, Division of Research The Economic Outlook Dr. Doug Woodward Director, Division of Research...

30

, Division of Research The Economic Outlook Dr. Doug Woodward Director, Division of Research Professor of Economics Orangeburg, SC November 12, 2008

-

Upload

francisco-childers -

Category

Documents

-

view

216 -

download

0

Transcript of , Division of Research The Economic Outlook Dr. Doug Woodward Director, Division of Research...

, Division of Research

The Economic Outlook

Dr. Doug WoodwardDirector, Division of Research

Professor of Economics

Orangeburg, SC

November 12, 2008

Overview

• Perspective on the financial crisis

• Perspective on the economic crisis– U.S.– South Carolina

• The Fundamentals: Long-term Competitiveness

Perspective on the Financial Crisis A parallel financial industry created,

sold, and bought trillions of dollars of derivative securities based upon "hedging" or "insuring"

the value of a much smaller base of real assets.

Akin to gambling: credit default swaps

Some versions of these instruments are imaginary capital. These claims overlap on the same

types of mortgages and other financial instruments.

TARP’s problem Hard to price and sell these

financial products.

Co-Pilots

“Beware …

of geeks … bearing formulas.”

C = S * N(d1) - K * (e ^ -rt) * N (d2)

d1 = ln (S / K) + (r + (sigma) ^ 2 / 2) * t / sigma * sqrt(t)

d2 = d1 - sigma * sqrt(t)

