Foreword · State of Food and Agriculture in Syria 2010 I Foreword The Agricultural and Food...

427

Transcript of Foreword · State of Food and Agriculture in Syria 2010 I Foreword The Agricultural and Food...

State of Food and Agriculture in Syria 2010

I

Foreword

The Agricultural and Food Policies Division (AFPD) of the National Agricultural Policy

Center (NAPC), which belongs to the Ministry of Agriculture and Agrarian Reform

(MAAR), is pleased to publish the fourth issue of its periodical report, the “State of Food

and Agriculture in Syria (SOFAS) 2010”. This report gives an idea about the current

situation and main issues characterizing the agricultural development in Syria. Therefore, it

is considered as one of the main outputs of the NAPC.

Consequently, in recognition of the significant role of the agricultural sector in Syria, the

NAPC issues periodically the SOFAS to provide policy makers, researchers and

stakeholders with an updated review of agricultural issues and related information and to

contribute to the implementation of the “Social Market Economy (SME)”. This edition of

the SOFAS focuses on the analysis of the data related to agriculture, agro-industries and

food security over the 1999-2009 period. In addition, it includes some important statistics

and policy issues related to 2010. Hence, it was called SOFAS 2010.

The SOFAS 2010 was accomplished by the staff of the AFPD: Mr Samir Jrad, chief, Ms

Basima Atieh, deputy chief, Mr Mouzad Karkout, Mr Fayez Mansour, Mr Nouman Al-

Amouri, Mr Mohanad Rezmi, Mrs Najla Wardi, and Mrs Basima Al-Halabi. In addition,

Mr Bashar Nahas of the Information and Communication Division (ICD) of the NAPC and

Ms Hajar Baghasa of the Tade Policy Division (TPD) of the NAPC contributed to the

accomplishment of Chapter 6 (food security). Mr Mahmoud Babili of the TPD of the

NAPC and Ms Hajar Baghsa offered additionally international trade data. The contribution

of the TPD, which provided trade data, and the ICD, which supplied data and was involved

in the finalization of the present publication, has also to be acknowledged. Moreover, the

report was reviewed by Mr Samir Jrad and Mr Haitham Al-Ashkar, Deputy Director of the

NAPC for studies, to produce a sound report. Additionally, coordination, orientation and

general supervision of the various phases of this activity were performed by Mr Atieh El-

Hindi, Director of the NAPC, to add important comments and to accomplish a coherent

publication.

The NAPC also wishes to express a deep gratitude to the departments and staff of the

MAAR, the Ministry of Economy and Trade (MET), the Central Bureau of Statistics

State of Food and Agriculture in Syria 2010

II

(CBS) and all the other institutions, which made this periodical possible by facilitating

access to data and information. Besides, the NAPC is especially thankful for the

contribution of the “Arab Fund for Economic and Social Development (AFESD)”, which

enriched this bulletin by its financial assistance to the NAPC, which was used to conduct

some studies.

A special gratefulness is directed as well to Mr. Dr. Adel Safar, the Minister of the MAAR,

for both his due attention and his instructions to put the NAPC activities into practice, and

to Mr. Dr. Nabi Rasheed Mohamed, Deputy Minister of the MAAR, for his facilities to

enable performing the tasks of the NAPC.

Finally, the NAPC will be grateful when comments, opinions and suggestions are

submitted to www.napcsyr.org ([email protected]) to improve this circular.

State of Food and Agriculture in Syria 2010

Table of Contents

Foreword ............................................................................................................................. I Abbreviations and Acronyms (A&A) ........................................................................... VII Brief Summary and Report Organization .................................................................... XI Chapter 1 – Country Development Opportunities for Agriculture and Agro-Industries ............................................................................................................................ 1

1.1. Geography and location ............................................................................................ 1 1.2. Climatic conditions.................................................................................................... 2 1.3. Natural resources ...................................................................................................... 4

1.3.1. Land...................................................................................................................... 4 1.3.2. Water .................................................................................................................... 7 1.3.3. Steppes and pastures ............................................................................................ 9 1.3.4. Forestry .............................................................................................................. 10 1.3.5. Fishery................................................................................................................ 11 1.3.6. Quarrying industries .......................................................................................... 13

1.4. Human resources ..................................................................................................... 13 1.5. Agricultural intermediate consumption ................................................................ 15 1.6. Agricultural supporting services ........................................................................... 18

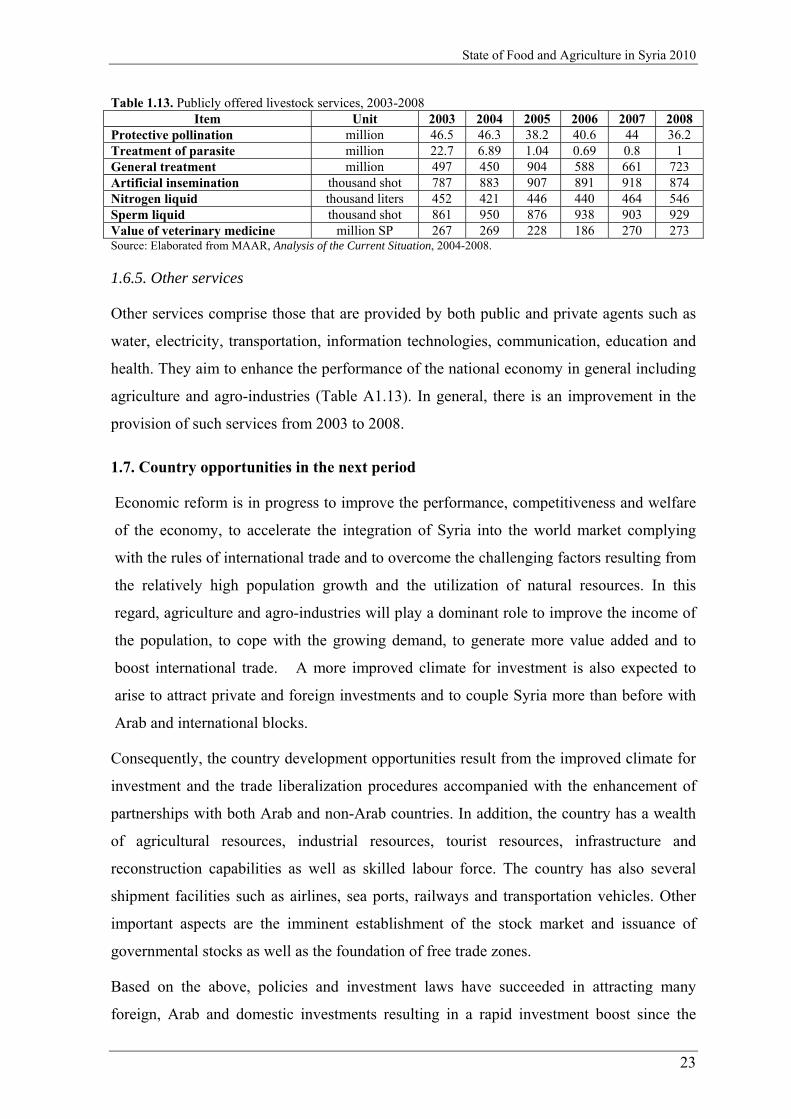

1.6.1. Agricultural credits ............................................................................................ 18 1.6.2. Agricultural scientific research .......................................................................... 20 1.6.3. Agricultural extension, training and education ................................................. 21 1.6.4. Veterinary and livestock services ....................................................................... 22 1.6.5. Other services..................................................................................................... 23

1.7. Country opportunities in the next period ............................................................. 23 Chapter 2 – Agriculture in the national economy ......................................................... 25

2.1. Contribution of agriculture to the gross output ................................................... 25 2.2. Contribution of agriculture to production inputs ................................................ 26 2.3. Contribution of agriculture to the gross domestic product ................................. 28 2.4. Contribution of agriculture to employment and income ..................................... 30 2.5. Contribution of agriculture to trade ..................................................................... 31 2.6. Contribution of agriculture to investment ............................................................ 32 2.7. Backward and forward linkages of agriculture ................................................... 34 2.8. Factors constraining the performance of the agricultural sector ....................... 36 2.9. Agricultural sector in the next period ................................................................... 37

Chapter 3 – Agricultural and food strategies and policies ........................................... 39 3.1. Strategies .................................................................................................................. 39

3.1.1. SAS and the 10th FYP ......................................................................................... 40 3.1.2. STI and the 10th FYP .......................................................................................... 42 3.1.3. Nutrition strategy (NS) ....................................................................................... 43 3.1.4. Investment strategy............................................................................................. 44 3.1.5. Social Market Economy (SME) .......................................................................... 44

