$$ Entrepreneurial Finance, 5th Edition Adelman and Marks 8-1 Pearson Higher Education ©2010 by...

33

$$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ $$ Entrepreneurial Finance, 5th Edition Adelman and Marks 8-1 Pearson Higher Education ©2010 by Pearson Education, Inc. Chapter 8 Time Value of Money Part I: Future and Present Value of Lump Sums

-

Upload

marianna-newman -

Category

Documents

-

view

225 -

download

1

Transcript of $$ Entrepreneurial Finance, 5th Edition Adelman and Marks 8-1 Pearson Higher Education ©2010 by...

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-1

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Chapter 8

Time Value of Money Part I: Future and Present Value of Lump Sums

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-2

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Learning Objectives

Explain the relationship between the time value of money and inflation.

Distinguish between effective rate and stated rate. Calculate the future value lump sum and present value

lump sum factors that are used to solve time value of money problems.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-3

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Learning Objectives (continued)

Compare bank discount and simple interest. Calculate the internal rate of return with respect to the

present value of a lump sum and future value of a lump sum.

Integrate the present value of a lump sum and the future value of a lump sum to solve real-life financial problems.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-4

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Present a spreadsheet of the mathematics of finance. Use financial tables to solve time value of money

problems. Use financial calculators to solve time value of money

problems.

Learning Objectives (continued)

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-5

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Simple Interest

Simple interest is the amount of interest earned on the principal amount stated.

Principal amount stated is the base amount that we borrow or save.

Prt I

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-6

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Simple Interest (Examples)

Interest on $1,000 borrowed for one year at 8%:

Interest on $1,000 borrowed for six months at 8%:

$80.08)(1)($1,000)(0 I

Prt I

$40 .08)(0.5)($1,000)(0I

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-7

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

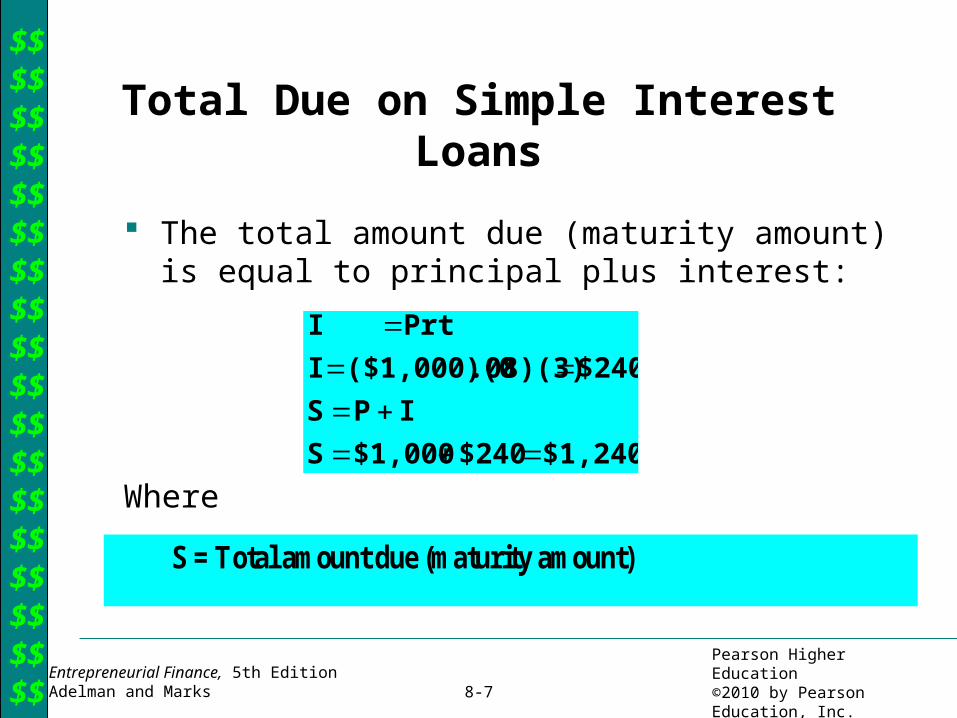

Total Due on Simple Interest Loans

The total amount due (maturity amount) is equal to principal plus interest:

$1,240 $240 $1,000S

I PS

$240.08)(3)($1,000)(0 I

Prt I

S = Total amount due (maturity amount)

Where

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-8

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Manipulating Simple Interest

If we know any three of the four variables: › Solving for principal

› Solving for time

Prt I

000,1$24.0

240$

)3)(08.0(

240$

)3)(08.0(240$

p

p

prtI

yearst

t

prtI

75.380$

300$

)08.0)(000,1($

300$

))(08.0)(1000($300$

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-9

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Fixed Principal Commercial Loans

Fixed Principal Commercial Loans are made using a fixed principal payment that remains constant for the life of the loan.

