© The McGraw-Hill Companies, Inc., 2007 McGraw-Hill/Irwin Chapter 18 Managerial Accounting Concepts...

42

© The McGraw-Hill Companies, Inc., 2007 McGraw-Hill/Irwin Chapter 18 Managerial Accounting Concepts and Principles

-

Upload

buck-foster -

Category

Documents

-

view

216 -

download

1

Transcript of © The McGraw-Hill Companies, Inc., 2007 McGraw-Hill/Irwin Chapter 18 Managerial Accounting Concepts...

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Chapter 18

Managerial Accounting Concepts and Principles

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Conceptual Learning ObjectivesC1: Explain the purpose and nature of

managerial accountingC2: Describe the lean business modelC3: Describe accounting concepts useful in

classifying costsC4: Define product and period costs and

explain how they impact financial statements

C5: Explain how the balance sheets for manufacturing and merchandising companies differ

C6: Explain manufacturing activities and the flow of manufacturing costs.

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

A1: Compute cycle time and cycle efficiency, and explain their importance to production management

P1: Compute cost of goods sold for a manufacturer

P2: Prepare a manufacturing statement and explain its purpose and links to financial statements.

Analytical Learning Objectives

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Managerial and Financial Accounting

C 1

Managerial accountingprovides financial and non-financial informationfor managers of anorganization and other decision makers

Financial accountingprovides generalpurpose financialinformation to thosewho are outsidethe organization.

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Planning and ControlC 1

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Financial Accounting Managerial Accounting

1. Users and Investors, creditors and Managers, employees and decision makers other external users other internal users

2. Purpose of Making investment, credit Planning and

information and other decisions control decisions

3. Flexibility Structured and often Relatively flexible

of practice controlled by GAAP (no GAAP)

4. Timeliness of Often available only Available quickly without

information after audit is complete need to wait for audit

5. Time dimension Historical information Many projections with some predictions and estimates

6. Focus of Emphasis on Projects, processes and

information whole organization segments of an organization

7. Nature of Monetary Monetary and

information information nonmonetary information

Nature of Managerial Accounting Exh.

18-2

C 1

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Lean Business Model

Customer Orientation

GlobalEconomy

LeanBusiness

Model

Eliminationof Waste

Satisfy theCustomer

PositiveReturn

C 2

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

on

Quality improvementapplied to all aspects of

business activities.

Seek and uncover waste.

Employees encouragedto try new methodsto improve quality.

Company emphasizesvalue of quality through

quality awards.

Total Quality ManagementC 2

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Complete productsjust in time to

ship to customers.

Complete partsjust in time for

assembly into products.

Receive materialsjust in time for

production.

Scheduleproduction.

Receivecustomer

orders.

Just-In-Time (JIT) Manufacturing

C 2

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Just-In-Time (JIT) Manufacturing

C 2

To accomplish just-in-time manufacturing:

Processes must be aligned to eliminate

delays and inefficiencies

Companies must establish good relations with

suppliers

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Implications of Lean Manufacturing

C 2

Understand the nature and

sources of cost

Measure value provided to customers

Determine price

customers pay

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Behavior

Traceability

Controllability

Relevance

Function

Cost Accounting ConceptsC 3

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Cost behavior means how a cost will react to changes in the level of business activity.

Classification by BehaviorC 3

A fixed cost does not change with changes in the volume of activity

A variable cost changes in proportion to changes in the volume

of activity

A mixed cost refers to a combination of fixed and variable

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Rent

Co

st

Tires

Co

stClassification by Behavior

Cost behavior means how a cost will react to changes in the level of business activity. Total fixed costs do

not change when activity changes.

Total variable costs change in proportionto activity changes.

