Contentmccibd.org/images/uploadimg/publication_file/Quarterly_Review/2015.pdf · peak hours was...

28

Transcript of Contentmccibd.org/images/uploadimg/publication_file/Quarterly_Review/2015.pdf · peak hours was...

Content02-04

Executive Summary

04-07Agriculture

07-09Industry

09-13Monetary and Credit Developments

13Capital Market

13-14Public Finance

15-16Exports

16Imports

16-17Remittances

17Foreign Aid

18Foreign Direct Investment (FDI)

19Balance of Payment

20Exchange Rate

20Foreign Exchange Reserves

20-21Overseas Employment Situation

22Price Situation

23Chamber’s Projection on Some Selected Economic Indicators

24Concluding Observations

2 QUARTERLY REVIEW

General

Inadequate infrastructure, shortage of power and energy, and political uncertainty - all have become serious impediments to the growth of the economy. Some donor agencies have revised down their forecast of Bangladesh’s GDP growth to between 5.6-6.1 percent as against the government’s original growth target of 7.3 percent. Bangladesh Bank, too, has revised down its growth projection to 6.5 percent for the present fiscal. The key reasons behind the low growth forecasts are political unrest, weak external and domestic demand, and poor infrastructure.

There is no alternative to raising the level of investment, if Bangladesh is to attain the status of a middle income country by 2021. The Sixth Five-Year Plan (2011-15) targeted an eight percent GDP growth rate by its terminal year. This would require the economy’s total investment to grow from the present 26-27 percent of GDP to reach 32.5 percent by fiscal 2015. All-out efforts will therefore be needed to encourage private investment, enhance public investment, and attract foreign direct investment (FDI).

Agriculture

The crop agriculture performed reasonably well in the quarter under review but farmers did not get back their proper production cost as they could not sell their products in the market due to the political unrest. Nevertheless, with continuing policy support from government, the target set for food grains production in the present fiscal should not be difficult to achieve. In non-crop agriculture, fish production has increased, keeping up with the growing demand at home and abroad but the livestock and poultry industry faced serious setbacks as small and medium farmers were incurring losses being unable to sell milk, meat, chicken and eggs due to transport problems caused by the nationwide blockades.

Industry

In the broad industrial sector, many industrial units were found operating below capacity because of irregular supply of energy, both power and gas. The sector also suffered heavily from the impact of shutdowns and blockades. Infrastructural bottlenecks,

shortage of power and gas, lack of investment and shortage of industrial land in export processing zones were affecting the performance of the sector. These problems persist today as well. One can therefore assume that the industrial sector growth in the quarter under review was much below than expected.

Construction, Power and Services

The political unrest during the quarter under review badly affected construction activities, including in construction works under both public and private sectors. According to the REHAB, the sector counted Tk.360 million loss each day of blockade, and around Tk.110 billion investment by builders remained virtually stuck up. Sales of flats and plots by developers have declined by 60 percent and adoption of new projects dropped by 75 percent.

The power supply situation improved in the quarter under review but the demand for power, too, shot up more than ever due to the advent of the summer. As of 31 March 2015, total actual generation during day peak hours was 5,433 mw and during evening peak hours was 6,644 mw. The demand was 6,284 mw and there was no load shedding on that day. The maximum generation in 2015 was 7,571 mw on 15 April 2015 and it was also the maximum generation in BPDB’s history. In April 2015, total installed capacity rose to 11,526 mw, and derated/present capacity to 10,530 mw, but production remained low because of gas shortage and also because some power stations were shut for maintenance.

The heightened political unrest in all three months of the quarter under review harmed the services sector more than any other sector of the economy. There are indications that activities of most of the nine sub-sectors under the broad services sector, viz., transport, hotels & restaurants, community & social services, financial intermediation, education, and wholesale & retail trade suffered heavily due to the political unrest.

Money and Capital Market

Broad money (M2) recorded a lower growth of 12.80 percent y-o-y at the end of February 2015 compared with the 15.85 percent growth witnessed at the end of February 2014. Domestic credit, on the other hand,

ExEcuTIvE SuMMARY

JAN.-MAR. 2015 (Q3 FY15) Issue 03

though the implementation rate (44%) was above the implementation rate achieved in the corresponding period of the previous fiscal (43%).

External Sector: Export, Import, Remittances, Foreign Aid, FDI and Exchange Rate

Export earnings grew by 2.99 percent during the first nine months of FY15 over the corresponding period of the previous fiscal year despite widespread political violence. The growth rate could be higher if there were no political unrest in the country, which hurt production and disrupted supply chains.

Import payments fell by 3.95 percent in February m-o-m and also registered a negative growth of 0.06 percent y-o-y mainly due to lower prices of petroleum products on the global market and a prolonged political unrest in the country. Most importers are now maintaining a ‘go-slow’ policy to avoid financial risks due to the rough political weather.

Inflows of remittance rose by 1.13 percent to uS$3.765 billion in the quarter under review compared with the same period in FY14 (uS$3.723 billion) as it began to rise faster after the political situation began cooling down. However, in the first nine months of the current fiscal, inward remittances grew by 7.19 percent to reach uS$11.251 billion compared to uS$10.496 billion in the corresponding period of the previous fiscal. At the same time, remittances grew 3.34 percent year-on-year in March 2015 to uS$1.332 billion from uS$1.289 billion.

The disbursement of foreign aid during the first eight months of the current fiscal increased slightly by 1.04 percent to uS$1.853 billion from uS$1.834 billion in the corresponding period of the previous fiscal year. On the other hand, the commitments of foreign aid were uS$2.47 billion in July-February of FY15. Month wise in February 2015, the net receipts of foreign aid stood lower at uS$54.84 million compared to net receipts of uS$113.58 million in February 2014, as aid disbursement of the corresponding month of the preceding fiscal was comparatively much higher.

In July-February of FY15, the net FDI increased by 7.15 percent to uS$1,004 million from uS$937 million in the corresponding period of FY14. According to industry insiders, this investment is not

recorded a growth of 10.64 percent (y-o-y) at the end of February 2015, which was slightly higher than the 9.74 percent growth recorded at the end of February 2014.

Total liquid assets of the scheduled banks increased by 5.44 percent and stood higher at Tk.226,353 crore as of end February 2015. Also, the required liquidity (SLR) stood higher at Tk.122,520 crore as of end February 2015, and hence the excess liquidity of scheduled banks as of end February 2015 stood much lower at Tk.103,833 crore, compared with Tk.143,397 crore as of end June 2014.

Both lending and deposit interest rates of scheduled banks recorded a decline, but the average spread between lending and deposit interest rates fell only marginally (from 5.06 % in January 2015 to 5.04 % in February 2015).

The disbursement of industrial term loans during October-December of FY15 stood 45.6 percent higher at Tk.18,645 crore, compared with Tk.12,809 crore during the immediate previous quarter (July-September of FY15). The increase was mainly due to higher lending on account of the import of capital machinery.

In the quarter (Q3) under review, the disbursement of agricultural credit and non-farm rural credit by banks increased by 2.37 percent while the recovery decreased by 4.78 percent due to recent spate of political violence.

The capital market remained volatile during the quarter under review because of the political unrest that dampened investors’ confidence in the stock market.

Public Finance

Total tax revenue collection (NBR and non-NBR) during the first eight months of FY15 stood higher by 16.09 percent at Tk.82,937 crore against the collection of Tk.71,442 crore during the corresponding period of FY14.

NBR tax revenue collection during July-February of FY15 stood at Tk.79,978 crore, which is also higher by 16.42 percent against the collection of Tk.68,699 crore during the same period of the previous fiscal year.

Nevertheless, NBR witnessed a revenue shortfall of Tk.2,968 crore in the first eight months, with the highest shortfall being in the value added taxes.

The implementation of the Annual Development Programme (ADP) failed to pick pace as expected in the first nine months of current fiscal (July-March of FY15)

4 QUARTERLY REVIEW

sufficient for the country’s development. The foreign investors have adopted a ‘go-slow’ policy in making fresh investments because of their lack of confidence in the business environment, which they attribute to the country’s underdeveloped infrastructure, shortage of power and energy, procedural bottlenecks, lack of proper regulatory framework, scarcity of industrial lands, and political uncertainty. The government needs to overcome these obstacles to attract more FDI in the country.

Trade deficit increased by uS$2.809 billion or 78.82 percent to uS$6.373 billion in the first eight months of FY15 compared with that of uS$3.564 billion during the corresponding period of FY14. According to Bangladesh Bank data, falling export growth of readymade garments, the main export product of the country, dented the overall earnings while import of capital machinery continued to rise significantly during the period.

Taka depreciated marginally (by 0.22%) in terms of uS dollar between end-June of 2014 and end-March of 2015. This indicates relative stability in the foreign exchange market. The foreign exchange reserve rose to uS$23.05 billion on 31 March 2015 from uS$22.99 billion on the previous working day following lower import payment pressure (along with lower prices of

petroleum products in the international market) and also steady growth in both export earnings and inward remittances despite political unrest.

Inflation

The general point-to-point inflation rose in March 2015 for the second month in a row as the political unrest crippled the country’s supply chain. The inflation rate crept up in March to 6.27 percent from 6.14 percent in February 2015. Food prices increased mainly due to higher transport cost.

The food inflation rose to 6.37 percent in March from 6.11 percent in February 2015. In contrast, non-food inflation slided down to 6.12 percent in March from 6.20 percent in the previous month. Prices of goods, mostly produced in the rural areas, increased because of the supply chain disruption.

Both urban and rural inflation showed an upward trend. In the urban areas, the general point-to-point inflation rate rose to 6.77 percent in March from 6.62 percent in February while in the rural areas it went up by 0.12 percentage points to 6.01 percent from 5.89 percent. Food inflation, both urban and rural areas, increased due to the communication disruption caused by the political unrest that increased the cost of transportation of goods, while the non-food inflation, both urban and rural areas, declined.

1.0 AGRIcuLTuREcomplete data on agricultural production in the third quarter of the present fiscal (Q3 of FY15) is yet to be available. Even though the economy witnessed extensive damages caused by the political unrest during the quarter, the cultivation of food grains did not suffer much as farmers got necessary inputs with continuing policy support from the government. The Department

of Agricultural Extension (DAE) is confident that the production target of food grains (rice and wheat) for the year will be achieved. The steady growth in food grains production, strong growth of horticulture, and good growth (8.11%) in the exports of agricultural products in the first nine months of the present fiscal indicate that, despite political unrest in the past months, the growth of the agriculture sector in FY15 will be higher than in the previous fiscal.

1.1 Food Situation Domestic Production

The Department of Agricultural Extension (DAE) had set the food grains (rice and wheat) production target for FY15 at 36.220 million metric tons (mmt), of which individual targets for aman, aus, boro and wheat were

JAN.-MAR. 2015 (Q3 FY15) Issue 03

13.454 mmt, 2.428 mmt, 19.005 mmt, and 1.333 mmt, respectively. This target is 1.58 percent higher than the actual production of FY14 (35.656 mmt). Estimation of aman and aus production has been finalized by the BBS at 13.190 mmt and 2.328 mmt, which are, respectively, 1.28 percent and 0.09 percent higher than the previous year’s actual production (13.023 mmt and 2.326 mmt). According to unofficial estimates of DAE, wheat production has been finalized at 1.350 mmt for FY15 which is 1.28 percent higher than the target (1.333 mmt). Boro harvest is not yet complete this year but due to better climatic condition and timely supply of irrigation water and fertilizer the boro target is very likely to be achieved.

