© 2003 – 2004 Practical Perspectives Getting Started A Brief Look at Using This Audit System ISO...

14

© 2003 – 2004 Practical Perspectives Getting Started A Brief Look at Using This Audit System ISO 9001:2000 Revision: 2/20/2004 PRACTICAL PERSPECTIV ES Brought to you by: TM

-

Upload

conner-biglin -

Category

Documents

-

view

214 -

download

0

Transcript of © 2003 – 2004 Practical Perspectives Getting Started A Brief Look at Using This Audit System ISO...

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

Getting StartedA Brief Look at Using

This Audit SystemISO 9001:2000

Revision: 2/20/2004

PRACTICAL

PERSPECTIVES

Brought to you by:

TM

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

• Audit Schedule(s)• Opening Meeting Materials • Audit Summary and Audit Report• Additional Questions• A Completed Audit Report• Management Summary• Closing Meeting• The Rest of the Story

(Audit Procedure)

The Audit Process

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

Area to be Audited or Applicable ISO 9001:2000 Clauses

(scope per 8.2.2 of ISO 9001:2000) Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec Auditor Sta

tus

Impo

rtan

ce

Aud

it R

esul

ts

CommentsCustomer Property 7.5.4 & 8.2.4 (as it relates to inspecting or testing customer property)

Customer-related Processes 7.2, 5.2, 8.1a, 8.2.1 & 8.4a

Document & Records Control 4.1a, 4.1d, 4.2.1c, 4.2.1e, 4.2.3, 4.2.4, & records maintenance requirements (5.6.1, 6.2.2e, 7.1d, 7.2.2, 7.3.2, 7.3.4, 7.3.5, 7.3.6, 7.3.7, 7.4.1, 7.5.2d, 7.5.3, 7.5.4, 7.6, 8.2.2, 8.2.4, 8.3, 8.5.2e & 8.5.3d)

Design & Development 7.3

Improvement Systems 8.5

Internal Audit System 8.2.2

Maintaining Calibration 7.6

Management Commitment 4.1e, 4.2.1a, 5.1a-e, 5.3a-e, 5.4.1, 5.5.3, 5.6, 6, 8.1b, 8.1c, & 8.4a-d

Nonconformance Control 8.3

Production and Service Provision 4.1a, 4.1c, 4.1d, 4.1e, 4.1f, 4.2.1e, 5.1e, 6.3, 6.4, 7.5.1, 7.5.3, 7.5.5, 7.6 (ID, monitoring/measurement and devices to be used), 8.1, 8.2.3, 8.2.4, 8.4b & 8.4c

Purchasing 7.4, 4.1 (outsourcing), 8.2.4 (monitoring/measurement of received product) & 8.4d

Quality Management System 1.2, 4.1, 4.1a-f, 4.2.1b-d, 4.2.2, 5.4.2 & 5.5.2

Realization Planning 4.1a-d, 4.1f, 4.1 (control of outsourced processes), 4.2.1e, 5.1e, 6.3, 6.4 & 7.1

Special Processes 7.5.2

Training 5.3d, 5.5.1, 6.2.1 & 6.2.2

Status is based upon how well the area is doing. Importance is based upon the need to ensure consistency in areas where the system is continuously and agressively exercised. Audit Results recognizes the need to increase or decrease the frequency of audits based upon the results of the previous audits.

(marlett "n") = okay, (marlett "r") = basis for increase in frequency (0 to 1 "x" in the three columns means one audit per year, 2 "x's" means two audits, and 3 "x's" means 3 or more audits per year).

Place an "X" or some other mark in the month(s) that audits will be conducted. Remember to schedule based upon status and importance and resuls of previous audits. Also, try to spread them out so the number per month and use of a particular auditor is balanced over time.

Independence = At a minimum, auditors cannot audit their own work. For best results, auditors should not work in or be directly responsible for the area being audited.

Examples and/or Explanations are in Blue Basis for number of audits per year.

An annual audit schedule based upon audit reports, which are in support of ISO

9001:2000.Audit Schedule – Annual Plan

(frequency and planned intervals of the audit program per ISO 9001:2000)

Audits are spread out to balance the work load. May be subdivided by process(es) for audits

covering more than one area (i.e., Production and Service Provision may involve multiple

processes).

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

AUDIT DATE(S): DAY 1 TIMES: 8:00 AM to 5:00 PM

Area(s) Addressed Day 1 Time Day 2 TimeGuide or Comment(comments are italicized) Event &/or Audit Report

Team 1 Auditor(s)

Day 1

Team 2 Auditor(s)

Day 1

Team 3 Auditor(s)

Day 1

Team 1 Auditor(s)

Day 2

Team 2 Auditor(s)

Day 2

Team 3 Auditor(s)

Day 2Overview of the documents review

All 8:00 - 9:00 All 8:00 - 9:00Audit Team Review (morning)

1:00 1:00 1:00 1:00 1:00 1:00

Auditors & Management RepAll 9:00 - 9:30

Tour0:30 0:30 0:30

Auditors & Client ManagementAll 9:30 - 9:45

Opening Meeting0:15 0:15 0:15

Audit Team Working LunchAll

11:45 - 12:45

Noon - 1:00Lunch

1:00 1:00 1:00 1:00 1:00 1:00

Customer Property (can be combined w/ Purchasing and/or Production and Service Provision)

