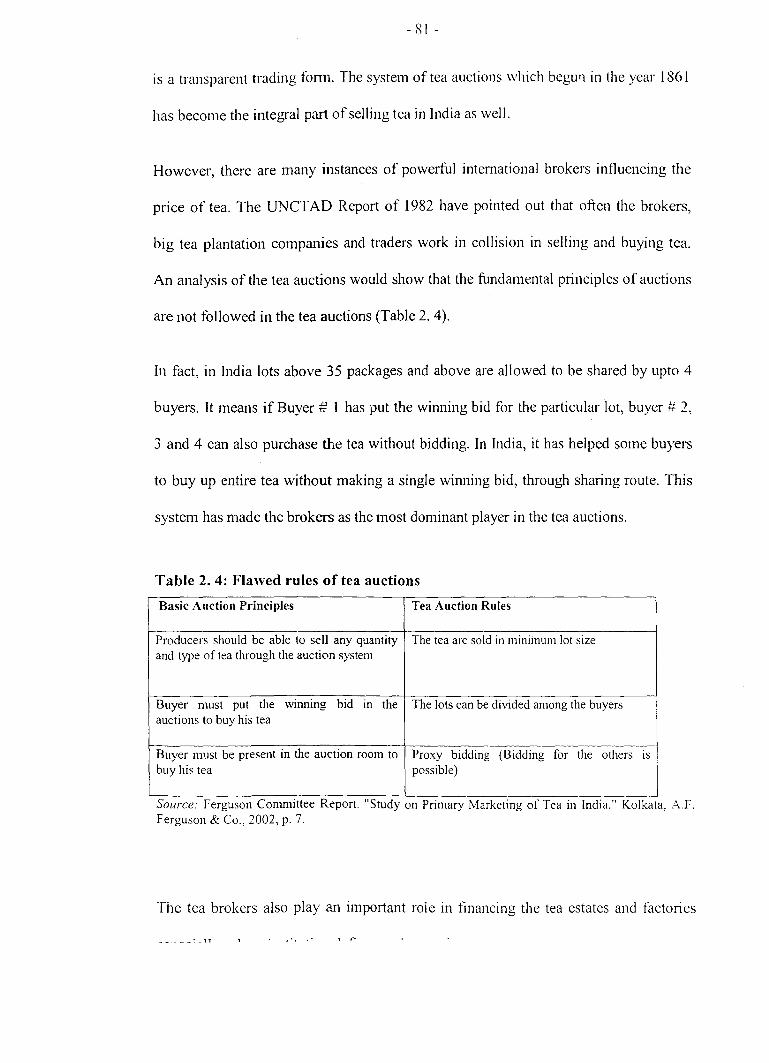

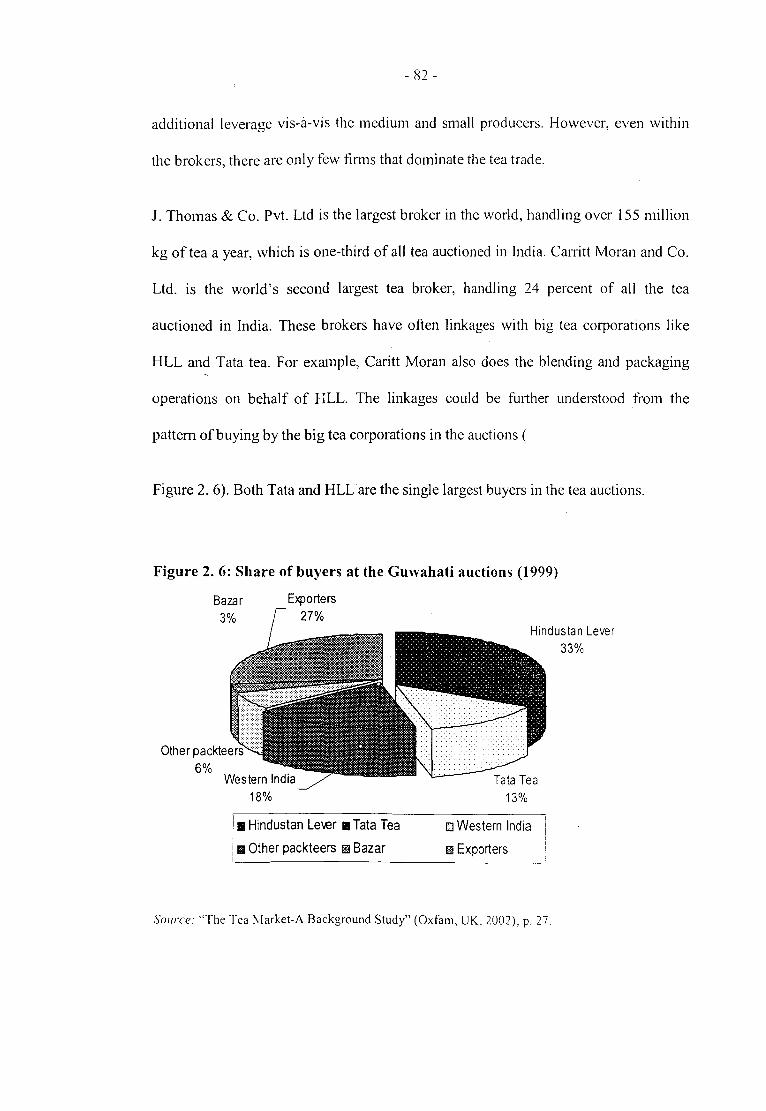

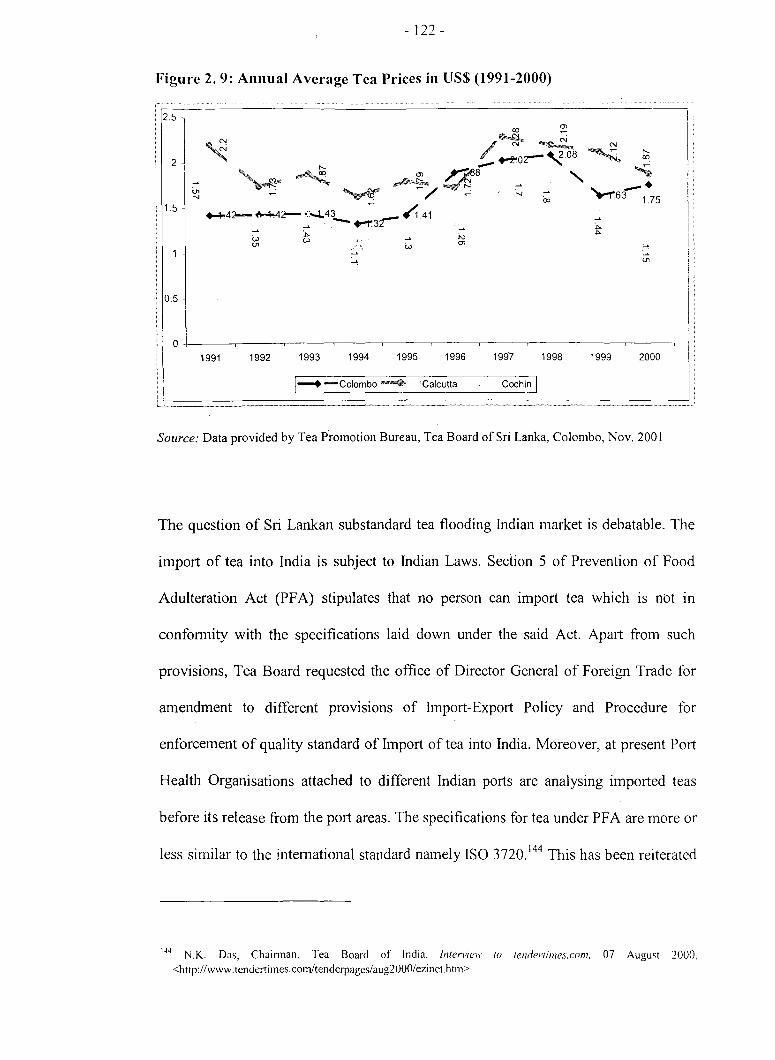

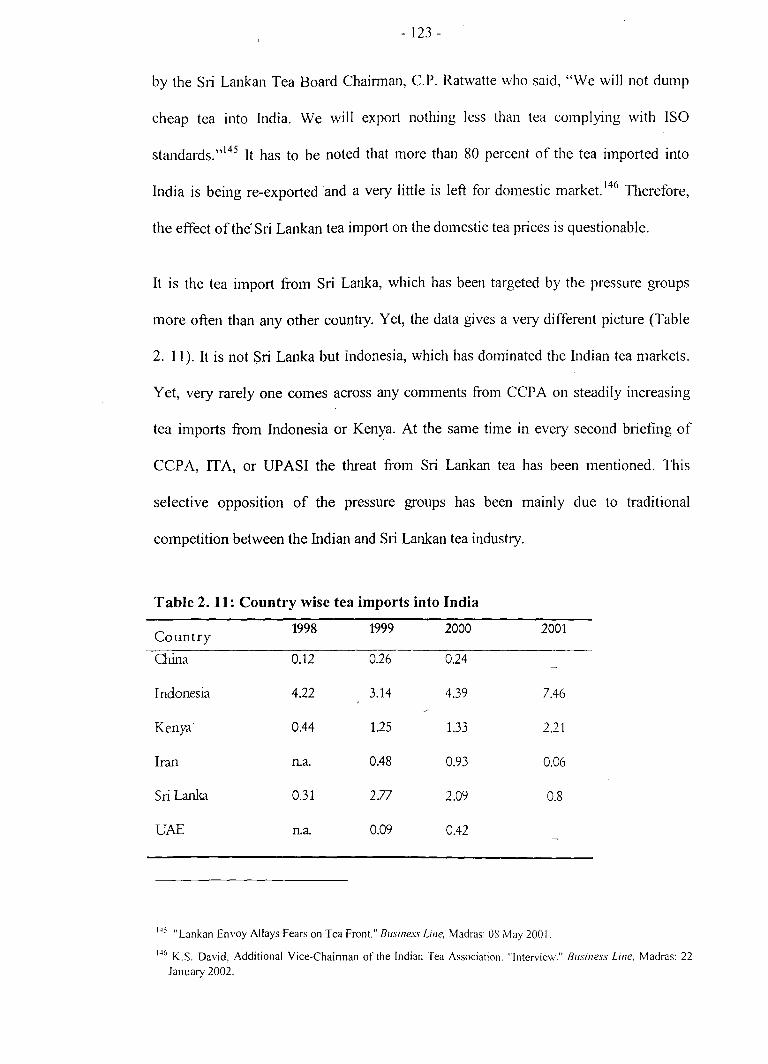

. form - Shodhganga : a reservoir of Indian theses @...

154

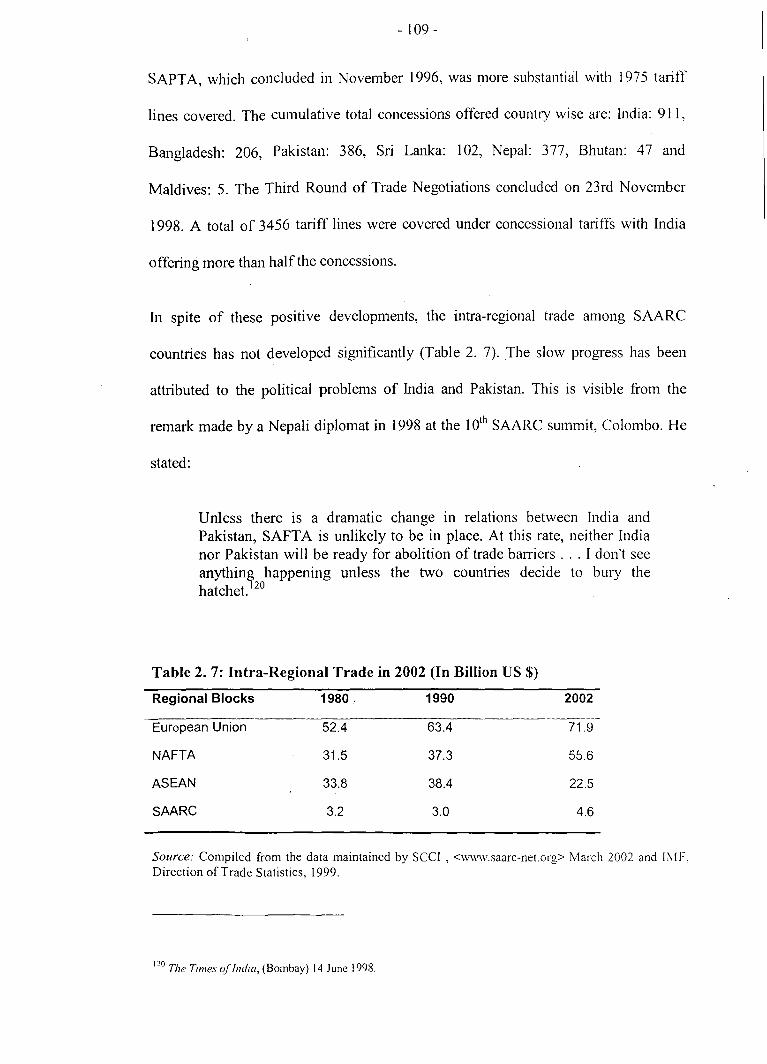

- 31 - Chapter II PRESSURE GROUPS AND TEA TRADE STRATEGIES OF INDIA AND SRI LANKA 1. Introduction Tea is one of the most important primary commodities produced in South Asia. The South Asian region accounts for 42 percent of the total black tea production in the world. It also constitutes about 39 percent of total world exports and 38 percent of consumption. Tea industry has a significant commercial importance for both India and Sri Lanka. The tea exports fetched around Rs. 15,028 million for India and Rs. 8250 million for Sri Lanka in 1998. 1 While Sri Lanka is the world's largest exporter of tea, India is the largest producer. India is also the largest (653 mi. Kg in 2000) and Pakistan, the third largest (110 ml. Kg in 2001) consumer of tea in the world. Hence, the tea trade strategies of both India and Sri Lanka have been formulated with regular intervention of their respective Governments. However, the pressure groups in the form of planters' associations, traders' associations, . brokers, and foreign agency houses were the most influential actors in the tea trade during the colonial period. After independence of India and Sri Lanka, the governments regulated the tea trade and tried to restrict the influence of the pressure groups. These regulations were in the form of various acts, legislations, and control orders. Sri Lankan Government even nationalised the tea plantations in 1975. 1 Mahendra P. Lama "Integrating the Tea Sector in South Asia: New Opportunities in the Global Market." Sowh Asian Survey, 8.1 (200 l ): pp. 67-97.