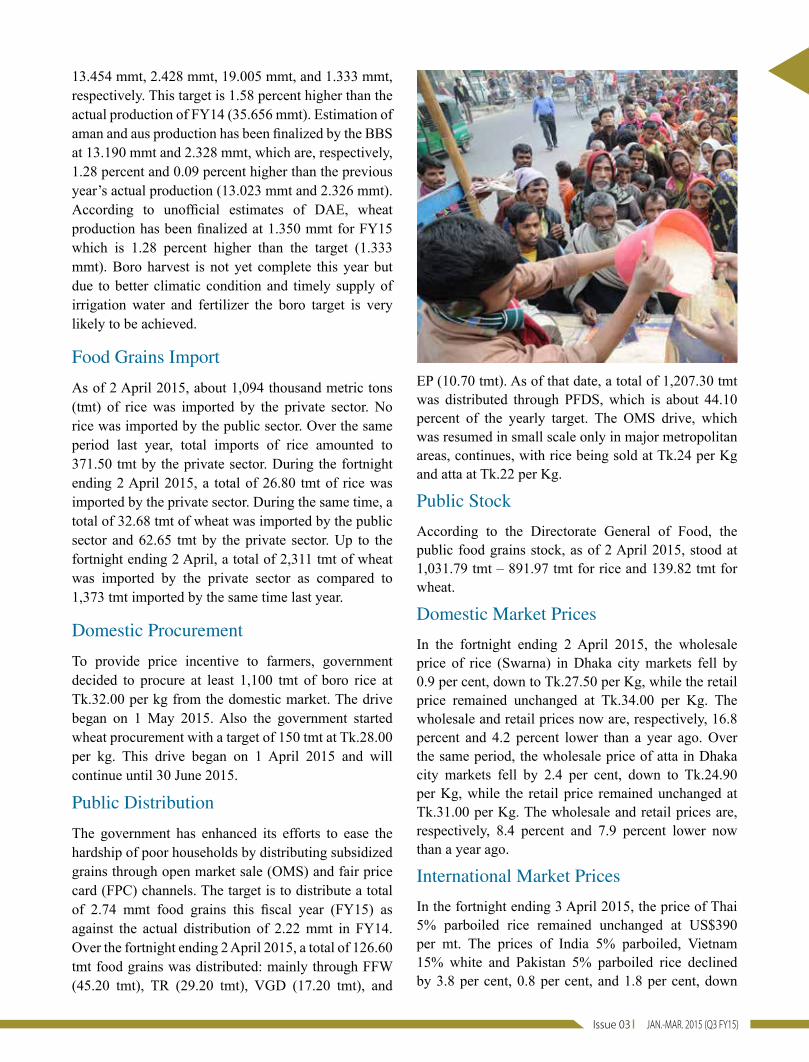

Food Grains Import

As of 2 April 2015, about 1,094 thousand metric tons (tmt) of rice was imported by the private sector. No rice was imported by the public sector. Over the same period last year, total imports of rice amounted to 371.50 tmt by the private sector. During the fortnight ending 2 April 2015, a total of 26.80 tmt of rice was imported by the private sector. During the same time, a total of 32.68 tmt of wheat was imported by the public sector and 62.65 tmt by the private sector. up to the fortnight ending 2 April, a total of 2,311 tmt of wheat was imported by the private sector as compared to 1,373 tmt imported by the same time last year.

Domestic Procurement

To provide price incentive to farmers, government decided to procure at least 1,100 tmt of boro rice at Tk.32.00 per kg from the domestic market. The drive began on 1 May 2015. Also the government started wheat procurement with a target of 150 tmt at Tk.28.00 per kg. This drive began on 1 April 2015 and will continue until 30 June 2015.

Public Distribution

The government has enhanced its efforts to ease the hardship of poor households by distributing subsidized grains through open market sale (OMS) and fair price card (FPc) channels. The target is to distribute a total of 2.74 mmt food grains this fiscal year (FY15) as against the actual distribution of 2.22 mmt in FY14. Over the fortnight ending 2 April 2015, a total of 126.60 tmt food grains was distributed: mainly through FFW (45.20 tmt), TR (29.20 tmt), vGD (17.20 tmt), and

EP (10.70 tmt). As of that date, a total of 1,207.30 tmt was distributed through PFDS, which is about 44.10 percent of the yearly target. The OMS drive, which was resumed in small scale only in major metropolitan areas, continues, with rice being sold at Tk.24 per Kg and atta at Tk.22 per Kg.

Public Stock

According to the Directorate General of Food, the public food grains stock, as of 2 April 2015, stood at 1,031.79 tmt – 891.97 tmt for rice and 139.82 tmt for wheat.

Domestic Market Prices

In the fortnight ending 2 April 2015, the wholesale price of rice (Swarna) in Dhaka city markets fell by 0.9 per cent, down to Tk.27.50 per Kg, while the retail price remained unchanged at Tk.34.00 per Kg. The wholesale and retail prices now are, respectively, 16.8 percent and 4.2 percent lower than a year ago. Over the same period, the wholesale price of atta in Dhaka city markets fell by 2.4 per cent, down to Tk.24.90 per Kg, while the retail price remained unchanged at Tk.31.00 per Kg. The wholesale and retail prices are, respectively, 8.4 percent and 7.9 percent lower now than a year ago.

International Market Prices

In the fortnight ending 3 April 2015, the price of Thai 5% parboiled rice remained unchanged at uS$390 per mt. The prices of India 5% parboiled, vietnam 15% white and Pakistan 5% parboiled rice declined by 3.8 per cent, 0.8 per cent, and 1.8 per cent, down

6 QUARTERLY REVIEW

to uS$375 per mt, uS$367 per mt, and uS$390 per mt, respectively. Also the price of West Bengal coarse rice decreased by 0.8 per cent, down to uS$339 per mt. However, the wholesale price of rice in Dhaka city decreased at uS$352 per mt on the same date. In the fortnight ending 3 April 2015, the prices of Russia and ukraine wheat decreased by 1.2 percent and 0.9 per cent, down to uS$213 per mt and uS$212 per mt, respectively, while uS Soft Red Winter (SRW) wheat price increased by 0.8 per cent, up to uS$219 per mt. On the same date, Dhaka city wholesale wheat price stood at uS$331 per mt.

1.2 Fisheries, Livestock and Poultry

According to BBS data, fisheries, livestock and poultry sub-sectors contributed around 5.5 percent to the GDP in FY14, of which the fish sector contributed around 3.7 percent and the livestock and poultry sectors contributed 1.8 percent. Nearly 17.1 million people are involved in the fish sector, while the poultry sector has created job opportunities for around 6.5 million people.

country’s fish production has been increasing to keep up with the growing demand at home and abroad for around a decade or so. In one estimate, fish production in the country soared nearly by 40 percent during the period between 2000 and 2014. Export of fish has increased more than hundred percent during the period. According to the Department of Fisheries (DoF), the country can achieve the production target of 3.50 million tons of fish in the current fiscal year, the market value of which will be over Tk.520 billion. In FY14 and FY13, the country produced 3.45 million tons and 3.40 million tons of fish, valued at Tk.500 billion and

Tk.450 billion, respectively. In the quarter under review, the production suffered a setback as the political unrest prevented sales in the local markets and also obstructed export. For gearing up the production of fish, the government has set up 120 hatcheries in different parts of the country to provide training to the people and hatchery owners under the ongoing ‘Rehabilitation of Infrastructure of Fish Seed Multiplication Firm and Production of Quality Fish Seed and Fingerling Project’. The project is aimed at giving training to 20,000 private sector hatchery owners by 2021 and also to provide modern technology to the farmers for producing a sufficient quantity of fish in the country to fulfill the deficiency of protein.

Recently the government has finalized the draft National Marine Fisheries Policy 2015 for optimum utilization of the marine resources for benefit of the nation and also keeping consistency with the national, regional and international fisheries policies and management practices for sustainable extraction of marine fisheries and other resources from the Bay of Bengal. The objectives of the draft National Marine Fisheries Policy 2015 are to develop the marine fisheries, protect the biodiversity and ecosystem of maritime zones, poverty alleviation and improvement of the living standard of fishermen that will help fulfill demand of nutrition through meeting the local demand and increase the export and boost the rate of economic growth. Besides, the policy has the provisions for taking compulsory licensing of fishing vessels, protecting the interest of fishermen, ensure better management for extraction of fisheries and mineral resources from the Bay of Bengal, setting up coastal radar station, introduce group insurance system for fishermen, taking permission from the Ministry of Fisheries and Livestock (MoFL) for renewal of trawlers licences and its handover. Moreover, the country’s victory over demarcation of maritime zones of the Bay of Bengal in the International Tribunal on the Law of the Sea-ITLOS, 2012 against India and Myanmar helped establish the country’s rights to extract maritime resources on 118,813 square- kilometer areas of the Bay of Bengal. According to the Marine Fisheries Department (MFD), marine fish catch increased to 0.606 million tons (17.6 % of total fish production) in FY14, from 0.58 million tons in FY13. Based on records in the past years, the MFD expects 0.65 million tons in FY15 because of good weather in the Bay of Bengal and victory over maritime dispute with India and Myanmar that brought a vast area under

JAN.-MAR. 2015 (Q3 FY15) Issue 03

Bangladesh’s fishing net. About 1.35 million people are dependent on the marine fishing sector for their livelihood.

The livestock and poultry industry, too, faced serious setbacks in the quarter under review as small and medium farmers incurred losses being unable to sell milk, meat, chicken and eggs due to transport problems caused by the nationwide blockades. The blockade-induced transportation disruption has forced farm owners to count losses as much as Tk.300 million per day, according to the Bangladesh Poultry Industries Association. Similarly thousands of people who are involved with the industry became unemployed. The country has now 93,000 poultry farms, down from 0.114 million in 2010. The poultry sector meets nearly 35 percent of the protein demand of the country, according to the Department of Livestock Services. Yet the country is facing a shortage of meat and eggs. At present, per capita consumption of chicken and eggs remains lower in Bangladesh than the recommended level of the Food and Agriculture Organization (FAO). A Bangladeshi consumes 3.63 Kg of chicken a year against the recommended level of 18-20 Kg. The per capita consumption of eggs stands at 45-50 pieces a year against FAO’s recommendation of 104.

developed by the BLRI, lays white egg. The new species can lay egg within 19-20 weeks and its annual capacity of laying eggs is around 300 and it will give eggs for 102 weeks while other varieties hardly give eggs for 80 weeks. The taste of meat of this variety is better than that of other layer varieties and it has disease-resistant power and also immunisation capacity to survive in local environment. The ‘Sarna’ has been developed under the ongoing research on developing local varieties of chicken since 2000.

2.0 INDuSTRYData on the country’s industry sector are not available for Q3 of FY15. The sector suffered the brunt of the impact of blockades and hartals in the quarter under review, similar to the losses suffered earlier in 2013; yet it managed to grow by 8.39 percent in FY14. However, according to recently released data by the Bangladesh Bureau of Statistics (BBS), industrial activities witnessed a moderately growing trend in the first half of the present fiscal year on the back of higher growth in pharmaceuticals, iron and steel, and cement sectors. The relatively calm political situation after 5 January 2014 elections helped the industries boost their output. The industrial production in July-December of FY15 grew by 10 percent from a year earlier.

2.1 Manufacturing Industries

Data on manufacturing industries are yet to be available for the quarter under review. However, during July-December of FY15, the Quantum Index of Industrial Production (QIIP) of medium and large scale manufacturing industries registered an increase by 12.84 percent to 231.83 points compared to 205.45 points over the corresponding period of FY14. According to the industry insiders, industrial activity went down in the following months due to supply disruption and weaker consumer confidence resulting from political unrest.