3.2. General objectives of agricultural policies ............................................................ 45 3.3. Macro and agricultural policies ............................................................................. 47

3.3.1. Monetary and fiscal policies .............................................................................. 47 3.3.2. Trade policy ....................................................................................................... 52

State of Food and Agriculture in Syria 2010

3.3.3. Investment policy ............................................................................................... 54 3.4. Other agricultural policies ..................................................................................... 59

3.4.1. Planning and production policies ...................................................................... 59 3.4.2. Pricing and marketing policies .......................................................................... 63 3.4.3. Policies related to supporting services .............................................................. 65 3.4.4. Policies related to agricultural production inputs ......................................... 66 3.4.5. Policies related to agricultural resources ......................................................... 68

3.4.5.1. Land resources ............................................................................................ 68 3.4.5.2. Water resources .......................................................................................... 70 3.4.5.3. Natural pastures and Al-Badia (Syrian Steppe) ......................................... 72 3.4.5.4. Forestry ....................................................................................................... 73 3.4.5.5 Fishery ......................................................................................................... 74 3.4.5.6. Human resources ........................................................................................ 74

3.5. Agro-industrial policies .......................................................................................... 75 3.6. Policies related to food security ............................................................................. 77 3.7. Support policies ....................................................................................................... 80 3.8. Policies related to food quality and safety ............................................................ 81 3.9. Agricultural and food policies in the next period ................................................ 82

Chapter 4 – Agricultural production ............................................................................. 85 4.1. Crop production ...................................................................................................... 85

4.1.1. Development of some economic aggregates related to crop production ........... 87 4.1.2. Cereals ............................................................................................................... 91 4.1.3. Dry legumes ....................................................................................................... 94 4.1.4. Grazing crops (green fodder) ............................................................................ 97 4.1.5. Industrial crops .................................................................................................. 98 4.1.6. Vegetables ........................................................................................................ 101 4.1.7. Fruit trees......................................................................................................... 103

4.2. Livestock production ............................................................................................ 107 4.2.1. Development of the number of livestock .......................................................... 107 4.2.2. Development of the livestock productivity ....................................................... 108 4.2.3. Development of the production of livestock products ...................................... 109 4.2.4. Value of the livestock production ..................................................................... 110

4.3. Costs of the agricultural produce ........................................................................ 112 4.4. Prices of the agricultural produce ....................................................................... 116 4.5. Agricultural trade and markets ........................................................................... 118 4.6. Factors constraining crop production ................................................................. 123 4.7. Factors constraining livestock production.......................................................... 124 4.8. Agricultural production in the next period ........................................................ 125

Chapter 5 – Agro-industries ......................................................................................... 127 5.1. Contribution of agro-industries to the gross output .......................................... 128 5.2. Contribution of agro-industries to the net domestic product ........................... 132 5.3. Contribution of agro-industries to investment and employment ..................... 134 5.4. Contribution of agro-industries to trade ............................................................ 137 5.5. Prices of agro-industrial products ....................................................................... 138 5.6. Enabling environments for competitive agro-industries ................................... 138 5.7. The need for adopting inclusive business models for small holders ................. 141

5.7.1. Background ...................................................................................................... 141 5.7.2. Important definitions ........................................................................................ 142 5.7.3. A business model defined ................................................................................. 142 5.7.4. Types of business models ................................................................................. 143

State of Food and Agriculture in Syria 2010

5.7.5. Adjusting business models in favor of small holders ....................................... 146 5.7.6. Considerations to work successfully with small holders ................................. 146

5.8. Agro-industries in the next period ....................................................................... 147 Chapter 6 – Food security ............................................................................................. 149

6.1. Food security definition and measurement......................................................... 149 6.2. Food availability .................................................................................................... 150

6.2.1. Aggregate food availabilities ........................................................................... 150 6.2.2. Aggregate per capita food availabilities .......................................................... 153

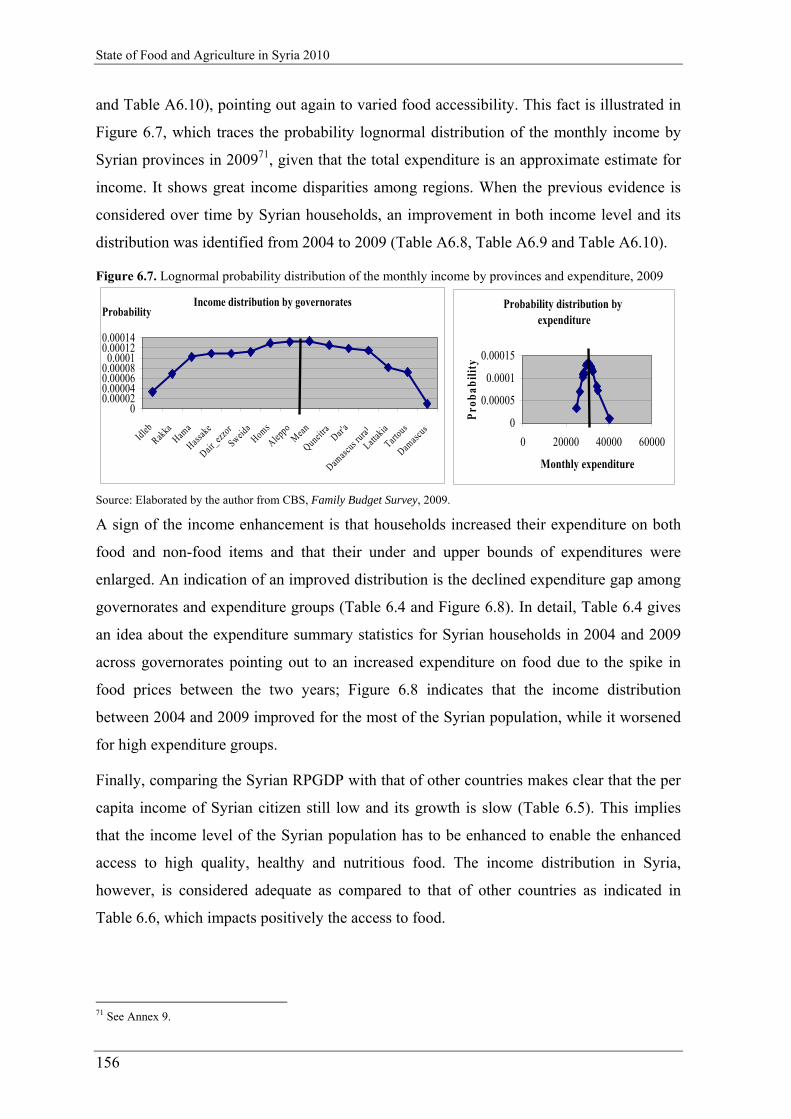

6.3. Access to food ......................................................................................................... 154 6.4. Stability of food supplies and access .................................................................... 158 6.5. Aggregate per capita daily food utilization ......................................................... 159

6.5.1. Background ...................................................................................................... 159 6.5.2. Methodological guidelines ............................................................................... 159 6.5.3. Expenditure on food ......................................................................................... 160 6.5.4. Calorie intakes ................................................................................................. 160 6.5.5. Protein intakes ................................................................................................. 162 6.5.6. Fat intakes ........................................................................................................ 163 6.5.7. Carbohydrate intakes ....................................................................................... 164 6.5.8. Vitamin C intakes ............................................................................................. 165 6.5.9. Vitamin A intakes ............................................................................................. 167 6.5.10. Vitamin B1 intakes ......................................................................................... 168 6.5.11. Vitamin B2 intakes ......................................................................................... 169 6.5.12. Vitamin B6 intakes ......................................................................................... 170 6.5.13. Vitamin B12 intakes ....................................................................................... 171 6.5.14. Iron intakes ..................................................................................................... 173 6.5.15. Iodine intakes ................................................................................................. 174 6.5.16. Calcium intakes .............................................................................................. 175

6.6. Food safety and quality ......................................................................................... 176 6.7. Undernourishment and malnutrition in the total population ........................... 177

Special Issue: National Programme for Food Security .............................................. 181 II.1. General overview.................................................................................................. 181 II.2. Background and justification .............................................................................. 182 II.3. The need for a coherent, cost and time bounded NPFS ................................... 185 II.4. NPFS linked to other national and international food security related initiatives ....................................................................................................................... 186 II.5. Objectives and framework of the NPFS ............................................................ 187 II.6. Prioritization criterions, beneficiaries and cost ................................................ 188

Annexes ........................................................................................................................... 190 References and data sources ......................................................................................... 406