3 1:00 - 2:00 T'heirst UffCustomer Property

1:00

7.5

.4

8.2

.4

Contract Review, Customer Communication, and Customer Satisfaction

19:45 - 11:45

Letsma K'DealCustomer-Related Processes

2:00

5.2

7.2

8.1

a

8.2

.1

8.4

a

Design & Development1

12:45 - 2:45

Phil D. O'DreamsDesign & Development

2:00

7.3

Document & Records Control

29:00 - 11:00 Doc Zarus

Document & Records Control

2:00

4.1

a &

d

4.2

.1c

4.2

.1e

4.2

.3

4.2

.4

Continual Improvement, Corrective Action, and Preventive Action 2

12:45 - 2:30

C. LosedloopImprovement Systems

1:45

8.5

.1

8.5

.2

8.5

.3

Internal Audits2 2:30 - 4:00 I. C. Ewe

Internal Audit System1:30

8.2

.2

Calibrated Device Controls3 2:30 - 4:00 O. N. Themony

Maintaining Calibration1:30

7.6

Internal Communication, Quality Policy, Objectives, Management Review, Resources, and Data

19:00 - 11:00 I. M. Incharge

Management Commitment2:00

4.1

e

4.2

.1a

5.1

a-e

5.3

a-e

5.4

.1

5.5

.3

5.6

6 8.1

b

8.1

c

8.4

a-d

Nonconformance Control3

9:00 - 11:00

Unda ThrugNonconformance Control

2:00

8.3

Process Control, Product ID/Status/Traceability, and Preservation

3

9:45 - 11:45

12:45 - 2:30

Bill T. Well

Production & Service Provision

3:45

4.1

a

4.1

c-f

4.2

.1e

5.1

e

6.3

6.4

7.5

.1

7.5

.3

7.5

.5

7.6

8.1

8.2

.3

8.2

.4

8.4

b-c

Purchasing, Outsourcing, and Incoming Inspection 2

9:45 - 11:45

C. U. AthemalPurchasing

2:00

4.1

7.4

8.2

.4

8.4

d

Quality Management System

111:00 - Noon

1:00 - 2:00I. M. Rep

Quality Management System

2:00

1.2

4.1

4.1

a-f

4.2

.1b

-d

4.2

.2

5.4

.2

5.5

.2

Realization Processes1 2:45 - 4:00 P. Lantophail

Realization Planning1:15

4.1

4.1

a-d

4.1

f

4.2

.1e

5.1

e

6.3

6.4

7.1

Products or Services Not Monitored, Measured, Inspected, or Tested to Requirements

311:00 - Noon

Isqual I. FiedSpecial Processes

1:00

7.5

.2

Responsibility, Authority, and Training 2

11:00 - Noon

1:00 - 2:00Ben E. Fit

Training2:00

5.3

d

5.5

.1

6.2

.1

6.2

.2

Audit Team Discussion & Report Preparation All 4:00 - 5:00 All 2:00 - 4:00

Audit Team Review (afternoon)1:00 1:00 1:00 2:00 2:00 2:00

Audit Team & ManagementAll 4:00 - 5:00

Closing Meeting1:00 1:00 1:00

9:00 9:00 9:00 9:00 9:00 9:00

I NNEEDO FALOOK, I nc.

DAY, TIME, AND PARTICIPANTS SCHEDULE AUDIT TEAM PLANNING WORKSHEET

Where each section of ISO 9001:2000 is audited.

Sampling records called for by 4.2.1e and referenced throughout

9001:2000

Hours in a Day Scheduled

to

ISO9001:2000 ELEMENTS COVERED

9/13 & 9/14 2003

AUDI T SCHEDULE - TEAM AUDI T OF ENTI RE SYSTEM5:00 PM8:00 AMDAY 2 TIMES:

Examples and/or Explanations are in Blue

An event-based schedule, using a team of auditors to audit the entire system.

This schedule tends only to be used when a team is involved or when we are

auditing a large portion of the system all at once.

Fill in the amount of time (hours & minutes) and the hours per day

calculate automatically.

Once you know how much time to designate for each, it’s just a

matter of setting the time slots

and getting the client (person requesting the

audit) to tell you who the guide

will be.

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

When should we conduct an opening meeting?

An opening meeting is typically done when the audit involves a large group, more than one area or

process, and/or when an external party (customer, registrar, etc.) is involved, but can be done for any

audit. It’s really up to you.

Lets us keep track of who attended, so we can prove

management was aware, when necessary.

Opening Meeting Materials(when we decide we need an opening meeting)

Opening MeetingSign-In

Date: ______________

NAME TITLE

What an opening meeting

should cover.

PRACTICAL

PERSPECTIVES

GreetingThank them for the invitation & provide a brief introduction of audit team.

Pass around attendance logPrinted names & date.

Defer questions to the endQuestions may be answered in the information provided.

Purpose of audit & scopeVerify compliance with the ________ standard & conformance of effective practices to documented system. Note: This is where you normally describe the process (desktop review, audit, & report/conclusion), with the scope being to verify effectiveness of the system to the applicable standard.

Audit process disclaimerRandom sample.

Verify availability of facilities & guides

Set time for Closing Meeting

Auditor ConfidentialityAuditor code of ethics requires confidentiality.

Open up for questions

(applicable)