Transcript of . form - Shodhganga : a reservoir of Indian theses @...

- 31 -

Chapter II

PRESSURE GROUPS AND TEA TRADE STRATEGIES OF INDIA AND SRI LANKA

1. Introduction

Tea is one of the most important primary commodities produced in South Asia. The South

Asian region accounts for 42 percent of the total black tea production in the world. It also

constitutes about 39 percent of total world exports and 38 percent of consumption. Tea

industry has a significant commercial importance for both India and Sri Lanka. The tea

exports fetched around Rs. 15,028 million for India and Rs. 8250 million for Sri Lanka in

1998.1 While Sri Lanka is the world's largest exporter of tea, India is the largest producer.

India is also the largest (653 mi. Kg in 2000) and Pakistan, the third largest (110 ml. Kg in

2001) consumer of tea in the world. Hence, the tea trade strategies of both India and Sri

Lanka have been formulated with regular intervention of their respective Governments.

However, the pressure groups in the form of planters' associations, traders' associations, . brokers, and foreign agency houses were the most influential actors in the tea trade during

the colonial period. After independence of India and Sri Lanka, the governments regulated

the tea trade and tried to restrict the influence of the pressure groups. These regulations

were in the form of various acts, legislations, and control orders. Sri Lankan Government

even nationalised the tea plantations in 1975.

1 Mahendra P. Lama "Integrating the Tea Sector in South Asia: New Opportunities in the Global Market." Sowh Asian Survey, 8.1 (200 l ): pp. 67-97.

- 32-

This Chapter argues that these pressure groups continued to exer1 significant influence on

the tea trade policies even after independence. Although. the pressure groups were less

dominant, they were active even during the nationalised phase of tea plantations in Sri

Lanka. In the 1990's, India embarked on a policy of economic liberalisation. During the

same time ( 1992), Sri Lanka began privatising its tea plantations as well. Under these

policies the private sector has begun to play a key role. In this kind of environment, the

pressure groups have become very influential. They have successfully lobbied with the

government to amend or to revoke various acts, regulations, and control orders operative in

the tea industry of India and Sri Lanka.

2. Pressure groups and Indian tea trade strategies

The Indian tea trade strategies are generally formulated on the basis of intense negotiations

·between the government and the private interests in the tea industry. The Consultative

Committee of Plantation Association (CCPA) represents the private interest in the tea

industry and it is composed of I 0 planters' associations. It is a forum for the tea planters to

discuss common problems. However, it is Indian Tea Association and United Planters'

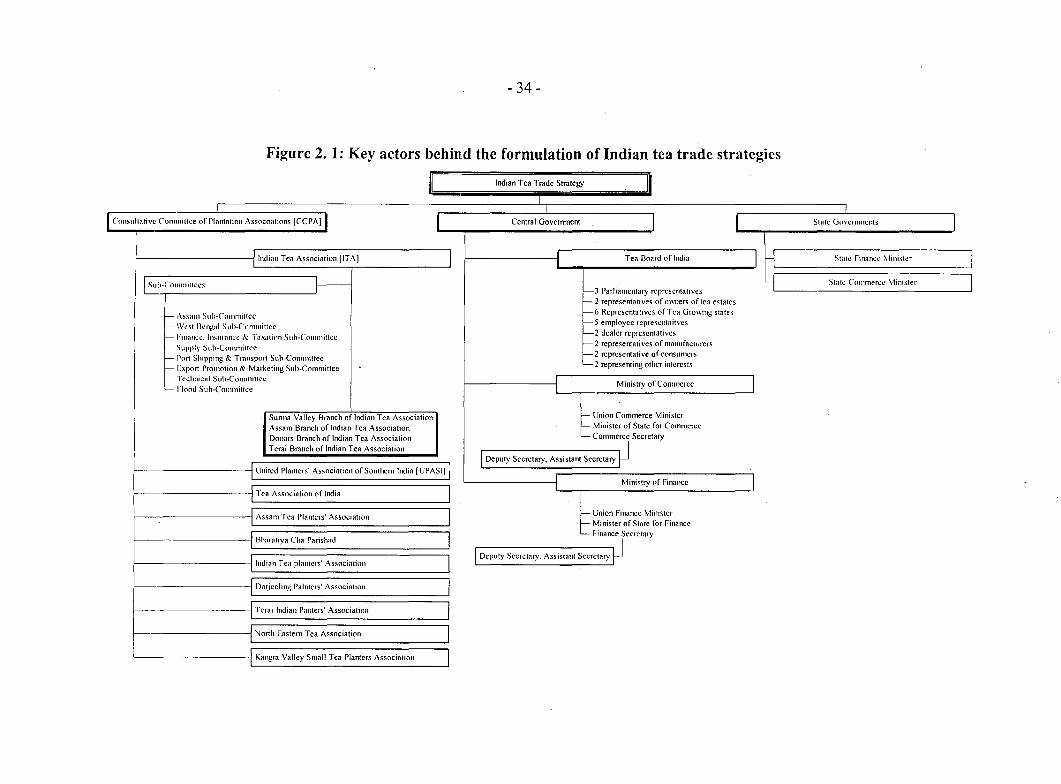

Association, which are the two most .influential actors within CCPA (Fig 2.1 ). The CCPA

acts as a strong pressure group for the planters and regularly lobbies with the government

officials from Central Government like Ministry of Commerce and Ministry of Finance.

However, the focus of lobbying by the pressure groups has been the Tea Board of India, a

commodity board under the administrative control of the Ministry of Commerce,

Government of India (Error! Reference source not found.). The Tea Board acts as a

bridge between the decision makers and the pressure groups. The CCPA and other pressure

groups have institutionalised channel of access to the Tea Board, which is also responsible

- 33 -

Figure 2. I). The Tea Board acts as a bridge between the decision makers and the

pressure groups. The CCP A and other pressure groups have institutionalised channel

of access to the Tea Board, which is also responsible for the implementation of the

government regulations and policies with regard to tea industry.

2.1 Tea Board of India

The Tea Board of India had its origin in the Indian Tea Market Expansion Board and

the Indian Tea Licensing Committee, the government regulatory bodies under the

British rule. After independence, a Central Tea Board was fonned on 1st August 1949

under the Central Tea Board Act, 1948 in place of Indian Tea Market Expansion

Board. The Tea Board took over the functions of the Central Tea Board and the Indian

Tea Licensing Committee under the Tea Act, 1953. The Tea Act aimed to centralize

control over the Indian Tea Industry, the cultivation of tea in India, export of tea and

to levy excise duty on tea produced in India. A Chairman, appointed by the

Government oflndia, heads the Tea Board India.

The Board also elects from among its members a Vice-Chairman who exercises such

of the powers and discharges such duties of the Chairman as may be delegated to him

by the Chairman.

-34-

Figure 2. 1: Key actors behind the formulation of Indian tea trade strategies

II Indian Tea Trade Strategy II

L Consultative Committ~e of Plantation Assocoations [CCPA] I Central Govenunent I I State Govcmments I

Indian Tea Association (ITA] I Tea Board of India J -l State Finance 1\ linister I I J Suh-Comminccs ~ State Commerce Minister

f-- 3 Parliarncntaiy representatives r-2 representatives of O\\·llers of tea estates

1--- Assam Suh-Commilfcc r---6 Representatives of Tea Growing st<ttes

\--\Vest Bengal Sub-Committee t--5 employee rcprcscntaitvcs

r- 1-'inallt.:c. Insurance & Taxation Sub-Committee f--2 dealer rep1csentatives

t-- Supply Sub-Committee r---2 representatives of manufactnrers

I-- Pot1 Shipping & Transp011 Sub-Committee r---2 representative of consumers

1-- Expo11 Promotion & Marketing Sub-Committee . L..-2 representing other interests

I-- Technical Sub-Committee Ministry of Commerce I L.._ flood Sub-Committee

Sunna Valley Branch of Indian Tea Association - Union Commerce Minister

Assam Branch oflndian Tea Association -Minister of State for Commerce

Dooars Branch of Indian Tea Association Commerce Secreta!)'

Terai Branch of Indian Tea Association J Deputy Secretcuy, Assistant Sccreta1y

United Planters' Association ofSouthcm India [UPASIJ I Mini~hy of Finnncc I ~ Tea Association of India I

Assam Tea Planters' Association I t- Union Finance Minister t- Minister of State for Finance

Bhnratiyn Cha Pmishad I L- Finance Secretary

J

I I Deputy Secretary. Assistant Secreta!)'

Indian Tea planters' Association

I Darjccling Painters' Association I !---· Terai Indian Panters' Association I

I Nm1h Eastem Tea Association I Kangra Valley Small Tea Planters Association I

- 35 -

Besides the Chairman and Vice Chaim1an, the Board represents vanous interest

groups of the tea industry. They are as following:

II 3 persons representing Parliament

• 2 persons representing owners of tea estates and gardens and growers of tea

• 6 persons representing the government of the principal tea-growing States

namely Assam, West Bengal, Tripura, Tamil Nadu, Kerala and Himachal

Pradesh

• 5 persons representing persons employed in tea estates and gardens

• 2 persons representing dealers including both exporters and internal traders

of tea

• 2 persons representing manufacturers of tea

• 2 persons representing consumers

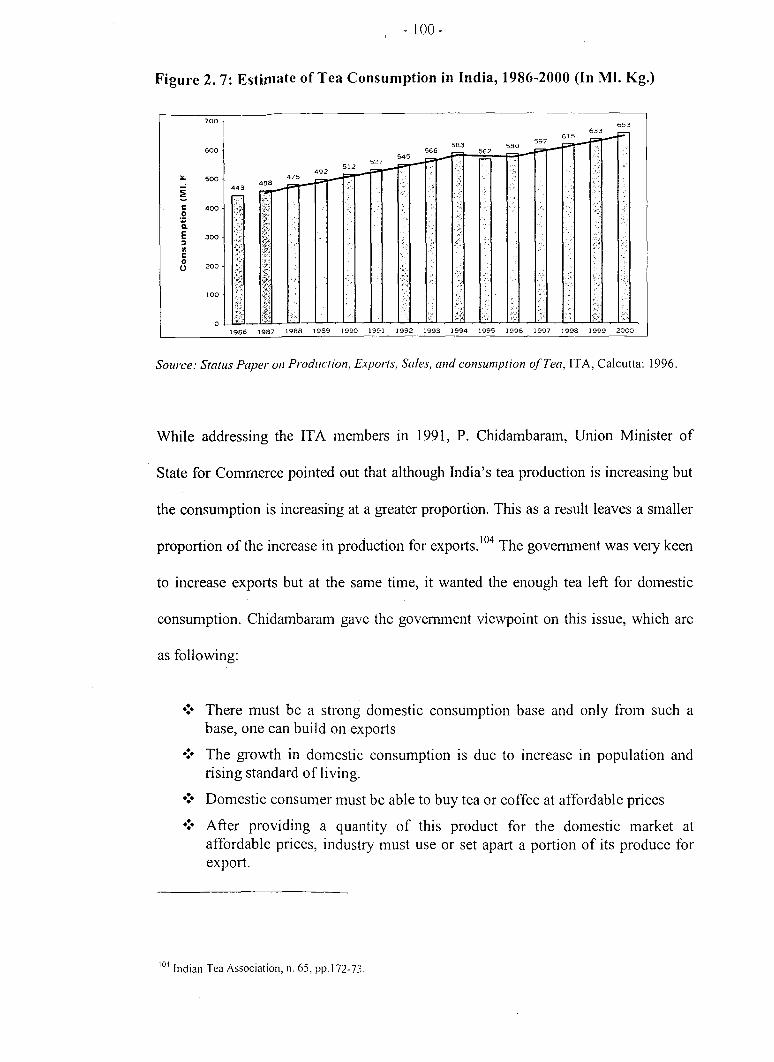

• 2 persons representing other interests

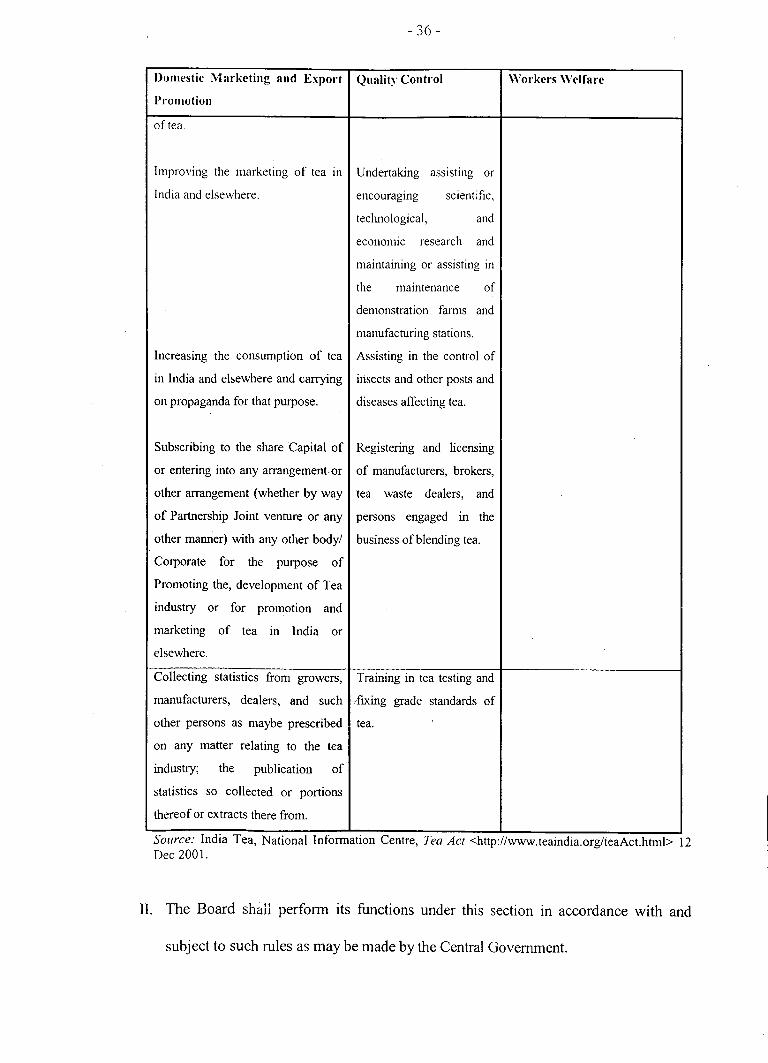

2.2 Functions of the Tea Board

The Tea Act of 1953 specifically mentions the following functions of the Tea Board:

I. It shall be the duty of the Board to promote, by such measures as it thinks fit, the

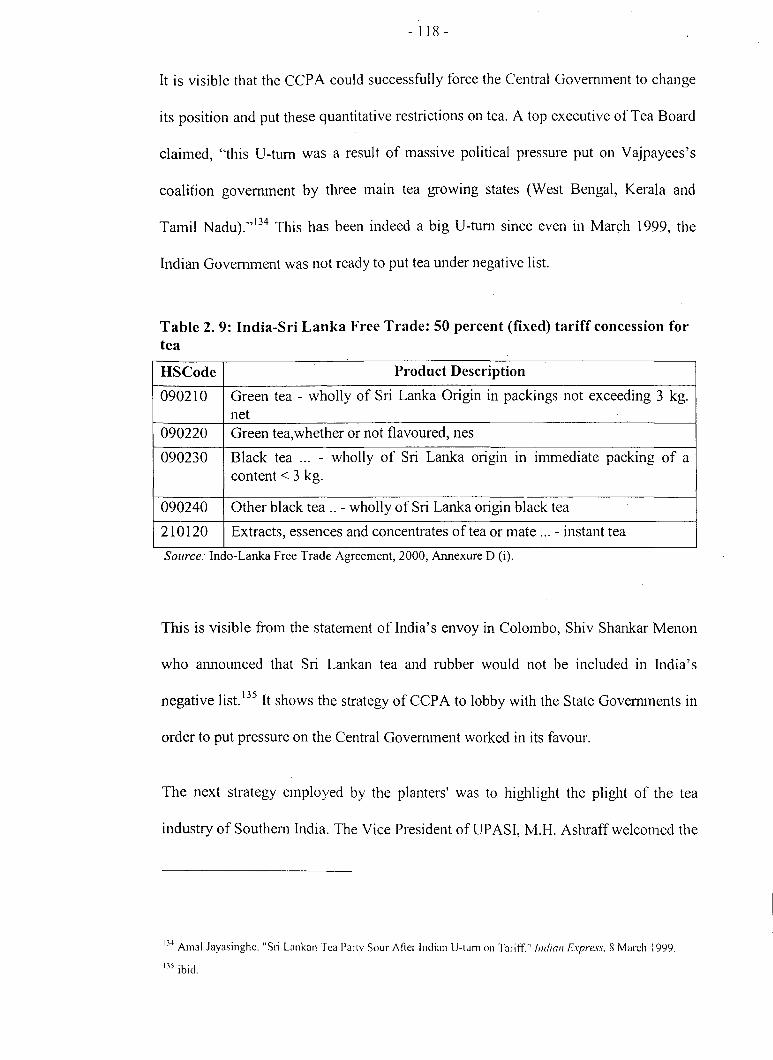

development of the tea industry under the control of the Central Government. Some

of the important functions oflndian Tea Board are as following:

Table 2. 1: Various functions of Tea Board oflndia under Sub-Section (1) of the Tea Act

Domestic Marketing and Export Quality Control Workers Welfare

Promotion

Regulating the sale and export of Regulating the production Securing better working

tea. and extent of cultivation of conditions and the ..

provisions

tea. and improvement of amenities

and incentives for workers.

Promoting co-operative efforts Improving the quality of

among growers and manufacturers tea

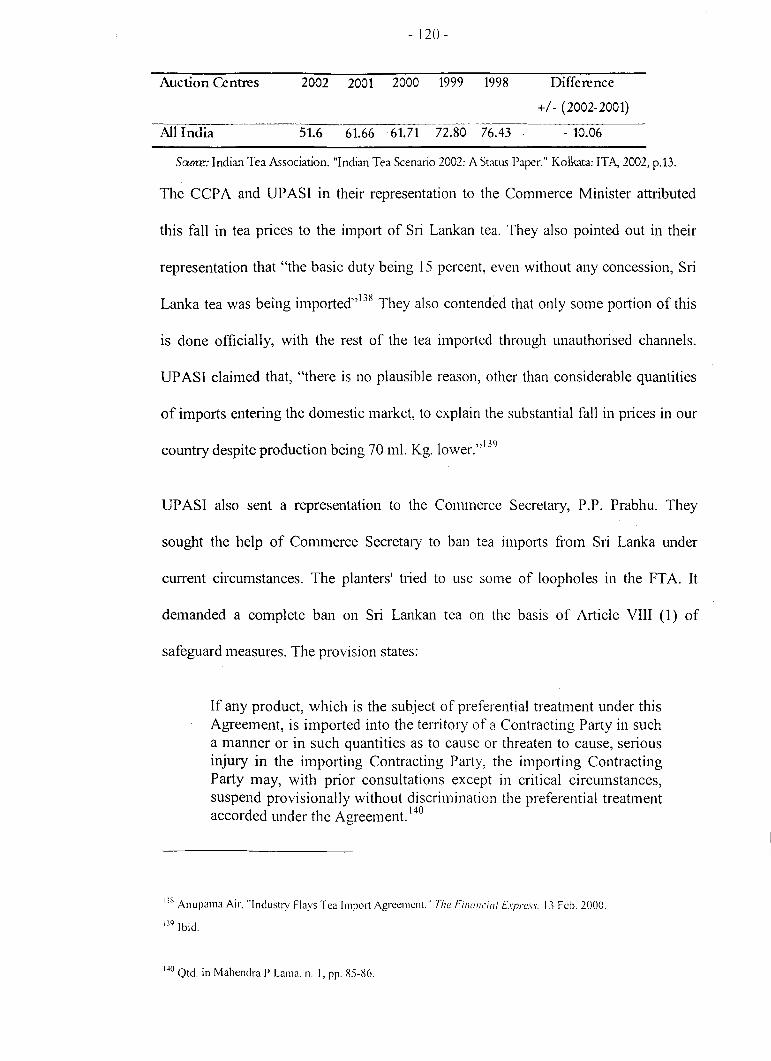

- 36-

Domestic Marketing and Exp01·t Quality Control

Promotion

of tea.

Improving the marketing of tea m Undertaking assisting or

India and elsewhere. encouraging scientific,

teclmological, and

economic research and

maintaining or assisting in

the maintenance of

demonstration farms and

manufacturing stations.

Increasing the consumption of tea Assisting in the control of

in India and elsewhere and canying insects and other posts and

on propaganda for that purpose. diseases affecting tea.

Subscribing to the share Capital of Registering and licensing

or entering into any arrangement or of manufacturers, brokers,

other arrangement (whether by way tea waste dealers, and

of Partnership Joint venture or any persons engaged in the

other manner) with any other body/ business of blending tea.

Corporate for the purpose of

Promoting the, development of Tea

industry or for promotion and

marketing of tea in India or

elsewhere.

Collecting statistics from growers, Training in tea testing and

manufacturers, dealers, and such ,fixing grade standards of

other persons as maybe prescribed tea.

on any matter relating to the tea

industry; the publication of

statistics so collected or portions

thereof or extracts there from.

\Vorkers \Velfare

Source: Indta Tea, NatiOnal InformatiOn Centre, Tea Act <http://www.teamdia.org/teaAct.html> 12 Dec 2001.

II. The Board shall perform its functions under this section in accordance with and

subject to such rules as may be made by the Central Government

- 3 7-

111. The following departments perfonn the above-mentioned functions and activities of

the Tea Board:

• Secretariat: Administrative work and co-ordination of the activities of the various departments.

• Finance: Internal audit and maintenance of Board's accounts. • Development: Administration of financial assistance scheme and assistance

to the industry for procurement for distribution and movement of essential inputs.

• Research: Grant loans to research organizations and maintaining internal re3earch facilities.

• Licensing: Regulates production, exports, and implementation of the Tea Waste (Control) Order.

• Tea Promotion: Marketing of tea in India and increase of exports. • Statistics: Collection of statistical data and undertaking cost studies. • Labour \Velfare: Implementing various labour welfare measures in the tea

industry. • Law: Deals with various miscellaneous legal matters arising in functional

departments.

The powers and functions vested upon Tea Board by the government make it the most

important organisation with regard to tea trade policy making in India. Therefore,

most of the lobbying by the pressure groups is focused on the Tea Board. The Tea

Board also encourages representation from the private sector with regard to various

issues related to tea trade. This is evident from the institutionalised system of

interaction between the private interests and the Tea Board.

3. Consultative Committee of Plantation Associations (CCPA)

With the independence of India, many British tea estates were transferred to Indian

buyers. This led to the emergence of new groups of proprietors and increase in the

number of tea producers' associations.2 Ministers and government officials were liable

to find themselves receiving several delegations on the same subject. Therefore, the

government officials were very keen that the tea industry should form a federation of

2 Parcivai.Griffiths, The History of the Indian tea Industry, (London: Weidenfeld and Nicolson, 1967), pp. 536-37.

- 38-

tea producers. Most of the producers were also in favour of this idea since it would

have obviated the danger of conflicting representations from different organizations.

Yet, they had the fear that the smaller associations would be in a disadvantageous

position vis-a-vis the bigger associations if the voting rights were given on the basis of

production or acreage. At the same time, the bigger associations were apprehensive of

being outvoted on vital matters by the smaller associations if all the association were

given equal rights and status.

Furthermore, the individual associations were unwilling to accept limitations on their

right to approach the govenunent directly. However, most of the tea associations also

felt that they were unable to take unified action because of disagreements with regard

to the organizational matters. Finally, in 1956 a Consultative Committee of Tea

Producer Associations (CCTPA) was formed with the following members:

• The Indian Tea Association (IT A), Calcutta

• The United Planters' Association of Southern India (UP ASI)

• The Indian Tea Planters' Association, Jalpaiguri

• The Assam Tea Planters' Association, Jorhat

• The Bharatiya Cha Parishad, Calcutta

• The Sunna Valley Indian Tea Planters' Association, Calcutta

• The Terai Indian Planters' Association

• The Tripura Tea Association, Calcutta

The major objectives of the CCTP A were:

To discuss matters of common interest and to endeavour to arrive at uniform and unanimous views on rp1estion of policy, while leaving to

- 39-

individual associations complete freedom of action and being satisfied, where unanimity was unattainable, with an agreement to differ. 3

The basic objective of CCTPA was to jointly lobby with the decision makers on

behalf of the planters on major policy issues that were affecting the tea producers. The

first meeting of the CCTP A was held in 91h August 1956. It was agreed that the

committee would meet at regular intervals and whenever the need arose. It was agreed

that there would be no voting and IT A, Calcutta, would look after the secretarial work.

It was also decided that Chainnan of ITA would be ex-officio Chairman ofCCTPA. It

could be observed that a lot of planning was done before deciding the structure of

CCTP A. Since no formal' constitution or voting system was adopted in CCTP A, it was

possible for the larger and smaller tea planters' associations to cooperate in a single

forum at the same time continue to function autonomously. The formation of CCTP A

in 1956 highlights the endeavour of the tea planters' to avoid conflict and to fonn a

strong pressure group in order to lobby with the government in a united manner for

common interests.

In 1964, the constituent associations felt that the scope of the CCTP A should be

enlarged to cover other plantation crops, namely, coffee, rubber and spices and the

name of the organisation was consequently changed to Consultative Committee of

Plantation Association (CCP A). 4 The present membership of CCP A is as following:

• The Indian Tea Association, Calcutta • The United Planters' Association of Southern India •• Tea Association of India

·'Griffiths, n.3, p. 536-37.

4 India International Mi/lenium Tea Convention (CCPA, Calcutta, March 2000), p.3.

- 40-

• The Assam Tea Planters' Association, Jorhat • The Bharatiya Cha Parishad, Calcutta • The Indian Tea Planters' Association, Jalpaiguri • Da1jeeling Planters' Association • Terai Indian Planters' Association • North Eastern Tea Association • Kangra Valley Small Tea Planters' Association.

Although, with the fonnation of CCP A many other plantation industries were brought

into its gambit, yet as we can see from the list of the members the association was

overwhelmingly dominated by tea planters and hence, it remained essentially a

pressure group for the tea producers. While the individual proble!'ns of their members

have been left to the different associations to handle, on matters of common or

industry wide issues, the CCP A has been speaking authoritatively and in one voice on

matters of tea production, research, taxation, industrial relations, labour welfare, tea

. d 5 promotion an exports.

Most of the member associations of CCP A are small and were set up by the Indian tea

planters after independence. Some of the tea planters of Indian origin felt that the

smaller Indian tea plantations are not adequately represented in bigger associations

like IT A and UP AS I. 6 There was a gulf of difference and social segregation among

the entrepreneurs in the trade. The Indian planters' felt a strong desire to be identified

with their cwn social exclusiveness blended with heritage, nationalistic ethos, and

concern for safeguarding the legitimate interests of the Indian planters and ventilation

5 ibid.