State of Food and Agriculture in Syria 2010

VII

Abbreviations and Acronyms (A&A)

A&A Abbreviations and Acronyms AFPD Agricultural and Food Policies Division AFESD Arab Fund for Economic and Social Development AASA Annual Agricultural Statistical Abstract ACH Average Change AAGR Average Annual Growth Rate AGR Annual Growth Rate AOAD Arab Organization for Agricultural Development ASA Annual Statistical Abstract ASR Agricultural Scientific Research ACB Agricultural Cooperative Bank AED Agricultural Extension Directorate AIDS Acquired Immunodeficiency Syndrome AAPP Annual Agricultural Production Plan APSF Agricultural Production Supporting Fund AIP Agro-industrial Production AIGO Agro-industrial Gross Output AINDP Agro-industrial Net Domestic Product ACSAD Arab Center for Studying Agricultural Dry Areas BC Building and Construction BOTS Building, Operating and Transporting System BCI Business Competitiveness Index CBS Central Bureau of Statistics CF Core Functions CA Central Administration CPI Consumer Price Index CV Coefficient of Variation CR Concentration Ratio CIP Competitive Industrial Performance CCI Current Competitiveness Index EPF Export Promotion Fund EPC Export Promotion Commission ERS Economic Research Service EU European Union FBS Food Balance Sheet FAO Food and Agriculture organization of the United Nations FAOSTAT Food and Agriculture organization of the United Nations Statistics FBS Food Balance Sheet FI Finance and Insurance FYP Five Year Plan FTA Free Trade Agreement FDI Foreign Direct Investment FSCN Food Supply Chain Network FBSD Family Budget Survey Data GO Gross Output GAFTA Great Arab Free Trade Area GDP Gross Domestic Product GOS Government of Syria GESM General Establishment for Seed Multiplication GOT General Organization of Tobacco GCASR General Commission for Agricultural Scientific Research

State of Food and Agriculture in Syria 2010

VIII

GEF General Establishment for Fodder GECTP General Establishment for Cereal Trade and Processing GCG General Commission for Al-Ghab Development GCGMD General Commission for Al-Ghab Management and Development GPU General Peasant Union GIS Geographical Information System GECG General Establishment for Consumption Goods GERT General Establishment for Retail Trade GEM General Establishment for Military GAP Good Agricultural Practices GOFI General Organization for Food Industries GOSI General Organization for Sugar Industries GOTI General Organization for Textile Industries GOCGW General Organization for Cotton Ginning and Weaving GCMDB General Commission for the Management and Development of Al-Badia GCDFR General Commission for the Development of Fishery Resources GOEI General Organization for Engineering Industries GOCI General Organization for Chemical Industries GCI Global Competitiveness Index g gram HACCP Hazard Analysis Critical Control Points HIV Human Immunodeficiency Virus ha hectare ICD Information and Communication Division IPM Integrated Pest Control Management IC Investment Commission IPR Intellectual Property Rights IDR Import Dependency Ratio IFAD International Fund for Agricultural Development ICE Italian Trade Commission I.E International Equivalent JAESA Joint Arab Economic and Social Act kg kilogram kcal kilocalorie km kilometer mkwh Million kilo watt hour MAAR Ministry of Agriculture and Agrarian Reform MET Ministry of Economy and Trade MI Ministry of Irrigation MOI Ministry of Industry Max Maximum MDGs Millennium Development Goals Min Minimum MICS Multiple Indicator Cluster Survey MM Mining and Manufacturing MOH Ministry of Health ME Monitoring and Evaluation mg milligram microg microgram NAPC National Agricultural Policy Center NPFS National Programme for Food Security NS Nutrition Strategy NP Number of Trading Partners NDP Net Domestic Product NDPTI Net Domestic Product of the Transformation Industries NGO Non-government Organization OR Organizational Results PE Production Establishments PAM Policy Analysis Matrix R and D Research and Development

State of Food and Agriculture in Syria 2010

IX

RCA Revealed Comparative Advantage RCAI Revealed Comparative Advantage Indicator REE Real Estate Establishment RUV Relative Unit Value RPGDP Real per Capita Gross Domestic Product RRA Rapid Rural Appraisal RE Retinol Equivalent SAR Syrian Arab Republic SOFAS State of Food and Agriculture in Syria SME Social Market Economy SG Syrian Government SPC State Planning Commission SADS Syrian Agricultural Development Strategy SAS Syrian Agricultural Strategy SP Syrian Pound STI Strategy of the Transformation Industries SSME Strategy of the Social Market Economy SO Strategic Objectives SCE Supreme Council for Export SIO Speed Intervention Office SIPA Syrian Intellectual Property Rights Association SCM Supply Chain Management SSR Self-Sufficiency Ratio STDEV Standard Deviation SOFI State of Food Insecurity SAM Social Accounting Matrix SEBC Syrian European Business Center SMSE Small-Medium Sized Enterprises TPD Trade Policy Division TCS Transport, Communication and Storage USD or US$ United States Dollar UNDAF United Nations Development Assistance Framework UNDP United Nations Development Programme UNFPA United Nations Food Programme Assistance UAE United Arab Emirate USA United States of America USDA United States Department of Agriculture UNICEF United Nations Children’ Fund UNIDO United Nations Industrial Development Organization VAT Value Added Tax VOCP Value of Crop Production VOAP Value of Agricultural Production WFS World Food Summit WIPO World Intellectual Property Rights Organization WTO World Trade Organization WHO World Health Organization WB World Bank WFP World Food Programme

State of Food and Agriculture in Syria 2010

XI

Brief Summary and Report Organization

Syria is still undergoing the reform process to modernize and develop its economy

focusing on its structural adjustment and its integration with the world economy. This will

strengthen the overall economic and social development in Syria, accelerate growth and

boost the performance of the economy complying with the needs of the economic and

social situation of the country.

The aforementioned focus also applies to the agricultural development in Syria because it

is considered as a major pillar of the sustainable development. It focuses on both the

development of human and the accomplishment of an agricultural progress that aligns with

the relatively high population growth and the increasing demand. This is possible because

Syria is characterized by a vagary of agro-climates that enables the country to produce all

agricultural products spreading out in the Mediterranean and to diversify both crops and

livestock in line with the demand for domestic consumption, processing and export. In

addition, it enhances employment and income generation and contributes soundly to food

security, trade and support of the other sectors of the economy. The aforementioned central

roles of Agriculture can be explained by its sound contribution to some economic

aggregates over the 1999-2009 period. Over this era, its share amounted to 17-23% of the

total gross output (GO) at current prices, 17-22% of the total GO at constant prices1, 19-

25% of the gross domestic product (GDP) at current prices, 18-26% of the GDP at constant

prices, 17-29% of the labour force, 9.1-20.5% of total trade, 6.6-20.3% of total exports,

11.3-20.6% of total imports, 7.8-16.2% of total investment at current prices and 8.2-16.4%

of total investment at constant prices. This indicates that the agricultural sector didn’t

receive the investment it deserves in line with its contribution to the gross domestic

product. This epoch was also characterized by the following:

The private agricultural investment was the major driving force of agricultural

activities; its donation accounted for 98.5% of total agricultural production,

1 Constant prices of 2000.

State of Food and Agriculture in Syria 2010

XII

whereas the share of the joint-sector was 1% and that of the public sector was

0.5%2.

The cultivable land witnessed a slight growth due to the reclamation of

mountainous and rocky areas, which were planted with suitable field crops and

fruit trees from environmental point of view. The reclamation activities were

constraint by the limited land resources.

A good progress was attained in the field of agricultural production and food

security in spite of the droughts and water deficits.

In-depth, this report is divided into two parts. The first section focuses on the assessment of

the state of food and agriculture in Syria, while the second piece summarizes the main

goals and components of the proposed National Programme for Food Security (NPFS). The

former consists of six chapters.

The first chapter gives an idea about the country development opportunities for agriculture

and agro-industries. They comprise the availability of natural resources (land, water,

pastures, forests and fishery), human resources, supporting services for agriculture and

agro-industries, coordination between both the public and private sectors to improve

economic performance, infrastructure, and trade and investment commitments with other

countries at both regional and international levels. The figures showed that a reasonable

improvement was accomplished in relation to the utilization of natural resources and

supply of supporting services in spite of the challenges and droughts that faced the

agricultural sector during the 2006-2009 period. From 1999 to 2009, the cultivable land

increased from 5,998 thousand hectares3 to 6,013 thousand ha and the irrigated land from

1,186 thousand ha to 1,238 thousand ha, respectively; the land productivity augmented

from SP447.4 thousand/ha in 2000 to SP57.1 thousand/ha in 2009; the land under modern

irrigation amplified from 110 thousand ha in 2001 to 282 thousand ha in 2009.