› Loan can be either fixed interest loan or variable interest loan.› Interest for loans tied to prime or some other federal rate as shown in

table 8-1.

FOMC Release Date Federal Funds Discount Rate Prime Rate

10/31/2007 4.50 5.00 7.5012/11/2007 4.25 4.75 7.251/21/2008 3.50 4.00 6.501/30/2008 3.00 3.50 6.003/18/2008 2.25 2.50 5.50

Table 8-1 Lending Rates

Federal Open Market Committee Statements & Minutes. Retrieved February 27, 2008 from http://www.federalreserve.gov/monetarypolicy/fomc.htm

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-10

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Example Fixed Interest Commercial Loan, fixed interest.

Table 8-2 Andre's Loan Schedule120,000.00$

9.50%5

602,000.00$

148,975.00$

Payment Number

Monthly Principal Payment

Monthly Interest Payment

Monthly Loan Payment Loan Balance

1 2,000.00$ 950.00$ 2,950.00$ 118,000.00$ 2 2,000.00 934.17 2,934.17$ 116,000.00 3 2,000.00 918.33 2,918.33$ 114,000.00 4 2,000.00 902.50 2,902.50$ 112,000.00 5 2,000.00 886.67 2,886.67$ 110,000.00 6 2,000.00 870.83 2,870.83$ 108,000.00 7 2,000.00 855.00 2,855.00$ 106,000.00 8 2,000.00 839.17 2,839.17$ 104,000.00 9 2,000.00 823.33 2,823.33$ 102,000.00

10 2,000.00 807.50 2,807.50$ 100,000.00 11 2,000.00 791.67 2,791.67$ 98,000.00 12 2,000.00 775.83 2,775.83$ 96,000.00

Monthly Principal Payment=Total Interest Paid=

Principal Amount of loan=Annual Interest Rate=

Number of Years=Number of Monthly Payments=

Loan for $120,000. Five years at 9.5 percent interest. Bank provides borrower with amortization table and payment book.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-11

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Fixed principal variable interest loan

Bank calculates daily interest which is adjusted every time prime interest rate changes.

Provides borrower with an invoice every month. Using Table 8-1, prime rate changed on December 11.

Therefore invoice for December would have 10 days of interest using prime of 7.5 percent and 21 days of interest using a prime rate of 7.25 percent.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-12

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Bridge Loans

Bridge loans are simple interest loans provided to borrowers who need a temporary loan to provide funds between the sale of one piece of property and the purchase of another piece of property.

Borrower actually owns two properties while awaiting the release of funds from the first piece of property.

Owner must have sufficient funds to make simultaneous payments on two properties.

When first property sells, and funds are released the borrower has sufficient funds to pay back bridge loan which is based on the days the loan is in effect.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-13

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Bank Discount

The bank discount is an amount of interest that is deducted from the amount you wish to borrow:

Where

SdtD

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-14

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Bank Discount (continued)

Proceeds are the amount the bank actually provides to the borrower after deducting the discount from the amount intended to be borrowed.

920$80$000,1$Proceeds

Proceeds

80$)1)(08.0(000,1$

DS

D

SdtD

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-15

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Bank Discount (continued)

96.086,1$92.0

000,1$

)1)(08.0(1

000,1$

dt-1

Proceeds Borrowed Amount

%70.810008696.0rateinterest annual Effective

100)1)(000,1($

96.86$100

(t)(proceeds)

paidinterest rateinterest annual Effective

x

xx

25.040,2$9803.0

000,2$

0198.01

000,2$

365

90)08.0(1

000,2$

dt-1

Proceeds Borrowed Amount

%16.81000816.0100

365

90)000,2($

25.40$

100(t)(proceeds)

paidinterest rateinterest annual Effective

xx

x

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-16

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Federal Treasury Bills

There are situations in which the entrepreneur can actually perform the function of a bank.

What better source of investing than to lend the government of the United States money for a short period of time?

The government issues discounted treasury bills in denominations of $10,000 for three months, six months, and one year.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-17

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Three-Month Treasury Bill

51.952,9$49.47$000,10$Proceeds

Proceeds

49.47$365

91)01905.0(000,10$

DS

D

SdtD

percentx

x

91.1100

365

91)51.952,9($

49.47$

100(t)(proceeds)

paidinterest rateinterest annual Effective

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-18

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Compound Interest

Compound interest is earned or charged on both the principal amount and on the accrued interest that has been previously earned or charged.

