experience local Kangaroo Island produce

than interstate visitors (83%); and

7 Winter visitors (62%) were less likely to experience this than spring (87%), Summer (89%)

and Autumn visitors (89%).

7 Air arrivals were more likely to experience local Kangaroo Island produce than sea

arrivals (82%);

KI TOMM: Visitor Exit Survey Report 2016-2017

42

42

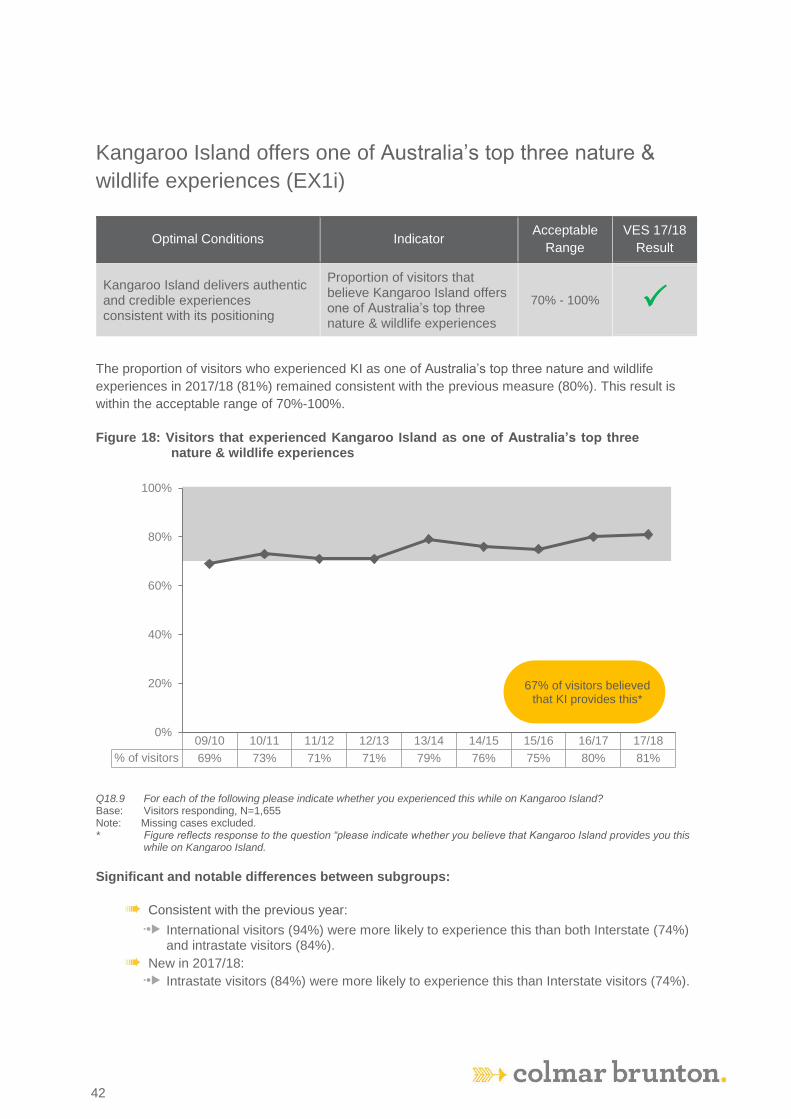

Kangaroo Island offers one of Australia’s top three nature &

wildlife experiences (EX1i)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that believe Kangaroo Island offers one of Australia’s top three nature & wildlife experiences

70% - 100%

The proportion of visitors who experienced KI as one of Australia’s top three nature and wildlife

experiences in 2017/18 (81%) remained consistent with the previous measure (80%). This result is

within the acceptable range of 70%-100%.