On the other hand, Bangladesh Livestock Research Institute (BLRI) has developed a local variety of chicken namely ‘Sarna’ ushering in a new hope in the country to reduce dependence on the import of layer chicken to meet the demand of protein. According to the Bangladesh Poultry Industries Association (BPIA), import cost for parental and grandparental stocks of broiler and layer chicken is nearly uS$110 million per year. Poultry sector insiders expressed hope that the variety’s commercial use could bring revolutionary changes for the country. The ‘Sarna’ will lay brown coloured egg when the earlier variety ‘Shubhra’, also

8 QUARTERLY REVIEW

Among medium and large-scale manufacturing industries, general indices that recorded an increase in July-December of FY15 compared to the corresponding period of the preceding year are: pharmaceuticals and medicinal chemical (69.79%), food products (42.85%), fabricated metal products except machinery (37.76%), non-metalic mineral products (17.42%), leather and related products (10.02%), basic metals (5.16%), chemicals and chemical products (2.84%), and wearing apparel (0.74%). On the other hand, there is some decrease in indices of textile (12.76%) and tobacco products (3.51%).

2.2 Construction

The political unrest during the quarter under review, just as in 2013 badly affected construction activities, including in construction works under both public and private sectors. According to the Real Estate and Housing Association of Bangladesh (REHAB), the sector counted Tk.360 million loss each day of blockade, and around Tk.110 billion investment by builders remained virtually stuck up. Sale of flats and plots by developers declined by 60 percent and the start-up of new projects dropped by 75 percent. Most of the realtors were selling flats and plots at a very low profit margin to maintain their cash flows. Nearly 11,000 ready apartments remained unsold due to the political unrest. As the sector is still passing through tough time, realtors have started cutting back on prices of apartments and plots in an attempt to lure back buyers as demand falls. The backward linkage industries were also in dire strait as demand for their products fell by over 60 percent. Manufacturers of construction materials like MS rod, cement, paints,

furniture and tiles were thus facing tough times. The sale of land plots across the country also declined to the lowest level.

2.3 Power

The power supply situation improved in the quarter under review but the demand for power, too, shot up more than ever due to the advent of the summer. As of 31 March 2015, total actual generation during day peak hours was 5,433 megawatt (mw) and during evening peak hours was 6,644 mw. The demand was 6,284 mw and no load shedding occurred on that day. The maximum generation in 2015 was 7,571 mw on 15 April 2015 and it was also the maximum generation in BPDB’s history. In April 2015, total installed capacity rose to 11,526 mw, and derated/present capacity to 10,530 mw, but production remained low because of gas shortage and also because some power stations were shut for maintenance.

According to the BPDB website, the 11,526 mw installed capacity of power plants comprised of coal 250 mw (2.17%), gas 7,723 mw (67.01%), HFO 2,034 mw (17.65%), HSD 789 mw (6.84%), Hydro 230 mw (2.0%), and imported 500 mw (4.33%).

According to the Ministry of Power, Energy and Mineral Resources (MoPEMR), the implementation of dozens of power projects has slowed down in the last one year. The Ministry expects to add as much as 1,500 mw power from six power plants to the national grid within three months beginning from late April.

After assuming office in 2009, the present government had rolled out plans to make load shedding a thing of the past within a few years.

JAN.-MAR. 2015 (Q3 FY15) Issue 03

According to the MoPEMR, the government is expecting to generate electricity of 13,301 mw at the end of this year and it has the vision to generate 20,000 mw with the aim to bring all citizens under electricity cover by 2021. To achieve the target, the government went for all kinds of power plants using petroleum fuel, gas, coal and renewable energy. The government has given top priority to the development of the sector considering its importance in the overall development of the country.

2.4 Services Sector

The heightened political unrest in the three months of the quarter under review harmed the services sector more than any other sector of the economy. The financial sector suffered badly because there were no new investments because of the unrest and the demand for bank loans declined. Tourism activities were hit hard because of non-stop shutdowns and blockades. The arrival of domestic tourists at resorts declined by a margin of about 90 percent and many foreign tourists cancelled their tour programmes.

The political unrest also affected the transport sector badly. Destruction of roads and uprooting of railway tracks caused a serious damage to road and rail communications in most regions of the country. Apart from this, almost all cNG filling stations had to

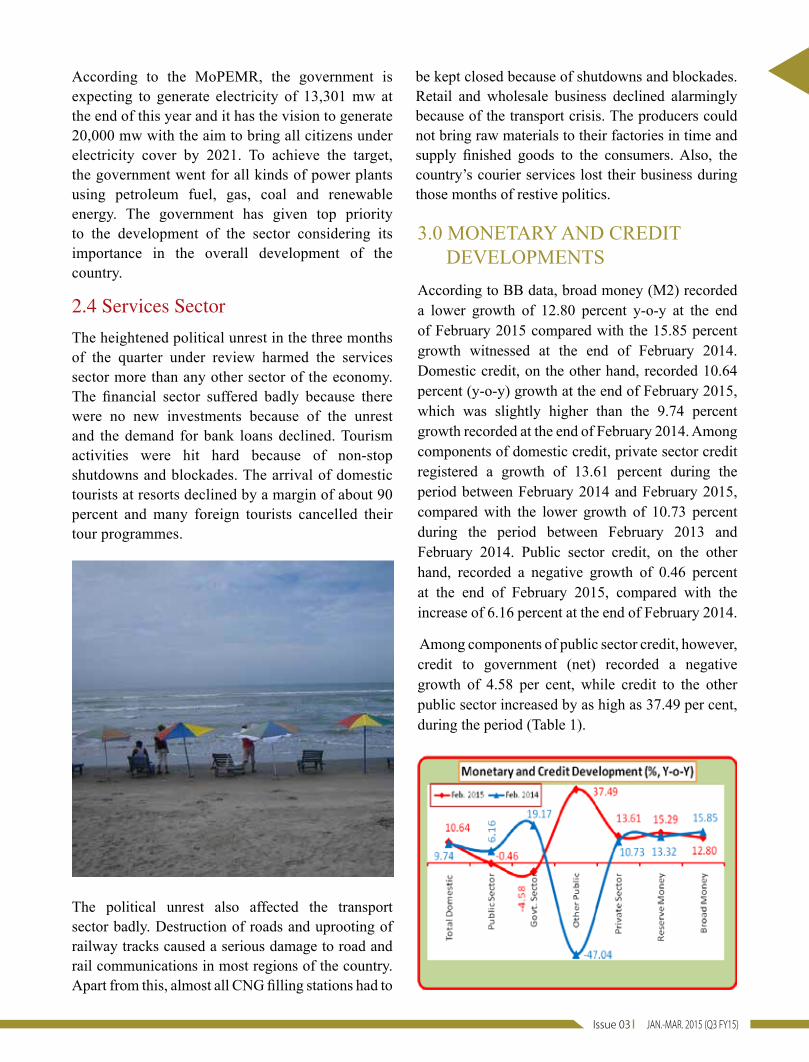

3.0 MONETARY AND cREDIT DEvELOPMENTS

According to BB data, broad money (M2) recorded a lower growth of 12.80 percent y-o-y at the end of February 2015 compared with the 15.85 percent growth witnessed at the end of February 2014. Domestic credit, on the other hand, recorded 10.64 percent (y-o-y) growth at the end of February 2015, which was slightly higher than the 9.74 percent growth recorded at the end of February 2014. Among components of domestic credit, private sector credit registered a growth of 13.61 percent during the period between February 2014 and February 2015, compared with the lower growth of 10.73 percent during the period between February 2013 and February 2014. Public sector credit, on the other hand, recorded a negative growth of 0.46 percent at the end of February 2015, compared with the increase of 6.16 percent at the end of February 2014.

Among components of public sector credit, however, credit to government (net) recorded a negative growth of 4.58 per cent, while credit to the other public sector increased by as high as 37.49 per cent, during the period (Table 1).

be kept closed because of shutdowns and blockades. Retail and wholesale business declined alarmingly because of the transport crisis. The producers could not bring raw materials to their factories in time and supply finished goods to the consumers. Also, the country’s courier services lost their business during those months of restive politics.

10 QUARTERLY REVIEW

Table 1: Monetary and Credit Indicators

Particulars

Outstanding Stock (Taka in crore) % Changes in Outstanding Stock

February 2013R

February 2014R

February 2015R

February 2015 over February

2014

February 2014 over February

2013Total Domestic credit 554799 608809 673576 10.64 9.74

credit to Public Sector 121171 128633 128042 (-) 0.46 6.16

Net credit to Government Sector 97356 116021 110702 (-) 4.58 19.17

credit to Other Public Sector 23815 12612 17340 37.49 (-) 47.04

credit to Private Sector 433629 480176 545535 13.61 10.73

Reserve Money (RM) 107168 121439 140012 15.29 13.32

Broad Money (M2) 571682 662311 747087 12.80 15.85Note: P=Provisional; R=Revised

Source: Bangladesh Bank

Total liquid assets of the scheduled banks increased by 5.44 percent and stood higher at Tk.226,353 crore as of end February 2015 compared with Tk.214,676 crore as of end June 2014. Also, the required liquidity (SLR) stood higher at Tk.122,520 crore as of end February 2015 compared with Tk.71,279 crore as of end June 2014. Thus, the excess liquidity of scheduled banks as of end February 2015 stood lower at Tk.103,833 crore, compared with Tk.143,397 crore as of end June 2014 (Table 2).

Table 2: Liquidity Position of Scheduled Banks (Taka in crore)

Bank GroupAs of end June, 2014R As of end February, 2015P

Total liquid assets

Required liquidity (SLR)

Excess liquidity

Total liquid assets

Required liquidity (SLR)

Excess liquidity

1 2 3 4 (2-3) 5 6 7 (5-6)

State owned banks 77237 20832 56405 81468 37463 44005

Private banks (other than Islamic) 91298 37265 54033 95571 60774 34797

Private banks (Islamic) 25026 6580 18446 26658 15958 10700

Foreign banks 16155 4836 11319 21108 6824 14284

Specialized banks* 4960 1766 3194 1548 1501 47

Total 214676 71279 143397 226353 122520 103833

Notes: P=Provisional; R=Revised; *= SLR does not apply to Specialized banks (except BASIC Bank) as exempted by the governmentSource: Bangladesh Bank

Bangladesh Bank data shows that, of the total liquid assets of scheduled banks as of end February 2015, some 4.62 percent is held in the form of cash in tills and Balances with Sonali Bank, 20.03 percent in the form of cRR, 0.75 percent in the form of Excess Reserves, 4.19 percent in the form of Balances with Bangladesh Bank in Foreign currency and the remainder 70.41 percent in the form of unencumbered approved securities.

3.1 Interest Rate Developments

Bangladesh Bank (BB) employs repo, reverse repo, and BB bill rates as policy instruments for influencing financial and real sector prices. Effective from 1 February 2013, the repo and reverse repo rates have remained unchanged at 7.25 percent and 5.25 per cent, respectively (Table 3).