Chapter two traces the overall role of the agricultural sector in the national economy

relying on the analysis of several economic aggregates such as GO, production inputs

(intermediate consumption), GDP, trade and investment, from 2000 to 2009. Over this

period, agricultural GO enlarged from SP341 billion to SP778 billion at current prices and

to SP394 billion at constant prices of 2000, agricultural intermediate consumption from

2 Investment of cooperatives is privately managed. 3 Hectare = ha. 4 US$1.0 = SP45.0. SP: Syrian Pound.

State of Food and Agriculture in Syria 2010

XIII

SP117 billion to SP212 billion at current prices and to SP129 billion at constant prices of

2000, agricultural GDP from SP224 billion to SP566 billion at current prices and to SP265

billion at constant prices of 2000, and agricultural investment5 from SP24.4 billion to

SP39.5 billion at current prices and to SP26.9 billion at constant prices of 2000,

respectively; from 2002 to 2009, total agricultural trade augmented from US$2,368 million

to US$2,885 million, total agricultural imports from US$1,034 million to US$1,423

million, and total agricultural exports from US$1,333 million to US$1,462 million,

respectively. As a consequence, from 2000 to 2009, the indicator of economic efficiency of

agriculture6 improved from 0.85 to 1.17 at current prices and to 0.97 at constant prices of

2000 and that of return to agricultural investment7 from 916% to 1,435% at current prices

and to 985% at constant prices of 2000, respectively.

Strengthening the role of agriculture in the national economy and enhancing agricultural

production, agro-industries and food security rely heavily on the strategies and policies

governing these areas. Therefore, chapter three addresses the latter at both macro and

micro levels and those underlying regulations.

Chapter four presents in-depth analysis of the development of agricultural production from

1999 to 2009 using various measures. These indicators include the cropped area, level of

production, yield, value of agricultural production, prices of agricultural products, costs of

agricultural products and agricultural trade. From 1999 to 2009, the cropped area decreased

from 4,633 thousand ha to 4,499 thousand ha, the irrigated cropped area increased from

1,283 thousand ha to 1,391 thousand ha and the rain-fed cropped area declined from 3,350

thousand ha to 3,108 thousand ha, respectively. At the same time, agricultural production

enhanced during the same period. From 1999 to 2009, crop production (plant production)8

augmented from 10,673 thousand tonnes to 13,965 thousand tonnes indicating an increase

in the average yield, meat production from 348 thousand tonnes to 459 thousand tonnes,

and milk production from 1,656 thousand tonnes to 2,409 thousand tonnes, respectively;

from 2000 to 2009, agricultural GO enlarged from SP337 billion to SP778 billion at

current prices and to SP394 billion at constant prices of 2000, the value of crop production

from SP215 billion to SP483 billion at current prices and to SP248 billion at constant

prices of 2000, and the value of livestock production (animal production) from SP122 5 Includes both investment related to the MAAR and that related to the Ministry of Irrigation (MI). 6 Indicator of economic efficiency of agriculture = share of agriculture in GDP /share of agriculture in work force. 7 Indicator of return to agricultural investment = agricultural GDP/agricultural investment * 100. 8 Crop production comprises field crops, vegetables and fruits.

State of Food and Agriculture in Syria 2010

XIV

billion to SP296 billion at current prices and to SP146 billion at constant prices of 2000,

respectively.

Chapter five reports the development of agro-industries from 1999 to 2009 relying on some

selected economic aggregates at current prices such as GO, net GDP, investment,

employment, trade and prices of processed products. From 2001 to 2009, the agro-

industrial GO increased from SP179 billion to SP280 billion and the agro-industrial net

GDP from SP45 billion to SP94 billion, respectively.

Chapter six focuses on the assessment of achieving the four food security dimensions

agreed upon internationally compared with the progress made in those in other countries

and the compliance to nutritional daily requirements per capita. These pillars comprise

food availability, access to food, stability of supplies and access, and food utilization, food

quality and food safety. The data from 1999 to 2009 showed that there was a reasonable

improvement in attaining these measures, but, there was still a deficiency in the acquisition

of some micro nutrients. Comparing the average of (1999-2001) with the average of (2006-

2008), the Syrian calorie intake increased from 3,056 kcal/capita/day to 3,116

kcal/capita/day and protein intake from 73.9 g/capita/day to 82.1 g/capita/day, while that of

fat decreased from 106.8 g/capita/day to 97.5 g/capita/day, respectively9. In this regard, it’s

worthy to note that the aforementioned estimates were calculated relying on the data of the

Syrian Food Balance Sheet (FBS) prepared by the MAAR. These values will be higher

when the actual consumption data are considered.

Finally, to strengthen the food security situation of the country and to target the less

privileged groups of the Syrian population in the context of reducing poverty, the Syrian

Government proposed a recent NPFS and approved it to be included in the 11th Tenth Five

Year Plan (FYP), 2011-2015 and the 12th FYP. This programme is the subject of the

special issue of this report.

9 kcal = kilocalorie; g = gram.

State of Food and Agriculture in Syria 2010

XV

Part I

Assessment of the State of Food and Agriculture

State of Food and Agriculture in Syria 2010

1

Chapter 1 – Country Development Opportunities for Agriculture and Agro-Industries

Seeking to enhance the utilization of resources related to agriculture and agro-industries,

the Syrian Government (SG) provides both supporting services and public investment. At

the same time, it promotes private investment to improve the performance of both

agricultural production, comprising both crops and livestock, and agro-processing. This is

in line with the ultimate goals of the sustainable development process currently going on in

Syria: assuring sufficient food complying with the needs of both food security and food

industry, creating new jobs for the labour force and producing food surplus for export. This

chapter contributes to the aforementioned subjects by giving an idea about geography and

location as well as the development of climatic conditions, agricultural resources, some

policy issues, production inputs, revenue streams and country development opportunities to

enhance agricultural and agro-industrial activities. This analysis focuses on the 1999-2009

period.

1.1. Geography and location

Syria is a Mediterranean country (Figure A1.1)10. It can be divided into four distinct

geographic regions: the coastal region, the mountainous region, the interior region and Al-

Badia. The coastal region, lying between the mountains and the sea, is characterized by a

high rate of relative humidity, heavy rainfall in winter and moderate temperatures in

summer; in the mountainous region, which includes the mountains stretching from north to

south in the western part of the country, rainfall may exceed 1,000 mm and the climate in

summer is moderate; the interior region, composed of the interior plains and located to the

east of the mountainous region, is distinguished by rainy winters and hot and dry summers

with considerable differences between the maximum and minimum intra-day temperatures;

and finally, the Al-Badia, in the south and east, consists of semi desert plains where rainfall

in winter is low and the summers are dry.

10 A denotes annex.

State of Food and Agriculture in Syria 2010

2

Syria can also be classified into: the northeastern region, including Al-Hassake, Al-

Raqqa11, Dair-ezzor, Idleb and Aleppo, the coastal region, comprising Lattakia and

Tartous, the middle region, incorporating Homs and Hama, and the southern region,

consisting of Damascus, Dar'a, Sweida and Quneitra12 (Figure A1.1).

1.2. Climatic conditions

Syria is a characterized by Mediterranean climate of rainy winters and hot summers

separated by two short transitional seasons (autumn and spring). It can be divided into five

stabilization zones, which are referred to different quantities of rainfall, diverse crops and

varied land altitudes (Figure A1.1 and Box A1.1).

From the rainfall point of view, the country can also be clustered as follows: it

regularly snows on all the regions exceeding 1,500 m above sea level;

snows and rains on the regions which their heights are between 800 and 1,500 m

above sea level;

rains on the regions their altitudes less than 800 m above sea level, but rarely snows

it;

rains in little amounts in Al-Badia (Syrian steppe).

Hence, the level of rainfall, its timing and its distribution affect considerably the

performance of both agricultural production and agricultural activities. This is especially

relevant for Syria because rain-fed agriculture accounted for about 71% of the cultivated

area in 2009.

In detail, Figure 1.1 indicates the development of the magnitude of the annual precipitation

from 1999 to 2008 considering the various stabilization zones (Table A1.1). It shows that

the amount of rain increased to reach its peak in 2003, then decreased thereafter to attain its

lowest level in 2008 because of the severe droughts over the 2006-2008 period. This of

course impacted negatively the performance of Syrian Agriculture and as a consequence

the livelihood of the rural population. The figure also implies that the First Ecological Zone

acquires the highest precipitation rate and subsequently the other zones.