Figure 18: Visitors that experienced Kangaroo Island as one of Australia’s top three nature & wildlife experiences

Q18.9 For each of the following please indicate whether you experienced this while on Kangaroo Island? Base: Visitors responding, N=1,655 Note: Missing cases excluded. * Figure reflects response to the question “please indicate whether you believe that Kangaroo Island provides you this

while on Kangaroo Island. Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 International visitors (94%) were more likely to experience this than both Interstate (74%) and intrastate visitors (84%).

6 New in 2017/18:

7 Intrastate visitors (84%) were more likely to experience this than Interstate visitors (74%).

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 69% 73% 71% 71% 79% 76% 75% 80% 81%

0%

20%

40%

60%

80%

100%

67% of visitors believed that KI provides this*

KI TOMM: Visitor Exit Survey Report 2016-2017

43

43

Kangaroo Island has a friendly local community (EX1j)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that believe Kangaroo Island has a friendly local community

80% - 100%

The proportion of visitors who experienced a friendly local community on KI was 93% in 2017/18. This

result is consistent with last year’s result (94%) and is within the acceptable range of 80%-100%.

Figure 19: Visitors that experienced a friendly local community on Kangaroo Island

Q18.10 For each of the following please indicate whether you experienced this while on Kangaroo Island? Base: Visitors responding, N=1,834 Note: Missing cases excluded. * Figure reflects response to the question “please indicate whether you believe that Kangaroo Island provides you this

while on Kangaroo Island. Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 Intrastate (97%) and interstate (95%) visitors were more likely to experience a friendly

local community than international visitors (83%);

7 Overnight visitors (96%) were more likely than day trippers (82%) to experience this; and

7 Those on a bus tour (81%) were less likely to experience this than other visitors (96%).

6 New in 2017/18:

7 Repeat visitors were more likely to experience a friendly local community than first time

visitors (92%)

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 90% 92% 93% 93% 91% 91% 92% 94% 93%

0%

20%

40%

60%

80%

100%

92% of visitors believed that KI provides this*

KI TOMM: Visitor Exit Survey Report 2016-2017

44

44

Agreement with positioning statement (EX1k)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors who agree** that Kangaroo Island is a wild and welcoming destination, that will surprise and amaze you, relax your mind, refresh your spirit and make you feel totally alive. It provides an opportunity to view and to discover all the scenic variety of mainland Australia

70% - 100%

The proportion of visitors who agreed with the positioning statement in 2017/18 (85%) was consistent

with agreement levels from the previous year (86%). This result remains within the acceptable range

of 70%-100%.

Figure 20: Visitors who agree that Kangaroo Island is a wild and welcoming destination

Q24 To what extent do you agree or disagree with this statement? Base: Visitors responding, N=2,009 Note: Missing cases excluded. ** Rated 7-10 on an eleven point scale, where 0 means strongly disagree and 10 means strongly agree.

Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 Intrastate visitors (90%) were more likely to agree with the positioning statement than

interstate visitors (80%).

6 New in 2017/18:

7 Repeat visitors (90%) were more likely to agree with the positioning statement than first

time visitors (83%).

7 Air arrivals (92%) were more likely to agree with the positioning statement than those

arriving by sea (85%).

09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 77% 81% 80% 82% 85% 85% 84% 86% 85%

0%

20%

40%

60%

80%

100%

KI TOMM: Visitor Exit Survey Report 2016-2017

45

45

Matching expectation set by marketing materials (EX1l)

Optimal Conditions Indicator Acceptable

Range

VES 17/18

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning

Proportion of visitors that state that their experience matched or exceeded expectation set by marketing materials

80% - 100%

The vast majority of visitors to Kangaroo Island who stated that their experience matched or

exceeded expectations set by marketing materials (94%) was comparable to last year (95%). This

result remains within the acceptable range of 80%-100%.

Figure 21: Visitors stating that their experience matched or exceeded the expectation set by marketing materials

Q21 Do you believe that Kangaroo Island’s marketing material matched the experience you had while visiting Kangaroo

Island?

Base: Visitors responding, N=1,977

Note: Missing cases excluded.