6 Griffiths, n.3, p.534-3 7.

- 41 -

of their grievances to the govemment machinery. 7 Hence, they fom1ed their own

associations. Brief profiles of some ofthese smaller associations are as follows:

3.1 Tea Association of India (TAl)

T AI owes its origin to some Indian entrepreneurs. These entrepreneurs fired by the

national spirit, entered the field of this industry, and developed the tea plantations. As

the number of Indian planters' had started rising rapidly, the need was felt to discuss

problems and exchange ideas among themselves. Thus, T AI was fmmed at a general

meeting of indigenous tea planters held on 2ih January 1956 with a view to promote

and protect their common interests and to promote trade and commerce in the domain

of tea industry. The T AI is now the second largest tea producers' association in North

India. T AI is also affiliated to the Indian Chamber of Commerce, Calcutta and

Federation oflndian Chamber of Commerce and Industry (FICCI).

3.2 The Indian Tea Planters' Association (ITPA)

The Indian tea planters' fonned ITP A in 1915 since they felt that they were not

adequately represented in the bigger tea planters' associations. With the establishment

ofiTP A, the bargaining power of the Indian planters' increased in a major way. It has

seen dramatic increase in its membership from 10 member tea estates in the beginning

to over 1 04 at present. ITP A has represented the interest of the planters' from West

Bengal as well as Assam and is the convenor of the CCP A, West Bengal branch.

7 India /nrernationa/ Millenium Tea ConFention, n.5, p.5.

- 42-

3.3 The Assam Tea Planters' Association (A TPA)

The A TP A was fonned in 23'd June 1933 at Dibrugarh, m response to a strong

movement 111 favour of fostering unity among the Indian tea planters. The A TP A

aimedto represent the Indian tea planters' with regard to the problems faced by them

like finance, sales, and transport. In the beginning, the association was known as

Assam Valley Indian Tea Planters' Association. The name of the association was

changed to Assam Tea Planters' Association (ATPA>"in 1947 after the independence

of India to cover the whole of Assam. At present A TP A represents around 200 tea

estates of various sizes and ownership.

3.4 The Bharatiya Cha Parishad (BCP)

The BCP fonned by the Indian tea planters' from Assam, Bengal, and Tripura. The

association was fonned on 16th September 1944 and was known as Assam Bengal

Indian Tea Planters' Association. It was renamed as Bharatiya Cha Parishad (BCP) in

March 1956. At present, the membership of BCP is confined to the Assam valley

only.

3.5 Terai Indian Planters' Association (TAPA)

TAP A was fonned in 1928, with only 28 member estates. It was formed because of a

friction between the Indian and British planters' in Terai Planters' association. The

Indian planters' felt that their interests were ignored and the British planters' were

getting preference in the Terai Planters' association. Hence, they decided to come out

of the association and formed Terai Indian Planters' Association.

- 43-

3.6 North Eastem Tea Association (NETA)

NETA was fonned by the smaller and medium planters' mainly located around

Golaghat district of Assam in July 1981. The focus of NET A from its inception has

been on the small and marginal tea estates. NET A was accorded the membership of

CCP A on 31st December 1992.

3. 7 Dmjeeling Planters' Association (DPA)

DP A was formed as early as in 1892. Unlike the other associations mentioned above,

DP A was not fonned to bring together the Indian planters. Therefore, it was not

surprising that DPA got affiliated to the Indian Tea Association (ITA), the bigger and

more resourceful tea planters' association in 1910. On 1st December 1951, under the

post Independence scenario, DP A in their last extraordinary meeting unanimously

decided to dissolve the association and transfer all its assets and liabilities to the newly

formed association called the Dmjeeling Branch of the Indian Tea Association

(DBIT A). However, some of the owners of Dmjeeling tea estates felt that although

IT A was fulfilling most of its requirements but it is necessary to highlight the issues

unique to Datjeeling like development, promotion, and protection of Darjeeling Tea.

Hence, they unanimously dissolved OBIT A and resurrected Datjeeling Planters'

Association (DPA) on 201h December 1983.8

The focus of DP A has been to promote the common interests of all persons engaged in

the cultivation and/or production and/or marketing and/or processing of Darjeeling

Tea. It also considers and discusses all matters related to growing, cultivation,

5 Datjecling Planters' Association, <http://WW\v.daijeelingtea.comldpa.htm> 5 February 2002.

- 44-

production, and marketing of Dmjeeling Tea and to enhance the contribution of the

Dmjeeling Tea Industry to the growth and development of the Indian Economy. 9

It could be seen that the above-mentioned members of CCP A are smaller regional

associations. These associations were fonned by the Indian planters' who felt that

associations having only Indian planters' as members will enhance their bargaining

power vis-a-vis British government. They are concerned with specific problems

related to their tea estates spread over a smaller geographical area. However, after

independence, there was a change in the attitude of the Indian tea planters'

associations towards IT A and UP AS I. They were keen to cooperate with each other.

This led to the fonnation of CCP A. These associations agreed to the greater role of

IT A and UP ASI, which have mainly dominated CCP A. Hence, the secretariat of

CCP A is located in the office of IT A and the Chainnan of IT A is ex -officio the

Chairman of CCP A. The President of UPASI is ex-officio Vice-Chairman of the

CCPA.

3.8 United Planters' Association of Southern India (UPASI)

UP ASI was founded in 1893 and is the apex organisation of the producers of tea,

coffee, rubber, and spices. The membership of association comprises small and large

propriety holdings as well as corporate bodies. The three state planters' associations

from Karnataka, Kerala and Tamil Nadu along with various district-planting

associations are affiliated to UP AS I.

9 Darjeeling Planters' Association, n. 9.

- 45-

During the period 1860 to 1870 the plantation industry had become important and

many district planters' associations were fonned in Wynaad, Coorg, North Mysore.

Travancore, the shevaroy hills, and Kolagheny hills of southem India. However, these

organisations were working independently and had no central organisation. The idea

of fonning a central organisation in order to lobby with the govenunent was

propounded by Digby T. Brett, Chaim1an of the North Mysore Planters' Association.

Brett took initiative to call a conference in Bangalore on August 28111 1893. In that

conference, it was decided to fonn United Planters' Association of Southem India

(UPASI).

The membership was restricted to the District Planters' Association and there was no

provision for individual membership. However, the members felt that various

influential proprietors and finns from southern India should also be incorporated in

UPASI so that it can play major role with regard to policy making in the plantation

sector. Eventually, in 1936 it was decided to convert UP ASI into an association of

proprietors, finns and district associations, divided by products into sections. 10

UP ASI was reorganised in 194 7 after Indian independence when many Indian planters

joined the association." D.C. Kothari became the first Indian President of UPASI. 12

UPASI went through another reorganisation on March 26, 1955. The member

associations from Madras, Travancore-Cochin, Mysore and Coorg took over the

responsibility of dealing with labour related issues along with other general planting

10 Griftith, n.3, p544-55.

11 Like ITA in the Northern tea plantations, UPASI remained mainly a European association until India's independence.

12 S. Muthiah, A ?laming Century: The Firs/ Hundred Years o{The L 'niled Planlers' Ass,?Ciation ofSoulhern /ndiC! (Coonoor, I994), pp. 265-68.

- 46-

problems within their own geographical territmies. This made UPASI a coordinating

and advisory body only. 13

At present, an elected Executive Committee (EC) manages the affairs of the

association. This Committee accords representation to all crops, size-groups and

states. There are nominated members as well in the fom1 of representatives from state

planters' associations, legal advisers and co-opted members. The EC fonns various

independent committees to focus on one particular commodity. The present

committees are as follows:

• Tea

• Coffee

• Rubber

• Spices

• Labour Liaison

• Tea Technical

• Rubber Technical

• Taxation and Finance

The President, Vice President, and the immediate Past President are the trustees. They

oversee the working of the Secretariat, Research Institute and advice Executive

Committee on various aspects of functioning of UP AS I.

Over the years, UP ASI has become one of the largest organisation of the plantation

produces in India. Yet, the role of UP ASI with regard to policy making in the tea

industry has not been as prominent as that of Indian Tea Association (ITA). The

reason being that tea is not the sole focus of UPASI. It also takes active interest in the

13 Muthiah, n.l3, pp.270-71.

-47-

affairs of other commodities like coffee, rubber, spices, and cardamom. 14 In fact, the

individual proprietors of coffee estates in Mysore and Coorg were the moving force

behind the fonnation ofthe UPASI. 15

Furthennore, individuals have always dominated UP ASI in contrast to IT A in which

big multinational companies acquired great influence at an early stage. The influential

members of UPASilike "C. Marsh, Congreve and J.J. Murphy looked at the United

Planters' Associations matters entirely from the proprietary planters' point of view and

suspected the big companies and Agency Houses"16 Most of the lobbying activities

were left to the sturdy individual proprietors, who could not play such dominant role

in formulating tea trade strategies as the well organised IT A. Even at present, these

equations have not changed and ITA continues to be the most influential pressure

group in the Indian tea industry.

4. Indian Tea Association (ITA)

ITA is the premier and the oldest organisation of tea producers in India. It has played a

major role in formulating policies and initiating action towards the development and

growth of the tea industry. ITA has 425 member gardens and represents over 60

percent of India's total tea production. 17 The ITA member gardens provide direct

employment to more than 400,000 people. Moreover, almost all the multinational and

national tea companies are members of IT A.

14 India is the third largest producer of rubber next only to Thailand and Indonesia, accounting for 9.1 per cent of the world output and most of these rubber plantations are members of UPASI.

15 Griffith, n.3, p.540-41.

16 Ibid.

17 India International Millennium Tea Convention, n.S, pp.S-6.

- 48-

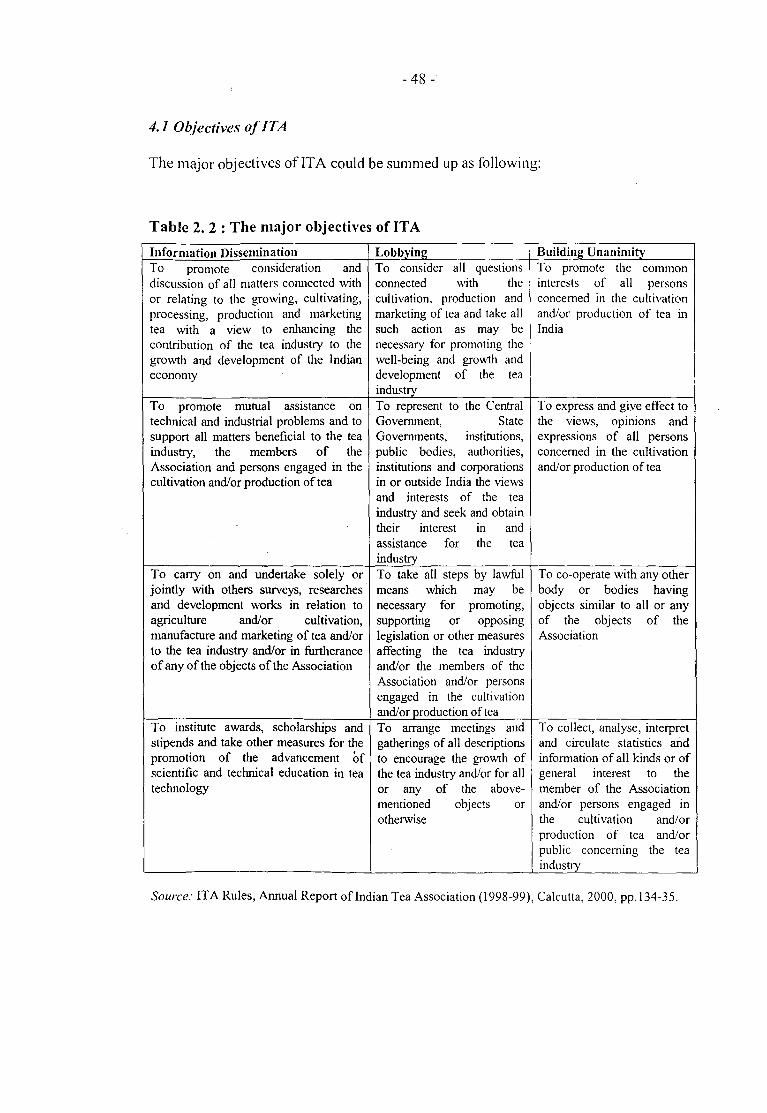

4.1 Objectives of/TA

The major objectives of IT A could be summed up as following:

Table 2. 2 : The major objectives of IT A

Information Dissemination To promote consideration and discussion of all matters connected with or relating to the growing, cultivating, processing, production and marketing tea with a view to enhancing the contribution of the tea industry to the growth and development of the Indian economy

To promote mutual assistance on technical and industrial problems and to support all matters beneficial to the tea industry, the members of the Association and persons engaged in the cultivation and/or production of tea

To carry on and undertake solely or jointly with others surveys, researches and development works in relation to agriculture and/or cultivation, manufacture and marketing of tea and/or to the tea industry and/or in furtherance of any of the objects of the Association

To institute awards, scholarships and stipends and take other measures for the promotion of the advancement of scientific and technical education in tea technology

Lobbying To consider all questions connected with the cultivation, production and marketing of tea and take all such action as may be necessary for promoting the well-being and growth and development of the tea industry To represent to the Central Government, State Governments, institutions, public bodies, authorities, institutions and corporations in or outside India the views and interests of the tea industry and seek and obtain their interest in and assistance for the tea industry To take all steps by lawful means which may be necessary for promoting, supporting or opposing legislation or other measures affecting the tea industry and/or the members of the Association and/or persons engaged in the cultivation and/or production of tea To arrange meetings and gatherings of all descriptions to encourage the growth of the tea industry and/or for all or any of the abovementioned objects or otherwise

Building Unanimity To promote the common interests of all persons concerned in the cultivation and/or production of tea in India

To express and give effect to the views, opinions and expressions of all persons concerned in the cultivation and/or production of tea

To co-operate with any other body or bodies having objects similar to all or any of the objects of the Association

To collect, analyse, interpret and circulate statistics and information of all kinds or of general interest to the member of the Association and/or persons engaged in the cultivation and/or production of tea and/or public concemmg the tea industry

Source: IT A Rules, Annual Report oflndian Tea Association (1998-99), Calcutta, 2000, pp.l34-35.