The distribution of rain also varies across governorates and regions (southern, middle,

coastal and northern areas), Figure 1.2 and Table A1.2. Figure 1.2 points out to the same

11 Can be written with Al or without. 12 Can be written with Al or without.

State of Food and Agriculture in Syria 2010

3

trend as shown in Figure 1.1 and clarifies that the coastal and middle areas receive the

highest amount of precipitation, whereas the other regions obtain the lowest level.

Figure 1.1. Development of the annual rainfall by stabilization zones, 1999-2008 (mm/year)

0

200

400

600

800

1,000

1,200

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

mm

Average

First Ecological Zone

Second Ecological Zone

Third Ecological Zone

Fourth Ecological Zone

Fifth Ecological Zone

Source: Elaborated from NAPC database. mm: millimeter.

Figure 1.2. Development of the annual rainfall by regions, 1999-2008 (mm/year)

0

500

1,000

1,500

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

mm

Southern area

Middle area

Coastal area

Northern area

Source: Elaborated from NAPC database. mm: millimeter.

As indicated above, Syria had a declining rate of rainfall from 2003 to 2008 because of the

repeated droughts, which influenced adversely both crop production, especially the rain-fed

crops, and the groundwater, which is used for irrigated agriculture. Therefore, the

Government has established the Project of Artificial Rainfall, which induced the amount of

rain by 6-16%13. In addition, it has initiated a Drought Response Plan since 2009 in

collaboration with the United Nations to mitigate the drought impact that has started since

2006. While the 2007-2008 droughts were very severe and had a wider geographical reach,

the current droughts have again affected a population that already suffering from the

impacts of previous drought spells. Some 1.3 million inhabitants of eastern Syria have been

affected by this disaster, out of which 803,000 have lost almost all of their livelihoods and

faced extreme hardship. These families are not able to sustain or restore their livelihood

without emergence support including food aid, farming inputs and animal feeds,

13 MAAR, Directorate of Artificial Rainfall.

State of Food and Agriculture in Syria 2010

4

supplemented by other types of assistance14. Concurrently with the drought spells, Syria is

subject to temperature variations, which in turn influence unfavorably Syrian agriculture15.

1.3. Natural resources

1.3.1. Land

Land is a natural fortune upon which agricultural activities depend. However, land

available for agriculture is actually rare and limited especially in developing countries

where it is not optimally exploited, is overpopulated and is being urbanized. Hence, many

countries are seeking to improve the land use and productivity so that agricultural

production is optimized and its cost per unit of area is reduced.

In relation to Syria, the SG gives due attention to optimize the utilization of land resources.

Therefore, it tries both to expand the cultivable land horizontally through reclamation and

rehabilitation activities and to increase the productivity of land (vertical utilization) by

encouraging the agricultural scientific research (ASR). The ASR focuses on the

development of suitable, high yielding and drought resisting varieties, which are

diversified by regions, and the adoption of appropriate crop rotations. Both horizontal and

vertical expansions (utilization) are important, but, the latter ranks first because of the

limited availability of land resources. The aforementioned actions are governed not only by

state strategies and policies but also by its cooperation with regional and international

institutions. In spite of these efforts, the productivity of Syrian land is still low as compared

to that of other countries. Therefore, it is advisable that the coordination with foreign

agencies concentrates on the improvement of the ASR.

In-depth, the area of the Syrian Arab Republic (SAR) amounts to 18,518 thousand ha. It’s

divided into cultivable land, uncultivable land, steppes and pastures, and forests. The

cultivable land comprises both invested and un-invested lands. The invested land consists

of irrigated, rain-fed (non-irrigated) and fallow lands. In 2009, the total area of Syria was

composed of 32.5% cultivable land, 30.6% invested land, 23.4% actually cultivated land,

7.2% fallow land, 1.9% un-invested land, 19.9% uncultivable land, 44.5% steppes and

pastures, and 3.1% forests (Table A1.3). The evolution of its structure is depicted in Figure

1.3 from 1999 to 2009. Figure 1.3 indicates an increase in the contribution of irrigated,

fallow and forest lands and a decrease in the share of the other lands. The cultivable land

14 Syrian Drought Response Plan (2009). 15 Central Bureau of Statistics (CBS), the Annual Statistical Abstract (ASA), various issues.

State of Food and Agriculture in Syria 2010

5

increased from 5,998 thousand ha in 1999 to 6,013 thousand ha in 2009, while the

cultivated land declined from 4,541 thousand ha in 1999 to 4,339 thousand ha in 2009. In

addition, Table 1.1 traces the development of the land use during the 1999-2009 period.

From 2003 to 2009, it showed an upward trend for cultivable, invested and fallow lands

from and a downward trend for the other lands because of the 2006-2009 drought spells.

Figure 1.3. Development of the composition of the land use, 1999-2009 (%)

0%

20%

40%

60%

80%

100%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Forests

Steppes and pastures

Uncultivable land

Un-invested land

Fallow land

Rain-fed land

Irrigated land

Source: Elaborated from the MAAR. The Annual Agricultural Statistical Abstract (AASA). Various issues.

Table 1.1. Evolution of the land use, 1999-2009 (000 ha, %)

Item Average

1999-2001 Average

2003-2005 Average

2007-2009 Change %2003-2009

Change % 1999-2009

AAGR % 1999-2009

Cultivable land 5,964 5,902 6,025 2.1 1.0 0.2 Invested land 5,435 5,522 5,671 2.7 4.3 0.7 Irrigated land 1,221 1,409 1,330 -5.6 8.9 1.4 Rain-fed land 3,324 3,346 3,226 -3.6 -3.0 -0.5 Fallow land 890 768 1,115 45.2 25.3 3.8 Cultivated land 4,546 4,754 4,556 -4.2 0.2 0 Un-invested land 529 380 354 -6.8 -33.0 -6.5 Uncultivable land 3,699 3,729 3,684 -1.2 -0.4 -0.1 Steppes and pastures 8,299 8,293 8,230 -0.8 -0.8 -0.1 Forests 556 594 579 -2.5 4.0 0.7

Source: Elaborated from the MAAR. The AASA. Various issues. AAGR: Average annual growth rate.

Table 1.1 also indicates that rain-fed, un-invested, uncultivable, steppes and pastures lands

declined from 1999 to 2009, while the other lands augmented; this implies that the

Government has succeeded in both conducting the reclamation activities and substituting

the rain-fed lands through irrigated lands. An increased irrigated land leads to higher land

productivity and a relatively enhanced fallow land in correspondence to drought maintains

it by rain-fed land. This productivity relies on several factors such as the level of

production, farming type (irrigated or rain-fed), holding size, soil type, degree of land

degradation, technological stand and the level of provided supporting services16. The

average impact of these determinants on the land productivity and the average area

16 See NAPC, SOFAS 2007, for more details.

State of Food and Agriculture in Syria 2010

6

development per capita are shown in Table 1.2 from 2000 to 2009 (Table A1.4) indicating

an increased productivity and a declined cultivable land per capita.

The aforementioned land use differs across governorates (Table A1.5 and Table A1.6) as

illustrated in Figure 1.4.

Table 1.2. Evolution of the land productivity and the land per capita, 2000-2009

Item Unit Average

2000-2002 Average

2007-2009 Change % 2000-2009

Land productivity 000 SP/ha 50.6 50.9 0.55

Cultivable land per capita ha/person 0.355 0.303 -14.61

Rural cultivable land per capita ha/person 0.711 0.655 -7.91 Source: Elaborated by the Rapporteur. Land productivity = value of crop production at constant prices/cultivated area.

Figure 1.4. Structure of the land use by governorates, 2009 (%)

0%

20%

40%

60%

80%

100%

Forests

Steppes and pastures

Uncultivable land

Cultivable land

Source: Elaborated from the MAAR. The AASA. 2009.

According to Figure 1.4, in 2009, the highest share of cultivable land was achieved in

Quneitra, Hassake and Aleppo, where the highest portion of uncultivable area prevailed in

Dair-Ezzor, Dar,a and Sweida.

Furthermore, land resources are managed by public, cooperative and private sectors (Table

1.3). Table 1.3 shows that the public sector has a minor share in the cultivable land,

whereas the cooperative and private sectors take the lead; the private sector acquires the

highest portion of the cultivable land.

Table 1.3. Evolution of the cultivable land by sectors, 2004-2008 (000 ha, %)

Item Public sector

Cooperative sector

Private sector

Total Share %

Public Cooperative Private 2004 12.0 2,495 3,402 5,909 0.21 42.22 57.57 2005 15.0 2,507 3,412 5,934 0.25 42.25 57.5 2006 1.0 2,515 3,433 5,949 0.01 42.28 57.71 2007 0.8 2,513 3,525 6,039 0.01 41.61 58.38 2008 0.8 2,501 3,521 6,023 0.01 41.52 58.47 Source: Elaborated from the MAAR. The AASA. 2008.