Significant and notable differences between subgroups:

6 Consistent with the previous year:

7 Air arrivals (97%) were more likely to believe this than sea arrivals (94%).

6 New in 2017/18:

7 Intrastate visitor’s (97%) expectations were more likely to be met or exceeded than interstate visitors (92%)

7 Winter visitor’s expectations were more likely to be met or exceeded than Spring (92%), summer (94%), Autumn visitors (93%)

7 Repeat visitor’s (96%) expectations were more likely to be met or exceeded than first time visitors (93%).

05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18

% of visitors 75% 74% 75% 82% 91% 91% 91% 92% 93% 91% 93% 95% 94%

0%

20%

40%

60%

80%

100%

KI TOMM: Visitor Exit Survey Report 2016-2017

46

46

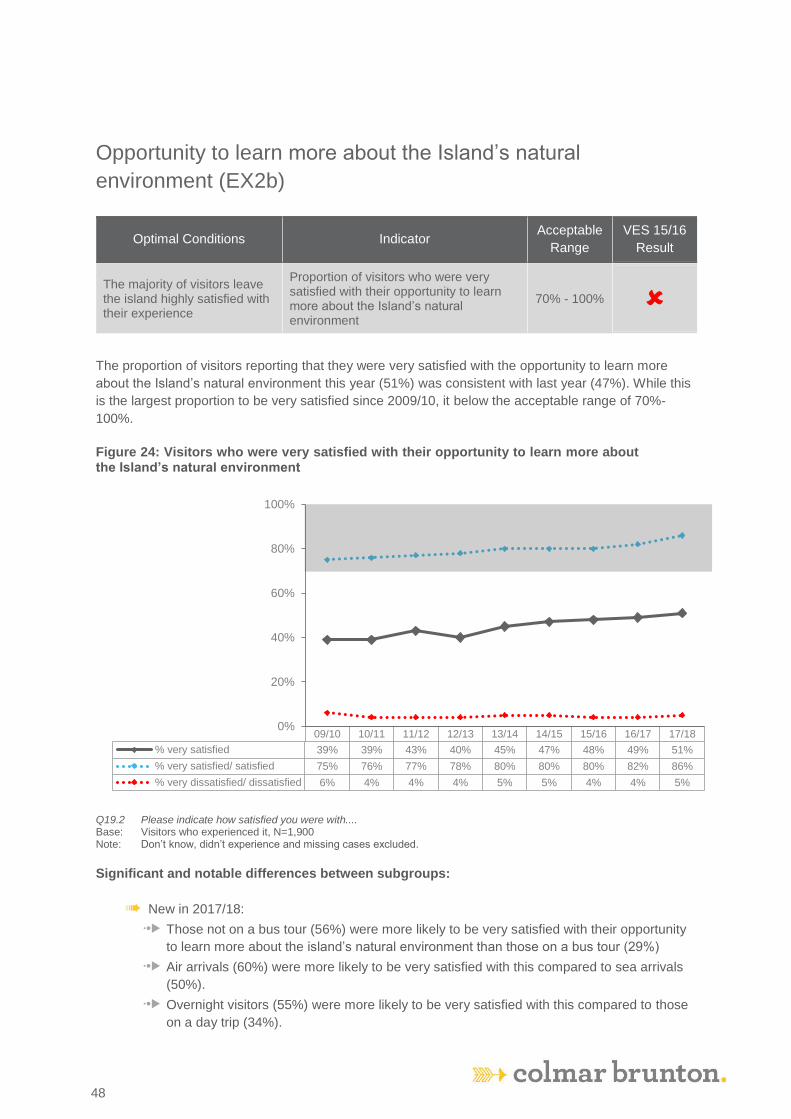

Satisfaction with overall experience (EX1m)

Optimal Conditions Indicator Acceptable

Range

VES 16/17

Result

Kangaroo Island delivers authentic and credible experiences consistent with its positioning