ParticularsOutstanding Stock % Changes in Outstanding Stock

February 2013R

February2014R

February2015P

February 2015 over February 2014

February 2014 over February 2013

Total Domestic credit 554799 608809 673576 10.64 9.74

credit to Public Sector 121171 128633 128042 (-) 0.46 6.16

Net credit to Government Sector 97356 116021 110702 (-) 4.58 19.17

credit to Other Public Sector 23815 12612 17340 37.49 (-) 47.04

credit to Private Sector 433629 480176 545535 13.61 10.73

Reserve Money (RM) 107168 121439 140012 15.29 13.32

Broad Money (M2) 571682 662311 747087 12.80 15.85

Bank Group

As of end June, 2014R As of end February, 2015P

Total liquid assets

Required liquidity

(SLR)

Excess liquidity

Total liquid assets

Mini.Required liquidity (SLR)

Excess liquidity

1 2 3 4 (2-3) 5 6 7 (5-6)State owned banks 77237 20832 56405 81468 37463 44005Private banks (other than Islamic) 91298 37265 54033 95571 60774 34797Private banks (Islamic) 25026 6580 18446 26658 15958 10700Foreign banks 16155 4836 11319 21108 6824 14284Specialized banks* 4960 1766 3194 1548 1501 47 Total 214676 71279 143397 226353 122520 103833

JAN.-MAR. 2015 (Q3 FY15) Issue 03

Table 3: Interest Rate (weighted average) movements in FY14 and FY15 (in percent)

Month/Quarter Repo Reverse Repo Lending Rate Deposit Rate Interest SpreadFY14R

July 7.25 5.25 13.63 8.61 5.02 August 7.25 5.25 13.56 8.55 5.01 September 7.25 5.25 13.51 8.50 5.01 October 7.25 5.25 13.42 8.47 4.95 November 7.25 5.25 13.42 8.45 4.97 December 7.25 5.25 13.45 8.39 5.06 January 7.25 5.25 13.39 8.40 4.99 February 7.25 5.25 13.40 8.34 5.06 March 7.25 5.25 13.36 8.21 5.15 April 7.25 5.25 13.25 8.11 5.14 May 7.25 5.25 13.23 8.01 5.22 June 7.25 5.25 13.10 7.79 5.31FY15P

July 7.25 5.25 12.84 7.71 5.13 August 7.25 5.25 12.75 7.63 5.12 September 7.25 5.25 12.58 7.48 5.10October 7.25 5.25 12.49 7.40 5.09November 7.25 5.25 12.49 7.32 5.17December 7.25 5.25 12.46 7.25 5.21January 7.25 5.25 12.32 7.26 5.06February 7.25 5.25 12.23 7.19 5.04March 7.25 5.25 NA NA NA

Notes: P=Provisional, R=Revised, NA=Not AvailableSource: Bagnladesh Bank

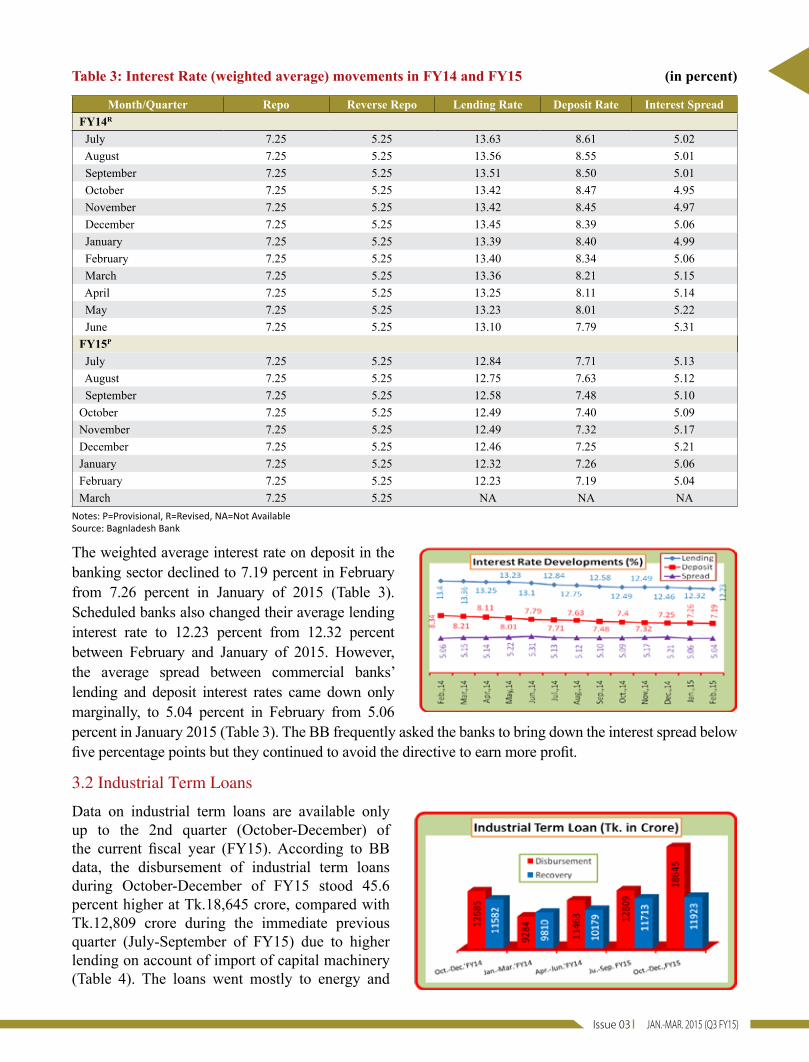

The weighted average interest rate on deposit in the banking sector declined to 7.19 percent in February from 7.26 percent in January of 2015 (Table 3). Scheduled banks also changed their average lending interest rate to 12.23 percent from 12.32 percent between February and January of 2015. However, the average spread between commercial banks’ lending and deposit interest rates came down only marginally, to 5.04 percent in February from 5.06 percent in January 2015 (Table 3). The BB frequently asked the banks to bring down the interest spread below five percentage points but they continued to avoid the directive to earn more profit.

3.2 Industrial Term Loans

Data on industrial term loans are available only up to the 2nd quarter (October-December) of the current fiscal year (FY15). According to BB data, the disbursement of industrial term loans during October-December of FY15 stood 45.6 percent higher at Tk.18,645 crore, compared with Tk.12,809 crore during the immediate previous quarter (July-September of FY15) due to higher lending on account of import of capital machinery (Table 4). The loans went mostly to energy and

12 QUARTERLY REVIEW

power, telecommunications, pharmaceuticals, textile, food processing, steel and engineering industries. The recovery of industrial term loans also increased by 1.8 percent to Tk.11,923 crore during October-December of FY15 from Tk.11,713 crore during July-September of FY15. The net disbursement of term loans was, however, higher because fresh disbursement exceeded recovery during the said quarter.Table 4: Disbursement and Recovery of Industrial Term Loans

(Tk. in crore)

QuarterDisbursement Recovery

LSI MSI SSCI Total LSI MSI SSCI Total

October-December of FY14R 8932 2803 950 12685 (42.8) 7919 2673 990 11582 (13.2)

January-March of FY14R 6054 2331 899 9284 (-26.8) 6976 2087 747 9810 (-15.3)

April-June of FY14P 7650 2848 965 11463 (23.5) 7023 2359 797 10179 (3.8)

July-September of FY15P 10325 1843 641 12809 (11.7) 7745 2778 1190 11713 (15.1)

October-December of FY15R 14074 3312 1259 18645 (45.6) 8682 2274 967 11923 (1.8)

Notes: LSI=Large Scale Industries, MSI=Medium Scale Industries and SSCI=Small Scale & Cottage Industries P=Provisional; R=Revised; Figures in parentheses indicate the percentage change over the previous quarter

Source: Bangladesh Bank

3.3 SME Loans

Data on loan disbursement to SME sector are not available for Q3 of FY15. According to BB data, total SME loans disbursed by all banks and non-bank financial institutions (NBFIs) increased by 17.5 percent to Tk.136,148 crore at the end of December 2014 from Tk.115,884 crore at the end of December 2013. The disbursement of SME loans was 24.5 percent of total loans disbursed by all banks and NBFIs at the end of December 2014 (Table 5).

Table 5: Outstanding Position of SME Loans (Tk. in crore)

Quarter Types of Loans SOBs PBs FBs SBs NBFIs Total

October-December of FY14R

Total LoansSME Loans

8404015445(+18.4)

31532985333(+27.1)

238532265(+9.5)

312149269

(+29.7)

314493572

(+11.4)

485885115884(+23.9)

January-March of FY14R

Total LoansSME Loans

8502615402(+18.1)

32120983873(+26.1)

230692061(+8.9)

314559435

(+30.0)

325483812

(+11.7)

493307114584(+23.2)

April-June of FY14PTotal LoansSME Loans

8488515698(+18.5)

33618488864(+26.4)

229992070(+9.0)

333689810

(+29.4)

338704065

(+12.0)

511306120507(+23.6)

July-September of FY15PTotal LoansSME Loans

8694616576(19.1)

34996892907(26.6)

233781905(8.2)

334619906(29.6)

356544321(12.1)

529408125615(23.7)

October-December of FY15R

Total LoansSME Loans

10239327215(26.6)

369935101978(27.6)

233851815(7.8)

22126760(3.4)

367984380(11.9)

554637136148(24.5)

% change of SME loans at the end of Sept. 2014 over Sept. 2013 +76.2 +19.5 -19.9 -91.8 +22.6 +17.5

Notes: P=Provisional, R=Revised; SOBs= State Owned Banks, PBs= Private Banks, FBs= Foreign Banks, SBs= Specialized Banks, NBFIs= Non-bank Financial Institutions; Figures in parentheses indicate SME loans as percentage of total loans Source: Bangladesh Bank

JAN.-MAR. 2015 (Q3 FY15) Issue 03

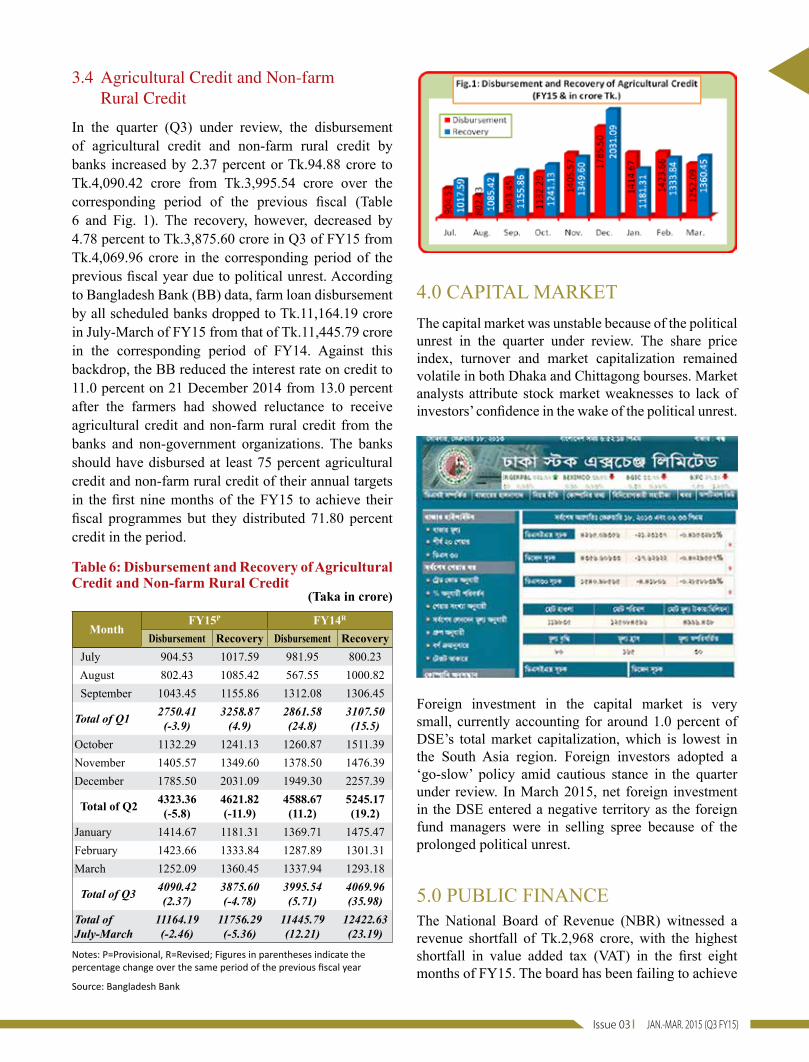

3.4 Agricultural Credit and Non-farm Rural Credit

In the quarter (Q3) under review, the disbursement of agricultural credit and non-farm rural credit by banks increased by 2.37 percent or Tk.94.88 crore to Tk.4,090.42 crore from Tk.3,995.54 crore over the corresponding period of the previous fiscal (Table 6 and Fig. 1). The recovery, however, decreased by 4.78 percent to Tk.3,875.60 crore in Q3 of FY15 from Tk.4,069.96 crore in the corresponding period of the previous fiscal year due to political unrest. According to Bangladesh Bank (BB) data, farm loan disbursement by all scheduled banks dropped to Tk.11,164.19 crore in July-March of FY15 from that of Tk.11,445.79 crore in the corresponding period of FY14. Against this backdrop, the BB reduced the interest rate on credit to 11.0 percent on 21 December 2014 from 13.0 percent after the farmers had showed reluctance to receive agricultural credit and non-farm rural credit from the banks and non-government organizations. The banks should have disbursed at least 75 percent agricultural credit and non-farm rural credit of their annual targets in the first nine months of the FY15 to achieve their fiscal programmes but they distributed 71.80 percent credit in the period.