-49-

4.2 Brief HistoiJ' of/TA

IT A was fonned with the initiative of A. Wilson of Jardine Skinner & Company and

D. Cruckshank of Begg, Dunlop & Company in a meeting held in Calcutta dming

May 1881. The main purpose behind the formation of IT A was to look in to and

resolve the problems faced by the British planters, like labour shortage and renewal of

agreements with the labourers. A.B. Inglis from Begg, Dunlop & Company laid down

the purpose of the association in a detailed manner. He said that united action amongst

the tea proprietors was lacking and the fonnation of IT A would bring about a certain

degree of concert and unity of action amongst the owners and managers of the tea

estates with regard to any grievances affecting tea interests. ITA would also look into

various legislations related to tea industry. Inglis added that IT A would take up the

typical problems faced by tea planters' of that time like communication with the tea

districts and various diseases affecting the tea plants. 18

By June 1881, the association was formally constituted and a general committee

consisting of nine firms was elected. IT A began functioning in a very professional

manner right from the time of its inception. It established a relationship with the

Bengal Chamber of Commerce (BCC) in order to benefit from the wider experience of

collective British business. The secretariat of ITA was also set up in the premises of

BCC in 1885 from where it continues to function even today.

ITA soon established District Committees comprising managers and superintendents

in Assam valley in order to be represented in those areas. However, the Assam valley

planters felt that only they could understand and assess the problems of Assam tea

18 Griffith, n.3, pp.513-15.

-50-

gardens. This led to the fonnation of Assam Branch of Indian Tea Association

(ABITA) with a separate Chainnan and Secretary in 1889 as a branch of IT A,

Calcutta. Soon a South Sylhet Branch of IT A was also fonned. In 1901, a Sunna

Valley Branch of IT A was fonned comprising four and five district committees in

Sylhet and Cachar respectively. In 1908, Datjeeling Planters' Association (DPA) also

became affiliated to IT A and remained as its part till 1983 when it decided to resurrect

the DPA.

It should be noted that IT A from the very beginning had taken up the leadership role

and was representing most of the tea producing districts of Northern India. ITA played

an important part in expanding the tea market in India. It also set up a Tea Cess

Committee, which was financed by statutory cess, for the expansion of tea market in

India. 19

4.3 ITA and its Early Political Influence

The success of most of the pressure groups depends upon their accessibility to the

decision makers. ITA realised this from the very beginning and actively took interest

in the political affairs as long as it pertained to the tea industry. It was due to the

constant lobbying by ITA, a 'fepresentative of the planters' were allowed in the

Viceroy's Legislative Council under Indi~ Councils Act, 1892. ITA further

succeeded in getting two separate tea industry representatives in the new council

formed under Morley-Minto reforms in 1909. In 1919 under Montague Chelmsford

Reforms, a representation to the Indian legislative assembly was granted to the Assam

1 ~ These cess are still collected, however after independence the administration of these Cess has been taken over by the Government oflndia.

- 51 -

Europeans. These Europeans were tea planters. The responsibility for filling the

Assam European seat in Indian Legislative Assembly was taken up by the IT A.

Furthennore, E.S. Roffey, the Secretary of ABITA was appointed the Political

Secretary of the European Group in the Assam Legislature in 1929.20

The interest of IT A in the political affairs is quite discernible in the statement made by

its Chainnan in the annual meeting in 1936:

" ... [C]oncern with politics is not made necessary solely because of the particular legislation which has more recently enacted (Government of India Act, 1935), and which we have now got to understand, so that we can apply it, but for years past we, in common with very nearly any other industry, have relied upon that splendid body of civil servants, to mother and father our political interests. If under reformed constitution, we have all individually to take our due share of political responsibility, for one thing because those civilians will have neither the time nor the opportunity to do it for us, then it is surely for us, in all matters, including finance and the release of

. personnel, to bear our share of that responsibility."21

ITA's lobbying efforts were successful and under 1935 Act seven seats were reserved

for British planters' in the Assam Legislative Assembly. Apart from that, one seat was

reserved for the European Commerce and Industry, and one for Europeans in Assam

generally. In the Upper House of Assam, also there were two seats reserved for the

planters'. The Europeans legislatures were provided a permanent secretariat located in

Shillong, and were collectively known as European group. The IT A mainly financed

the expenses of the group. In Bengal, under the 1935 Act two seats in the Legislative

20 Griffith, n.3, pp 526-27.

21 Griffith, n.3, pp 526-27.

-52-

Assembly were given to the ITA. In the Central Legislature, a single member

represented the Assam Europeans. Even that member was actively involved with the

affairs ofiTA 22 Although, ITA's direct representation in the government ceased with

India's independence, it continues to be the most influential pressure group with

representation in various government and non-government bodies associated with

policy making in the tea industry. The pattern of present day cooperation between IT A

and the Indian policy makers can be observed from the speech given by the Chainnan

of ITA in 1991. He said:

" In all our tasks the underlying assumption is that of an environment of close cooperation between industry and government. The tea industry has been particularly fortunate in having a responsive government in a position to appreciate the issues of concern to us and to frame appropriate policies to further the growth and development of this industry. Notwithstanding sporadic aberrations and conflicts of interest, cooperation between industry and government has also so far demonstrated ample resilience and maturity and it is this continued trust that will bring to fruition our further plans for growth. The Association believes in the validity and sanctity of partnership between industry and government, which alone can contribute to policies, which are balanced and realistic".23

4.4 Organisation of ITA

The proprietors, partnership ·companies (public or private), cooperatives, and

corporate bodies, engaged in the production or cultivation of tea are eligible for

membership of the ITA.24 The members are admitted by a majority of the General

Committee. It comprises of 20 representatives who are elected annually by the

22 ibid.

23 Speech by ITA Chainnan. "Annual General Body Meeting." Annual Report, Calcutta: ITA, 1991, pp. 214-15.

24 Rule ( 4) of IT A Rules, n.19, p.136.

-53 -

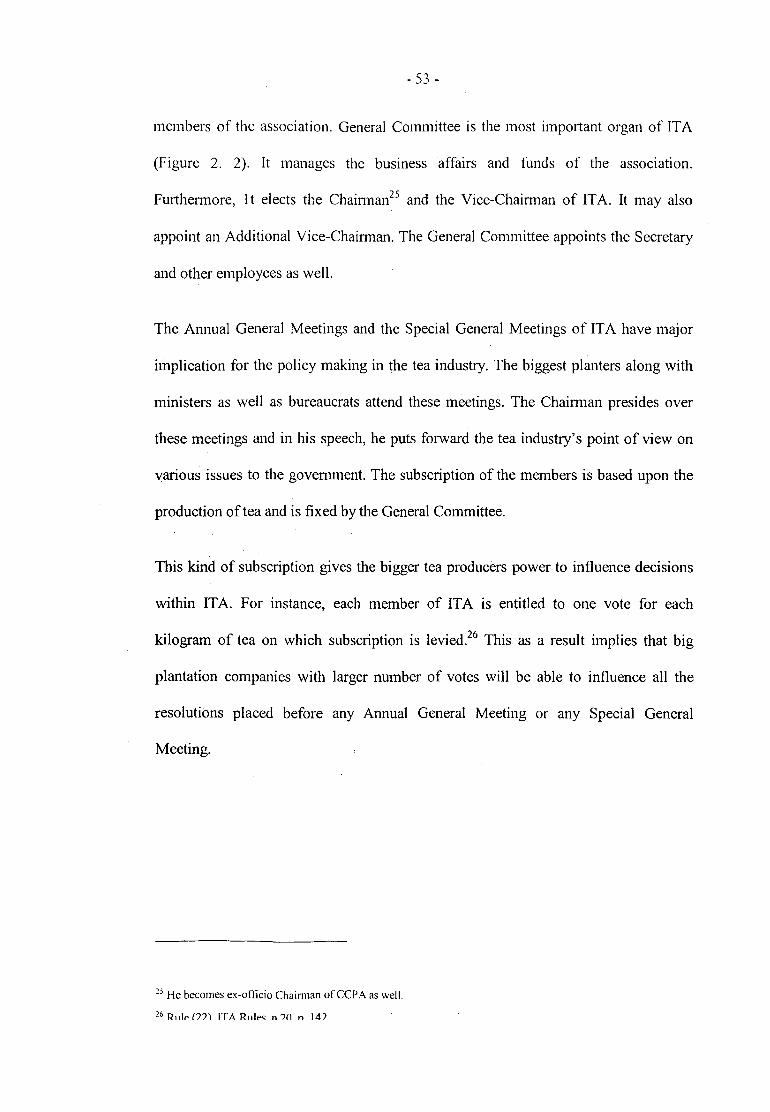

members of the association. General Committee is the most impOitant organ of IT A

(Figure 2. 2). It manages the business affairs and funds of the association.

Furthermore, 1 t elects the ChainnmP and the Vice-Chainnan of IT A. It may also

appoint an Additional Vice-Chairman. The General Committee appoints the Secretary

and other employees as well.

The Annual General Meetings and the Special General Meetings of IT A have major

implication for the policy making in the tea industry. The biggest planters along with

ministers as well as bureaucrats attend these meetings. The Chainnan presides over

these meetings and in his speech, he puts forward the tea industry's point of view on

various issues to the govenunent. The subscription of the members is based upon the

production of tea and is fixed by the General Committee.

This kind of subscription gives the bigger tea producers power to influence decisions

within IT A. For instance, each member of ITA is entitled to one vote for each

kilogram of tea on which subscription is levied.26 This as a result implies that big

plantation companies with larger number of votes will be able to influence all the

resolutions placed before any Annual General Meeting or any Special General

Meeting.

25 He becomes ex-oflicio Chainnan ofCCPA as well.

26 R11IP I?)) ITA Rul""' n In n 14?

-54-

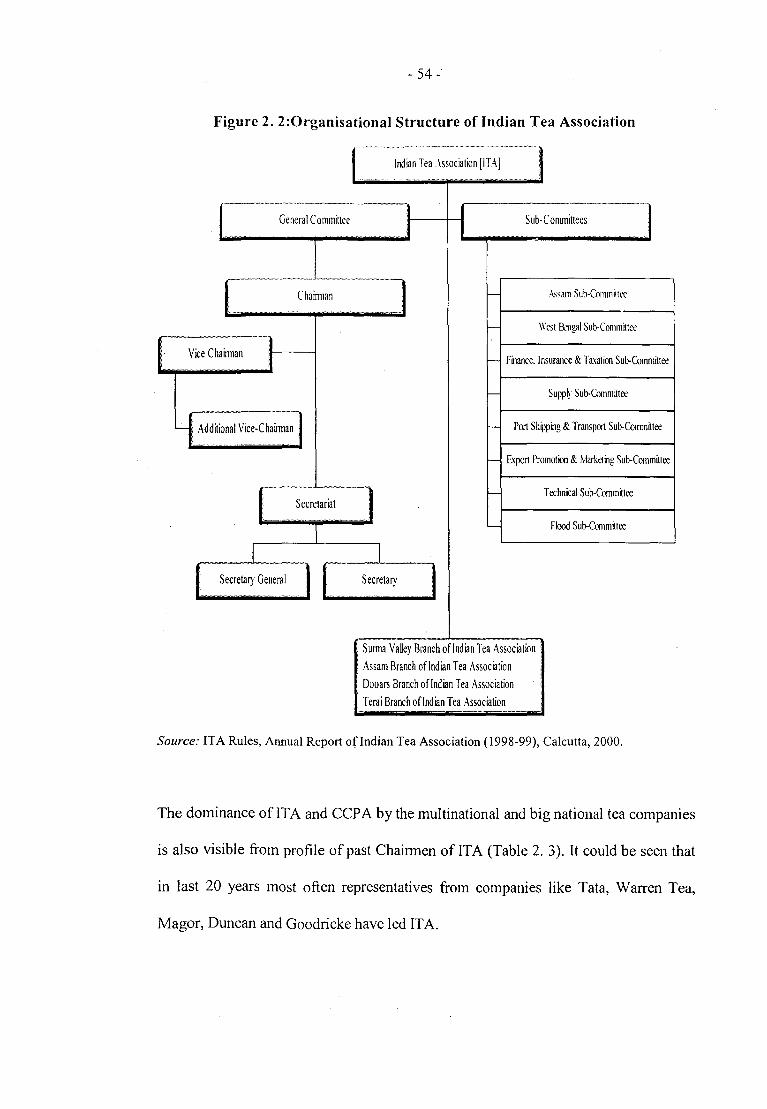

Figure 2. 2:0rganisational Structure of Indian Tea Association

General C omminee

Chaim1an

Vice Chainnan

Additional Vice-Chairman

Indian Tea .-\ssociation [ITA]

Sub-C onuninees

Assam Sub-Commiltl'C

West &,1gal Sub-Commrttee

Finance. Insurance & Taxation Sub-Commrttee

Supp~ Sub-Committee

Port Shipping & Transport Sub-Commrttee

Export Promotion & Marketing Sub-Committee

Technical Sub-Commrttee

Flood Sub-Committee

. Sunna Valley Branch oflndian Tea Association Assam Branch oflndian Tea Association Dooars Branch oflndian Tea Association Terai Branch oflndian Tea Association

Source: ITA Rules, Annual Report oflndian Tea Association (1998-99), Calcutta, 2000.