Finally, land use is still subject to the following constraints:

State of Food and Agriculture in Syria 2010

7

The productivity of some parts of the land is decreasing because of fertility

reduction, salinity and contamination resulting from the intensification

programmes. Therefore, these areas have to be rehabilitated.

The un-invested land requires great efforts to be invested, which implies a

challenge for the operations of horizontal development17 and a shift towards

vertical expansion18.

The land is fragmented to the extent that investment and mechanization are

constrained. In spite of this challenge, no serious actions are taken.

A great attention isn’t being given to applying appropriate crop rotations that

maintain soil fertility and improve the competitiveness of Syrian agricultural

products.

1.3.2. Water

Syria is classified internationally among the countries that have meager water resources

(less than 1,000 m3/ person/ year). Therefore, the GOS places high consideration on the

implementation of water-harvesting and water-saving technologies. In spite of these

efforts, Syria is still subject to water deficit in the amount of 3.5 billion m3 annually. This

water shortage relates to increased water consumption in the various sectors exceeding the

renewable water supply and to recent climatic changes Syria has been undergoing. These

environmental variations, which have impacted negatively the water level, comprise high

temperatures, limited rainfall and exclusion of some rivers and springs. The

aforementioned water deficiency is limited to Dajleh and Al-Kabour basins (2.3 billion m3/

year) and to Orientes Basin (1.2 billion m3/ year), see Figure A1.1. In this regard,

agriculture consumes about 90% of the available water, whereas the respective shares of

drink water and water for industrial uses amount to 8% and 2% respectively. Hence, the

available water for agriculture accounts for about 16 billion m3 annually. This water supply

is distributed differently across water basins (Figure A1.1) and is decreasing per capita

owing to the relatively high population growth.

Consequently, the Government puts high emphasis on the transformation of modern

irrigation technologies into agriculture and cooperates closely with regional and

international agencies to make a better use of the available water resources and to improve

17 Area increase. 18 Yield increase.

State of Food and Agriculture in Syria 2010

8

both water management and water harvesting. This fact is confirmed in Table 1.4, which

indicates the development of the irrigated area diversified by both water sources and

irrigation methods from 2001 to 2009 (Table A1.7).

Table 1.4. Evolution of the irrigated area by sources and methods, 2001-2009 (ha, %)

Item Average

1 01-03

Average 2

04-06

Average 3

07-09

Change % 3/2

Change % 3/1

AAGR % 3/1

Total irrigated area 1,320,294 1,422,366 1,330,391 -6.5 0.8 0.2 Out of which (sources) Irrigated from wells by pumping 808,736 860,419 743,399 -13.6 -8.1 -2.1 Irrigated from Government projects by pumping

315,444 333,968 370,416 10.9 17.4 4.1

Irrigated from river and springs by gravity

196,114 227,979 216,576 -5.0 10.4 2.5

Out of which (methods) Sprinkler irrigation 112,664 151,125 168,420 11.4 49.5 10.6 Drip irrigation 57,575 71,533 91,699 28.2 59.3 12.3 Total modern irrigation 170,239 222,658 260,119 16.8 52.8 11.2 Source: Elaborated from the MAAR. The AASA. 2009.

Table 1.4 also shows that the total irrigated area and the irrigated land from wells, springs

and rivers declined from 2004 to 2009, while the irrigated area from governmental projects

and the area under modern irrigation increased. Over the 2001-2009 period, on the other

hand, only the irrigated land from wells diminished. The decrease in the irrigated area can

be related to the drought spells during the 2006-2009 period and to the increase in fuel

prices, which influenced negatively the irrigated area from wells. In contrast, the

augmentation of the irrigated area from governmental projects refers to both Government

policies, which focus on the storage of water in dams, and the very low irrigation cost of

state projects as compared to that of wells.

Furthermore, Table A1.7 illustrates the distribution of the irrigated area by governorates

from 2001 to 2009 considering both irrigation sources and irrigation methods. It illustrates

that the irrigated area by sources is concentrated in the northern regions (Aleppo, Al-

Raqqa, Dair-Ezzor and Al-Hassake), where the irrigated area under modern irrigation is

intense in the provinces of Hama, Idleb, Aleppo and Al-Hassake (Figure 1.5).

State of Food and Agriculture in Syria 2010

9

Figure 1.5. Structure of the irrigated area under modern irrigation by regions, 2009 (%)

0%

20%

40%

60%

80%

100%

Al-Sweid

aDar

'a

Al-Qun

eitra

R. Dam

ascu

s

Homs

Hama

Al-Gha

bId

leb

Tarto

us

Lattak

ia

Alepp

o

Al-Raq

qa

Dair-E

zzor

Al-Has

sake

Irrigated by sprinklers Irrigated by drip

Source: Elaborated from the MAAR. The AASA. 2009. R: Rural.

Finally, the water sector is still subject to the following obstacles:

Decrease of all water sources especially ground water as a result of an unorganized

wells digging and water pumping, a deficit between supply and demand and a

deterioration of irrigation water quality. In addition, there is a slowdown in switching

towards advanced irrigation technologies.

Domination of traditional irrigation schemes given that the project of modern irrigation

is still subject to difficulties by its implementation because of the lack of credits,

licenses and requirements.

Contamination of water in almost all water basins due to agricultural intensification

strategies, industrial residues and salinity (in Al-Badia for example).

1.3.3. Steppes and pastures

Al-Badia (Syrian steppe) covers around 55% of the total area of the country. It is usually

affected negatively by the desertification in many parts of it due to low rainfall,

overgrazing, erosion, and degradation of fodder crops used for animal feeding. Therefore,

various programmes focusing on the conservation and rehabilitation of Al-Badia land

resources are being implemented to address the aforementioned major environmental and

economic problems. In addition, regulations and decrees have been issued to reverse this

situation and preserve natural pastures in the Syrian steppe. For example, crop cultivation

in Al-Badia has been prohibited and protection zones have been established. Furthermore,

the Government has executed a series of projects to develop Al-Badia and to enhance the

livelihood of its population.

Nevertheless, the area of steppes and pastures declined slightly from 8,299 thousand ha

(average (1999-2001)) to 8,230 thousand ha (average (2007-2009)), Table A1.3. This area

State of Food and Agriculture in Syria 2010

10

is allocated differently across governorates as indicated in Figure 1.6, which points out to

its concentration in the regions of Homs, Dair-Ezzor, Rural Damascus and Aleppo.

Figure 1.6. Distribution of steppes and pastures by regions, 2009 (%)

Dar'a0.35%

Al-Ghab0.03%

Idleb0.52% Tartous

0.03%

Al-Sweida2.55%

Al-Quneitra0.15%

Al-Hassake6.53%Dair-Ezzor

22.84%

Al-Raqqa11.91%

Aleppo2.74%

Lattakia0.02%

Hama3.81%

Rural Damascus15.95%

Homs32.57%

Source: Elaborated from the MAAR. The AASA. 2009.

Finally, the constraints facing Al-Badia utilization and deteriorating its performance can be

summarized as follows:

Weak infrastructures accompanied with uncooperative efforts to its development in

various fields: health, education, police posts, fodder stores, drink water, wells, roads,

pasture cultivations, protection zones, etc. Therefore, it is necessary to manage steppes

and pastures so that they will be sustainable.

Shortage in the provision of inputs that are used for sheep breeding because of both Al-

Badia overgrazing and droughts.

Salinity of water, which impacts negatively the performance of the livestock sector and

needs to be removed.

Weakness in processing and marketing operations related to livestock products and in

the training and education activities of the local communities.

Degradation and erosion of Al-Badia resources as a consequence of natural phenomena

especially winds.

1.3.4. Forestry

Syrian forests constitute on average 3% of the total area of the country; their main products

are forestry seedlings, charcoal, fuel wood and industrial wood. They are characterized by

several weaknesses such as low tree density, high tree mortality rate because of droughts,

fire degradation, overgrazing and accomplishment of forest roads. Therefore, the

Government has proposed numerous comprehensive policies19 as indicated in the Syrian

19 See chapter three.

State of Food and Agriculture in Syria 2010

11

Agricultural Strategy (SAS), 10th FYP and 11th FYP to improve the performance of the

forestry sector. These policies seek to maintain and develop forestry resources, increase

productivity of these assets, improve the income of local communities, retain the

environment, attain efficient forestry resource management in cooperation with local

communities, enhance the forestation of deteriorated and new areas to expand forests

according to ecological conditions and raise the role of forest products in achieving food

security.