Table 6: Disbursement and Recovery of Agricultural Credit and Non-farm Rural Credit (Taka in crore)

MonthFY15P FY14R

Disbursement Recovery Disbursement Recovery July 904.53 1017.59 981.95 800.23 August 802.43 1085.42 567.55 1000.82 September 1043.45 1155.86 1312.08 1306.45

Total of Q1 2750.41(-3.9)

3258.87(4.9)

2861.58(24.8)

3107.50(15.5)

October 1132.29 1241.13 1260.87 1511.39November 1405.57 1349.60 1378.50 1476.39December 1785.50 2031.09 1949.30 2257.39

Total of Q2 4323.36(-5.8)

4621.82(-11.9)

4588.67(11.2)

5245.17(19.2)

January 1414.67 1181.31 1369.71 1475.47February 1423.66 1333.84 1287.89 1301.31March 1252.09 1360.45 1337.94 1293.18

Total of Q3 4090.42(2.37)

3875.60(-4.78)

3995.54(5.71)

4069.96(35.98)

Total of July-March

11164.19(-2.46)

11756.29(-5.36)

11445.79(12.21)

12422.63(23.19)

Notes: P=Provisional, R=Revised; Figures in parentheses indicate the percentage change over the same period of the previous fiscal year

Source: Bangladesh Bank

4.0 cAPITAL MARKET The capital market was unstable because of the political unrest in the quarter under review. The share price index, turnover and market capitalization remained volatile in both Dhaka and chittagong bourses. Market analysts attribute stock market weaknesses to lack of investors’ confidence in the wake of the political unrest.

Foreign investment in the capital market is very small, currently accounting for around 1.0 percent of DSE’s total market capitalization, which is lowest in the South Asia region. Foreign investors adopted a ‘go-slow’ policy amid cautious stance in the quarter under review. In March 2015, net foreign investment in the DSE entered a negative territory as the foreign fund managers were in selling spree because of the prolonged political unrest.

5.0 PuBLIc FINANcEThe National Board of Revenue (NBR) witnessed a revenue shortfall of Tk.2,968 crore, with the highest shortfall in value added tax (vAT) in the first eight months of FY15. The board has been failing to achieve

14 QUARTERLY REVIEW

its revenue target mainly due to political unrest. All three wings (customs, value-added tax and income tax) of the NBR have witnessed the shortfalls.

The NBR had set a revenue collection target of Tk.149,720 crore for FY15, which is about 10 percent higher than that of the previous fiscal year’s original target (Tk.136,090 crore). In the remaining four months of FY15, the NBR will face a massive challenge as it will have to collect Tk.69,742 crore or 46.58 percent of total target of Tk.149,720 crore for the entire fiscal year to achieve its target.

However, total tax revenue collection (NBR and non-NBR) during the first eight months of FY15 stood higher by 16.09 percent at Tk.82,937 crore against the collection of Tk.71,442 crore during the corresponding period of FY14. At the same time, NBR tax revenue collection during July-February of FY15 stood at Tk.79,978 crore, which is higher by 16.42 percent against the collection of Tk.68,699 crore during the same period of the previous fiscal year (Table 7 and Fig. 2). Table 7: Government Tax Revenue Collections

Month

Tax Revenue Collections (in crore Taka)NBR

Non-NBR

GrandTotal customs

Duties vAT IncomeTax Others* Total

FY15P

July 1036 3615 2024 1313 7988 345 8333August 1254 3576 2301 1747 8878 372 9250September 1296 3924 4111 2024 11355 381 11736October 1023 3824 3242 1696 9785 309 10094November 1148 3871 2948 1752 9719 380 10099December 1208 4164 4094 1872 11338 414 11752January 1172 4092 3190 2331 10785 399 11184February 1152 3981 2998 1999 10130 359 10489

July-Feb. 9289(11.92)

31047(16.24)

24908(17.75)

14734(17.53)

79978(16.42)

2959(7.9)

82937(16.09)

FY14R

July 1033 3415 1865 1474 7787 392 8179August 939 2978 1987 1303 7207 256 7463September 1164 3441 3461 1595 9661 398 10059October 1024 3257 2959 1664 8904 287 9191November 961 3287 2601 1484 8333 315 8648December 1072 3318 3024 1371 8785 315 9100January 1068 3515 2742 1834 9159 402 9561February 1039 3498 2515 1811 8863 378 9241

July-Feb. 8300(-3.85)

26709(8.53)

21154(15.38)

12536(10.75)

68699(9.23)

2743(5.55)

71442(9.08)

Notes: P=Provisional; R=Revised; *=include supplementary duties and travel tax; Figures in brackets indicate percentage changes over the corresponding period of the preceding year.

Sources: NBR and Office of the Controller General of Accounts

5.1 Public Expenditure

The implementation of the Annual Development Programme (ADP) failed to pick pace in the current fiscal year. The implementation rate in the first nine months was 44 per cent, just 1.0 percentage point above the implementation rate achieved in the corresponding period of the previous fiscal (43%). All the implementing ministries and agencies utilized Tk.351.53 billion during July-March of FY15, out of the total ADP outlay (except self-financed) of Tk.803.15 billion. Of the amount used in the first nine months of FY15, Tk.238.97 billion came from the government’s own fund and Tk.112.56 billion from foreign aid. The political unrest badly hit the development works of the government, which affected overall project implementation. However, the government ministries and divisions have shown their highest capability in spending funds allocated from its internal resources rather than from the external sources. The poor spending rate from the external resources (project aid) has affected overall foreign aid inflow to the country.

JAN.-MAR. 2015 (Q3 FY15) Issue 03

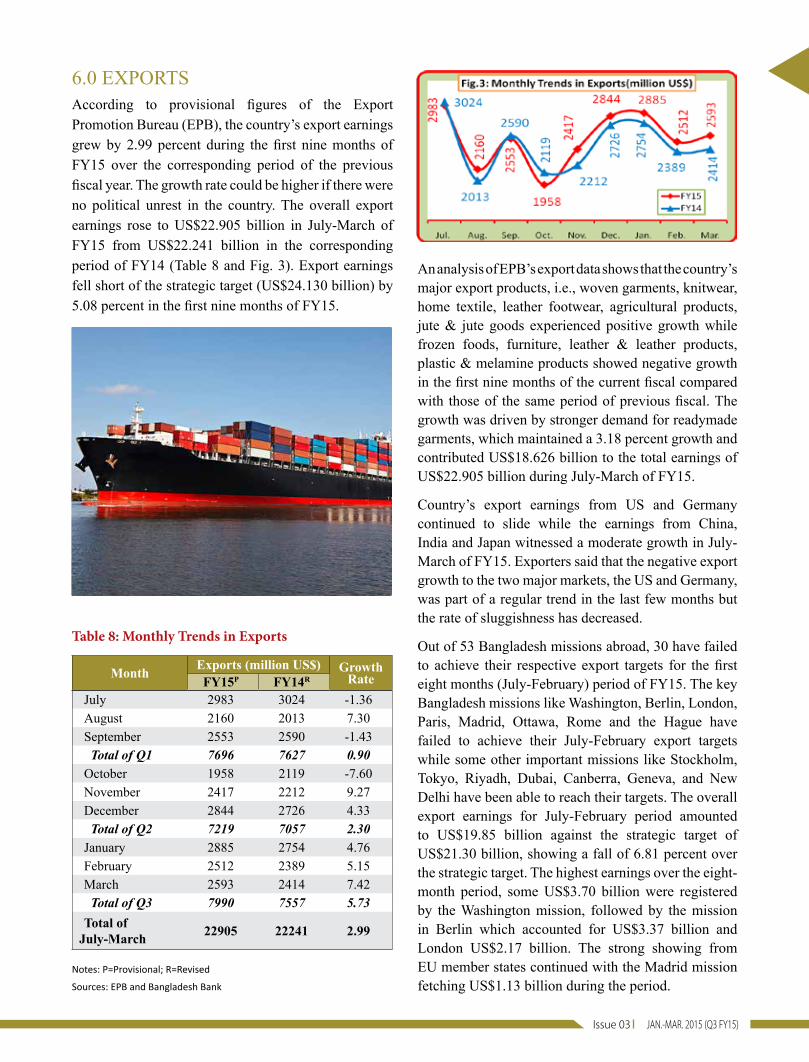

6.0 ExPORTSAccording to provisional figures of the Export Promotion Bureau (EPB), the country’s export earnings grew by 2.99 percent during the first nine months of FY15 over the corresponding period of the previous fiscal year. The growth rate could be higher if there were no political unrest in the country. The overall export earnings rose to uS$22.905 billion in July-March of FY15 from uS$22.241 billion in the corresponding period of FY14 (Table 8 and Fig. 3). Export earnings fell short of the strategic target (uS$24.130 billion) by 5.08 percent in the first nine months of FY15.

Table 8: Monthly Trends in Exports

Month Exports (million US$) Growth RateFY15P FY14R

July 2983 3024 -1.36August 2160 2013 7.30September 2553 2590 -1.43 Total of Q1 7696 7627 0.90October 1958 2119 -7.60November 2417 2212 9.27December 2844 2726 4.33 Total of Q2 7219 7057 2.30January 2885 2754 4.76February 2512 2389 5.15March 2593 2414 7.42 Total of Q3 7990 7557 5.73Total of

July-March 22905 22241 2.99

Notes: P=Provisional; R=Revised

Sources: EPB and Bangladesh Bank

An analysis of EPB’s export data shows that the country’s major export products, i.e., woven garments, knitwear, home textile, leather footwear, agricultural products, jute & jute goods experienced positive growth while frozen foods, furniture, leather & leather products, plastic & melamine products showed negative growth in the first nine months of the current fiscal compared with those of the same period of previous fiscal. The growth was driven by stronger demand for readymade garments, which maintained a 3.18 percent growth and contributed uS$18.626 billion to the total earnings of uS$22.905 billion during July-March of FY15.

country’s export earnings from uS and Germany continued to slide while the earnings from china, India and Japan witnessed a moderate growth in July-March of FY15. Exporters said that the negative export growth to the two major markets, the uS and Germany, was part of a regular trend in the last few months but the rate of sluggishness has decreased.