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

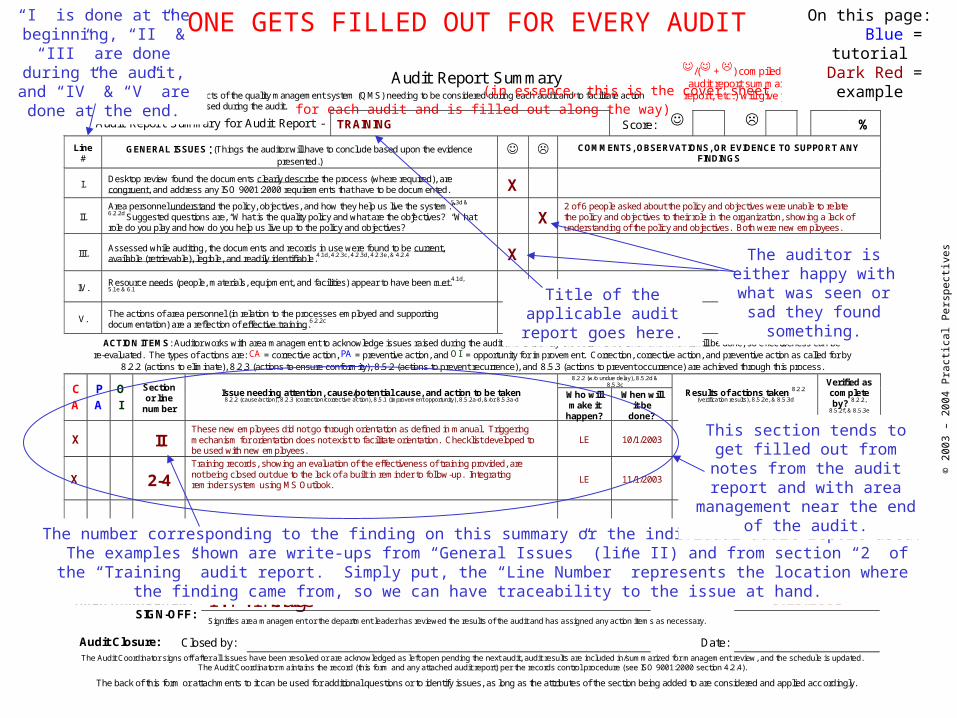

Audit Report Summary

Revision: 10/20/2003 Page 1 of 1

Purpose: To address aspects of the quality management system (QMS) needing to be considered during each audit and to facilitate action on any issues raised during the audit.

Audit Report Summary for Audit Report - TRAINING Score: %

Line #

GENERAL ISSUES: (Things the auditor will have to conclude based upon the evidence presented.)

COMMENTS, OBSERVATIONS, OR EVIDENCE TO SUPPORT ANY

FINDINGS

I. Desktop review found the documents clearly describe the process (where required), are congruent, and address any ISO 9001:2000 requirements that have to be documented. X

II. Area personnel understand the policy, objectives, and how they help us live the system.5.3d &

6.2.2d Suggested questions are, “What is the quality policy and what are the objectives?” “What role do you play and how do you help us live up to the policy and objectives?”

X 2 of 6 people asked about the policy and objectives were unable to relate the policy and objectives to their role in the organization, showing a lack of understanding of the policy and objectives. Both were new employees.

III. Assessed while auditing, the documents and records in use were found to be current, available (retrievable), legible, and readily identifiable.4.1d, 4.2.3c, 4.2.3d, 4.2.3e, & 4.2.4 X

IV. Resource needs (people, materials, equipment, and facilities) appear to have been met.4.1d,

5.1e & 6.1

V. The actions of area personnel (in relation to the processes employed and supporting documentation) are a reflection of effective training.6.2.2c

ACTION ITEMS: Auditor works with area management to acknowledge issues raised during the audit and to identify the action to be taken and when it will be done, so effectiveness can be re-evaluated. The types of actions are: CA = corrective action, PA = preventive action, and OI = opportunity for improvement. Correction, corrective action, and preventive action as called for by

8.2.2 (actions to eliminate), 8.2.3 (actions to ensure conformity), 8.5.2 (actions to prevent recurrence), and 8.5.3 (actions to prevent occurrence) are achieved through this process. 8.2.2 (w/o undue delay), 8.5.2d &

8.5.3c CA

PA

OI

Section or line

number

Issue needing attention, cause/potential cause, and action to be taken 8.2.2 (cause/action), 8.2.3 (correction/corrective action), 8.5.1 (improvement opportunity), 8.5.2a-d, &/or 8.5.3a-d

Who will make it

happen?

When will it be

done?

Results of actions taken 8.2.2

(verification results), 8.5.2e, & 8.5.3d

Verified as complete by? 8.2.2,

8.5.2f, & 8.5.3e

X II These new employees did not go through orientation as defined in manual. Triggering mechanism for orientation does not exist to facilitate orientation. Checklist developed to be used with new employees.

LE 10/1/2003

X 2-4 Training records, showing an evaluation of the effectiveness of training provided, are not being closed out due to the lack of a built in reminder to follow-up. Integrating reminder system using MS Outlook.

LE 11/1/2003

I .M. I ncharge Date: 9/15/2003 AREA MANAGEMENT SIGN-OFF:

Signifies area management or the department leader has reviewed the results of the audit and has assigned any action items as necessary.

Audit Closure: Closed by: Date: The Audit Coordinator signs off after all issues have been resolved or are acknowledged as left open pending the next audit, audit results are included in/summarized for management review, and the schedule is updated.

The Audit Coordinator maintains the record (this form and any attached audit report) per the records control procedure (see ISO 9001:2000 section 4.2.4).

The back of this form or attachments to it can be used for additional questions or to identify issues, as long as the attributes of the section being added to are considered and applied accordingly.

/( + ) compiled from all sheets (this audit report summary, applicable audit

report, etc.) will give you the percentage!

On this page: Blue = tutorial

Dark Red = example

Title of the applicable audit report goes

here.

“I” is done at the beginning, “II” & “III” are done during the audit, and “IV” & “V” are done at the end.

The number corresponding to the finding on this summary or the individual audit report used. The examples shown are write-ups from “General Issues” (line II) and from section “2” of the “Training” audit report. Simply put, the “Line Number” represents the location where the finding came from, so we can have

traceability to the issue at hand.

The auditor is either happy with what was

seen or sad they found something.

This section tends to get filled out from notes from the

audit report and with area management near the end of

the audit.