C 3

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

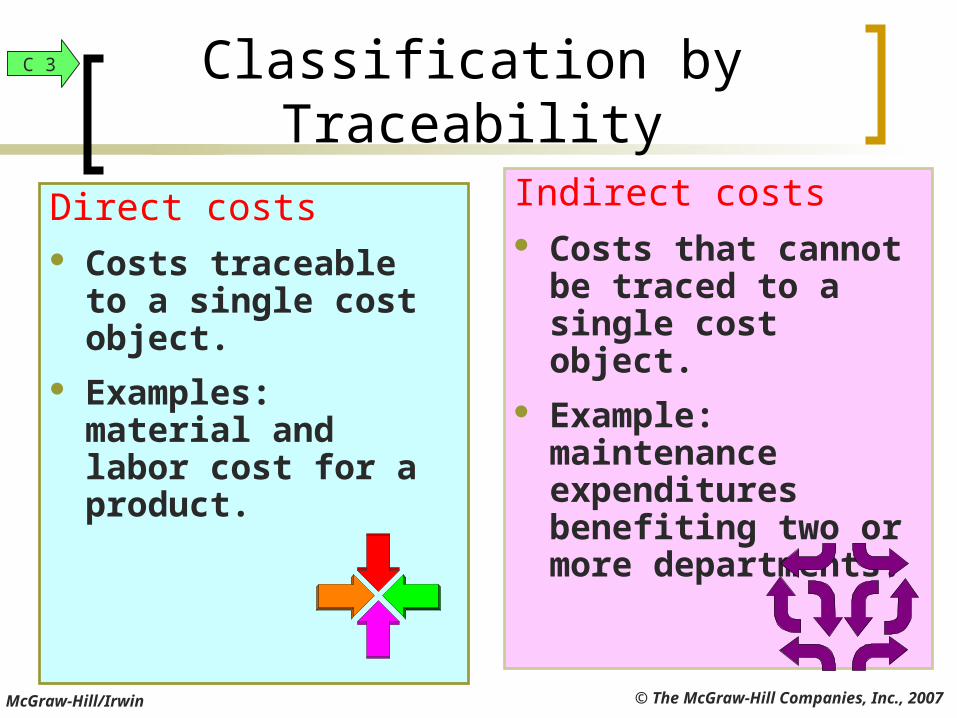

Direct costs Costs traceable to a

single cost object. Examples: material

and labor cost for a product.

Indirect costs Costs that cannot be

traced to a single cost object.

Example: maintenance expenditures benefiting two or more departments.

Classification by TraceabilityC 3

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

The degree of control depends on thelevel of management in the organization.

More C

ontrolM

ore

Con

trol

Very little control

Classification by ControllabilityC 3

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

All costs incurred in the past that cannot be avoided or changed.

Sunk costs should not be considered in decisions.

Example: You bought an automobile that cost $15,000 two years ago. The $15,000 cost is sunk because whether you drive it, park it, trade it, or sell it, you cannot change the $15,000 cost.

Classification by Relevance:Sunk Costs

C 3

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Classification by Relevance:Out-of-Pocket Costs

C 3

A cost that requires a future outlay of cash.

Out-of-pocket costs should be considered in decisions.

Example: You plan on buying a new car for $25,000 next month. The cost of the new car is an out-of-pocket cost because you can choose to spend the $25,000 or not in the future

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

The potential benefit lost by choosing a specific action from two or more alternatives

Example: If you were not attending college, you could be earning $20,000 per year. Your opportunity cost of attending college for one year is $20,000.

Classification by Relevance: Opportunity Costs

C 3

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

TheProduct

Classification by Function:Product Costs

DirectLabor

DirectMaterial

Manufacturing Overhead

C 4

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Period costs are expensesnot attached to the product.

Classification by Function:Period Costs

Administrative Costs

Non-manufacturing costsof staff support and

administrative functions –accounting, data processing,

personnel, researchand development.

Selling Costs

Costs incurred to obtain customer orders and todeliver finished goods

to customers –advertising and shipping.

C 4

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Period Costs(Expenses)

Product Costs(Inventory)

Inventory Not Sold in 2008

OperatingExpenses

Cost ofGoods Sold

Raw MaterialsGoods in ProcessFinished Goods

Cost ofGoods Sold

2008 CostsIncurred

2008 IncomeStatement

2009 IncomeStatement

2008 BalanceSheet Inventory

InventorySold in 2008

Period and Product Costsin Financial Statements Exh.

18-8

C 4

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Cost Item Behavior Traceability Function

Materials Variable Direct Product

Assembly Wages Variable Direct Product

Advertising Fixed Indirect Period

Production Manager's Salary Fixed Indirect Product

Office Depreciation Fixed Indirect Period

Cost Item Behavior Traceability Function

Materials Variable Direct Product

Assembly Wages Variable Direct Product

Advertising Fixed Indirect Period

Production Manager's Salary Fixed Indirect Product

Office Depreciation Fixed Indirect Period

Potential Multiple Cost Classifications Exh.

18-9

C 4

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Merchandisers . . .Buy finished goods.

Sell finished goods.

SaleMart

Manufacturers . . .Buy raw materials.

Produce and sell finished goods.