Out of 53 Bangladesh missions abroad, 30 have failed to achieve their respective export targets for the first eight months (July-February) period of FY15. The key Bangladesh missions like Washington, Berlin, London, Paris, Madrid, Ottawa, Rome and the Hague have failed to achieve their July-February export targets while some other important missions like Stockholm, Tokyo, Riyadh, Dubai, canberra, Geneva, and New Delhi have been able to reach their targets. The overall export earnings for July-February period amounted to uS$19.85 billion against the strategic target of uS$21.30 billion, showing a fall of 6.81 percent over the strategic target. The highest earnings over the eight-month period, some uS$3.70 billion were registered by the Washington mission, followed by the mission in Berlin which accounted for uS$3.37 billion and London uS$2.17 billion. The strong showing from Eu member states continued with the Madrid mission fetching uS$1.13 billion during the period.

16 QUARTERLY REVIEW

According to BB data, the settlement of import Letters of credit (Lcs) increased by 5.44 percent to uS$25.437 billion during July-February of FY15 from uS$24.125 billion in the corresponding period of the previous fiscal. On the other hand, opening of Lcs rose by 7.95 percent to uS$28.044 billion in the first eight months of FY15 from uS$25.979 billion in the corresponding period of the previous fiscal.

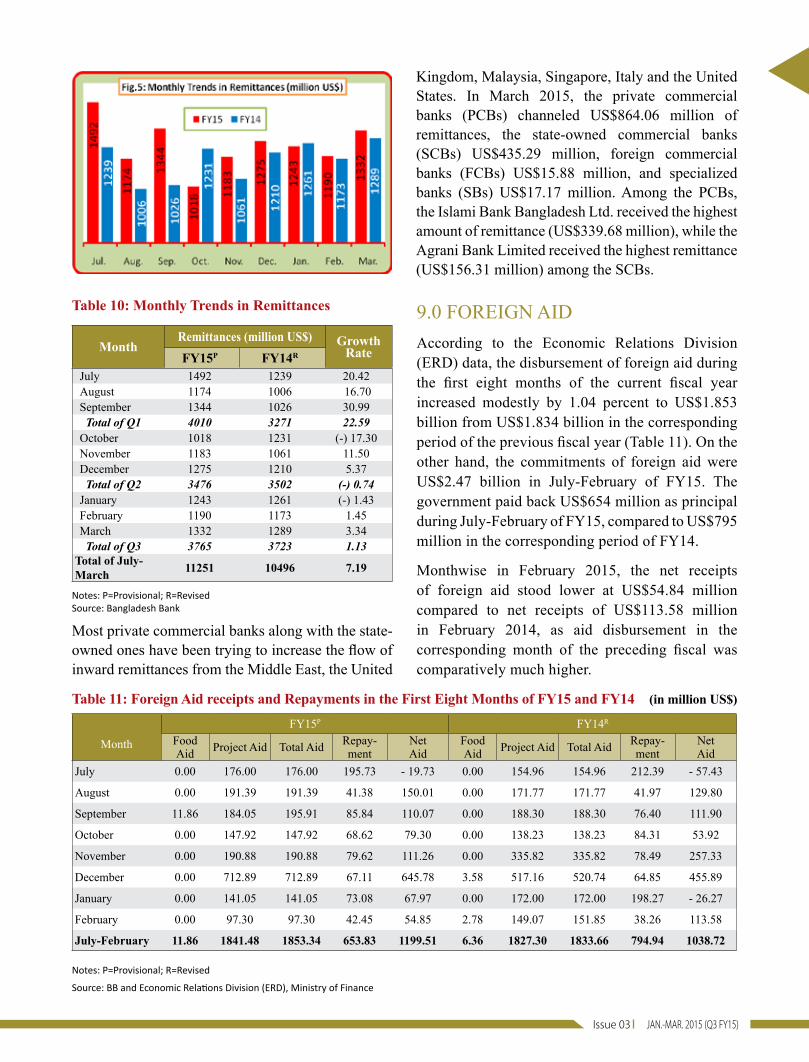

8.0 REMITTANcESAfter a declining trend in January and February, the flow of inward remittances rebounded in March 2015 as the political unrest started cooling down. In the first nine months of the current fiscal year, inward remittances grew by 7.19 percent to reach uS$11.251 billion compared to the corresponding period of the previous fiscal year (uS$10.496 billion). The central bank has recently approved a number of exchange houses abroad for the scheduled banks which boosted up the inflow of remittances. Besides, the rules and regulations of the international anti-money laundering have been strengthened to tackle the terrorist financing which discouraged the expatriate Bangladeshis to send the remittances through ‘hundi’ channel. The higher manpower export and stable exchange rate of Taka against the uS dollar also have contributed to raising the flow of inward remittances in the recent months. At the same time, remittances grew 3.34 percent year-on-year in March 2015 to uS$1.332 billion from uS$1.289 billion (Table 10 and Fig. 5). Also remittance inflows in the quarter under review rose by 1.13 percent to uS$3.765 billion compared with the same period in FY14 (uS$3.723 billion).

The latest EPB data also revealed that out of the 17 Bangladesh missions having commercial wings, only seven have achieved their export targets while 10 others could not achieve their respective targets. The seven missions with commercial wings, which achieved their respective export target, are Tokyo, canberra, New Delhi, Dubai, Geneva, Tehran and Yangon

7.0 IMPORTSImport payments fell in February 2015 mainly due to lower prices of petroleum products on the global market and a prolonged political unrest in the country. In January last, imports also went down by 10.64 percent m-o-m mainly due to the political unrest over the poll issues. Import payments fell by 3.95 percent to uS$3.475 billion in February m-o-m and also registered a negative growth of 0.06 percent y-o-y (Table 9 and Fig. 4).

Most importers are now maintaining a ‘go-slow’ policy to avoid financial risks due to the rough political weather. In fact, the supply chain has been affected since January 05 following the countrywide blockade and shutdowns. However, import payments during July-February of FY15 stood at uS$29.363 billion, which was 14.24 percent higher than import payments during the corresponding months of FY14 (uS$25.704 billion).

Table 9: Monthly Trends in Imports

Month Imports (million US$) Growth RateFY15P FY14R

July 3077 3472 (-) 11.38August 3686 2952 24.86September 4354 3355 29.78October 3602 3055 17.91November 3502 2782 25.88December 4049 3205 26.33January 3618 3406 6.22February 3475 3477 (-) 0.06Total of July-February Q2 29363 25704 14.24

Notes: P=Provisional; R=Revised Source: Bangladesh Bank

JAN.-MAR. 2015 (Q3 FY15) Issue 03

Table 10: Monthly Trends in Remittances

MonthRemittances (million US$) Growth

RateFY15P FY14R

July 1492 1239 20.42August 1174 1006 16.70September 1344 1026 30.99 Total of Q1 4010 3271 22.59October 1018 1231 (-) 17.30November 1183 1061 11.50December 1275 1210 5.37 Total of Q2 3476 3502 (-) 0.74January 1243 1261 (-) 1.43February 1190 1173 1.45March 1332 1289 3.34 Total of Q3 3765 3723 1.13

Total of July-March 11251 10496 7.19

Notes: P=Provisional; R=RevisedSource: Bangladesh Bank

Most private commercial banks along with the state-owned ones have been trying to increase the flow of inward remittances from the Middle East, the united

9.0 FOREIGN AID According to the Economic Relations Division (ERD) data, the disbursement of foreign aid during the first eight months of the current fiscal year increased modestly by 1.04 percent to uS$1.853 billion from uS$1.834 billion in the corresponding period of the previous fiscal year (Table 11). On the other hand, the commitments of foreign aid were uS$2.47 billion in July-February of FY15. The government paid back uS$654 million as principal during July-February of FY15, compared to uS$795 million in the corresponding period of FY14.

Monthwise in February 2015, the net receipts of foreign aid stood lower at uS$54.84 million compared to net receipts of uS$113.58 million in February 2014, as aid disbursement in the corresponding month of the preceding fiscal was comparatively much higher.

Kingdom, Malaysia, Singapore, Italy and the united States. In March 2015, the private commercial banks (PcBs) channeled uS$864.06 million of remittances, the state-owned commercial banks (ScBs) uS$435.29 million, foreign commercial banks (FcBs) uS$15.88 million, and specialized banks (SBs) uS$17.17 million. Among the PcBs, the Islami Bank Bangladesh Ltd. received the highest amount of remittance (uS$339.68 million), while the Agrani Bank Limited received the highest remittance (uS$156.31 million) among the ScBs.

Table 11: Foreign Aid receipts and Repayments in the First Eight Months of FY15 and FY14 (in million US$)

Month

FY15P FY14R

Food Aid Project Aid Total Aid Repay-

mentNet Aid

Food Aid Project Aid Total Aid Repay-

mentNet Aid

July 0.00 176.00 176.00 195.73 - 19.73 0.00 154.96 154.96 212.39 - 57.43

August 0.00 191.39 191.39 41.38 150.01 0.00 171.77 171.77 41.97 129.80

September 11.86 184.05 195.91 85.84 110.07 0.00 188.30 188.30 76.40 111.90

October 0.00 147.92 147.92 68.62 79.30 0.00 138.23 138.23 84.31 53.92

November 0.00 190.88 190.88 79.62 111.26 0.00 335.82 335.82 78.49 257.33

December 0.00 712.89 712.89 67.11 645.78 3.58 517.16 520.74 64.85 455.89

January 0.00 141.05 141.05 73.08 67.97 0.00 172.00 172.00 198.27 - 26.27

February 0.00 97.30 97.30 42.45 54.85 2.78 149.07 151.85 38.26 113.58

July-February 11.86 1841.48 1853.34 653.83 1199.51 6.36 1827.30 1833.66 794.94 1038.72

Notes: P=Provisional; R=Revised

Source: BB and Economic Relations Division (ERD), Ministry of Finance

18 QUARTERLY REVIEW

10.0 FOREIGN DIREcT INvESTMENT (FDI)

The financial account in the balance of payments statement (see Table 12) shows that net foreign direct investment (FDI) in the first eight months of the present fiscal (July-February of FY15) increased by 7.15 percent to uS$1,004 million from uS$937 million in the corresponding period of FY14. According to industry insiders, this investment is not enough for the country’s development. It needs uS$7.4 billion to uS$10.0 billion annually to spend for infrastructural development in line with its target of graduating to a middle-income country by 2021.

Bangladesh has a bright future due to its large domestic market of 160 million, the fast growing middle class, and 17 percent of its population being youngsters. Bangladesh is a safe haven of FDI as the government offers various incentives, including corporate tax holiday ranging from 5-7 years in certain areas and sectors. The government reduced import duty on machinery and spares and allowed accelerated depreciation on cost of machinery and new industries. Besides, the incentives also include a liberal regulatory environment characterized by allowance of 100 percent foreign equity, unrestricted exit policy, full repatriation of dividends and capital and remittance of royalty and attractive incentive package for export-oriented industries. But the investors are still to get back the confidence. The prospective foreign investors have adopted a ‘go-slow’ strategy in making fresh investments since 2013. Investors identified underdeveloped infrastructure, shortage of power and energy, procedural bottlenecks, lack of proper regulatory framework, scarcity of industrial lands, and political uncertainty as major impediments to new investment. The government needs to address these impediments to attract more FDI in the country.