Prt I $40 .04)(1)($1,000)(0 1year for Interest

$41.60 .04)(1)($1,040)(0 2year for Interest

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-19

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Compound Interest (continued)

We can bypass the multiple individual steps in computing compound interest by using the following compound interest formula to determine future value:

niPVFV )1(

FV = Future value

PV = Present value, or current principal amount

i = Interest rate earned per period of compounding

n = Number of compounding periods that the money will be invested

(FVF) factor valueFuture ni)1(

Where

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-20

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

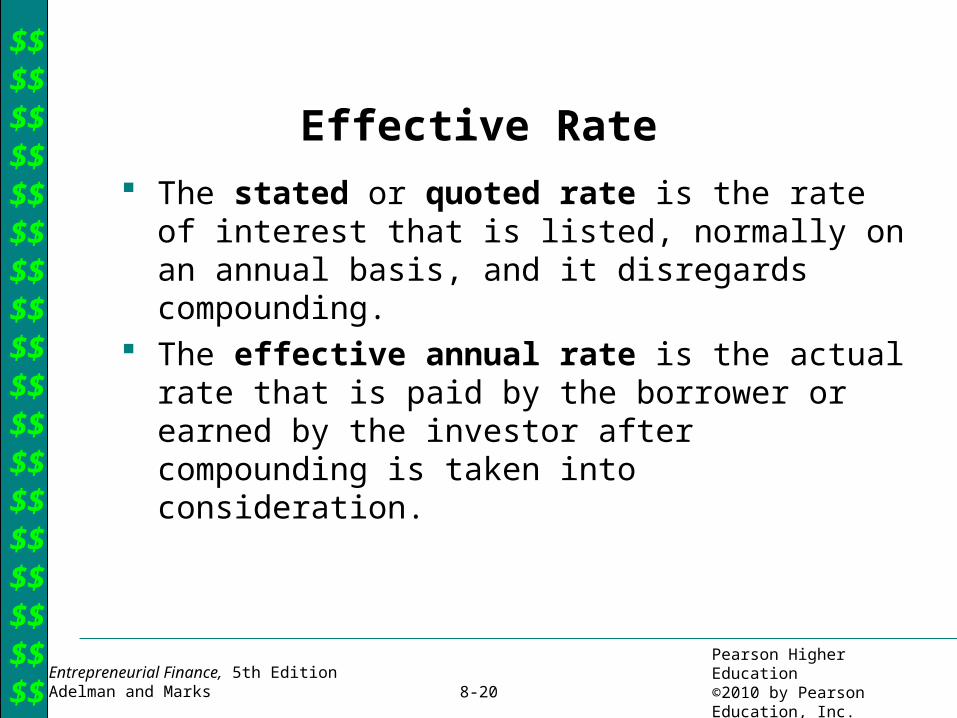

Effective Rate The stated or quoted rate is the rate of interest that is

listed, normally on an annual basis, and it disregards compounding.

The effective annual rate is the actual rate that is paid by the borrower or earned by the investor after compounding is taken into consideration.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-21

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Effective Rate (continued)

Example: A bank quotes 8 percent annual rate. The bank wants monthly payments, so it compounds monthly.

1001i)(1 Rate Annual Effective n x

i = Interest rate per period (found by dividing the quoted rate by the number of

compounding periods)

n = Number of compounding periods per year

%30.81000830.010010830.11001)0067.1(

100112

08.011001i)(1 Rate Annual Effective

12

12n

xxx

xx

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-22

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Future Value of a Lump Sum

What is the future value of a lump sum amount for n periods and at i rate of return?

)(FVFPVFV Where

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-23

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Future Value of a Lump Sum (Examples)

You save $10,000 at 5 percent interest for 10 years compounded annually. What is the future value of this investment after 10 years?

289,16$)6289.1(000,10$05.1000,10$

)1()(10

FV

iPVFVFPVFV n

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-24

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Future Value of a Lump Sum (Examples)

If a wedding costs $20,000 today, how much will the wedding cost 10 years from now if inflation averages 4% a year?

What is the future value of $100,000 if money is compounded monthly at 6% for 18 years? Note: The answer below was obtained by using a calculator. If you use tables, the answer is $293,680.

604,29$)4802.1(000,20$04.1000,20$

)1()(10

FV

iPVFVFPVFV n

60.676,293$9368.2000,100$

)005.1(000,100$12

06.1000,100$

)1()(

180

1218

x

FV

iPVFVFPVFV n

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-25

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Present Value of a Future Lump Sum

What is the present value of a future lump sum amount for n periods at an i rate of return?

Where

)(PVFFVPV

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-26

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Present Value of a Lump Sum (Examples)

How much do you have to deposit in an account today that will have a value of $10,000,000 in 7 years if annual interest is 6% compounded annually? Note: If tables are used rather than a calculator, the answer will be $6,651,000.