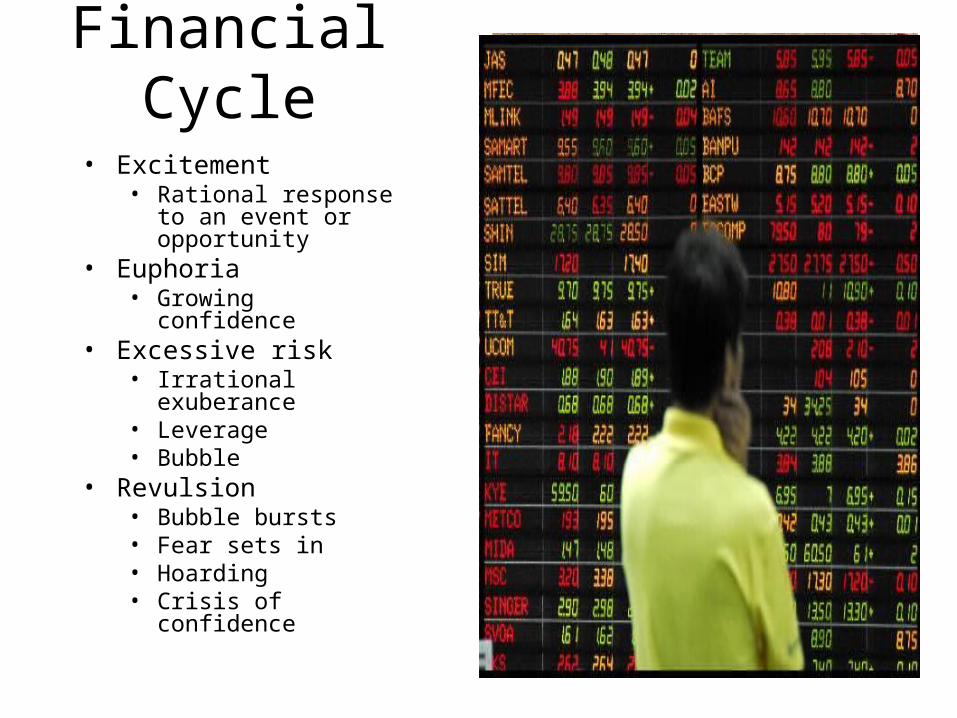

Financial Cycle

• Excitement• Rational response to

an event or opportunity

• Euphoria• Growing confidence

• Excessive risk• Irrational exuberance• Leverage• Bubble

• Revulsion• Bubble bursts• Fear sets in• Hoarding• Crisis of confidence

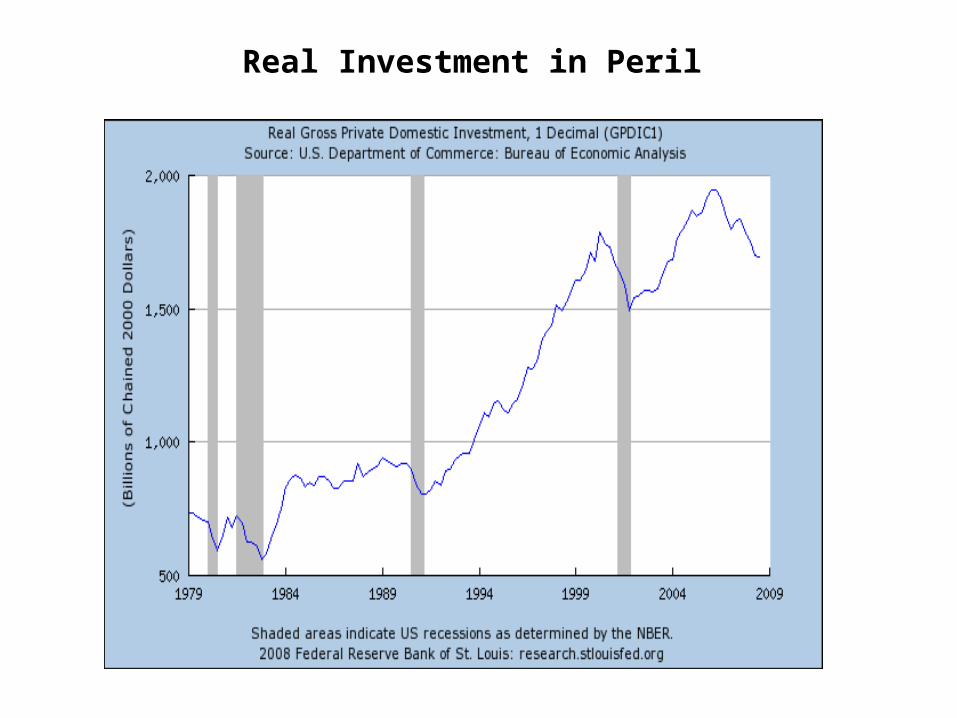

Real Investment Matters• Financial disorder creates a crisis of

confidence– Fundamental uncertainty

• Financial crises can have real consequences– Consumer retrench– Loss of confidence and animal spirits

(Keynes)

• Real investment stagnates– Real investment is plant, equipment, even

housing– Productivity enhancing investments

decline

• Government fiscal stimulus needed

The Forecast for the Real U.S. Economy

Recession …

What is a Recession?

Two quarters of declining GDP

Further:

A significant decline in economic activity spread across the economy

• Consumers retrench and wholesale-retail sales weaken

• Employment losses mount

The Long-run Business Cycle

Real Investment in Peril

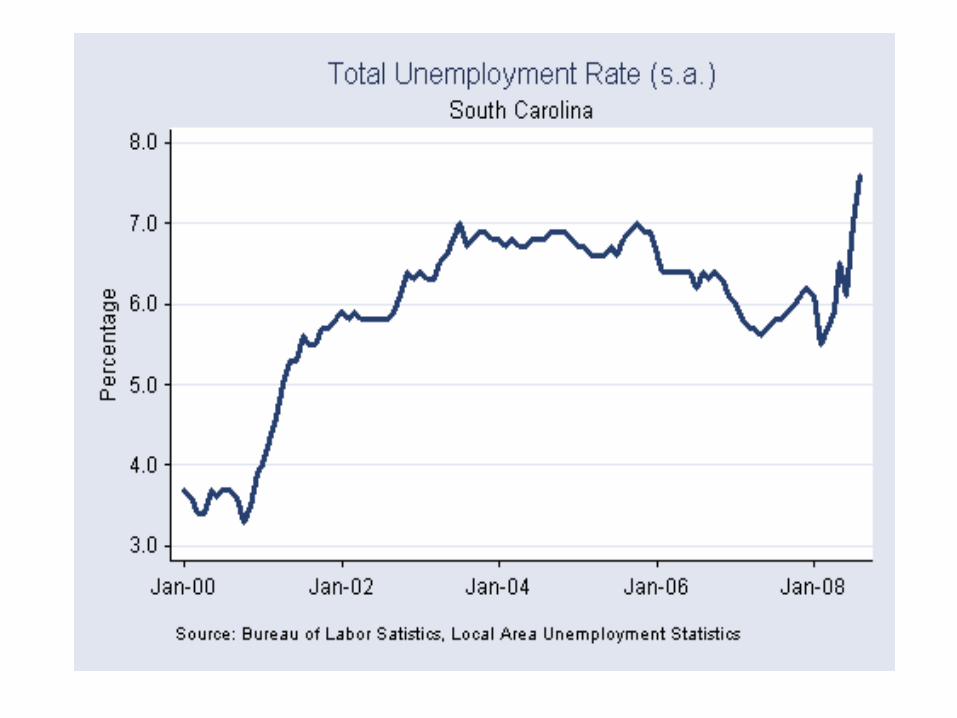

The Forecast for the Real South Carolina Economy

Recession …

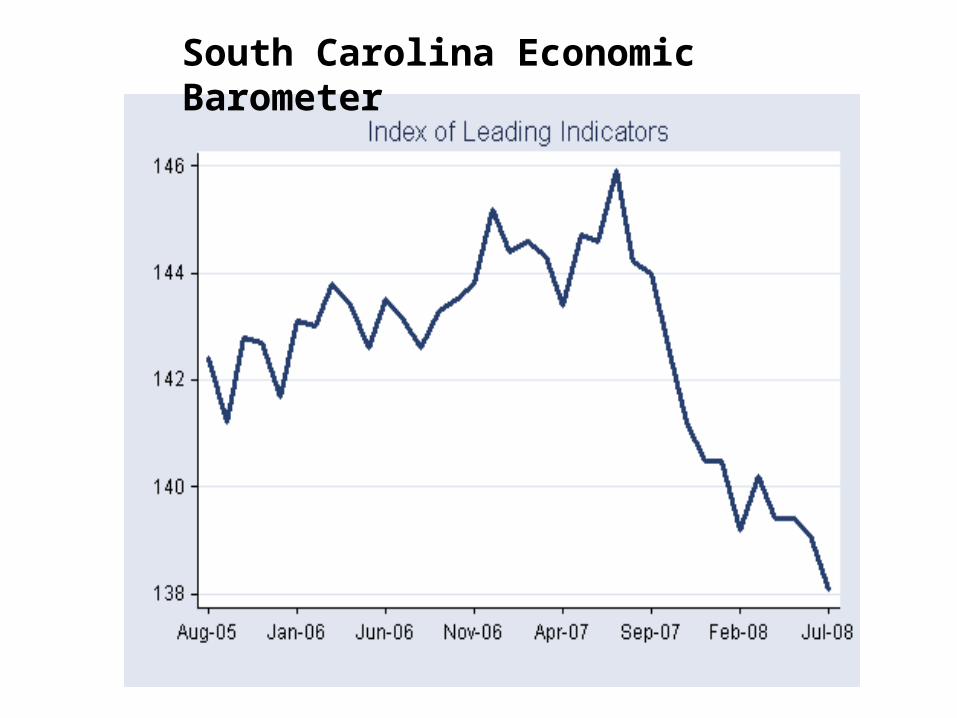

South Carolina Economic Barometer

Retail Rebound for Christmas?

• Low gas prices

• Stock market recovery

• No more financial shocks

• Rising confidence

• Stimulus checks

Exports Holding Up Manufacturing

• Dollar’s decline helped the S.C. economy

• Growing exports were a central reason why the S.C. economy stabilized in 2008

• But the latest data show …– Exports of goods will slow in 2009– They were growing at double digit rates

BMW’s Cumulative Capital Investmentin South Carolina in 2007 Dollars

Millions

Figure 3BMW Employment Impact

(2007 Values)

5,400

10,124

7,526

23,050

0

5,000

10,000

15,000

20,000

25,000

Direct Indirect Induced Total

Outlook Summary

• The ongoing financial crises will ensure a national recession.

• Meager economic gains during 2009.• Mild recovery possible in mid-2009.

• Local and state government in fiscal crisis.

Looking further ahead

• A rebound in 2010.• 2010–15: South Carolina will be a leading state

economy with export clusters.• More diversified• Cluster and competitiveness initiatives are still

the key to long run growth.

Thank you!

Additional information available at the web site for the Division of Research, Moore School of Business, University of South Carolina:

http://mooreschool.sc.edu/moore/research/

28th Annual Economic Outlook ConferenceDecember 3, 2008

Marriott Columbia City Center

8:30 am Continental Breakfast and Networking

9:30 am Check-in

10:00 am-12:00 noon "Outlook for the U.S. and S.C. Economy 2009"

Luncheon Speaker: Daniel H. Stern--"Current Status of the Financial Markets"

Cost is $75 (includes morning program and luncheon.)

Visit Moore School Website orcall 800-393-2362

Deadline to register is Nov. 26