ONE GETS FILLED OUT FOR EVERY AUDIT (in essence, this is

the cover sheet for each audit and is filled out along the way)

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

Audit Report – Training 5.3d, 5.5.1, 6.2.1 & 6.2.2A u d i t R e p o r t – T r a i n i n g 5 . 3 d , 5 . 5 . 1 , 6 . 2 . 1 & 6 . 2 . 2

S c o p e : R e s p o n s i b i l i t y , A u t h o r i t y , a n d T r a i n i n g

D a t e : A u d i t o r ( s ) : W i t n e s s ( e s ) :

D o c u m e n tr e v i e w

( 1 )( s e e a u d i t

p r o c e d u r e )

R e c o r d s s h o w t h e n e e d f o rt r a i n i n g o r o t h e r a c t i o n w a s

i d e n t i f i e d a n d p r o v i d e d( 2 - 3 & 2 - 4 )

R e c o r d s s h o w t h e a c t i o n s t a k e n t od e c l a r e c o m p e t e n c e i n c l u d e e v a l u a t i o n

o f e f f e c t i v e n e s s o f t h o s e a c t i o n s( 2 - 3 & 2 - 4 )

R e c o r d s o f a p p r o p r i a t ee d u c a t i o n , t r a i n i n g , s k i l l s , a n d

e x p e r i e n c e a r e m a i n t a i n e d( 2 - 6 )

V e r i f y c o m p e t e n c e i s b a s e du p o n a p p r o p r i a t e e d u c a t i o n ,

t r a i n i n g , s k i l l s , a n d e x p e r i e n c e( 2 - 2 )

V e r i f y r e s p o n s i b i l i t y & a u t h o r i t ya n d d e f i n e d a n d c o m m u n i c a t e d

( 2 - 1 )

P u l l a s a m p l e o f r e c o r d si n v o l v i n g v a r i o u s t y p e s o f

e m p l o y e e s( 2 )

R e l e v a n c e / i m p o r t a n c e o f t h e e m p l o y e e s a c t i v i t i e s , h o w t h ee m p l o y e e s c o n t r i b u t e t o t h e q u a l i t y o b j e c t i v e s , a n d a n

u n d e r s t a n d i n g o f t h e q u a l i t y p o l i c y i s c o m m u n i c a t e d( 2 - 5 )

S E C T I O N 2 2 - 1 2 - 2 2 - 3 2 - 4 2 - 5 2 - 6

R e s p o n s i b i l i t y & a u t h o r i t y a r e d e f i n e d a n d c o m m u n i c a t e d ?

5 . 5 . 1

C o m p e t e n c e f o r e a c h p o s i t i o n i n t h e

o r g a n i z a t i o n h a s b e e n d e t e r m i n e d ?

6 . 2 . 2 a

E v i d e n c e e m p l o y e e a r r i v e d w i t h

c o m p e t e n c e , h a s r e c e i v e d t r a i n i n g , o r i s

i n t r a i n i n g e x i s t s ? 6 . 2 . 1 & 6 . 2 . 2 b

R e c o r d s s h o w t r a i n i n g p r o v i d e d o r

a s s e s s m e n t o f c o m p e t e n c e

e m p l o y e e a r r i v e d w i t h a r e e v a l u a t e d f o r

e f f e c t i v e n e s s ? 6 . 2 . 2 c

T r a i n i n g e n s u r e s t h e e m p l o y e e

u n d e r s t a n d s h i s o r h e r r o l e i n f u l f i l l i n g t h e p o l i c y , o b j e c t i v e s , a n d

t h e a c t i v i t i e s o f t h e j o b h e o r s h e f u l f i l l s ?

5 . 3 d & 6 . 2 . 2 d

R e c o r d s o f e d u c a t i o n ,

t r a i n i n g , s k i l l s , a n d e x p e r i e n c e

a r e m a i n t a i n e d p e r r e c o r d s

c o n t r o l s ? 4 . 2 . 1 e & 6 . 2 . 2 e

I d e n t i f y E m p l o y e e s F o r S a m p l e S e l e c t a t l e a s t 5 e m p l o y e e s ( f r o m p o s i t i o n s i n

t h e o r g a n i z a t i o n , i n c l u d i n g c o n t r a c t l a b o r , i f a p p l i c a b l e ) , m a k i n g n o t e o f t h e i r n a m e s o r

o t h e r u n i q u e i d e n t i f i e r s . O n c e t h e e m p l o y e e s h a v e b e e n i d e n t i f i e d , g o t o w h e r e r e c o r d s o f

a p p r o p r i a t e e d u c a t i o n , t r a i n i n g , s k i l l s , a n d e x p e r i e n c e a r e m a i n t a i n e d a n d p u l l t h e

r e c o r d s f o r t h e s e e m p l o y e e s .

C l a r i f i c a t i o n s : A u t h o r i t y – W h a t s o m e o n e c a n d o . C o m p e t e n c e – C a p a b l e o f o r q u a l i f i e d t o p e r f o r m s p e c i f i e d a c t i v i t i e s . R e s p o n s i b i l i t y – W h a t s o m e o n e i s s u p p o s e d t o d o .

E v i d e n c e , O b s e r v a t i o n s , a n d / o r C o m m e n t s

A d d - o n q u e s t i o n s , i d e n t i f i e d a s p a r t o f d o c u m e n t r e v i e w ( S e c t i o n 1 ) c a n b e a t t a c h e d t o t h i s f o r m o r a d d e d o n t h e b a c k , a s l o n g a s t h e q u e s t i o n s i n c l u d e c o n c l u s i o n s ( & ) .

T h e n u m b e r s i n t h e b o x e s r e l a t e t o t h e s e c t i o n n u m b e r s b e l o w , w h e r e a p p l i c a b l e . m e a n s t h e a u d i t o r f o u n d e v i d e n c e o f c o n f o r m a n c e o r a n o p p o r t u n i t y f o r i m p r o v e m e n t . m e a n s t h e a u d i t o r f o u n d a n o n c o n f o r m a n c e t h a t n e e d s a t t e n t i o n . R e f e r e n c e s t o I S O 9 0 0 1 : 2 0 0 0 a r e i n c l u d e d b e l o w , w h e r e a p p l i c a b l e .