However, according to the Board of Investment (BoI) data, foreign investment proposals fell 73.53 percent in the quarter under review (January-March of FY15) from the previous quarter, mainly due to a volatile political environment. commitments by foreign investors stood at Tk.1,046.66 crore during January-March of FY15, down from Tk.3,954.78

crore in October-December of FY15. The number of investment proposals from foreign investors or joint ventures also dropped in Q3 of FY15; only 24 investment proposals, including 8 fully-foreign investment proposals, were registered at BoI. The number was 30 in the previous quarter. But local investment rose by 48.13 percent in the same period. Local entrepreneurs proposed to invest Tk.24,598.58 crore in 336 proposals during January-March of FY15, while 291 proposals worth Tk.16,605.60 crore were proposed in the immediate past quarter. Among the proposals, the highest, 51.89 per cent, were registered for agro-based projects, followed by 10.46 percent in chemicals sector, 8.94 percent in engineering sector, 8.52 percent in textiles and 20.19 percent for the other sectors. Once the investment proposals are implemented, it would create employment opportunities for around 53,744 people.

The government has, reportedly, decided to go aggressive in wooing the private entrepreneurs to invest in the economic zones (EZs) of the country. Of the 17 EZs approved, three will be developed as private economic zones and one each exclusively for chinese and Japanese investors in the first phase. Besides export, the investors inside the EZs will be allowed to sell their produce in the local market which is not allowed in case of the Export Processing Zone (EPZs). The government has planned to set up some 100 EZs on 30,000 hectares of land over the next 15 years. countries like vietnam, Myanmar and china have already gone for setting up special economic zones (SEZs) replete with physical infrastructure including power, road and rail links to woo foreign investment. vietnam has already established 400 SEZs. Recently, Myanmar is making fast progress, to catch the waves of global investors. Bangladesh is lagging far behind in this race.

There are vast tracks of unutilized lands in the Bangladesh Small industries corporation’s (BScIc) existing industrial units. The government needs to consider these lands for selecting the feasible sites of the proposed EZs. Efforts should have been made to locate some of the EZs in such industrial estates of the BScIc where the land is now being used for anything other than industrial operations.

JAN.-MAR. 2015 (Q3 FY15) Issue 03

Table 12: Balance of Payments (in million uS$)

Items July-February of FY15P

July-February of FY14R Change

Trade Balance -6373 -3564 (-) 2809

Exports f.o.b (including EPZ)* 20061 19583 -

Imports f.o.b (including EPZ)* 26434 23147 -

Services -3179 -2608 (-) 571

credit 2008 2046 -

Debit 5187 4654 -

Primary Income -1870 -1683 (-) 187

credit 53 105 -

Debit 1923 1788

Of which: Official Interest Payment 288 314 -

Secondary Income 10332 9679 + 653

Official Transfers 35 42 -

Private Transfers 10297 9637Of which: Workers’ Remittances (current a/c portion) 9835 9139 + 696

current Account Balance -1090 1824 (-) 2914

capital Account 311 296 -

capital Transfers 311 296 -

Financial Account 3535 661 + 2874

Foreign Direct Investment (net) 1004 937 + 67

Portfolio Investment (net) 524 390 -Of which: Workers’ Remittances (financial a/c portion) 84 68 -

Other Investment (net) 2007 -666 -

Errors and Omissions -533 548 (-) 1081

Overall Balance 2223 3329 (-) 1106

Notes: P=Provisional; R=Revised; * = Exports and Imports both are compiled on the basis of shipment data

Source: Bangladesh Bank

11.0 BALANcE OF

PAYMENTSTrade deficit increased by uS$2.809 billion or 78.82 percent to uS$6.373 billion in the first eight months of FY15 compared with that of uS$3.564 billion during the corresponding period of FY14. According to Bangladesh Bank, falling export growth of readymade garments, the main export product of the country, dented the overall earnings in July-February of FY15 while import of capital machinery continued to rise significantly during the period. Export earnings registered only a 2.45 percent growth in July-February of FY15 compared with that of 13.59 percent growth in the same period of FY14. On the other hand, imports registered a 14.22 percent growth in July-February of FY15 compared with that of 6.24 percent growth in the corresponding period of FY14. The higher trade deficit turned the current account balance from a surplus of uS$1.824 billion into a big deficit of uS$1.090 billion despite the uptrend in inward remittances, which increased by uS$696 million or 7.62 percent to uS$9.835 billion in the first eight months of FY15. The overall balance also decreased but remained positive, thanks to a large increase in the financial account balance (Table 12).

20 QUARTERLY REVIEW

12.0 ExcHANGE RATE Between end-June of 2014 and end-March of 2015, Taka depreciated marginally (by 0.22%) in terms of uS dollar, showing stability in the foreign exchange market. On the inter-bank market, the uS dollar was quoted at Tk.77.6300 at the end of June 2014 and Tk.77.8000 at the end of March 2015 (Table 13).

Table 13: Monthly Exchange Rate

MonthFY15P (Taka per US$) FY14R (Taka per US$)

Month Average

End Month

Month Average

End Month

June - - 77.6301 77.6300

July 77.5907 77.5005 77.7570 77.7500

August 77.4588 77.4000 77.7537 77.7500

September 77.4006 77.4000 77.7502 77.7505

October 77.4031 77.4009 77.7506 77.7500

November 77.5149 77.7000 77.7509 77.7540

December 77.8563 77.9500 77.7500 77.7500

January 77.8726 77.7510 77.7505 77.7500

February 77.8000 77.8000 77.7502 77.7311

March 77.8000 77.8000 77.7113 77.6700

Note: i) P=Provisional; R=Revised

ii) Exchange rate represents the mid-value of buying and selling rates

Source: Bangladesh Bank

13.0 FOREIGN ExcHANGE RESERvESAccording to BB data, the central bank’s foreign exchange reserves crossed the uS$23 billion-mark for the second time on 31 March 2015 following lower import payment pressure (along with lower prices of petroleum products in the international market) and also steady growth in both export earnings and inward remittances despite political unrest. The reserves rose to uS$23.05 billion on the day from uS$22.99 billion on the previous working day. The country will be able to settle more than six-month import bills with the existing reserves. It was almost 20 percent higher than uS$19.295 billion in the same day of the previous year (Table 14 and Fig. 6).

A healthy reserve allows a country to get higher credit rating and helps its private sector to get loans from foreign sources at low interest rates. The current reserves will help keep the Taka stable against the uS dollar, according to BB.

The BB has continued purchasing uS dollars from the commercial banks directly in order to keep the exchange rate stable, which, incidentally has also contributed to the increase in the foreign exchange reserve. The BB has purchased a total of uS$2.69 billion from the commercial banks directly between 2 July and 13 April of FY15 for offsetting its increased supply to the market, which is also a reason behind the increase of foreign exchange reserve.

Table 14: Monthly Trends in Foreign Exchange Reserves

Month (million US$)FY15P FY14R

July 21383 15534August 22070 16252September 21837 16155October 22312 17345November 21590 17106December 22310 18075January 22042 18119February 23032 19151March 23050 19295

Notes: P=Provisional; R=RevisedSource: Bangladesh Bank

14.0 OvERSEAS EMPLOYMENT SITuATION

Manpower export of the country faced difficulties following the suspension of labour import by various Middle-Eastern countries while both public and private sectors are trying to expand manpower export in different countries, including Thailand and Japan. Only 108,709 workers from Bangladesh entered the international markets with jobs during the quarter under review (January-March of FY15). Of them, 28,333 went in January, 35,057 in February and 45,319 in March, according to Bureau of Manpower,

JAN.-MAR. 2015 (Q3 FY15) Issue 03

Employment and Training (BMET). The number of emigrants was 117,142 during the previous quarter (October-December of FY15).

Meanwhile, as the government has intensified efforts to diversify its labour market abroad, several meetings have been held with stakeholders in Bangladeshi embassies in various potential job markets in the Middle East and Libya. The government is trying to explore markets in Europe, Russia, Belarus and Sudan as there is potential demand for foreign workers in those countries. It is trying to send more workers following the government-to-government (G2G) migration process to Malaysia and Thailand.

Recently the Kingdom of Saudi Arabia (KSA) has decided to reopen its labour market for local jobseekers after a seven-year ban on manpower recruitment from Bangladesh. The Bangladeshis will now be able to get visas for all sectors, including construction and services. The country’s overall manpower export started declining significantly when the Saudi authorities brought allegations of anomalies in the recruitment process and subsequently slapped a ban on hiring of workers from Bangladesh in 2008. Before the ban, around 0.1 million Bangladeshis used to migrate to KSA every year. However, only a few Bangladeshis (10,657 in 2014) could obtain labour visas for cleaning jobs in the Kingdom during the period of ban. very recently, the government received a demand for recruiting 40,000 Bangladeshi female workers from the Saudi authority for housekeeping jobs. After completion of all formalities including 42 days’ residential training with Arabic language classes in three technical training centres (TTcs), the female workers will able to go to the Kingdom within a short period. But the authorities in Bangladesh did not get the expected level of response from women job-seekers because of safety fear and lower wages, although there is a large demand for domestic help in KSA.

Again, Qatar will recruit nearly 0.15 million workers from Bangladesh this year at zero migration cost to meet its demand for foreign workers and it has already

given approval of some 50,000 visas for Bangladeshi workers, which will be sent to the country within three months.

Meantime, the government urged the Emirates authorities to remove the obstacles to reopening its labour market for the Bangladeshis. The matter could be resolved through government-level talks like holding discussions between the uAE interior ministry and the home ministry of Bangladesh. After long seven years of closure, the government of Kuwait opened its labour market to the Bangladeshi workers last year.

citing a recent survey by the Global Knowledge Partnership on Migration and Development, the World Bank said that Bangladeshi migrant workers pay the highest recruitment costs in the world. The worker-paid recruitment costs averaged uS$1,955 in Kuwait with the Bangladeshis paying the highest, ranging between uS$1,675 and uS$5,154. Almost 10 million people use regular channels to migrate in search of employment every year. A large number of them pay illegal recruitment fees to recruitment agents. A 2009 Bangladesh Household Remittance Survey conducted by the International Organisation for Migration (IOM) found that more than half of the migrants paid over uS$2,000 in recruitment fees. Fees paid to smugglers for crossing international borders, a reasonable proxy for the black market recruitment fees, tend to be even more exorbitant. For example, according to the European union, smuggling fees in 2013 to Europe ranged from uS$5,000 in the case of vietnamese workers to more than uS$15,000 for Bangladeshi workers. On top of these direct fees paid to recruitment agents, migrant workers are often subjected to usurious interest rates of over 50 percent on loans taken to cover the costs of migration, according to the study. The government is also probing the reasons behind high costs of visa and other migration-related charges or fees which are hindering the country’s manpower exports abroad. In fact, high migration cost is preventing a large number of jobseekers to go abroad. The government is trying to bring down the cost.

Besides, a growing number of female job-seekers are now going abroad. In fact, 22,560 female workers entered the international markets with jobs during January-March of FY15. The number of female emigrants was 21,131 during the previous quarter (October-December of FY15). The overseas employment of female workers increased by 6.76 percent during the quarter. Female workers, mostly housemaids and garment workers were being employed in Jordan, Lebanon, uAE, Oman and Qatar.