As a consequence, the forest area increased by an AGR of 0.7% from 556 thousand ha

(average (1999-2001)) to 579 thousand ha (average (2007-2009)), Table A1.3. This area

was mostly concentrated in Hassake, Lattakia and Idleb in 2009 as shown in Figure 1.7.

Figure 1.7. Distribution of forests by regions, 2009 (%)

Idleb13.8%

Al-Ghab6.4%

Hama6.7%

Homs9.8%

Damascus10.0%

Dar'a1.8%

Al-Quneitra0.6%

Al-Sweida1.4%

Al-Hassake16.0%

Al-Raqqa2.8%

Dair-Ezzor1.5%

Aleppo9.3%

Lattakia14.7%

Tartous5.4%

Source: Elaborated from the MAAR. The AASA. 2009.

1.3.5. Fishery

The increasing number of the population has actually led to the hunger phenomenon in

many developing countries. Consequently, efforts have been directed to find alternative

food sources and to improve the productivity of them. Aquacultures, in particular fishery,

are considered as one of these most important sources to supplement food economically

and efficiently for human beings.

In relation to Syria, the Syrian coast extends over 183 km and the continental shelf covers

1,373 square miles. Its fish stock is estimated at 0.9 tonnes/mile2, which is very low as

compared to that of other countries. In addition, internal lakes and rivers are under-utilized

in the field of fishing. The total area covered by lakes totaled 1,017 km2, out of which only

about a half is used for fishing or fish farming. Therefore, fish production in Syria is limited.

As a result, fish play a minor role in the traditional Syrian diet, with a per capita

consumption less than 1 kg/year.

State of Food and Agriculture in Syria 2010

12

Hence, the SG has given due attention to raise the efficiency of fish production in all

sources through establishing both a project for the development of fishery in the interior

water and the General Commission for Fishery. Besides, it encourages all sectors (public,

cooperative, private and joint sectors) to invest in the fish sector, organizes fishing in both

the Syrian coast and the internal water and provides the needed inputs to develop

aquacultures.

The aforementioned actions of the Government resulted in a satisfactory growth in fish

production during the 1999-2009 period as depicted in Table 1.5 (Table A1.8). Table 1.5

reveals that total fish production increased from 14 thousand tonnes (average (1999-2001))

to 16 thousand tonnes (average (2007-2009)).

Table 1.5. Development of fish production by sectors, 1999-2009 (tonne, %) Item Public sector Cooperative sector Private sector Joint sector Total

Average (1999-2001) 1 1,424 3,873 8,589 17 13,904 Average (2007-2009) 2 1,213 1,922 12,736 88 15,959 Average change % 2/1 --14.9 -50.4 48.3 415.7 14.8 AAGR % (2/1) -2.6 -11.0 6.8 31.4 2.3 Source: Elaborated from MAAR, the AASA, various issues.

Table 1.5 also indicates that the production of both the private and joint sectors augmented

while that of the public and cooperative sectors declined, the private sector dominated fish

production, and the joint sector enhanced its production at a high pace.

The total fish production presented in Table 1.5 is further diversified in Figure 1.8 into fish

types (Table A1.8) during the 1999-2009 period. Figure 1.8 makes clear that farm fish

dominated other fish, there was an increase in both farm and sea fish while fish of lakes,

dams and rivers declined, and fish production increased to attain its peak in 2007 and

diminished thereafter.

Figure 1.8. Development of fish production by types, 1999-2009 (tonne)

05,000

10,00015,00020,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

tonneSea fish

Fish of lakes, dams andriversFarm fish

Source: Elaborated from the MAAR. The AASA. Various issues.

Figure 1.9 presents the production of the aforesaid fish types by governorates (Table 1.8). It

shows that fish farming is absent in both Sweida and Rural Damascus while it concentrates

in Al-Ghab (28.1%), Lattakia (20.1%), Raqqa (14.3%) and Aleppo (12.3%). Furthermore,

State of Food and Agriculture in Syria 2010

13

sea fish is mostly located in Lattakia (82.2%) and Tartous (17.8%); farm fish in Al-Ghab

(57.3%); fish of lakes, dams and rivers in Aleppo (30.1%) and Raqqa (30.4%).

Figure 1.9. Distribution of fish production by governorates, 2009 (%)

0%

20%

40%

60%

80%

100%

Sea fish Farm fish Fish of lakes, dams andrivers

Total fish

Sweida Dar'a Quneitra Rural Damascus Homs

Hama Al-Ghab Idleb Tartous Lattakia

Aleppo Raqqa Dair-Ezzor Hassake

Source: Elaborated from the MAAR. The AASA. Various issues.

1.3.6. Quarrying industries

This section focuses on petroleum and phosphate owing to their importance for agriculture

and economic development. Fuel and natural gas as the former derivatives are considered

as the most important energy sources in the country. Their economic importance also

results from the fact that they contribute to a fifth of the GDP, ¾ of the export earnings and

a half of the Government budget20. These resources, however, are diminishing. Petroleum

production decreased from 540 thousand barrel/day in 2000 to 425 thousand barrel/day in

recent years21. Therefore, the Government tries to enhance other revenue sources especially

agriculture. Table 1.6 traces the evolution of the production of the aforementioned

quarrying products from 2004 to 2009 confirming their drop.

Table 1.6. Development of the production of petroleum and phosphate, 2004-2008 Item Unit 2004 2005 2006 2007 2008 2009 AGR %

Petroleum 000 m3 25,721 23,961 22,417 21,420 21,614 21,241 -3.8 Phosphate 000 tonnes 2,882 2,925 2,904 2,900 2,629 2,128 -5.9 Source: Elaborated from CBS, the ASA, various issues.

1.4. Human resources

The Syrian population consists of about 51% females and 49% males. It is also divided

into about 54% urban and 46% rural and is dominated by a young structure. The people

below 24 of age amount to about 62% of the inhabitants. Table 1.7 gives an idea about the

evolution of some indicators related to these human resources during the 2000-2009 period

(Table A1.9). It indicates that the number of population increased on average by an annual

20 Elaborated from the State Planning Commission (SPC), the 10th FYP. 21 Elaborated from the SPC, the 10th FYP.

State of Food and Agriculture in Syria 2010

14

growth rate of 3.5% and rural residents augmented by a rate lower than that of the total

population while urban citizen grew faster than the total population.

Table 1.7. Development of some indicators related to population, 2000-2009 (000 persons, %)

Item Average

(2000-2002) Average

(2007-2009) Average change %

(2000-2009) AAGR %

(2000-2009) Total population 16,723 19,889 18.9 3.5

Rural population 8,351 9,211 10.3 2.0

Urban population 8,373 10,678 27.5 5.0

Total labour force 5,224 4,829 -7.6 -1.9 Agricultural labour force 1,455 946 -35.0 -10.2 Source: Elaborated from CBS, the ASA, various issues.

Table 1.7 also shows that the urban and rural populations have an approximately equal

share, which leads to the conclusion that a high share of the inhabitants is involved in

agricultural activities. The number of this agricultural labour force decreased by a higher

rate than that of the total labour force during the considered period owing to the 2006-2009

droughts spells, introduction of modern technologies and immigration from the country

side to the city. As a consequence, the real annual agricultural per capita GDP declined

from SP15 thousand in 2002 to SP13 thousand in 2009 in reference to the total population

and from SP31 thousand to SP28 thousand, respectively, in relation to the rural population,

while it increased from SP178 thousand to SP280 thousand, respectively, when agricultural

labour force is considered.

Finally, the human resources are subject to the following constraints:

The relatively high population growth impacts negatively the performance of the

national economy in general and the natural resources utilization in particular.

There is a decrease in the provision of job opportunities due to adverse climatic

conditions and water scarcity because of droughts and irrational use of water

resources, which affects negatively the agricultural seasonal labor.

The share of agricultural investment in total investment is low due the long

recovery period of agricultural investments and risk, which limits the creation of

the required jobs.

The increase in the rural immigration and changes in consumption habits induce an

urgent need to enhance domestic production and imports, to provide competitive

goods and to expand the services supplied to cities especially those related to folk

parts of the city.

State of Food and Agriculture in Syria 2010

15

1.5. Agricultural intermediate consumption

Since the 1990s agricultural input policies have generally moved towards a gradual

elimination of subsidies of some inputs such as fuel, irrigation cost for state projects, and

electricity, while the prices of other inputs have been liberalized such as chemical

fertilizers, pesticides, machinery and some seed varieties. At the same time, they have

continued to facilitate the provision of agricultural inputs for private sector agencies who

took part in producing, importing, and trading most of these inputs especially pesticides,

fertilizers, seeds of vegetables, seedlings, machinery, and agricultural tools, in addition to

livestock production inputs such as veterinary care and fodder, etc. A more in-depth

investigation of those is presented below.