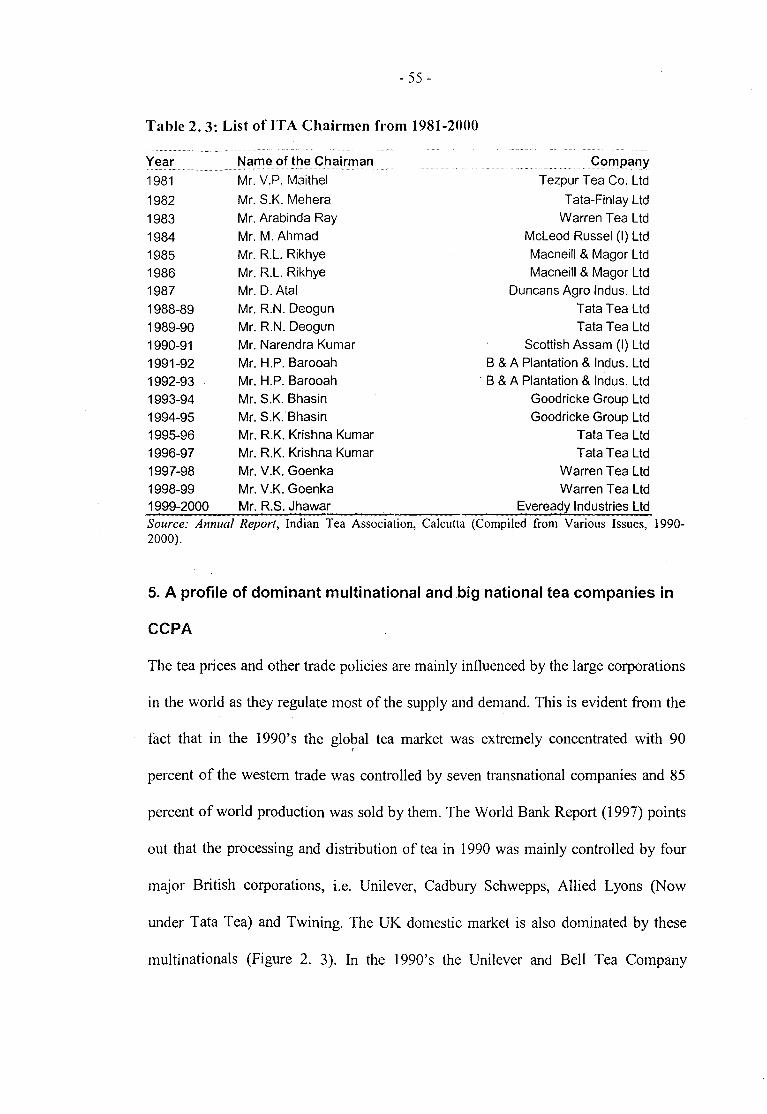

The dominance of IT A and CCP A by the multinational and big national tea companies

is also visible from profile of past Chairmen of IT A (Table 2. 3 ). It could be seen that

in last 20 years most often representatives from companies like Tata, Warren Tea,

Magor, Duncan and Goodricke have led IT A.

-55-

Table 2. 3: List of ITA Chairmen from 1981-2000

Year Name of the Chairman Co111pany

1981 Mr. V.P. Maithel Tezpur Tea Co. Ltd

1982 Mr. S.K. Mehera T ata-Finlay Ltd

1983 Mr. Arabinda Ray Warren Tea Ltd

1984 Mr. M. Ahmad Mcleod Russel (I) Ltd

1985 Mr. R.L. Rikhye Macneill & Magor Ltd

1986 Mr. R.L. Rikhye Macneill & Magor Ltd

1987 Mr. D. Atal Duncans Agro Indus. Ltd

1988-89 Mr. R.N. Deogun Tata Tea Ltd

1989-90 Mr. R.N. Deogun Tata Tea Ltd

1990-91 Mr. Narendra Kumar Scottish Assam (I) Ltd

1991-92 Mr. H.P. Barooah B & A Plantation & Indus. Ltd

1992-93 Mr. H.P. Barooah B & A Plantation & Indus. Ltd

1993-94 Mr. S.K. Bhasin Goodricke Group Ltd

1994-95 Mr. S.K. Bhasin Goodricke Group Ltd

1995-96 Mr. R.K. Krishna Kumar Tata Tea Ltd

1996-97 Mr. R.K. Krishna Kumar Tata Tea Ltd

1997-98 Mr. V.K. Goenka Warren Tea Ltd

1998-99 Mr. V.K. Goenka Warren Tea Ltd 1999-2000 Mr. R.S. Jhawar Eveready Industries Ltd Source: Annual Report, Indian Tea Association, Calcutta (Compiled from Various Issues, 1990-2000).

5. A profile of dominant multinational and big national tea companies in

CCPA

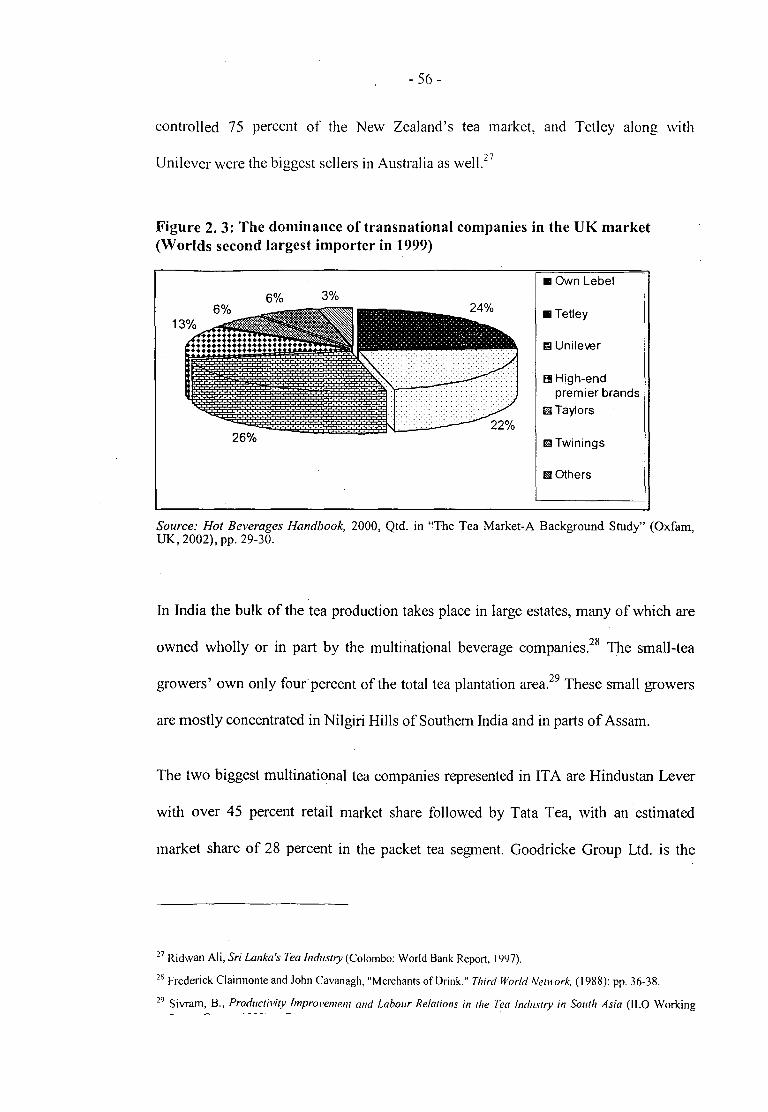

The tea prices and other trade policies are mainly influenced by the large corporations

in the world as they regulate most of the supply and demand. This is evident from the

fact that in the 1990's the glo?al tea market was extremely concentrated with 90

percent of the western trade was controlled by seven transnational companies and 85

percent of world production was sold by them. The World Bank Report (1997) points

out that the processing and distribution of tea in 1990 was mainly controlled by four

major British corporations, i.e. Unilever, Cadbury Schwepps, Allied Lyons (Now

under Tata Tea) and Twining. The UK domestic market is also dominated by these

multinationals (Figure 2. 3). In the 1990's the Unilever and Bell Tea Company

-56-

controlled 75 percent of the New Zealand's tea market, and Tetley along with

Unilever were the biggest sellers in Australia as well.27

Figure 2. 3: The dominance of transnational companies in the UK market (Worlds second largest importer in 1999)

6% 3% • Own Lebel

• Tetley

~Unile~r

Bl High-end premier brands

m Taylors

m1 Twinings

mOthers

Source: Hot Beverages Handbook, 2000, Qtd. in "The Tea Market-A Background Study" (Oxfam, UK, 2002), pp. 29-30.

In India the bulk of the tea production takes place in large estates, many of which are

owned wholly or in part by the multinational beverage companies?8 The small-tea

growers' own only four-percent of the total tea plantation area?9 These small growers

are mostly concentrated in Nilgiri Hills of Southern India and in parts of Assam.

The two biggest multinational tea companies represented in IT A are Hindustan Lever

with over 45 percent retail market share followed by Tata Tea, with an estimated

market share of 28 percent in the packet tea segment. Goodricke Group Ltd. is the

27 Ridwan Ali, Sri Lanka's Tea Industry (Colombo: World Bank Report, i'N7).

28 Frederick Clainnonte and John Cavanagh, "Merchants of Drink." Third World Network, ( 1988): pp. 36-38.

29 Sivrarn, B., Productivity Improvement and Labour Relations in the Tea Industry in South Asia (lLO Working - -

-57-

third most impm1ant multinational tea company in India. The rest of the market is

dominated by the Goenkas.30 The Goenkas manage and own big tea companies like

Duncan, Harrison-Malayalam and Warren Tea Ltd. The other leading national tea

companies are Birla owned Jayashree Tea and Assam Tea Company Ltd and

Khaitan's William Magor. 31

5.1 Hindustan Lever

Hindustan Lever Limited (HLL) is India's largest foods and beverages company. It

also holds leadership position in consumer goods, personal care products, and

speciality chemicals. It has around 36,000 employees, including 1300 managers all

over India. HLL is a subsidiary of the multinational Unilever Ltd, which holds 52

percent of the equity.32 Unilever is a 'Fortune 500' multinational, which sells over

I 000 Foods and Home and Personal Care brands through 300 subsidiary companies in

88 countries worldwide, with products on sale in another 70 countries. Unilever

dominates the world tea industry, spanning plantations, proces<::ing, and marketing.

The acquisition of Liptons in 1972 and Brooke Bond in 1984 effectively made

Unilever the world's largest buyer and distributor of tea. 33 At present, it handles 19

percent of world tea production and has around 16,000 hectares of tea plan~ations in

Kenya, Tanzania,, Malawi, and South Africa.34

30 G.P. Gocnka Group, S.P. Goenka Group, and R.P. Goenka Group.

31 India Infoline Sector Report on Tea <http://www.indiainfoline.com sect!teil/chO I.html> 20 Sep 200 I.

Jc The otliciJI website of the Hindustan Lever Ltd.< http://www.hll.c0m HLLI/businesscat.html> 6 Sep. 200 I.

·11 Unilevcr Tea <http://www.unilevcr.com/co/oc.html> 5 Oct. 2001.

"Ibid.

- 5~-

H LL has 15 tea estates and factories distributed between South India and Assam \\·ith

planted area of over 6800 hectares. The tea estates under HLL are witnessing

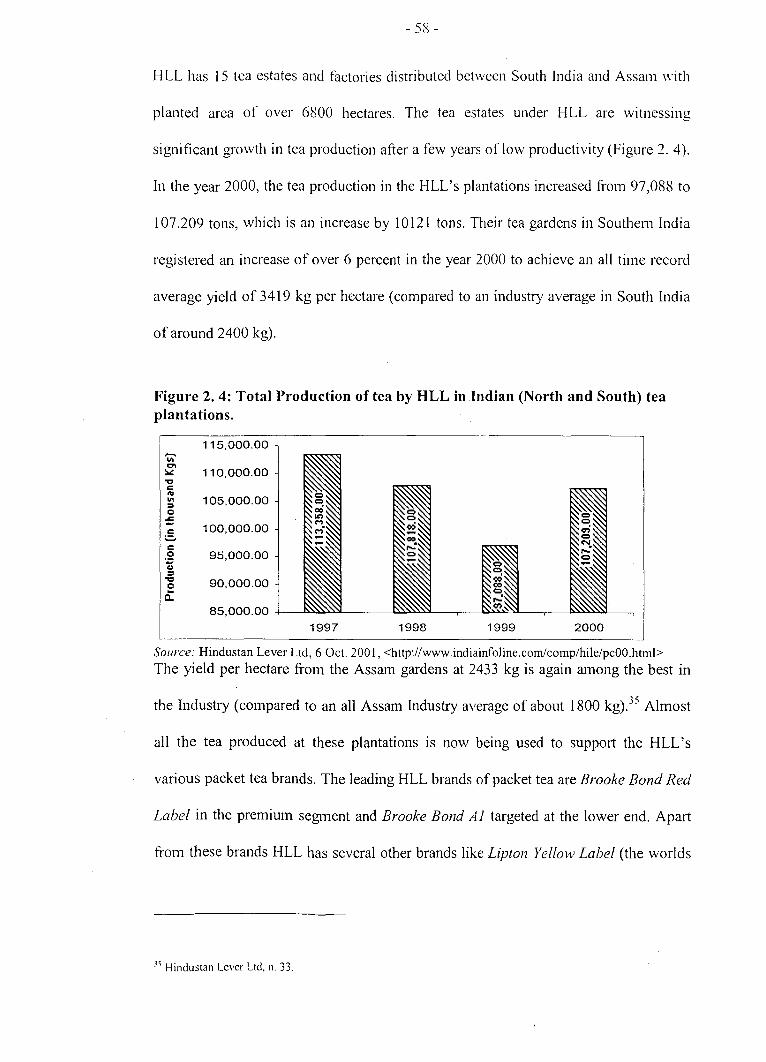

significant growth in tea production after a few years of low productivity (Figure 2. 4).

In the year 2000, the tea production in the HLL's plantations increased fi·om 97,088 to

107.209 tons, which is an increase by 10121 tons. Their tea gardens in Sou them India

registered an increase of over 6 percent in the year 2000 to achieve an all time record

average yield of 3419 kg per hectare (compared to an industry average in South India

of around 2400 kg).