Audit Reports (like this one) have been developed to cover all of the requirements, in a process-

oriented manner. Each one includes a flowchart (an overview of the audit being performed) and lays out

the series of events, including the evidence and conclusions reached. In other words, the flowchart

is fulfilled simply by answering the questions.

Directions provide a starting point and suggested sample

sizes.

Questions include the clause(s) in ISO

9001:2000 so you can fall back on the

standard if needed.

The numbers over each question relate to the flowchart and allow for

traceability when a finding or improvement opportunity is

identified.

The auditor is either happy

with what was seen or sad they found something.

May be a definition, examples of what to look for, or scenarios to consider.

Examples and/or Explanations are in Blue

Additional questions can and should be added where procedures call for requirements greater than those in ISO

9001:2000 (regulatory, customer, legal, those the organization imposes on itself, etc.).

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

Audit Report – Training 5.3d, 5.5.1, 6.2.1 & 6.2.2A u d i t R e p o r t – T r a i n i n g 5 . 3 d , 5 . 5 . 1 , 6 . 2 . 1 & 6 . 2 . 2

S c o p e : R e s p o n s i b i l i t y , A u t h o r i t y , a n d T r a i n i n g

D a t e : 9 / 1 5 / 0 3 A u d i t o r ( s ) : D u d e I . M a n a u d i t o r W i t n e s s ( e s ) : V i c T i m ’ a m i

D o c u m e n tr e v i e w

( 1 )( s e e a u d i t

p r o c e d u r e )

R e c o r d s s h o w t h e n e e d f o rt r a i n i n g o r o t h e r a c t i o n w a s

i d e n t i f i e d a n d p r o v i d e d( 2 - 3 & 2 - 4 )

R e c o r d s s h o w t h e a c t i o n s t a k e n t od e c l a r e c o m p e t e n c e i n c l u d e e v a l u a t i o n

o f e f f e c t i v e n e s s o f t h o s e a c t i o n s( 2 - 3 & 2 - 4 )

R e c o r d s o f a p p r o p r i a t ee d u c a t i o n , t r a i n i n g , s k i l l s , a n d

e x p e r i e n c e a r e m a i n t a i n e d( 2 - 6 )

V e r i f y c o m p e t e n c e i s b a s e du p o n a p p r o p r i a t e e d u c a t i o n ,

t r a i n i n g , s k i l l s , a n d e x p e r i e n c e( 2 - 2 )

V e r i f y r e s p o n s i b i l i t y & a u t h o r i t ya n d d e f i n e d a n d c o m m u n i c a t e d

( 2 - 1 )

P u l l a s a m p l e o f r e c o r d si n v o l v i n g v a r i o u s t y p e s o f

e m p l o y e e s( 2 )

R e l e v a n c e / i m p o r t a n c e o f t h e e m p l o y e e s a c t i v i t i e s , h o w t h ee m p l o y e e s c o n t r i b u t e t o t h e q u a l i t y o b j e c t i v e s , a n d a n

u n d e r s t a n d i n g o f t h e q u a l i t y p o l i c y i s c o m m u n i c a t e d( 2 - 5 )

S E C T I O N 2 2 - 1 2 - 2 2 - 3 2 - 4 2 - 5 2 - 6

R e s p o n s i b i l i t y & a u t h o r i t y a r e d e f i n e d a n d c o m m u n i c a t e d ?

5 . 5 . 1

C o m p e t e n c e f o r e a c h p o s i t i o n i n t h e

o r g a n i z a t i o n h a s b e e n d e t e r m i n e d ?

6 . 2 . 2 a

E v i d e n c e e m p l o y e e a r r i v e d w i t h

c o m p e t e n c e , h a s r e c e i v e d t r a i n i n g , o r i s

i n t r a i n i n g e x i s t s ? 6 . 2 . 1 & 6 . 2 . 2 b

R e c o r d s s h o w t r a i n i n g p r o v i d e d o r

a s s e s s m e n t o f c o m p e t e n c e

e m p l o y e e a r r i v e d w i t h a r e e v a l u a t e d f o r

e f f e c t i v e n e s s ? 6 . 2 . 2 c

T r a i n i n g e n s u r e s t h e e m p l o y e e

u n d e r s t a n d s h i s o r h e r r o l e i n f u l f i l l i n g t h e p o l i c y , o b j e c t i v e s , a n d

t h e a c t i v i t i e s o f t h e j o b h e o r s h e f u l f i l l s ?

5 . 3 d & 6 . 2 . 2 d

R e c o r d s o f e d u c a t i o n ,

t r a i n i n g , s k i l l s , a n d e x p e r i e n c e

a r e m a i n t a i n e d p e r r e c o r d s

c o n t r o l s ? 4 . 2 . 1 e & 6 . 2 . 2 e

I d e n t i f y E m p l o y e e s F o r S a m p l e S e l e c t a t l e a s t 5 e m p l o y e e s ( f r o m p o s i t i o n s i n

t h e o r g a n i z a t i o n , i n c l u d i n g c o n t r a c t l a b o r , i f a p p l i c a b l e ) , m a k i n g n o t e o f t h e i r n a m e s o r

o t h e r u n i q u e i d e n t i f i e r s . O n c e t h e e m p l o y e e s h a v e b e e n i d e n t i f i e d , g o t o w h e r e r e c o r d s o f

a p p r o p r i a t e e d u c a t i o n , t r a i n i n g , s k i l l s , a n d e x p e r i e n c e a r e m a i n t a i n e d a n d p u l l t h e

r e c o r d s f o r t h e s e e m p l o y e e s .

