Northwest Colorado Oil & Gas Forum June 5, 2008 Northwest Colorado Oil & Gas Forum June 5, 2008.

Upload

russell-wadeCategory

view

213download

0

© OECD/IEA - 2008

NATURAL GAS

MARKEREVIEW

2008

Gas and the Sustainability Drive: what will it do the fuel mix?

Ian Cronshaw, Head of Energy Ian Cronshaw, Head of Energy Diversification DivisionDiversification Division

International Energy AgencyInternational Energy Agency

GIE Annual Conference, BucharestGIE Annual Conference, Bucharest23 October 2008 23 October 2008

OECD Europe--Gas Delivered

22,419

32,419

42,419

52,419

62,419

72,419

Jan

Feb Mar Apr

May Ju

nJu

lAug

Sep OctNov

Dec

Mill

ion

Cu

bic

Met

ers

2002 - 2007 Range 2006 2007 2008

Spain’s economy slows—but not gas demand

1,184

1,684

2,184

2,684

3,184

3,684

4,184

Jan

Feb Mar Apr

May Ju

nJu

lAug

Sep OctNov

Dec

Mill

ion

Cu

bic

Met

ers

2002 - 2007 Range 2006 2007 2008

Japan—demand growth surprisesJapan Annual Totals BCM % Change

2002 78.71 2003 86.37 9.7%2004 83.26 -3.6%

2005 84.98 2.1%2006 86.11 1.3%2007 95.96 11.4%

2008 52.48 11.9%

4,799

5,799

6,799

7,799

8,799

9,799

Jan

Feb Mar Apr

May Ju

nJu

lAug

Sep OctNov

Dec

Mill

ion

Cu

bic

Met

ers

2002 - 2007 Range 2006 2007 2008

Increase in Global Natural Gas Demand, 2005-2030

Natural gas demand grows by 2.1% per year through to 2030, from 2 854 bcm in 2005 to 4 779 bcm in 2030.

250

MiddleEast

Trans.economies

OECDN.

America

OECDEurope

China LatinAmerica

Rest of Asia

AfricaPacific

India

20%

13%12% 11%

10% 10% 9%

7%

5% 4%

0

50

100

150

200

300

350

400

OECD

billio

n cu

bic

met

res

% Share of increase in world primary natural gas demand, 2005-2030

OECD Power generation growthIncremental generation 2000-2007

745

315

11984

28

-57-126

1108

-200

0

200

400

600

800

1000

1200

Gas Coal Wind Other renewables

Nuclear Hydro Oil Total

TWh

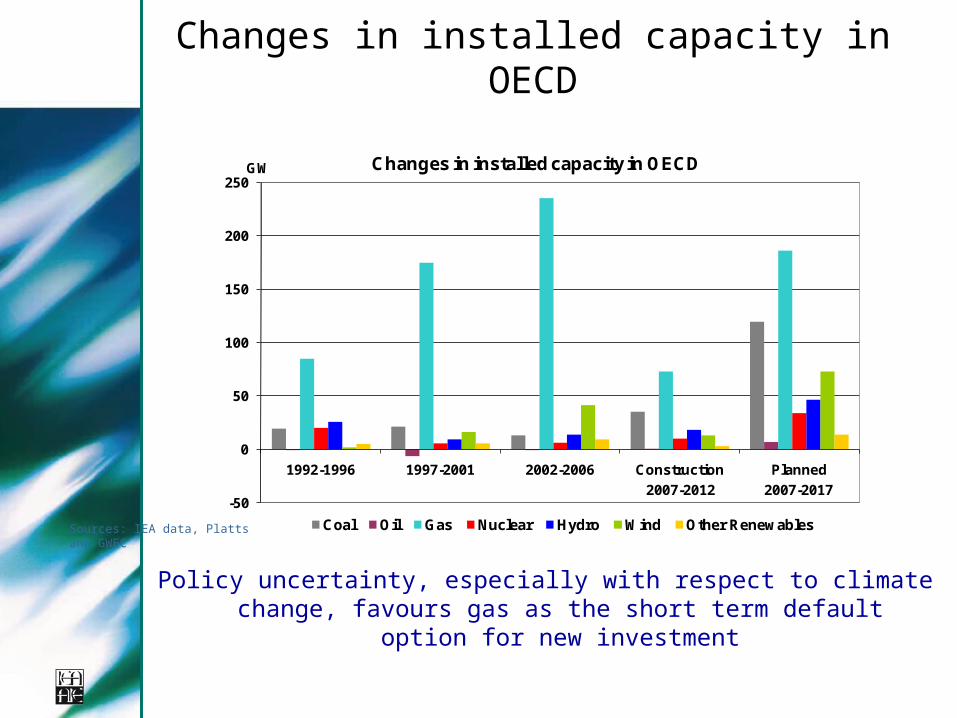

Changes in installed capacity in OECD

-50

0

50

100

150

200

250

1992-1996 1997-2001 2002-2006 Construction Planned

Changes in installed capacity in OECD

Coal Oil Gas Nuclear Hydro Wind Other Renewables

GW

2007-2012 2007-2017

Sources: IEA data, Platts and GWEC

Policy uncertainty, especially with respect to climate change, favours gas as the short term default option for new

investment

Share of gas-fired power in electricity output, and demand of gas for power

188

30

12

52

106

31

22

242

40

16

75

15 13

47

28

0%

10%

20%

30%

40%

50%

60%

70%

US UK Spain* Japan** Canada France Italy Germany

2005 2006 2020

* Spain forecast for 2010. ** Japan forecast for 2030. (Bcm at top of bars). Source: IEA data and forecasts from national government submissions

Gas-fired power in the US increased by 10% last year. All larger OECD countries foresee further increases in gas demand for

power.

Monthly average prices of gas and power in the UK, coal, and CO² in EU ETS

Investment:EPC unit costs in LNG rise sharply

Investment: Pipeline projects in Eurasia

Impact of financial crisis?

There is no major concern about gas consumption growth except timely construction of supply infrastructure

Financial crises may cause better sentiment for tangible projects with (fairly)stable return rate

Raw materials cost drop might be beneficial, but regulatory framework and formal difficulties associated with infrastructure projects that were a concern before the summer remain

Average Annual Power Generation Capacity Additions Average Annual Power Generation Capacity Additions in the “50% COin the “50% CO2 2 Reduction Scenario” Reduction Scenario” 2010 – 20502010 – 2050

Some summary observations

Demand growth still strong; both inside IEA and non member countries

Gas consumption growth strong in 2007-08 despite slowing/zero growth

Electricity and gas markets now strongly linked.

LNG grows fast, but demand grows faster

Europe imports by pipeline and LNG Global Gas Market Interactions Increase

Key message

In all scenarios, gas is a key source of energy for the foreseeable future

Gas meets some interlinked challenges:

security of supply, environment , affordability

Gas power generation seems to be the default option providing needed flexibility and back up to wind and hydro power generation