Governmental policies towards agriculture still give focused attention to the provision of

improved seeds for strategic crops (wheat, barley, cotton, sugar beet and tobacco) in

addition to some quantities of lentils, chickpeas , beans, corn, and potato. These seeds are

provided by the General Establishment for seed Multiplication (GESM) with the exception

of tobacco seeds, which are supplied by the General Organization for Tobacco (GOT).

Both establishments are owned by the state. The GESM, however, covers only 35-50% of

wheat seeds requirement, and only 1% of barley seeds demand. Therefore, the remaining

quantities of these seeds are supplied by farmers or by the private sector. On the other

hand, production and marketing of seeds related to cotton and sugar beet are confined to

the GESM, which intends to attain self-sufficiency of these seeds in addition to potato

seeds to substitute imports and to save foreign currency. The GESM increased the

aforementioned capacities of seed multiplication after acquiring 11 centers for sieving and

disinfection of seeds from the General Establishment for Silos complying with demand for

seeds. In this regard, Table 1.8 indicates the evolution in the production of improved seeds

related to wheat, cotton and potato during the 2003-2008 period. It shows that there was an

improvement in the production of wheat seeds, whereas that associated with cotton and

potato seeds decreased owing to the droughts, reduction of the cultivated area linked to

cotton and variation in the demand for seeds.

Table 1.8. Evolution in the production of the most important improved seeds of the GESM, 2003-2008 (000 tonnes)

Item 2003 2004 2005 2006 2007 2008 Average

03-05 Average

06-08 ACH %

03-08 AGR %

03-08 Wheat 85.7 139.3 134.3 124.0 72.3 193.4 119.8 129.9 8.5 17.7 Cotton 18.7 20.7 19.4 18.0 17.9 17.9 19.6 17.9 -8.5 -0.9 Potato 26.4 25.5 20.5 18.8 15.3 20.8 24.1 18.3 -24.2 -4.7 Source: Elaborated from MAAR, Achievement Report, 1970-2006, and Analysis of the Current Situation, 2004-2008. ACH: Average change. AGR: Annual growth rate.

State of Food and Agriculture in Syria 2010

16

In addition, fruit bearing seedlings are grown by both the MAAR and the private sector.

For this purpose, the MAAR has specialized nurseries, which expand or reduce their

production according to their annual plan. Pastoral and forestry seedlings, on the other

hand, are produced exclusively by the MAAR also according to an annual plan. Table 1.9

clarifies the production of the aforementioned seedlings related to the MAAR from 2003 to

2008 indicating on average an increase in the production of fruit bearing and pastoral

seedlings and a decline in that of forestry seedlings.

Table 1.9. Evolution in the production of seedlings related to the MAAR, 2003-2008 (million seedlings)

Item 2003 2004 2005 2006 2007 2008 Average

03-05 Average

06-08 ACH %

03-08 AGR %

03-08 Fruit bearing 7.9 8.3 5.4 7.9 7.6 8.3 7.2 7.9 10.2 1.0 Forestry 21.9 20.9 18.9 20.0 11.9 18.1 20.6 16.7 -19.0 -3.7 Pastoral 15.4 14.3 15.1 15.3 15.0 14.7 14.9 15.0 0.4 -0.9 Source: Elaborated from MAAR, Achievement Report, 1970-2006, and Analysis of the Current Situation, 2004-2008.

Furthermore, fertilizers play a substantial role in the vertical expansion22 of the agricultural

production to increase productivity, especially because of the limited agricultural land,

which induces a difficulty to expand horizontally. Therefore, during the last three decades,

the state occupied a prominent position in the provision of essential fertilizers, which were

distributed solely by the Agricultural Cooperative Bank (ACB) and its branches to the

public, cooperative and private sectors, complying with the strategic orientation to promote

the introduction of modern production techniques in the agricultural sector and to increase

agricultural production. At a later stage, Agricultural policies have shifted towards the

rationalization of the use of these fertilizers by implementing “fertilizers criteria” upon

analyzing agricultural soil and identifying the required quantity of chemicals. In spite of

these actions, fertilizers use increased on average over the 1999-2009 period as illustrated

in Table 1.10 and Figure 1.10 (Table A1.10) due to the expansion of the cultivated area and

the increase in the irrigated area. Figure 1.110 clarifies further that nitrogen fertilizers are

the most widely used chemicals, followed by phosphate, then by potash.

Table 1.10. Evolution in fertilizer use, 1999-2009 (000 tonnes) Item Nitrogen (N) Phosphate (P) Potash (K) Total

Average (1999-2001) 1 210 104 8 321 Average (2003-2005) 2 245 112 9 365 Average (2007-2009) 3 248 109 10 367 Average change % (3/2) 1.2 -2.7 11.1 0.5 Average change % (3/1) 18.1 4.8 25.0 14.3 AAGR % (3/1) 2.8 0.8 3.8 2.3 Source: Elaborated from MAAR, the AASA, various issues.

22 It focuses on making a better use of agricultural land to increase return and efficiency.

State of Food and Agriculture in Syria 2010

17

Figure 1.10. Evolution in fertilizer use, 1999-2009 (000 tonnes)

0

100

200

300

400

500

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

000 tonnes

Potash (K)

Phosphate (P)

Nitrogen (N)

Source: Elaborated from MAAR, the AASA, various issues.

The above-mentioned fertilizer use varies among governorates as depicted in Figure 1.11

owing to the prevailing cultivations and their size. Figure 1.11 also indicates that fertilizer

acquisition concentrates in the provinces of Hassake, Aleppo and Raqqa.

Figure 1.11. Distribution of fertilizer use by regions, 2009 (%) Sweida 0.2%

Dar'a 2.4%

Quneitra 0.4%

Rural Damascus 1.6%

Homs 6.0%

Hama 8.3%

Al-Ghab 3.1%

Idleb 7.8%

Tartous 3.9%

Lattakia 4.7%

Aleppo 19.4%

Raqqa 10.6%

Dair-Ezzor 6.6%

Hassake 25.0%

Source: Elaborated from MAAR, the AASA, 2009.

The Government also places high value on the provision of control materials and their

rational use. However, it provides only compulsory chemicals, where the private sector

supplies the rest. Table 1.11 illustrates the controlling activities conducted by the state

represented by the MAAR over the 2003-2008 period. It indicates that these actions

followed a declining trend complying with the state policy that focuses on the reduction

and rationalization of control substances.

Table 1.11. Evolution in controlling activities of the MAAR, 2003-2008 (000 ha, value: 000 SP)

Item 2003 2004 2005 2006 2007 2008 Average

03-05 Average

06-08 ACH %

03-08 Insects 386 589 226 167 265 131 400 188 -53.1 Diseases 178 161 116 102 3 5 152 37 -75.8 Weeds 1,284 742 492 852 158 18 839 343 -59.2 Field mouse 1,161 916 548 569 766 319 875 551 -37.0 Value 629,874 341,196 211,506 90,235 57,388 39 394,192 49,221 -87.5 Source: Elaborated from MAAR Achievements Report, 1970-2006 and Analysis of the Current Situation, 2004-2008.

In contrast to the aforementioned state interventions, the private sector administers fully

the prerequisite of agricultural machinery. Its supply of agricultural equipment increased in

line with the enlargement of agricultural operations excluding fixed threshers and dusters

State of Food and Agriculture in Syria 2010

18

(Table A1.11). The number of machines augmented from 485 thousand (average (1999-

2001)) to 588 thousand (average (2006-2008)). In 2008, the number of these machines was

fairly distributed by governorates in line with the size of regional agricultural activities

(Figure 1.12).

Figure 1.12. Distribution of agricultural equipment by governorates, 2008 (%)

Quneitra1%

Dar'a5%

Sweida4%

Hassake10%

Raqqa5%

Dair-Ezzor4%

Aleppo16%

Lattakia6%

Tartous8%

Idleb8%

Al-Ghab5%

Hama7%

Homs10%

Rural Damascus11%

Source: Elaborated from the MAAR, the AASA, 2008.

Finally, the Government provides additionally agricultural producers with feed for the

livestock through both domestic production and imports, and with containers especially for

strategic crops.

1.6. Agricultural supporting services

Agricultural supporting services include many activities provided by the public sector

particularly by the MAAR. The objective of these services in the middle and long run is to

increase production and productivity. They comprise the provision of credit, agricultural