14.571,650,6$6651.0000,000,10$

5036.1

1000,000,10$

06.01

1000,000,10$

1

1)(

7

PV

iFVPVFFVPV n

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-27

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

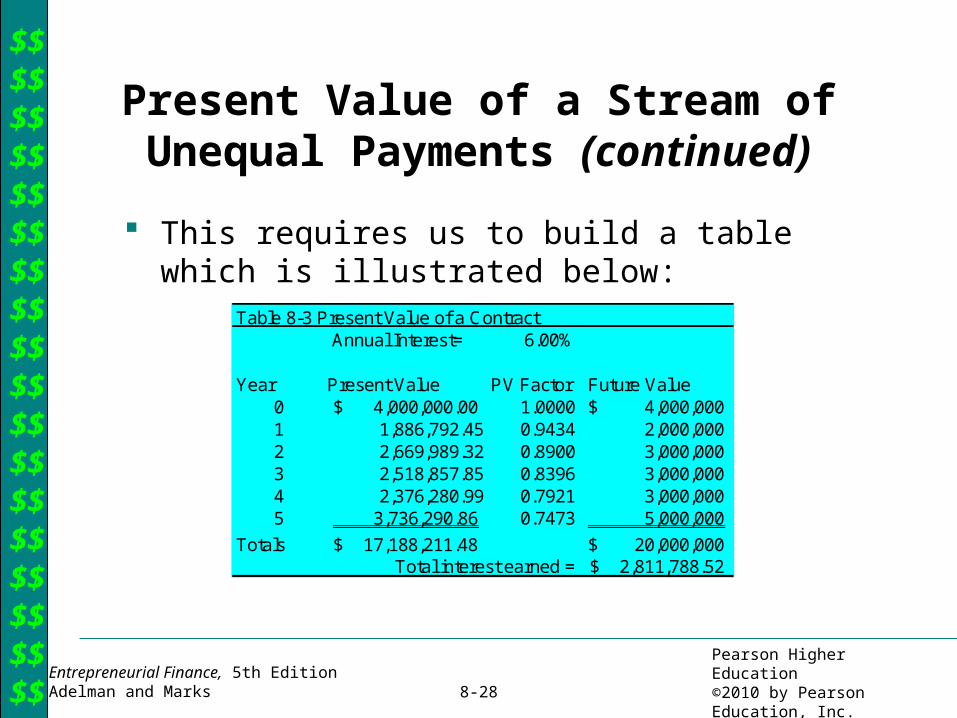

Present Value of a Stream of Unequal Payments

An athlete is offered a $20 million contract over 5 years with a $4 million signing bonus. The contract consists of $2 million for year 1, $3 million for year 2, $3 million for year 3, $3 million for year 4, and $5 million for year 5. What is the present value of the $20 million contract if money can earn 5 percent annual interest?

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-28

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Present Value of a Stream of Unequal Payments (continued)

This requires us to build a table which is illustrated below:

Annual Interest= 6.00%

Year Present Value PV Factor Future Value0 4,000,000.00$ 1.0000 4,000,000$ 1 1,886,792.45 0.9434 2,000,000 2 2,669,989.32 0.8900 3,000,000 3 2,518,857.85 0.8396 3,000,000 4 2,376,280.99 0.7921 3,000,000 5 3,736,290.86 0.7473 5,000,000

Totals 17,188,211.48$ 20,000,000$ 2,811,788.52$

Table 8-3 Present Value of a Contract

Total interest earned =

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-29

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Internal Rate of Return

Internal Rate of Return (IRR) is the actual rate of return that equates a dollar invested now with a dollar received in the future.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-30

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

The IRR is found by using a calculator and the following formula:

Internal Rate of Return (continued)

1001IRR

:is formula same thedepicting ofy Another wa

1001

1

xPV

FV

xPV

FVIRR

n

n

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-31

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

IRR Problem

In January 2002, you bought 10,000 shares of a stock at $2 per share. In January 2006, you sold the 10,000 shares at $3 a share. What is the internal rate of return?

%67.101001067.0

10011067.110015.11001000,20$

000,30$

1001

44

x

xxxIRR

xPV

FVIRR n

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-32

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

Rule of 72 We can also find an approximation of the amount of time

that it takes a present sum of money to double by dividing the number 72 by the interest rate earned on an investment. This procedure is known as the rule of 72. Example: How long will it take $1,000 to double if it can be invested at 12%?

Time for investment to double 72

Annual interest rate

72

126 years

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

Entrepreneurial Finance, 5th EditionAdelman and Marks

8-33

Pearson Higher Education©2010 by Pearson Education, Inc.Upper Saddle River, NJ 07458

We can also find the interest required if we know how long it takes an investment to double.

Example: We want $1,000 to double in eight years. What interest to we have to earn on our investment?

percent98

72

double to investment for Time

72 rate interest Annual

Rule of 72 (continued)