Reporting Manufacturing Activities

C 5

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

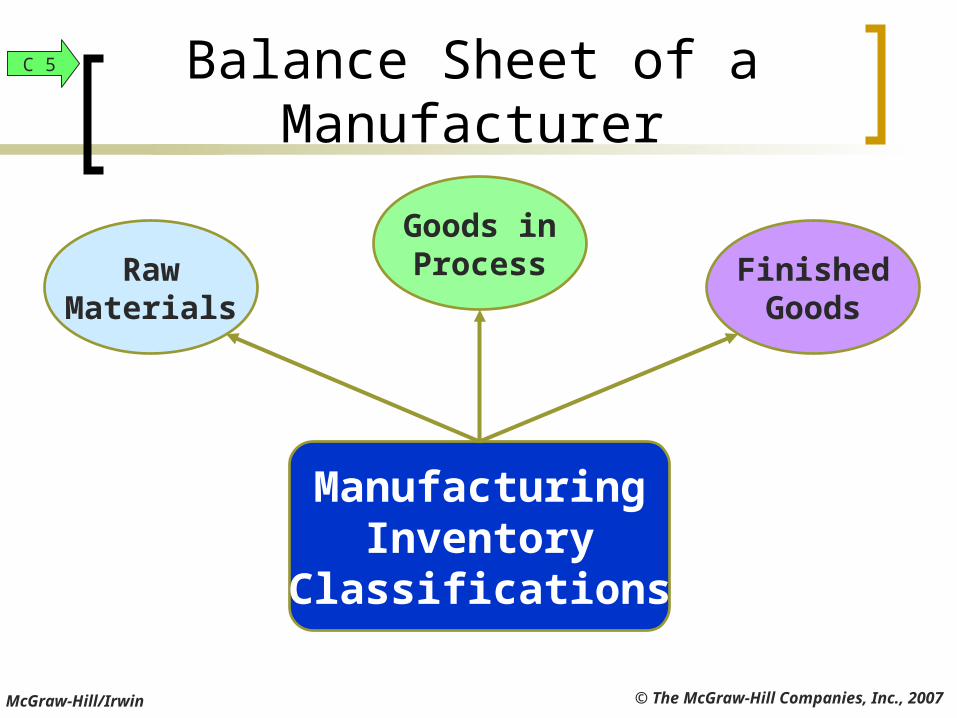

ManufacturingInventory

Classifications

Balance Sheet of a Manufacturer

RawMaterials

FinishedGoods

Goods inProcess

C 5

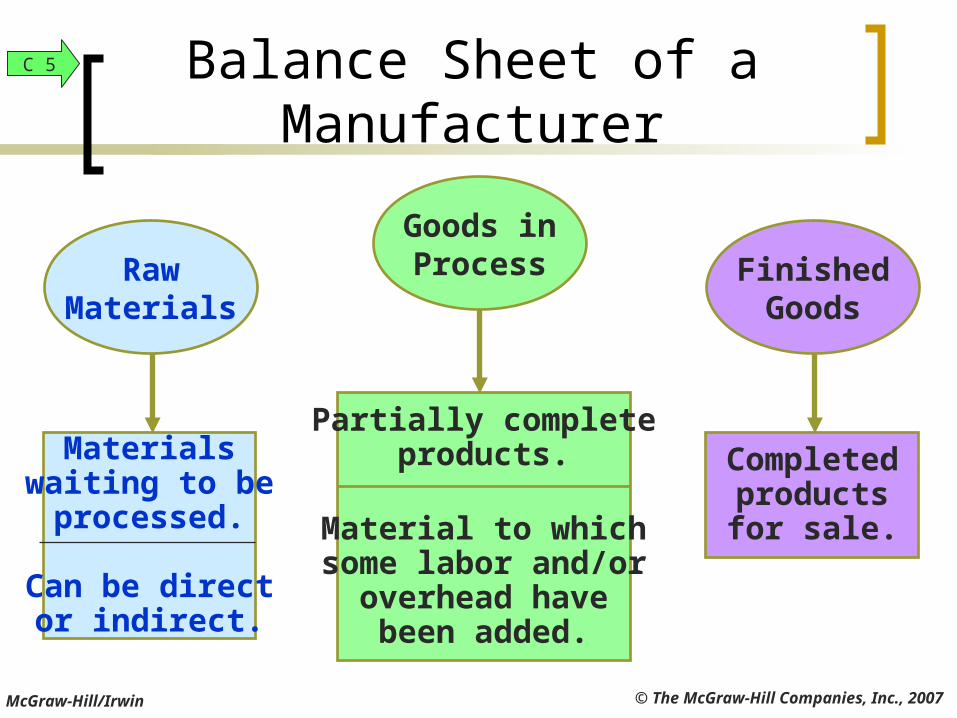

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Completedproductsfor sale.

Materialswaiting to beprocessed.

Can be director indirect.

Partially completeproducts.

Material to whichsome labor and/or

overhead havebeen added.

Balance Sheet of a Manufacturer

RawMaterials

FinishedGoods

Goods inProcess

C 5

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

MERCHANDISER

Current Assets Cash Receivables Merchandise

Inventory

MANUFACTURER

Current Assets Cash Receivables Inventories

Raw MaterialsGoods in ProcessFinished Goods

The only difference is inventory.