Figure 2. 4: Total Production of tea by HLL in Indian (North and South) tea plantations.

115,000.00 Vi' C'l

::..: 110,000.00 "CC c ~ VI 105,000.00 = 0

of: 100,000.00

~ c

.5! 95,000.00 z = "CC 90,000.00 0 a: 85,000.00

1997 1998 1999 2000

Source: Hindustan Lever Ltd, 6 Oct 2001, <http://www.indiainfoline.com/comp/hile/pcOO.html>

The yield per hectare from the Assam gardens at 2433 kg is again among the best in

the Industry (compared to an all Assam Industry average of about 1800 kg). 35 Almost

all the tea produced at these plantations is now being used to support the HLL's

various packet tea brands. The leading HLL brands of packet tea are Brooke Bond Red

Label in the premium segment and Brooke Bond Al targeted at the lower end. Apart

from these brands HLL has several other brands like Lipton Yellow Label (the worlds

" Hindustan Lever Ltd, n. 33.

-59-

most popular tea brand), Green Label, Taaza and 3 Roses, Super Dust, Top Star, Rubr

Dust etc, positioned in different price segments.

5.2 Tata Tea Limited

The Tata Group is one of the biggest industrial houses in India with interests in

diverse businesses such as Steel, Automobiles, Tea, Hotels, Information Technology.

and Chemicals. Tata Tea has more than 50 tea estates in India.36 It was the first tea

company in India to set up processing and packing facilities at the tea estates itself.

Tata Tea's CTC factory at Kakajan in Assam processes nearly 0.1 mn kg of tea per

day. It also has a fully automated advanced tea factory at Madupatty in Murmar,

Kerala. The instant tea manufacturing facility for Exports, located at Munnar, is the

largest Instant Tea factory outside USA.37 Presently, Tata Tea is the leading tea

plantation company in India and the largest integrated tea producer in the world.

Tata Tea was incorporated in 1962 as Tata Finlay Ltd, and commenced business in

1963. Initially the company started with the instant tea factory at Munnar, Kerala and

blending! packaging unit at Bangalore. The Company had a technical and financial

collaboration with James Finlay & Co. Glasgow, UK. In 1976, it acquired the Indian

interests of James Finlay & Company along with its 7 associate sterling tea

companies.38 Tata also acquired the foreign holdings of James Finlay and Mcleod

-'6 India Infoline Sector Report on Tea, n.33.

37 Tata Tea Ltd, <http://www.tatatea.com/varied.html> 26 Sep. 2000.

'8 It was said that a consideration of about Rs I 15mn was paid through issue of equity shares (Rs! 9.8mn) and Rs.

95mn was retained as unsecured loans at 5% p.a. interest. (Tata Tea, http://www.indiainfoline.com/eomp/tate/mrtll.html, 20 Jan 2002.

Russell in December 1 9~2. Consequently, in 1983. the Company's name\\ as changed

to Tata Tea Ltd.

Tata Tea on March 31. 2000 acquired entire shareholding of world's second largest

branded tea company. Tetley Group Limited, for £271 mn. Tetley has a major

presence in many countries and primarily blends, packs and distributes tea products

(mainly in tea bags) in Canada, Australia, USA, and number of European countries

including Poland, UK, and in Russia. It is the largest selling tea brand in the UK and

in Canada. The Tetley Group is still a profit making company with good cash t1ow:' 9

The acquisition of Tetley has made the Tata Tea the second largest tea multinational

in the world. Tetley has six production centres - two in UK, two in USA, one in

Australia and one in India and all these centres have state-of-the ari technologies and

have latest facilities for tea bag packaging.

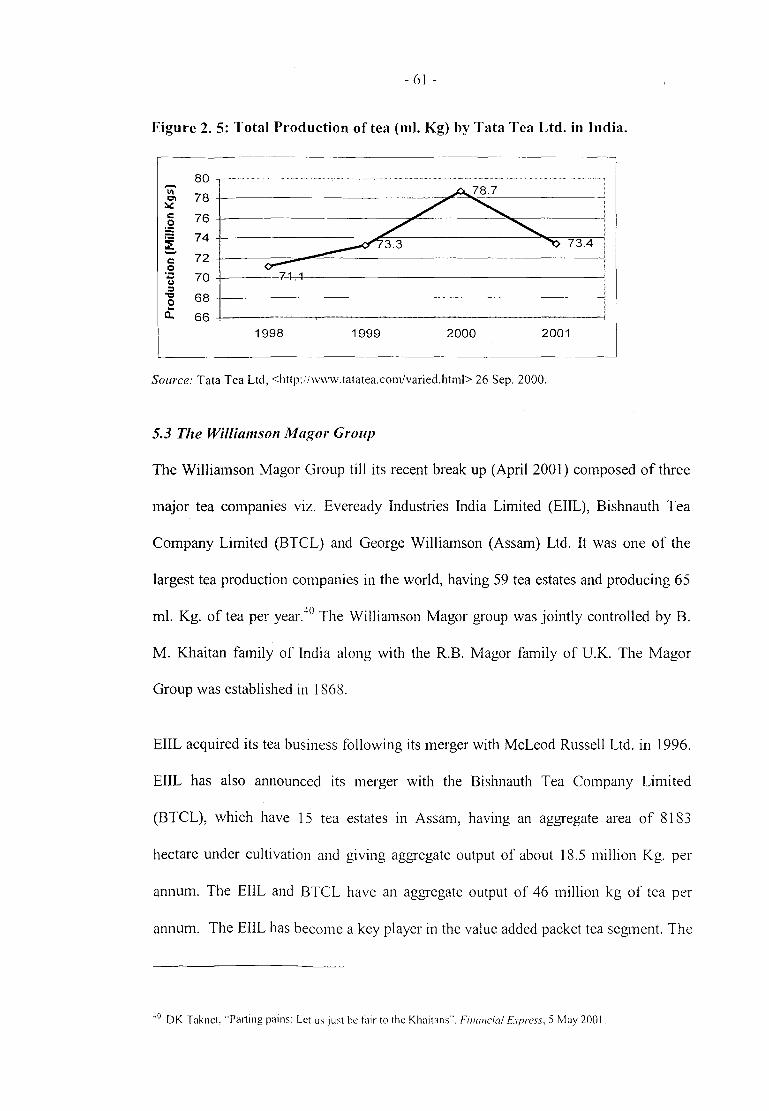

Tata tea has also witnessed a major growth in tea production (Figure 2. 5). It went up

from 71.1 mi. Kg in 1998 to 78.7 mi. Kg in 2000 to comedown at 73.4 mi. Kg in

2001. Most of the tea is sold in the packet fonn under various brand names of Tata.

Tata Tea's t1agship brand has a 12 percent market share. Other Tata Tea brands are

Kannan Demn, Chakra Gold, Gemini, Agni, and Ludy Cup. The Tata Tea's brands

have a dommant hold over the markets in Southem India.

''> Tuta Tel Ltd. Direeiors ·Report (Calcutta, 31st July. 2000).

- 61 -

Figure 2. 5: Total Production of tea (mi. Kg) by Tata Tea Ltd. in India.

80 Vi' 78 go, ::..:: c 76 ~ ~ 74 73.4 - 72 c 0

·;:: 70 <:o = '1:1 68 0 ..

0.. 66 1998 1999 2000 2001

Source: Tata Tea Ltd, <http:/iwww.tatatea.com/varied.html> 26 Sep. 2000.

5.3 The Williamson Magor Group

The Williamson Magor Group till its recent break up (April 2001) composed of three

major tea companies viz. Eveready Industries India Limited (EIIL), Bishnauth Tea

Company Limited (BTCL) and George Williamson (Assam) Ltd. It was one of the

largest tea production companies in the world, having 59 tea estates and producing 65

mi. Kg. of tea per year.40 The Williamson Magor group was jointly controlled by B.

M. Khaitan family of India along with the R.B. Magor family of U.K. The Magor

Group was established in 1868.

EIIL acquired its tea business following its merger with McLeod Russell Ltd. in 1996.

EIIL has also announced its merger with the Bishnauth Tea Company Limited

(BTCL), which have 15 tea estates in Assam, having an aggregate area of 8183

hectare under cultivation and giving aggregate output of about 18.5 million Kg. per

annum. The EIIL and BTCL have an ag!:,rregate output of 46 million kg of tea per

annum. The EIIL has become a key player in the value added packet tea segment. The

~0 DK Taknct. .. Parting pains: Let us just be E1ir to the Khaitans ... Financial Express, 5 May 200 I.

- 62-

EILL brands like Tez and Premium Gold are quite popular in India. It also sells

unbranded tea in bulk fonn.

In April 2001, there was a break up of the Magor Group following differences

between the Khaitan family and the Magor family. According to the new agreement,

the Khaitans will continue to own and run their tea gardens that have existed under the

bmmer of Bislmauth Tea Company and Mcleod Russel, which are now part of

Eveready Industries India Ltd. The Khaitans are now left with only 25 tea gardens.

The 'Williamson Tea' logo is also the registered property of the Khaitans.41 In the

new set up, the Magor Group has taken over the full ownership of George Williamson

Company and its 17 tea gardens in Assam having annual produce of 19.5 million

kilograms.42

5. 4 Goodricke Group Ltd

The Goodricke Group is the leading producer of Dmjeeling tea and the third largest

tea producer in India. The company owns 17 gardens spread over 9500 hectares. The

Goodricke Group is subsidiary of Lawrie Group Plantation Company (LGP) of United

Kingdom. LGP is one of the world's largest and most profitable tea producers.

Goodricke not only access LGP's global marketing and distribution network but also

the expertise of the parent's management team.

Goodricke was fanned in 1978 by taking over nine sick tea gardens in Darjeeling,

which were nursed back to health. At present, the company operates 12 gardens in

~ 1 Rediff Money Matters, ··Williamson Tea to take managerial control of George Williamson·· 21 April 2001< http://www.rcditfeom/moncy/200 I /apr/21 risc.htm>

~ 2 Rcditl' Money Matters, n. 42.

- 63-

Dooars, three in Da~jeeling and two in Assam.43 In Dmjeeling and the northeast,

Goodricke operates another 17 gardens through its group companies. The LGP is the

majority shareholder with a 74 percent stake in these tea gardens. LGP also have

overseas interests in trading, engineering, food and financial services business, apmt

from tea plantation activities in Malawi, Kenya, and Bangladesh.

Goodricke's gardens produce very high quality CTC and Orthodox teas. The total

production in the year 2000 was 16.78 ml. Kg. compared to 15.83 ml. Kg. in the

previous year. Initially Goodricke used to sell most of its tea in bulk fonn at the

auction market. However, presently Goodricke has an equal proportion of sales in the

bulk and packet tea segments, besides a significant presence in the export market.

Goodricke sells one of the costliest tea brands in the world known as Castleton Tea.44

Apart from this Goodricke also sells premium black tea under the brand name of

Badamtam, Thurbo and Premium Dmjeeling. The tea bags are sold under the brand

name of Fine Estate. The CTC tea is sold as Goodricke Tea in poly-pouches, cartons,

and pet jars.

5. 5 Assam Company Ltd

Assam Company Ltd. is a part of the UK based Duncan McNeill Group. The company

owns 28 tea estates in the North Eastern part of the country. Besides bulk tea, the

company sells packed tea under brands like Regular, Jumbo, Premium and tea bags

43 Tea estates- Goodricke Group in India < http://www.goodricke.com estates.htm> I 0 Oct. 200 I.

44 Castleton Tea recently surpassed its own previous world records b\ fetching R~:. 15,000 (around US$ 360) per kg at the Calcutta Auction.

- 64-

under the umbrella brand, Assam Gold. The company also has a large expm1 market in

Europe and is looking at expanding its presence in other countries.

"'Assam Tea Company was the first commercial tea company established in 1839 under

the Royal statute of the British Parliament. The company was set up as a subsidiary of

UK based Duncan Mcneill Group. The company went public in 1977 after being

amalgamated with five sterling tea companies- Assam Estates, Greenwood Tea Co.,

Salonah Tea Co., Thanai Tea Co. and Upper Assam Tea Co. and was renamed as

Assam Company (India) Ltd. The name of the company was changed to Assam Tea

Company Ltd. in 1989.45

The company owns 28 tea estates located at Doom Dooma, Moran, Panitola,

Dibrugarh, Nowgong and Jorhat, and spread over 7400 hectares and 17 tea

manufacturing factories.

5.6 Duncans Industries Limited

Duncans Industries Limited (OIL) is the third largest seller of branded tea in India

with a nine percent market share. OIL is an assisted flagship company of the G.P.

Goenka Group. The OIL was set up in the year 1859 by the name of Playfair Duncan

Company.46 In the year 1951, the Goenka family, a leading business enterprise of

India, took over the reins of Duncans. OIL is a highly diversified conglomerate with

20 operating companies and a work force of over 40,000 employees. The Duncan-

45 India Infoline Sector Repmt, .. Assam Company", <http://www.indiainfolinc.convcomp/assa.html> 20 Sept. 2001.

46 Duncan Goenka Group <http://www.duncans-tea.com/about.htm> l 2 October 200 I.

- 65-

Goenka Group has interests in Fertilizer, Tea, Paper, Cement, Chemical,

Petrochemicals, Synthetic fibres, Healthcare, Infonnation technology, and other fields.

DIL has 12 tea gardens in the Dooars, Terai and Darjeeling area of West Bengal with

a total area of about 7500 hectares under cultivation, giving an average annual output

of about 17.5 million kg.47 The company operates mainly in the value added packet

tea segment which accounts for 85 to 90 percent of the company sales while the

balance 10 to 15 percent is sold through auctions. OIL has set up a state of the art tea-

processing factory within its plantations in Dinajpur and Jalpaiguri districts of West

Bengal. The factory has the capacity of producing 1,800 tons of tea per annum.48 The

company also exports tea, mainly by purchasing it from auctions and blending/

packaging it. Exports constitute on an average about 3 percent of the company's total

tea sales and the company is a recognized Export House. The well-known brands of

the OIL are Double Diamond, Sargam, Pikup, No.1, ShaA.1i and Rzmglee Rungliot,

which together accounts for about 1 0 percent of the market share in packet tea

segment.