J u s t i n I . T ’ F o r t h e m o n y ( A c c t g . ) X X X X X X X X

I n i t ’ f o r T h e l o n g h a u l ( P r o d . ) X X X X X X X

L e s s a C l u e ( P r o d M g r . ) X X X X X X X

I . M . I n c h a r g e ( P r e s i d e n t ) X X X X X X X X

B o S . S e s s o n ( Q u a l i t y ) X X X X X X X X

I . S . N o r e a l o t ( H R ) X X X X X X X

M . P r o v i s o r ( E n g . ) X X X X X X X

C l a r i f i c a t i o n s : A u t h o r i t y – W h a t s o m e o n e c a n d o . C o m p e t e n c e – C a p a b l e o f o r q u a l i f i e d t o p e r f o r m s p e c i f i e d a c t i v i t i e s . R e s p o n s i b i l i t y – W h a t s o m e o n e i s s u p p o s e d t o d o .

E v i d e n c e , O b s e r v a t i o n s , a n d / o r C o m m e n t s

L e s s a C l u e & M . P r o v i s o r ( n e w s i n c e l a s t a u d i t ) a r e n o l o n g e r i n t r a i n i n g , b u t n o r e c o r d s o f t h i s e x i s t . T r a i n i n g n e e d s f o r J u s t i n I . T ’ f o r t h e m o n y ( s e m i n a r a n d i n - h o u s e , I . M . I n c h a r g e ( i n - h o u s e t r a i n i n g ) a n d B o S . S e s s o n ( s e m i n a r ) w e r e i d e n t i f i e d , t r a i n i n g w a s p r o v i d e d f o r , b u t e f f e c t i v e n e s s o f t h e t r a i n i n g ( s h o w i n g c o m p e t e n c e ) w a s n o t e v a l u a t e d . O t h e r r e c o r d s f o r t h e s e a n d o t h e r e m p l o y e e s s h o w s o m e e v a l u a t i o n i s o c c u r r i n g .

A d d - o n q u e s t i o n s , i d e n t i f i e d a s p a r t o f d o c u m e n t r e v i e w ( S e c t i o n 1 ) c a n b e a t t a c h e d t o t h i s f o r m o r a d d e d o n t h e b a c k , a s l o n g a s t h e q u e s t i o n s i n c l u d e c o n c l u s i o n s ( & ) .

T h e n u m b e r s i n t h e b o x e s r e l a t e t o t h e s e c t i o n n u m b e r s b e l o w , w h e r e a p p l i c a b l e . m e a n s t h e a u d i t o r f o u n d e v i d e n c e o f c o n f o r m a n c e o r a n o p p o r t u n i t y f o r i m p r o v e m e n t . m e a n s t h e a u d i t o r f o u n d a n o n c o n f o r m a n c e t h a t n e e d s a t t e n t i o n . R e f e r e n c e s t o I S O 9 0 0 1 : 2 0 0 0 a r e i n c l u d e d b e l o w , w h e r e a p p l i c a b l e .

It is possible to have and or more than one or on any given question, when the evidence tells you some of the item is done correctly (i.e., happy some are right, but sad

to say it is not enough) or a question has more than one piece of evidence collected.

A Completed Audit ReportOn this page:Blue = tutorial

Dark Red = example

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

Audit Report Summary

Revision: 10/20/2003 Page 1 of 1

Purpose: To address aspects of the quality management system (QMS) needing to be considered during each audit and to facilitate action on any issues raised during the audit.

Audit Report Summary for Audit Report - TRAINING Score: 51 6 89.5 %

Line #

GENERAL ISSUES: (Things the auditor will have to conclude based upon the evidence presented.)

COMMENTS, OBSERVATIONS, OR EVIDENCE TO SUPPORT ANY

FINDINGS

I. Desktop review found the documents clearly describe the process (where required), are congruent, and address any ISO 9001:2000 requirements that have to be documented. X

II. Area personnel understand the policy, objectives, and how they help us live the system.5.3d &

6.2.2d Suggested questions are, “What is the quality policy and what are the objectives?” “What role do you play and how do you help us live up to the policy and objectives?”

X 2 of 6 people asked about the policy and objectives were unable to relate the policy and objectives to their role in the organization, showing a lack of understanding of the policy and objectives. Both were new employees.

III. Assessed while auditing, the documents and records in use were found to be current, available (retrievable), legible, and readily identifiable.4.1d, 4.2.3c, 4.2.3d, 4.2.3e, & 4.2.4 X

IV. Resource needs (people, materials, equipment, and facilities) appear to have been met.4.1d,

5.1e & 6.1 X

V. The actions of area personnel (in relation to the processes employed and supporting documentation) are a reflection of effective training.6.2.2c X

ACTION ITEMS: Auditor works with area management to acknowledge issues raised during the audit and to identify the action to be taken and when it will be done, so effectiveness can be re-evaluated. The types of actions are: CA = corrective action, PA = preventive action, and OI = opportunity for improvement. Correction, corrective action, and preventive action as called for by

8.2.2 (actions to eliminate), 8.2.3 (actions to ensure conformity), 8.5.2 (actions to prevent recurrence), and 8.5.3 (actions to prevent occurrence) are achieved through this process. 8.2.2 (w/o undue delay), 8.5.2d &

8.5.3c CA

PA

OI

Section or line

number

Issue needing attention, cause/potential cause, and action to be taken 8.2.2 (cause/action), 8.2.3 (correction/corrective action), 8.5.1 (improvement opportunity), 8.5.2a-d, &/or 8.5.3a-d

Who will make it

happen?

When will it be

done?

Results of actions taken 8.2.2

(verification results), 8.5.2e, & 8.5.3d

Verified as complete by? 8.2.2,

8.5.2f, & 8.5.3e

X II These new employees did not go through orientation as defined in manual. Triggering mechanism for orientation does not exist to facilitate orientation. Checklist developed to be used with new employees.

LE 10/1/2003 Review on 11/15/2003 found

checklist in place and has been used with new hires.