22 QUARTERLY REVIEW

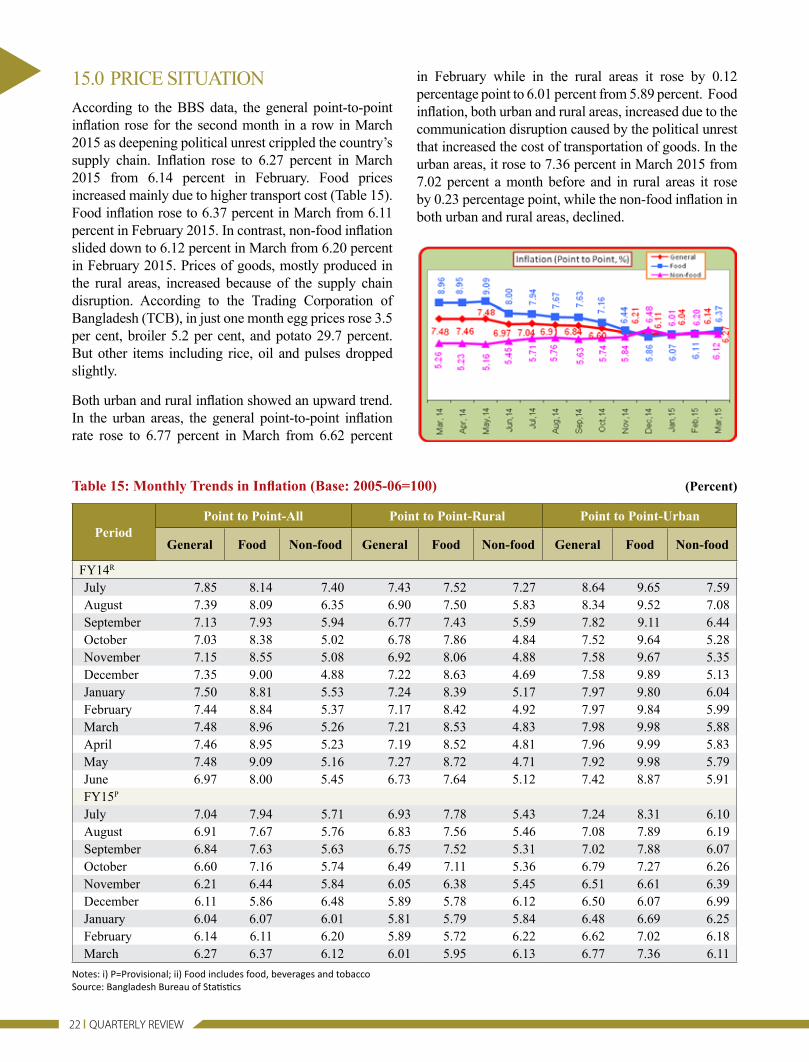

15.0 PRIcE SITuATIONAccording to the BBS data, the general point-to-point inflation rose for the second month in a row in March 2015 as deepening political unrest crippled the country’s supply chain. Inflation rose to 6.27 percent in March 2015 from 6.14 percent in February. Food prices increased mainly due to higher transport cost (Table 15). Food inflation rose to 6.37 percent in March from 6.11 percent in February 2015. In contrast, non-food inflation slided down to 6.12 percent in March from 6.20 percent in February 2015. Prices of goods, mostly produced in the rural areas, increased because of the supply chain disruption. According to the Trading corporation of Bangladesh (TcB), in just one month egg prices rose 3.5 per cent, broiler 5.2 per cent, and potato 29.7 percent. But other items including rice, oil and pulses dropped slightly.

Both urban and rural inflation showed an upward trend. In the urban areas, the general point-to-point inflation rate rose to 6.77 percent in March from 6.62 percent

in February while in the rural areas it rose by 0.12 percentage point to 6.01 percent from 5.89 percent. Food inflation, both urban and rural areas, increased due to the communication disruption caused by the political unrest that increased the cost of transportation of goods. In the urban areas, it rose to 7.36 percent in March 2015 from 7.02 percent a month before and in rural areas it rose by 0.23 percentage point, while the non-food inflation in both urban and rural areas, declined.

Table 15: Monthly Trends in Inflation (Base: 2005-06=100) (Percent)

PeriodPoint to Point-All Point to Point-Rural Point to Point-Urban

General Food Non-food General Food Non-food General Food Non-food

FY14R

July 7.85 8.14 7.40 7.43 7.52 7.27 8.64 9.65 7.59August 7.39 8.09 6.35 6.90 7.50 5.83 8.34 9.52 7.08September 7.13 7.93 5.94 6.77 7.43 5.59 7.82 9.11 6.44October 7.03 8.38 5.02 6.78 7.86 4.84 7.52 9.64 5.28November 7.15 8.55 5.08 6.92 8.06 4.88 7.58 9.67 5.35December 7.35 9.00 4.88 7.22 8.63 4.69 7.58 9.89 5.13January 7.50 8.81 5.53 7.24 8.39 5.17 7.97 9.80 6.04February 7.44 8.84 5.37 7.17 8.42 4.92 7.97 9.84 5.99March 7.48 8.96 5.26 7.21 8.53 4.83 7.98 9.98 5.88April 7.46 8.95 5.23 7.19 8.52 4.81 7.96 9.99 5.83May 7.48 9.09 5.16 7.27 8.72 4.71 7.92 9.98 5.79June 6.97 8.00 5.45 6.73 7.64 5.12 7.42 8.87 5.91FY15P

July 7.04 7.94 5.71 6.93 7.78 5.43 7.24 8.31 6.10August 6.91 7.67 5.76 6.83 7.56 5.46 7.08 7.89 6.19September 6.84 7.63 5.63 6.75 7.52 5.31 7.02 7.88 6.07October 6.60 7.16 5.74 6.49 7.11 5.36 6.79 7.27 6.26November 6.21 6.44 5.84 6.05 6.38 5.45 6.51 6.61 6.39December 6.11 5.86 6.48 5.89 5.78 6.12 6.50 6.07 6.99January 6.04 6.07 6.01 5.81 5.79 5.84 6.48 6.69 6.25February 6.14 6.11 6.20 5.89 5.72 6.22 6.62 7.02 6.18March 6.27 6.37 6.12 6.01 5.95 6.13 6.77 7.36 6.11

Notes: i) P=Provisional; ii) Food includes food, beverages and tobacco Source: Bangladesh Bureau of Statistics

JAN.-MAR. 2015 (Q3 FY15) Issue 03

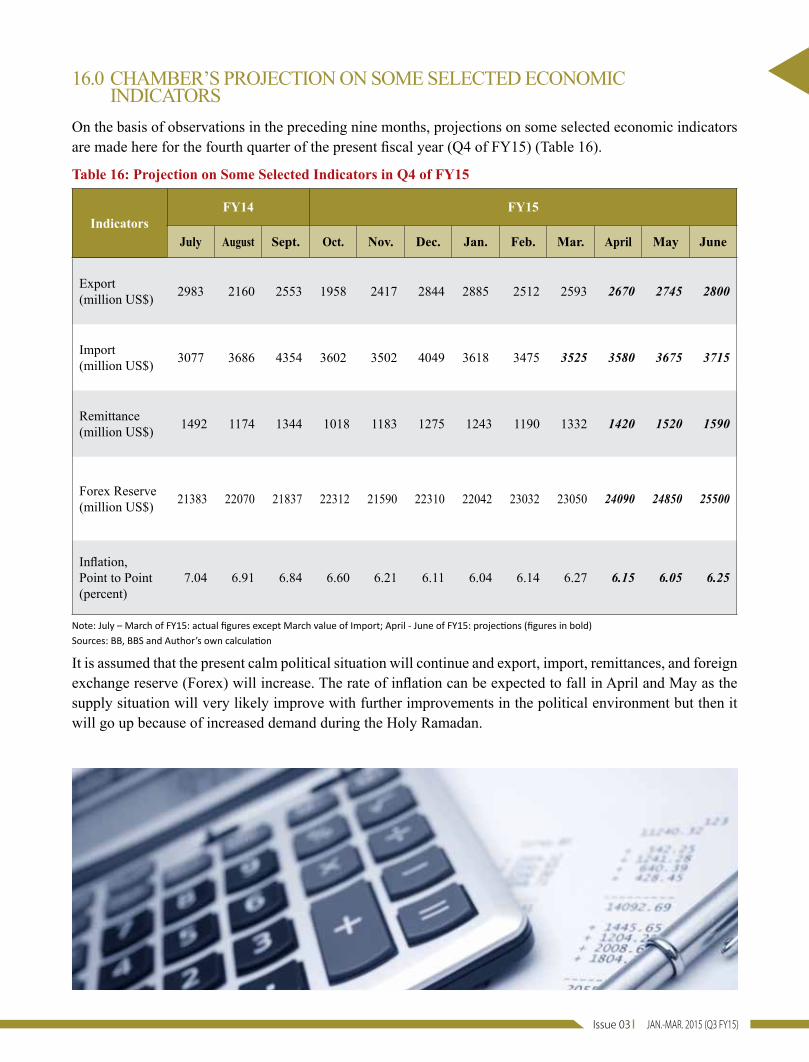

16.0 cHAMBER’S PROJEcTION ON SOME SELEcTED EcONOMIc INDIcATORS

On the basis of observations in the preceding nine months, projections on some selected economic indicators are made here for the fourth quarter of the present fiscal year (Q4 of FY15) (Table 16).

Table 16: Projection on Some Selected Indicators in Q4 of FY15

IndicatorsFY14 FY15

July August Sept. Oct. Nov. Dec. Jan. Feb. Mar. April May June

Export(million uS$) 2983 2160 2553 1958 2417 2844 2885 2512 2593 2670 2745 2800

Import (million uS$) 3077 3686 4354 3602 3502 4049 3618 3475 3525 3580 3675 3715

Remittance(million uS$) 1492 1174 1344 1018 1183 1275 1243 1190 1332 1420 1520 1590

Forex Reserve(million uS$) 21383 22070 21837 22312 21590 22310 22042 23032 23050 24090 24850 25500

Inflation, Point to Point (percent)

7.04 6.91 6.84 6.60 6.21 6.11 6.04 6.14 6.27 6.15 6.05 6.25

Note: July – March of FY15: actual figures except March value of Import; April - June of FY15: projections (figures in bold) Sources: BB, BBS and Author’s own calculation

It is assumed that the present calm political situation will continue and export, import, remittances, and foreign exchange reserve (Forex) will increase. The rate of inflation can be expected to fall in April and May as the supply situation will very likely improve with further improvements in the political environment but then it will go up because of increased demand during the Holy Ramadan.

24 QUARTERLY REVIEW

17.0 cONcLuDING OBSERvATIONS

Political violence in the quarter under review (January-March of FY15) of course disrupted economic activity and caused loss of life and property, but with extensive government

and private sector efforts economic activities returned to normalcy. The overall scenario is encouraging although slower export growth and slowing private sector investment remain a major challenge. Shortfall in revenue collection and weak ADP implementation are also worrying for the economy. There are nevertheless some brighter aspects. The inflation rate is on a declining trend since March of FY14. Internal demand remains vibrant riding on positive development in agriculture, dynamism in rural economy, healthy remittance in flow and wage hike in the garments sector. The fall in fuel prices in the world market has given a fiscal space to the government. The plummeting fuel oil prices in the international markets enabled government to slash its subsidy expenditure and enhance public allocations to priority sectors of the economy. Bank interest rates along with inflation have

seen downward trends with currency exchange rates remaining stable, which are indicators of macroeconomic stability and preconditions for economic expansion. Besides, political stability would be vital to ensure the sustainability of the growth process. The continuous efforts of the government to accelerate power, energy and transport sectors reforms would result in better environment for investment in future.

According to the Moody’s Investors Service, a global credit-rating agency, Bangladesh’s present economic situation is stable, but restive politics remains a looming risk to a robust performance. Bangladesh is rated Ba3 with a note of caution about the limiting factors stemming from both economics and politics. This rating reflects its track record of macroeconomic stability, a modest debt burden, and limited external vulnerabilities with an ample foreign reserve buffer. But a fractious political environment, narrow tax-revenue base, and low level of per capita income constrain the ratings. The credit-rating agency has now rated Bangladesh’s outlook as stable for the sixth consecutive year.