Balance Sheet of a Manufacturer

C 5

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Beginning Merchandise

Inventory

Beginning Finished Goods

Inventory

Cost of Goods Purchased

Cost of GoodsManufactured

Ending Merchandise

Inventory

EndingFinished Goods

Inventory

Cost of Goods Sold

Merchandiser Manufacturer

+

_

+

==

_

The major difference

Income Statement of a Manufacturer Exh.

18-11

P1

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Manufacturing Company

Cost of goods sold: Beg. finished goods inv. 14,200$ + Cost of goods manufactured 234,150 = Goods available for sale 248,350$ - Ending finished goods inventory (12,100) = Cost of goods sold 236,250$

Merchandising Company

Cost of goods sold: Beg. merchandise inventory 14,200$ + Purchases 234,150 = Goods available for sale 248,350$ - Ending merchandise inventory (12,100) = Cost of goods sold 236,250$

Cost of goods sold for manufacturers differs only slightly from cost of goods sold for merchandisers.

Income Statement of a Manufacturer Exh.

18-12

P1

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Direct Materials

Materials that are separately and readily traced to a particular product.

Direct Materials

Materials that are separately and readily traced to a particular product.

Example:Steel used tomanufacture

the automobile.

Example:Steel used tomanufacture

the automobile.

Income Statement of a Manufacturer

P1

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Direct Labor

Labor costs that are separately and readily traced to finished product.

Direct Labor

Labor costs that are separately and readily traced to finished product.

Example:Wages paid to an

automobile assemblyworker.

Example:Wages paid to an

automobile assemblyworker.

Income Statement of a Manufacturer

P1

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Factory Overhead

All manufacturing costs exceptdirect material and direct labor

Factory costs that cannot beseparately or readily traced directly to

products.

Factory Overhead

All manufacturing costs exceptdirect material and direct labor

Factory costs that cannot beseparately or readily traced directly to

products.Examples:

Indirect labor – maintenanceIndirect material – cleaning supplies

Factory utility costsSupervisory costs

Income Statement of a Manufacturer

P1

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

DirectMaterial

DirectLabor

ManufacturingOverhead

PrimeCost

ConversionCost

Manufacturing costs are oftencombined as follows:

Income Statement of a Manufacturer

P1

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Finished GoodsBeginning Inventory

Cost of GoodsManufactured

FinishedGoodsEnding

Inventory

RawMaterials

BeginningInventory

RawMaterials

Purchases

Raw MaterialsEnding Inventory

Costof

GoodsSold

Goods in ProcessBeginning Inventory

Direct Labor

FactoryOverhead

Raw MaterialsUsed

Sales activityProduction activityMaterialsactivity

Flow of Manufacturing Activities

Goods in ProcessEnding Inventory

Exh. 18-15

C 6

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

Summarizes the types and amounts of costsIncurred in a company’s manufacturing process.

Direct Materials Used + Direct Labor + Factory Overhead = Total Manufacturing Costs + Beginning Work in Process – Ending Work in Process = Cost of Goods Manufactured

Manufacturing StatementP2

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2008

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Exh. 18-16

P2

Manufacturing Statement

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2008

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Exh. 18-16

Computation of Cost of Direct Material Used

Beginning raw materials inventory 8,000$

Add: Purchases of raw materials 86,500

Cost of raw materials available for use 94,500$

Deduct: Ending raw materials inventory 9,000

Cost of direct materials used in production 85,500$

P2

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2008

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Include all direct labor costs incurred during the

current period.

Exh. 18-16

P2

Manufacturing Statement

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2008

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Manufacturing Statement Exh. 18-16

Computation of Total Manufacturing Overhead

Indirect labor 9,000$

Factory supervision 6,000

Factory utilities 2,600

Property taxes, factory building 1,900

Factory supplies used 600

Factory insurance expired 1,100

Depreciation, building and equipment 5,300

Other factory overhead 3,500

Total factory overhead costs 30,000$

P2

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2008

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Beginning work in process inventory is carried over from the

prior period.

Exh. 18-16

P2

Manufacturing Statement

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

ROCKY MOUNTAIN BIKES

Manufacturing Statement

For Year Ended December 31, 2008

Direct materials used in production 85,500$

Direct labor 60,000

Total factory overhead costs 30,000

Total manufacturing costs for the period 175,500$

Add: Beginning goods in process inventory 2,500

Total cost of goods in process 178,000$

Deduct: Ending goods in process inventory 7,500

Cost of goods manufactured 170,500$

Ending work in process inventory contains the cost of unfinished

goods, and is reported in the current assets section of the balance sheet.

Exh. 18-16

P2

Manufacturing Statement

© The McGraw-Hill Companies, Inc., 2007McGraw-Hill/Irwin

End of Chapter 18