RF

X 2-4 Training records, showing an evaluation of the effectiveness of training provided, are not being closed out due to the lack of a built in reminder to follow-up. Integrating reminder system using MS Outlook.

LE 11/1/2003

Effectiveness evaluations are now triggered by MS Outlook in HR, with status of evaluations

current as of 11/15/2003.

RF

I .M. I ncharge Date: 9/15/2003 AREA MANAGEMENT SIGN-OFF:

Signifies area management or the department leader has reviewed the results of the audit and has assigned any action items as necessary.

Audit Closure: Closed by: Audie T. Co’Ordinator Date: 11/16/2003 The Audit Coordinator signs off after all issues have been resolved or are acknowledged as left open pending the next audit, audit results are included in/summarized for management review, and the schedule is updated.

The Audit Coordinator maintains the record (this form and any attached audit report) per the records control procedure (see ISO 9001:2000 section 4.2.4).

The back of this form or attachments to it can be used for additional questions or to identify issues, as long as the attributes of the section being added to are considered and applied accordingly.

/( + ) compiled from all sheets (this audit report summary, applicable audit

report, etc.) will give you the percentage!

When everything is dealt with and

verified as being effective, the audit coordinator closes

out the audit.

On this page:Blue = tutorial

Dark Red = example

ONE GETS FILLED OUT FOR EVERY AUDIT (here is the completed summary for the completed audit

report on the previous slide)

The Audit Report should be attached and this record filed per

records control procedures.

Don’t forget to score the audit.

“IV” & “V” are done at the

end.

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

When should we conduct a closing meeting?

A closing meeting is typically done when the audit involves a large group, more than one area or process, and/or when an external party (customer, registrar,

etc.) is involved, but can be done for any audit. It’s really up to you.

Lets us keep track of who attended, so we can prove

management was aware, when necessary.

Closing Meeting Materials

(when we decide we need a closing meeting, especially if we already had an

opening meeting)Closing Meeting

Sign-In

Date: ______________

NAME TITLE

Reporting on the results and providing a conclusion can be accomplished with the Management Summary! (see

next slide)

What a closing

meeting should cover.

PRACTICAL

PERSPECTIVES

GreetingThank them for the audit opportunity & the guides for participating in audit.

Pass around attendance logPrinted names & date.

Defer questions to the endQuestions may be answered in the information provided & allows those needing detail to stay while the others are free to leave.

Purpose of audit & scopeVerify compliance with the _________ standard & conformance of effective practices to documented system. Note: This is where you normally describe the process (desktop review, audit, & report/conclusion), with the scope being to verify effectiveness of the system to the applicable standard.

Audit process disclaimerRandom sample.

Auditor ConfidentialityConfidentiality due to auditor ethics.

Report on results of audit

Provide a conclusion

Open up for questions

Provide client with audit summary

(applicable)

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

Management Summary (page 1)(can be used to report the results of audits over the year

and/or as the summary for any audit involving multiple areas)

CLIENT INFORMATIONCom pany Nam e: Phone:

Em ail:Address: Fax:

A/R

Lead Auditor (LA)

LA's Email

LA's Phone #

GENERAL THOUGHTS & CONCLUSIONS

© 2003 – 2004 Practical Perspectives

8.5

.3d

Instructions: This form is used to summarize audits falling within the selected date range. If a particular checklist was not involved during this time period, simply leave that section of the summary blank. Additional instructions are embedded as comments in the header of most sections (only available when reviewing an electronic copy of this report).

Nam e: (Contact)

DATE RANGE OF AUDIT

TO

AUDIT CRITERIA ON-SITE DAYS

ISO9001:2000

AUDIT TEAM MEMBERS

Au

dit

or(

s)

Realization Planning(13)

Maintaining Calibration(7)

4.2

.3 &

4.2

.4

4.2

.1c

& e

ISO 9001:2000

Document & Records Control(4)

8.2

.2 &

8.2

.4

Calibration

5.6

.1 &

6.2

.2

7.1

d &

7.2

.2

7.3

.2 &

7.3

.4

7.3

.5 &

7.3

.6

7.3

.7 &

7.4

.1

7.5

.2 &

7.5

.3

7.5

.4 &

7.6

4.2

.1b

-d

Quality Management System Structure

1.2

Quality Management System(12)

Document & Records Control, (acknow ledging the records involved)

4.1

a &

d

5.4

.2

4.2

.2

4.1

0

4.1

a-f

5.5

.2

0.0%0 0 0CHECKLIST SUMMARY WRITE-UP TOTALS 0 0

Communication, Policy, Objectives, Resources, and Data

4.1

e

4.2

.1a

5.1

a-e

5.3

a-e

5.4

.1

5.5

.3

5.6

0 THE FACTS

Nonconformance Control

8.3

Continual Improvement, Corrective Action, and Preventive Action

8.5

.1

Improvement Systems(5)

8.5

.3

8.5

.2

8.3

& 8

.5.2

e

Design & Development

7.3

Design & Development(3)

8.2

.1

8.4

a

Contract Review , Customer Satisfaction, and Analysis of Data related to Customer Satisfaction

5.2

7.2

8.1

a

Customer-Related Processes(2)

COMMENT MAIN AREAS COVEREDCHECKLIST ACCEPT TOTALACCEPT.