5. 7 Warren Tea Ltd.

Warren Tea is the flagship tea company of the S.P. Goenka Group. The company was

incorporated in 1977 for production and processing of tea. The company has thirteen

tea estates covering a total cultivable area of 6846.6 hectares, in upper Assam with the

production capacity of 16 mi. Kg. Moreover, the company has interest in the tea

business through another group-company, Darjeeling Plantation Industries Limited

47 Ibid.

48 West Beng<JI Industrial Development Corporation (WBIDC), 'What·s Happening in West Bengal ... <http://www.wbidc.com>, October II, 200 I

- 66-

(DPL), which has 6 gardens in Darjeeling covering a totnl cultivable area of 1445.1

hectares.

The company is one of the largest producer of Darjeeling variety of tea and DPL's

production of 0.8 million Kg. of black tea (1998-99) represents approximately 10

percent of the total production of Darjeeling tea during the year. DPL has facilities for

cultivation and processing of 0.8 million Kg. of tea per annum. DPL's production is

mainly sold through auctions at Kolkata and the company's tea, especially First Flush

tea enjoys considerable premium in the export market.

5.8 Jayashree Tea and Industries ltd.

Jayshree Tea & Industries Limited (JTI), belonging to the B K Birla group has

facilities for the cultivation and manufacture of premium quality tea at its tea estates at

Darjeeling, Islampur, Jalpaiguri and Dooars in West Bengal. JTI sells about 20

percent of its tea in packets and the balance as loose tea. The company's tea brands

Birla Tea -Shandaar, Jaandar and Sadabahar and Jayshree Tea - Sholayar have

become very popular and widely accepted in the areas where they are sold. Around 50

percent of its production is sold through agents and retailers, 40 percent through

auction houses and balance 10 percent is exported.49

6. Influence of Multinationals on National Policy Issues

It can be observed from the above analysis that India's top business corporations like

Tata's, Goenka's, Birla's, Khaitan's along with the HLL, are the dominant actors

within IT A and in the tea industry of India. Most of these multinational and big

49 West Bengal industrial Development Corporation, n. 49.

- 67 ~

national tea companies have their own estates along with trading, processing, and

blending facilities. Their ownership of both plantations and processing factories is

called horizontal integration. However, there is a vertical integration also as they

control transport companies, fertilizer companies, shipping agencies etc. Due to this

control of entire production process from tea shrubs to tea bags, these companies have

considerable influence on supply and demand and thereby on the tea trade policies.

One early example of the influence ofbig tea companies on Indian tea trade policy can

be seen from the action of the tvfNC's in the 1980's. During mid-1980's Indian tea

prices went up considerably because the former Soviet Union bought up large

quantities of tea, while consumption in India was increasing as well. The big

multinational tea companies were faced with severe losses, as they had to buy tea for

global market at a higher price. In retaliation, they decided to bring down the high

price by temporarily refraining from buying Indian tea, which gradually depressed the

price. During this period, Indian government attempted twice to get a grip on the

market by imposing export restrictions, thus trying to avoid shortages on the local

market. At the same time, it set a minimum export price with the aim of keeping

prices at a profitable level. The large tea companies then decided to collectively

withdraw from Indian market with the result that nothing could be exported at all. The

Indian government was thus forced to retreat and lift the measures again. 50

5° Fair Trade Organisations, '·Report of Dutch India Working Group on Tea Industry", 1994

< www. transfair.calfairtrade/fair66 7 .html> 6 Oct 200 I.

~ 68-

These big tea companies could afford to take such actions because of their high degree

of flexibility, their butler stocks, and their speculative transactions.51 Ihese

multinationals have been deliberately reducing the differences in the quality of tea.

That is the tea MNCs are buying tea wherever it is cheapest, blending them and

pushing them under their brand name. Except for some of the quality conscious

consumer countties, the consumer usually gets adapted to the branded tea sold by the

MNCs. Some of the blends were created after mixing tea of as many as 35 varieties.

For example the popular Tetley tea is a blend of supplies from 30 different countries

in the world, bought at all the auctions around the world. 52 Premier Brands, UK g:ets it

supply from 12 countries. Hence, none of the MNCs were dependent on any- one

particular source, and they could easily withdraw from India.

Although these multinational and big national tea companies are individually very

powerful pressure groups, yet most of the time they have tried to influence tea trade

policy in a collective manner through the influential pressure groups like IT A and

CCP A. Due to collective actions through ITA and CCPA, the big tea plantation

companies have been able to achieve a high degree of success. The only pressure

group, which has tried to oppose some of the policies of CCPA, is Calcutta Tea

Traders Association (CT A).

51 Ibid.

52 "The Tea Market-A Background Study .. (Oxfam-GB, 2002), pp. 30-3 I.

- 69-

7. Major Incidents of pressure group influence on Indian tea trade

strategies

The CCP A, for a long time, have sought changes in the various provisions of the Tea

Act, 1953. In 1991, the CCP A undertook a comprehensive exercise to review the

various provisions of Tea Act. The review by CCPA sought to withdraw various

Control Orders53 like Tea (Distribution & Export) Control Order, 1957, Tea

(Regulation of Export) licensing Order, 1984 and Tea (Marketing) Control Order,

1984.54

The Control Orders like Tea (Regulation of Export) licensing Order and Tea

(Marketing) Control Order were framed by the Ministry of Commerce in response to

the withdrawal of multinational tea companies in the 1980's from the Indian market.

The purpose of these regulations was to avoid shortages on the local market. At the

same time, it aimed to keep the prices at a profitable level.

CCP A has been successful in amending various provisions of these Control Orders

through extensive lobbying. The strategy followed by CCP A has been to present

evidences to the Tea Board officials in favour of amending the Tea Act and follow it

up with reminders, both written as well as verbal. These evidences were based on the

comprehensive review of the Tea Act earlier conducted by the Working Committee of

CCP A, mainly comprising of IT A General Committee members. The committee had

5·' Tea Control Orders: Since tea was put into the category of essential commodity, the Control Orders under the Tea

Act, gave the government power to control production, supply, distribution etc. of tea for maintaining or increasing supplies and for securing their equitable distribution and availability at fair prices.

54 Indian Tea Association. "Tea Act 1953: Related Orders." Annual Report, Calcutta: ITA, 1991. 70-72.

- 70-

observed that the "Control Orders have outlived their purpose and bore no relevance

in the climate ofliberalisation and decontrol."55

- In continuation with its lobbying efforts to amend the Tea Act, CCP A made a major

representation to the Ministry of Commerce in 1991. The representation worked in

favour of CCP A and the Ministry of Commerce to set up a Core Group in 1993 to

look into the issues related to Control Orders. It was set up under the Chaim1anship of

the Commerce Secretary with representation from the tea producers (CCPA) along

with the traders and brokers. On 5111 Dec 1994, the Core Group asked the Tea Board

for its viewpoint. Following this, the Tea Board also fonned a Working Group with

representatives from tea industry. The influence of CCP A and IT A in amending

various Tea Control Orders under the Tea Act has been analysed below in details.

7.1 Tea (Regulation of Export) Licensing Order, 1984

The Union Ministry of Commerce issued an order [No. S.O. I 08 (E)] dated 22nd Feb

1984 captioned the Tea (Regulation of Export Licensing) Order, 1984, which was

given effect to from i 11 March 1984. Under the said order, all exports (barring some

exemptions), were covered by a license and all contracts for bulk tea exports, with the

exception of tea purchased through auctions, would have to be submitted in a

specified manner for prior registration with the licensing authority (in the tea board).

The order also specified:

55 Indian Tea Association. "Tea Act 1953: Related Orders." Annual Report, Calcutta: IT A, 1994. 70-71.

- 71 -

0 That all application of contracts would have to be accompanied by a Valuation Report of an independent broker.

0 That the Licensing Authority could appoint a 'Panel of Expe1is' to assist Tea Board in taking view on the contract.

This Order was promulgated by the Govemment of India in order to ensure adequate

availability of tea for domestic consumption and also to regulate tea expmis. The

CCP A strongly objected to these regulations as CCP A was composed of mainly big

tea companies who had high stakes in the tea expmi market. They actively lobbied

with the officials from the Tea Board and the Ministry of Commerce in order to repeal

various sections of the Tea Licensing Order.

The strategy adopted by CCP A was to firstly build consensus among its members on

the demerits of Tea Licensing Order. The process of consensus building among the

major actors in the Indian tea industry usually begins from the General Committee of

IT A. In the case of Tea Licensing Order also, the ITA General Committee

unanimously passed various resolutions from time to time. These resolutions were in

favour of amending the various provisions of the Tea Licensing Order. The next step

for the CCPA was to make representations to the Tea Board and the Ministry of

Commerce.

The CCPA contended that due to the 'complex processes' of present Tea Licensing

Order, the tea industry is facing problems in getting shipment licenses. Moreover, the

validity of the shipment licenses should be extended from 90 days to 120 days. They

also complained that the validity of registration with the licensing authority should not

be restricted to 90 days only. It should also be extended to 120 days.

- 72-

The success of the CCPA could be seen from the Tea Board's action of amending

various provisions of Tea Licensing Order. 56 The amendments were as following:

1. The refusal to register tor exports were now allowed to be conveyed within seven

days, which was previously 15 days.

2. The validity of the registration period was extended from 90 days to 120 days.

3. The validity of the shipment licenses was also extended to 120 days from previous

90 days.

The Tea Board further simplified the shipment licensing procedure in 1991 by doing

away with the provisions of separate approaches for shipment licensing and

registration of contracts. 57 These amendments were due to the regular representations

made by CCP A to the Ministry of Commerce. Eventually, CCP A was successful in

getting the Tea (Regulation of Export Licensing) Order, 1984 altogether repealed in

1993.58 The revocation of the legislation helped the exporters to obtain license for any

tea export and register expm1 contracts with the licensing authority, i.e. the Tea Board.

7.2 Tea (Marketing) Control Order (TMCO), 1984

In the early 1980's the demand for Indian tea shot up because of increase in domestic

consumption and large purchases by former Soviet Union. The government was keen

that the majority of Indian population should get tea at a cheaper rate and hence

wanted to regulate the activities of tea manufacturers, auction organisers, and brokers.

It also wanted them to maintain records of production, purchase, stocks exports, etc.

56 Tea Board of India . .Yotijicatio11 '."u. SO. 520 (£) 14 August 1991.

57 Tea Board of India. "Tea Board Circular." Circular Lel!er No.5 (}9J1LC/9 I II 028, 9 September 1991.

ss This Order was revoked by the Tea Baord of India. "Tea (Regulation of bpon Licensing) (RepeJI) Order."

Notification No: S 0. 875 (Ej I:-, \ov 1993.

- 73-

Hence, The Ministry of Commerce, Govemment of India issued the Tea (Marketing)

Control Order, I 984 (vide S.D. 313 E dated 19th April 1984) under the powers of

Section 30 of the Tea Act, 1953. The order was given in effect from 19th July 1984.

The salient features of the order were as follows:

I. All the manufacturers of tea were required to obtain a valid registration of the

licensing authority (i.e. Tea Board).

2. Organisers of public tea auctions required to obtain License from Tea Board.

3. Licensing Authority empowered to issue directions to manufacturers, auction

organisers, and brokers to maintain records of production, purchase, stocks

exports, etc.

4. Manufacturers required to sell a minimum of 70 percent of tea manufactured

through public tea auctions. In 1985, the Ministry of Commerce further increased

the percentage of obligatory sales under tea auctions in India to 75 percent.

Exemptions were granted to manufacturers owning a single garden with less than

I 00 hectares under cultivation. 59

The tea producers were highly affected by this order as they wanted to retain the

option of selling tea both privately as well as through auctions. The IT A played a

crucial role in repealing the TMCO. It lobbied with the Ministry of Commerce for 17

years and eventually was successful in convincing the decision makers to withdraw

the Control Order. Yet, in the beginning IT A did not demand the complete revocation

;•J Indian Tea Association. "Annual Report." Calcutta: ITA. 1991. p. 79

- 74-

of TMCO. Rather, it slowly built up its case against the Order. IT A used its offices as

well as the CCPA channels in order to lobby the wider section of decision makers.

The first step it took, immediately after the promulgation of the TMCO was to send a

comprehensive memorandum to the Ministry of Commerce in 1985. In the

memorandum, IT A pleaded for relaxations in the order, pointing out in particular the

problems arising in areas such as Cachar (Assam), which produces plainer varieties of

tea. IT A fommlated a detailed note on Cachar highlighting the factors, which

accentuated economic backwardness of the region. It stressed on the established

private channels of marketing and role of ex-garden sales in the resurgence of Cachar

tea industry. 60 Based on these facts the IT A demanded an exemption for Cachar

district. It could be observed again that as a method of lobbying, IT A firstly conducts

complete research on a particular policy issue it seeks to change. They follow it up

with various memorandums to the Ministry of Commerce and the Tea Board.

In 1986, it was transpired that the govemment was averse to making any relaxation in

the TMCO. This is visible from govemment's refusal to give concessions with regard

to Cachar tea industry. Yet, the IT A continued to lobby by taking up the issue of

TMCO with decision makers from various forums. In 1988, the Additional Secretary,

Commerce convened a meeting to assess whether the conditions had materially altered

which warrants modifications in the order. The meeting noted that while IT A in

particular and CCPA in general had sought to impress upon the adverse effect of the

i•O Indian Tea Association, n.61, pp. -,-80.

- 75 -

order. 61 However, it was also noted that these representations had not been able to

convince government of the need to effect relaxations.

During 1989, ITA agam sent a representation to the Tea Board for obtaining

appropriate relaxations in the TMCO. This time they requested that expmis effected

through third parties or agents should be kept outside the 75 percent stipulation of

sales through auctions. Since the domestic prices of tea in 1989 were very high, IT A