RATE MAJOR MINORCustomer Property

7.5

.4

8.2

.4

Customer Property(1)

Internal Audit System(6)

7.6

Internal Audits

8.2

.2

Management Commitment(8)

6 8.1

b

8.1

c

8.4

a-d

Nonconformance Control(9)

Purchasing(11)

Purchasing, Outsourcing, and Incoming Inspection

4.1

7.4

8.2

.4

8.4

d

Production & Service Provision(10)

7.5

.1

7.5

.3

Process Control, Product ID/Status/Traceability, Statistical Techniques, and Preservation of Product 4

.1a

& c

-f

4.2

.1e

5.1

e

8.2

.4

8.4

b &

c

& R

ec

ord

s

7.5

.5

7.6

8.1

0

8.2

.3

6.3

6.4

4.1

4.1

a-d

& f

4.2

.1e

Realization Processes

5.1

e

6.3

6.4

7.1

Special Processes(14)

Special Processes

7.5

.2

Training(15)

Responsibility, Authority, and Training

5.3

d

5.5

.1

6.2

.1

6.2

.2

These are the totals from the

Audit Summary for each audit. The “Accept.

Rate” calculates

automatically.

This is where you note the

significant issues (typically in a

bulleted fashion) and let

management know whether the system is

conforming with requirements based upon a score of 80%+

on each checklist and no Major

nonconformances.

Each finding, noted in the “Issue needing attention…” section of the

Audit Summary for each audit is acknowledged as a Major (system-

wide breakdown or missing ISO 9001:2000 requirement), Minor

(issue needing to be resolved, but not a Major), or Comment (positive or negative feedback that could be acted on to make things better or to prevent potential problems).

Explanations are in

BlueInstructions are embedded

as comments in the MS Excel file “Management

Summary”

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

FINDINGSTANDARD/BASIS

MAJOR = Will take quite a bit of w ork to resolve; MINOR = Needs a little touch-up; COMMENT = May be a praise or m ay be pointing out things that could use a little w ork (correction, preventive action, or opportunities for im provem ent).

REPORT & SECTION OR LINE #CLAUSE/PARA # OBSERVATION & ACTION TAKEN

AUDIT FINDINGS© 2003 – 2004 Practical Perspectives

OBSERVATIONS & ACTIONS TAKEN, WHERE KNOWN

Management Summary (page 2)(can be used to report the results of audits over the year

and/or as the summary for any audit involving multiple areas)

Explanations are in

BlueInstructions are embedded

as comments in the MS Excel file “Management

Summary”

Reference to what is not being

lived up to.

Each finding, noted in the “Issue needing attention…” section of the Audit Summary for each audit is documented in this section to

provide management with an overall ‘laundry list.’ The FINDING forms the basis upon which the MAJOR/MINOR/COMMENT conclusion is made on page one of this summary. REPORT & SECTION OR LINE

# is how we tie the finding back to the actual audit. The OBSERVATIONS & ACTIONS TAKEN, WHERE KNOWN is where we

quote the requirement(s) not lived up to (paraphrased as much as possible) and a summary of the evidence supporting the finding.

The action taken, including evidence of effectiveness would also be helpful.

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

The Rest of the StoryWhile this tutorial provides a nice overview, the

procedure (including supporting notes)

covers the process in detail!

Note 1.

Auditassigned(frequency)

Pull applicabledocuments

Meetrequirements?

System or Desktop Audit(audit criteria, scope & methods)

I f it is okay ¬ worthmentioning,move on.

NO

YES, WITHFINDINGS

Process Audit(methods)

YES

NO

Note 2. Note 4.

Ask OPEN-ENDEDquestions.

Note 11.

Not here to audit theperson. Here to auditthe process, with thewitness speaking on

behalf of that process.

Com

plet

e th

e cy

cle.

Ask

que

stio

ns a

nd v

erif

yco

nfor

man

ce u

ntil

the

audit

is d

one.

Note 7.

Notes 8 (when formality is needed)&/or 9 (area or audit report specific).

Note 12. Note 13.

Note 14.

Note 15. Note 16.

Note 18.Notes 10&/or 17.

Desktop review &checklist (audit

report)development

Discontinue if toomany problems

identified

Give witness anadvance copy of

the checklist

Set thetone of the

audit

Ask a question toverify

conformance &effectiveness

AssessmentNonconformance or

ineffectivenessConformance &

effectiveness

Discomfort

Dig deeper

Assessment

Get comfortablewith your

discomfort

Note concerns onaudit report or

notes

Obtainagreement &

dispel concerns

Last question?

Record results Close out audit

Findings inneed of action?

Corrective orpreventive action

&/orimprovementopportunity

taken

Wait for effectiveimplementation

Note 3.

Note 6.

Resolve witharea

management

Can the auditproceed?

NO YES

Note 5.

MAYBE

If we cannot work it out with area management

YES

NO

Note 10.

YES,AUDIT

ISDONE

Note 19.

Note 19.

Formality or what might be referred to asa 2nd or 3rd party audit process involvesan opening and closing meeting withmanagement. This is typically done whena team of auditors is involved.

© 2

003

– 20

04 P

ract

ical

Per

spec

tives

If additional assistance is needed:

Business ConsultingWe provide on-site assistance in quality (ISO

9001:2000, AS9100, ISO/TS 16949:2002, ISO 13485:2003, etc.), environmental (ISO 14001 and Texas EMS), and safety (ISO 18001) management

systems, transitional management, leadership development, strategic planning, auditing services, and serve as the management representative for some of our clients. For information, visit us at:

PERSPECTIVESPRACTICAL

4405 Seville Lane, Suite 100McKinney, Texas 75070-4437

(469) 667-5440 (phone)(214) 853-5390 (fax)

www.perspicuous.com (website)

[email protected] (email)

www.an-answer.com (website)

[email protected] (email)

On-line, On-site, In-class TrainingWe provide on-line training in auditing and management system development , for the

adventurous at heart, with time to spare, or as a result of a tight budget. These courses provide the same

type of information companies receiving on-site assistance are getting, but in a cost-effective, do-it-

yourself kind of way. Those successfully completing one of our courses receive a certificate of completion, intended to satisfy requirements for effectiveness of

training and/or for continuing professional development (CPD). To see the courses we currently have available, or to be notified of new offerings, visit

us at: